A Comparative Analysis of Financial and Management Accounting Methods

VerifiedAdded on 2023/01/11

|8

|1617

|90

Report

AI Summary

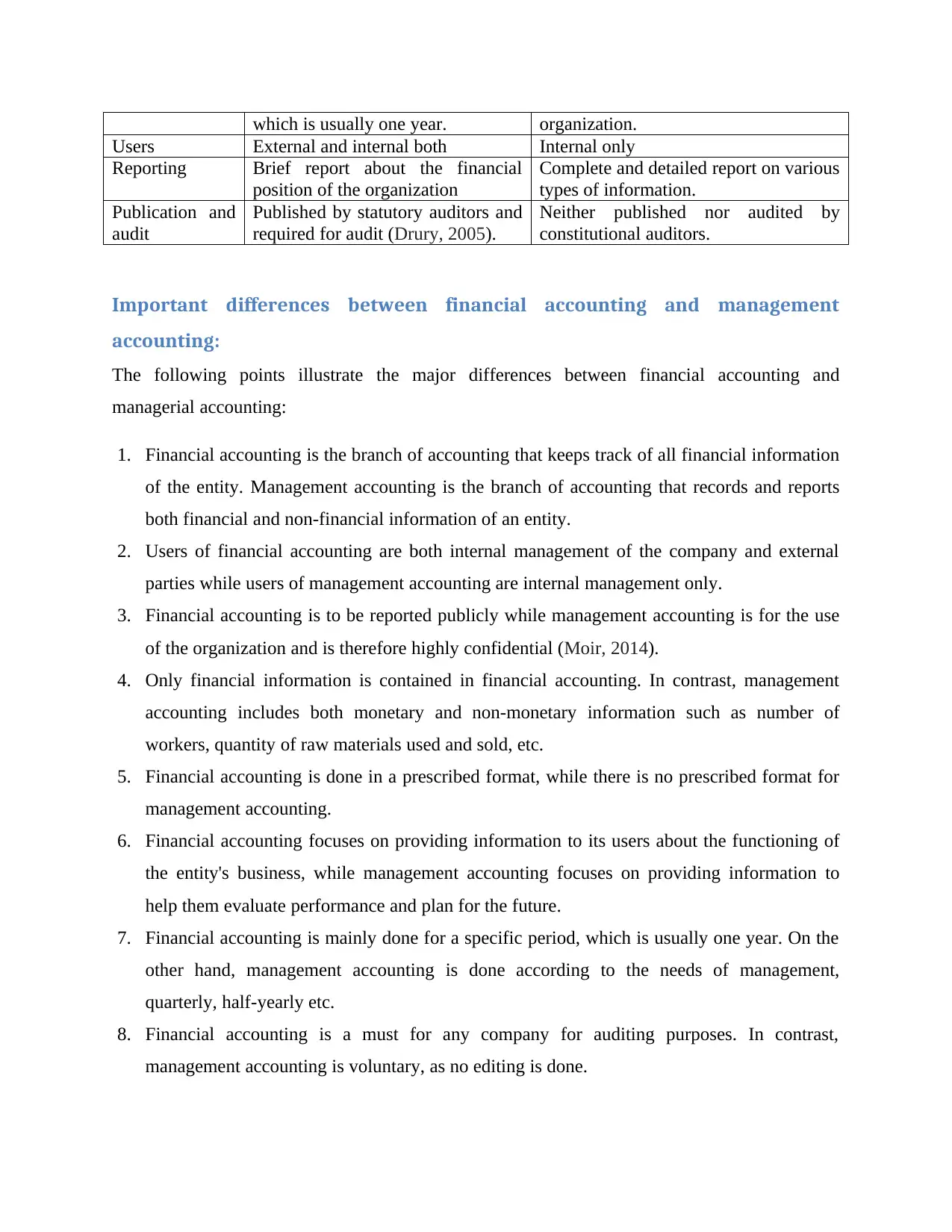

This report provides a comprehensive comparison between financial accounting and management accounting. It begins by defining both concepts and highlighting their fundamental differences, including their purposes, target audiences, and the types of information they provide. Financial accounting focuses on preparing financial statements for external stakeholders such as investors and creditors, adhering to specific accounting standards and regulations. Management accounting, on the other hand, is tailored for internal use, assisting managers in decision-making, planning, and controlling business operations. The report details the usefulness of each accounting type to both internal and external users, emphasizing how financial accounting aids in assessing overall financial performance, while management accounting supports strategic choices and operational efficiency. The conclusion underscores the importance of both accounting methods for sound financial management and organizational success, referencing various scholarly sources to support its analysis.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.