Management Accounting Report: Costing Methods and Systems

VerifiedAdded on 2021/02/20

|19

|3705

|28

Report

AI Summary

This report on management accounting explores its significance in business operations, using Brightstar and Hawthorn International as examples. It is divided into four tasks. Task 1 defines management accounting and its types, emphasizing its role in decision-making and its distinction from financial accounting. Task 2 details costing techniques like absorption and marginal costing for income statement preparation. Task 3 examines planning tools and their merits/demerits, while Task 4 discusses how businesses use management accounting to address financial problems. The report covers various cost accounting systems, inventory management, and pricing optimization, highlighting their benefits and the importance of reliable information. Different types of managerial accounting reports, including budget, accounts receivable aging, performance, and inventory reports, are also discussed. Additionally, it covers costing methods like marginal costing, absorption costing, and activity-based costing, alongside valuation methods like LIFO, FIFO, and weighted average. The report concludes by emphasizing the importance of management accounting in enhancing profitability and operational efficiency.

Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................1

TASK 1 ....................................................................................................................................1

P1.Management accounting and its various types:......................................................................1

P2.Different methods for management accounting reporting: ....................................................2

TASK 2 ..........................................................................................................................................5

P3.Costing Techniques to prepare income statements:................................................................5

TASK 3............................................................................................................................................9

P4 Merit and demerit of planning tools:......................................................................................9

TASK 4..........................................................................................................................................13

P5 the way in which business entities are using management accounting systems to respond

financial problems......................................................................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION...........................................................................................................................1

TASK 1 ....................................................................................................................................1

P1.Management accounting and its various types:......................................................................1

P2.Different methods for management accounting reporting: ....................................................2

TASK 2 ..........................................................................................................................................5

P3.Costing Techniques to prepare income statements:................................................................5

TASK 3............................................................................................................................................9

P4 Merit and demerit of planning tools:......................................................................................9

TASK 4..........................................................................................................................................13

P5 the way in which business entities are using management accounting systems to respond

financial problems......................................................................................................................13

CONCLUSION..............................................................................................................................16

REFERENCES..............................................................................................................................17

INTRODUCTION

In any business environment, management accounting system shall be considered as a

important aspects for functioning of business operations effectively and efficiently. Management

accounting system plays a important role because it acts as a link between finance operations and

other functions of a business organisation. By applying various management accounting

techniques such as budgetary tools, cost accounting, job costing, an organisation can identify its

core weaknesses and it may leads to enhancing profitability in long run. For better understanding

of management accounting, Brightstar is chosen which is engaged in providing financial

consultancy services to manufacturing firms and other companies. Hawthorn International is

also considered which is UK based manufacturing company. This report is divided into four

tasks, in which task one defines about the MA and MAS and its various types. Task two provides

the details about the two techniques for calculating the income statements which is absorption

costing and marginal costing. Task three mentioned different planning tools which are used in

management accounting whereas, task four includes ways in which an company may use such

system to respond to financial problems.

TASK 1

P1.Management accounting and its various types:

Management accounting refers to the process of preparing management reports and

related accounts that give correct and timely financial and statistical information required by

managers for its day to day decisions.

Management accounting system may be defined as a method that provides financial

information to the management for reporting purposes. It is deployed to provide information that

management can use to make good decisions. Such system includes various accounting

techniques such as cost volume profit (CVP) analysis, budgetary control, cash budget, marginal

costing and so on.

Importance to integrate this system within an organisation includes various aspects

such as assist companies by providing quantitative and qualitative information financial

performance, continuous improvement for its business operations, and assist in cost

management. The benefits from implementing such system is that it assist in increasing the

In any business environment, management accounting system shall be considered as a

important aspects for functioning of business operations effectively and efficiently. Management

accounting system plays a important role because it acts as a link between finance operations and

other functions of a business organisation. By applying various management accounting

techniques such as budgetary tools, cost accounting, job costing, an organisation can identify its

core weaknesses and it may leads to enhancing profitability in long run. For better understanding

of management accounting, Brightstar is chosen which is engaged in providing financial

consultancy services to manufacturing firms and other companies. Hawthorn International is

also considered which is UK based manufacturing company. This report is divided into four

tasks, in which task one defines about the MA and MAS and its various types. Task two provides

the details about the two techniques for calculating the income statements which is absorption

costing and marginal costing. Task three mentioned different planning tools which are used in

management accounting whereas, task four includes ways in which an company may use such

system to respond to financial problems.

TASK 1

P1.Management accounting and its various types:

Management accounting refers to the process of preparing management reports and

related accounts that give correct and timely financial and statistical information required by

managers for its day to day decisions.

Management accounting system may be defined as a method that provides financial

information to the management for reporting purposes. It is deployed to provide information that

management can use to make good decisions. Such system includes various accounting

techniques such as cost volume profit (CVP) analysis, budgetary control, cash budget, marginal

costing and so on.

Importance to integrate this system within an organisation includes various aspects

such as assist companies by providing quantitative and qualitative information financial

performance, continuous improvement for its business operations, and assist in cost

management. The benefits from implementing such system is that it assist in increasing the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

PDCA cycle efficiency almost 50%. It means that foremost importance of this integration is to

increase the work efficiency of the management management accounting provides quantitative

and qualitative information on operational and financial matters. Management accounting system

is used by the owners, mangers and working staff which uses it to control and plan operations

and assist in taking effective decision making (Serena Chiucchi, 2013).

Origin, Role and Principles of management accounting: It is originated from financial

accounting, but it is very different from financial accounting. It is originated during the 1900's

but at that time more focus was placed on financial accounting. Its main role is to serve the core

needs of internal management. It includes principle of causality and principle of analogy. These

principles helps the company in improving its overall business operations that helps in enhancing

the profitability of the company which is the ultimate goal of an entity.

Distinction between management accounting and financial accounting:

Basis Management accounting Financial accounting

Information mainly for For Internal use For External use

Purpose of information To aid planning, controlling

and decision making

To record financial

performance in a period

Legal requirements None To record the financial

transactions and prepared the

financial statements.

P2.Different methods for management accounting reporting:

In management accounting system, there are different methods which may be used for

reporting purposes by the company which are as follows:

Cost accounting systems: It is a system used by firms to estimate overall cost of their

product and thereafter compare with actual figures for profitability evaluation. This may

assist the company like Hawthorn International in identify the products which are not

profitable for the company in terms cost involved.

Inventory management systems: This is very useful for the companies in manufacturing

sector to have such inventory management system. Because it helps the Hawthorn

International in tracking inventory, orders, sales and deliveries and also useful in

increase the work efficiency of the management management accounting provides quantitative

and qualitative information on operational and financial matters. Management accounting system

is used by the owners, mangers and working staff which uses it to control and plan operations

and assist in taking effective decision making (Serena Chiucchi, 2013).

Origin, Role and Principles of management accounting: It is originated from financial

accounting, but it is very different from financial accounting. It is originated during the 1900's

but at that time more focus was placed on financial accounting. Its main role is to serve the core

needs of internal management. It includes principle of causality and principle of analogy. These

principles helps the company in improving its overall business operations that helps in enhancing

the profitability of the company which is the ultimate goal of an entity.

Distinction between management accounting and financial accounting:

Basis Management accounting Financial accounting

Information mainly for For Internal use For External use

Purpose of information To aid planning, controlling

and decision making

To record financial

performance in a period

Legal requirements None To record the financial

transactions and prepared the

financial statements.

P2.Different methods for management accounting reporting:

In management accounting system, there are different methods which may be used for

reporting purposes by the company which are as follows:

Cost accounting systems: It is a system used by firms to estimate overall cost of their

product and thereafter compare with actual figures for profitability evaluation. This may

assist the company like Hawthorn International in identify the products which are not

profitable for the company in terms cost involved.

Inventory management systems: This is very useful for the companies in manufacturing

sector to have such inventory management system. Because it helps the Hawthorn

International in tracking inventory, orders, sales and deliveries and also useful in

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

production related documents (Lindholm, Laine and Suomala, 2017). Due to this,

company' cost in maintaining its inventory related cost gets reduced by implementing this

system.

Job- costing systems: It includes that system which provides the process of gathering

information about the costs which is associated with a specific production or service job.

This provides details about the workers performance regarding a specific job.

Price optimisation systems: This is a type of a tools which helps the company like

Hawthorn International in fixing the prices of a particular product. It also help in

determining the customer's response in case of different prices of a product set by the

company.

Benefits of different types of systems:

By using these systems which have tremendous effect on the functioning of a company in

a positive manner. There are various benefits of using these systems as discussed as above:

Particulars Benefits

Cost accounting Systems It has tremendous benefits as it gives an

opportunity to Hawthorn International in

estimating its product's cost accurately. It helps

company in raising the required money in

advance for future operations.

Inventory management systems It provides benefits to the company in

controlling and reducing its inventory related

cost.

Job costing Systems It provides the Hawthorn International proper

information about each job task which is

performed by a specific worker.

Price optimisation systems It helps the Hawthorn International in

determining the correct price of its products

based on pricing strategy.

Characteristics of good information:

company' cost in maintaining its inventory related cost gets reduced by implementing this

system.

Job- costing systems: It includes that system which provides the process of gathering

information about the costs which is associated with a specific production or service job.

This provides details about the workers performance regarding a specific job.

Price optimisation systems: This is a type of a tools which helps the company like

Hawthorn International in fixing the prices of a particular product. It also help in

determining the customer's response in case of different prices of a product set by the

company.

Benefits of different types of systems:

By using these systems which have tremendous effect on the functioning of a company in

a positive manner. There are various benefits of using these systems as discussed as above:

Particulars Benefits

Cost accounting Systems It has tremendous benefits as it gives an

opportunity to Hawthorn International in

estimating its product's cost accurately. It helps

company in raising the required money in

advance for future operations.

Inventory management systems It provides benefits to the company in

controlling and reducing its inventory related

cost.

Job costing Systems It provides the Hawthorn International proper

information about each job task which is

performed by a specific worker.

Price optimisation systems It helps the Hawthorn International in

determining the correct price of its products

based on pricing strategy.

Characteristics of good information:

In any companies in manufacturing sector like Hawthorn International, Information is to

be considered as an important and essential resources, because profitability of company depends

upon a reliable information. Business organisation needs to control and monitor the process of

creation such information within the organisation. Some of the characteristics of information are

as follows:

Reliability: It is a measure of failure or success of using information for decision-making.

If information leads to correct decision on many occasions, than it is said that information

is correct.

Accuracy: Information provided should be accurate in itself because only right

information can be used in decision making process. Therefore Hawthorn International

shall considered this fact while creating and communicating of information.

Up to date: The information should be refreshed from time to time as it usually rots with

time and usage. In case of communication of information which is outdated may lead to

conflict and loss of profitability in a manufacturing organisation such as Hawthorn

International.

Reasons for presentation of information shall be understandable:

It is necessary to present the information in legible and understandable way because if

information is not presented in accurate way then it can not be useful for any one in the

organisation (Stechemesser and Guenther, 2012).

Different types of managerial accounting reports:

Budget Report: This report helps the companies like Hawthorn International to evaluate

its performance which may lead to control the cost. The estimated budget for the period is

generally based on the actual expenses of previous years. It can be use as providing

incentives to the employees if they meet the specific budget criteria.

Accounts receivable ageing reports: It is a critical tool for managing cash flow for the

companies that sells goods on credit to its customers. It helps the management in finding

the issues with company's collections process.

Performance report: It provides management with a report which assist the company like

Hawthorn International in evaluating its employee's performance. If there is positive

changes in the performance of the employees then company shall required to give

incentives to the employees for future survival and profitability of company.

be considered as an important and essential resources, because profitability of company depends

upon a reliable information. Business organisation needs to control and monitor the process of

creation such information within the organisation. Some of the characteristics of information are

as follows:

Reliability: It is a measure of failure or success of using information for decision-making.

If information leads to correct decision on many occasions, than it is said that information

is correct.

Accuracy: Information provided should be accurate in itself because only right

information can be used in decision making process. Therefore Hawthorn International

shall considered this fact while creating and communicating of information.

Up to date: The information should be refreshed from time to time as it usually rots with

time and usage. In case of communication of information which is outdated may lead to

conflict and loss of profitability in a manufacturing organisation such as Hawthorn

International.

Reasons for presentation of information shall be understandable:

It is necessary to present the information in legible and understandable way because if

information is not presented in accurate way then it can not be useful for any one in the

organisation (Stechemesser and Guenther, 2012).

Different types of managerial accounting reports:

Budget Report: This report helps the companies like Hawthorn International to evaluate

its performance which may lead to control the cost. The estimated budget for the period is

generally based on the actual expenses of previous years. It can be use as providing

incentives to the employees if they meet the specific budget criteria.

Accounts receivable ageing reports: It is a critical tool for managing cash flow for the

companies that sells goods on credit to its customers. It helps the management in finding

the issues with company's collections process.

Performance report: It provides management with a report which assist the company like

Hawthorn International in evaluating its employee's performance. If there is positive

changes in the performance of the employees then company shall required to give

incentives to the employees for future survival and profitability of company.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Inventory Report: This report may be made by the company for its physical inventory

which lead to providing more efficient process for production system. A company like

Hawthorn International may compare the different assembly lines within the company for

evaluating the best performing production line (McVay, Kennedy and Fullerton, 2016).

TASK 2

P3.Costing Techniques to prepare income statements:

The term cost can be defined as amount of money which occur in process of

manufacturing of any kind of product. Under this cost various kind of expenses are included and

it plays an important role in order to set the price at an effective level. There are a wide range of

costs which occur in companies operations and activities. Some of them are mentioned below

which are as follows such as:

Fixed cost: It is a periodic cost that remains same irrespective of the output level or sales

revenue. Fixed cost are recovered by the organisation by different recovery rates such as

labour recovery rates, material recovery rates and so on.

Variable cost: a variable cost is the cost which changes with the changes in the output or

sales volume of an company.

Direct Cost: A direct cost is a that can be completely occurred related to production of a

particular goods or services. Such cost includes material cost, direct labour expenses and

so on.

Indirect cost: Indirect costs are costs that are not directly attributable to a specific

production of goods and services such as depreciation, administration expenses and so

on.

Cost volume profit: This may be defined as a kind of method which is used by companies in

order to assess the variation in cost and volume that can impact to revenues. The above

Hawthorn international company is using this technique to evaluate the change in cost and

volume.

Flexible budgeting: This is being used by Hawthorn International for future period level of

operation which are not fix. Therefore, as name suggest, this budget is prepared for more than

one level of operation.

which lead to providing more efficient process for production system. A company like

Hawthorn International may compare the different assembly lines within the company for

evaluating the best performing production line (McVay, Kennedy and Fullerton, 2016).

TASK 2

P3.Costing Techniques to prepare income statements:

The term cost can be defined as amount of money which occur in process of

manufacturing of any kind of product. Under this cost various kind of expenses are included and

it plays an important role in order to set the price at an effective level. There are a wide range of

costs which occur in companies operations and activities. Some of them are mentioned below

which are as follows such as:

Fixed cost: It is a periodic cost that remains same irrespective of the output level or sales

revenue. Fixed cost are recovered by the organisation by different recovery rates such as

labour recovery rates, material recovery rates and so on.

Variable cost: a variable cost is the cost which changes with the changes in the output or

sales volume of an company.

Direct Cost: A direct cost is a that can be completely occurred related to production of a

particular goods or services. Such cost includes material cost, direct labour expenses and

so on.

Indirect cost: Indirect costs are costs that are not directly attributable to a specific

production of goods and services such as depreciation, administration expenses and so

on.

Cost volume profit: This may be defined as a kind of method which is used by companies in

order to assess the variation in cost and volume that can impact to revenues. The above

Hawthorn international company is using this technique to evaluate the change in cost and

volume.

Flexible budgeting: This is being used by Hawthorn International for future period level of

operation which are not fix. Therefore, as name suggest, this budget is prepared for more than

one level of operation.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost variances: It refers to the differences among the actual costs of an organisation like

Hawthorn International with its estimated the standard figures.

Marginal Costing: Marginal costing is the technique of cost accounting in which only relevant

cost is to be considered i.e. the cost which is to be responsible for manufacturing of a product).

Absorption costing: It is a technique of management cost accounting in which company like

Hawthorn International also consider the fixed cost or historical cost. It is considered when

entity's has an existing product.

Cost allocation: It means determining and assigning the cost to various products in an

organization. Hawthorn International used this in order to effective allocation of expenditures in

particular activities seprately (Schaltegger, 2012).

Normal costing: This can be defined as a kind of costing method by which companies can

compute total cost of a produced product. Under above company, they are using this costing

method for assessing actual cost.

Activity based costing: It is an method of allocating the fixed cost based on the activities which

are most utilised by the different activities.

Standard costing: This is the system of cost accounting in which company like Hawthorn

International uses the standard cost in which it is compares with actual figures.

Valuation methods:

LIFO: Under it, stock which is first purchased are utilises first in production system.

FIFO: Under it, stock which is last purchased are utilises first in production system

irrespective of purchase order.

Weighted average: Under it, inventories are valued as per weighted average cost of

available stock of inventory.

Overhead: It is an expense which are occurred indirectly and can not be identified in a particular

product's cost. Such as in above Hawthorn international company some types of overhead like

rent, salaries which are not linked with any specific product.

Income statement under Marginal costing technique for month of May

Heads amount amount

sales revenue 15000

less: Cost of production

opening stock 0

Add: Cost of production 8000

less: closing inventories 3200

Hawthorn International with its estimated the standard figures.

Marginal Costing: Marginal costing is the technique of cost accounting in which only relevant

cost is to be considered i.e. the cost which is to be responsible for manufacturing of a product).

Absorption costing: It is a technique of management cost accounting in which company like

Hawthorn International also consider the fixed cost or historical cost. It is considered when

entity's has an existing product.

Cost allocation: It means determining and assigning the cost to various products in an

organization. Hawthorn International used this in order to effective allocation of expenditures in

particular activities seprately (Schaltegger, 2012).

Normal costing: This can be defined as a kind of costing method by which companies can

compute total cost of a produced product. Under above company, they are using this costing

method for assessing actual cost.

Activity based costing: It is an method of allocating the fixed cost based on the activities which

are most utilised by the different activities.

Standard costing: This is the system of cost accounting in which company like Hawthorn

International uses the standard cost in which it is compares with actual figures.

Valuation methods:

LIFO: Under it, stock which is first purchased are utilises first in production system.

FIFO: Under it, stock which is last purchased are utilises first in production system

irrespective of purchase order.

Weighted average: Under it, inventories are valued as per weighted average cost of

available stock of inventory.

Overhead: It is an expense which are occurred indirectly and can not be identified in a particular

product's cost. Such as in above Hawthorn international company some types of overhead like

rent, salaries which are not linked with any specific product.

Income statement under Marginal costing technique for month of May

Heads amount amount

sales revenue 15000

less: Cost of production

opening stock 0

Add: Cost of production 8000

less: closing inventories 3200

total cost of production 4800

contribution 10200

less: Fixed costs

production overheads 4000

selling costs 4000

administration overheads 2000

sales commission 750 10750

profit -550

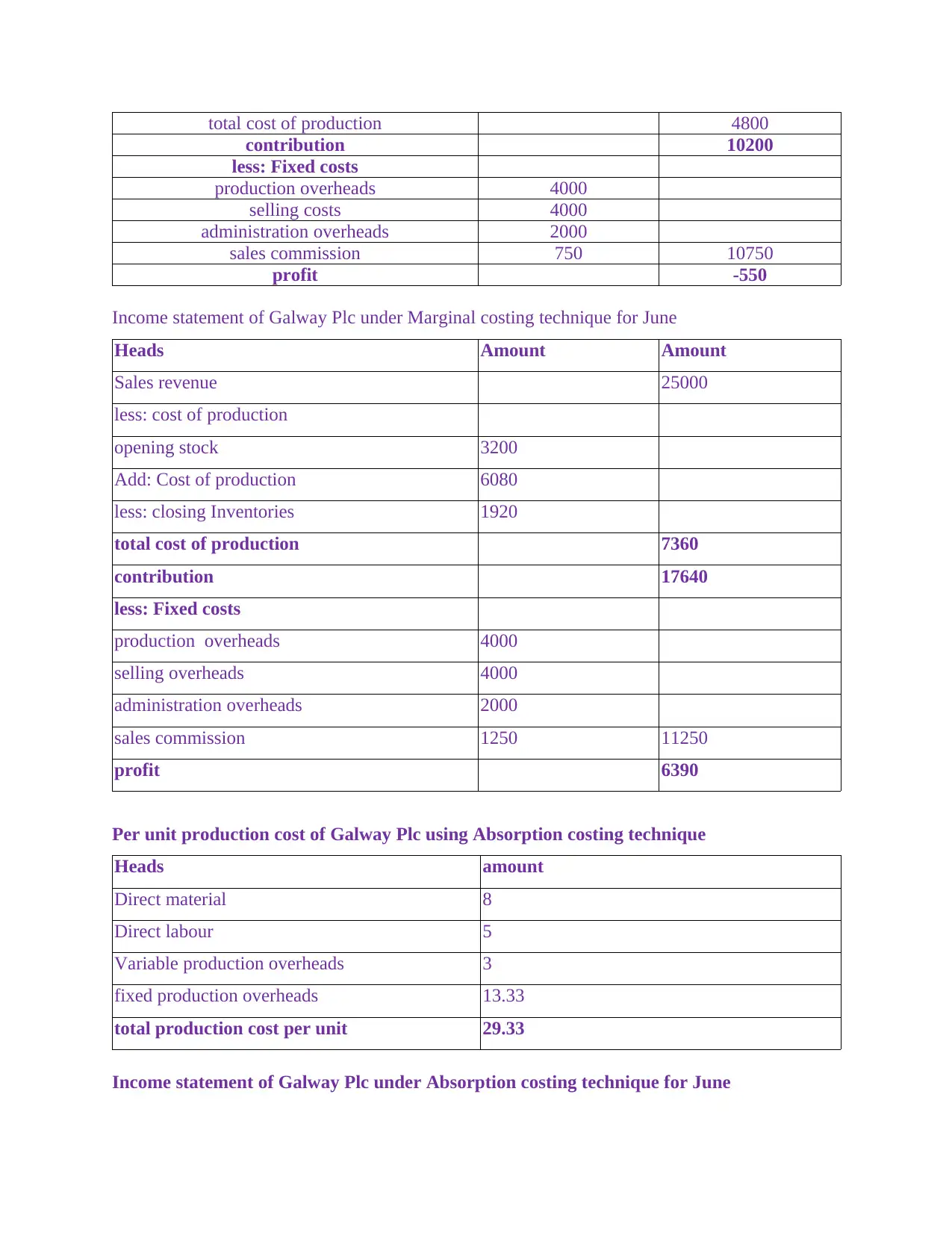

Income statement of Galway Plc under Marginal costing technique for June

Heads Amount Amount

Sales revenue 25000

less: cost of production

opening stock 3200

Add: Cost of production 6080

less: closing Inventories 1920

total cost of production 7360

contribution 17640

less: Fixed costs

production overheads 4000

selling overheads 4000

administration overheads 2000

sales commission 1250 11250

profit 6390

Per unit production cost of Galway Plc using Absorption costing technique

Heads amount

Direct material 8

Direct labour 5

Variable production overheads 3

fixed production overheads 13.33

total production cost per unit 29.33

Income statement of Galway Plc under Absorption costing technique for June

contribution 10200

less: Fixed costs

production overheads 4000

selling costs 4000

administration overheads 2000

sales commission 750 10750

profit -550

Income statement of Galway Plc under Marginal costing technique for June

Heads Amount Amount

Sales revenue 25000

less: cost of production

opening stock 3200

Add: Cost of production 6080

less: closing Inventories 1920

total cost of production 7360

contribution 17640

less: Fixed costs

production overheads 4000

selling overheads 4000

administration overheads 2000

sales commission 1250 11250

profit 6390

Per unit production cost of Galway Plc using Absorption costing technique

Heads amount

Direct material 8

Direct labour 5

Variable production overheads 3

fixed production overheads 13.33

total production cost per unit 29.33

Income statement of Galway Plc under Absorption costing technique for June

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

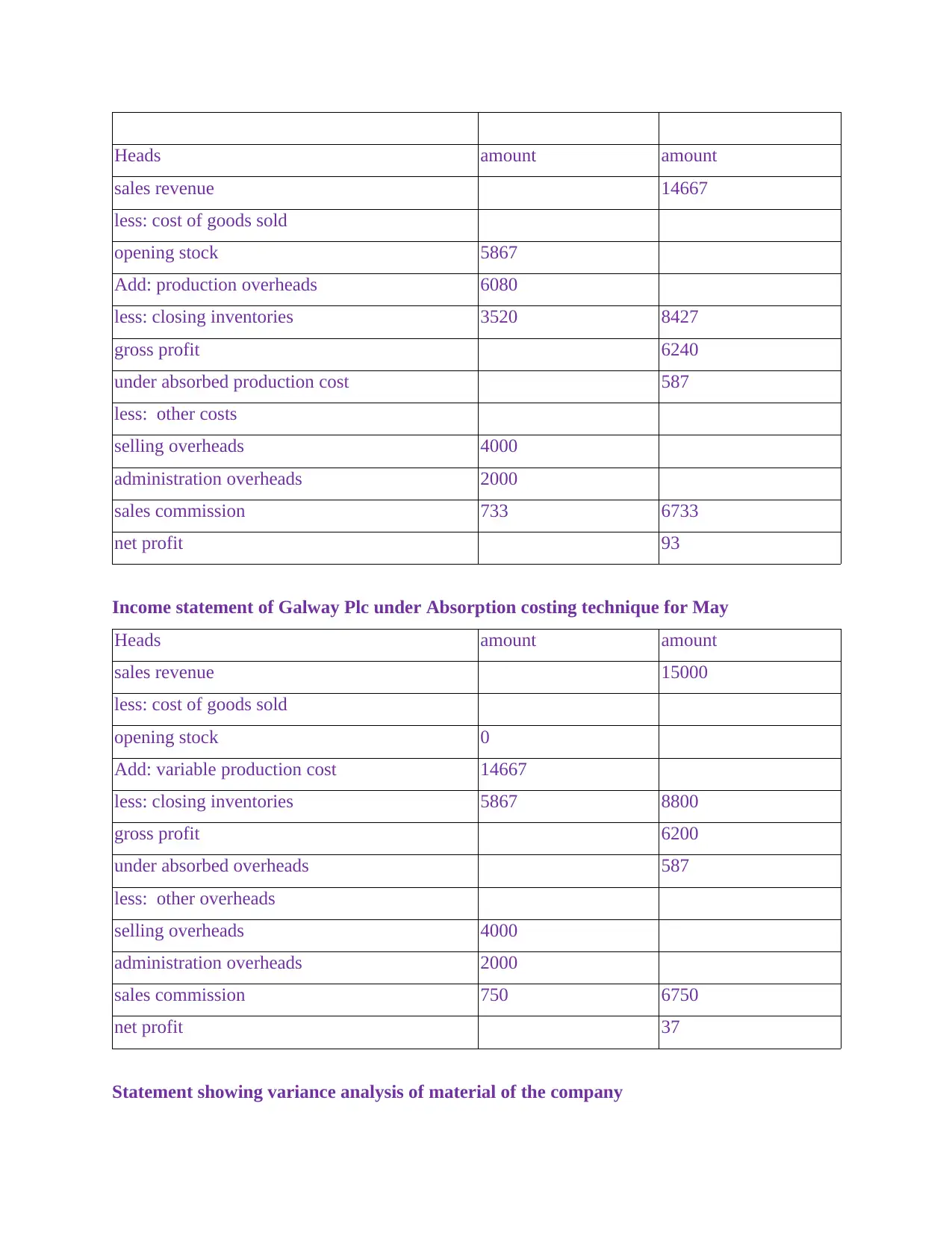

Heads amount amount

sales revenue 14667

less: cost of goods sold

opening stock 5867

Add: production overheads 6080

less: closing inventories 3520 8427

gross profit 6240

under absorbed production cost 587

less: other costs

selling overheads 4000

administration overheads 2000

sales commission 733 6733

net profit 93

Income statement of Galway Plc under Absorption costing technique for May

Heads amount amount

sales revenue 15000

less: cost of goods sold

opening stock 0

Add: variable production cost 14667

less: closing inventories 5867 8800

gross profit 6200

under absorbed overheads 587

less: other overheads

selling overheads 4000

administration overheads 2000

sales commission 750 6750

net profit 37

Statement showing variance analysis of material of the company

sales revenue 14667

less: cost of goods sold

opening stock 5867

Add: production overheads 6080

less: closing inventories 3520 8427

gross profit 6240

under absorbed production cost 587

less: other costs

selling overheads 4000

administration overheads 2000

sales commission 733 6733

net profit 93

Income statement of Galway Plc under Absorption costing technique for May

Heads amount amount

sales revenue 15000

less: cost of goods sold

opening stock 0

Add: variable production cost 14667

less: closing inventories 5867 8800

gross profit 6200

under absorbed overheads 587

less: other overheads

selling overheads 4000

administration overheads 2000

sales commission 750 6750

net profit 37

Statement showing variance analysis of material of the company

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

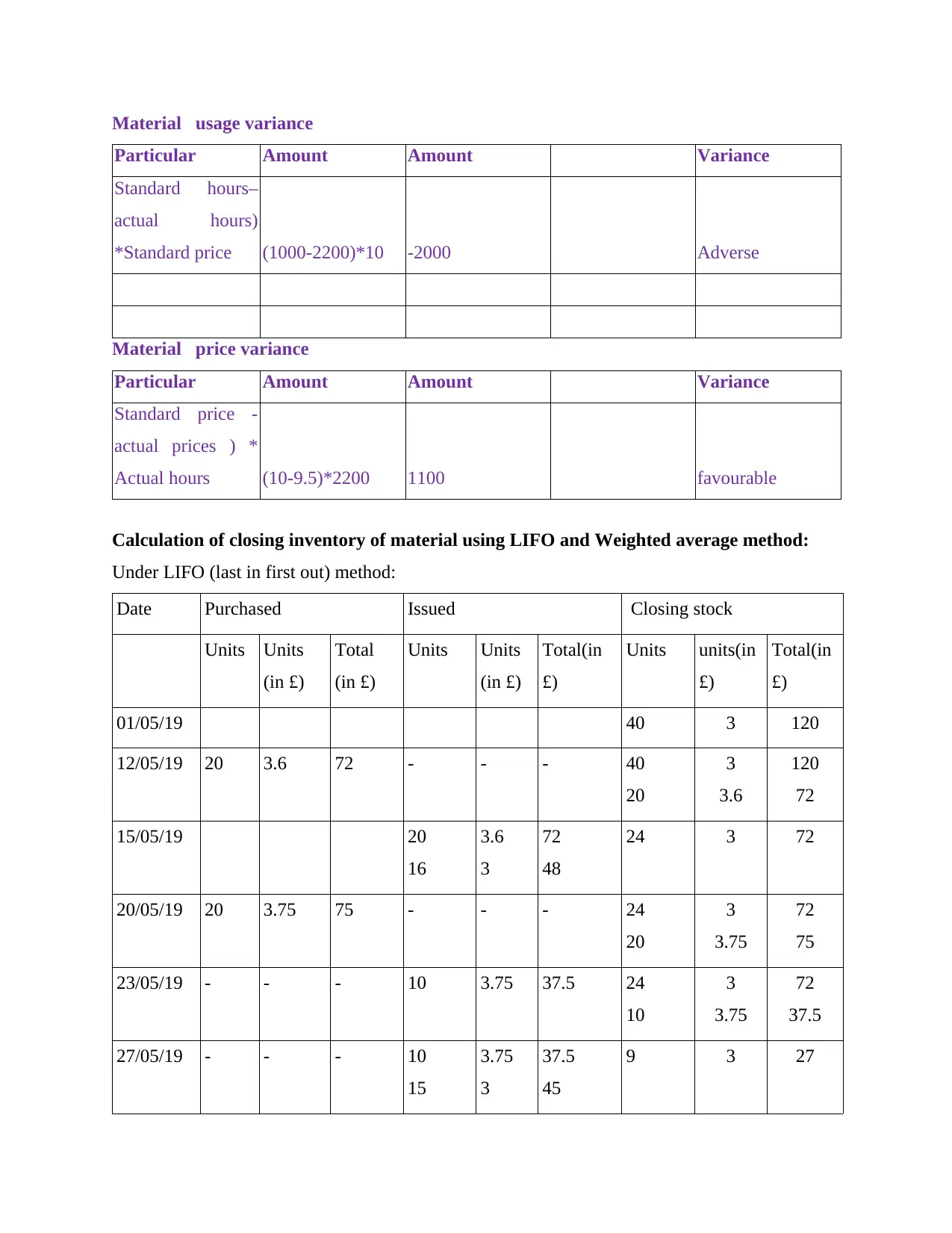

Material usage variance

Particular Amount Amount Variance

Standard hours–

actual hours)

*Standard price (1000-2200)*10 -2000 Adverse

Material price variance

Particular Amount Amount Variance

Standard price -

actual prices ) *

Actual hours (10-9.5)*2200 1100 favourable

Calculation of closing inventory of material using LIFO and Weighted average method:

Under LIFO (last in first out) method:

Date Purchased Issued Closing stock

Units Units

(in £)

Total

(in £)

Units Units

(in £)

Total(in

£)

Units units(in

£)

Total(in

£)

01/05/19 40 3 120

12/05/19 20 3.6 72 - - - 40

20

3

3.6

120

72

15/05/19 20

16

3.6

3

72

48

24 3 72

20/05/19 20 3.75 75 - - - 24

20

3

3.75

72

75

23/05/19 - - - 10 3.75 37.5 24

10

3

3.75

72

37.5

27/05/19 - - - 10

15

3.75

3

37.5

45

9 3 27

Particular Amount Amount Variance

Standard hours–

actual hours)

*Standard price (1000-2200)*10 -2000 Adverse

Material price variance

Particular Amount Amount Variance

Standard price -

actual prices ) *

Actual hours (10-9.5)*2200 1100 favourable

Calculation of closing inventory of material using LIFO and Weighted average method:

Under LIFO (last in first out) method:

Date Purchased Issued Closing stock

Units Units

(in £)

Total

(in £)

Units Units

(in £)

Total(in

£)

Units units(in

£)

Total(in

£)

01/05/19 40 3 120

12/05/19 20 3.6 72 - - - 40

20

3

3.6

120

72

15/05/19 20

16

3.6

3

72

48

24 3 72

20/05/19 20 3.75 75 - - - 24

20

3

3.75

72

75

23/05/19 - - - 10 3.75 37.5 24

10

3

3.75

72

37.5

27/05/19 - - - 10

15

3.75

3

37.5

45

9 3 27

30/05/19 - - - 5 3 15 4 3 12

Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.000

0

05/12 Bought 25 units

at £ 3.60 each 25 3.60 90. 65 3.2308 210.000

0

05/15 Issued 36 units 36 3.2308 116.30

77 29 3.2308 93.6923

05/20 Bought 20 units

at £ 3.75 each 20 3.75 75. 49 3.4427 168.692

3

05/23 Issued 10 units 10 3.4427 34.427

0 39 3.4427 134.265

3

05/27 Issued 25 units 25 3.4427 86.067

5 14 3.4427 48.1978

05/30 Issued 5 units 5 3.44 17.213

5 9 3.4427 30.9843

TASK 3

P4 Merit and demerit of planning tools:

In present time every type of business prepare budget to estimate income and expenses of

each department of company. The budgets are produced for a particular time and present in front

of top management. It will help in taking effective decisions. Hawthorn International, prepare of

budget by determining of actual financial position in reference to improve the reliability in

budgeted figures (Schaltegger, 2012).

Budgetary control is systematic process which can control business activities and used in

Hawthorn International to analysis the projected budgets with real information at a specific time

frame. The budget of the company prepare in systematic manner, The following steps are

required to follow to prepare budget -

Set goals of the company

Analysis income and expenses of a company

Valuation of closing stock by using weighted average method:

05/01 Previous balance

(inventory) 40 3.0000 120.000

0

05/12 Bought 25 units

at £ 3.60 each 25 3.60 90. 65 3.2308 210.000

0

05/15 Issued 36 units 36 3.2308 116.30

77 29 3.2308 93.6923

05/20 Bought 20 units

at £ 3.75 each 20 3.75 75. 49 3.4427 168.692

3

05/23 Issued 10 units 10 3.4427 34.427

0 39 3.4427 134.265

3

05/27 Issued 25 units 25 3.4427 86.067

5 14 3.4427 48.1978

05/30 Issued 5 units 5 3.44 17.213

5 9 3.4427 30.9843

TASK 3

P4 Merit and demerit of planning tools:

In present time every type of business prepare budget to estimate income and expenses of

each department of company. The budgets are produced for a particular time and present in front

of top management. It will help in taking effective decisions. Hawthorn International, prepare of

budget by determining of actual financial position in reference to improve the reliability in

budgeted figures (Schaltegger, 2012).

Budgetary control is systematic process which can control business activities and used in

Hawthorn International to analysis the projected budgets with real information at a specific time

frame. The budget of the company prepare in systematic manner, The following steps are

required to follow to prepare budget -

Set goals of the company

Analysis income and expenses of a company

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.