QAA Level 7 Financial Decision Making: Harvey Homes Plc Case Study

VerifiedAdded on 2020/07/22

|16

|5699

|44

Report

AI Summary

This report presents a comprehensive financial analysis of Harvey Homes Plc, evaluating its business performance and financial position. The analysis includes a detailed examination of the company's statement of profit or loss, statement of financial position, and statement of cash flow, alongside the calculation and interpretation of various financial ratios such as profitability, liquidity, solvency, and efficiency ratios. Furthermore, the report delves into market segment analysis and investment appraisal techniques, including payback period, accounting rate of return, and net present value, to assess the viability of the Midland acquisition. The executive summary highlights key financial highlights, including revenue, gross profit, and net profit, along with an assessment of the company's strengths and weaknesses. Recommendations are provided for future expansion and financial management. The report concludes with a recommendation to undertake the Midland project and suggests strategies to maximize its performance.

Module name Financial Decision Making

QAA Level 7

Schedule Term One

Student Reference Number (SRN) BP0168166

Report/Assignment Title CASE STUDY – HARVEY HOMES plc

Date of Submission

(Please attach the confirmation of

any extension received)

QAA Level 7

Schedule Term One

Student Reference Number (SRN) BP0168166

Report/Assignment Title CASE STUDY – HARVEY HOMES plc

Date of Submission

(Please attach the confirmation of

any extension received)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

FINANCIAL

DECISION MAKING

DECISION MAKING

Table of Contents

EXEUCTIVE SUMMARY.............................................................................................................1

PART 1: BUSINSS PERFORMANCE ANALYSIS......................................................................2

Statement of profit or loss............................................................................................................2

Statement of financial position....................................................................................................4

Liquidity & working capital.........................................................................................................4

Solvency ratios.............................................................................................................................6

Efficiency ratios...........................................................................................................................7

Statement of cash flow.................................................................................................................7

Market Segment analysis.............................................................................................................9

PART 2 INVESTMENT APPRAISALS.......................................................................................10

Management forecast.................................................................................................................10

Investment appraisal techniques................................................................................................11

Payback period...........................................................................................................................11

Accounting rate of return...........................................................................................................12

Net present value........................................................................................................................12

Sources of finance......................................................................................................................13

Non-Financial factors.................................................................................................................13

REFERENCES..............................................................................................................................15

APPENDIX....................................................................................................................................17

Appendix 1: Profitability ratios..................................................................................................17

Appendix 2: Absolute & percentage change in overhead..........................................................17

Appendix 3: Calculation of liquidity ratios................................................................................18

Appendix 4: Calculation of solvency ratios...............................................................................18

EXEUCTIVE SUMMARY.............................................................................................................1

PART 1: BUSINSS PERFORMANCE ANALYSIS......................................................................2

Statement of profit or loss............................................................................................................2

Statement of financial position....................................................................................................4

Liquidity & working capital.........................................................................................................4

Solvency ratios.............................................................................................................................6

Efficiency ratios...........................................................................................................................7

Statement of cash flow.................................................................................................................7

Market Segment analysis.............................................................................................................9

PART 2 INVESTMENT APPRAISALS.......................................................................................10

Management forecast.................................................................................................................10

Investment appraisal techniques................................................................................................11

Payback period...........................................................................................................................11

Accounting rate of return...........................................................................................................12

Net present value........................................................................................................................12

Sources of finance......................................................................................................................13

Non-Financial factors.................................................................................................................13

REFERENCES..............................................................................................................................15

APPENDIX....................................................................................................................................17

Appendix 1: Profitability ratios..................................................................................................17

Appendix 2: Absolute & percentage change in overhead..........................................................17

Appendix 3: Calculation of liquidity ratios................................................................................18

Appendix 4: Calculation of solvency ratios...............................................................................18

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Appendix 5: Calculation of efficiency ratios.............................................................................18

Appendix 6: Calculation of operating cash cycle or cash conversion cycle..............................19

Appendix 7: Market segmental analysis....................................................................................19

Appendix 6: Calculation of operating cash cycle or cash conversion cycle..............................19

Appendix 7: Market segmental analysis....................................................................................19

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Index of Figures

Figure 1 Graph of Harvey Homes Plc's profitability ratios.............................................................2

Figure 2 Changes in operational cost from 2015 to 2016................................................................3

Figure 3 Current ratio and quick ratio of Harvey Homes Plc..........................................................5

Figure 4 Debt to equity and interest bearing ratio of Harvey Homes plc........................................6

Figure 5 Assets turnover ratio & inventory turnover ratio of Harvey Homes Plc...........................7

Figure 6 Segmental revenue and operating profit of Harvey Homes Plc........................................9

Figure 7 Managerial forecast of Midland Acquisition..................................................................10

Figure 8 Net-cash flow for Midland Acquisition..........................................................................11

Index of Tables

Table 1 Calculation of profitability ratios.....................................................................................17

Table 2 Calculation of absolute and percentage change in operational cost.................................17

Table 3 Calculation of liquidity ratios...........................................................................................18

Table 4 Calculation of solvency ratios..........................................................................................18

Table 5 Calculation of efficiency ratios.........................................................................................18

Table 6 Calculation of cash conversion cycle...............................................................................19

Table 7 Market segmental analysis................................................................................................19

Figure 1 Graph of Harvey Homes Plc's profitability ratios.............................................................2

Figure 2 Changes in operational cost from 2015 to 2016................................................................3

Figure 3 Current ratio and quick ratio of Harvey Homes Plc..........................................................5

Figure 4 Debt to equity and interest bearing ratio of Harvey Homes plc........................................6

Figure 5 Assets turnover ratio & inventory turnover ratio of Harvey Homes Plc...........................7

Figure 6 Segmental revenue and operating profit of Harvey Homes Plc........................................9

Figure 7 Managerial forecast of Midland Acquisition..................................................................10

Figure 8 Net-cash flow for Midland Acquisition..........................................................................11

Index of Tables

Table 1 Calculation of profitability ratios.....................................................................................17

Table 2 Calculation of absolute and percentage change in operational cost.................................17

Table 3 Calculation of liquidity ratios...........................................................................................18

Table 4 Calculation of solvency ratios..........................................................................................18

Table 5 Calculation of efficiency ratios.........................................................................................18

Table 6 Calculation of cash conversion cycle...............................................................................19

Table 7 Market segmental analysis................................................................................................19

EXEUCTIVE SUMMARY

In today’s uncertain and turbulent corporate environment, volatility in the market such as

high cost of interest, inability to access external borrowings and others are the factors responsible

for financial risk. The present report had analyzed the performance and financial position of

Harvey Homes Plc which aims at delivering high-quality housing facilities to the people with the

objective of getting maximum return for the shareholders. Segmental analysis reported that

southern region’s GM & OM is reported highest to 30% and 24.60% whilst the Northern &

Midland’s profit margin is comparatively less. The reasons behind change this is operational cost

of Midland have been increased by 20% whilst in Northern region, it shown highest growth of

25% and in Southern, it reflects modest growth of 14.81%.

Key financial highlights

Year\(£m) Revenue Gross

profit

Net profit GM NM ROCE

2015 1083 272 171 25.12% 15.79% 20.29%

2016 1297 332 194 25.60% 14.96% 18.34%

% change 19.76% 22.06% 13.45% - - -

Financial statement analysis through different ratios founded that net profitability shows

poor results, however, company has good liquidity strength. It had taken loan in current year to

finances its Midland acquisition so as to manage solvency position. More debt borrowings will

enable it to reach the idle solvency ratio of 0.50:1. Moreover, for the further expansion in France,

it has been recommended to choose a combination of equity & debt for monetary collection for

the sound solvency management. Besides this, for maximizing Midland’s performance, firm is

required to be recommended to control cost, hire experienced managerial team and make sound

pricing decision to boost market demand.

Investment appraisal viability

Initial outlay £500m

Payback period 4 years 6 months

ARR 6%

Page 1

In today’s uncertain and turbulent corporate environment, volatility in the market such as

high cost of interest, inability to access external borrowings and others are the factors responsible

for financial risk. The present report had analyzed the performance and financial position of

Harvey Homes Plc which aims at delivering high-quality housing facilities to the people with the

objective of getting maximum return for the shareholders. Segmental analysis reported that

southern region’s GM & OM is reported highest to 30% and 24.60% whilst the Northern &

Midland’s profit margin is comparatively less. The reasons behind change this is operational cost

of Midland have been increased by 20% whilst in Northern region, it shown highest growth of

25% and in Southern, it reflects modest growth of 14.81%.

Key financial highlights

Year\(£m) Revenue Gross

profit

Net profit GM NM ROCE

2015 1083 272 171 25.12% 15.79% 20.29%

2016 1297 332 194 25.60% 14.96% 18.34%

% change 19.76% 22.06% 13.45% - - -

Financial statement analysis through different ratios founded that net profitability shows

poor results, however, company has good liquidity strength. It had taken loan in current year to

finances its Midland acquisition so as to manage solvency position. More debt borrowings will

enable it to reach the idle solvency ratio of 0.50:1. Moreover, for the further expansion in France,

it has been recommended to choose a combination of equity & debt for monetary collection for

the sound solvency management. Besides this, for maximizing Midland’s performance, firm is

required to be recommended to control cost, hire experienced managerial team and make sound

pricing decision to boost market demand.

Investment appraisal viability

Initial outlay £500m

Payback period 4 years 6 months

ARR 6%

Page 1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

NPV £22,000 Favorable

It clearly depicted that Harvey Homes Plc must undertaken its Midland project as it

indicates the possibility of favorable return worth £22,000 and high ARR of 6% than targeted

rate of 5%.

PART 1: BUSINSS PERFORMANCE ANALYSIS

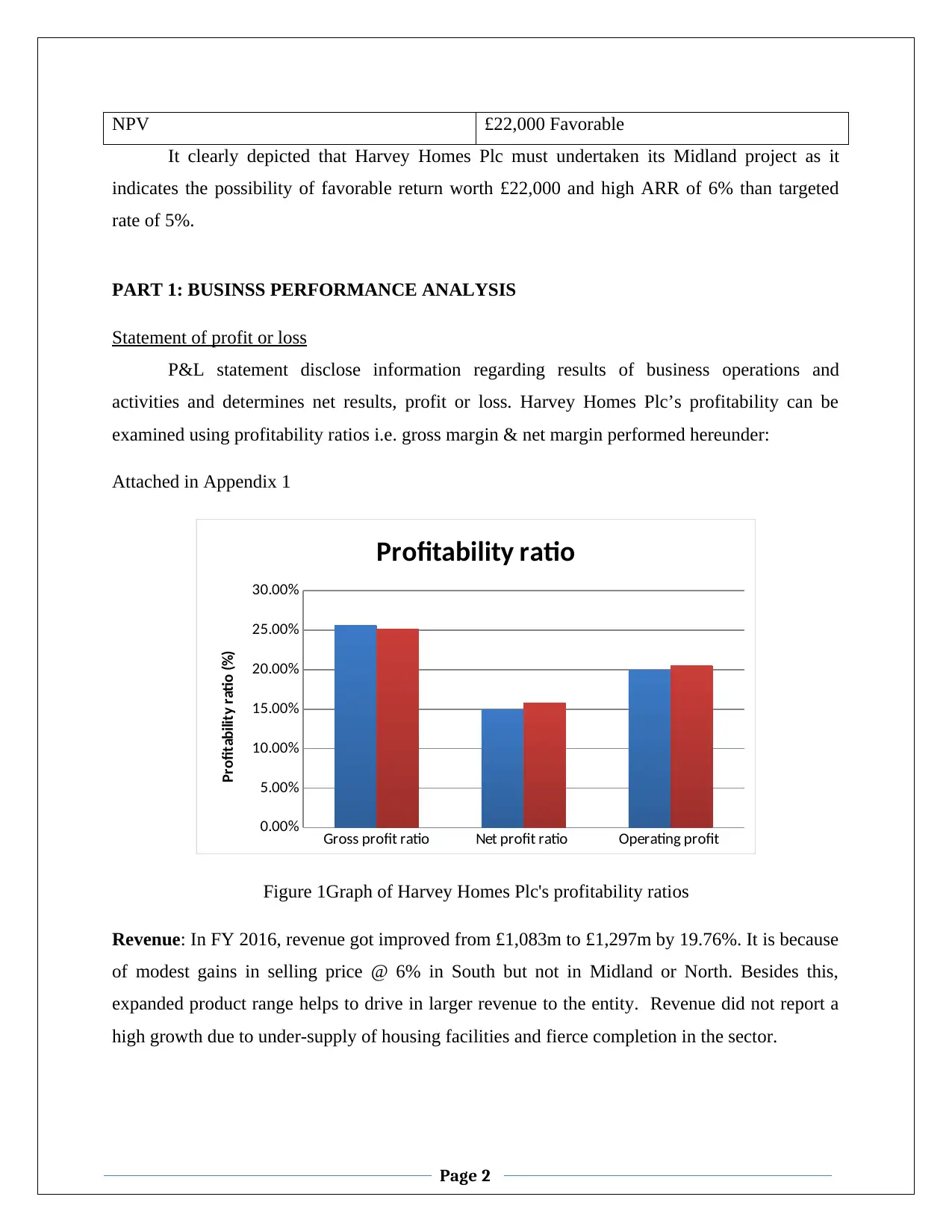

Statement of profit or loss

P&L statement disclose information regarding results of business operations and

activities and determines net results, profit or loss. Harvey Homes Plc’s profitability can be

examined using profitability ratios i.e. gross margin & net margin performed hereunder:

Attached in Appendix 1

Gross profit ratio Net profit ratio Operating profit

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Profitability ratio

Profitability ratio (%)

Figure 1Graph of Harvey Homes Plc's profitability ratios

Revenue: In FY 2016, revenue got improved from £1,083m to £1,297m by 19.76%. It is because

of modest gains in selling price @ 6% in South but not in Midland or North. Besides this,

expanded product range helps to drive in larger revenue to the entity. Revenue did not report a

high growth due to under-supply of housing facilities and fierce completion in the sector.

Page 2

It clearly depicted that Harvey Homes Plc must undertaken its Midland project as it

indicates the possibility of favorable return worth £22,000 and high ARR of 6% than targeted

rate of 5%.

PART 1: BUSINSS PERFORMANCE ANALYSIS

Statement of profit or loss

P&L statement disclose information regarding results of business operations and

activities and determines net results, profit or loss. Harvey Homes Plc’s profitability can be

examined using profitability ratios i.e. gross margin & net margin performed hereunder:

Attached in Appendix 1

Gross profit ratio Net profit ratio Operating profit

0.00%

5.00%

10.00%

15.00%

20.00%

25.00%

30.00%

Profitability ratio

Profitability ratio (%)

Figure 1Graph of Harvey Homes Plc's profitability ratios

Revenue: In FY 2016, revenue got improved from £1,083m to £1,297m by 19.76%. It is because

of modest gains in selling price @ 6% in South but not in Midland or North. Besides this,

expanded product range helps to drive in larger revenue to the entity. Revenue did not report a

high growth due to under-supply of housing facilities and fierce completion in the sector.

Page 2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of sale: (25.60%) Increase in cost is the result of inflation in building cost because

company has used modern construction methods to offer hi-tech integrated apartments & houses

and satisfy their needs.

Gross margin (GM): This ratio quantifies the percentage of gross profit that Harvey Homes Plc

has earned on their total sales revenue. In FY 2015, GM reported to 25.12% that increased to

25.60% in FY 2016. It is because revenue reported a high growth of 19.76% whereas cost of

purchase land and its development shown slightly lower growth by 16.67%, analyzed in detail as

follow:

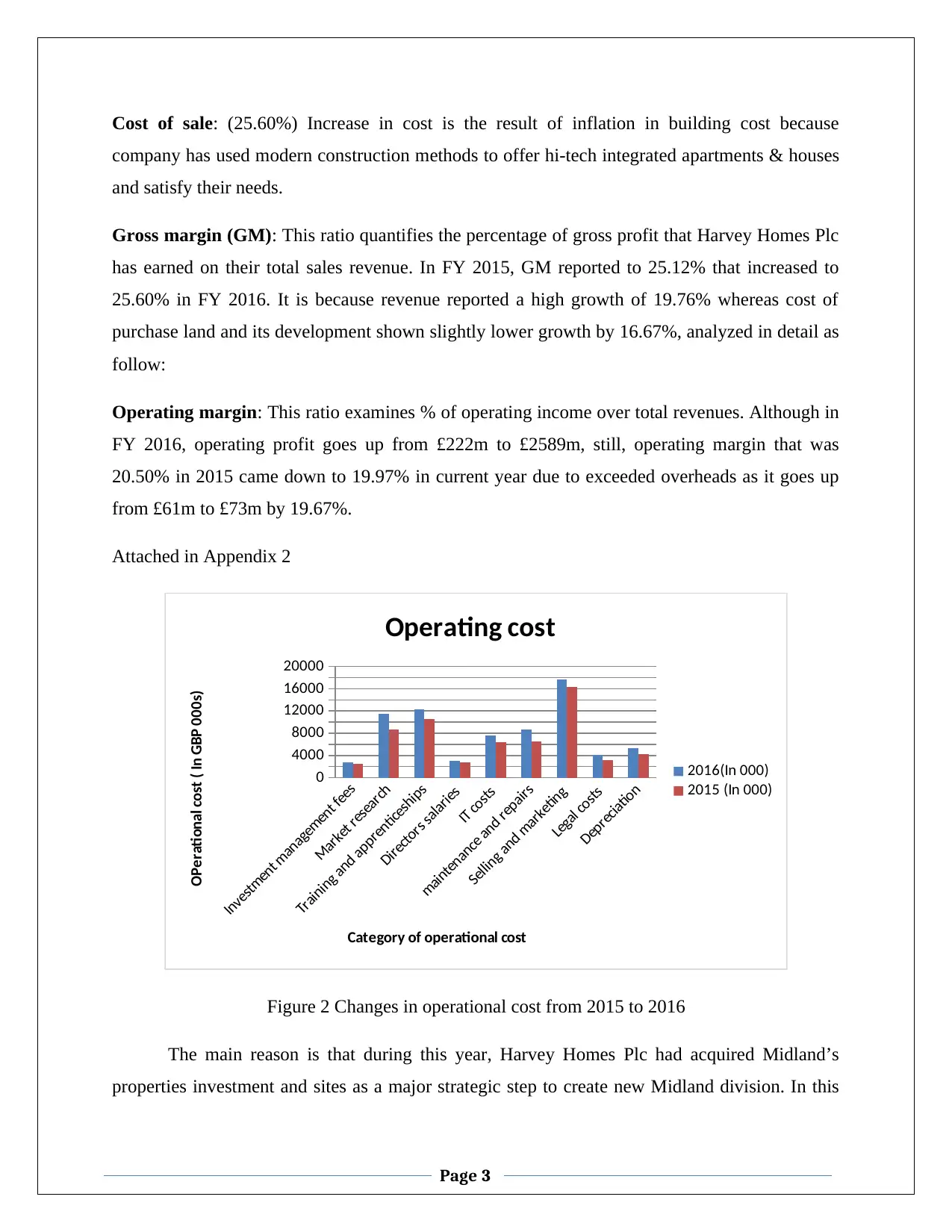

Operating margin: This ratio examines % of operating income over total revenues. Although in

FY 2016, operating profit goes up from £222m to £2589m, still, operating margin that was

20.50% in 2015 came down to 19.97% in current year due to exceeded overheads as it goes up

from £61m to £73m by 19.67%.

Attached in Appendix 2

Investment management fees

Market research

Training and apprenticeships

Directors salaries

IT costs

maintenance and repairs

Selling and marketing

Legal costs

Depreciation

0

4000

8000

12000

16000

20000

Operating cost

2016(In 000)

2015 (In 000)

Category of operational cost

OPerational cost ( In GBP 000s)

Figure 2 Changes in operational cost from 2015 to 2016

The main reason is that during this year, Harvey Homes Plc had acquired Midland’s

properties investment and sites as a major strategic step to create new Midland division. In this

Page 3

company has used modern construction methods to offer hi-tech integrated apartments & houses

and satisfy their needs.

Gross margin (GM): This ratio quantifies the percentage of gross profit that Harvey Homes Plc

has earned on their total sales revenue. In FY 2015, GM reported to 25.12% that increased to

25.60% in FY 2016. It is because revenue reported a high growth of 19.76% whereas cost of

purchase land and its development shown slightly lower growth by 16.67%, analyzed in detail as

follow:

Operating margin: This ratio examines % of operating income over total revenues. Although in

FY 2016, operating profit goes up from £222m to £2589m, still, operating margin that was

20.50% in 2015 came down to 19.97% in current year due to exceeded overheads as it goes up

from £61m to £73m by 19.67%.

Attached in Appendix 2

Investment management fees

Market research

Training and apprenticeships

Directors salaries

IT costs

maintenance and repairs

Selling and marketing

Legal costs

Depreciation

0

4000

8000

12000

16000

20000

Operating cost

2016(In 000)

2015 (In 000)

Category of operational cost

OPerational cost ( In GBP 000s)

Figure 2 Changes in operational cost from 2015 to 2016

The main reason is that during this year, Harvey Homes Plc had acquired Midland’s

properties investment and sites as a major strategic step to create new Midland division. In this

Page 3

acquisition, it has incurred legal cost to comply with the governmental legislation as a result it

gone up from £3,131m to £4,087m by £956 at a percentage growth of 30.57%. In addition to

this, due to chronic local skills shortage, it has organized trainings programs as results its cost

has been increased by 17.23%. Besides this, business unit had incurred considerable expenses in

building improvements, more importantly, for updating bought-in sites and incurred heavy cost

than normally expected cost (Kim and et.al., 2016). Evidencing the same, in FY 2016,its total

repair and maintenance cost improved by 32.42%. Furthermore, high management fees by

9.47%, director’s salaries by 7.57%, market research by 33.44%, IT costs by 19.48%, selling &

marketing cost by 8.74% and depreciation increase on purchased properties by 26.40% are the

reason behind declined operating profit ratio.

Net margin: This measures business efficiency to earn return as an excess of revenues

over total cost incurred (Cesarini and et.al., 2010). In FY 2016, NM dropped down from 15.79%

to 14.96% which indicates that firm has gained lesser return this year on their total turnover.

Although, net profit shows a growth by 13.45% as it has been increased from £171m to £194m,

still, percentage of return over sales came down and reported poor performance. Besides, inflated

housing prices and exceeding overheads, financial cost; interest gone up from £9m to £15m by

66.67% because Harvey Homes Plc had taken borrowings worth £150m in 2016 to finance its

acquisition strategy. In this year, business had paid more tax worth £50m due to higher

availability of profit before tax (PBT) worth £244m. Decreased net profit is a negative sign as it

reflects that company did not performed excellent this year due to poor earnings on total revenue

(Kim and et.al., 2016).

Return on capital employed: This ratio measures operating profit % on total capital

employed in the business. In FY 2015, it was 20.29% dropped down to 18.34% by 9.61% which

reflects that Harvey Homes Plc has earned less earnings on their capital invested in the business

unit (Kumar and Rao, 2016). Although, OP increased by 16.67%, still, high growth in capital

employed from £1,094m to £1,412m by 29.07% due to procurement of funds worth £150m from

the bank borrowings is the main reason behind less ROCE.

Page 4

gone up from £3,131m to £4,087m by £956 at a percentage growth of 30.57%. In addition to

this, due to chronic local skills shortage, it has organized trainings programs as results its cost

has been increased by 17.23%. Besides this, business unit had incurred considerable expenses in

building improvements, more importantly, for updating bought-in sites and incurred heavy cost

than normally expected cost (Kim and et.al., 2016). Evidencing the same, in FY 2016,its total

repair and maintenance cost improved by 32.42%. Furthermore, high management fees by

9.47%, director’s salaries by 7.57%, market research by 33.44%, IT costs by 19.48%, selling &

marketing cost by 8.74% and depreciation increase on purchased properties by 26.40% are the

reason behind declined operating profit ratio.

Net margin: This measures business efficiency to earn return as an excess of revenues

over total cost incurred (Cesarini and et.al., 2010). In FY 2016, NM dropped down from 15.79%

to 14.96% which indicates that firm has gained lesser return this year on their total turnover.

Although, net profit shows a growth by 13.45% as it has been increased from £171m to £194m,

still, percentage of return over sales came down and reported poor performance. Besides, inflated

housing prices and exceeding overheads, financial cost; interest gone up from £9m to £15m by

66.67% because Harvey Homes Plc had taken borrowings worth £150m in 2016 to finance its

acquisition strategy. In this year, business had paid more tax worth £50m due to higher

availability of profit before tax (PBT) worth £244m. Decreased net profit is a negative sign as it

reflects that company did not performed excellent this year due to poor earnings on total revenue

(Kim and et.al., 2016).

Return on capital employed: This ratio measures operating profit % on total capital

employed in the business. In FY 2015, it was 20.29% dropped down to 18.34% by 9.61% which

reflects that Harvey Homes Plc has earned less earnings on their capital invested in the business

unit (Kumar and Rao, 2016). Although, OP increased by 16.67%, still, high growth in capital

employed from £1,094m to £1,412m by 29.07% due to procurement of funds worth £150m from

the bank borrowings is the main reason behind less ROCE.

Page 4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Statement of financial position

Liquidity & working capital

This ratio provides a quick indication about the firm’s ability to meet out its short-term

liabilities, more importantly, payment to the suppliers.

Attached in Appendix 3

2016 2015

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Current ratio and quick ratio

Figure 3 Current ratio and quick ratio of Harvey Homes Plc

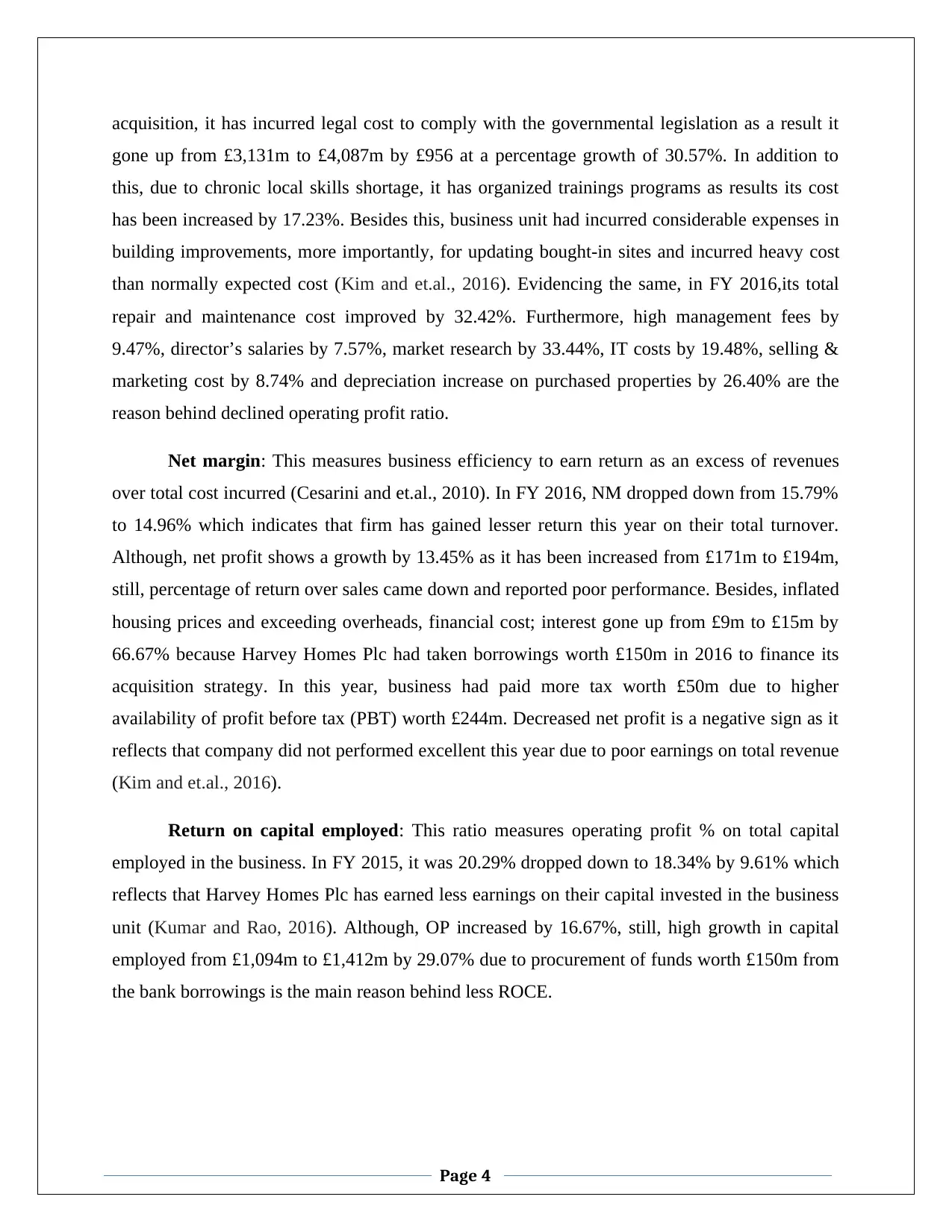

Current ratio: It analyzes that whether the establishment is equipped with enough

amountsof short-term resources or not to pay their current liabilities (Goldmann, 2017). From the

results derived, it can be seen that in 2016, CR shows increase from 3.12:1 to 2.90:1 due to high

growth in CA by 24.08% in comparison to the current liabilities by 15.27%. It is above the

industrialidle ratio of 2:1 that clearly shows that suppliers have no fear regarding their payments

for the credit services provided to Harvey Homes Plc due to sufficient amount of resource

availability. Growth in inventory by 20.53% and better cash liquidity by 141.07% YOY increase

are the reason behind increased liquidity. In contrast, receivables came down by 7.69% because

of decline in credit period allowed to debtors from 13 to 10 days. However, it must be noted that

exceeding CR over standard is a sign of inefficient and unproductive use of cash funds;

therefore, it is considered better to suggest the company to minimize its CR till the target level of

2:1.

Page 5

Liquidity & working capital

This ratio provides a quick indication about the firm’s ability to meet out its short-term

liabilities, more importantly, payment to the suppliers.

Attached in Appendix 3

2016 2015

0.00

0.50

1.00

1.50

2.00

2.50

3.00

3.50

Current ratio and quick ratio

Figure 3 Current ratio and quick ratio of Harvey Homes Plc

Current ratio: It analyzes that whether the establishment is equipped with enough

amountsof short-term resources or not to pay their current liabilities (Goldmann, 2017). From the

results derived, it can be seen that in 2016, CR shows increase from 3.12:1 to 2.90:1 due to high

growth in CA by 24.08% in comparison to the current liabilities by 15.27%. It is above the

industrialidle ratio of 2:1 that clearly shows that suppliers have no fear regarding their payments

for the credit services provided to Harvey Homes Plc due to sufficient amount of resource

availability. Growth in inventory by 20.53% and better cash liquidity by 141.07% YOY increase

are the reason behind increased liquidity. In contrast, receivables came down by 7.69% because

of decline in credit period allowed to debtors from 13 to 10 days. However, it must be noted that

exceeding CR over standard is a sign of inefficient and unproductive use of cash funds;

therefore, it is considered better to suggest the company to minimize its CR till the target level of

2:1.

Page 5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

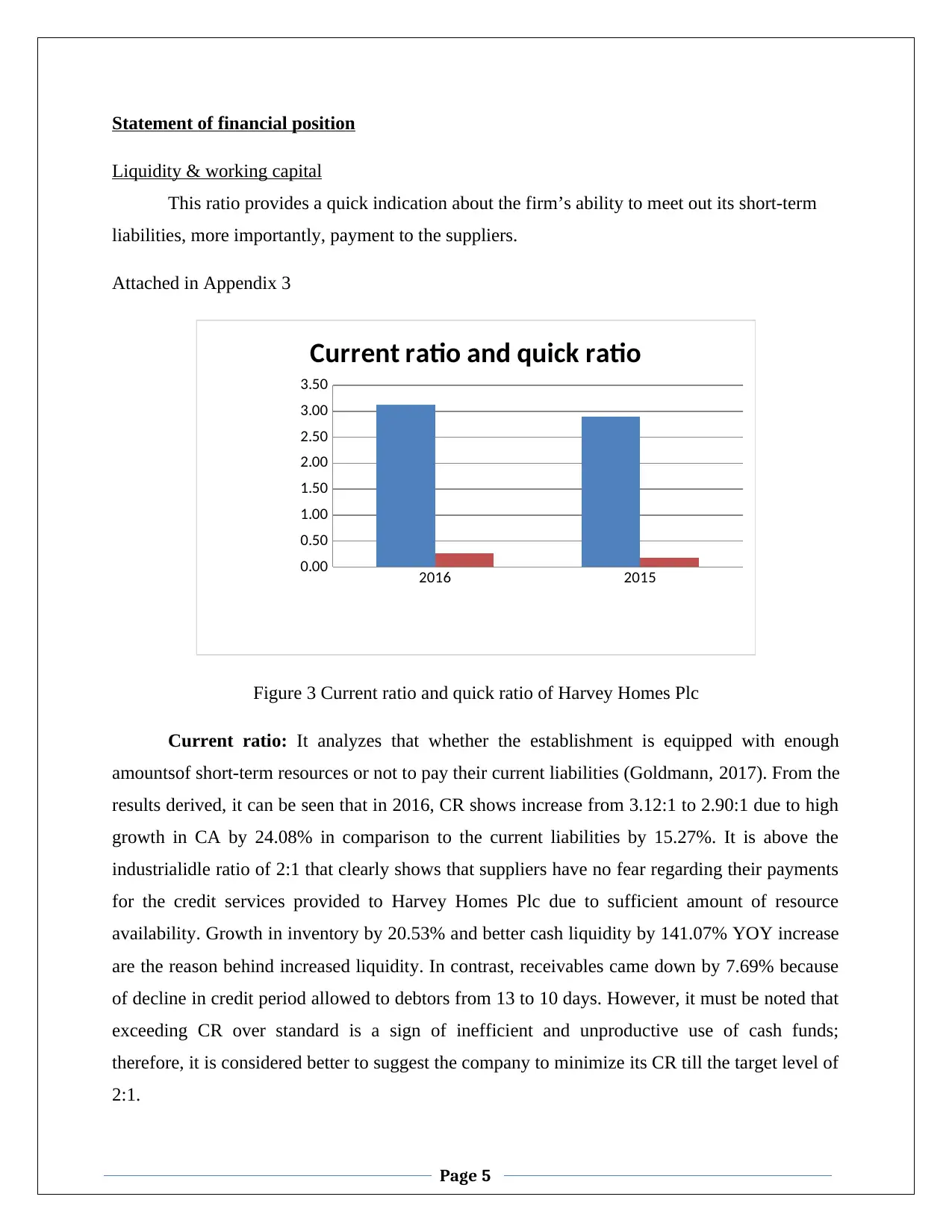

Quick ratio: It goes up from 0.17:1 to 0.27:1 which is not in line (below) with the

industrial benchmark of 1:1. It is far below that CR because high proportion of current assets

comprises inventory balance and in 2016, it goes up by 20.53% from £1,500m to £1,808m. Thus,

without having stock, Harvey Homes Plc will not be able to pay its deferred obligations on time

to their creditors and lack their trustworthiness.

Solvency ratios

This ratio examines company’s financial capabilities to pay off their long-term

obligations, more importantly,lenders.

Attached in Appendix 4

2016 2015

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Debt to equity and interest bearing

ratio

Figure 4 Debt to equity and interest bearing ratio of Harvey Homes plc

In2016, debt to equity ratio has been increased from0.29:1 to 0.39:1 due to more use of

debt collection worth £150m with a YOY% increase of 61.22% whereas equity goes up at an

absolute change of £168m at % change of 19.79%. The ratio is below the reasonable industrial

standard of 0.50:1 which states that it is good for the Harvey Homes Plc to use long-term

borrowings to finance its Midland acquisition project till the time the ratio reaches the target of

0.50:1. Although borrowings bring fixed burden for the business, still, tax benefits and

managerial control are the benefits of it (Lewis and Tan, 2016). It is better to suggest company to

procure funds through debt because in 2016, although, interest bearing ratio goes declined from

Page 6

industrial benchmark of 1:1. It is far below that CR because high proportion of current assets

comprises inventory balance and in 2016, it goes up by 20.53% from £1,500m to £1,808m. Thus,

without having stock, Harvey Homes Plc will not be able to pay its deferred obligations on time

to their creditors and lack their trustworthiness.

Solvency ratios

This ratio examines company’s financial capabilities to pay off their long-term

obligations, more importantly,lenders.

Attached in Appendix 4

2016 2015

0.00

5.00

10.00

15.00

20.00

25.00

30.00

Debt to equity and interest bearing

ratio

Figure 4 Debt to equity and interest bearing ratio of Harvey Homes plc

In2016, debt to equity ratio has been increased from0.29:1 to 0.39:1 due to more use of

debt collection worth £150m with a YOY% increase of 61.22% whereas equity goes up at an

absolute change of £168m at % change of 19.79%. The ratio is below the reasonable industrial

standard of 0.50:1 which states that it is good for the Harvey Homes Plc to use long-term

borrowings to finance its Midland acquisition project till the time the ratio reaches the target of

0.50:1. Although borrowings bring fixed burden for the business, still, tax benefits and

managerial control are the benefits of it (Lewis and Tan, 2016). It is better to suggest company to

procure funds through debt because in 2016, although, interest bearing ratio goes declined from

Page 6

24.67 times to 17.27 times 0.29 which indicates that it is not capable to bear more debt burden

due to increased financial cost. However, on the other side, the ratio is still above the minimum

safety limit of 3:1, therefore, managers must have ability to take additional bank borrowings and

finance their long-term capital requirement by paying debt interest from EBIT as per the loan

repayment scheduled. Designing a balanced capital structure is necessary to maintain financial

cost at minimum level with good solvency (Ucal and Oksay, 2011).

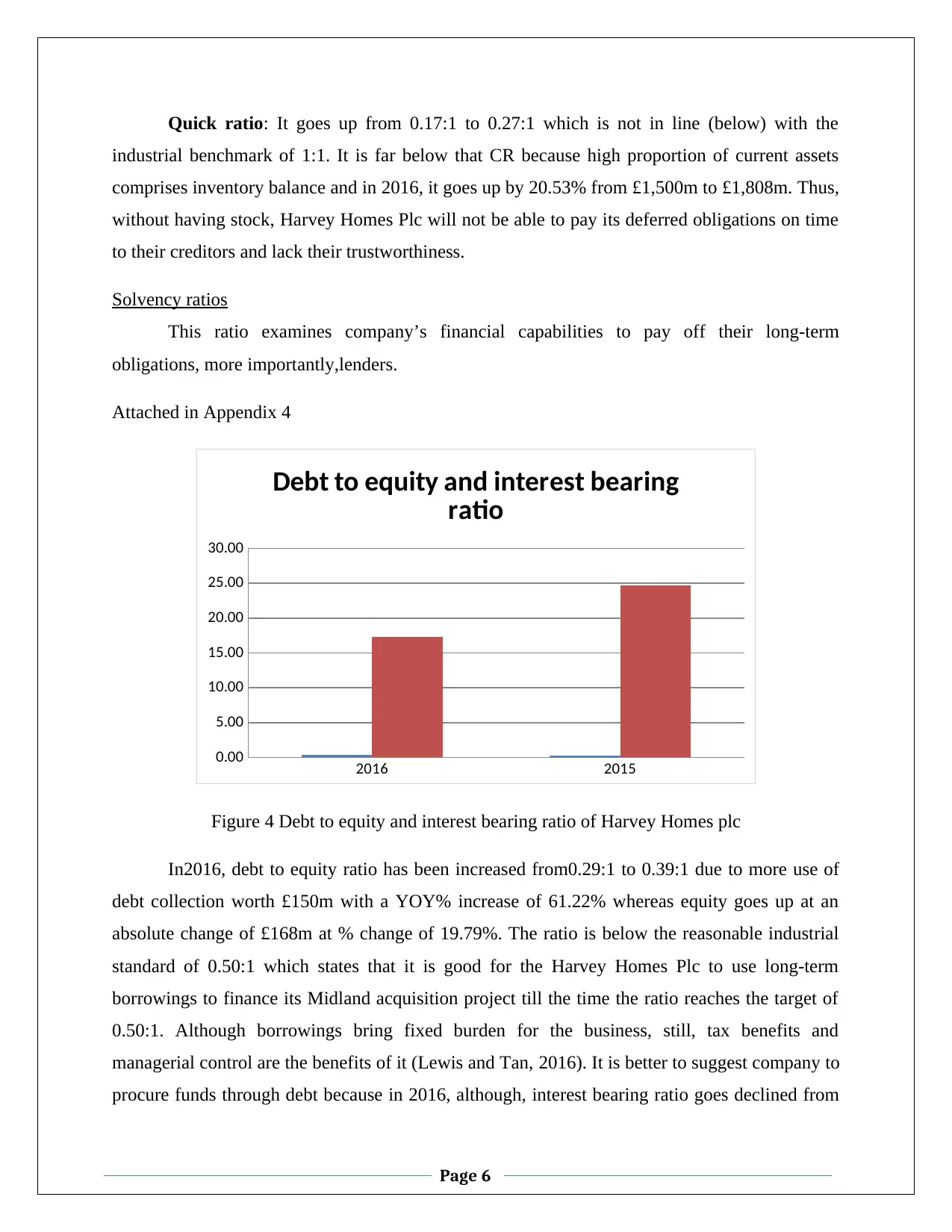

Efficiency ratios

This ratio helps to examine that how productively and efficiently, company is using their

business assets in order to obtain revenue from their operational activities.

Attached in Appendix 5

2016 2015

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Assets turnover ratio and inventory

turnover ratio

Figure 5 Assets turnover ratio & inventory turnover ratio of Harvey Homes Plc

Assets turnover ratio: It goes slightly down from 0.66 times to 0.63 times which

showcase that managers had not utilized their total business assets optimally and effectively as it

do not significantly contributed towards growth in sales revenue.Limited purchase of goods to

not allow the excessive storage of merchandising stock and sales maximization without

purchasing any additional assets will enable entity to raise its assets using efficiency (Delen,

Kuzey and Uyar, 2013).

Page 7

due to increased financial cost. However, on the other side, the ratio is still above the minimum

safety limit of 3:1, therefore, managers must have ability to take additional bank borrowings and

finance their long-term capital requirement by paying debt interest from EBIT as per the loan

repayment scheduled. Designing a balanced capital structure is necessary to maintain financial

cost at minimum level with good solvency (Ucal and Oksay, 2011).

Efficiency ratios

This ratio helps to examine that how productively and efficiently, company is using their

business assets in order to obtain revenue from their operational activities.

Attached in Appendix 5

2016 2015

0.00

0.10

0.20

0.30

0.40

0.50

0.60

0.70

0.80

0.90

1.00

Assets turnover ratio and inventory

turnover ratio

Figure 5 Assets turnover ratio & inventory turnover ratio of Harvey Homes Plc

Assets turnover ratio: It goes slightly down from 0.66 times to 0.63 times which

showcase that managers had not utilized their total business assets optimally and effectively as it

do not significantly contributed towards growth in sales revenue.Limited purchase of goods to

not allow the excessive storage of merchandising stock and sales maximization without

purchasing any additional assets will enable entity to raise its assets using efficiency (Delen,

Kuzey and Uyar, 2013).

Page 7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.