MA vs FA: Differences, Users of Financial Information, and Analysis

VerifiedAdded on 2023/01/11

|8

|1291

|35

Report

AI Summary

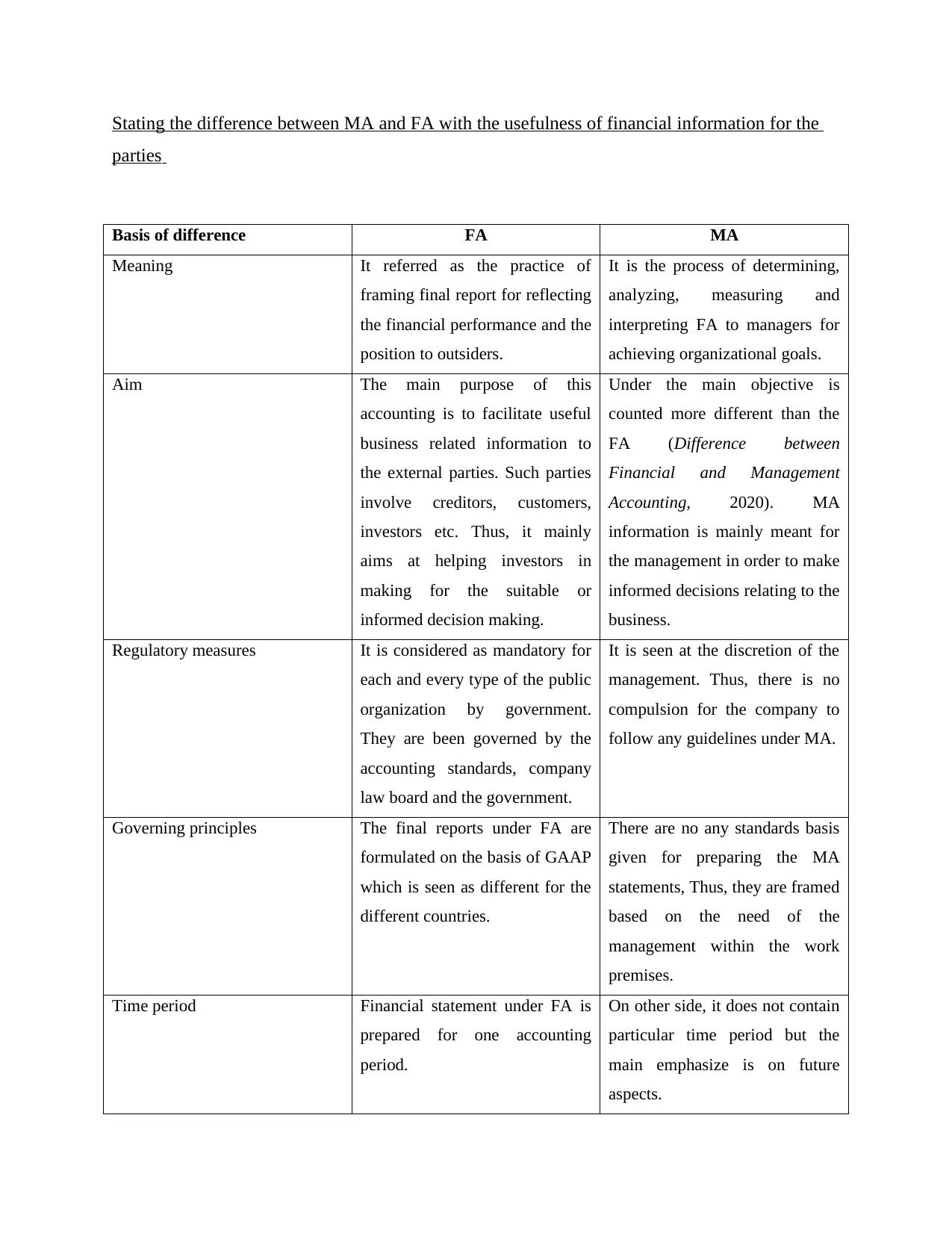

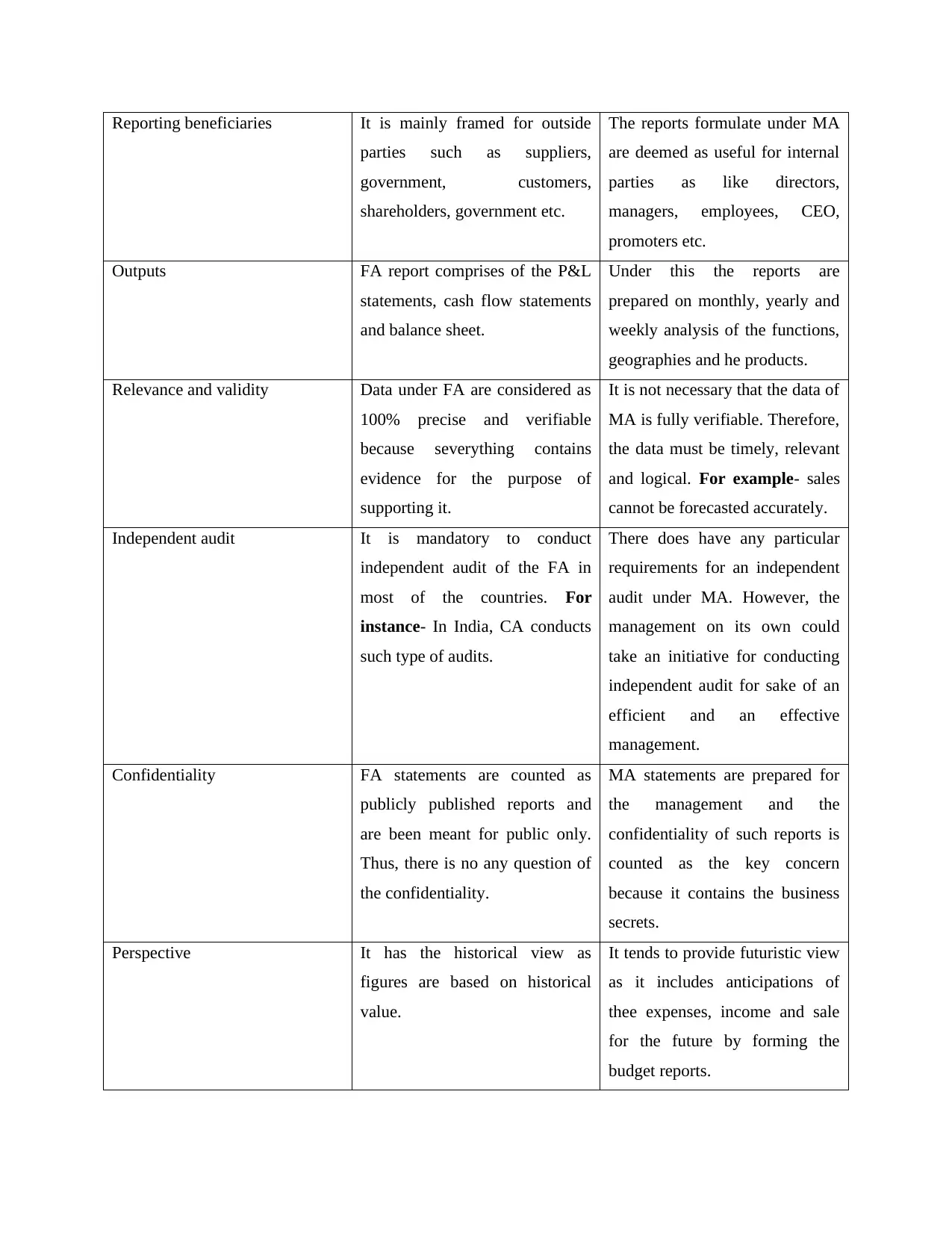

This report offers a detailed comparison between Management Accounting (MA) and Financial Accounting (FA), highlighting their fundamental differences in terms of purpose, users, governing principles, and reporting practices. Financial Accounting focuses on providing information to external stakeholders like investors, creditors, and the government, adhering to standardized accounting principles and producing reports such as the P&L statement, cash flow statements and balance sheet. Management Accounting, on the other hand, is designed for internal use by managers to aid in decision-making, with a focus on future aspects and flexibility. The report also identifies the various users of financial information, including owners, managers, banks, suppliers, investors, lenders, government agencies, and customers, explaining how each group utilizes financial data to make informed decisions. References from books and journals are included to support the analysis. The report emphasizes the importance of financial information for informed decision-making across different organizational levels and external entities.

1 out of 8

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.