Accountancy and Finance: Hilton Hotels Financial Performance Analysis

VerifiedAdded on 2023/01/03

|20

|5141

|78

Report

AI Summary

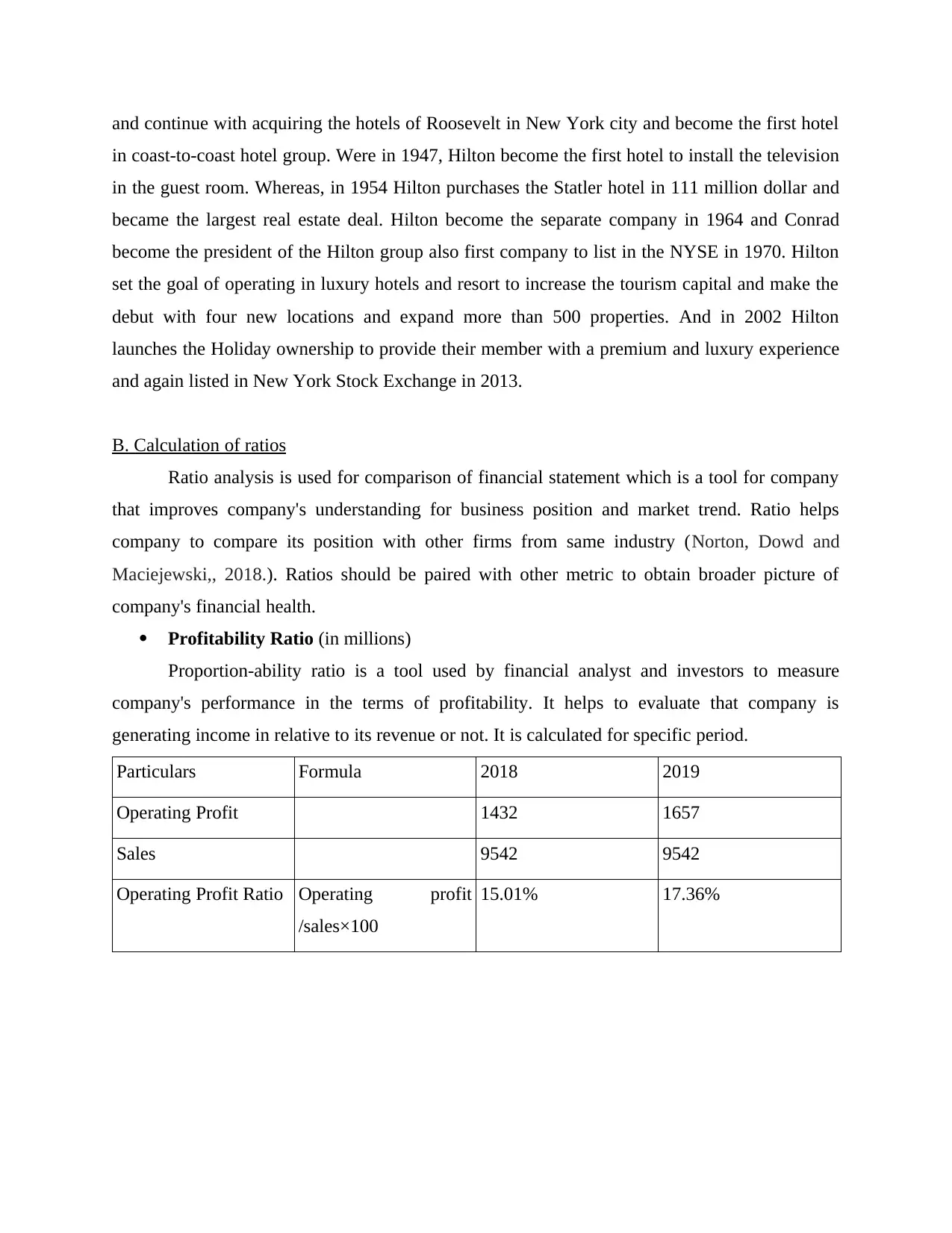

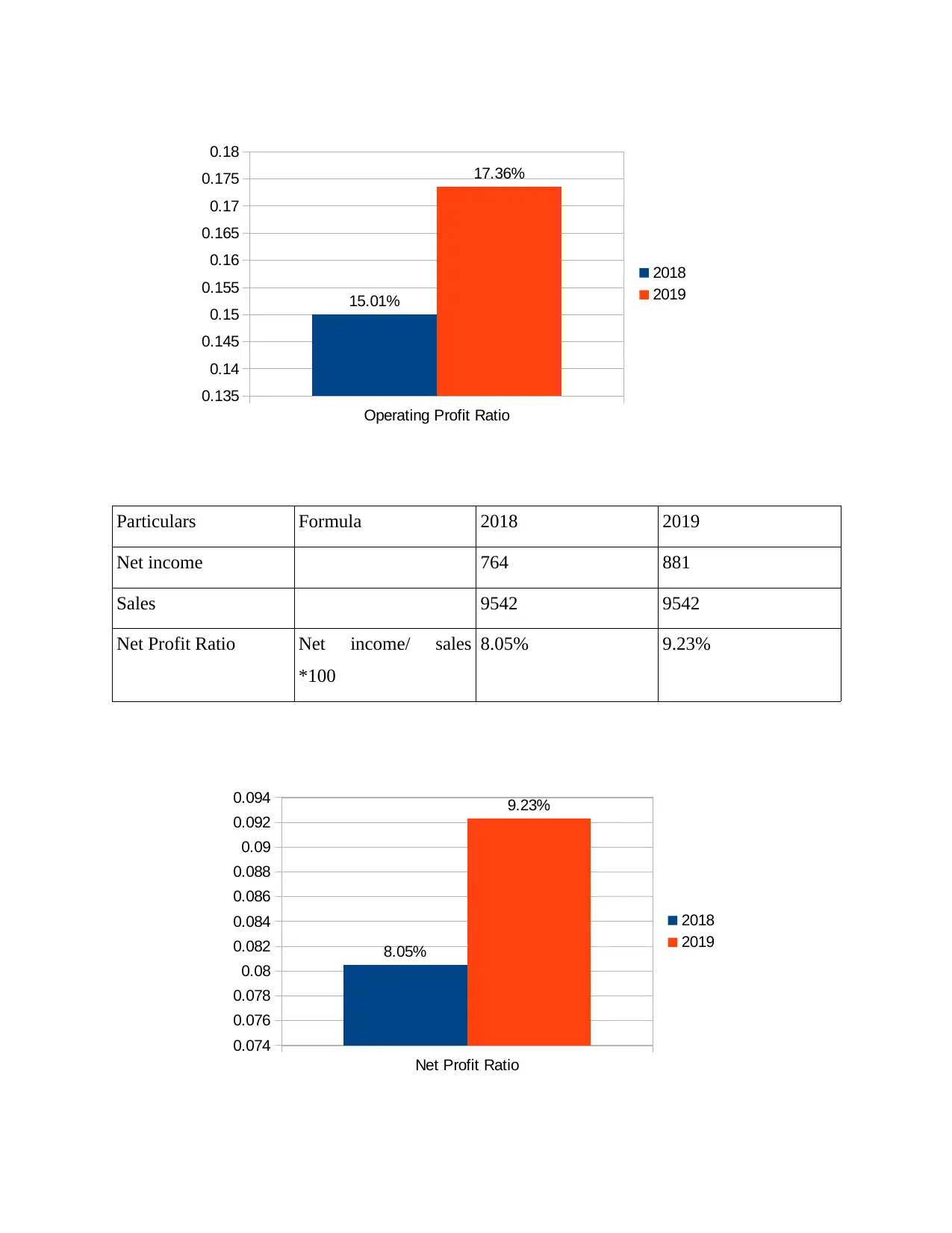

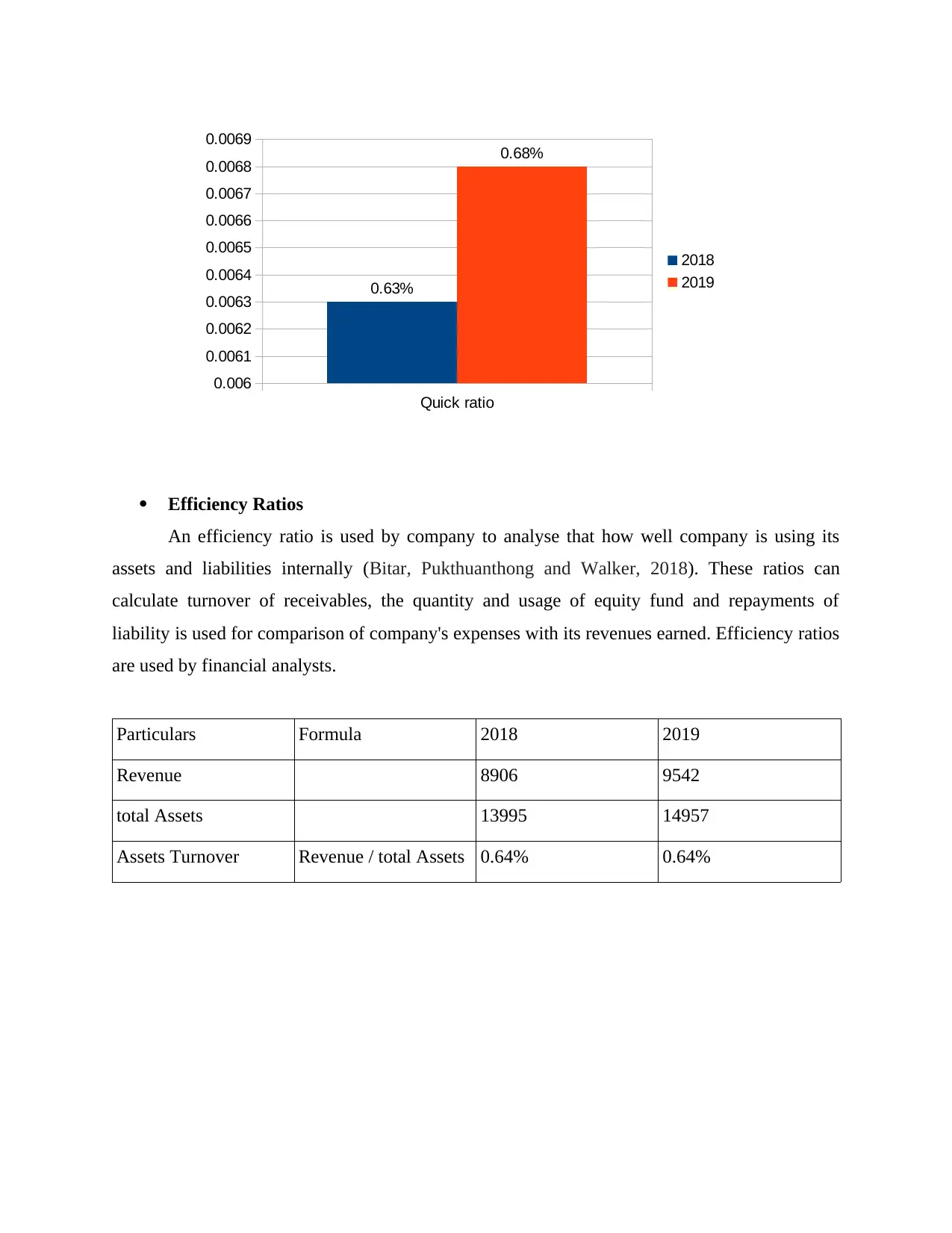

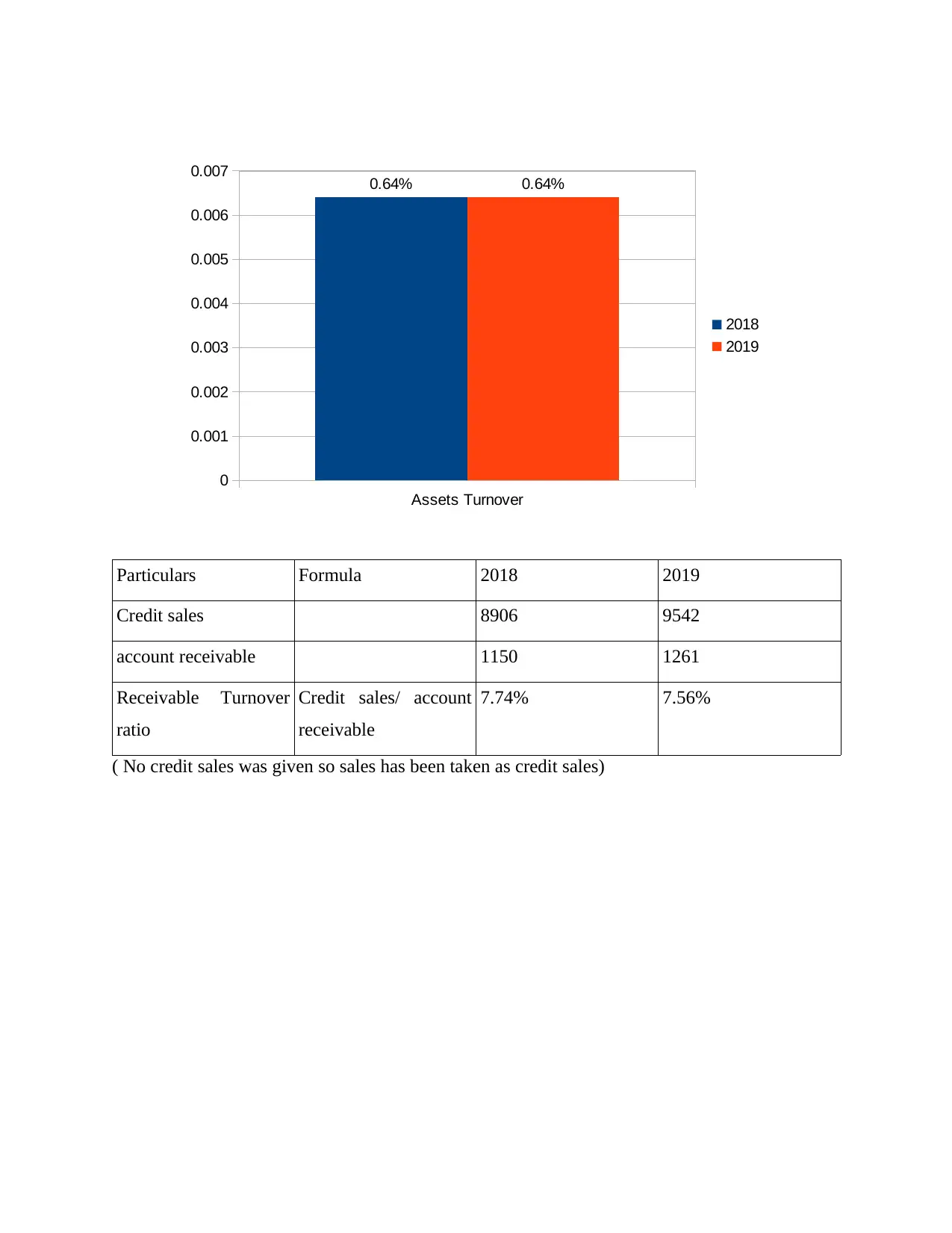

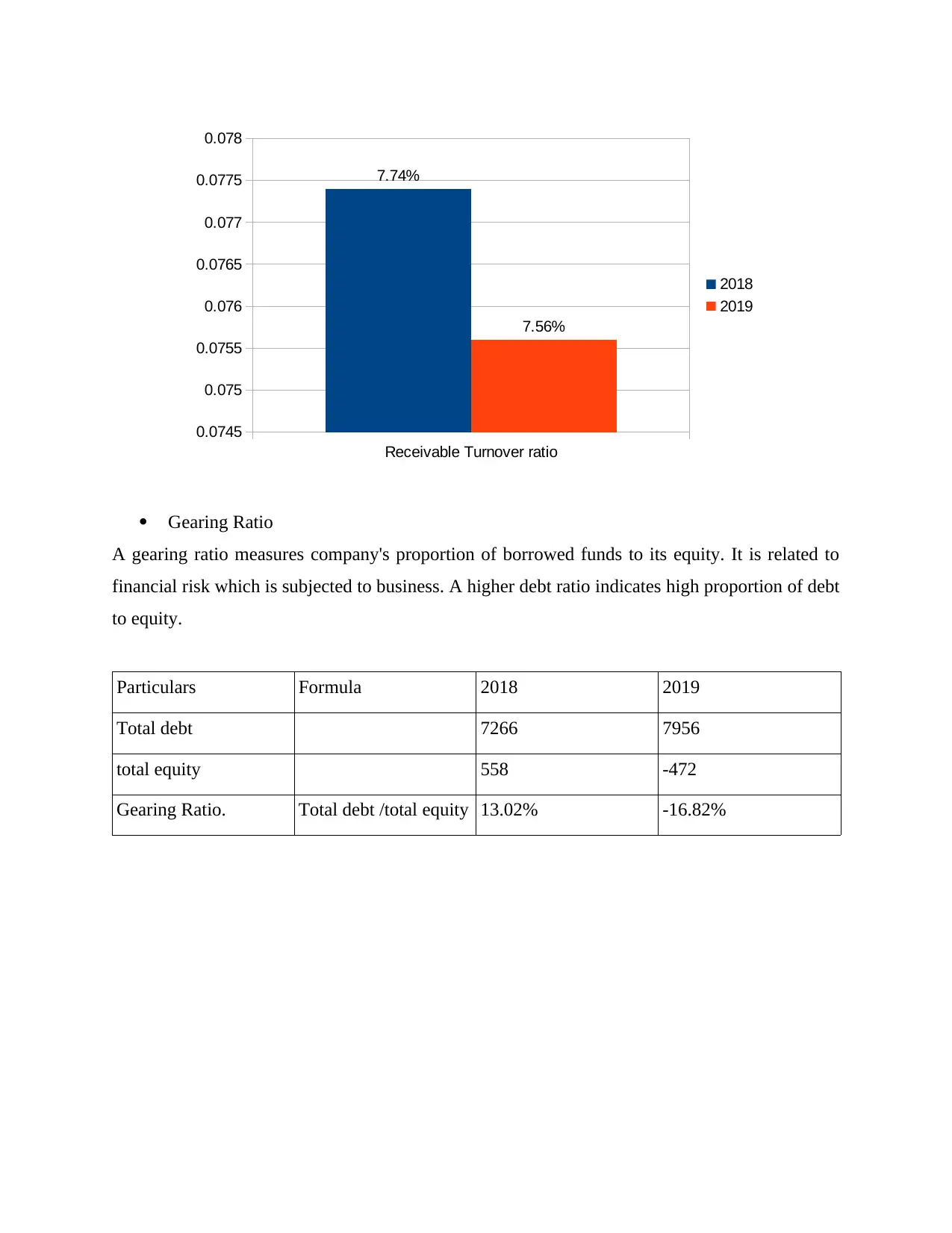

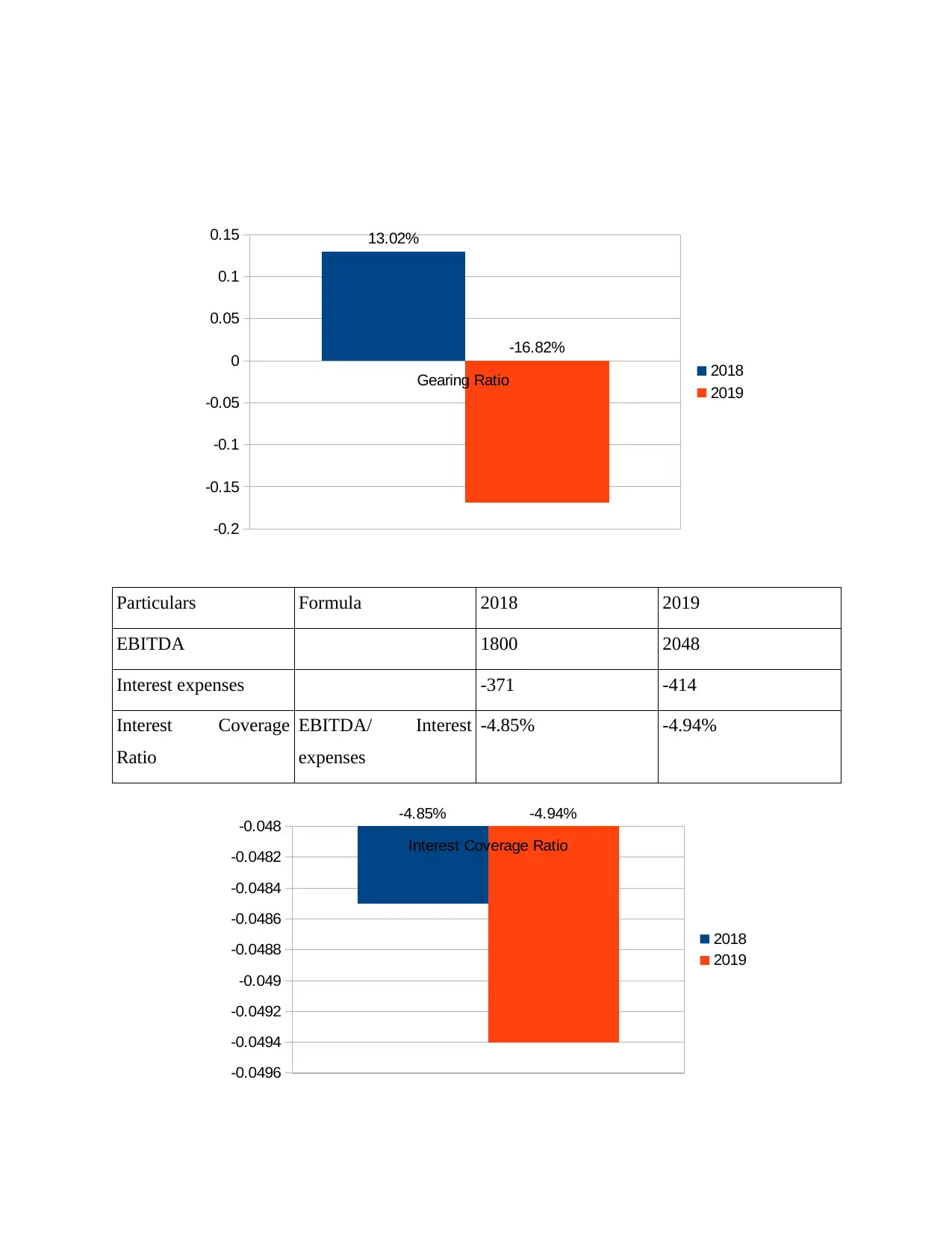

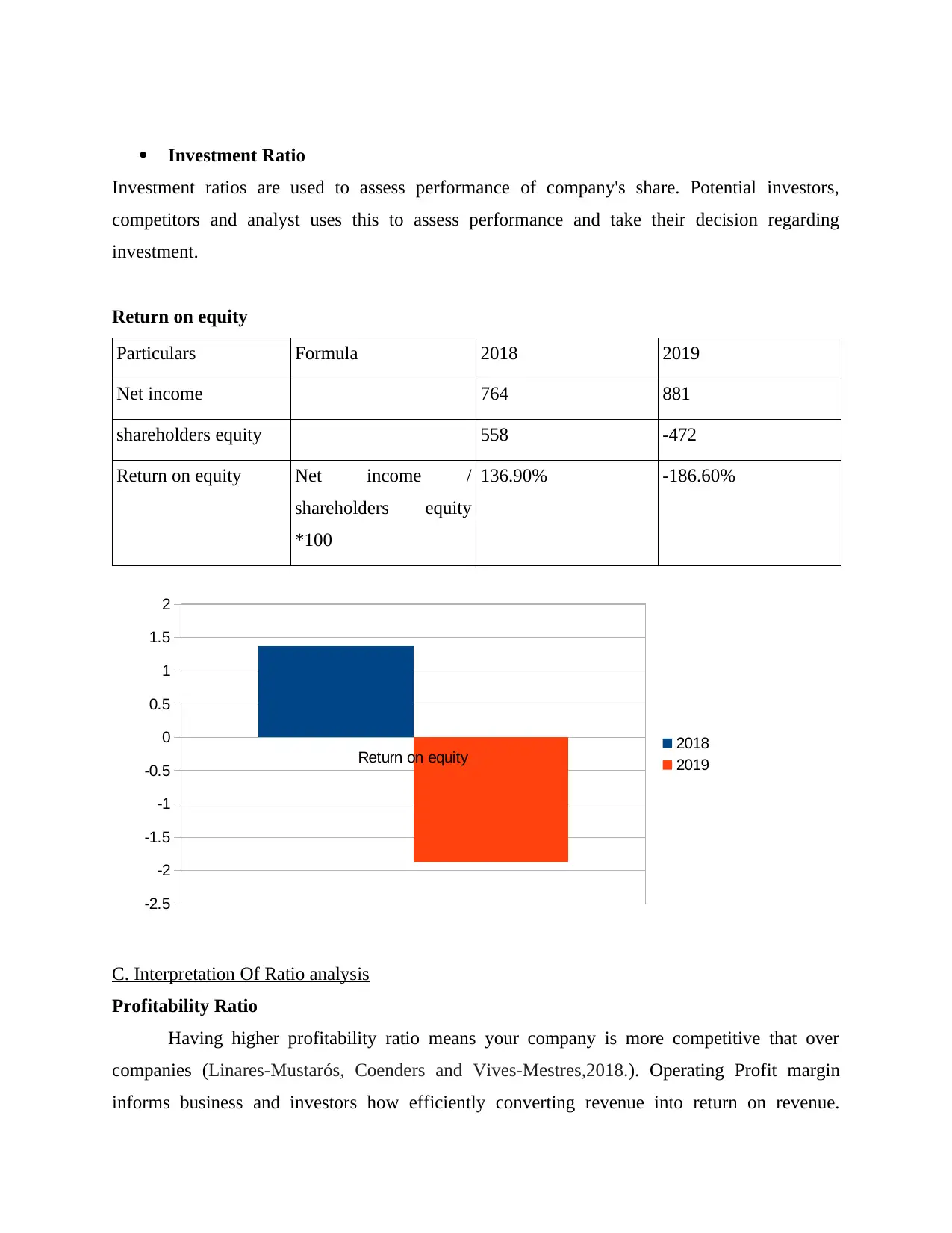

This report presents a comprehensive financial analysis of Hilton Hotels, examining its performance through various financial ratios including profitability, liquidity, efficiency, gearing, and investment ratios. The analysis covers the years 2018 and 2019, providing insights into the company's financial health and trends. Furthermore, the report delves into the strategic aspects of Hilton, incorporating SWOT and PESTLE analyses to evaluate its internal strengths and weaknesses, as well as external opportunities and threats. The report also discusses the strategic and financial rationale for potential investors, considering the company's performance and future prospects. The conclusion synthesizes the findings, offering a holistic view of Hilton's financial standing and strategic positioning in the hospitality industry, making this report valuable for students seeking to understand financial analysis and strategic management.

1 out of 20

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.