TACC401 Report: Financial Analysis of Australian Company Liquidations

VerifiedAdded on 2020/02/24

|10

|2762

|150

Report

AI Summary

This report provides an in-depth analysis of the liquidations of ABC Learning, HIH Insurance, and One.Tel, focusing on the financial and ethical factors that led to their failures. The report examines ABC Learning's collapse due to financial misstatements, including the overvaluation of intangible assets and related-party transactions. It details the downfall of HIH Insurance, highlighting issues such as inadequate provisions for future claims, market misstatements, and the lack of corporate governance. The analysis extends to One.Tel, exploring the impact of wrong pricing policies, strategic mistakes, and poor corporate structure. The study emphasizes that liquidations stem from various causes, including breaches of ethics, legal violations, and ineffective corporate governance, with financial liabilities often being a consequence of these underlying issues. The report concludes by underscoring the importance of robust corporate governance and internal control systems to prevent fraud and ensure sustainable business growth, referencing Australian laws and regulations designed to protect stakeholder interests.

TACC401

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction................................................................................................................................3

Main body..................................................................................................................................3

Liquidation of ABC Learning................................................................................................3

Liquidation of HIH insurance................................................................................................5

Liquidation of One.Tel Phone Company...............................................................................5

Conclusion..................................................................................................................................6

References..................................................................................................................................7

Introduction................................................................................................................................3

Main body..................................................................................................................................3

Liquidation of ABC Learning................................................................................................3

Liquidation of HIH insurance................................................................................................5

Liquidation of One.Tel Phone Company...............................................................................5

Conclusion..................................................................................................................................6

References..................................................................................................................................7

INTRODUCTION

Liquidation can be defined as a situation of winding up of business in which assets are

sold to pay off the remaining obligations. Liquidation can take place voluntarily or

compulsorily as per the conditions of business (Manganelli, Morano, and Tajani, 2014). The

present study is focused on the description of events that led up to liquidation of ABC

Learning, HIH Insurance and One.Tel Phone Company. The financial stress of cited

companies will be supported by the description of ethics and governance.

MAIN BODY

In liquidation, entity winds up, sold its assets and the profits from sales are given to

the creditors or entities having claims on the company. The procedure of liquidations is

mandatory if the wind up takes place as the consequence of an order of the court (Lessambo,

2014). Other are considered as voluntary when the owners or shareholders engaged in

operating the business choose to end operations. The universal reasons of liquidations are

legal problems, insufficient desire, and bankruptcy, between the individuals running the

business to be maintaining it as operating.

In past few years, several liquidations of multinational firms and strengthen business

entities have occurred in Australia. In accordance with the viewpoint of Foreman (2014),

court rules stated that liquidations differ all over the world, but these measures classically

begun by the business itself on behalf of their creditors or shareholders. The party desires to

start the proceeding while making a court filing describing the reason for choosing

liquidations and if the request is accepted by the judge, then the firm must end their

operations and supervisors and are generally agreed by the court to manage their assets sale

(Chow, 2017). Liquidation is not primarily due to financial obligations as it is supported by

various other reasons such as breach of ethical and legal aspects, frauds and inappropriate

business strategies.

Liquidation of ABC Learning

Companies suffer from failure primarily because of financial dispensaries. In

accordance with the ACCC (Australian competition and consumer commission)

representative, ABC’s collapse was not because of increasing competition, but it has been

Liquidation can be defined as a situation of winding up of business in which assets are

sold to pay off the remaining obligations. Liquidation can take place voluntarily or

compulsorily as per the conditions of business (Manganelli, Morano, and Tajani, 2014). The

present study is focused on the description of events that led up to liquidation of ABC

Learning, HIH Insurance and One.Tel Phone Company. The financial stress of cited

companies will be supported by the description of ethics and governance.

MAIN BODY

In liquidation, entity winds up, sold its assets and the profits from sales are given to

the creditors or entities having claims on the company. The procedure of liquidations is

mandatory if the wind up takes place as the consequence of an order of the court (Lessambo,

2014). Other are considered as voluntary when the owners or shareholders engaged in

operating the business choose to end operations. The universal reasons of liquidations are

legal problems, insufficient desire, and bankruptcy, between the individuals running the

business to be maintaining it as operating.

In past few years, several liquidations of multinational firms and strengthen business

entities have occurred in Australia. In accordance with the viewpoint of Foreman (2014),

court rules stated that liquidations differ all over the world, but these measures classically

begun by the business itself on behalf of their creditors or shareholders. The party desires to

start the proceeding while making a court filing describing the reason for choosing

liquidations and if the request is accepted by the judge, then the firm must end their

operations and supervisors and are generally agreed by the court to manage their assets sale

(Chow, 2017). Liquidation is not primarily due to financial obligations as it is supported by

various other reasons such as breach of ethical and legal aspects, frauds and inappropriate

business strategies.

Liquidation of ABC Learning

Companies suffer from failure primarily because of financial dispensaries. In

accordance with the ACCC (Australian competition and consumer commission)

representative, ABC’s collapse was not because of increasing competition, but it has been

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

due to financial misstatements such as high acquisitions and debts. Also, the failure was the

result of financial dispensaries offered by the company (Lewis, 2013).

ABC lost its loyalty and reputation among customers and public at the time of

financial crisis in 2008. The entire world had evidenced the story behind this collapse. The

crises of sub prime lead to self-awareness among various countries regarding the malpractices

been used by companies in the market. ABC’s financial information gave a severe picture

entirely.

The balance sheet of company assets side represented intangible assets of 72% to

81%. These intangible assets were inclusive of several operating licenses. Further, it was a

big concern for government, and they handled this matter to ASIC by setting up a

commission. The commission subjected ASIC failure in this concern to efficiently assess

company’s operating license (Marks, 2015). ABC asserted a big amount of the licenses which

were not even worth in the operating sense of the term. It is because; the high value of

operating licence was set in order to draw traders in the marketplace. The committee asked

ASIC to make consideration of the real value of the operating license and to determine

whether they add any value to the business. The consideration is still in progress, but ASIC

announces that the licences were not 'material to the company’.

The revaluation of operating license was legal in accordance with the accounting

standards in June 2005 for the year ended and after that the new standards of accounting will

be applied. Under the new standard of AASB 138 "Intangible Assets" enables the intangible

assets revaluation only in some situations (Gitman, Juchau and Flanagan, 2015). However,

these standards are only applicable when the treatment of accounting creates a materialistic

impact. ASIC illustrated that at the point of its investigation, the concerns of financial were

not material to the company.

The main component in the downfall of ABC was the existence of transactions of

related parties. Eddy Grooves was involved in the growth and development of the company.

The company was successful in a short term. However, it was stated that Mr Grooves failed

to manage the company (Lessons to be learnt from ABC Learning's collapse, 2009). The

company didn’t follow the framework of business governance rules during the supremacy of

Mr Grooves there were various related party transactions. In 2006, a broking firm named

Austock consisted significant shares by Grooves while entering in transactions with ABC

(Marley and Pedersen, 2015). ABC gave an amount of $27 million to Austock as

result of financial dispensaries offered by the company (Lewis, 2013).

ABC lost its loyalty and reputation among customers and public at the time of

financial crisis in 2008. The entire world had evidenced the story behind this collapse. The

crises of sub prime lead to self-awareness among various countries regarding the malpractices

been used by companies in the market. ABC’s financial information gave a severe picture

entirely.

The balance sheet of company assets side represented intangible assets of 72% to

81%. These intangible assets were inclusive of several operating licenses. Further, it was a

big concern for government, and they handled this matter to ASIC by setting up a

commission. The commission subjected ASIC failure in this concern to efficiently assess

company’s operating license (Marks, 2015). ABC asserted a big amount of the licenses which

were not even worth in the operating sense of the term. It is because; the high value of

operating licence was set in order to draw traders in the marketplace. The committee asked

ASIC to make consideration of the real value of the operating license and to determine

whether they add any value to the business. The consideration is still in progress, but ASIC

announces that the licences were not 'material to the company’.

The revaluation of operating license was legal in accordance with the accounting

standards in June 2005 for the year ended and after that the new standards of accounting will

be applied. Under the new standard of AASB 138 "Intangible Assets" enables the intangible

assets revaluation only in some situations (Gitman, Juchau and Flanagan, 2015). However,

these standards are only applicable when the treatment of accounting creates a materialistic

impact. ASIC illustrated that at the point of its investigation, the concerns of financial were

not material to the company.

The main component in the downfall of ABC was the existence of transactions of

related parties. Eddy Grooves was involved in the growth and development of the company.

The company was successful in a short term. However, it was stated that Mr Grooves failed

to manage the company (Lessons to be learnt from ABC Learning's collapse, 2009). The

company didn’t follow the framework of business governance rules during the supremacy of

Mr Grooves there were various related party transactions. In 2006, a broking firm named

Austock consisted significant shares by Grooves while entering in transactions with ABC

(Marley and Pedersen, 2015). ABC gave an amount of $27 million to Austock as

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

transactional fees. QMS (Queensland Maintenance Services) was underneath the directorship

of Frank Zullo, who was relative (brother-in-law) of Mr Grooves. The company had

compensated the loss of $74 million in exchange for their work centre of ABC. Grooves

owned the team of Brisbane Bullets Basketball team, and it was sponsored by ABC. ABC

declared that the transactions were not material and related to the company and contained no

interest also. However, there was the proof of the weak business measure of the company,

and this considerably weakens the confidence of company’s investors.

Liquidation of HIH insurance

The failure of HIH Insurance in March 2001 trembled the Australian business

community. HIH was world’s second largest employer and at the hindmost part of a major

achievement binge that had observed the company’s major purchases of insurance in New

Zealand, Argentina. In early 2001, the company was suffering from the unstable financial

position and later they suffered the biggest corporate failure in the history of Australia, with a

loss of more than $5bn (Damiani, Bourne and Foo, 2015). With the firm ongoing to act

purely in order to examine old claims without new business taken to abroad, financial

regulators of Australia were placed to identify the clear chain of measures that resulted in

HIH collapse.

There was a proper collapse in the operational area, and the level of the failure was so

high that the charges were taken against the company’s key members like Rodney Adler, Ray

Williams, William Howard and Geoffrey Cohen (Doyle, 2017). Especially, Rodney Adler

was charged on the basis of four particular claim which is fraudulence in the liberty of his

duties and purposely distribution of fake information and data. Adler was found guilty of

deliberately distributing financial data. However, separate calls were made regarding the

queries that the corporate governance systems of HIH were unsuccessful because Adler

misuses his powers and position. In a separate claim, Adler was blamed for influencing HIH

to make an investment of a $2m loan in Business Thinking Systems (BTS). In this

transaction, Adler had an interest in the cited company.

Another main weak point that resulted in the failure of HIH was the lack to offer

future claim in a proper manner, and other problem raised from this single issue. Covering of

future claim is considered to the most significant aspect of any insurance company. However,

by the end of the survival of HIH was in a situation in which just a negative shift of 1.7% will

be sufficient in leading the company into insolvency. The most important reason for this

of Frank Zullo, who was relative (brother-in-law) of Mr Grooves. The company had

compensated the loss of $74 million in exchange for their work centre of ABC. Grooves

owned the team of Brisbane Bullets Basketball team, and it was sponsored by ABC. ABC

declared that the transactions were not material and related to the company and contained no

interest also. However, there was the proof of the weak business measure of the company,

and this considerably weakens the confidence of company’s investors.

Liquidation of HIH insurance

The failure of HIH Insurance in March 2001 trembled the Australian business

community. HIH was world’s second largest employer and at the hindmost part of a major

achievement binge that had observed the company’s major purchases of insurance in New

Zealand, Argentina. In early 2001, the company was suffering from the unstable financial

position and later they suffered the biggest corporate failure in the history of Australia, with a

loss of more than $5bn (Damiani, Bourne and Foo, 2015). With the firm ongoing to act

purely in order to examine old claims without new business taken to abroad, financial

regulators of Australia were placed to identify the clear chain of measures that resulted in

HIH collapse.

There was a proper collapse in the operational area, and the level of the failure was so

high that the charges were taken against the company’s key members like Rodney Adler, Ray

Williams, William Howard and Geoffrey Cohen (Doyle, 2017). Especially, Rodney Adler

was charged on the basis of four particular claim which is fraudulence in the liberty of his

duties and purposely distribution of fake information and data. Adler was found guilty of

deliberately distributing financial data. However, separate calls were made regarding the

queries that the corporate governance systems of HIH were unsuccessful because Adler

misuses his powers and position. In a separate claim, Adler was blamed for influencing HIH

to make an investment of a $2m loan in Business Thinking Systems (BTS). In this

transaction, Adler had an interest in the cited company.

Another main weak point that resulted in the failure of HIH was the lack to offer

future claim in a proper manner, and other problem raised from this single issue. Covering of

future claim is considered to the most significant aspect of any insurance company. However,

by the end of the survival of HIH was in a situation in which just a negative shift of 1.7% will

be sufficient in leading the company into insolvency. The most important reason for this

collapse was misstatements in changing conditions of the market, which extremely enlarged

the liabilities of HIH. These aspects were not compensated by viable strategic planning due to

which changing conditions of markets lead to serious damage in the insurance companies, but

companies are known about these risks, and they do planning in order to reduce the risks.

Furthermore, HIH radically coverage itself was the part to be concerned with the

extreme expansion of the company. HIH got holding of several companies in their ending

year and was building a chief drive for the global expansion. These expansions was a strong

move for business, as it brings increased liabilities and HIH acted on the basis of its belief

that liabilities will be compensated to the expansion. The Company appear to have primarily

misinterpreted the level by which extra provisions were required to be considered as per

changing market conditions.

This was the primary mistake made by the company, as if it deals with at the same

time it could have been resolved. Namely, HIH board went evident while practising this

strategy; it demonstrated that there was downfall of corporate governance at HIH, without

real omission applicable to check either the strategy implemented was appropriate or

financial sustainable

With the collapse of HIH insurance, there were significant changes in regulations

made by Australian Securities and Investments Commission (ASIC) for prevention of similar

issues (Kehl, 2001). For this aspect, a new set of corporate governance rules has been

designed regarding expansion. The company could prevent liquidation if management were

more cautious about liabilities while expansion (Betta, 2016). They were in a position to

introduce cost cutting programs and ignoring decision taken by Rodney Adler of securing

investment on the basis of false statements. Further, they provided a lesson to have effective

market research prior to entering any new market to prevent issues related to

mismanagement.

Liquidation of One.Tel Phone Company

The collapse of One-Tel is considered to significant liquidation case in Australia in

2001 as it was fourth largest telecommunication company with a customer base of two

million in eight countries. The collision of the company was due to wrong pricing policy,

strategic mistakes and unbridled growth. The primary issue with the company was an

inappropriate corporate structure which causes ineffective communication (Adams, 2014).

Their centralization strategy of promoting Yes man by humiliating managers who were

the liabilities of HIH. These aspects were not compensated by viable strategic planning due to

which changing conditions of markets lead to serious damage in the insurance companies, but

companies are known about these risks, and they do planning in order to reduce the risks.

Furthermore, HIH radically coverage itself was the part to be concerned with the

extreme expansion of the company. HIH got holding of several companies in their ending

year and was building a chief drive for the global expansion. These expansions was a strong

move for business, as it brings increased liabilities and HIH acted on the basis of its belief

that liabilities will be compensated to the expansion. The Company appear to have primarily

misinterpreted the level by which extra provisions were required to be considered as per

changing market conditions.

This was the primary mistake made by the company, as if it deals with at the same

time it could have been resolved. Namely, HIH board went evident while practising this

strategy; it demonstrated that there was downfall of corporate governance at HIH, without

real omission applicable to check either the strategy implemented was appropriate or

financial sustainable

With the collapse of HIH insurance, there were significant changes in regulations

made by Australian Securities and Investments Commission (ASIC) for prevention of similar

issues (Kehl, 2001). For this aspect, a new set of corporate governance rules has been

designed regarding expansion. The company could prevent liquidation if management were

more cautious about liabilities while expansion (Betta, 2016). They were in a position to

introduce cost cutting programs and ignoring decision taken by Rodney Adler of securing

investment on the basis of false statements. Further, they provided a lesson to have effective

market research prior to entering any new market to prevent issues related to

mismanagement.

Liquidation of One.Tel Phone Company

The collapse of One-Tel is considered to significant liquidation case in Australia in

2001 as it was fourth largest telecommunication company with a customer base of two

million in eight countries. The collision of the company was due to wrong pricing policy,

strategic mistakes and unbridled growth. The primary issue with the company was an

inappropriate corporate structure which causes ineffective communication (Adams, 2014).

Their centralization strategy of promoting Yes man by humiliating managers who were

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

showcasing problems had increased employee turnover. Management of company was too

autocratic, and opinions of employees were ignored which had raised the issue of

understaffing and consequently customers satisfaction was affected. These issues had wasted

technology and created financial issues for business.

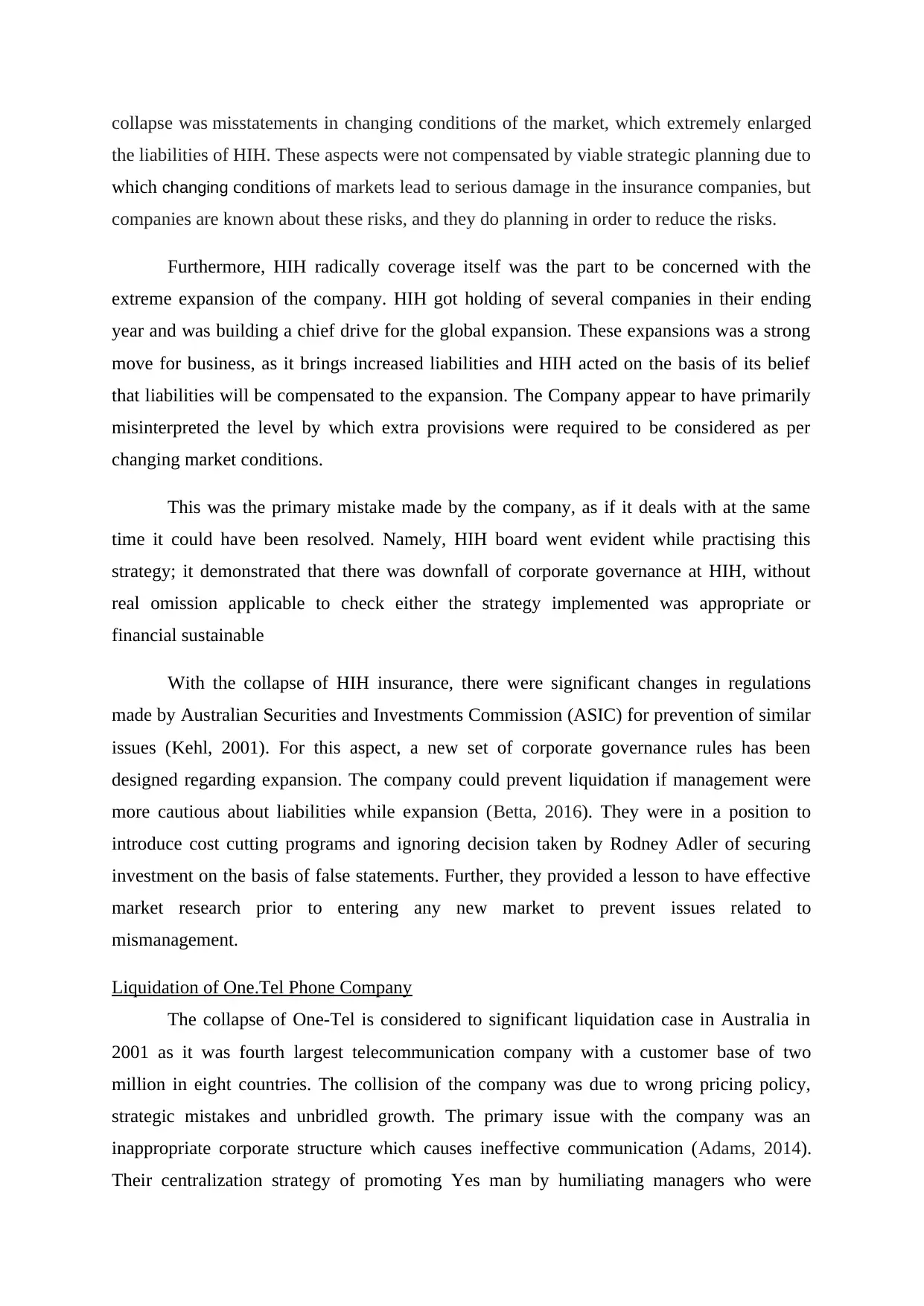

Figure 1: Key performance indicators of One-Tel

By considering financial figures of commendable company growth in sales and

customers based can be noticed, but same has not been translated into increased profitability.

All financial issues primarily arise due to corporate governance issues such as inappropriate

managerial authorities; unclear allocation of responsibilities, ineffective internal control and

increasing work issues (Debbage and Dickinson, 2013). In One-Tel there was a major breach

of corporate governance such as non-compliance of law related to fiduciary duties of

directors. For example, Adler contravened directorial duties sec 181, 182 and 183 as loans

were raised without considering the interest of shareholders as it was not in good faith. Mark

Silberman fail to supervise business activities and misled the board in terms of actual cash

flow (Avison and Wilson, 2002).

Liquidation of the company shows that it is not sufficient for companies to attain large

scale customers until they made a contribution towards profitability of the firm. Further,

implementation of highly competitive price strategy merely to gain market share can cause

disastrous consequences, and sales revenues must be supported by cash collection strategies

else there will be a liquidity crisis.

CONCLUSION

By considering the present study, it can be concluded that primary reason of

liquidation is not financial liabilities as it is supported by various other reasons such as breach

of ethical and legal aspects, frauds and inappropriate business strategies. It is because,

financial obligations are a consequence of inappropriate business strategies, contravention of

autocratic, and opinions of employees were ignored which had raised the issue of

understaffing and consequently customers satisfaction was affected. These issues had wasted

technology and created financial issues for business.

Figure 1: Key performance indicators of One-Tel

By considering financial figures of commendable company growth in sales and

customers based can be noticed, but same has not been translated into increased profitability.

All financial issues primarily arise due to corporate governance issues such as inappropriate

managerial authorities; unclear allocation of responsibilities, ineffective internal control and

increasing work issues (Debbage and Dickinson, 2013). In One-Tel there was a major breach

of corporate governance such as non-compliance of law related to fiduciary duties of

directors. For example, Adler contravened directorial duties sec 181, 182 and 183 as loans

were raised without considering the interest of shareholders as it was not in good faith. Mark

Silberman fail to supervise business activities and misled the board in terms of actual cash

flow (Avison and Wilson, 2002).

Liquidation of the company shows that it is not sufficient for companies to attain large

scale customers until they made a contribution towards profitability of the firm. Further,

implementation of highly competitive price strategy merely to gain market share can cause

disastrous consequences, and sales revenues must be supported by cash collection strategies

else there will be a liquidity crisis.

CONCLUSION

By considering the present study, it can be concluded that primary reason of

liquidation is not financial liabilities as it is supported by various other reasons such as breach

of ethical and legal aspects, frauds and inappropriate business strategies. It is because,

financial obligations are a consequence of inappropriate business strategies, contravention of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ethical aspect and laws and ineffective corporate governance. To prevent this, laws of

Australia has been stricken to ensure corporate governance and protect the interest of

stakeholders. Further, companies have mandatory obligations to comply with developed laws

else they have to face severe adverse consequences such as penalties and compulsory

liquidation. However, the interest of stakeholders and economy will be cushioned by

imposing a penalty on individual who is liable for misconduct. The study also shows that for

sustainable growth and success it is essential to have effective corporate governance and

internal control system to prevent frauds in business. In addition to this, managerial

authorities should focus on long term sustainability instead of having short term profits.

Australia has been stricken to ensure corporate governance and protect the interest of

stakeholders. Further, companies have mandatory obligations to comply with developed laws

else they have to face severe adverse consequences such as penalties and compulsory

liquidation. However, the interest of stakeholders and economy will be cushioned by

imposing a penalty on individual who is liable for misconduct. The study also shows that for

sustainable growth and success it is essential to have effective corporate governance and

internal control system to prevent frauds in business. In addition to this, managerial

authorities should focus on long term sustainability instead of having short term profits.

REFERENCES

Adams, M.A., 2014. Faulty lines in corporate law: issues for insurance policies. Governance

Directions, 66(8), p.504.

Betta, M., 2016. Three Case Studies: Australian HIH, American Enron, and Global Lehman

Brothers. In Ethicmentality-Ethics in Capitalist Economy, Business, and Society (pp. 79-97).

Springer Netherlands.

Chow, J.C., 2017. ANALYSIS OF FINANCIAL CREDIT RISK USING MACHINE

LEARNING.

Damiani, C., Bourne, N. and Foo, M., 2015. The HIH claims support scheme. Economic

Round-up, (1), p.37.

Debbage, S. and Dickinson, S., 2013. The rationale for the prudential regulation and

supervision of insurers.

Doyle, M., 2017. Market-based indirect causation after HIH. Australian Resources and

Energy Law Journal, 35(3), p.205.

Foreman, R., 2014. Insolvency: It's a wind-up. Law Society Journal: the official journal of

the Law Society of New South Wales, 52(1), p.71.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Lessambo, F.I., 2014. Corporate Governance, Accounting and Auditing Scandals. In The

International Corporate Governance System (pp. 244-263). Palgrave Macmillan UK.

Lewis, G., 2013. Australia's regulatory panopticon. AQ-Australian Quarterly, 84(4), p.26.

Manganelli, B.E.N.E.D.E.T.T.O., Morano, P.I.E.R.L.U.I.G.I. and Tajani,

F.R.A.N.C.E.S.C.O., 2014. Companies in liquidation. a model for the assessment of the value

of used machinery. WSEAS Trans. Bus. Econ, 11, pp.683-691.

Marks, R.E., 2015. Learning Lessons: The Global Financial Crisis in Retrospect.

Adams, M.A., 2014. Faulty lines in corporate law: issues for insurance policies. Governance

Directions, 66(8), p.504.

Betta, M., 2016. Three Case Studies: Australian HIH, American Enron, and Global Lehman

Brothers. In Ethicmentality-Ethics in Capitalist Economy, Business, and Society (pp. 79-97).

Springer Netherlands.

Chow, J.C., 2017. ANALYSIS OF FINANCIAL CREDIT RISK USING MACHINE

LEARNING.

Damiani, C., Bourne, N. and Foo, M., 2015. The HIH claims support scheme. Economic

Round-up, (1), p.37.

Debbage, S. and Dickinson, S., 2013. The rationale for the prudential regulation and

supervision of insurers.

Doyle, M., 2017. Market-based indirect causation after HIH. Australian Resources and

Energy Law Journal, 35(3), p.205.

Foreman, R., 2014. Insolvency: It's a wind-up. Law Society Journal: the official journal of

the Law Society of New South Wales, 52(1), p.71.

Gitman, L.J., Juchau, R. and Flanagan, J., 2015. Principles of managerial finance. Pearson

Higher Education AU.

Lessambo, F.I., 2014. Corporate Governance, Accounting and Auditing Scandals. In The

International Corporate Governance System (pp. 244-263). Palgrave Macmillan UK.

Lewis, G., 2013. Australia's regulatory panopticon. AQ-Australian Quarterly, 84(4), p.26.

Manganelli, B.E.N.E.D.E.T.T.O., Morano, P.I.E.R.L.U.I.G.I. and Tajani,

F.R.A.N.C.E.S.C.O., 2014. Companies in liquidation. a model for the assessment of the value

of used machinery. WSEAS Trans. Bus. Econ, 11, pp.683-691.

Marks, R.E., 2015. Learning Lessons: The Global Financial Crisis in Retrospect.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Marley, S. and Pedersen, J., 2015. Accounting for Business: An Introduction. Pearson Higher

Education AU.

Sirtes, G., Lo Surdo, A. and White, R., 2016. Corporations law and class actions: Court

recognises indirect or market-based causation in shareholder claims. LSJ: Law Society of

NSW Journal, (23), p.80.

Online

Avison, D. and Wilson, D., 2002. IT FAILURE AND THE COLLAPSE OF ONE.TEL. [PDF].

Available through < https://link.springer.com/content/pdf/10.1007/978-0-387-35604-

4_3.pdf>. [Accessed on 29th August 2017].

Kehl, D., 2001. HIH Insurance Group Collapse. [Online]. Available through <

http://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Librar

y/Publications_Archive/archive/hihinsurance>. [Accessed on 29th August 2017].

Lessons to be learnt from ABC Learning's collapse. 2009. [Online]. Available through <

http://www.smh.com.au/business/lessons-to-be-learnt-from-abc-learnings-collapse-

20090101-78f8.html>. [Accessed on 29th August 2017].

Education AU.

Sirtes, G., Lo Surdo, A. and White, R., 2016. Corporations law and class actions: Court

recognises indirect or market-based causation in shareholder claims. LSJ: Law Society of

NSW Journal, (23), p.80.

Online

Avison, D. and Wilson, D., 2002. IT FAILURE AND THE COLLAPSE OF ONE.TEL. [PDF].

Available through < https://link.springer.com/content/pdf/10.1007/978-0-387-35604-

4_3.pdf>. [Accessed on 29th August 2017].

Kehl, D., 2001. HIH Insurance Group Collapse. [Online]. Available through <

http://www.aph.gov.au/About_Parliament/Parliamentary_Departments/Parliamentary_Librar

y/Publications_Archive/archive/hihinsurance>. [Accessed on 29th August 2017].

Lessons to be learnt from ABC Learning's collapse. 2009. [Online]. Available through <

http://www.smh.com.au/business/lessons-to-be-learnt-from-abc-learnings-collapse-

20090101-78f8.html>. [Accessed on 29th August 2017].

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.