Financial and Management Accounting Report: Concepts and Techniques

VerifiedAdded on 2023/01/18

|22

|3454

|53

Report

AI Summary

This report provides a comprehensive overview of financial and management accounting. Section A delves into financial accounting, covering journal entries, trial balances, and the creation of income statements, owner's equity statements, and balance sheets as of April 30, 2019. It also highlights the distinctions between financial and management accounting, along with the characteristics of high-quality financial information. Section B focuses on management accounting techniques, including total cost per unit calculations under traditional costing, under/over absorption analysis, and profit comparisons under marginal and absorption costing methods. The report concludes with recommendations and references, offering a complete analysis of both accounting disciplines.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ACCOUNTING

ABSTRACT

The present report will reveal about the different accounting that are financial accounting and the

management accounting. The will report will give understanding of the financial accounting

concepts in Section A and of management accounting techniques in Section B. It will also give

characteristics of quality financial statements to management.

The present report will reveal about the different accounting that are financial accounting and the

management accounting. The will report will give understanding of the financial accounting

concepts in Section A and of management accounting techniques in Section B. It will also give

characteristics of quality financial statements to management.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

TABLE OF CONTENTS

ABSTRACT.....................................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION A1...................................................................................................................................1

1. Journal Entries.........................................................................................................................1

2. Unadjusted Trial Balance.........................................................................................................5

3. Income Statement, owner's equity and balance sheet as at April 30, 2019.............................5

SECTION A2...................................................................................................................................7

Difference between management accounting and financial accounting......................................7

Characteristic of high quality financial information to management of both companies............9

Statement describing each of the financial statements..............................................................10

SECTION B...................................................................................................................................10

Total Cost per unit under traditional costing system.................................................................10

Under or Over absorption for Product B and Product C............................................................11

Profits under Marginal and Absorption costing.........................................................................11

CONCLUSION and RECOMMENDATIONS.............................................................................13

REFERENCES..............................................................................................................................14

ABSTRACT.....................................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION A1...................................................................................................................................1

1. Journal Entries.........................................................................................................................1

2. Unadjusted Trial Balance.........................................................................................................5

3. Income Statement, owner's equity and balance sheet as at April 30, 2019.............................5

SECTION A2...................................................................................................................................7

Difference between management accounting and financial accounting......................................7

Characteristic of high quality financial information to management of both companies............9

Statement describing each of the financial statements..............................................................10

SECTION B...................................................................................................................................10

Total Cost per unit under traditional costing system.................................................................10

Under or Over absorption for Product B and Product C............................................................11

Profits under Marginal and Absorption costing.........................................................................11

CONCLUSION and RECOMMENDATIONS.............................................................................13

REFERENCES..............................................................................................................................14

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION

Financial accounting refers to the recording of the transactions and events occurring in

the organisation where the management accounting deals with preparing reports that will

enhance the profitability of the company. Both management and financial accounting have

separate importance for the company. The present report is about the financial accounting

methods and the management accounting techniques for recording the separate transactions

(Barron, Chung and Yong, 2016). It will be providing better understanding about both the

accounting methods through solutions.

SECTION A1

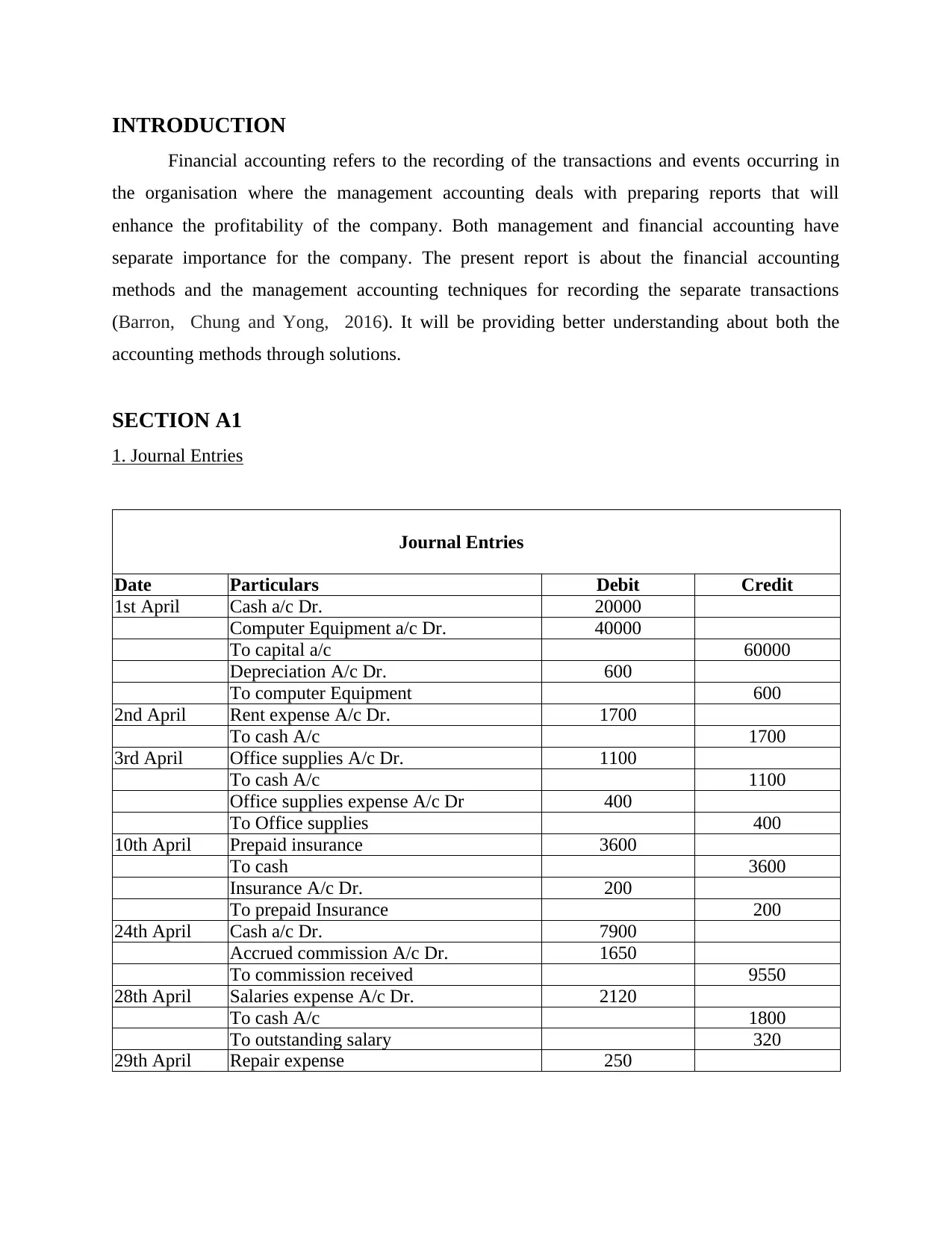

1. Journal Entries

Journal Entries

Date Particulars Debit Credit

1st April Cash a/c Dr. 20000

Computer Equipment a/c Dr. 40000

To capital a/c 60000

Depreciation A/c Dr. 600

To computer Equipment 600

2nd April Rent expense A/c Dr. 1700

To cash A/c 1700

3rd April Office supplies A/c Dr. 1100

To cash A/c 1100

Office supplies expense A/c Dr 400

To Office supplies 400

10th April Prepaid insurance 3600

To cash 3600

Insurance A/c Dr. 200

To prepaid Insurance 200

24th April Cash a/c Dr. 7900

Accrued commission A/c Dr. 1650

To commission received 9550

28th April Salaries expense A/c Dr. 2120

To cash A/c 1800

To outstanding salary 320

29th April Repair expense 250

Financial accounting refers to the recording of the transactions and events occurring in

the organisation where the management accounting deals with preparing reports that will

enhance the profitability of the company. Both management and financial accounting have

separate importance for the company. The present report is about the financial accounting

methods and the management accounting techniques for recording the separate transactions

(Barron, Chung and Yong, 2016). It will be providing better understanding about both the

accounting methods through solutions.

SECTION A1

1. Journal Entries

Journal Entries

Date Particulars Debit Credit

1st April Cash a/c Dr. 20000

Computer Equipment a/c Dr. 40000

To capital a/c 60000

Depreciation A/c Dr. 600

To computer Equipment 600

2nd April Rent expense A/c Dr. 1700

To cash A/c 1700

3rd April Office supplies A/c Dr. 1100

To cash A/c 1100

Office supplies expense A/c Dr 400

To Office supplies 400

10th April Prepaid insurance 3600

To cash 3600

Insurance A/c Dr. 200

To prepaid Insurance 200

24th April Cash a/c Dr. 7900

Accrued commission A/c Dr. 1650

To commission received 9550

28th April Salaries expense A/c Dr. 2120

To cash A/c 1800

To outstanding salary 320

29th April Repair expense 250

To cash 250

30th April Telephone bill expense A/c Dr. 650

To cash 650

30th April Drawing A/c Dr. 1500

To cash A/c 1500

81670 81670

Ledger Accounts

Dr.

Cash a/c

Cr.

Date Particulars Amount Date Particulars Amount

1st April To capital 20000 2nd April

By rent

expense 1700

24th April

To commission

received 7900 3rd April

By office

supplies 1100

10th April

By prepaid

insurance 3600

28th April By salaries 1800

29th April

By repair

expense 250

30th April

By telephone

bill expense 650

30th April By Drawings 1500

30th April By balance c/d 17300

27900 27900

Dr.

Computer equipment A/c

Cr.

Date Particulars Amount Date Particulars Amount

1st April To capital 40000 30th April

By

depreciation 600

30th April By balance c/d 39400

40000 40000

Dr.

Capital A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To balance c/d 60000 1st April By cash A/c 20000

By computer 40000

2

30th April Telephone bill expense A/c Dr. 650

To cash 650

30th April Drawing A/c Dr. 1500

To cash A/c 1500

81670 81670

Ledger Accounts

Dr.

Cash a/c

Cr.

Date Particulars Amount Date Particulars Amount

1st April To capital 20000 2nd April

By rent

expense 1700

24th April

To commission

received 7900 3rd April

By office

supplies 1100

10th April

By prepaid

insurance 3600

28th April By salaries 1800

29th April

By repair

expense 250

30th April

By telephone

bill expense 650

30th April By Drawings 1500

30th April By balance c/d 17300

27900 27900

Dr.

Computer equipment A/c

Cr.

Date Particulars Amount Date Particulars Amount

1st April To capital 40000 30th April

By

depreciation 600

30th April By balance c/d 39400

40000 40000

Dr.

Capital A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To balance c/d 60000 1st April By cash A/c 20000

By computer 40000

2

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

equipment

60000 60000

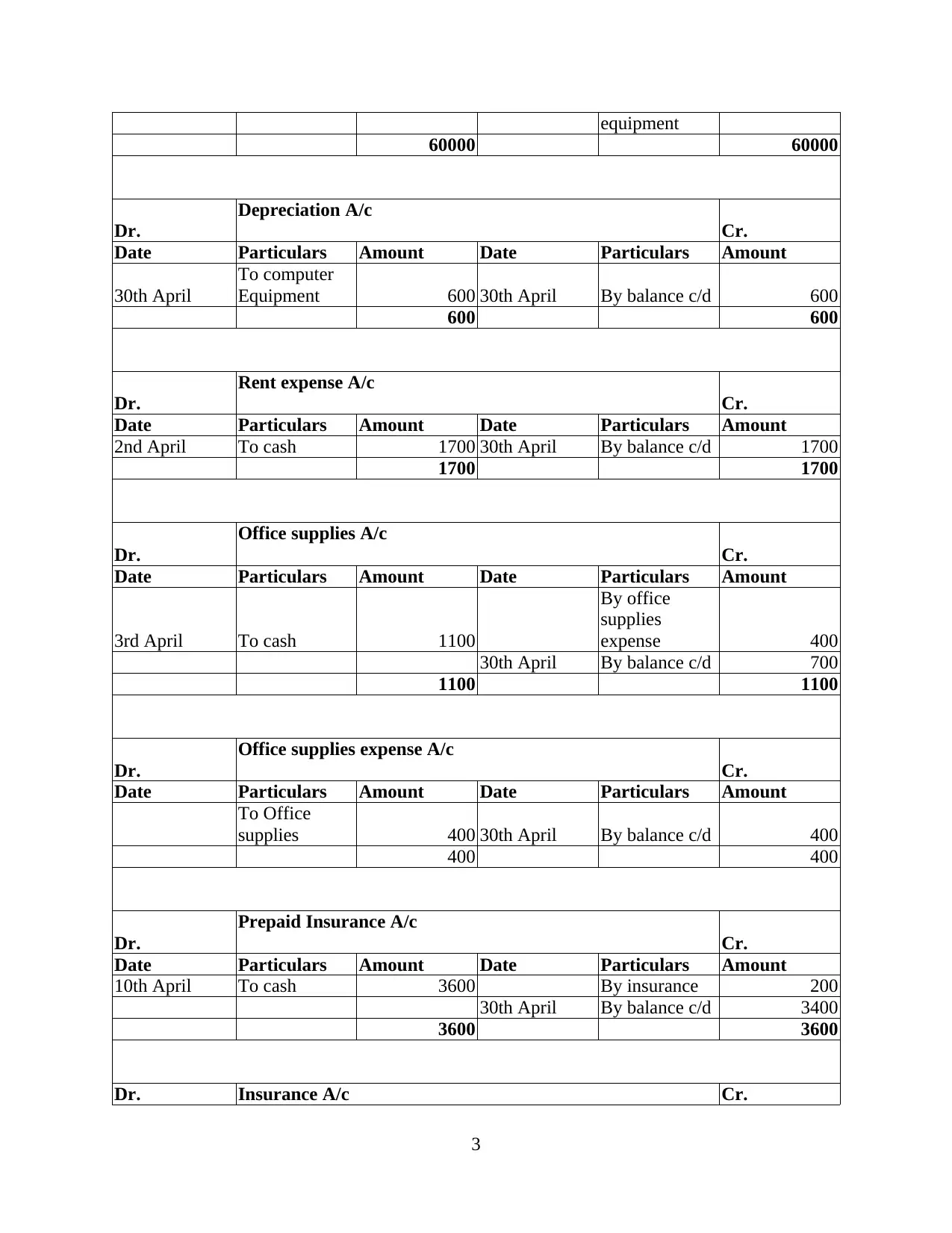

Dr.

Depreciation A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April

To computer

Equipment 600 30th April By balance c/d 600

600 600

Dr.

Rent expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

2nd April To cash 1700 30th April By balance c/d 1700

1700 1700

Dr.

Office supplies A/c

Cr.

Date Particulars Amount Date Particulars Amount

3rd April To cash 1100

By office

supplies

expense 400

30th April By balance c/d 700

1100 1100

Dr.

Office supplies expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

To Office

supplies 400 30th April By balance c/d 400

400 400

Dr.

Prepaid Insurance A/c

Cr.

Date Particulars Amount Date Particulars Amount

10th April To cash 3600 By insurance 200

30th April By balance c/d 3400

3600 3600

Dr. Insurance A/c Cr.

3

60000 60000

Dr.

Depreciation A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April

To computer

Equipment 600 30th April By balance c/d 600

600 600

Dr.

Rent expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

2nd April To cash 1700 30th April By balance c/d 1700

1700 1700

Dr.

Office supplies A/c

Cr.

Date Particulars Amount Date Particulars Amount

3rd April To cash 1100

By office

supplies

expense 400

30th April By balance c/d 700

1100 1100

Dr.

Office supplies expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

To Office

supplies 400 30th April By balance c/d 400

400 400

Dr.

Prepaid Insurance A/c

Cr.

Date Particulars Amount Date Particulars Amount

10th April To cash 3600 By insurance 200

30th April By balance c/d 3400

3600 3600

Dr. Insurance A/c Cr.

3

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

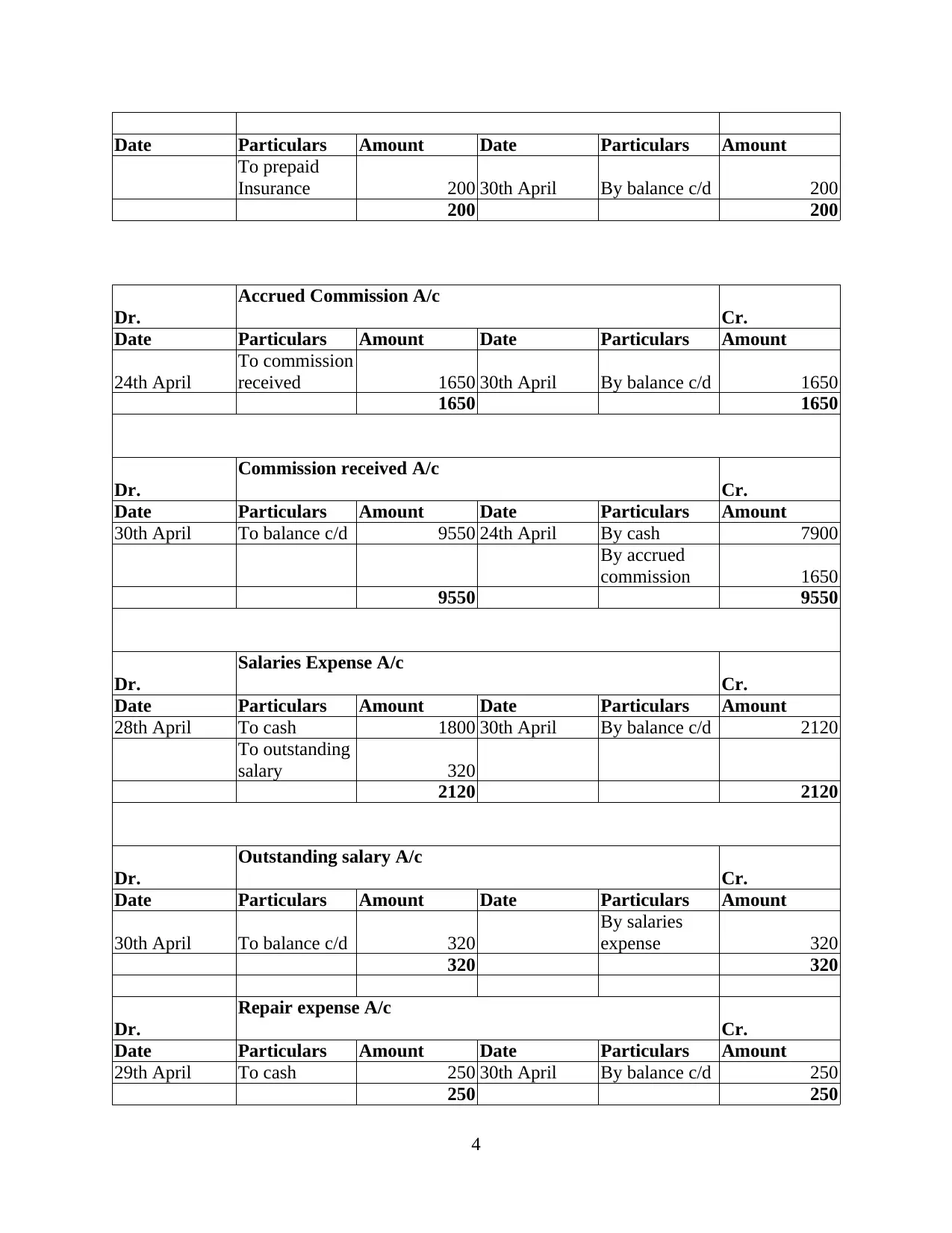

Date Particulars Amount Date Particulars Amount

To prepaid

Insurance 200 30th April By balance c/d 200

200 200

Dr.

Accrued Commission A/c

Cr.

Date Particulars Amount Date Particulars Amount

24th April

To commission

received 1650 30th April By balance c/d 1650

1650 1650

Dr.

Commission received A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To balance c/d 9550 24th April By cash 7900

By accrued

commission 1650

9550 9550

Dr.

Salaries Expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

28th April To cash 1800 30th April By balance c/d 2120

To outstanding

salary 320

2120 2120

Dr.

Outstanding salary A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To balance c/d 320

By salaries

expense 320

320 320

Dr.

Repair expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

29th April To cash 250 30th April By balance c/d 250

250 250

4

To prepaid

Insurance 200 30th April By balance c/d 200

200 200

Dr.

Accrued Commission A/c

Cr.

Date Particulars Amount Date Particulars Amount

24th April

To commission

received 1650 30th April By balance c/d 1650

1650 1650

Dr.

Commission received A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To balance c/d 9550 24th April By cash 7900

By accrued

commission 1650

9550 9550

Dr.

Salaries Expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

28th April To cash 1800 30th April By balance c/d 2120

To outstanding

salary 320

2120 2120

Dr.

Outstanding salary A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To balance c/d 320

By salaries

expense 320

320 320

Dr.

Repair expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

29th April To cash 250 30th April By balance c/d 250

250 250

4

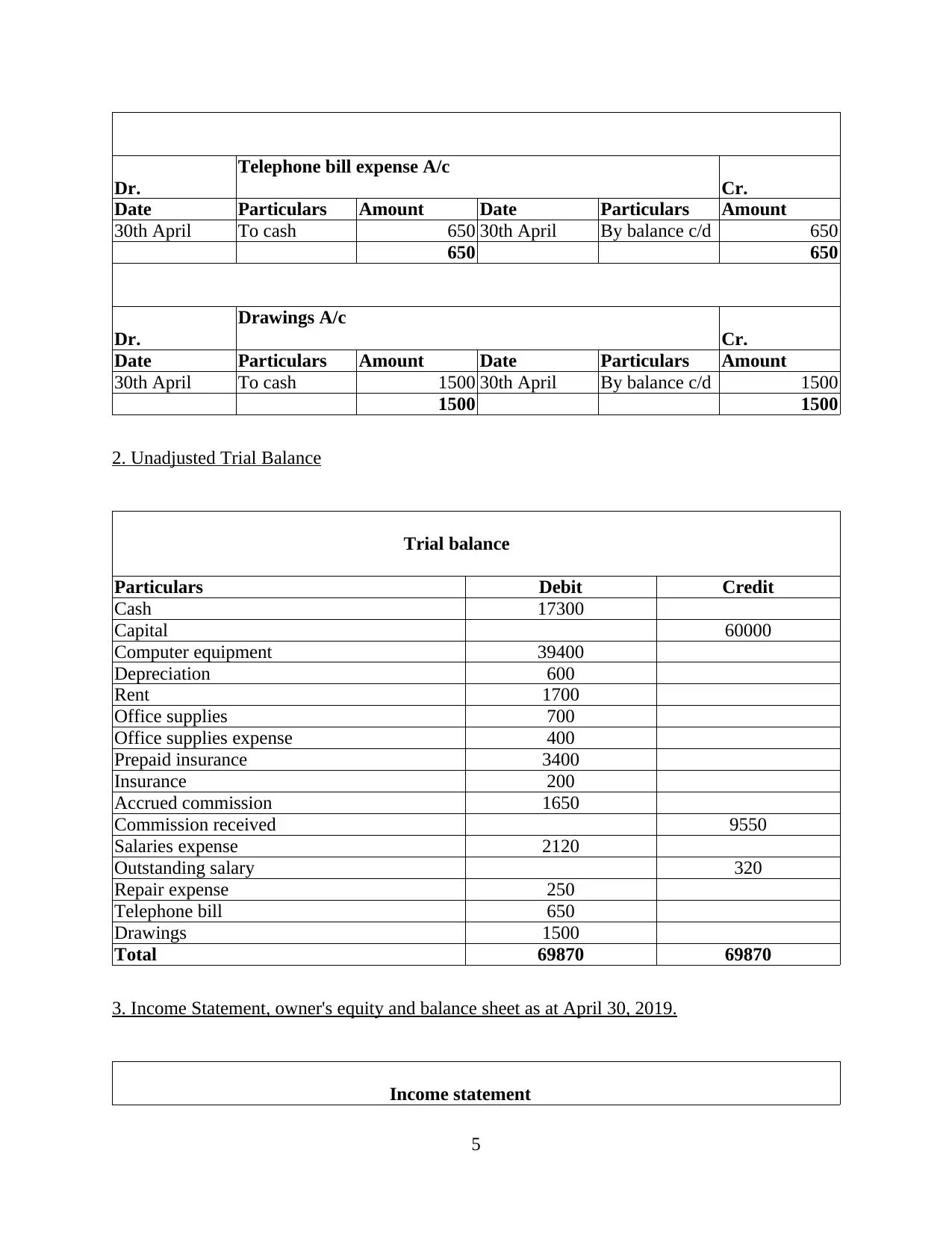

Dr.

Telephone bill expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To cash 650 30th April By balance c/d 650

650 650

Dr.

Drawings A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To cash 1500 30th April By balance c/d 1500

1500 1500

2. Unadjusted Trial Balance

Trial balance

Particulars Debit Credit

Cash 17300

Capital 60000

Computer equipment 39400

Depreciation 600

Rent 1700

Office supplies 700

Office supplies expense 400

Prepaid insurance 3400

Insurance 200

Accrued commission 1650

Commission received 9550

Salaries expense 2120

Outstanding salary 320

Repair expense 250

Telephone bill 650

Drawings 1500

Total 69870 69870

3. Income Statement, owner's equity and balance sheet as at April 30, 2019.

Income statement

5

Telephone bill expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To cash 650 30th April By balance c/d 650

650 650

Dr.

Drawings A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To cash 1500 30th April By balance c/d 1500

1500 1500

2. Unadjusted Trial Balance

Trial balance

Particulars Debit Credit

Cash 17300

Capital 60000

Computer equipment 39400

Depreciation 600

Rent 1700

Office supplies 700

Office supplies expense 400

Prepaid insurance 3400

Insurance 200

Accrued commission 1650

Commission received 9550

Salaries expense 2120

Outstanding salary 320

Repair expense 250

Telephone bill 650

Drawings 1500

Total 69870 69870

3. Income Statement, owner's equity and balance sheet as at April 30, 2019.

Income statement

5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

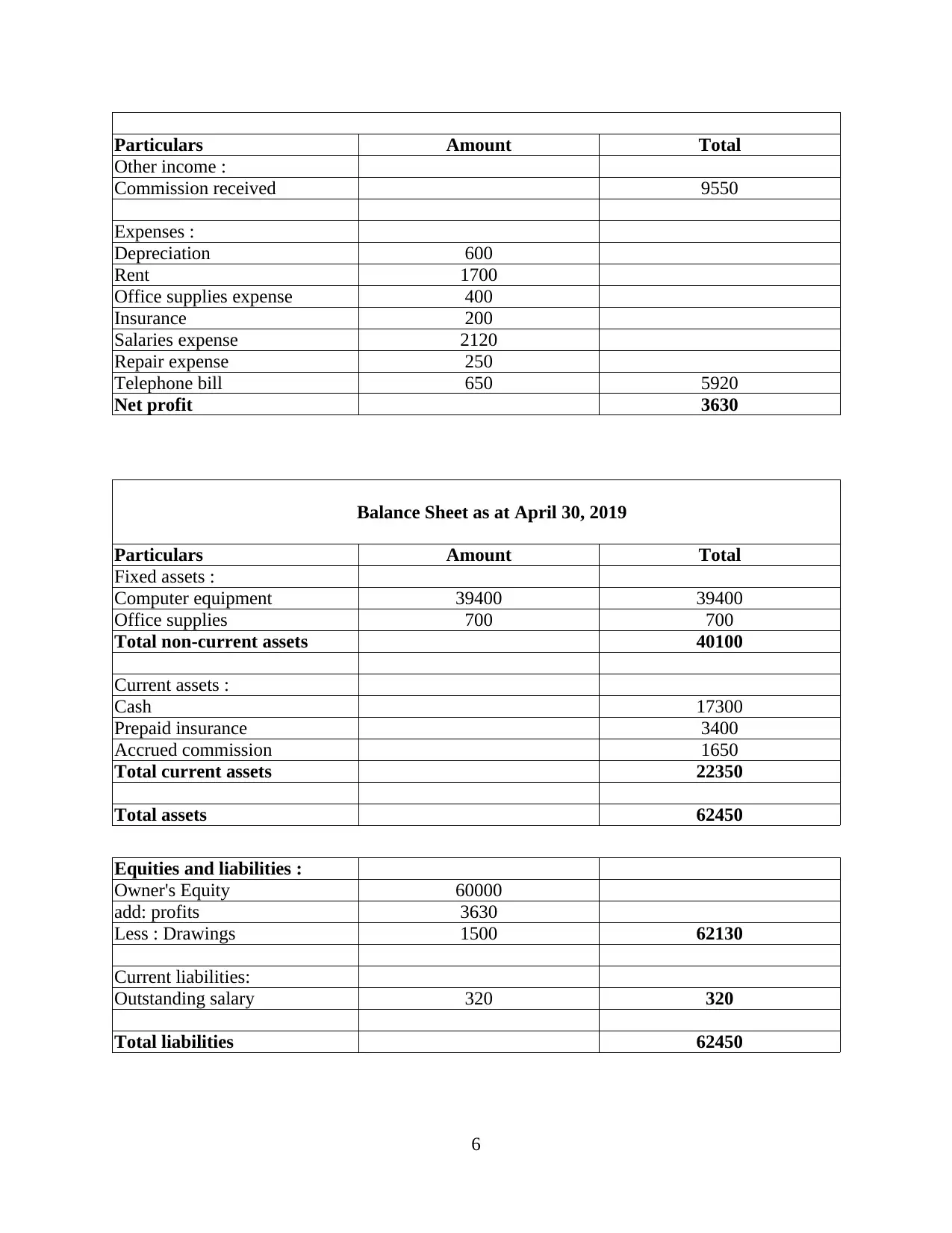

Particulars Amount Total

Other income :

Commission received 9550

Expenses :

Depreciation 600

Rent 1700

Office supplies expense 400

Insurance 200

Salaries expense 2120

Repair expense 250

Telephone bill 650 5920

Net profit 3630

Balance Sheet as at April 30, 2019

Particulars Amount Total

Fixed assets :

Computer equipment 39400 39400

Office supplies 700 700

Total non-current assets 40100

Current assets :

Cash 17300

Prepaid insurance 3400

Accrued commission 1650

Total current assets 22350

Total assets 62450

Equities and liabilities :

Owner's Equity 60000

add: profits 3630

Less : Drawings 1500 62130

Current liabilities:

Outstanding salary 320 320

Total liabilities 62450

6

Other income :

Commission received 9550

Expenses :

Depreciation 600

Rent 1700

Office supplies expense 400

Insurance 200

Salaries expense 2120

Repair expense 250

Telephone bill 650 5920

Net profit 3630

Balance Sheet as at April 30, 2019

Particulars Amount Total

Fixed assets :

Computer equipment 39400 39400

Office supplies 700 700

Total non-current assets 40100

Current assets :

Cash 17300

Prepaid insurance 3400

Accrued commission 1650

Total current assets 22350

Total assets 62450

Equities and liabilities :

Owner's Equity 60000

add: profits 3630

Less : Drawings 1500 62130

Current liabilities:

Outstanding salary 320 320

Total liabilities 62450

6

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

SECTION A2

Difference between management accounting and financial accounting

Financial Accounting

It is concerned with preparing financial statements for outside users like shareholders,

creditors, suppliers, investors, customers and many more. It is an accounting form where proper

records keeping and the financial reporting is done, for providing material and relevant

information to the users (Lento, 2016). FA are based on number of principles, assumptions and

conventions such as materiality, going concern, realisation, conservatism, accrual , historical

costs, consistency etc. Financial statements include Income statements, statements of financial

position and the Cash flow statements that are prepared using guidelines given by statues

(Financial Accounting, 2019).

Management Accounting

It is accounting for managers that helps management of company in formulating policies,

forecasting, and planning & controlling the daily business operations of company. Management

accounting analyses and captures both qualitative and quantitative informations (Collis and

Hussey, 2017). It is not limited with providing the cost and financial accounting information but

also helps management by assisting management in setting goals, budgeting, decision making fir

the business. This accounting do not have specific time frames for preparation it could be

prepared monthly, quarterly or even weekly as per the requirement of management (Thomas,

2016).

It is important to understand the differences between management and financial

accounting as both the accounting are having different path. Financial accounting deals with

aggregating accounting information into the financial statements where the management

accounting deals with the internal process used for accounting of business transactions. There are

differences between management and financial accounting.

Aggregation

Reports for results of entire business is given under financial accounting. Management

accounting have to report in detailed levels like profit per product, product line, customers and

the geographic region.

Efficiency

7

Difference between management accounting and financial accounting

Financial Accounting

It is concerned with preparing financial statements for outside users like shareholders,

creditors, suppliers, investors, customers and many more. It is an accounting form where proper

records keeping and the financial reporting is done, for providing material and relevant

information to the users (Lento, 2016). FA are based on number of principles, assumptions and

conventions such as materiality, going concern, realisation, conservatism, accrual , historical

costs, consistency etc. Financial statements include Income statements, statements of financial

position and the Cash flow statements that are prepared using guidelines given by statues

(Financial Accounting, 2019).

Management Accounting

It is accounting for managers that helps management of company in formulating policies,

forecasting, and planning & controlling the daily business operations of company. Management

accounting analyses and captures both qualitative and quantitative informations (Collis and

Hussey, 2017). It is not limited with providing the cost and financial accounting information but

also helps management by assisting management in setting goals, budgeting, decision making fir

the business. This accounting do not have specific time frames for preparation it could be

prepared monthly, quarterly or even weekly as per the requirement of management (Thomas,

2016).

It is important to understand the differences between management and financial

accounting as both the accounting are having different path. Financial accounting deals with

aggregating accounting information into the financial statements where the management

accounting deals with the internal process used for accounting of business transactions. There are

differences between management and financial accounting.

Aggregation

Reports for results of entire business is given under financial accounting. Management

accounting have to report in detailed levels like profit per product, product line, customers and

the geographic region.

Efficiency

7

Management accounting reports about the issues that are causing variations and solutions

for fixing them where the financial accounting report only over the profitability.

Proven Information

Records of financial accounting requires considerable precision for proving that financial

statements are accurate. Management accounting deals frequently with estimates than verifiable

and proven facts.

Reporting Focus

Management accounting is focused over operational reports, and are only for the internal

information of the company. Financial accounting is concerned with preparation of financial

statements that are useful for both internal and outside users (Thomas, 2016).

Standards

Management accounting is not required to comply with standards as the information is

for internal purposes where financial accounting is required to comply with number of

standards.

Time Periods

Financial accounting are concerned with financial results that the business has achieved

already, therefore it has historical orientation. Management accounting generally address

forecasts and budgets that are future oriented.

Systems

Management accounting is concerned with every bottleneck operations and different ways of

enhancing profits by resolution of bottleneck issues. Financial accounting does not give any

attention over the systems of company for generating profits but with only its outcomes.

Timings

Under financial accounting financial statements are prepared at the end of accounting

period. In management accounting reports are prepared more frequently because information

provided is important and relevant for managers.

Valuation

Financial accounting provides proper valuation of the assets & liabilities, including

revaluations , impairments and so forth where management accounting is only concerned with

their productivity and not their valuation.

8

for fixing them where the financial accounting report only over the profitability.

Proven Information

Records of financial accounting requires considerable precision for proving that financial

statements are accurate. Management accounting deals frequently with estimates than verifiable

and proven facts.

Reporting Focus

Management accounting is focused over operational reports, and are only for the internal

information of the company. Financial accounting is concerned with preparation of financial

statements that are useful for both internal and outside users (Thomas, 2016).

Standards

Management accounting is not required to comply with standards as the information is

for internal purposes where financial accounting is required to comply with number of

standards.

Time Periods

Financial accounting are concerned with financial results that the business has achieved

already, therefore it has historical orientation. Management accounting generally address

forecasts and budgets that are future oriented.

Systems

Management accounting is concerned with every bottleneck operations and different ways of

enhancing profits by resolution of bottleneck issues. Financial accounting does not give any

attention over the systems of company for generating profits but with only its outcomes.

Timings

Under financial accounting financial statements are prepared at the end of accounting

period. In management accounting reports are prepared more frequently because information

provided is important and relevant for managers.

Valuation

Financial accounting provides proper valuation of the assets & liabilities, including

revaluations , impairments and so forth where management accounting is only concerned with

their productivity and not their valuation.

8

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 22

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.