Report: Importance of Financial Information for Sainsbury's PLC, 2017

VerifiedAdded on 2021/04/17

|16

|3740

|150

Report

AI Summary

This report critically examines the importance of financial information, using Sainsbury's PLC as a case study. It explores how financial data meets the needs of five key non-management external users: investors, trade creditors, banks and other lenders, tax authorities and regulatory agencies, and employees and labor unions. The report analyzes Sainsbury's financial statements, including the income statement, balance sheet, and cash flow statement, to demonstrate how these stakeholders utilize the company's financial information for decision-making. Furthermore, the report delves into the qualitative characteristics of financial information, differentiating between fundamental characteristics like relevance and faithful representation, and enhancing characteristics such as comparability, verifiability, and timeliness. The analysis highlights how Sainsbury's financial reporting practices adhere to these characteristics, ensuring the information's usefulness and reliability for its external stakeholders.

Running head: IMPORTANCE OF FINANCIAL INFORMATION

Importance of Financial Information

Name of the Student

Name of the University

Author’s Note

Importance of Financial Information

Name of the Student

Name of the University

Author’s Note

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

1IMPORTANCE OF FINANCIAL INFORMATION

Table of Contents

Introduction......................................................................................................................................2

Meeting the Needs of Five Non-Management External Users of Financial Information................2

Qualitative Characteristics of Financial Information......................................................................7

Fundamental Qualitative Characteristics.....................................................................................8

Enhancing Qualitative Characteristics.........................................................................................9

Provision of Information................................................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

Table of Contents

Introduction......................................................................................................................................2

Meeting the Needs of Five Non-Management External Users of Financial Information................2

Qualitative Characteristics of Financial Information......................................................................7

Fundamental Qualitative Characteristics.....................................................................................8

Enhancing Qualitative Characteristics.........................................................................................9

Provision of Information................................................................................................................10

Conclusion.....................................................................................................................................11

References......................................................................................................................................12

2IMPORTANCE OF FINANCIAL INFORMATION

Introduction

Among all the different activities of the business organization, accounting and finance is

considered as the backbone for achieving the organizational objectives and goals. In the process

of accounting and finance, financial information is considered as an integral part for the financial

success of the companies. Different kind of financial information of the companies include credit

information, information about different financial accounts, loan information, taxation

information and many others (Amiram 2012). All these information has a vital part to play in the

decision making process of the people related with the business organizations. In this context, it

needs to be mentioned that there are two types of users of these financial information; they are

internal management users and external non-management users. The main aim of this report is to

analyze and evaluate the aspect that whether the provided financial information of the business

organizations meet the need of five different non-management external users (Theriou 2015). It

is required for this report to consider a London Stock Exchange listed company of United

Kingdom (UK). Thus, Sainsbury’s PLC is taken for this report. Sainsbury’s is the second largest

retail chain having business operation all over UK. The company was founded in the year of

1869 and is headquartered at London, UK. The main products of the company involve

convenience store, supermarket chain, hypermarket and others (About.sainsburys.co.uk 2018).

This particular report involves in the analysis of various financial statements of the company for

the year 2017 in order to achieve its main objective.

Meeting the Needs of Five Non-Management External Users of Financial Information

The above part of the report has mentioned about the existence of two types of users of

financial information; they are internal management users and external non-management users.

Introduction

Among all the different activities of the business organization, accounting and finance is

considered as the backbone for achieving the organizational objectives and goals. In the process

of accounting and finance, financial information is considered as an integral part for the financial

success of the companies. Different kind of financial information of the companies include credit

information, information about different financial accounts, loan information, taxation

information and many others (Amiram 2012). All these information has a vital part to play in the

decision making process of the people related with the business organizations. In this context, it

needs to be mentioned that there are two types of users of these financial information; they are

internal management users and external non-management users. The main aim of this report is to

analyze and evaluate the aspect that whether the provided financial information of the business

organizations meet the need of five different non-management external users (Theriou 2015). It

is required for this report to consider a London Stock Exchange listed company of United

Kingdom (UK). Thus, Sainsbury’s PLC is taken for this report. Sainsbury’s is the second largest

retail chain having business operation all over UK. The company was founded in the year of

1869 and is headquartered at London, UK. The main products of the company involve

convenience store, supermarket chain, hypermarket and others (About.sainsburys.co.uk 2018).

This particular report involves in the analysis of various financial statements of the company for

the year 2017 in order to achieve its main objective.

Meeting the Needs of Five Non-Management External Users of Financial Information

The above part of the report has mentioned about the existence of two types of users of

financial information; they are internal management users and external non-management users.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

3IMPORTANCE OF FINANCIAL INFORMATION

This study involves in the analysis and evaluation of non-management external users of financial

information of Sainsbury’s. Non-management external users refer to the entities or individuals

non involved in the management of the business organizations but are interested in acquiring the

financial information of the companies for different purposes other than management decision-

making. There are different types of non-management external users of financial information for

the companies. In case of Sainsbury’s, five types of non-management external users of financial

information are Investors, Trade Creditors or Suppliers, Bank and Other Lenders, Tax

Authorities and Regulatory Agencies, and Employees and Labor Unions (Arnold et al. 2012).

The following discussion shows how the provided financial information of Sainsbury’s meets the

needs of the above-mentioned external users.

Investors: Investors refer to the persons or business organizations who commit capital in the

businesses in order to get good financial returns and for this reasons, investors are considered as

one of the major non-management external users of financial information (Hull 2012). It needs to

be mentioned that the area of interest of the investors is the past performance of the business

organizations and the potential of the business for future earnings. For this particular reason, it is

required for the business organizations to supersize the historical financial information on their

business performance as it is vital for the investors to assess the profitability of their businesses.

Based on this information, the investors decide whether to hold the investors or to sell it. In case

of Sainsbury’s, it can be seen that the company provides all the financial statements of their

companies for last five years in their official website from where the investors can access all the

required financial information of the company’s performance. Apart from this, Sainsbury’s

always provide five-year financial record in the annual report of each year (Gennaioli, Martin

This study involves in the analysis and evaluation of non-management external users of financial

information of Sainsbury’s. Non-management external users refer to the entities or individuals

non involved in the management of the business organizations but are interested in acquiring the

financial information of the companies for different purposes other than management decision-

making. There are different types of non-management external users of financial information for

the companies. In case of Sainsbury’s, five types of non-management external users of financial

information are Investors, Trade Creditors or Suppliers, Bank and Other Lenders, Tax

Authorities and Regulatory Agencies, and Employees and Labor Unions (Arnold et al. 2012).

The following discussion shows how the provided financial information of Sainsbury’s meets the

needs of the above-mentioned external users.

Investors: Investors refer to the persons or business organizations who commit capital in the

businesses in order to get good financial returns and for this reasons, investors are considered as

one of the major non-management external users of financial information (Hull 2012). It needs to

be mentioned that the area of interest of the investors is the past performance of the business

organizations and the potential of the business for future earnings. For this particular reason, it is

required for the business organizations to supersize the historical financial information on their

business performance as it is vital for the investors to assess the profitability of their businesses.

Based on this information, the investors decide whether to hold the investors or to sell it. In case

of Sainsbury’s, it can be seen that the company provides all the financial statements of their

companies for last five years in their official website from where the investors can access all the

required financial information of the company’s performance. Apart from this, Sainsbury’s

always provide five-year financial record in the annual report of each year (Gennaioli, Martin

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

4IMPORTANCE OF FINANCIAL INFORMATION

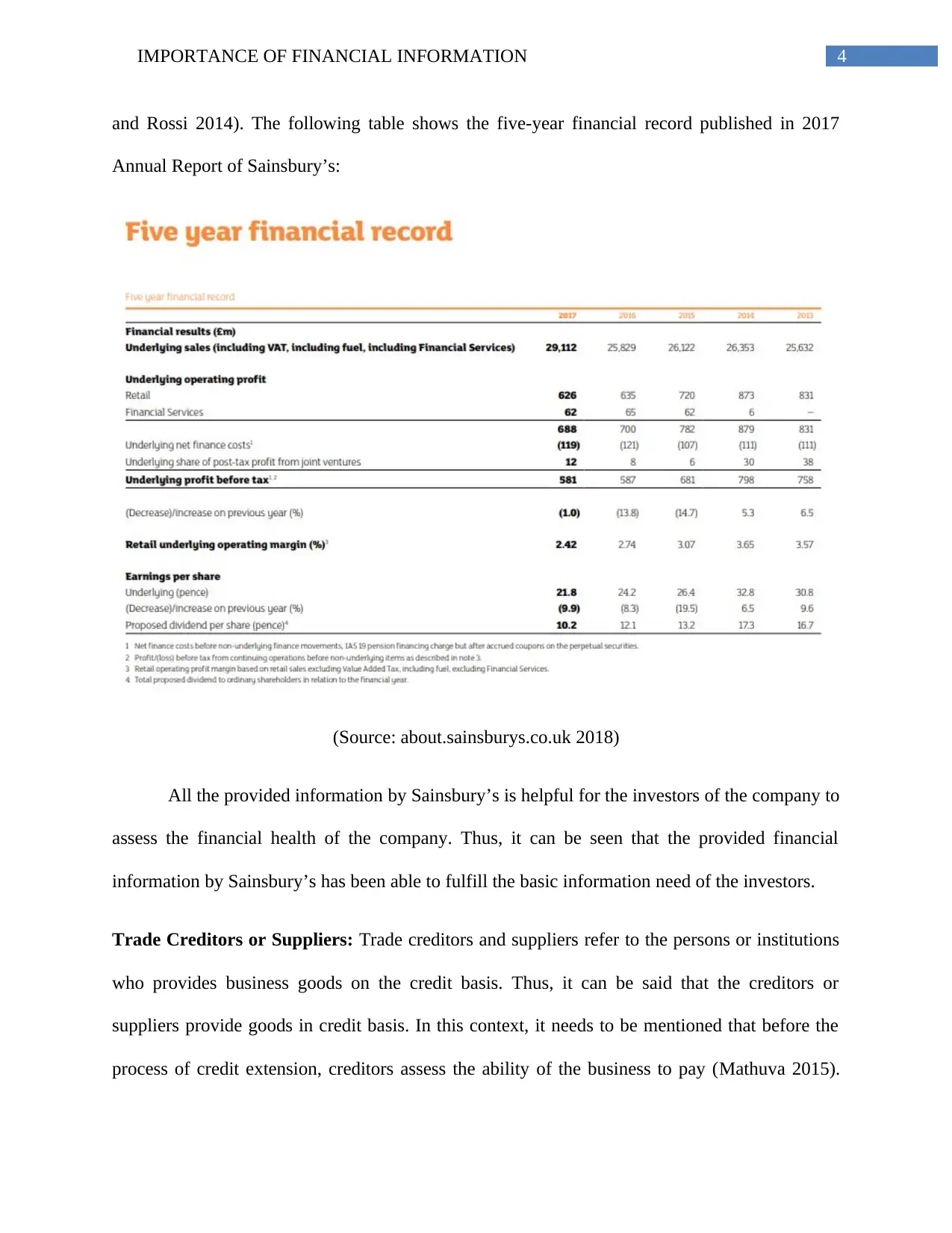

and Rossi 2014). The following table shows the five-year financial record published in 2017

Annual Report of Sainsbury’s:

(Source: about.sainsburys.co.uk 2018)

All the provided information by Sainsbury’s is helpful for the investors of the company to

assess the financial health of the company. Thus, it can be seen that the provided financial

information by Sainsbury’s has been able to fulfill the basic information need of the investors.

Trade Creditors or Suppliers: Trade creditors and suppliers refer to the persons or institutions

who provides business goods on the credit basis. Thus, it can be said that the creditors or

suppliers provide goods in credit basis. In this context, it needs to be mentioned that before the

process of credit extension, creditors assess the ability of the business to pay (Mathuva 2015).

and Rossi 2014). The following table shows the five-year financial record published in 2017

Annual Report of Sainsbury’s:

(Source: about.sainsburys.co.uk 2018)

All the provided information by Sainsbury’s is helpful for the investors of the company to

assess the financial health of the company. Thus, it can be seen that the provided financial

information by Sainsbury’s has been able to fulfill the basic information need of the investors.

Trade Creditors or Suppliers: Trade creditors and suppliers refer to the persons or institutions

who provides business goods on the credit basis. Thus, it can be said that the creditors or

suppliers provide goods in credit basis. In this context, it needs to be mentioned that before the

process of credit extension, creditors assess the ability of the business to pay (Mathuva 2015).

5IMPORTANCE OF FINANCIAL INFORMATION

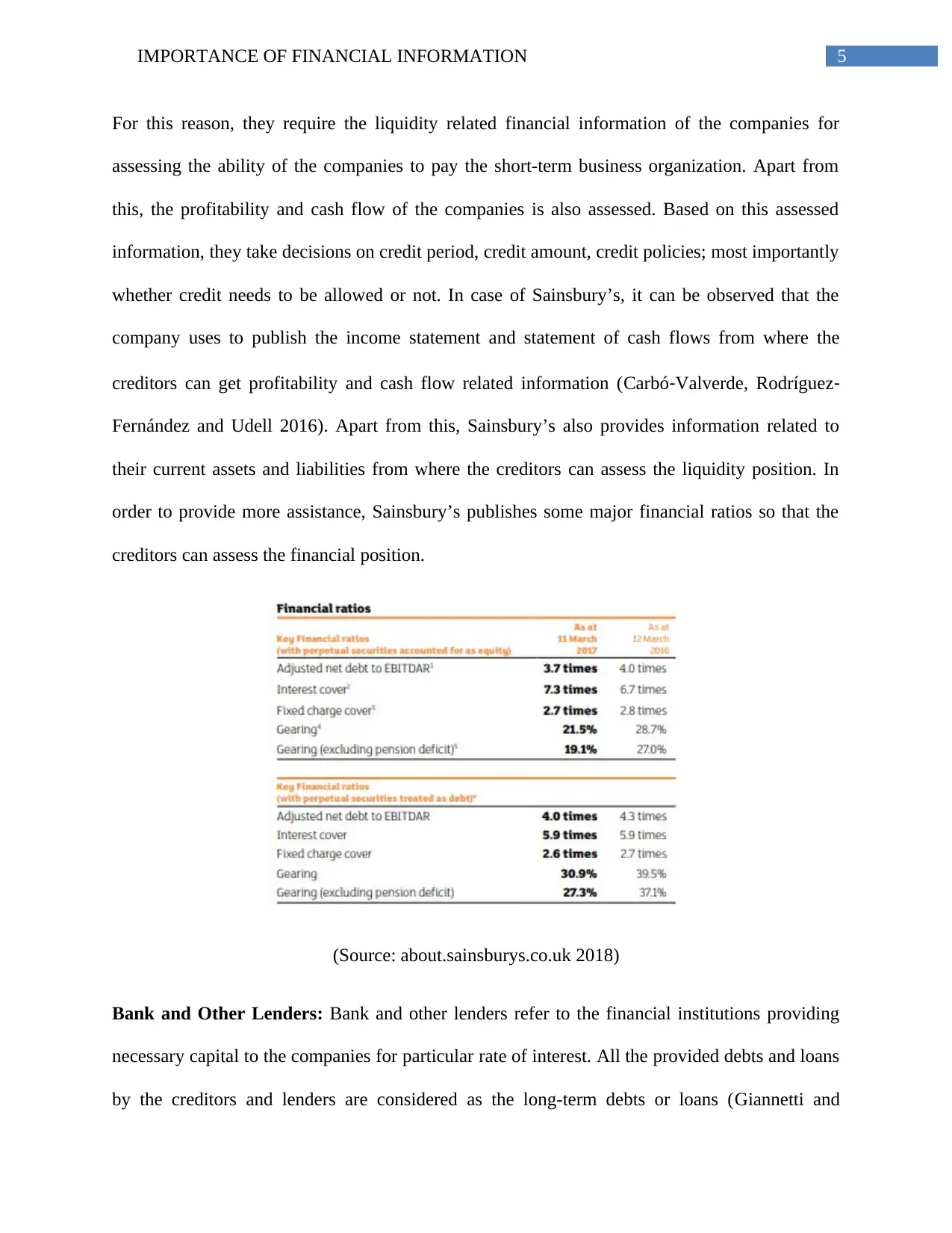

For this reason, they require the liquidity related financial information of the companies for

assessing the ability of the companies to pay the short-term business organization. Apart from

this, the profitability and cash flow of the companies is also assessed. Based on this assessed

information, they take decisions on credit period, credit amount, credit policies; most importantly

whether credit needs to be allowed or not. In case of Sainsbury’s, it can be observed that the

company uses to publish the income statement and statement of cash flows from where the

creditors can get profitability and cash flow related information (Carbó‐Valverde, Rodríguez‐

Fernández and Udell 2016). Apart from this, Sainsbury’s also provides information related to

their current assets and liabilities from where the creditors can assess the liquidity position. In

order to provide more assistance, Sainsbury’s publishes some major financial ratios so that the

creditors can assess the financial position.

(Source: about.sainsburys.co.uk 2018)

Bank and Other Lenders: Bank and other lenders refer to the financial institutions providing

necessary capital to the companies for particular rate of interest. All the provided debts and loans

by the creditors and lenders are considered as the long-term debts or loans (Giannetti and

For this reason, they require the liquidity related financial information of the companies for

assessing the ability of the companies to pay the short-term business organization. Apart from

this, the profitability and cash flow of the companies is also assessed. Based on this assessed

information, they take decisions on credit period, credit amount, credit policies; most importantly

whether credit needs to be allowed or not. In case of Sainsbury’s, it can be observed that the

company uses to publish the income statement and statement of cash flows from where the

creditors can get profitability and cash flow related information (Carbó‐Valverde, Rodríguez‐

Fernández and Udell 2016). Apart from this, Sainsbury’s also provides information related to

their current assets and liabilities from where the creditors can assess the liquidity position. In

order to provide more assistance, Sainsbury’s publishes some major financial ratios so that the

creditors can assess the financial position.

(Source: about.sainsburys.co.uk 2018)

Bank and Other Lenders: Bank and other lenders refer to the financial institutions providing

necessary capital to the companies for particular rate of interest. All the provided debts and loans

by the creditors and lenders are considered as the long-term debts or loans (Giannetti and

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

6IMPORTANCE OF FINANCIAL INFORMATION

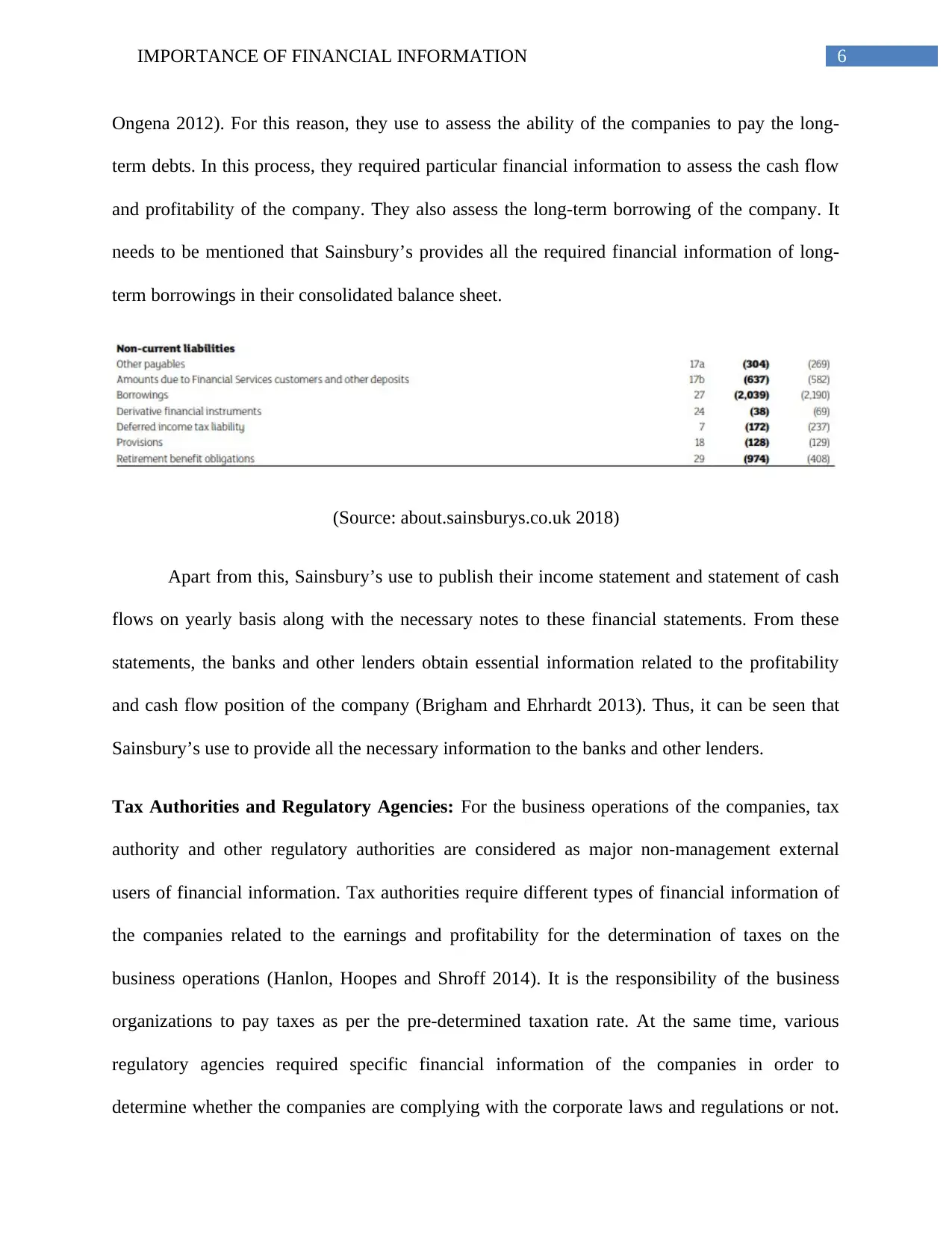

Ongena 2012). For this reason, they use to assess the ability of the companies to pay the long-

term debts. In this process, they required particular financial information to assess the cash flow

and profitability of the company. They also assess the long-term borrowing of the company. It

needs to be mentioned that Sainsbury’s provides all the required financial information of long-

term borrowings in their consolidated balance sheet.

(Source: about.sainsburys.co.uk 2018)

Apart from this, Sainsbury’s use to publish their income statement and statement of cash

flows on yearly basis along with the necessary notes to these financial statements. From these

statements, the banks and other lenders obtain essential information related to the profitability

and cash flow position of the company (Brigham and Ehrhardt 2013). Thus, it can be seen that

Sainsbury’s use to provide all the necessary information to the banks and other lenders.

Tax Authorities and Regulatory Agencies: For the business operations of the companies, tax

authority and other regulatory authorities are considered as major non-management external

users of financial information. Tax authorities require different types of financial information of

the companies related to the earnings and profitability for the determination of taxes on the

business operations (Hanlon, Hoopes and Shroff 2014). It is the responsibility of the business

organizations to pay taxes as per the pre-determined taxation rate. At the same time, various

regulatory agencies required specific financial information of the companies in order to

determine whether the companies are complying with the corporate laws and regulations or not.

Ongena 2012). For this reason, they use to assess the ability of the companies to pay the long-

term debts. In this process, they required particular financial information to assess the cash flow

and profitability of the company. They also assess the long-term borrowing of the company. It

needs to be mentioned that Sainsbury’s provides all the required financial information of long-

term borrowings in their consolidated balance sheet.

(Source: about.sainsburys.co.uk 2018)

Apart from this, Sainsbury’s use to publish their income statement and statement of cash

flows on yearly basis along with the necessary notes to these financial statements. From these

statements, the banks and other lenders obtain essential information related to the profitability

and cash flow position of the company (Brigham and Ehrhardt 2013). Thus, it can be seen that

Sainsbury’s use to provide all the necessary information to the banks and other lenders.

Tax Authorities and Regulatory Agencies: For the business operations of the companies, tax

authority and other regulatory authorities are considered as major non-management external

users of financial information. Tax authorities require different types of financial information of

the companies related to the earnings and profitability for the determination of taxes on the

business operations (Hanlon, Hoopes and Shroff 2014). It is the responsibility of the business

organizations to pay taxes as per the pre-determined taxation rate. At the same time, various

regulatory agencies required specific financial information of the companies in order to

determine whether the companies are complying with the corporate laws and regulations or not.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

7IMPORTANCE OF FINANCIAL INFORMATION

In case of Sainsbury’s, it can be observed that the company uses to publish all the required

information related to taxation in their annual report. For example, it can be mentioned that

Sainsbury’s has provided all the taxation related information in Notes 7 in the annual report of

2017. Apart from this, Sainsbury’s uses to provide information related with the basis of

preparation of their different financial statements along with the significant accounting estimates,

judgments and assumptions (Gitman, Juchau and Flanagan 2015). From all of these financial

statements and notes, the respective tax and regulatory authorities can get their required financial

information.

Employees and Labor Unions: Employees are considered as an important part of the

companies achieving the organizational goals and objectives. At the same time, it is the

responsibility of the business organizations to pay all the necessary remuneration and benefits of

the employees (Benmelech, Bergman and Enriquez 2012). For this reason, it is required for the

employees to obtain necessary financial information related to the performance of the

companies. Thus, the employee and labor unions review the financial condition and performance

of the companies for demining the increase in salary, remuneration and other benefits. Thus, they

can get the required financial information from different financial statements of the companies. It

can be observed that Sainsbury’s use to publish their income statement from where these labor

unions can get the profitability related to the organization (Bova 2013). Apart from this, from the

consolidated balance sheet of Sainsbury’s, they can assess the asset and liability positing. Thus,

it can be said that Sainsbury’s provides all the necessary financial information to the employee

and labor unions with the help of their different financial statements.

In case of Sainsbury’s, it can be observed that the company uses to publish all the required

information related to taxation in their annual report. For example, it can be mentioned that

Sainsbury’s has provided all the taxation related information in Notes 7 in the annual report of

2017. Apart from this, Sainsbury’s uses to provide information related with the basis of

preparation of their different financial statements along with the significant accounting estimates,

judgments and assumptions (Gitman, Juchau and Flanagan 2015). From all of these financial

statements and notes, the respective tax and regulatory authorities can get their required financial

information.

Employees and Labor Unions: Employees are considered as an important part of the

companies achieving the organizational goals and objectives. At the same time, it is the

responsibility of the business organizations to pay all the necessary remuneration and benefits of

the employees (Benmelech, Bergman and Enriquez 2012). For this reason, it is required for the

employees to obtain necessary financial information related to the performance of the

companies. Thus, the employee and labor unions review the financial condition and performance

of the companies for demining the increase in salary, remuneration and other benefits. Thus, they

can get the required financial information from different financial statements of the companies. It

can be observed that Sainsbury’s use to publish their income statement from where these labor

unions can get the profitability related to the organization (Bova 2013). Apart from this, from the

consolidated balance sheet of Sainsbury’s, they can assess the asset and liability positing. Thus,

it can be said that Sainsbury’s provides all the necessary financial information to the employee

and labor unions with the help of their different financial statements.

8IMPORTANCE OF FINANCIAL INFORMATION

Qualitative Characteristics of Financial Information

The above discussion shows how Sainsbury’s meets the financial information need of the

specified five types of non-management external users. Now, it needs to be mentioned that the

financial information of the companies has some major qualitative characteristics making the

information purposeful for the users. They are divided into two parts; fundamental qualitative

characteristics and enhancing qualitative characteristics. The following discussion discusses

about these qualitative characteristics:

Fundamental Qualitative Characteristics

Relevance: The acquired financial information by the external users is required to be relevant

with the decision-making process of them as relevant financial information has the ability to

make difference in the decision-making process. Thus, the financial information must contain

both predictive and confirmatory values. Moreover, both these values are interrelated. In case of

Sainsbury’s, it can be observed that the provided financial information by the company assists

different external users for their different purposes. Moreover, the financial information of

Sainsbury’s has material effect on the financial position of the company (Nobes and Stadler

2015).

Faithful Representation: The financial statements of the companies are full of economic

phenomena in words and numbers. In order to be purposeful to the external users, the financial

information is required to be relevant and it must be presented in the most faithful manner in

order to represent its purposes. Completeness, neutrality and freedom of financial information

increase in the presence of faithful representation (Gebhardt, Mora and Wagenhofer 2014). It

needs to be mentioned that Sainsbury’s has presented all of their financial information by

Qualitative Characteristics of Financial Information

The above discussion shows how Sainsbury’s meets the financial information need of the

specified five types of non-management external users. Now, it needs to be mentioned that the

financial information of the companies has some major qualitative characteristics making the

information purposeful for the users. They are divided into two parts; fundamental qualitative

characteristics and enhancing qualitative characteristics. The following discussion discusses

about these qualitative characteristics:

Fundamental Qualitative Characteristics

Relevance: The acquired financial information by the external users is required to be relevant

with the decision-making process of them as relevant financial information has the ability to

make difference in the decision-making process. Thus, the financial information must contain

both predictive and confirmatory values. Moreover, both these values are interrelated. In case of

Sainsbury’s, it can be observed that the provided financial information by the company assists

different external users for their different purposes. Moreover, the financial information of

Sainsbury’s has material effect on the financial position of the company (Nobes and Stadler

2015).

Faithful Representation: The financial statements of the companies are full of economic

phenomena in words and numbers. In order to be purposeful to the external users, the financial

information is required to be relevant and it must be presented in the most faithful manner in

order to represent its purposes. Completeness, neutrality and freedom of financial information

increase in the presence of faithful representation (Gebhardt, Mora and Wagenhofer 2014). It

needs to be mentioned that Sainsbury’s has presented all of their financial information by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

9IMPORTANCE OF FINANCIAL INFORMATION

complying with the required accounting policies, regulations and company laws. All these

aspects promote faithful representation of the financial information.

Enhancing Qualitative Characteristics

Comparability: Information of the business organizations becomes purposeful when it can be

compared to the similar information of other entities or the same company for other periods. In

the presence of comparability characteristic, the external users can identify and understand the

similarities and differences between this financial information (Yip and Young 2012). In case of

Sainsbury’s, it can be seen that the financial information of this company can be easily compared

to another period or the other companies.

Verifiability: In the presence of verifiability, the external users of financial information can

assure that the financial information is presented faithfully to represent its economic phenomena.

At the same time, in the presence of verifiability, different observers can reach to logical

consensus about the aspect of faithful representation (Tasios and Bekiaris 2012). From the

annual report of Sainsbury’s, it can be observed that the company has provided different kinds of

financial notes to the financial statements that establish the verifiability aspect of financial

information.

Timeliness: External users of financial information need the required financial information at the

time of decision-making. Thus, timeliness characteristic states that financial information needs to

be available to the users at the time of decision-making so that they can influence their decisions

(Kargin 2013). It can be observed that Sainsbury’s use to publish their financial statements at a

particular time of the year so that all the uses can use them at the time of decision-making. Apart

complying with the required accounting policies, regulations and company laws. All these

aspects promote faithful representation of the financial information.

Enhancing Qualitative Characteristics

Comparability: Information of the business organizations becomes purposeful when it can be

compared to the similar information of other entities or the same company for other periods. In

the presence of comparability characteristic, the external users can identify and understand the

similarities and differences between this financial information (Yip and Young 2012). In case of

Sainsbury’s, it can be seen that the financial information of this company can be easily compared

to another period or the other companies.

Verifiability: In the presence of verifiability, the external users of financial information can

assure that the financial information is presented faithfully to represent its economic phenomena.

At the same time, in the presence of verifiability, different observers can reach to logical

consensus about the aspect of faithful representation (Tasios and Bekiaris 2012). From the

annual report of Sainsbury’s, it can be observed that the company has provided different kinds of

financial notes to the financial statements that establish the verifiability aspect of financial

information.

Timeliness: External users of financial information need the required financial information at the

time of decision-making. Thus, timeliness characteristic states that financial information needs to

be available to the users at the time of decision-making so that they can influence their decisions

(Kargin 2013). It can be observed that Sainsbury’s use to publish their financial statements at a

particular time of the year so that all the uses can use them at the time of decision-making. Apart

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

10IMPORTANCE OF FINANCIAL INFORMATION

from this, Sainsbury’s also publishes quarterly interim financial reports at the particular time of

the year in order to provide more support in their decision-making process.

Understandability: Understandability of the financial information can be established by

classifying, characterizing and presenting the financial information in a clear and concise manner

(Gebhardt, Mora and Wagenhofer 2014). For this reason, financial statements must be prepared

in simple form. In case of Sainsbury’s, it can be observed that the company uses to prepare their

financial statements in user-friendly manner so that the users can easily access information from

them for the purpose of analysis and evaluation.

Provision of Information

From the analysis of the annual report of Sainsbury’s, it can be observed that the

company uses to provide all kind of financial information with the help of different financial

statements like income statement, consolidated balance sheet, statement of cash flow, statement

of change in equity and statement of cash flow (Togashi et al. 2014). In this context, provision of

information refers to the process within which financial information is provided to the non-

management external users. In case of Sainsbury’s, it can be observed that the main provision of

information of this company is the publication of financial statements of the company.

Sainsbury’s publishes their financial statements along with their annual report. Apart from this,

the company uses to publish their interim financial report on quarterly basis. These are the main

provisions for financial information in Sainsbury’s. Moreover, the company also arranges

different meetings in order to announce the good performance of their business. In addition,

external users can use the official website of Sainsbury’s to access the required financial

information (Godoy et al. 2012). Thus, from the above discussion, it can be seen Sainsbury’s has

from this, Sainsbury’s also publishes quarterly interim financial reports at the particular time of

the year in order to provide more support in their decision-making process.

Understandability: Understandability of the financial information can be established by

classifying, characterizing and presenting the financial information in a clear and concise manner

(Gebhardt, Mora and Wagenhofer 2014). For this reason, financial statements must be prepared

in simple form. In case of Sainsbury’s, it can be observed that the company uses to prepare their

financial statements in user-friendly manner so that the users can easily access information from

them for the purpose of analysis and evaluation.

Provision of Information

From the analysis of the annual report of Sainsbury’s, it can be observed that the

company uses to provide all kind of financial information with the help of different financial

statements like income statement, consolidated balance sheet, statement of cash flow, statement

of change in equity and statement of cash flow (Togashi et al. 2014). In this context, provision of

information refers to the process within which financial information is provided to the non-

management external users. In case of Sainsbury’s, it can be observed that the main provision of

information of this company is the publication of financial statements of the company.

Sainsbury’s publishes their financial statements along with their annual report. Apart from this,

the company uses to publish their interim financial report on quarterly basis. These are the main

provisions for financial information in Sainsbury’s. Moreover, the company also arranges

different meetings in order to announce the good performance of their business. In addition,

external users can use the official website of Sainsbury’s to access the required financial

information (Godoy et al. 2012). Thus, from the above discussion, it can be seen Sainsbury’s has

11IMPORTANCE OF FINANCIAL INFORMATION

established some effective means for provision of information for the external users and all these

provisions are effective to provide financial information to the external users. Hence, it can be

said that there is not any weakness in the provision of information for Sainsbury’s to the external

users.

Conclusion

From the above discussion, it can be observed that the business organizations are required

to provide the external users with necessary financial information for the purpose of different

decision-making. The above discussion states that there are five major non-management external

users of financial information; they are Investors, Trade Creditors or Suppliers, Bank and Other

Lenders, Tax Authorities and Regulatory Agencies, and Employees and Labor Unions. All these

non-management external users of financial information require different and in some cases,

similar types of financial information for different purposes like investment decision-making,

credit decision-making, decision related to the increase in salary, determination of taxation

expenses and others. From the above discussion, it can also be seen that the financial information

needs to possess some qualitative characteristics in order to be useful to the external users for

various purposes. The fundamental qualitative characteristics are relevance and faithful

representation; the enhancing qualitative characteristics are verifiability, comparability,

timeliness and understandability. Lastly, it can be observed that Sainsbury’s has established

effective provisions for financial information to their external users like publication of annual

report, interim financial report and others. For this reason, there is not much weaknesses in the

process of provision of information in Sainsbury’s.

established some effective means for provision of information for the external users and all these

provisions are effective to provide financial information to the external users. Hence, it can be

said that there is not any weakness in the provision of information for Sainsbury’s to the external

users.

Conclusion

From the above discussion, it can be observed that the business organizations are required

to provide the external users with necessary financial information for the purpose of different

decision-making. The above discussion states that there are five major non-management external

users of financial information; they are Investors, Trade Creditors or Suppliers, Bank and Other

Lenders, Tax Authorities and Regulatory Agencies, and Employees and Labor Unions. All these

non-management external users of financial information require different and in some cases,

similar types of financial information for different purposes like investment decision-making,

credit decision-making, decision related to the increase in salary, determination of taxation

expenses and others. From the above discussion, it can also be seen that the financial information

needs to possess some qualitative characteristics in order to be useful to the external users for

various purposes. The fundamental qualitative characteristics are relevance and faithful

representation; the enhancing qualitative characteristics are verifiability, comparability,

timeliness and understandability. Lastly, it can be observed that Sainsbury’s has established

effective provisions for financial information to their external users like publication of annual

report, interim financial report and others. For this reason, there is not much weaknesses in the

process of provision of information in Sainsbury’s.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.