Financial Analysis Report: UK Tools Ltd and Fortune Trading

VerifiedAdded on 2023/06/10

|7

|1222

|412

Report

AI Summary

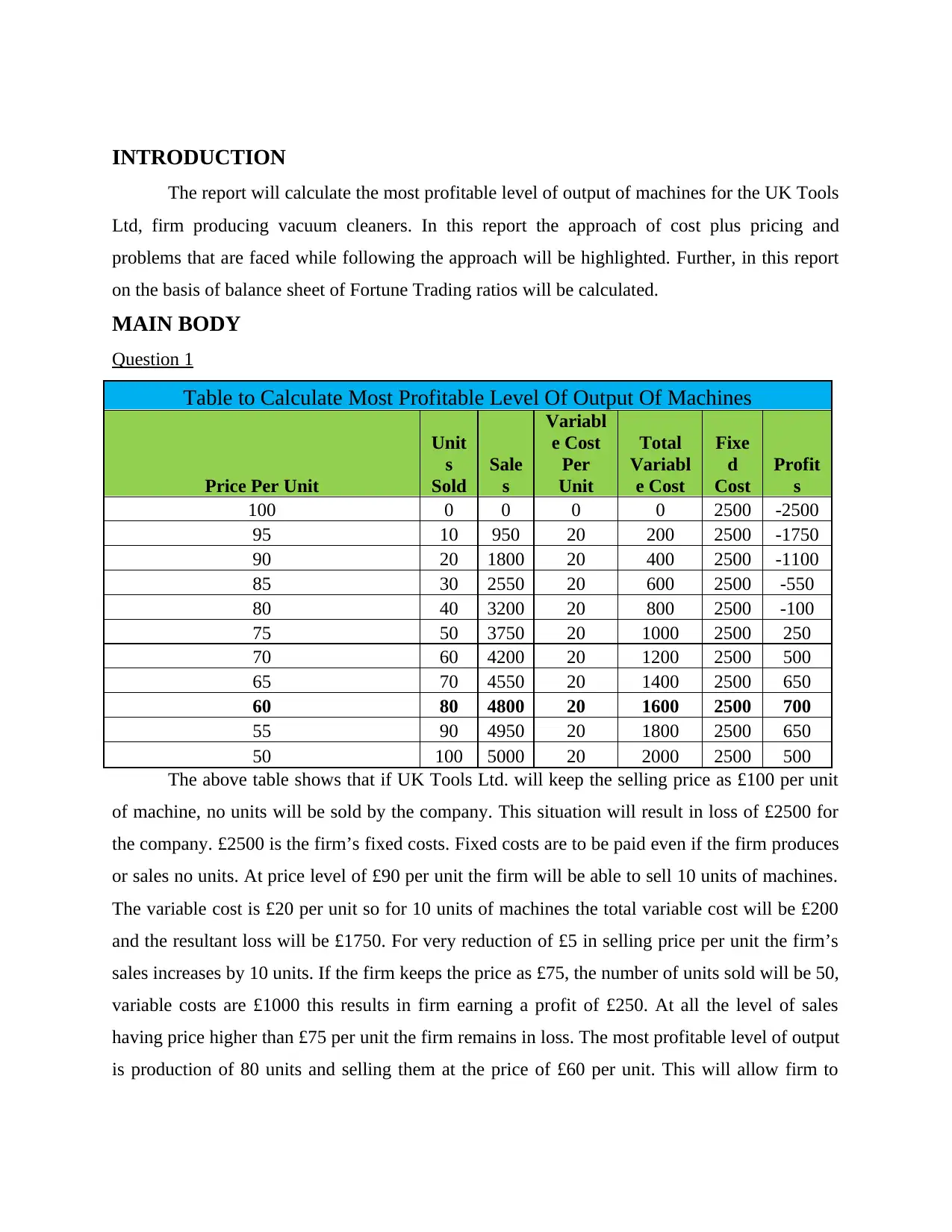

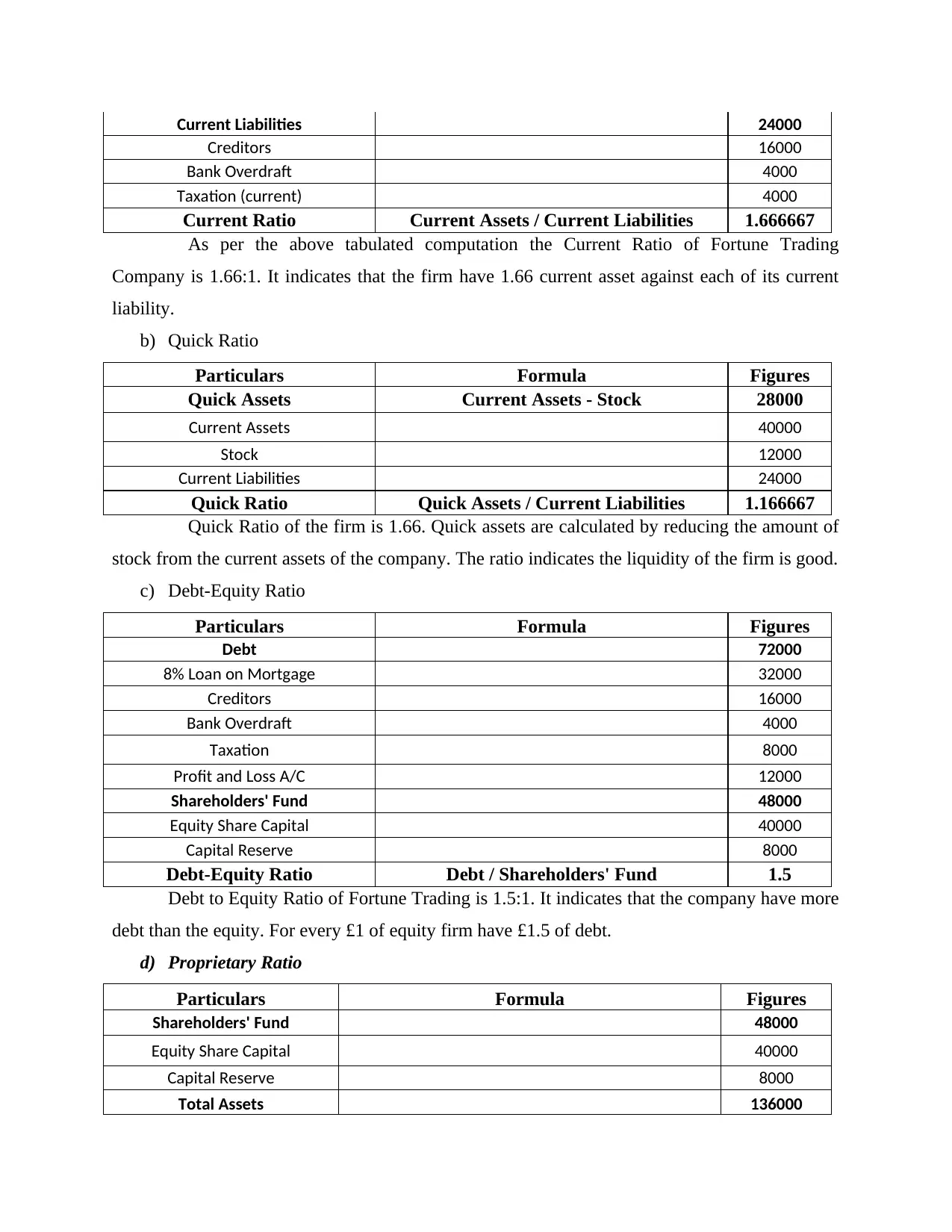

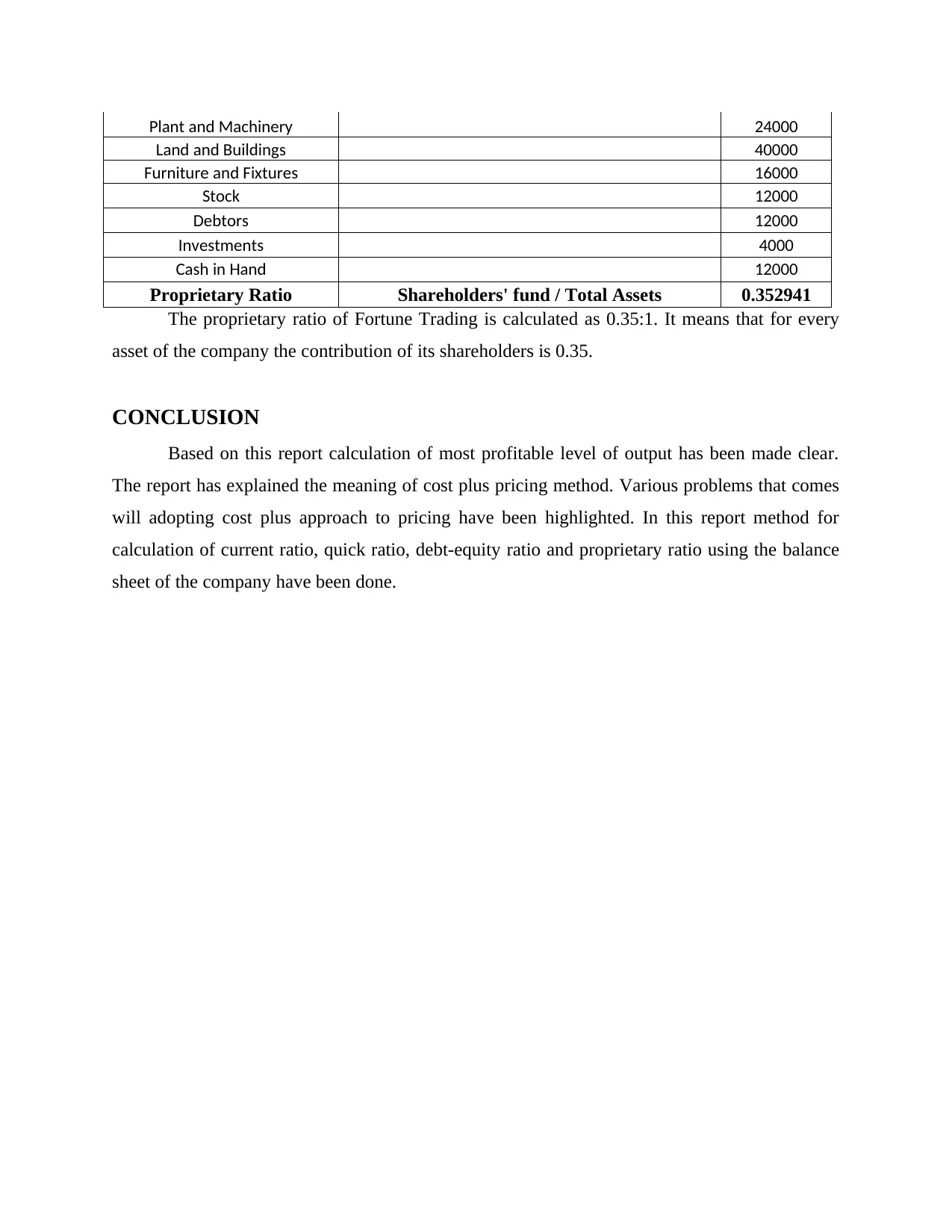

This report provides a comprehensive analysis of financial resource management, focusing on UK Tools Ltd and Fortune Trading. It begins by calculating the most profitable output level for UK Tools Ltd, considering variable and fixed costs to determine optimal pricing. The report then delves into cost-plus pricing, explaining its methodology and highlighting associated problems such as ignoring competition, potential cost overruns, and overlooking replacement costs. Finally, the report analyzes Fortune Trading's financial health by calculating key ratios, including the current ratio, quick ratio, debt-equity ratio, and proprietary ratio, using provided balance sheet information. The report concludes with a summary of the findings, emphasizing the importance of financial analysis in business decision-making.

1 out of 7

Related Documents

![Managing Financial Resources: Assessment Report - [University]](/_next/image/?url=https%3A%2F%2Fdesklib.com%2Fmedia%2Fimages%2Frj%2Fffeb11b89b8749a4afd2e6bcf0186e51.jpg&w=256&q=75)

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.