Financial Accounting Report: Legal and Regulatory Influences Analysis

VerifiedAdded on 2019/12/04

|8

|1222

|330

Report

AI Summary

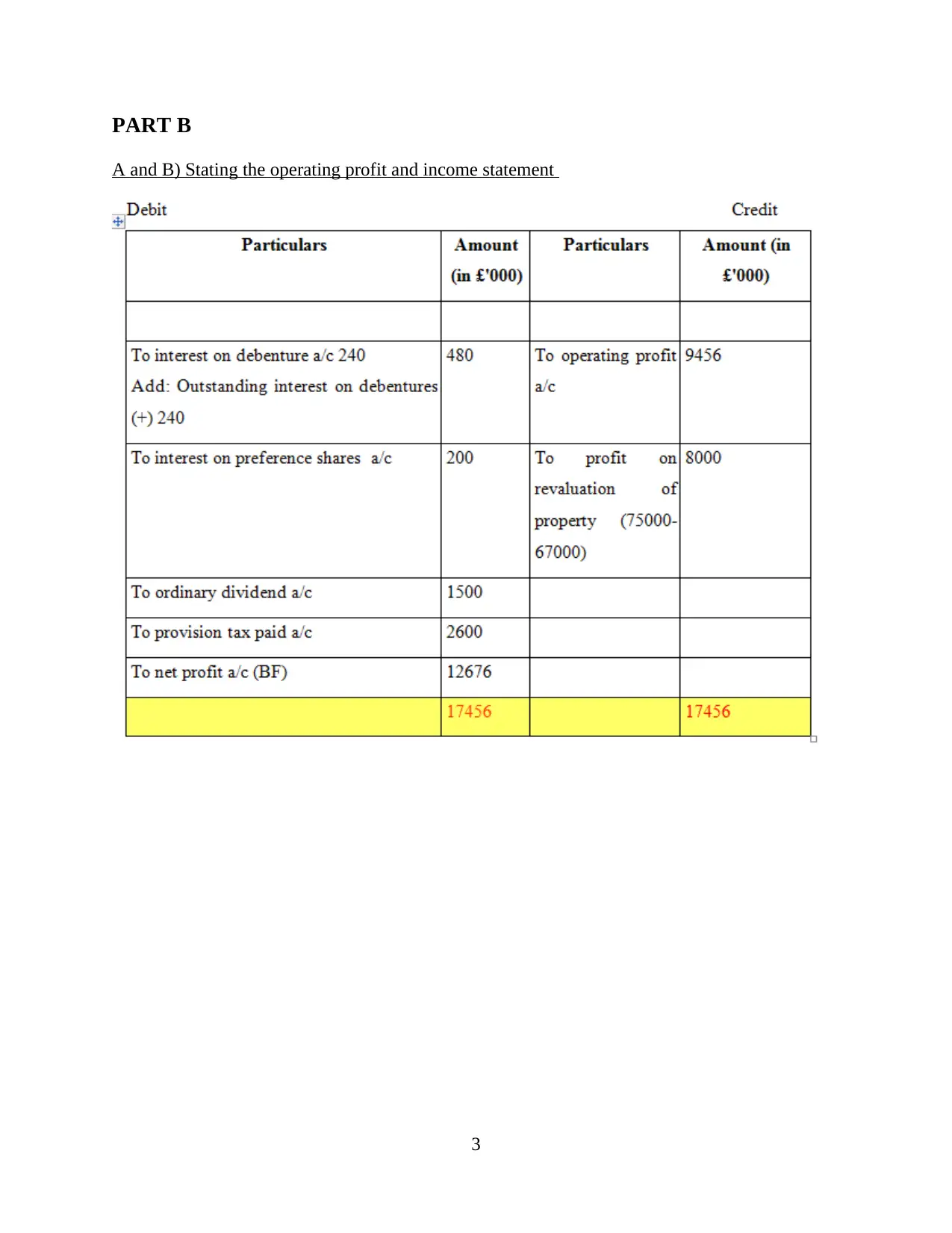

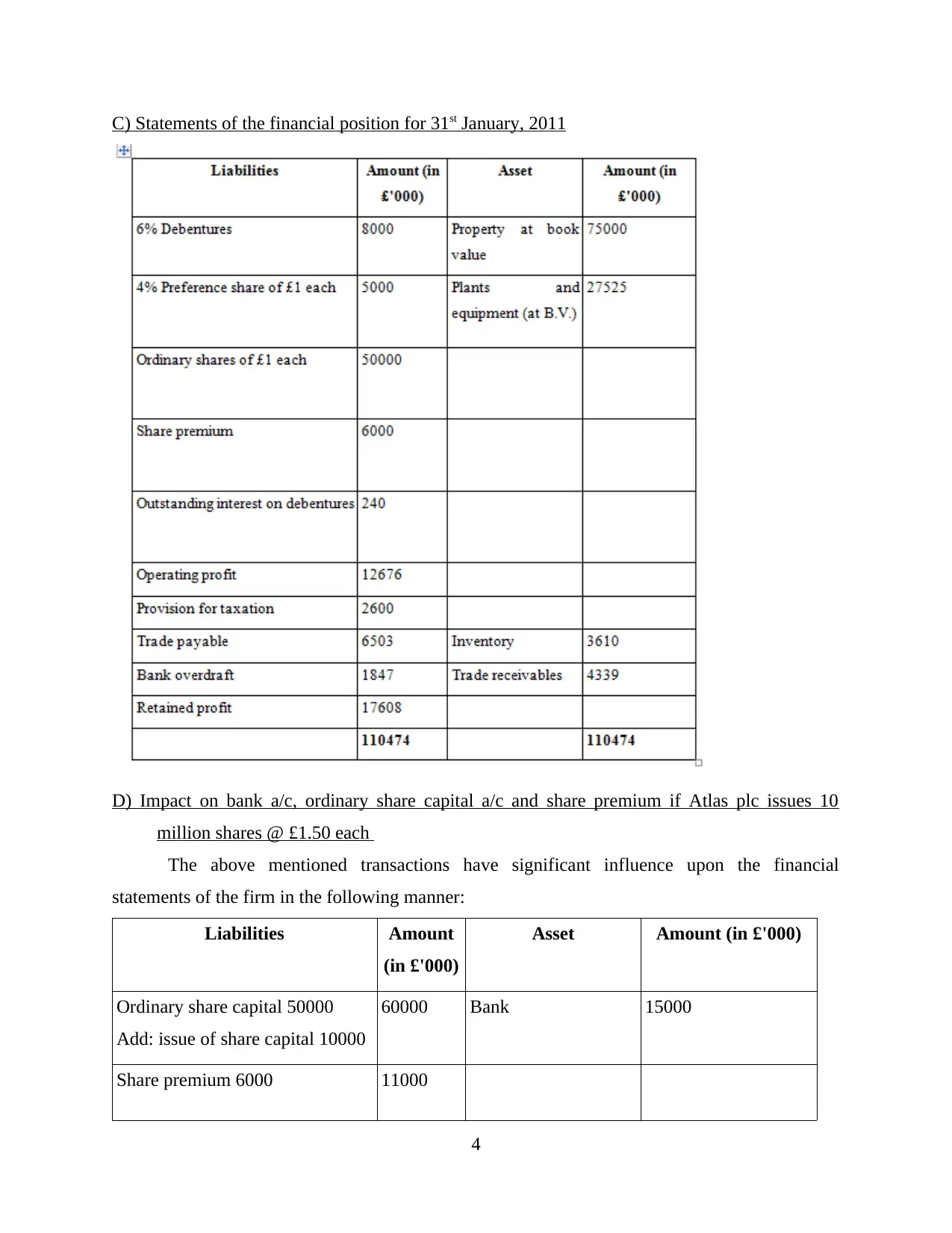

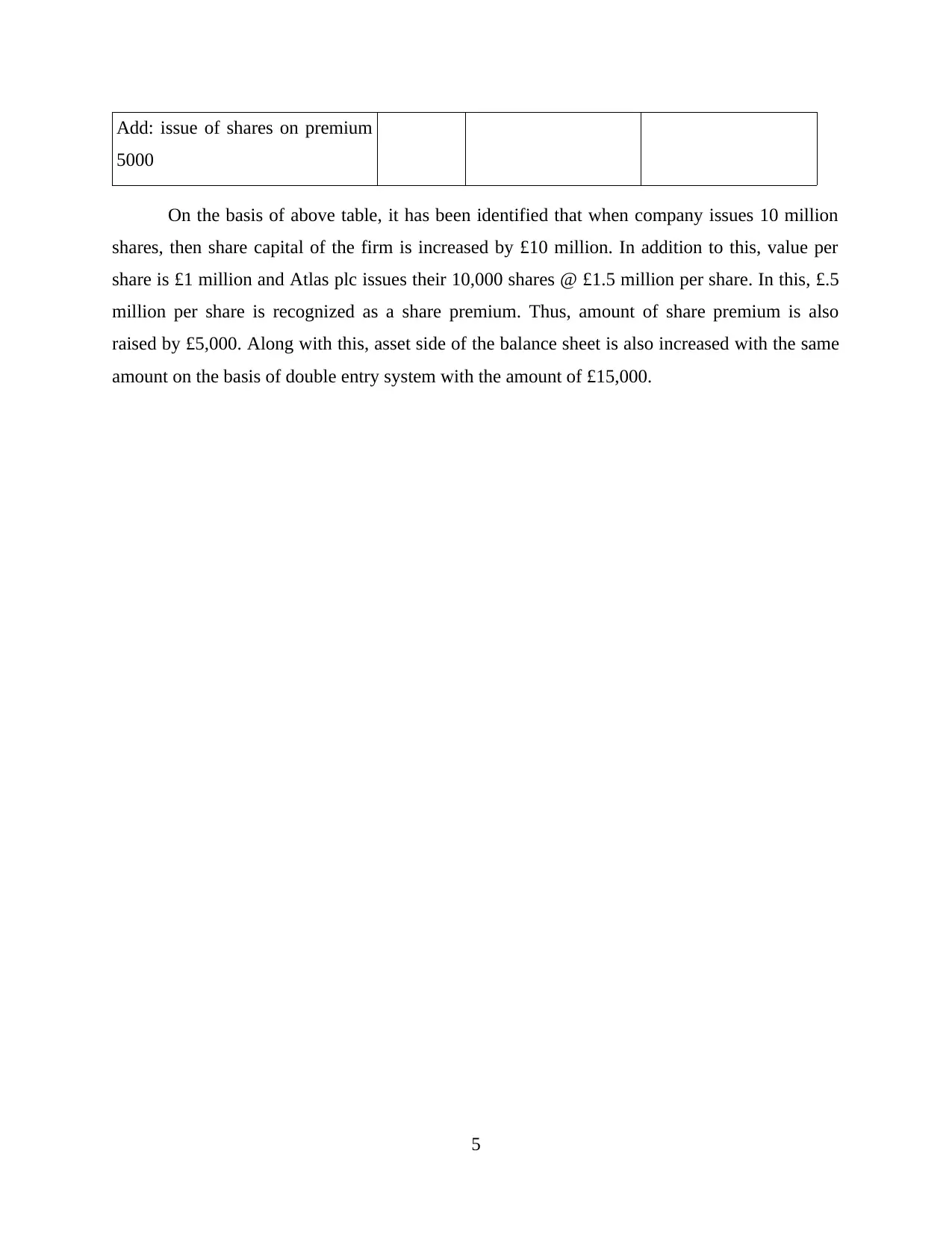

This report delves into the realm of financial accounting, meticulously examining the profound impact of legal and regulatory frameworks on financial statements. It begins by outlining the influences of these frameworks, such as the UK's Company Act 2006 and International Accounting Standards (IAS), on the preparation of financial statements, including the importance of providing information on income, expenses, assets, liabilities, and cash-related activities. The report then assesses the implications of these influences on various users of financial statements, including managers, shareholders, financial institutions, and government entities, highlighting how these stakeholders rely on financial data for decision-making. The analysis extends to specific examples, such as the impact of issuing shares on the balance sheet, and includes financial statements such as operating profit and income statements. The report emphasizes the importance of adhering to accounting principles and providing a fair view of a company's financial position. Finally, the report provides a comprehensive understanding of the interplay between legal requirements and financial reporting practices.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.