Financial & Management Accounting: Profitability, BEP & Variances

VerifiedAdded on 2023/06/11

|11

|2521

|61

Report

AI Summary

This report provides a detailed analysis of financial and management accounting concepts, focusing on Stell Co ltd's profitability, break-even point (BEP) for DK machines, and variance analysis for Concorde Constructions. The profitability analysis includes calculations of gross and net profit, along with their respective ratios, highlighting a decline in Stell Co ltd's profits and exploring the reasons behind increasing cash flow problems. The report suggests strategies to improve Stell Co ltd's financial position, such as social media marketing, recovering outstanding payments, and lowering indirect expenses. The BEP analysis computes the break-even point for DK machines using the net contribution method and discusses its importance in setting profitable revenue targets. Activity-based costing is examined for its potential to improve goal setting and monitoring. Furthermore, the report computes significant variances for Concorde Constructions, assesses their possible causes and likely consequences, and suggests strategies for their elimination or correction. Finally, it evaluates the advantages and disadvantages of switching from incremental-based budgeting to zero-based budgeting.

Financial and Management Accounting

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

QUESTION 1...................................................................................................................................3

1 Calculating Gross Profit and Net Profit...................................................................................3

2 Calculation of Gross profit and net profit ratios and its significance in profitability analysis 3

3. The reason for decline in profits and increasing cash flow problems.....................................4

4.Explaining three strategies that would be recommended to the firm to improve the financial

position........................................................................................................................................5

QUESTION 2...................................................................................................................................5

1. Computing BEP by using net contribution method ...............................................................5

2.How might break even analysis enables the company to set profitable revenues target........6

3.Explaining how activity based costing would improve ability to set and monitor goals ......7

QUESTION 3...................................................................................................................................7

1. Computing three most significant variances ..........................................................................7

2. Assessing possible causes of variances identified..................................................................8

3. Identifying projection of likely consequences for the business pertaining to each of the

variance chosen...........................................................................................................................8

4. Suggested strategies for elimination or correction of the variances ....................................9

5. Evaluation of advantages disadvantages of a switch from Incremental Based Budgeting to

Zero Based Budgeting.................................................................................................................9

REFRENCES.................................................................................................................................10

QUESTION 1...................................................................................................................................3

1 Calculating Gross Profit and Net Profit...................................................................................3

2 Calculation of Gross profit and net profit ratios and its significance in profitability analysis 3

3. The reason for decline in profits and increasing cash flow problems.....................................4

4.Explaining three strategies that would be recommended to the firm to improve the financial

position........................................................................................................................................5

QUESTION 2...................................................................................................................................5

1. Computing BEP by using net contribution method ...............................................................5

2.How might break even analysis enables the company to set profitable revenues target........6

3.Explaining how activity based costing would improve ability to set and monitor goals ......7

QUESTION 3...................................................................................................................................7

1. Computing three most significant variances ..........................................................................7

2. Assessing possible causes of variances identified..................................................................8

3. Identifying projection of likely consequences for the business pertaining to each of the

variance chosen...........................................................................................................................8

4. Suggested strategies for elimination or correction of the variances ....................................9

5. Evaluation of advantages disadvantages of a switch from Incremental Based Budgeting to

Zero Based Budgeting.................................................................................................................9

REFRENCES.................................................................................................................................10

QUESTION 1

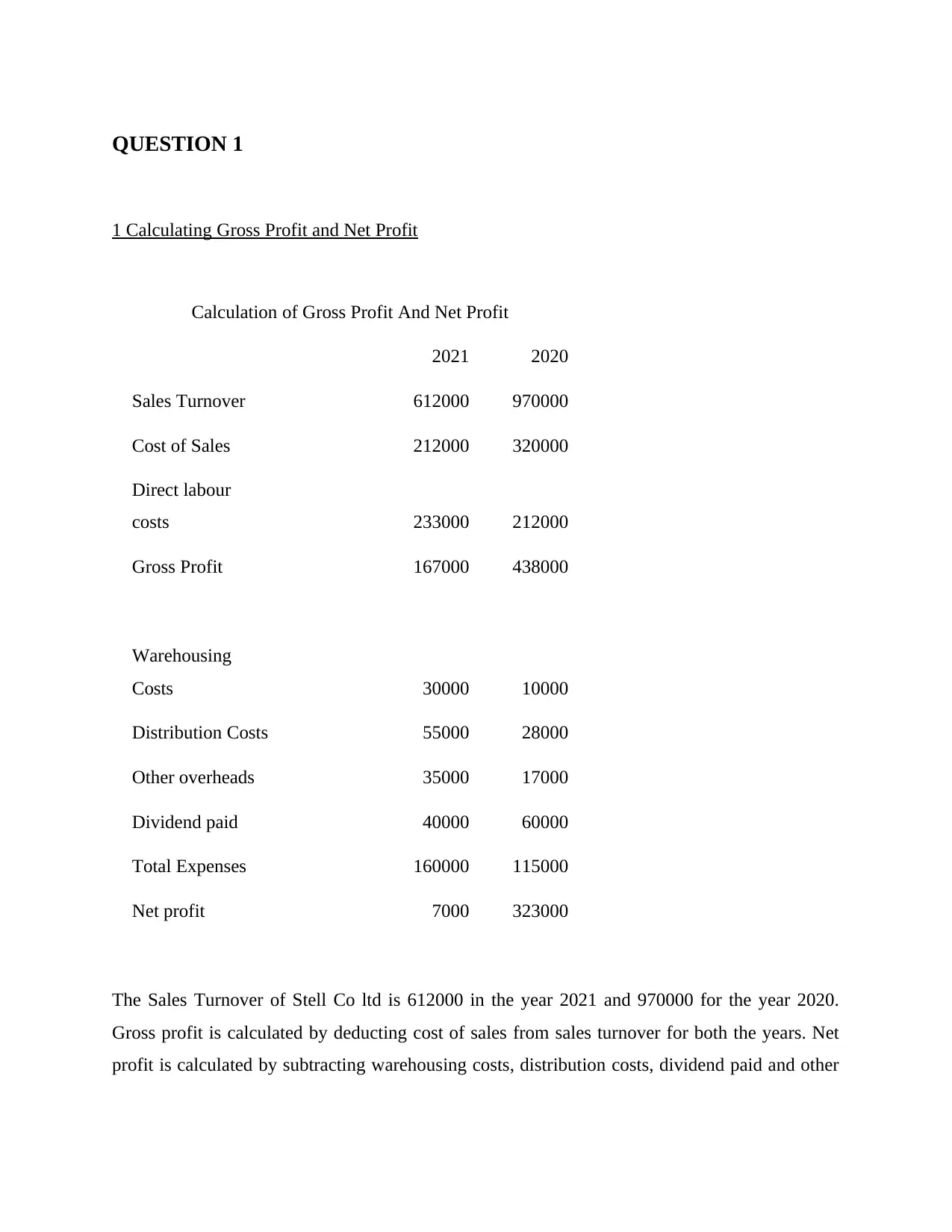

1 Calculating Gross Profit and Net Profit

Calculation of Gross Profit And Net Profit

2021 2020

Sales Turnover 612000 970000

Cost of Sales 212000 320000

Direct labour

costs 233000 212000

Gross Profit 167000 438000

Warehousing

Costs 30000 10000

Distribution Costs 55000 28000

Other overheads 35000 17000

Dividend paid 40000 60000

Total Expenses 160000 115000

Net profit 7000 323000

The Sales Turnover of Stell Co ltd is 612000 in the year 2021 and 970000 for the year 2020.

Gross profit is calculated by deducting cost of sales from sales turnover for both the years. Net

profit is calculated by subtracting warehousing costs, distribution costs, dividend paid and other

1 Calculating Gross Profit and Net Profit

Calculation of Gross Profit And Net Profit

2021 2020

Sales Turnover 612000 970000

Cost of Sales 212000 320000

Direct labour

costs 233000 212000

Gross Profit 167000 438000

Warehousing

Costs 30000 10000

Distribution Costs 55000 28000

Other overheads 35000 17000

Dividend paid 40000 60000

Total Expenses 160000 115000

Net profit 7000 323000

The Sales Turnover of Stell Co ltd is 612000 in the year 2021 and 970000 for the year 2020.

Gross profit is calculated by deducting cost of sales from sales turnover for both the years. Net

profit is calculated by subtracting warehousing costs, distribution costs, dividend paid and other

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

overheads from the gross profit. Both the gross profit and net profit of Stell Co ltd have declined

as compared to the previous year.

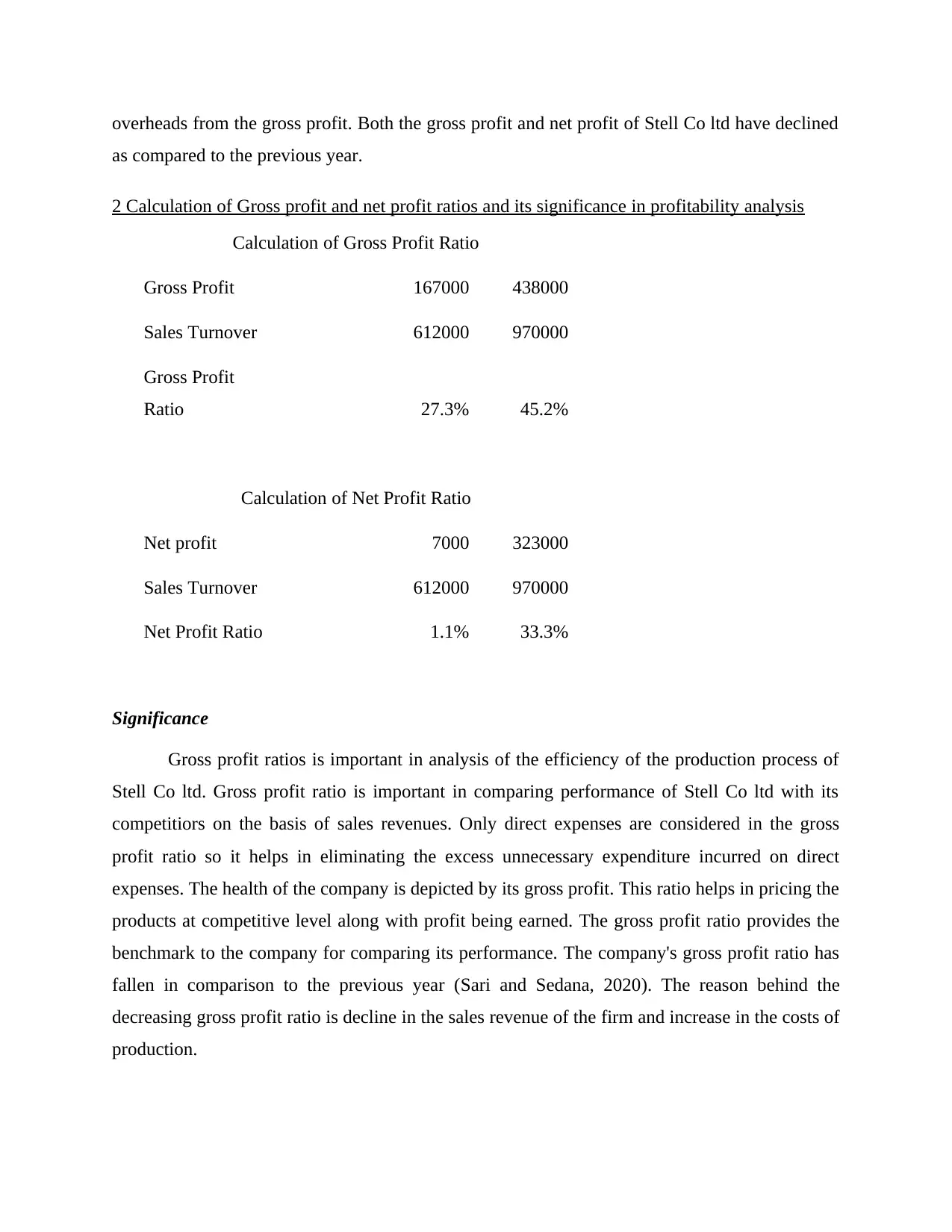

2 Calculation of Gross profit and net profit ratios and its significance in profitability analysis

Calculation of Gross Profit Ratio

Gross Profit 167000 438000

Sales Turnover 612000 970000

Gross Profit

Ratio 27.3% 45.2%

Calculation of Net Profit Ratio

Net profit 7000 323000

Sales Turnover 612000 970000

Net Profit Ratio 1.1% 33.3%

Significance

Gross profit ratios is important in analysis of the efficiency of the production process of

Stell Co ltd. Gross profit ratio is important in comparing performance of Stell Co ltd with its

competitiors on the basis of sales revenues. Only direct expenses are considered in the gross

profit ratio so it helps in eliminating the excess unnecessary expenditure incurred on direct

expenses. The health of the company is depicted by its gross profit. This ratio helps in pricing the

products at competitive level along with profit being earned. The gross profit ratio provides the

benchmark to the company for comparing its performance. The company's gross profit ratio has

fallen in comparison to the previous year (Sari and Sedana, 2020). The reason behind the

decreasing gross profit ratio is decline in the sales revenue of the firm and increase in the costs of

production.

as compared to the previous year.

2 Calculation of Gross profit and net profit ratios and its significance in profitability analysis

Calculation of Gross Profit Ratio

Gross Profit 167000 438000

Sales Turnover 612000 970000

Gross Profit

Ratio 27.3% 45.2%

Calculation of Net Profit Ratio

Net profit 7000 323000

Sales Turnover 612000 970000

Net Profit Ratio 1.1% 33.3%

Significance

Gross profit ratios is important in analysis of the efficiency of the production process of

Stell Co ltd. Gross profit ratio is important in comparing performance of Stell Co ltd with its

competitiors on the basis of sales revenues. Only direct expenses are considered in the gross

profit ratio so it helps in eliminating the excess unnecessary expenditure incurred on direct

expenses. The health of the company is depicted by its gross profit. This ratio helps in pricing the

products at competitive level along with profit being earned. The gross profit ratio provides the

benchmark to the company for comparing its performance. The company's gross profit ratio has

fallen in comparison to the previous year (Sari and Sedana, 2020). The reason behind the

decreasing gross profit ratio is decline in the sales revenue of the firm and increase in the costs of

production.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Net Profit Ratio is used in measuring the overall profitability of the Stell Co ltd. It

indicates the amount of profit earned by the firm from every pound of sales that has made by the

firm with the deduction of all the expenses that were incurred in the process to earn the revenue.

The efficiency of the company over time is indicated through net profit ratio. The net profit ratio

of the Stell Co ltd has experienced a drastic decline.

3. The reason for decline in profits and increasing cash flow problems

The reason for decline in company's profit is poor sales and increase in total expenses

incurred by the company. The reasons for increasing cash flow problems for Stell Co ltd are low

profits earned by the company. Over investment by the company for expanding on fast phase.

High overhead expenses and unexpected expenses by the company are also the main reason

behind the company's increasing cash flow problems. High dividend being distributed by the

company. The product pricing of the company may not be properly set. The financial planning of

the company is weak and company also overstock the inventories. Late payments by the

company are also the reason behind its poor cash flow. The declining profits for the company is

majorly due to its excessive expenses.

4.Explaining three strategies that would be recommended to the firm to improve the financial

position

Use of social media marketing: The firm should use more of social media marketing

channels to promote it business and services to large number of people. Furthermore, it would

also improve the asset position the company as with more funds the company would be able to

diversify its operations and generate more revenues for the business. Moreover, with the use of

the social media marketing the company would also reduce the unnecessary expenses so that

financial situation might be improved to the greater extent.

Recovering outstanding payments: The company should also focus on recovering

amounts from the unpaid invoices so that more money might be brought into the business that

would help in improving financial position. Also, at the tine of sale agreements the firm need to

know clearly about the due payment date and the terms of the overdue payments.

indicates the amount of profit earned by the firm from every pound of sales that has made by the

firm with the deduction of all the expenses that were incurred in the process to earn the revenue.

The efficiency of the company over time is indicated through net profit ratio. The net profit ratio

of the Stell Co ltd has experienced a drastic decline.

3. The reason for decline in profits and increasing cash flow problems

The reason for decline in company's profit is poor sales and increase in total expenses

incurred by the company. The reasons for increasing cash flow problems for Stell Co ltd are low

profits earned by the company. Over investment by the company for expanding on fast phase.

High overhead expenses and unexpected expenses by the company are also the main reason

behind the company's increasing cash flow problems. High dividend being distributed by the

company. The product pricing of the company may not be properly set. The financial planning of

the company is weak and company also overstock the inventories. Late payments by the

company are also the reason behind its poor cash flow. The declining profits for the company is

majorly due to its excessive expenses.

4.Explaining three strategies that would be recommended to the firm to improve the financial

position

Use of social media marketing: The firm should use more of social media marketing

channels to promote it business and services to large number of people. Furthermore, it would

also improve the asset position the company as with more funds the company would be able to

diversify its operations and generate more revenues for the business. Moreover, with the use of

the social media marketing the company would also reduce the unnecessary expenses so that

financial situation might be improved to the greater extent.

Recovering outstanding payments: The company should also focus on recovering

amounts from the unpaid invoices so that more money might be brought into the business that

would help in improving financial position. Also, at the tine of sale agreements the firm need to

know clearly about the due payment date and the terms of the overdue payments.

Lowering indirect expense : It is another strategy that might be used by the firm where

all the indirect expense that are incurred by the firm might be reduced so that financial position

is improved in the best manner and the losses might be recovered all the future undertakings.

QUESTION 2

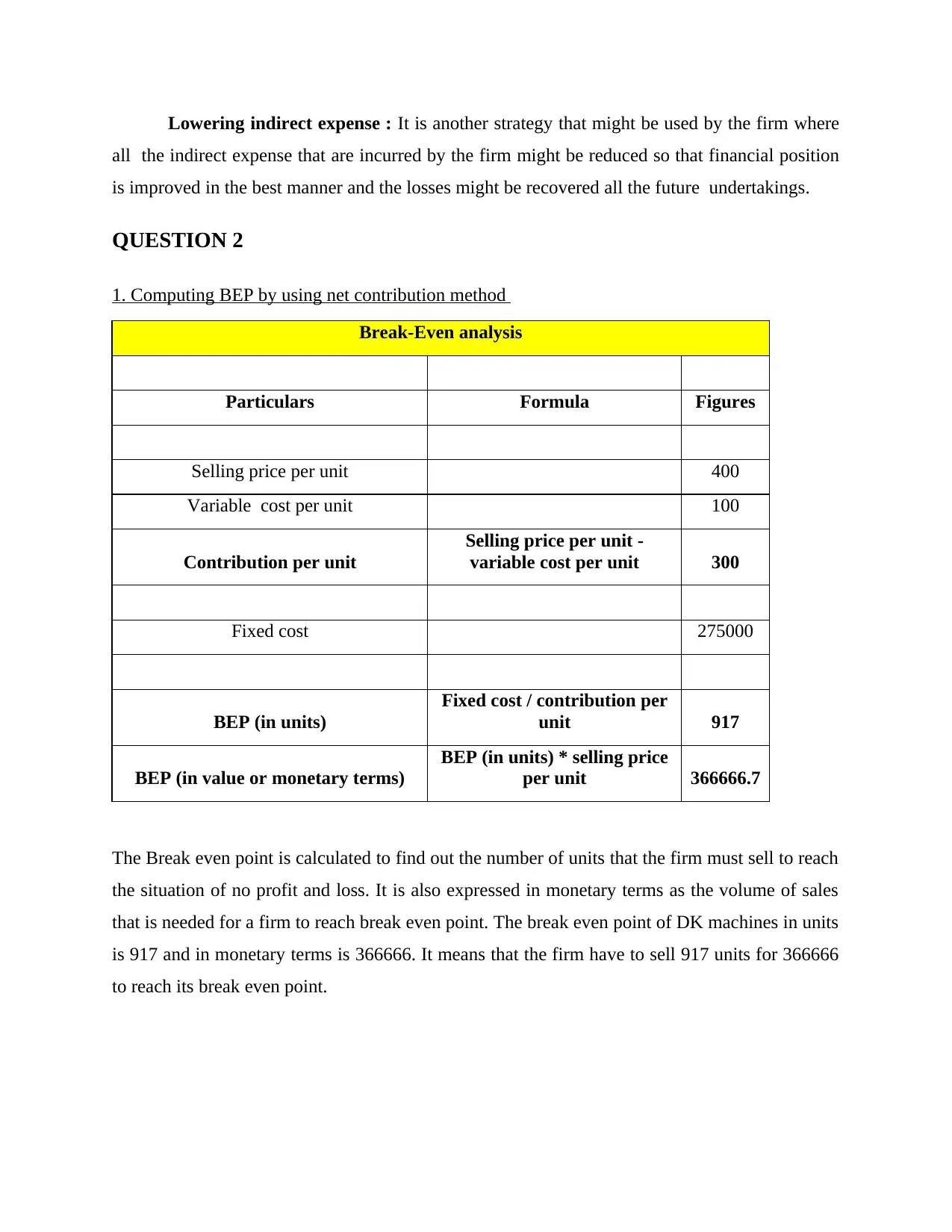

1. Computing BEP by using net contribution method

Break-Even analysis

Particulars Formula Figures

Selling price per unit 400

Variable cost per unit 100

Contribution per unit

Selling price per unit -

variable cost per unit 300

Fixed cost 275000

BEP (in units)

Fixed cost / contribution per

unit 917

BEP (in value or monetary terms)

BEP (in units) * selling price

per unit 366666.7

The Break even point is calculated to find out the number of units that the firm must sell to reach

the situation of no profit and loss. It is also expressed in monetary terms as the volume of sales

that is needed for a firm to reach break even point. The break even point of DK machines in units

is 917 and in monetary terms is 366666. It means that the firm have to sell 917 units for 366666

to reach its break even point.

all the indirect expense that are incurred by the firm might be reduced so that financial position

is improved in the best manner and the losses might be recovered all the future undertakings.

QUESTION 2

1. Computing BEP by using net contribution method

Break-Even analysis

Particulars Formula Figures

Selling price per unit 400

Variable cost per unit 100

Contribution per unit

Selling price per unit -

variable cost per unit 300

Fixed cost 275000

BEP (in units)

Fixed cost / contribution per

unit 917

BEP (in value or monetary terms)

BEP (in units) * selling price

per unit 366666.7

The Break even point is calculated to find out the number of units that the firm must sell to reach

the situation of no profit and loss. It is also expressed in monetary terms as the volume of sales

that is needed for a firm to reach break even point. The break even point of DK machines in units

is 917 and in monetary terms is 366666. It means that the firm have to sell 917 units for 366666

to reach its break even point.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2.How might break even analysis enables the company to set profitable revenues target

Break even analysis tool helps the firm in analysing the no profit and no loss situation of

the firm. Moreover, it is the best tool that help the company to set the best profitable targets in

the future through following ways:

Pricing : It is valuable technique as it shows number of products to be sold in order to make

the desired profit for the business (Sintha, 2020). Also, it helps the firm in understanding

whether it would be good decisions or not of the firm to sell particular product in the market.

Gaining funds: When the company need to collect various finances for the business than it can

said that break even analysis is very effective as it shows whether the funds would be made

easily available or not. Moreover, low break even point will ease the firm in getting the extra

debt and financing.

Helps in identifying goals: It is very useful tool as it helps in determining the precise goals for

the team. Thus, when the company had the precise goals and time frame in mind than it provide

ease for the firm to decide the revenue goals.

3.Explaining how activity based costing would improve ability to set and monitor goals

Activity based costing is very good as it allows in giving realistic and more accurate

production cost for the specific items. Thus, it helps in giving the clear understanding of

manufacturing cost and also it can be said that process of the gathering data in activity based

costing is also easier. Moreover, through this type of costing specific overhead costs might be

assigned to more expensive products . Also, this method allow the managers to assign values to

the indirect costs treating them as direct cost (Amin and Nengzih, 2021). Thus activity based

budgeting would allow managers to evaluate on things like efficient processes, management

influence and overall cost of the different departments. Moreover, activity based costing would

help the firm in getting more accurate data for the profit margins so that important decision

might be taken by the firm easily. Furthermore ,this type of costing might be used by all the

industries unlike other traditional costing methods that does not work efficiently in the

industries like services that have minimal amount of direct costs.

Break even analysis tool helps the firm in analysing the no profit and no loss situation of

the firm. Moreover, it is the best tool that help the company to set the best profitable targets in

the future through following ways:

Pricing : It is valuable technique as it shows number of products to be sold in order to make

the desired profit for the business (Sintha, 2020). Also, it helps the firm in understanding

whether it would be good decisions or not of the firm to sell particular product in the market.

Gaining funds: When the company need to collect various finances for the business than it can

said that break even analysis is very effective as it shows whether the funds would be made

easily available or not. Moreover, low break even point will ease the firm in getting the extra

debt and financing.

Helps in identifying goals: It is very useful tool as it helps in determining the precise goals for

the team. Thus, when the company had the precise goals and time frame in mind than it provide

ease for the firm to decide the revenue goals.

3.Explaining how activity based costing would improve ability to set and monitor goals

Activity based costing is very good as it allows in giving realistic and more accurate

production cost for the specific items. Thus, it helps in giving the clear understanding of

manufacturing cost and also it can be said that process of the gathering data in activity based

costing is also easier. Moreover, through this type of costing specific overhead costs might be

assigned to more expensive products . Also, this method allow the managers to assign values to

the indirect costs treating them as direct cost (Amin and Nengzih, 2021). Thus activity based

budgeting would allow managers to evaluate on things like efficient processes, management

influence and overall cost of the different departments. Moreover, activity based costing would

help the firm in getting more accurate data for the profit margins so that important decision

might be taken by the firm easily. Furthermore ,this type of costing might be used by all the

industries unlike other traditional costing methods that does not work efficiently in the

industries like services that have minimal amount of direct costs.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 3

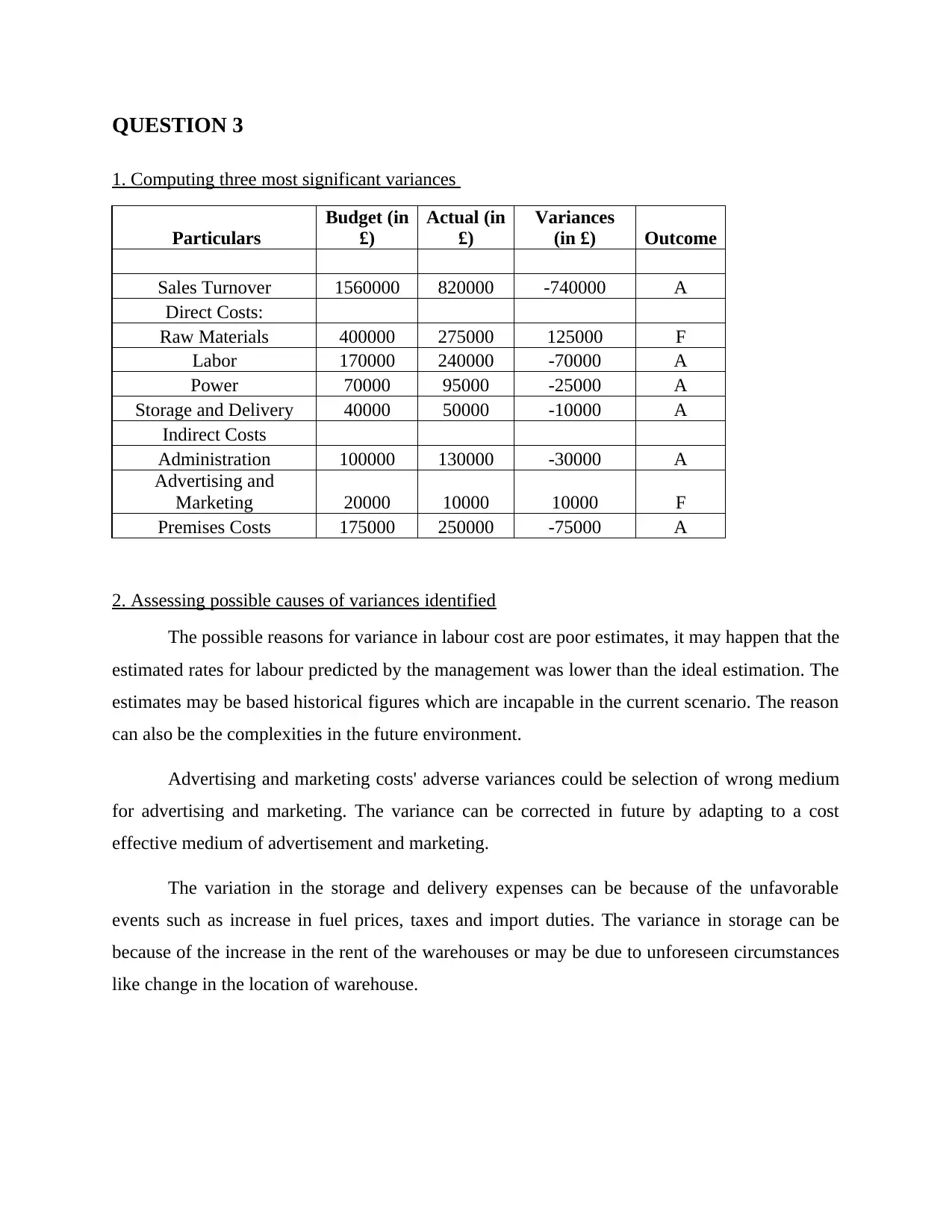

1. Computing three most significant variances

Particulars

Budget (in

£)

Actual (in

£)

Variances

(in £) Outcome

Sales Turnover 1560000 820000 -740000 A

Direct Costs:

Raw Materials 400000 275000 125000 F

Labor 170000 240000 -70000 A

Power 70000 95000 -25000 A

Storage and Delivery 40000 50000 -10000 A

Indirect Costs

Administration 100000 130000 -30000 A

Advertising and

Marketing 20000 10000 10000 F

Premises Costs 175000 250000 -75000 A

2. Assessing possible causes of variances identified

The possible reasons for variance in labour cost are poor estimates, it may happen that the

estimated rates for labour predicted by the management was lower than the ideal estimation. The

estimates may be based historical figures which are incapable in the current scenario. The reason

can also be the complexities in the future environment.

Advertising and marketing costs' adverse variances could be selection of wrong medium

for advertising and marketing. The variance can be corrected in future by adapting to a cost

effective medium of advertisement and marketing.

The variation in the storage and delivery expenses can be because of the unfavorable

events such as increase in fuel prices, taxes and import duties. The variance in storage can be

because of the increase in the rent of the warehouses or may be due to unforeseen circumstances

like change in the location of warehouse.

1. Computing three most significant variances

Particulars

Budget (in

£)

Actual (in

£)

Variances

(in £) Outcome

Sales Turnover 1560000 820000 -740000 A

Direct Costs:

Raw Materials 400000 275000 125000 F

Labor 170000 240000 -70000 A

Power 70000 95000 -25000 A

Storage and Delivery 40000 50000 -10000 A

Indirect Costs

Administration 100000 130000 -30000 A

Advertising and

Marketing 20000 10000 10000 F

Premises Costs 175000 250000 -75000 A

2. Assessing possible causes of variances identified

The possible reasons for variance in labour cost are poor estimates, it may happen that the

estimated rates for labour predicted by the management was lower than the ideal estimation. The

estimates may be based historical figures which are incapable in the current scenario. The reason

can also be the complexities in the future environment.

Advertising and marketing costs' adverse variances could be selection of wrong medium

for advertising and marketing. The variance can be corrected in future by adapting to a cost

effective medium of advertisement and marketing.

The variation in the storage and delivery expenses can be because of the unfavorable

events such as increase in fuel prices, taxes and import duties. The variance in storage can be

because of the increase in the rent of the warehouses or may be due to unforeseen circumstances

like change in the location of warehouse.

3. Identifying projection of likely consequences for the business pertaining to each of the

variance chosen

The consequences that the organization will likely suffer are that first the profits

generated by the firm will be affected negatively. Net profit is net total sales subtract total

expenses. The adverse variances in labour costs, advertising and marketing, and storage and

delivery expenses means that the actual expenses incurred on these areas is more than the

expected ones. Increase in expenses mean less profit earned by the firm. Concorde Constructions

will have less money for investment, expansion, dividend distribution purposes. Increase in

labour cost will increase the cost of services provided by the company so customers will more

likely tend towards the more cost effective alternative companies. The sales of the company will

decline. Increase in advertising and marketing costs will increase the indirect costs of the

company resulting in lower net profit.

4. Suggested strategies for elimination or correction of the variances

For above variances in labour it can be said that appropriate training and development

programs might be developed so that labour is able to acquire new skills and competencies

required to carry out the business. Furthermore, through developing the proper incentive plans

the firm would be able to retain the best quality labour within the workplace that would

achieve certain targets of the business in well defined manner reducing the variances

Moreover, in the advertising and marketing head the firm might use the cost benefit

analysis through using current costing model so that estimated growth of the business might be

analysed well in advance . Furthermore, through analysing total cost the firm might than be able

to conduct various promotional activities in the well defined manner.

Also, for storage and delivery it can be said that company should install new

technologies in the business so that faster delivery and change in operations might be done to

correct this variance.

5. Evaluation of advantages disadvantages of a switch from Incremental Based Budgeting to

Zero Based Budgeting

It there is switch from the incremental based budgeting to zero based budgeting than

major advantages is that it promotes optimization in the business process management in terms

variance chosen

The consequences that the organization will likely suffer are that first the profits

generated by the firm will be affected negatively. Net profit is net total sales subtract total

expenses. The adverse variances in labour costs, advertising and marketing, and storage and

delivery expenses means that the actual expenses incurred on these areas is more than the

expected ones. Increase in expenses mean less profit earned by the firm. Concorde Constructions

will have less money for investment, expansion, dividend distribution purposes. Increase in

labour cost will increase the cost of services provided by the company so customers will more

likely tend towards the more cost effective alternative companies. The sales of the company will

decline. Increase in advertising and marketing costs will increase the indirect costs of the

company resulting in lower net profit.

4. Suggested strategies for elimination or correction of the variances

For above variances in labour it can be said that appropriate training and development

programs might be developed so that labour is able to acquire new skills and competencies

required to carry out the business. Furthermore, through developing the proper incentive plans

the firm would be able to retain the best quality labour within the workplace that would

achieve certain targets of the business in well defined manner reducing the variances

Moreover, in the advertising and marketing head the firm might use the cost benefit

analysis through using current costing model so that estimated growth of the business might be

analysed well in advance . Furthermore, through analysing total cost the firm might than be able

to conduct various promotional activities in the well defined manner.

Also, for storage and delivery it can be said that company should install new

technologies in the business so that faster delivery and change in operations might be done to

correct this variance.

5. Evaluation of advantages disadvantages of a switch from Incremental Based Budgeting to

Zero Based Budgeting

It there is switch from the incremental based budgeting to zero based budgeting than

major advantages is that it promotes optimization in the business process management in terms

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

of efficiency, cost reductions and much more. Also, using this type budget the strategic growth

and transparency of the business is also increased through promoting the innovation and

minimising the waste of the business (Al-attara, Mashkourb and Hassanc, 2020). However ,even

though zero based budgeting is good in some aspects but the major disadvantages is that it can

be quite complex and expensive budgeting method to the company as extra training is required to

be provided by the company regarding the software , workflows etc. Also, it is resource

intensive process as it would take lot of time and effort to closely review and justify all the

budget elements. Moreover, there are higher chances that it is manipulated by the savvy

managers so that more resources might be get into the department.

and transparency of the business is also increased through promoting the innovation and

minimising the waste of the business (Al-attara, Mashkourb and Hassanc, 2020). However ,even

though zero based budgeting is good in some aspects but the major disadvantages is that it can

be quite complex and expensive budgeting method to the company as extra training is required to

be provided by the company regarding the software , workflows etc. Also, it is resource

intensive process as it would take lot of time and effort to closely review and justify all the

budget elements. Moreover, there are higher chances that it is manipulated by the savvy

managers so that more resources might be get into the department.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

REFRENCES

Al-attara, H.A., Mashkourb, S.C. and Hassanc, M.G., 2020. Zero-based budget system and its

active role in choosing the best alternative to rationalise government

spending. International Journal of Innovation, Creativity and Change. 13. pp.244-265.

Amin, M.N. and Nengzih, N., 2021. Proposed Application of the use of Activity-based

Budgeting (ABB) Method for Cost Control of Daily and Casual Workers (A Case Study

at PT XYZ). Saudi J Econ Fin. 5(9). pp.411-420.

Sari, I. A. G. D. M. and Sedana, I. B. P., 2020. Profitability and liquidity on firm value and

capital structure as intervening variable. International research journal of management,

IT and Social Sciences. 7(1). pp.116-127.

Sintha, L., 2020. Importance of Break-Even Analysis for the Micro, Small and Medium

Enterprises. International Journal of Research-Granthaalayah. 8(6).

Al-attara, H.A., Mashkourb, S.C. and Hassanc, M.G., 2020. Zero-based budget system and its

active role in choosing the best alternative to rationalise government

spending. International Journal of Innovation, Creativity and Change. 13. pp.244-265.

Amin, M.N. and Nengzih, N., 2021. Proposed Application of the use of Activity-based

Budgeting (ABB) Method for Cost Control of Daily and Casual Workers (A Case Study

at PT XYZ). Saudi J Econ Fin. 5(9). pp.411-420.

Sari, I. A. G. D. M. and Sedana, I. B. P., 2020. Profitability and liquidity on firm value and

capital structure as intervening variable. International research journal of management,

IT and Social Sciences. 7(1). pp.116-127.

Sintha, L., 2020. Importance of Break-Even Analysis for the Micro, Small and Medium

Enterprises. International Journal of Research-Granthaalayah. 8(6).

1 out of 11

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.