Accounting and Finance: Investment Analysis and Recommendation Report

VerifiedAdded on 2020/01/28

|16

|3659

|165

Report

AI Summary

This report provides a comprehensive financial analysis of two companies, Next PLC and Hennes & Mauritz, to aid Asol Ltd. in making investment decisions. The analysis includes a detailed examination of financial ratios such as gross profit margin, net profit margin, current ratio, and return on equity, comparing their performance over several years. The report also includes non-financial ratio analysis, charts and recommendations for Hennes & Mauritz to improve its financial performance. Furthermore, the report applies capital investment appraisal techniques, including payback period and cash flow analysis, to evaluate potential investments for Hilltop Limited. The conclusion emphasizes the importance of financial analysis in making informed investment choices and highlights the limitations of ratio analysis.

ACCOUNTING AND

FINANCE

1 | P a g e

FINANCE

1 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION......................................................................................................................1

Financial performance analysis..................................................................................................1

Analyse the performance and financial position...................................................................1

Preparation of Charts.............................................................................................................3

Recommendation to Hennes & Mauritz................................................................................6

Limitation of ratio analysis....................................................................................................7

CAPITAL INVESTMENT APPRAISAL TECHNIQUES........................................................7

Cash inflow............................................................................................................................7

Payback period......................................................................................................................8

Net present value...................................................................................................................9

Accounting rate of return (ARR).........................................................................................10

Limitations of investment appraisal techniques..................................................................10

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................12

2 | P a g e

INTRODUCTION......................................................................................................................1

Financial performance analysis..................................................................................................1

Analyse the performance and financial position...................................................................1

Preparation of Charts.............................................................................................................3

Recommendation to Hennes & Mauritz................................................................................6

Limitation of ratio analysis....................................................................................................7

CAPITAL INVESTMENT APPRAISAL TECHNIQUES........................................................7

Cash inflow............................................................................................................................7

Payback period......................................................................................................................8

Net present value...................................................................................................................9

Accounting rate of return (ARR).........................................................................................10

Limitations of investment appraisal techniques..................................................................10

CONCLUSION........................................................................................................................10

REFERENCES.........................................................................................................................12

2 | P a g e

Illustration Index

Illustration 1: Gross profit ratio of Next PLC............................................................................3

Illustration 2: Gross profit ratio of H & M business..................................................................4

Illustration 3: Net profit of Next PLC........................................................................................4

Illustration 4: Net profit margin Of H & M................................................................................5

Illustration 5: Current ratio and quick ratio of Next PLC..........................................................5

Illustration 6: Current ratio and quick ratio of H & M...............................................................6

3 | P a g e

Illustration 1: Gross profit ratio of Next PLC............................................................................3

Illustration 2: Gross profit ratio of H & M business..................................................................4

Illustration 3: Net profit of Next PLC........................................................................................4

Illustration 4: Net profit margin Of H & M................................................................................5

Illustration 5: Current ratio and quick ratio of Next PLC..........................................................5

Illustration 6: Current ratio and quick ratio of H & M...............................................................6

3 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Accounting and finance plays a significant role in every organization to take qualified

decisions. Asol Ltd. is a large fashion retailer company considering to purchase shares in

either Next PLC or Hennes & Maurtiz Company. In this report, financial analysis has been

done for both theses two cloth retailing company that are listed on London Stock Exchange.

Through making financial as well as non financial analysis, the CFO of Asol Ltd. will be able

to take appropriate investment decisions. In addition to it, capital budgeting tools also will be

applied to take long term investment decisions for Hilltop Limited.

FINANCIAL PERFORMANCE ANALYSIS

Analyse the performance and financial position

Analysing the business performance through financial ratios is explained here:

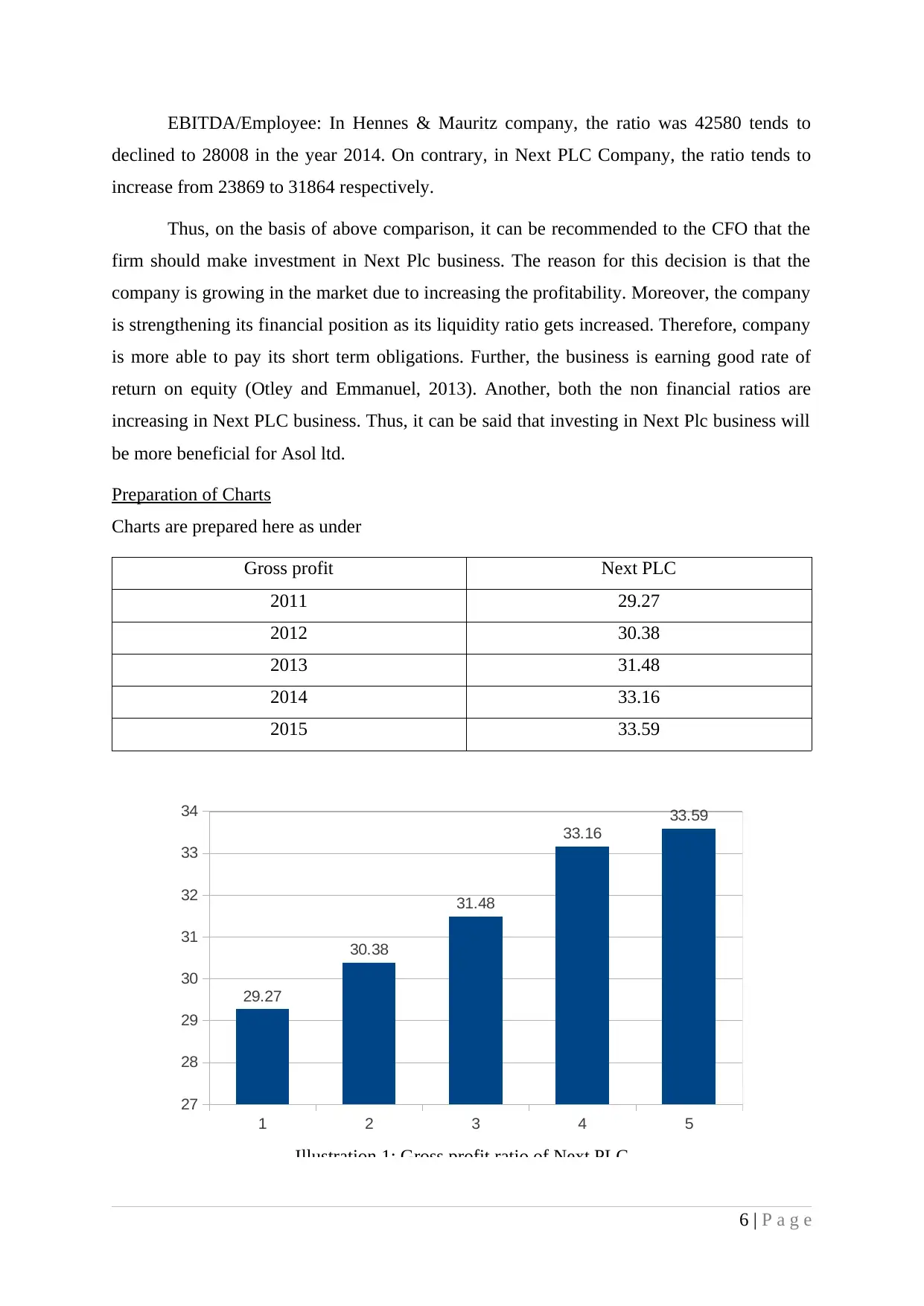

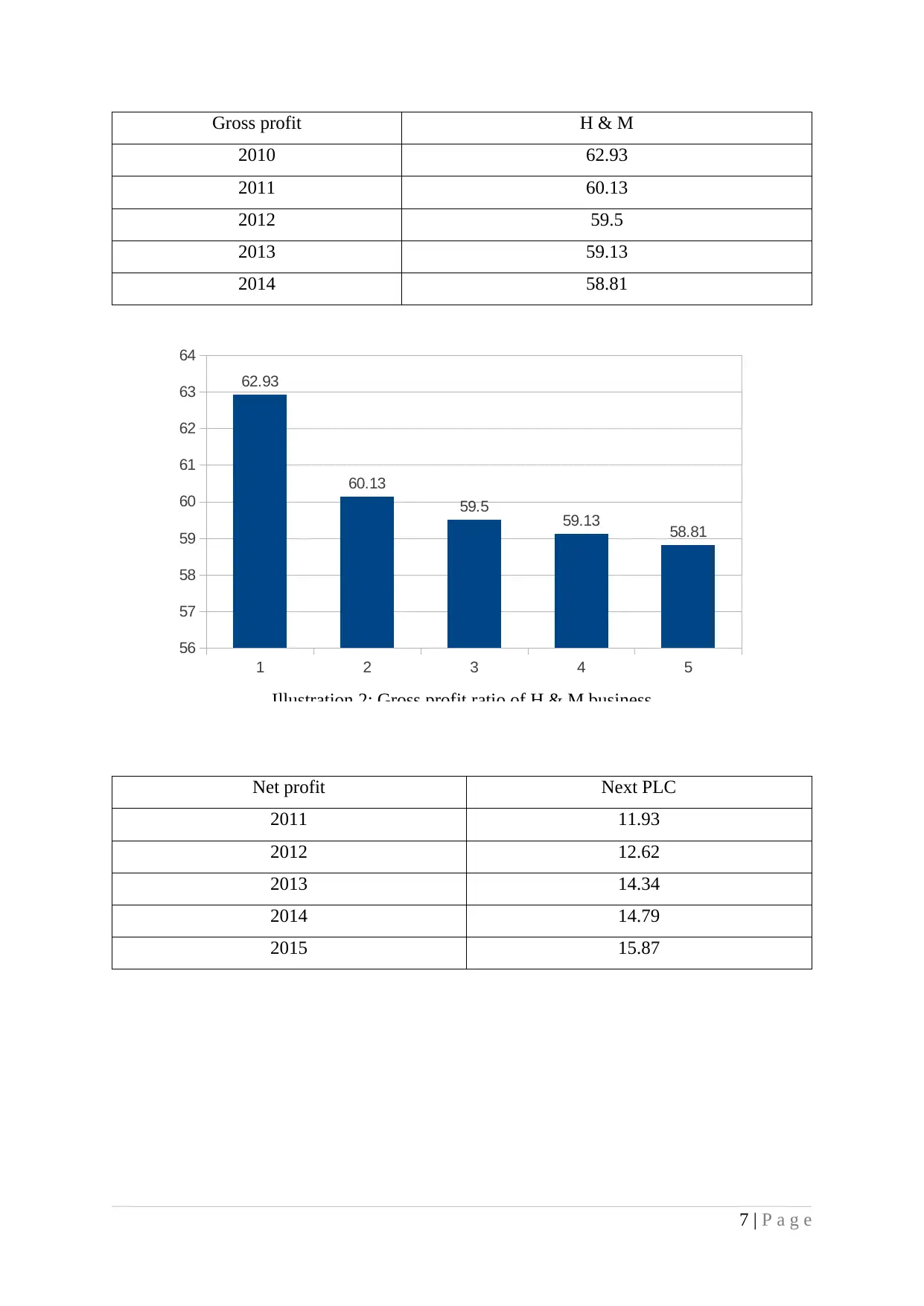

Gross profit ratio: The excess of total business revenues over the total cost of goods

sold is known as gross profit margin (Kaplan and Atkinson, 2015). The gross profit ratio of

Next PLC business shows an increasing trend. In the year 2011, the gross margin was 29.27%

get increased to 33.59% in the year 2015. However, the gross profit ratio of H & M business

shows an declining trend as it get decreased from 62.93% to 58.81% respectively. The ratio

indicates that Next PLC is generating greater gross profitability for the business implies that

the business is performing better as compare to the H & M.

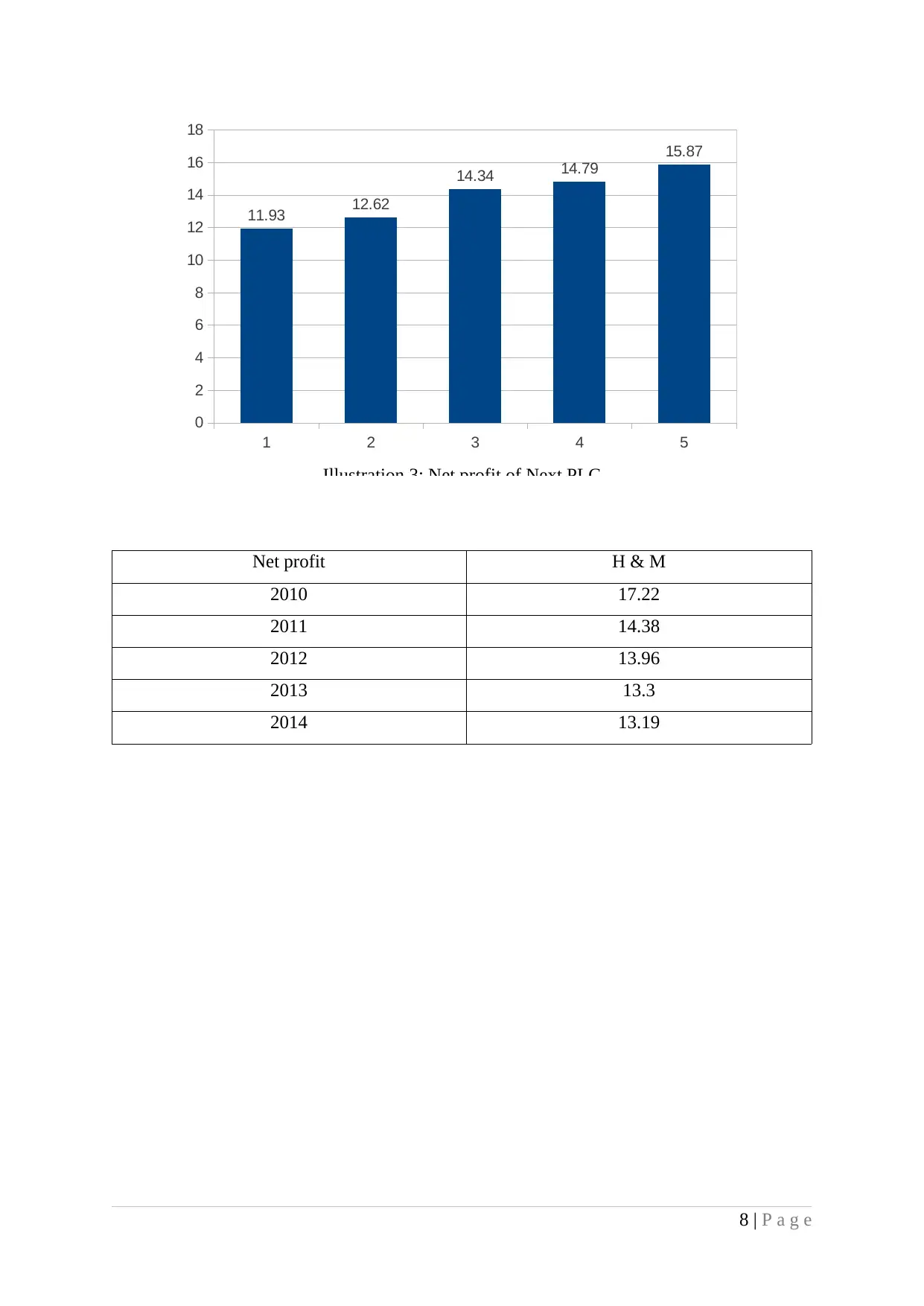

Net profit ratio: Net profit is the difference between gross margin and total of indirect

business expenses. It represents the net operational results of the business operations (Ward,

2012). The net profit margin of H & M business shows a decreasing trend. In the year 2010,

the net profit margin was 17.22% get decreased to 13.19% in the year 2014. However, the net

profit margin of Next PLC business gets increase from 11.93% to 15.87% in the year 2015. It

implies that Next PLC is earning higher net profits indicate better business performance.

Operating profit ratio: In H & M Company, the operating margin gets declined from

22.73% to 16.90% in the year 2014. However, in Next PLC the ratio get increased from

17.19% to 20.62%. Thus, it can be said that Next PLC Company is generating higher the

operating profit from its operating functions.

Return on equity: Hennes and Mauritz business is earning return on equity of 41.27%

while return on equity for Next PLC business is 208.75%. It indicates that Next PLC business

is getting larger amount of profitability on its equity. Thus, the performance of Next PLC

Company is quite better than Hennes and Mauritz (Gadoiu, n.d).

4 | P a g e

Accounting and finance plays a significant role in every organization to take qualified

decisions. Asol Ltd. is a large fashion retailer company considering to purchase shares in

either Next PLC or Hennes & Maurtiz Company. In this report, financial analysis has been

done for both theses two cloth retailing company that are listed on London Stock Exchange.

Through making financial as well as non financial analysis, the CFO of Asol Ltd. will be able

to take appropriate investment decisions. In addition to it, capital budgeting tools also will be

applied to take long term investment decisions for Hilltop Limited.

FINANCIAL PERFORMANCE ANALYSIS

Analyse the performance and financial position

Analysing the business performance through financial ratios is explained here:

Gross profit ratio: The excess of total business revenues over the total cost of goods

sold is known as gross profit margin (Kaplan and Atkinson, 2015). The gross profit ratio of

Next PLC business shows an increasing trend. In the year 2011, the gross margin was 29.27%

get increased to 33.59% in the year 2015. However, the gross profit ratio of H & M business

shows an declining trend as it get decreased from 62.93% to 58.81% respectively. The ratio

indicates that Next PLC is generating greater gross profitability for the business implies that

the business is performing better as compare to the H & M.

Net profit ratio: Net profit is the difference between gross margin and total of indirect

business expenses. It represents the net operational results of the business operations (Ward,

2012). The net profit margin of H & M business shows a decreasing trend. In the year 2010,

the net profit margin was 17.22% get decreased to 13.19% in the year 2014. However, the net

profit margin of Next PLC business gets increase from 11.93% to 15.87% in the year 2015. It

implies that Next PLC is earning higher net profits indicate better business performance.

Operating profit ratio: In H & M Company, the operating margin gets declined from

22.73% to 16.90% in the year 2014. However, in Next PLC the ratio get increased from

17.19% to 20.62%. Thus, it can be said that Next PLC Company is generating higher the

operating profit from its operating functions.

Return on equity: Hennes and Mauritz business is earning return on equity of 41.27%

while return on equity for Next PLC business is 208.75%. It indicates that Next PLC business

is getting larger amount of profitability on its equity. Thus, the performance of Next PLC

Company is quite better than Hennes and Mauritz (Gadoiu, n.d).

4 | P a g e

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

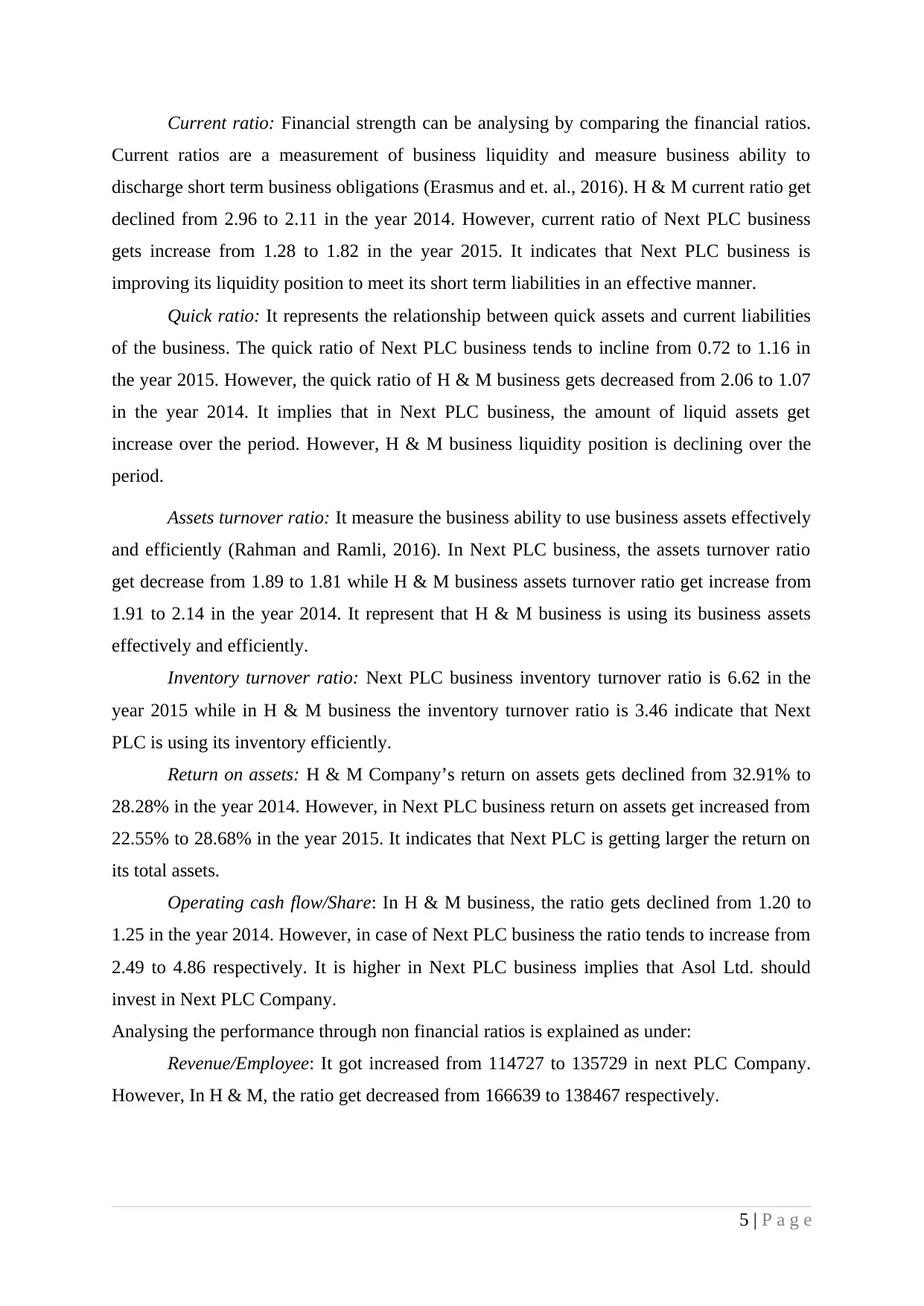

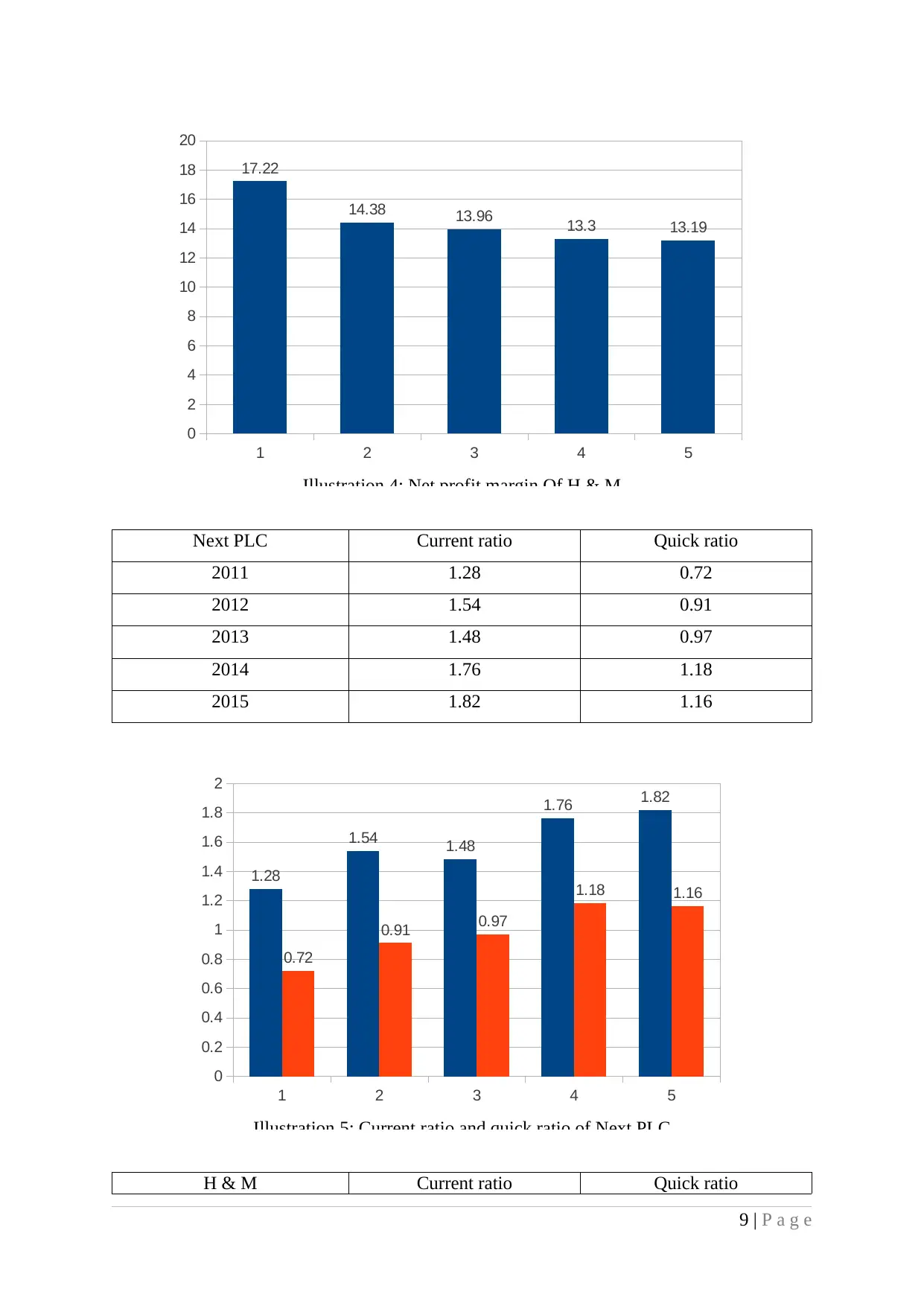

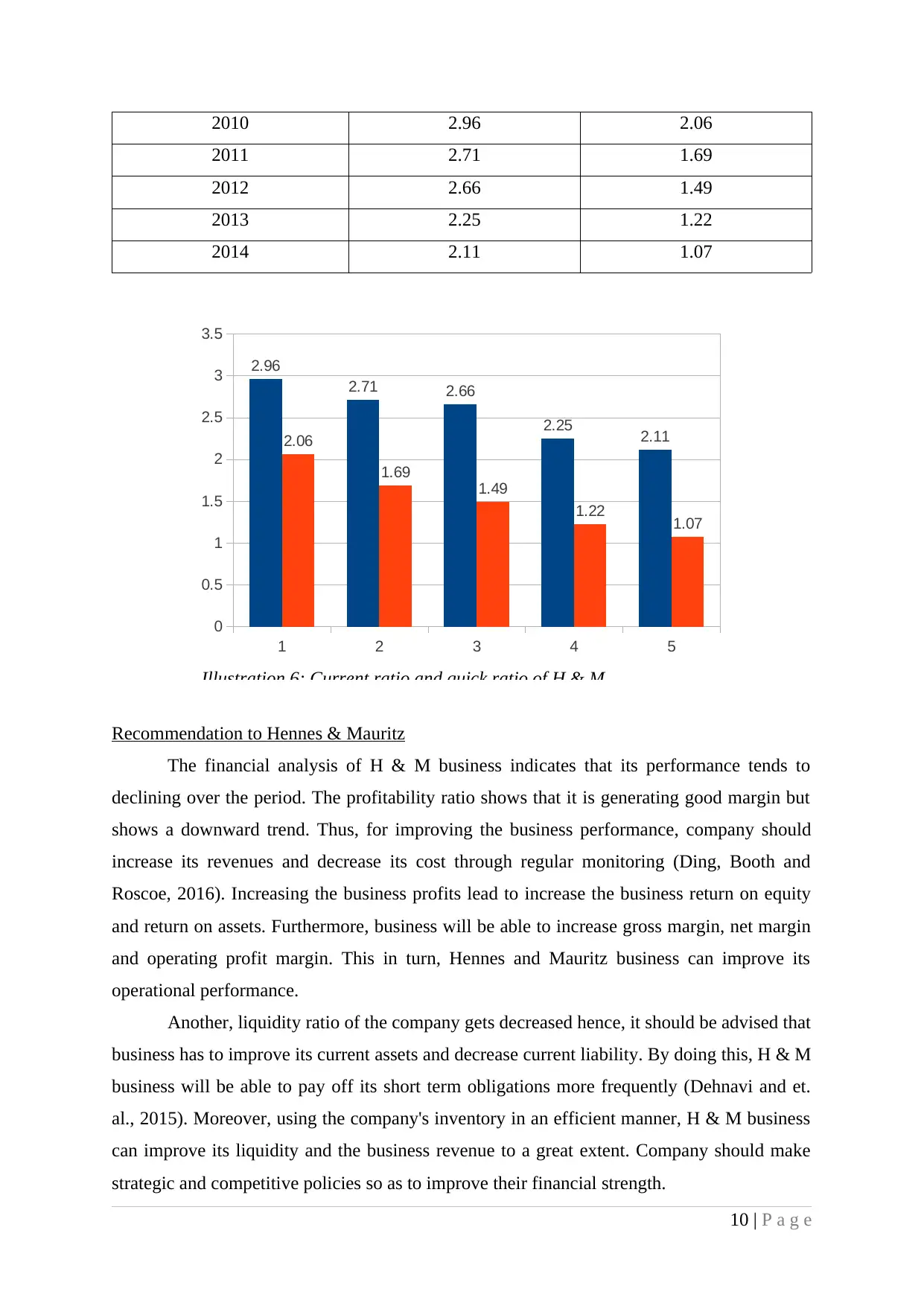

Current ratio: Financial strength can be analysing by comparing the financial ratios.

Current ratios are a measurement of business liquidity and measure business ability to

discharge short term business obligations (Erasmus and et. al., 2016). H & M current ratio get

declined from 2.96 to 2.11 in the year 2014. However, current ratio of Next PLC business

gets increase from 1.28 to 1.82 in the year 2015. It indicates that Next PLC business is

improving its liquidity position to meet its short term liabilities in an effective manner.

Quick ratio: It represents the relationship between quick assets and current liabilities

of the business. The quick ratio of Next PLC business tends to incline from 0.72 to 1.16 in

the year 2015. However, the quick ratio of H & M business gets decreased from 2.06 to 1.07

in the year 2014. It implies that in Next PLC business, the amount of liquid assets get

increase over the period. However, H & M business liquidity position is declining over the

period.

Assets turnover ratio: It measure the business ability to use business assets effectively

and efficiently (Rahman and Ramli, 2016). In Next PLC business, the assets turnover ratio

get decrease from 1.89 to 1.81 while H & M business assets turnover ratio get increase from

1.91 to 2.14 in the year 2014. It represent that H & M business is using its business assets

effectively and efficiently.

Inventory turnover ratio: Next PLC business inventory turnover ratio is 6.62 in the

year 2015 while in H & M business the inventory turnover ratio is 3.46 indicate that Next

PLC is using its inventory efficiently.

Return on assets: H & M Company’s return on assets gets declined from 32.91% to

28.28% in the year 2014. However, in Next PLC business return on assets get increased from

22.55% to 28.68% in the year 2015. It indicates that Next PLC is getting larger the return on

its total assets.

Operating cash flow/Share: In H & M business, the ratio gets declined from 1.20 to

1.25 in the year 2014. However, in case of Next PLC business the ratio tends to increase from

2.49 to 4.86 respectively. It is higher in Next PLC business implies that Asol Ltd. should

invest in Next PLC Company.

Analysing the performance through non financial ratios is explained as under:

Revenue/Employee: It got increased from 114727 to 135729 in next PLC Company.

However, In H & M, the ratio get decreased from 166639 to 138467 respectively.

5 | P a g e

Current ratios are a measurement of business liquidity and measure business ability to

discharge short term business obligations (Erasmus and et. al., 2016). H & M current ratio get

declined from 2.96 to 2.11 in the year 2014. However, current ratio of Next PLC business

gets increase from 1.28 to 1.82 in the year 2015. It indicates that Next PLC business is

improving its liquidity position to meet its short term liabilities in an effective manner.

Quick ratio: It represents the relationship between quick assets and current liabilities

of the business. The quick ratio of Next PLC business tends to incline from 0.72 to 1.16 in

the year 2015. However, the quick ratio of H & M business gets decreased from 2.06 to 1.07

in the year 2014. It implies that in Next PLC business, the amount of liquid assets get

increase over the period. However, H & M business liquidity position is declining over the

period.

Assets turnover ratio: It measure the business ability to use business assets effectively

and efficiently (Rahman and Ramli, 2016). In Next PLC business, the assets turnover ratio

get decrease from 1.89 to 1.81 while H & M business assets turnover ratio get increase from

1.91 to 2.14 in the year 2014. It represent that H & M business is using its business assets

effectively and efficiently.

Inventory turnover ratio: Next PLC business inventory turnover ratio is 6.62 in the

year 2015 while in H & M business the inventory turnover ratio is 3.46 indicate that Next

PLC is using its inventory efficiently.

Return on assets: H & M Company’s return on assets gets declined from 32.91% to

28.28% in the year 2014. However, in Next PLC business return on assets get increased from

22.55% to 28.68% in the year 2015. It indicates that Next PLC is getting larger the return on

its total assets.

Operating cash flow/Share: In H & M business, the ratio gets declined from 1.20 to

1.25 in the year 2014. However, in case of Next PLC business the ratio tends to increase from

2.49 to 4.86 respectively. It is higher in Next PLC business implies that Asol Ltd. should

invest in Next PLC Company.

Analysing the performance through non financial ratios is explained as under:

Revenue/Employee: It got increased from 114727 to 135729 in next PLC Company.

However, In H & M, the ratio get decreased from 166639 to 138467 respectively.

5 | P a g e

EBITDA/Employee: In Hennes & Mauritz company, the ratio was 42580 tends to

declined to 28008 in the year 2014. On contrary, in Next PLC Company, the ratio tends to

increase from 23869 to 31864 respectively.

Thus, on the basis of above comparison, it can be recommended to the CFO that the

firm should make investment in Next Plc business. The reason for this decision is that the

company is growing in the market due to increasing the profitability. Moreover, the company

is strengthening its financial position as its liquidity ratio gets increased. Therefore, company

is more able to pay its short term obligations. Further, the business is earning good rate of

return on equity (Otley and Emmanuel, 2013). Another, both the non financial ratios are

increasing in Next PLC business. Thus, it can be said that investing in Next Plc business will

be more beneficial for Asol ltd.

Preparation of Charts

Charts are prepared here as under

Gross profit Next PLC

2011 29.27

2012 30.38

2013 31.48

2014 33.16

2015 33.59

6 | P a g e

1 2 3 4 5

27

28

29

30

31

32

33

34

29.27

30.38

31.48

33.16

33.59

Illustration 1: Gross profit ratio of Next PLC

declined to 28008 in the year 2014. On contrary, in Next PLC Company, the ratio tends to

increase from 23869 to 31864 respectively.

Thus, on the basis of above comparison, it can be recommended to the CFO that the

firm should make investment in Next Plc business. The reason for this decision is that the

company is growing in the market due to increasing the profitability. Moreover, the company

is strengthening its financial position as its liquidity ratio gets increased. Therefore, company

is more able to pay its short term obligations. Further, the business is earning good rate of

return on equity (Otley and Emmanuel, 2013). Another, both the non financial ratios are

increasing in Next PLC business. Thus, it can be said that investing in Next Plc business will

be more beneficial for Asol ltd.

Preparation of Charts

Charts are prepared here as under

Gross profit Next PLC

2011 29.27

2012 30.38

2013 31.48

2014 33.16

2015 33.59

6 | P a g e

1 2 3 4 5

27

28

29

30

31

32

33

34

29.27

30.38

31.48

33.16

33.59

Illustration 1: Gross profit ratio of Next PLC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Gross profit H & M

2010 62.93

2011 60.13

2012 59.5

2013 59.13

2014 58.81

Net profit Next PLC

2011 11.93

2012 12.62

2013 14.34

2014 14.79

2015 15.87

7 | P a g e

1 2 3 4 5

56

57

58

59

60

61

62

63

64

62.93

60.13

59.5 59.13 58.81

Illustration 2: Gross profit ratio of H & M business

2010 62.93

2011 60.13

2012 59.5

2013 59.13

2014 58.81

Net profit Next PLC

2011 11.93

2012 12.62

2013 14.34

2014 14.79

2015 15.87

7 | P a g e

1 2 3 4 5

56

57

58

59

60

61

62

63

64

62.93

60.13

59.5 59.13 58.81

Illustration 2: Gross profit ratio of H & M business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net profit H & M

2010 17.22

2011 14.38

2012 13.96

2013 13.3

2014 13.19

8 | P a g e

1 2 3 4 5

0

2

4

6

8

10

12

14

16

18

11.93 12.62

14.34 14.79

15.87

Illustration 3: Net profit of Next PLC

2010 17.22

2011 14.38

2012 13.96

2013 13.3

2014 13.19

8 | P a g e

1 2 3 4 5

0

2

4

6

8

10

12

14

16

18

11.93 12.62

14.34 14.79

15.87

Illustration 3: Net profit of Next PLC

Next PLC Current ratio Quick ratio

2011 1.28 0.72

2012 1.54 0.91

2013 1.48 0.97

2014 1.76 1.18

2015 1.82 1.16

H & M Current ratio Quick ratio

9 | P a g e

1 2 3 4 5

0

2

4

6

8

10

12

14

16

18

20

17.22

14.38 13.96 13.3 13.19

Illustration 4: Net profit margin Of H & M

1 2 3 4 5

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

1.28

1.54 1.48

1.76 1.82

0.72

0.91 0.97

1.18 1.16

Illustration 5: Current ratio and quick ratio of Next PLC

2011 1.28 0.72

2012 1.54 0.91

2013 1.48 0.97

2014 1.76 1.18

2015 1.82 1.16

H & M Current ratio Quick ratio

9 | P a g e

1 2 3 4 5

0

2

4

6

8

10

12

14

16

18

20

17.22

14.38 13.96 13.3 13.19

Illustration 4: Net profit margin Of H & M

1 2 3 4 5

0

0.2

0.4

0.6

0.8

1

1.2

1.4

1.6

1.8

2

1.28

1.54 1.48

1.76 1.82

0.72

0.91 0.97

1.18 1.16

Illustration 5: Current ratio and quick ratio of Next PLC

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2010 2.96 2.06

2011 2.71 1.69

2012 2.66 1.49

2013 2.25 1.22

2014 2.11 1.07

Recommendation to Hennes & Mauritz

The financial analysis of H & M business indicates that its performance tends to

declining over the period. The profitability ratio shows that it is generating good margin but

shows a downward trend. Thus, for improving the business performance, company should

increase its revenues and decrease its cost through regular monitoring (Ding, Booth and

Roscoe, 2016). Increasing the business profits lead to increase the business return on equity

and return on assets. Furthermore, business will be able to increase gross margin, net margin

and operating profit margin. This in turn, Hennes and Mauritz business can improve its

operational performance.

Another, liquidity ratio of the company gets decreased hence, it should be advised that

business has to improve its current assets and decrease current liability. By doing this, H & M

business will be able to pay off its short term obligations more frequently (Dehnavi and et.

al., 2015). Moreover, using the company's inventory in an efficient manner, H & M business

can improve its liquidity and the business revenue to a great extent. Company should make

strategic and competitive policies so as to improve their financial strength.

10 | P a g e

1 2 3 4 5

0

0.5

1

1.5

2

2.5

3

3.5

2.96

2.71 2.66

2.25 2.112.06

1.69

1.49

1.22 1.07

Illustration 6: Current ratio and quick ratio of H & M

2011 2.71 1.69

2012 2.66 1.49

2013 2.25 1.22

2014 2.11 1.07

Recommendation to Hennes & Mauritz

The financial analysis of H & M business indicates that its performance tends to

declining over the period. The profitability ratio shows that it is generating good margin but

shows a downward trend. Thus, for improving the business performance, company should

increase its revenues and decrease its cost through regular monitoring (Ding, Booth and

Roscoe, 2016). Increasing the business profits lead to increase the business return on equity

and return on assets. Furthermore, business will be able to increase gross margin, net margin

and operating profit margin. This in turn, Hennes and Mauritz business can improve its

operational performance.

Another, liquidity ratio of the company gets decreased hence, it should be advised that

business has to improve its current assets and decrease current liability. By doing this, H & M

business will be able to pay off its short term obligations more frequently (Dehnavi and et.

al., 2015). Moreover, using the company's inventory in an efficient manner, H & M business

can improve its liquidity and the business revenue to a great extent. Company should make

strategic and competitive policies so as to improve their financial strength.

10 | P a g e

1 2 3 4 5

0

0.5

1

1.5

2

2.5

3

3.5

2.96

2.71 2.66

2.25 2.112.06

1.69

1.49

1.22 1.07

Illustration 6: Current ratio and quick ratio of H & M

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Furthermore, company should increase its non financial ratio through providing better

quality of services to the customers. It helps to increase customer satisfaction level.

Furthermore, providing good monetary benefits and working environment, business will be

able to enhance its employee turnover ratio. This in turn, business can achieve higher the

success and survive for a longer time period.

Limitation of ratio analysis

Although ratio analysis is a best way of analysing the financial performance but still it

has certain limitations. One of the most important limitations is that it analyse the historical

performance of the business hence, cannot be used to measure future business performance.

Another, different business organization use distinct accounting standard and policies to

record business transactions (Ratio analysis: application, Limitations and Dangers-A

perspective, n.d.). Thus, it impairs the comparability between the companies. Furthermore,

some elements of balance sheet recorded at historical cost while income statement elements

are recorded at current cost. In that case, ratio analysis does not provide significant and

meaningful results. In addition to it, different organizations operate with distinct market

environment which is not considered by ratio analysis method. Moreover, in context to

profitability analysis, the inflation rate also impacts business profits which are not considered

by profitability ratios.

CAPITAL INVESTMENT APPRAISAL TECHNIQUES

Hilltop Limited is a medium sized manufacturing company. As per the scenario, there

are two potential and mutually exclusive projects available for the Hilltop Ltd. Each project

consists of purchasing machines with amounted to 120000£. Investment appraisal techniques

help to identify the potential of each investment project so as to select appropriate investment

proposal (Upton and et. al., 2015). The scenario indicates the net profits from both the

projects for upcoming 6 years from 2016 to 2021.

Cash inflow

Cash inflows from both the projects are calculated here as under:

Table 1: Cash inflow from project A

Machine 1 (net

profit) Depreciation Sale of machine

Machine

purchase Cash inflow

40000 33000 73000

40000 33000 73000

40000 33000 21000 -50000 44000

11 | P a g e

quality of services to the customers. It helps to increase customer satisfaction level.

Furthermore, providing good monetary benefits and working environment, business will be

able to enhance its employee turnover ratio. This in turn, business can achieve higher the

success and survive for a longer time period.

Limitation of ratio analysis

Although ratio analysis is a best way of analysing the financial performance but still it

has certain limitations. One of the most important limitations is that it analyse the historical

performance of the business hence, cannot be used to measure future business performance.

Another, different business organization use distinct accounting standard and policies to

record business transactions (Ratio analysis: application, Limitations and Dangers-A

perspective, n.d.). Thus, it impairs the comparability between the companies. Furthermore,

some elements of balance sheet recorded at historical cost while income statement elements

are recorded at current cost. In that case, ratio analysis does not provide significant and

meaningful results. In addition to it, different organizations operate with distinct market

environment which is not considered by ratio analysis method. Moreover, in context to

profitability analysis, the inflation rate also impacts business profits which are not considered

by profitability ratios.

CAPITAL INVESTMENT APPRAISAL TECHNIQUES

Hilltop Limited is a medium sized manufacturing company. As per the scenario, there

are two potential and mutually exclusive projects available for the Hilltop Ltd. Each project

consists of purchasing machines with amounted to 120000£. Investment appraisal techniques

help to identify the potential of each investment project so as to select appropriate investment

proposal (Upton and et. al., 2015). The scenario indicates the net profits from both the

projects for upcoming 6 years from 2016 to 2021.

Cash inflow

Cash inflows from both the projects are calculated here as under:

Table 1: Cash inflow from project A

Machine 1 (net

profit) Depreciation Sale of machine

Machine

purchase Cash inflow

40000 33000 73000

40000 33000 73000

40000 33000 21000 -50000 44000

11 | P a g e

30000 10000 40000

30000 10000 40000

20000 10000 30000

Total = 200000

Table 2: Cash inflow from project B

Year Machine 2 ( net profits) Depreciation Cash inflow

2016 10000 20000 30000

2017 20000 20000 40000

2018 30000 20000 50000

2019 60000 20000 80000

2020 70000 20000 90000

2021 55000 20000 75000

Total 245000

Payback period

The time period required to get back the initial cash outflow of 120000£ will be

known as payback period. The selection criteria on the basis of this method is that the

investment project that has lower the payback period should be prefer by Hilltop Limited

(Götze, Northcott and Schuster, 2015).

Table 3: Payback period of project A

Year Cash inflow Cumulative cash inflow

0 -120000 -120000

2016 73000 -47000

2017 73000 26000

2018 44000 70000

2019 40000 110000

2020 40000 150000

2021 30000 180000

Payback period = 1 year + (47000£/73000£ * 12)

= 1 year + 7.72 months

12 | P a g e

30000 10000 40000

20000 10000 30000

Total = 200000

Table 2: Cash inflow from project B

Year Machine 2 ( net profits) Depreciation Cash inflow

2016 10000 20000 30000

2017 20000 20000 40000

2018 30000 20000 50000

2019 60000 20000 80000

2020 70000 20000 90000

2021 55000 20000 75000

Total 245000

Payback period

The time period required to get back the initial cash outflow of 120000£ will be

known as payback period. The selection criteria on the basis of this method is that the

investment project that has lower the payback period should be prefer by Hilltop Limited

(Götze, Northcott and Schuster, 2015).

Table 3: Payback period of project A

Year Cash inflow Cumulative cash inflow

0 -120000 -120000

2016 73000 -47000

2017 73000 26000

2018 44000 70000

2019 40000 110000

2020 40000 150000

2021 30000 180000

Payback period = 1 year + (47000£/73000£ * 12)

= 1 year + 7.72 months

12 | P a g e

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.