Strategic Management Analysis in the Financial Industry: Report

VerifiedAdded on 2021/04/21

|21

|3775

|62

Report

AI Summary

This report provides a comprehensive analysis of strategic management within the financial industry. It begins with an introduction to the industry, highlighting key features such as market size, growth rate, and competitiveness. The report then delves into external factors impacting the industry, employing PESTLE and Porter's Five Forces analyses to assess political, economic, social, technological, legal, and environmental influences, as well as competitive dynamics. Furthermore, the report examines changes within financial companies, particularly focusing on innovation in resources and capabilities. The analysis covers the global significance of the financial industry, market structure, and the impact of globalization and technology. Finally, the report offers real-life examples of financial institutions and their strategic adaptations, providing a well-rounded understanding of the subject.

STRATEGIC MANAGEMENT

(FINANCIAL INDUSTRY)

1

(FINANCIAL INDUSTRY)

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of contents

Introduction:............................................................................................................... 3

Key features of the financial industry:........................................................................3

PESTLE analysis:......................................................................................................... 7

5 Forces Analysis:....................................................................................................... 8

Changes in the Companies in the Financial Industry: Innovating Resources and

Capabilities............................................................................................................... 12

Conclusion:............................................................................................................... 18

2

Introduction:............................................................................................................... 3

Key features of the financial industry:........................................................................3

PESTLE analysis:......................................................................................................... 7

5 Forces Analysis:....................................................................................................... 8

Changes in the Companies in the Financial Industry: Innovating Resources and

Capabilities............................................................................................................... 12

Conclusion:............................................................................................................... 18

2

Introduction:

Financial institution all over the world is dependent on the international financial

industry as it determines strategic management decisions of the organizations.

Globalization has made competition even tough in the industry, the key aim is

survival and success of many financial institutions is to implement strategic

partnership, which makes them more competitive and offer diverse services to their

clients and consumers. It can also be observed that the immediate effects of

deregulation lead to geographic diversification and changes in policies, which

further results in the implementation of interstate banking restrictions and gradual

reduction of intrastate. Technology and innovation play an important role in the

finance industry, organisations adapt to these in order to conform to the demand of

the global customers (Coleman, 2016). Some of the organisations that

internationally operate in an authoritative position are: The World Bank,

International Monetary Fund, European central bank, World Economic Forum etc.

The assignment focuses on the strategic management and its implementation on

financial industries. The essay also highlights the key features of financial industry

comprised of market size, industry growth rate, competitiveness and market

structure. It also analyses the external factors using Porter five forces and PESTEL

analysis, focusing on its high impact on the strategic management strategy of the

financial industry. In fact, this essay also deals with a real-life example of many

financial companies to focus the way the external forces impact on their

innovativeness and implementation of resources and capabilities.

Key features of the financial industry:

Market size:

As per Organization for Economic Cooperation and Development (OECD), financial

services make up 20-30% of total service market revenue and about 20% of the

total Gross Domestic Product(GDP) in developed economies like Denmark, Germany

and Singapore. According to Al-Mulaliand Ozturk (2015), the most important three

financial services like retail banking, life insurance and property and casual

3

Financial institution all over the world is dependent on the international financial

industry as it determines strategic management decisions of the organizations.

Globalization has made competition even tough in the industry, the key aim is

survival and success of many financial institutions is to implement strategic

partnership, which makes them more competitive and offer diverse services to their

clients and consumers. It can also be observed that the immediate effects of

deregulation lead to geographic diversification and changes in policies, which

further results in the implementation of interstate banking restrictions and gradual

reduction of intrastate. Technology and innovation play an important role in the

finance industry, organisations adapt to these in order to conform to the demand of

the global customers (Coleman, 2016). Some of the organisations that

internationally operate in an authoritative position are: The World Bank,

International Monetary Fund, European central bank, World Economic Forum etc.

The assignment focuses on the strategic management and its implementation on

financial industries. The essay also highlights the key features of financial industry

comprised of market size, industry growth rate, competitiveness and market

structure. It also analyses the external factors using Porter five forces and PESTEL

analysis, focusing on its high impact on the strategic management strategy of the

financial industry. In fact, this essay also deals with a real-life example of many

financial companies to focus the way the external forces impact on their

innovativeness and implementation of resources and capabilities.

Key features of the financial industry:

Market size:

As per Organization for Economic Cooperation and Development (OECD), financial

services make up 20-30% of total service market revenue and about 20% of the

total Gross Domestic Product(GDP) in developed economies like Denmark, Germany

and Singapore. According to Al-Mulaliand Ozturk (2015), the most important three

financial services like retail banking, life insurance and property and casual

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

insurance generate annual revenue of approximately $6.6 trillion and have tended

to grow at 6% compound annual rate over the preceding decade.

Industry growth rate:

International Monetary Fund (IMF) stated that the total global economy is worth

$77.6 trillion in recent years. Therefore, if the financial services from banking and

insurance sector are kept up to 6% growth rate for the years from 2014 to 2015,

then its 2016 figure would be $13.1 trillion(Baptistaand Oliveira, 2015).On the other

hand, particularly global banking industry has experienced a healthy growth rate in

recent years, generating the Compound Annual Growth Rate (CAGR) of 4.7%

between 2016 and 2017 for reaching a value of $134.1 trillion, as per the data from

MarkerLine Research Firm.

The global significance of financial industry:

This industry has global significance because global financial markets have

undergone major structural changes in recent years. Due to accelerating integration

and globalization, there is a prevalence of certain changes in world financial

markets. Apart from this, global financial markets also recently experienced

increased securitization.According to Borio (2014), these developments are also

spurred due to effective mergers and acquisitions worldwide. Broadening and

expansion of derivative markets are also one of a factor that makes this industry

global. For examples, banks in all over Europe are merging and forming alliances on

an unparalleled scale and thereby changing the banking environment and creating

global networks.

Competitiveness:

Competitors in banking sectors:

International banks continue to grow their assets as the world economy expands. In

fact, there is debate whether China's economy is bigger than the United States

regarding banking industries.

4

to grow at 6% compound annual rate over the preceding decade.

Industry growth rate:

International Monetary Fund (IMF) stated that the total global economy is worth

$77.6 trillion in recent years. Therefore, if the financial services from banking and

insurance sector are kept up to 6% growth rate for the years from 2014 to 2015,

then its 2016 figure would be $13.1 trillion(Baptistaand Oliveira, 2015).On the other

hand, particularly global banking industry has experienced a healthy growth rate in

recent years, generating the Compound Annual Growth Rate (CAGR) of 4.7%

between 2016 and 2017 for reaching a value of $134.1 trillion, as per the data from

MarkerLine Research Firm.

The global significance of financial industry:

This industry has global significance because global financial markets have

undergone major structural changes in recent years. Due to accelerating integration

and globalization, there is a prevalence of certain changes in world financial

markets. Apart from this, global financial markets also recently experienced

increased securitization.According to Borio (2014), these developments are also

spurred due to effective mergers and acquisitions worldwide. Broadening and

expansion of derivative markets are also one of a factor that makes this industry

global. For examples, banks in all over Europe are merging and forming alliances on

an unparalleled scale and thereby changing the banking environment and creating

global networks.

Competitiveness:

Competitors in banking sectors:

International banks continue to grow their assets as the world economy expands. In

fact, there is debate whether China's economy is bigger than the United States

regarding banking industries.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

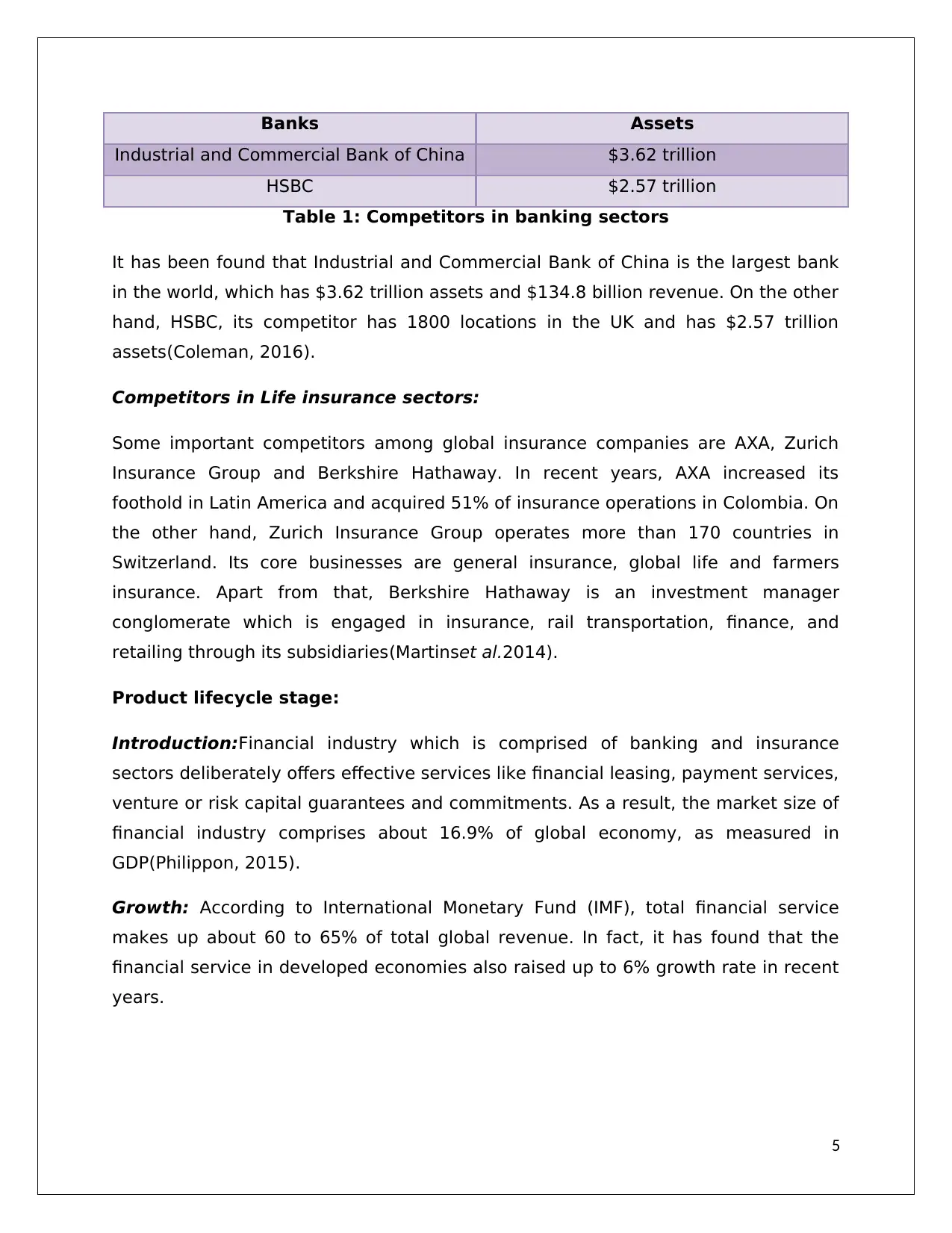

Banks Assets

Industrial and Commercial Bank of China $3.62 trillion

HSBC $2.57 trillion

Table 1: Competitors in banking sectors

It has been found that Industrial and Commercial Bank of China is the largest bank

in the world, which has $3.62 trillion assets and $134.8 billion revenue. On the other

hand, HSBC, its competitor has 1800 locations in the UK and has $2.57 trillion

assets(Coleman, 2016).

Competitors in Life insurance sectors:

Some important competitors among global insurance companies are AXA, Zurich

Insurance Group and Berkshire Hathaway. In recent years, AXA increased its

foothold in Latin America and acquired 51% of insurance operations in Colombia. On

the other hand, Zurich Insurance Group operates more than 170 countries in

Switzerland. Its core businesses are general insurance, global life and farmers

insurance. Apart from that, Berkshire Hathaway is an investment manager

conglomerate which is engaged in insurance, rail transportation, finance, and

retailing through its subsidiaries(Martinset al.2014).

Product lifecycle stage:

Introduction:Financial industry which is comprised of banking and insurance

sectors deliberately offers effective services like financial leasing, payment services,

venture or risk capital guarantees and commitments. As a result, the market size of

financial industry comprises about 16.9% of global economy, as measured in

GDP(Philippon, 2015).

Growth: According to International Monetary Fund (IMF), total financial service

makes up about 60 to 65% of total global revenue. In fact, it has found that the

financial service in developed economies also raised up to 6% growth rate in recent

years.

5

Industrial and Commercial Bank of China $3.62 trillion

HSBC $2.57 trillion

Table 1: Competitors in banking sectors

It has been found that Industrial and Commercial Bank of China is the largest bank

in the world, which has $3.62 trillion assets and $134.8 billion revenue. On the other

hand, HSBC, its competitor has 1800 locations in the UK and has $2.57 trillion

assets(Coleman, 2016).

Competitors in Life insurance sectors:

Some important competitors among global insurance companies are AXA, Zurich

Insurance Group and Berkshire Hathaway. In recent years, AXA increased its

foothold in Latin America and acquired 51% of insurance operations in Colombia. On

the other hand, Zurich Insurance Group operates more than 170 countries in

Switzerland. Its core businesses are general insurance, global life and farmers

insurance. Apart from that, Berkshire Hathaway is an investment manager

conglomerate which is engaged in insurance, rail transportation, finance, and

retailing through its subsidiaries(Martinset al.2014).

Product lifecycle stage:

Introduction:Financial industry which is comprised of banking and insurance

sectors deliberately offers effective services like financial leasing, payment services,

venture or risk capital guarantees and commitments. As a result, the market size of

financial industry comprises about 16.9% of global economy, as measured in

GDP(Philippon, 2015).

Growth: According to International Monetary Fund (IMF), total financial service

makes up about 60 to 65% of total global revenue. In fact, it has found that the

financial service in developed economies also raised up to 6% growth rate in recent

years.

5

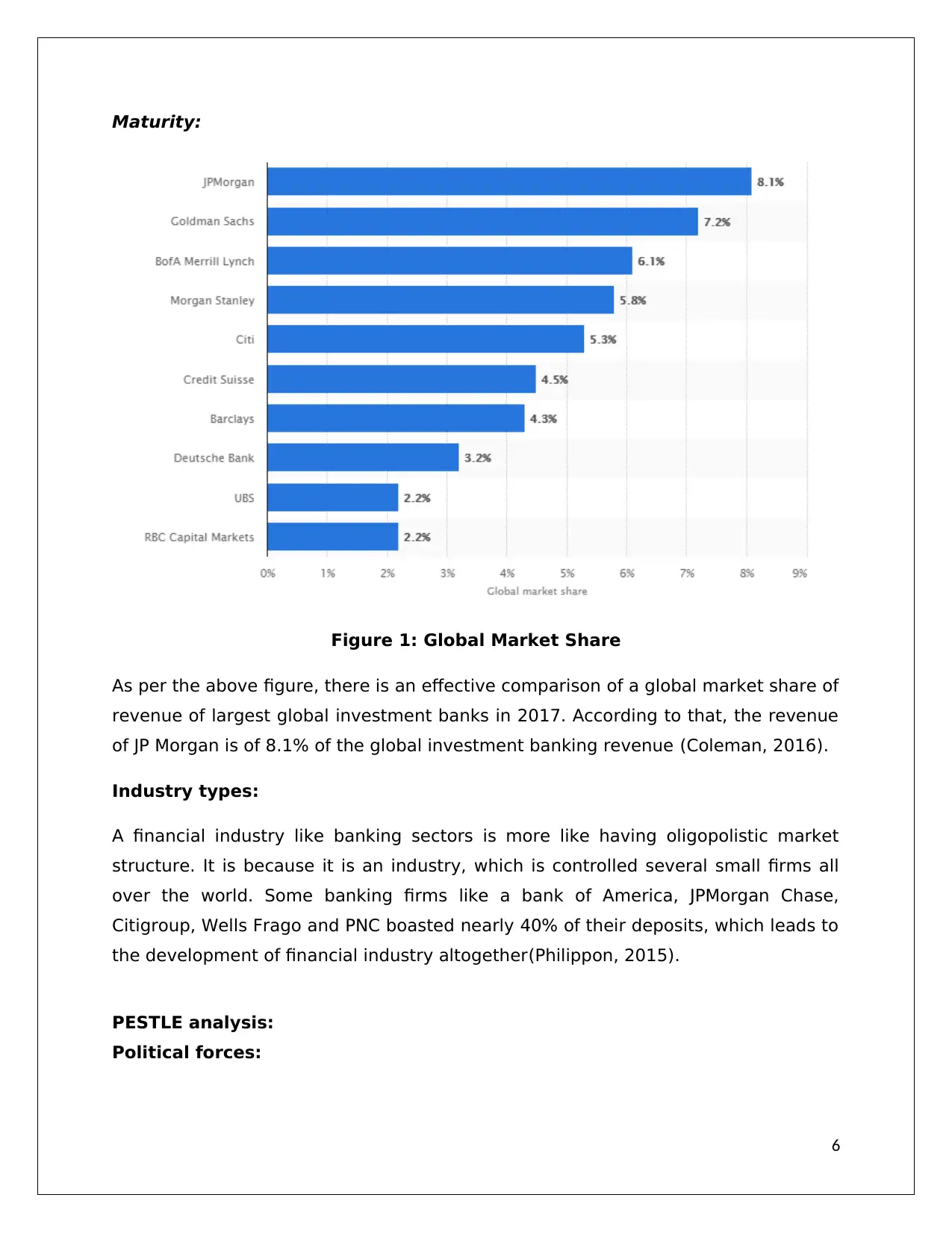

Maturity:

Figure 1: Global Market Share

As per the above figure, there is an effective comparison of a global market share of

revenue of largest global investment banks in 2017. According to that, the revenue

of JP Morgan is of 8.1% of the global investment banking revenue (Coleman, 2016).

Industry types:

A financial industry like banking sectors is more like having oligopolistic market

structure. It is because it is an industry, which is controlled several small firms all

over the world. Some banking firms like a bank of America, JPMorgan Chase,

Citigroup, Wells Frago and PNC boasted nearly 40% of their deposits, which leads to

the development of financial industry altogether(Philippon, 2015).

PESTLE analysis:

Political forces:

6

Figure 1: Global Market Share

As per the above figure, there is an effective comparison of a global market share of

revenue of largest global investment banks in 2017. According to that, the revenue

of JP Morgan is of 8.1% of the global investment banking revenue (Coleman, 2016).

Industry types:

A financial industry like banking sectors is more like having oligopolistic market

structure. It is because it is an industry, which is controlled several small firms all

over the world. Some banking firms like a bank of America, JPMorgan Chase,

Citigroup, Wells Frago and PNC boasted nearly 40% of their deposits, which leads to

the development of financial industry altogether(Philippon, 2015).

PESTLE analysis:

Political forces:

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

These are the rules, framework and guidelines that are associated with the

governments, financial institutions and authoritative bodies. Based on geographical

locations of the organisations the management of the companies is bound by the

rules and regulations which govern the company (Valdezand Molyneux, 2015).

Some of the aspects which impact the organisations in this industry are:

international legislations, labour regulations, trade rules and regulations in the

country of operation, international relation, political stability and favorability of the

government. Based on the region on operations the organisation has to follow the

rules set out by authoritative organisations like the ones mentioned above

(Valdezand Molyneux, 2015). For example, SAP Financial Services Forum looks into

the opportunities and benefits of digitalization and explores the implementation of

disruptive technologies in banking and insurance companies. Another example is

Coalition Agreement in the UK, which leads to a huge deficit in the insurance sector

and disarray in a banking system, due to which there is a huge loss in sovereign

debts market of UK (Valdezand Molyneux, 2015). Even due to this agreement, there

are low-interest rates on financial stability and long-term impacts of quantitative

easing (QE ).

Economic forces:

In the industry, there are factors such as the rate of the currency in the

international market, inflation rate, market and trade cycles, interest rate etc which

impact the industry. The economic factors are important as they provide growth

and expansion opportunities for the organisations, if the conditions are favorable

then new organisations in the finance industry have scope to invest as well as

operating organisations. For example: The financial crash of 2008-2009 impacts on

financial operations of banking industries. Several leading banks had to deal with a

problem of cyber security. Market orientation and banking structure also lead to the

change in the development of financial operations of banking and insurance

companies. In fact, interest rates also have some impacts on share prices in the

financial services industries like banks and insurance companies. For example,

HSBC bank has tax benefits with the deposit tenure of 5 years.

Technological forces:

7

governments, financial institutions and authoritative bodies. Based on geographical

locations of the organisations the management of the companies is bound by the

rules and regulations which govern the company (Valdezand Molyneux, 2015).

Some of the aspects which impact the organisations in this industry are:

international legislations, labour regulations, trade rules and regulations in the

country of operation, international relation, political stability and favorability of the

government. Based on the region on operations the organisation has to follow the

rules set out by authoritative organisations like the ones mentioned above

(Valdezand Molyneux, 2015). For example, SAP Financial Services Forum looks into

the opportunities and benefits of digitalization and explores the implementation of

disruptive technologies in banking and insurance companies. Another example is

Coalition Agreement in the UK, which leads to a huge deficit in the insurance sector

and disarray in a banking system, due to which there is a huge loss in sovereign

debts market of UK (Valdezand Molyneux, 2015). Even due to this agreement, there

are low-interest rates on financial stability and long-term impacts of quantitative

easing (QE ).

Economic forces:

In the industry, there are factors such as the rate of the currency in the

international market, inflation rate, market and trade cycles, interest rate etc which

impact the industry. The economic factors are important as they provide growth

and expansion opportunities for the organisations, if the conditions are favorable

then new organisations in the finance industry have scope to invest as well as

operating organisations. For example: The financial crash of 2008-2009 impacts on

financial operations of banking industries. Several leading banks had to deal with a

problem of cyber security. Market orientation and banking structure also lead to the

change in the development of financial operations of banking and insurance

companies. In fact, interest rates also have some impacts on share prices in the

financial services industries like banks and insurance companies. For example,

HSBC bank has tax benefits with the deposit tenure of 5 years.

Technological forces:

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Technology is improving, advancing with research and development and in every

business industry, it plays an important role it provides scope and opportunity for

the business to innovate and grow. It makes the process of Innovations in

technology have played an important role in the industry, now anyone can use a

card and conduct transactions form any part of the world. Core banking, online and

mobile banking. Fin-tech disruptor is one of the financial technologies that mainly

focused on the mobile payments to insurance. Organisations incorporate technology

in the business operation which includes hardware software, internal and external

services. Moreover, it can be assumed that by 2020, there will be decentralized

asset ownership with the use of information technology rather than automatic turn

to banks as an intermediary. According to Philippon (2015), Blockchain “public

ledger” can be a significant part of financial institutions’ technology and

infrastructure, as it moves from large retail sector to institutional use.

5 Forces Analysis:

The 5 Forces Analysis is a tool that is used to study the intensity of the

competition in the Industry at the same time it indicates scopes and opportunities

that organisations operating in the industry may have. This tool was developed in

1979 by Michael Porter. This is used as a strategic management tool to develop the

policies and formulate plans for the company to successfully grow in the

competitive market (Ho 2014).

Rivalry

among

Competing

Firms:

The competition in the market is created by the firms who provide

similar kind of products and services. It is important to analyze

the rate to competition in the industry because it will help the

company to formulate strategic decisions better. In the global

financial services market, the number of competing financial firms

is limited, which makes the competitors compete for the same

customers and resources. The lower storage costs also enable the

competitors to bear lower risks to unload their inventory all at a

time. Besides, due to the increasing growth of the financial

services industry, it is evitable that all the competitors are

growing in terms of revenue creation which gives a substantial

reason that the competitors need not to compete to take the

8

business industry, it plays an important role it provides scope and opportunity for

the business to innovate and grow. It makes the process of Innovations in

technology have played an important role in the industry, now anyone can use a

card and conduct transactions form any part of the world. Core banking, online and

mobile banking. Fin-tech disruptor is one of the financial technologies that mainly

focused on the mobile payments to insurance. Organisations incorporate technology

in the business operation which includes hardware software, internal and external

services. Moreover, it can be assumed that by 2020, there will be decentralized

asset ownership with the use of information technology rather than automatic turn

to banks as an intermediary. According to Philippon (2015), Blockchain “public

ledger” can be a significant part of financial institutions’ technology and

infrastructure, as it moves from large retail sector to institutional use.

5 Forces Analysis:

The 5 Forces Analysis is a tool that is used to study the intensity of the

competition in the Industry at the same time it indicates scopes and opportunities

that organisations operating in the industry may have. This tool was developed in

1979 by Michael Porter. This is used as a strategic management tool to develop the

policies and formulate plans for the company to successfully grow in the

competitive market (Ho 2014).

Rivalry

among

Competing

Firms:

The competition in the market is created by the firms who provide

similar kind of products and services. It is important to analyze

the rate to competition in the industry because it will help the

company to formulate strategic decisions better. In the global

financial services market, the number of competing financial firms

is limited, which makes the competitors compete for the same

customers and resources. The lower storage costs also enable the

competitors to bear lower risks to unload their inventory all at a

time. Besides, due to the increasing growth of the financial

services industry, it is evitable that all the competitors are

growing in terms of revenue creation which gives a substantial

reason that the competitors need not to compete to take the

8

market share. In addition to these, the low exit barriers in the

market enable the competitors to increase their profits naturally.

All these factors ensure that the rivalry among the competing

firms in the financial services market is moderately low (Porter,

2016).

Threat of

entry of new

competitors:

This is the scope of new organisations to start their business in

the industry. This creates new competition as new firms bring

new values and innovations to the industry. The distribution

network in the global financial services market is weak and it is

also very expensive to move the financial goods in the market.

High capital requirement is also a barrier to the financial

companies and they need to spend a lot of capital to survive in

the market. Besides the introduction of the sunk costs, facing the

existing big brands, inability to cope the advanced financial

technologies, smaller economies of scale, and contingencies

related to local government policies also make the threat of new

entry in the global financial sector very low (Storey, 2016).

9

RivalryamongFirms:ModeratelyLowThreatofNewEntry:LowThreatofSubstitutes:LowBargainingPowerofConsumers:ModerateBargainingPowerofSuppliers:ModeratelyLow

market enable the competitors to increase their profits naturally.

All these factors ensure that the rivalry among the competing

firms in the financial services market is moderately low (Porter,

2016).

Threat of

entry of new

competitors:

This is the scope of new organisations to start their business in

the industry. This creates new competition as new firms bring

new values and innovations to the industry. The distribution

network in the global financial services market is weak and it is

also very expensive to move the financial goods in the market.

High capital requirement is also a barrier to the financial

companies and they need to spend a lot of capital to survive in

the market. Besides the introduction of the sunk costs, facing the

existing big brands, inability to cope the advanced financial

technologies, smaller economies of scale, and contingencies

related to local government policies also make the threat of new

entry in the global financial sector very low (Storey, 2016).

9

RivalryamongFirms:ModeratelyLowThreatofNewEntry:LowThreatofSubstitutes:LowBargainingPowerofConsumers:ModerateBargainingPowerofSuppliers:ModeratelyLow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Figure 2: Five Forces analysis

Bargaining

power of

suppliers:

There is a high level of competition among the suppliers in the

financial services sector which has a positive impact on the sector

as the suppliers cannot have bargaining leverage over the

producers. Apart from that, the low concentration of suppliers,

diverse distribution channels, and financial firms’ ability to switch

suppliers reduce their bargaining power. Bedside the local

government intervention makes it difficult for the suppliers to

bargain for the services they offer (Minsky, 2016). Suppliers in the

finance industry are can be third party service providers,

hardware and software suppliers etc.

Threat of

development

of substitute

products:

The substitutes are the indirect threats in the industry. The

substitutes of the global financial services industry usually show

lower performance, so the customers feel no urge to switch from

the financial sector. Besides, the limited number of substitutes

and the products and services offered by these substitutes do not

let the development of substitute products pose a strong threat to

the industry (Webb and Martin, 2017).

Bargaining

power of

consumers:

In the financial services sector, the customer has no bargaining

power as negotiator and they also do not get much of attention

when they need customization in their schemes. Low customer

price sensitivity, low dependence on the distributor and large

number of customer base disable the customers to have the

bargaining power, but sometimes the competitors can offer

services that are suitable for the customers, but the end it is the

customers who need to negotiate with the terms and schemes

(Shoup, 2017).

Weakest force:

The weakest force among these five forces is apparently the threat of substitutes.

There is actually no closer substitute for the financial services around the world

except for few countries such as the US and the UK where the microfinance services

10

Bargaining

power of

suppliers:

There is a high level of competition among the suppliers in the

financial services sector which has a positive impact on the sector

as the suppliers cannot have bargaining leverage over the

producers. Apart from that, the low concentration of suppliers,

diverse distribution channels, and financial firms’ ability to switch

suppliers reduce their bargaining power. Bedside the local

government intervention makes it difficult for the suppliers to

bargain for the services they offer (Minsky, 2016). Suppliers in the

finance industry are can be third party service providers,

hardware and software suppliers etc.

Threat of

development

of substitute

products:

The substitutes are the indirect threats in the industry. The

substitutes of the global financial services industry usually show

lower performance, so the customers feel no urge to switch from

the financial sector. Besides, the limited number of substitutes

and the products and services offered by these substitutes do not

let the development of substitute products pose a strong threat to

the industry (Webb and Martin, 2017).

Bargaining

power of

consumers:

In the financial services sector, the customer has no bargaining

power as negotiator and they also do not get much of attention

when they need customization in their schemes. Low customer

price sensitivity, low dependence on the distributor and large

number of customer base disable the customers to have the

bargaining power, but sometimes the competitors can offer

services that are suitable for the customers, but the end it is the

customers who need to negotiate with the terms and schemes

(Shoup, 2017).

Weakest force:

The weakest force among these five forces is apparently the threat of substitutes.

There is actually no closer substitute for the financial services around the world

except for few countries such as the US and the UK where the microfinance services

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

firms are seen as the potential substitutes for the global financial services industry.

In these countries the microfinance providers cater to the low or middle income

families to meet their basic needs at lower interest rates. But in many countries like

India, the microfinance service providers are also treated as a valuable part of the

entire financial services gamut (Shoup, 2017).

Competitor’s response to force:

Comparatively the bargaining power of consumers is a stronger force that the

competitors in the global financial services industry need to respond meticulously.

The consumers, nowadays, tend to have various demands such as digitization,

personalization and more. The financial services around the world are also more

inclined to know what the consumers really demand and they come up with

different latest solutions such as integration of data as currency, automated

servicing, digital services, personalization, and different channel agnostic.

Apparently the weaker force is the threat of substitutes and the competitors

sometimes find the substitutes profitable and they tend to follow the strategy of

merge &acquisition with these potential substitutes and enhance their portfolio with

various offerings (Aalbers, 2017).

Changing of Forces in Next 3 Years:

Pertaining to the five forces, the changes in these forces in the next three years are

not expected to be very significant.

The finance industry is a huge industry where the competitors do not need to steal

the market share as this industry undoubtedly an ever growing industry because of

increasing demand from the customers and also it caters to all kinds of consumers

such as business entities, corporate, middle class workers and lower class people.

Besides, the current slowdown in the global economy is going to cast a negative

impact on the global financial services industry (Porter, 2016).

The landscape of the threat of new competitors is expected to change if the global

government policies go through serious amendments. But as for now, there is no

11

In these countries the microfinance providers cater to the low or middle income

families to meet their basic needs at lower interest rates. But in many countries like

India, the microfinance service providers are also treated as a valuable part of the

entire financial services gamut (Shoup, 2017).

Competitor’s response to force:

Comparatively the bargaining power of consumers is a stronger force that the

competitors in the global financial services industry need to respond meticulously.

The consumers, nowadays, tend to have various demands such as digitization,

personalization and more. The financial services around the world are also more

inclined to know what the consumers really demand and they come up with

different latest solutions such as integration of data as currency, automated

servicing, digital services, personalization, and different channel agnostic.

Apparently the weaker force is the threat of substitutes and the competitors

sometimes find the substitutes profitable and they tend to follow the strategy of

merge &acquisition with these potential substitutes and enhance their portfolio with

various offerings (Aalbers, 2017).

Changing of Forces in Next 3 Years:

Pertaining to the five forces, the changes in these forces in the next three years are

not expected to be very significant.

The finance industry is a huge industry where the competitors do not need to steal

the market share as this industry undoubtedly an ever growing industry because of

increasing demand from the customers and also it caters to all kinds of consumers

such as business entities, corporate, middle class workers and lower class people.

Besides, the current slowdown in the global economy is going to cast a negative

impact on the global financial services industry (Porter, 2016).

The landscape of the threat of new competitors is expected to change if the global

government policies go through serious amendments. But as for now, there is no

11

Low Medium High

Low

Medium

High

Industry Attractiveness

Business Unit Strength

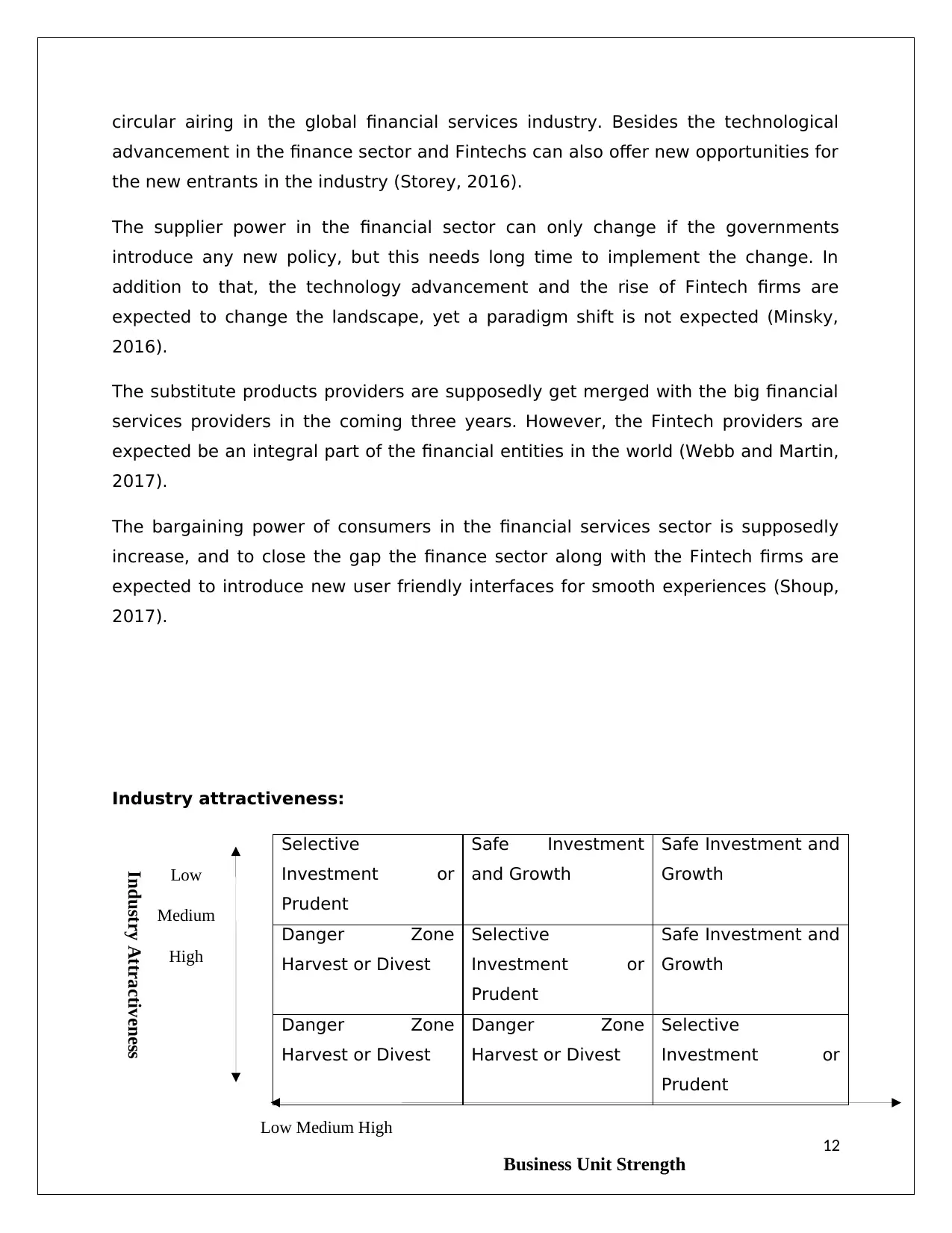

circular airing in the global financial services industry. Besides the technological

advancement in the finance sector and Fintechs can also offer new opportunities for

the new entrants in the industry (Storey, 2016).

The supplier power in the financial sector can only change if the governments

introduce any new policy, but this needs long time to implement the change. In

addition to that, the technology advancement and the rise of Fintech firms are

expected to change the landscape, yet a paradigm shift is not expected (Minsky,

2016).

The substitute products providers are supposedly get merged with the big financial

services providers in the coming three years. However, the Fintech providers are

expected be an integral part of the financial entities in the world (Webb and Martin,

2017).

The bargaining power of consumers in the financial services sector is supposedly

increase, and to close the gap the finance sector along with the Fintech firms are

expected to introduce new user friendly interfaces for smooth experiences (Shoup,

2017).

Industry attractiveness:

Selective

Investment or

Prudent

Safe Investment

and Growth

Safe Investment and

Growth

Danger Zone

Harvest or Divest

Selective

Investment or

Prudent

Safe Investment and

Growth

Danger Zone

Harvest or Divest

Danger Zone

Harvest or Divest

Selective

Investment or

Prudent

12

Low

Medium

High

Industry Attractiveness

Business Unit Strength

circular airing in the global financial services industry. Besides the technological

advancement in the finance sector and Fintechs can also offer new opportunities for

the new entrants in the industry (Storey, 2016).

The supplier power in the financial sector can only change if the governments

introduce any new policy, but this needs long time to implement the change. In

addition to that, the technology advancement and the rise of Fintech firms are

expected to change the landscape, yet a paradigm shift is not expected (Minsky,

2016).

The substitute products providers are supposedly get merged with the big financial

services providers in the coming three years. However, the Fintech providers are

expected be an integral part of the financial entities in the world (Webb and Martin,

2017).

The bargaining power of consumers in the financial services sector is supposedly

increase, and to close the gap the finance sector along with the Fintech firms are

expected to introduce new user friendly interfaces for smooth experiences (Shoup,

2017).

Industry attractiveness:

Selective

Investment or

Prudent

Safe Investment

and Growth

Safe Investment and

Growth

Danger Zone

Harvest or Divest

Selective

Investment or

Prudent

Safe Investment and

Growth

Danger Zone

Harvest or Divest

Danger Zone

Harvest or Divest

Selective

Investment or

Prudent

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.