Financial Malpractices and Audit of ABC Learning: Presentation

VerifiedAdded on 2021/04/17

|12

|1176

|116

Presentation

AI Summary

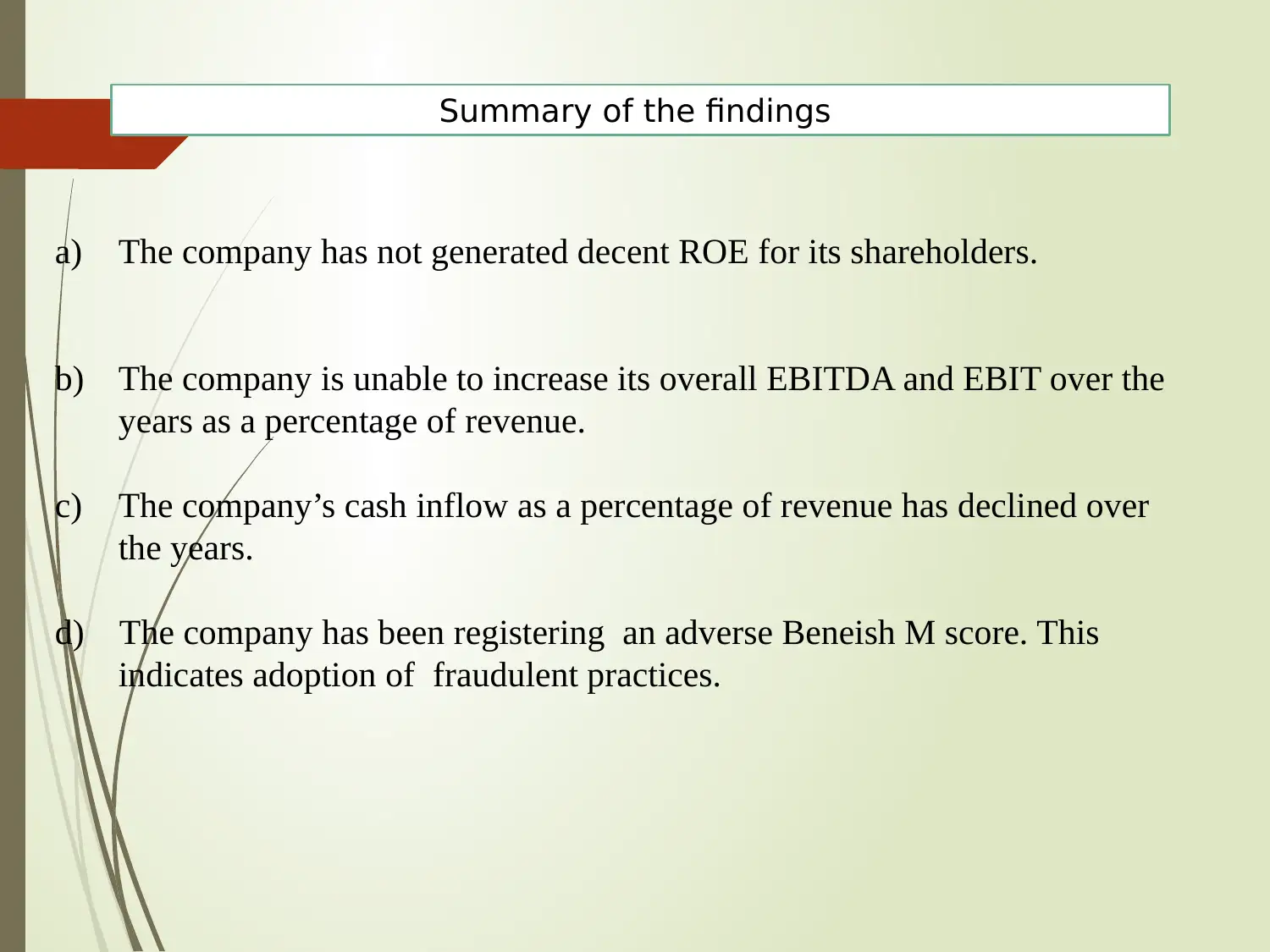

This presentation provides a detailed audit of ABC Learning, focusing on the impact of financial malpractices. It begins with an introduction outlining the presentation's purpose, which is to analyze the financial performance of the company and highlight how adopting malpractices can lead to significant issues. The presentation utilizes relevant auditing standards (ASA 200, 220, 230, 240, 315, and 500) to guide the analysis. Financial tools such as DuPont analysis, common size statement analysis, trend analysis, and Beneish M-score analysis are employed to assess the company's financial health. The analysis reveals a drastic reduction in ROE, declining EBITDA and EBIT, and an adverse Beneish M-score, indicating potential fraudulent practices. The presentation concludes with recommendations to stop fraudulent activities, reduce operating costs, and increase profitability to improve the company's financial standing, emphasizing the importance of maintaining a positive balance in reserves and surplus to avoid shareholder disinterest and the eventual destruction of the company's image.

1 out of 12

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.