Financial Analysis: Case 2 - Leasing Decision and Evaluation

VerifiedAdded on 2022/08/26

|7

|951

|17

Case Study

AI Summary

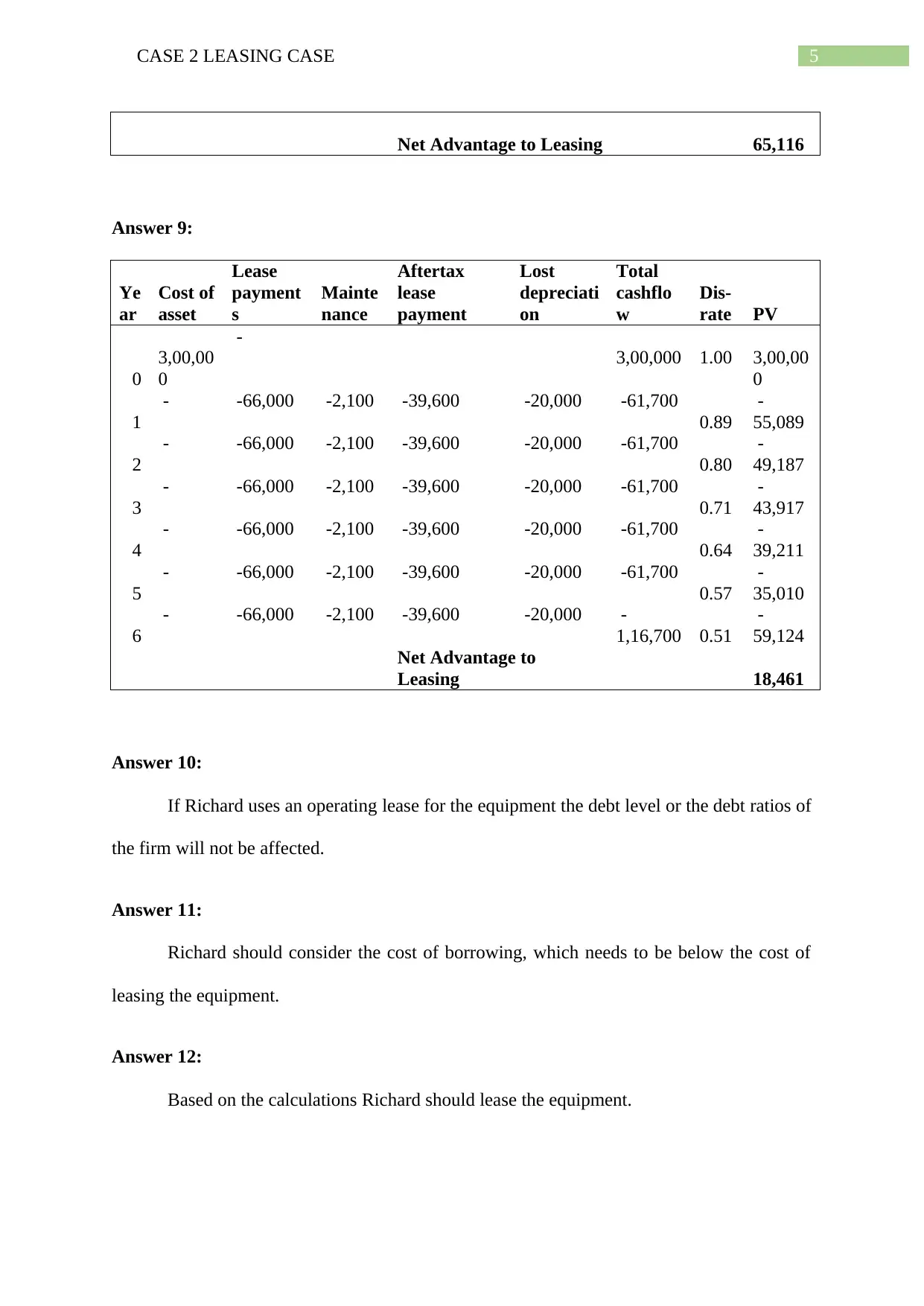

This case study analyzes a leasing scenario involving Richard, a grocery store owner, who needs to replace aging refrigeration units. The assignment explores the differences between financial and operating leases, the advantages and disadvantages of each, and the factors influencing the lease versus buy decision. It involves calculating cash flows, considering tax implications, determining the appropriate discount rate, and evaluating the net advantage to leasing. The analysis determines whether Richard should lease the equipment, considering after-tax lease payments, maintenance costs, and the impact on the company's debt levels. The case provides a detailed financial analysis to guide the decision-making process.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.