Analysis of Financial Lease Accounting and Impairment Loss

VerifiedAdded on 2023/04/25

|6

|1499

|442

Homework Assignment

AI Summary

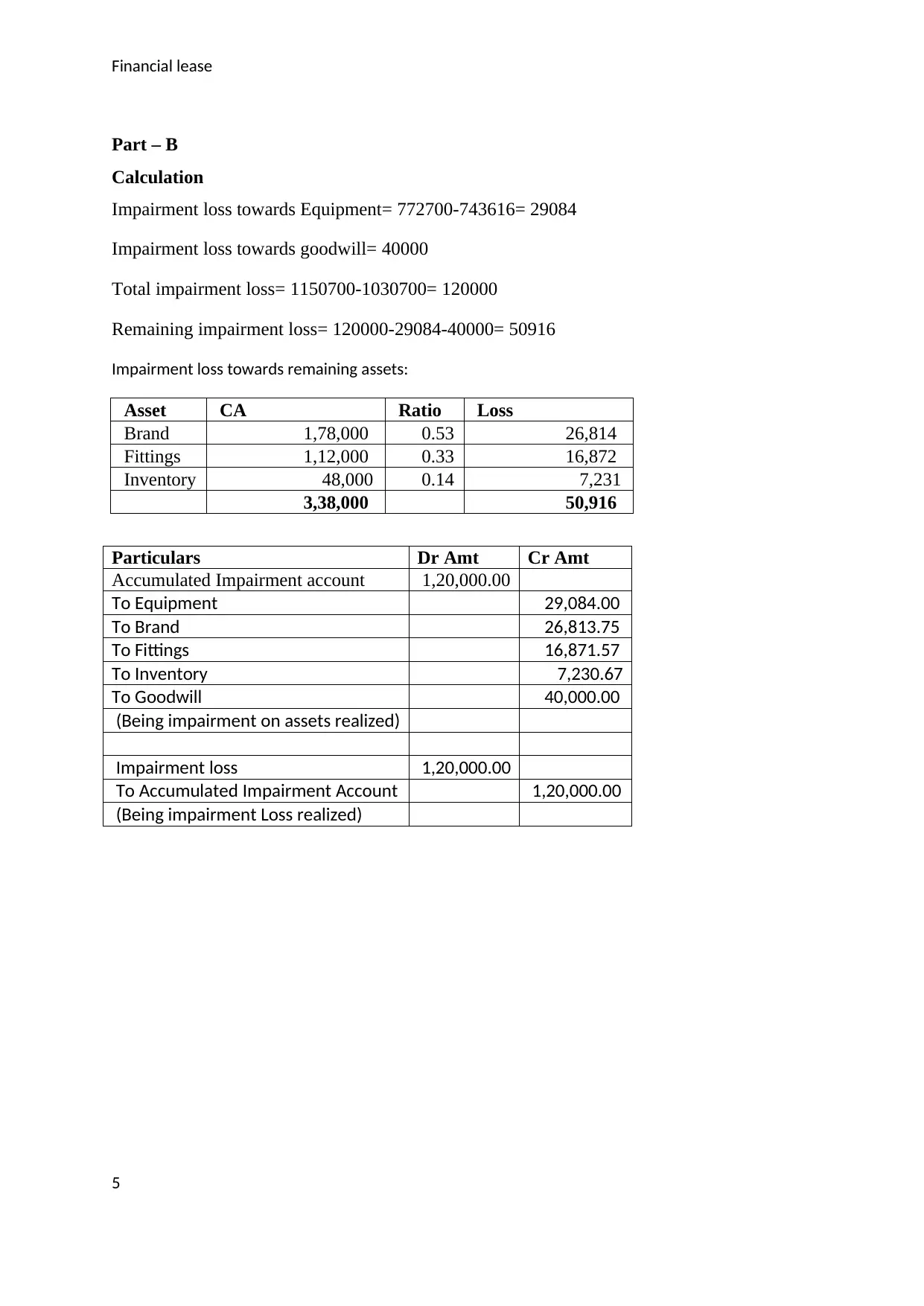

This assignment solution provides a comprehensive analysis of financial lease accounting, focusing on the application of IAS 17 and the accounting treatment of impairment losses. Part A delves into the specifics of financial leases, defining key terms like lessor and lessee, and explaining the historical context of off-balance sheet financing. It elaborates on the accounting procedures for dealer lessors, including the recognition of finance lease receivables, the calculation of present values of minimum lease payments, and the impact on financial statements. Part B presents a practical calculation of impairment loss, detailing the allocation of losses across various assets such as equipment, goodwill, brand, fittings, and inventory. The solution includes journal entries to reflect the impairment loss and provides references to relevant accounting standards and literature. This assignment is a valuable resource for students studying financial accounting, offering a clear understanding of complex lease accounting principles and their practical application.

1 out of 6

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.