Financial and Management Accounting Report for See It Now Ltd.

VerifiedAdded on 2023/01/18

|18

|3482

|98

Report

AI Summary

This report delves into the realms of financial and management accounting, offering a comprehensive analysis of their principles and applications. Section A1 meticulously details journal entries, ledger postings, and the creation of an unadjusted trial balance, culminating in the preparation of income statements, owner's equity statements, and balance sheets for See It Now Ltd. Section A2 then contrasts financial and management accounting, highlighting their differing scopes, regulatory requirements, and time horizons, while also identifying characteristics of high-quality financial information crucial for management decision-making. Section B transitions to management accounting, calculating total cost per unit under a traditional costing system, analyzing under or over absorption, and comparing profits under marginal and absorption costing. The report concludes by summarizing the key findings and emphasizing the importance of both financial and management accounting in organizational success.

ACCOUNTING

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

ABSTRACT

Report will provide understanding about the financial and management accounting. How they

are used in the organisation and their relevant importance for the organisations. It will cover

different sections for providing and understanding about the management and financial

accounting procedures. It will also cover the differences between management accounting and

financial accounting.

Report will provide understanding about the financial and management accounting. How they

are used in the organisation and their relevant importance for the organisations. It will cover

different sections for providing and understanding about the management and financial

accounting procedures. It will also cover the differences between management accounting and

financial accounting.

TABLE OF CONTENTS

ABSTRACT.....................................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION A1...................................................................................................................................1

1. Journal Entries for recording the transactions for April..........................................................1

2. Unadjusted Trial Balance as at April 30..................................................................................5

3. Income Statement, owner's equity and balance sheet as at April 30, 2019 of See It now Ltd.

......................................................................................................................................................6

SECTION A2...................................................................................................................................7

Difference between management accounting and financial accounting......................................7

Characteristic of high quality financial information to management of both companies............8

Statement describing each of the financial statements................................................................9

SECTION B...................................................................................................................................10

Total Cost per unit under traditional costing system.................................................................10

Under or Over absorption for Product B and Product C............................................................10

Profits under Marginal and Absorption costing.........................................................................10

CONCLUSION..............................................................................................................................13

ABSTRACT.....................................................................................................................................2

INTRODUCTION...........................................................................................................................1

SECTION A1...................................................................................................................................1

1. Journal Entries for recording the transactions for April..........................................................1

2. Unadjusted Trial Balance as at April 30..................................................................................5

3. Income Statement, owner's equity and balance sheet as at April 30, 2019 of See It now Ltd.

......................................................................................................................................................6

SECTION A2...................................................................................................................................7

Difference between management accounting and financial accounting......................................7

Characteristic of high quality financial information to management of both companies............8

Statement describing each of the financial statements................................................................9

SECTION B...................................................................................................................................10

Total Cost per unit under traditional costing system.................................................................10

Under or Over absorption for Product B and Product C............................................................10

Profits under Marginal and Absorption costing.........................................................................10

CONCLUSION..............................................................................................................................13

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Financial accounting refers to the specialised accounting branch that keep the track

record of each and every financial transaction of the company. Financial accounting uses

standard guidelines for recording, summarizing and presenting in financial statements or

financial reports like income statements or balance sheet (Chan, 2015). Management accounting

refers to process of providing the financial informations and resources for decision making to the

managers of the company (Bailey and Samuels, 2018). Both the accounting are different from

each other. The study will include the process followed in financial accounting and techniques

used in management costing. It will also cover the differences between the management and

financial accounting. It will be providing the characteristics of qualitative financial statement and

their importance to the management of the company. Report is divided into two sections ;

Section A covers Financial accounting and Section B covers Management accounting.

SECTION A1

1. Journal Entries for recording the transactions for April

JOURNAL ENTRIES

Date Particulars Debit Credit

1st April Cash a/c Dr. 20000

Computer Equipment a/c Dr. 40000

To capital a/c 60000

Depreciation A/c Dr. 600

To computer Equipment 600

2nd April Rent expense A/c Dr. 1700

To cash A/c 1700

3rd April Office supplies A/c Dr. 1100

To cash A/c 1100

Office supplies expense A/c Dr 400

To Office supplies 400

10th April Prepaid insurance 3600

To cash 3600

Insurance A/c Dr. 200

To prepaid Insurance 200

24th April Cash a/c Dr. 7900

Accrued commission A/c Dr. 1650

To commission received 9550

1

Financial accounting refers to the specialised accounting branch that keep the track

record of each and every financial transaction of the company. Financial accounting uses

standard guidelines for recording, summarizing and presenting in financial statements or

financial reports like income statements or balance sheet (Chan, 2015). Management accounting

refers to process of providing the financial informations and resources for decision making to the

managers of the company (Bailey and Samuels, 2018). Both the accounting are different from

each other. The study will include the process followed in financial accounting and techniques

used in management costing. It will also cover the differences between the management and

financial accounting. It will be providing the characteristics of qualitative financial statement and

their importance to the management of the company. Report is divided into two sections ;

Section A covers Financial accounting and Section B covers Management accounting.

SECTION A1

1. Journal Entries for recording the transactions for April

JOURNAL ENTRIES

Date Particulars Debit Credit

1st April Cash a/c Dr. 20000

Computer Equipment a/c Dr. 40000

To capital a/c 60000

Depreciation A/c Dr. 600

To computer Equipment 600

2nd April Rent expense A/c Dr. 1700

To cash A/c 1700

3rd April Office supplies A/c Dr. 1100

To cash A/c 1100

Office supplies expense A/c Dr 400

To Office supplies 400

10th April Prepaid insurance 3600

To cash 3600

Insurance A/c Dr. 200

To prepaid Insurance 200

24th April Cash a/c Dr. 7900

Accrued commission A/c Dr. 1650

To commission received 9550

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

28th April Salaries expense A/c Dr. 2120

To cash A/c 1800

To outstanding salary 320

29th April Repair expense 250

To cash 250

30th April Telephone bill expense A/c Dr. 650

To cash 650

30th April Drawing A/c Dr. 1500

To cash A/c 1500

81670 81670

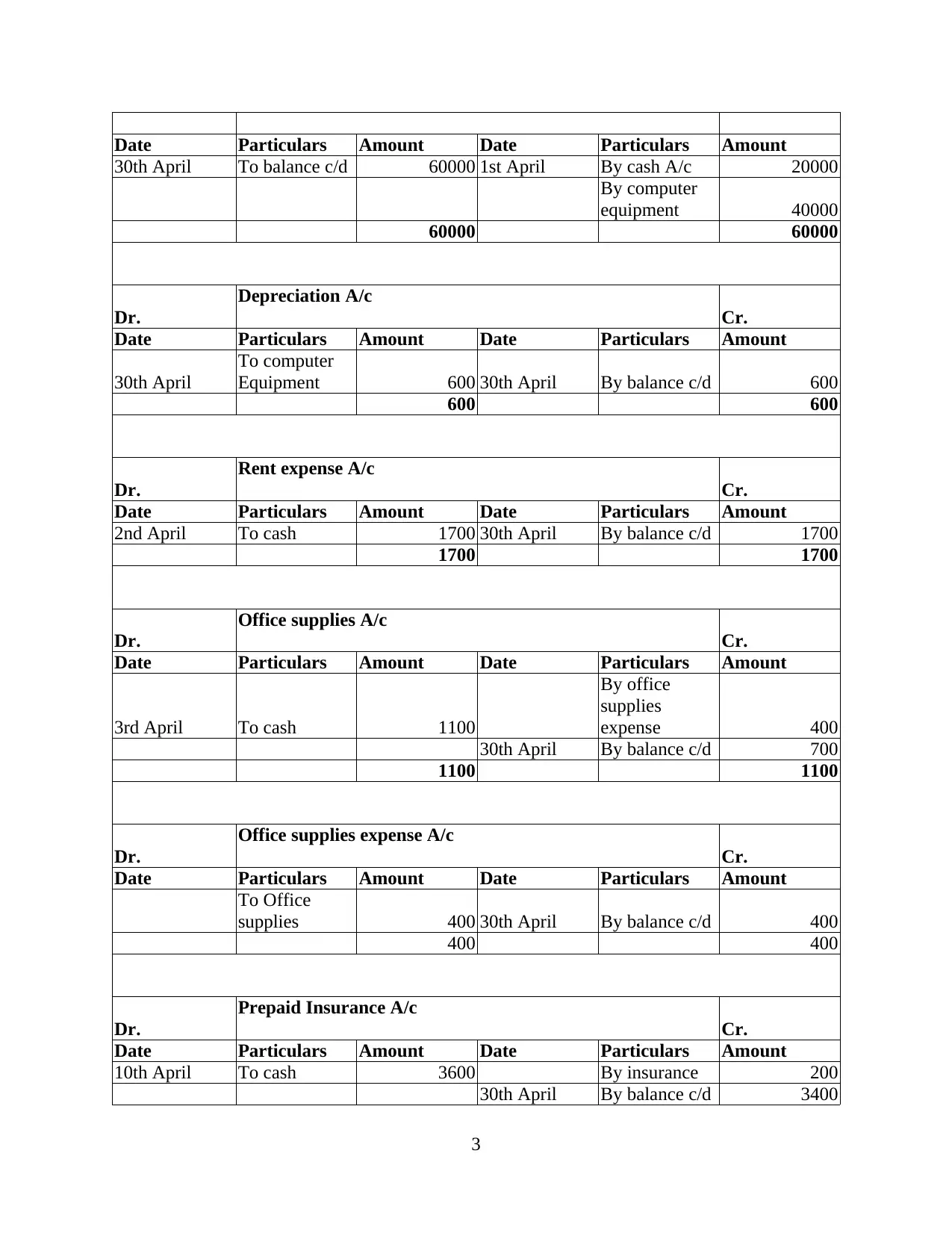

Ledger posting of the journal entries to the relevant accounts

LEDGER ACCOUNTS

Dr.

Cash a/c

Cr.

Date Particulars Amount Date Particulars Amount

1st April To capital 20000 2nd April

By rent

expense 1700

24th April

To commission

received 7900 3rd April

By office

supplies 1100

10th April

By prepaid

insurance 3600

28th April By salaries 1800

29th April

By repair

expense 250

30th April

By telephone

bill expense 650

30th April By Drawings 1500

30th April By balance c/d 17300

27900 27900

Dr.

Computer equipment A/c

Cr.

Date Particulars Amount Date Particulars Amount

1st April To capital 40000 30th April

By

depreciation 600

30th April By balance c/d 39400

40000 40000

Dr. Capital A/c Cr.

2

To cash A/c 1800

To outstanding salary 320

29th April Repair expense 250

To cash 250

30th April Telephone bill expense A/c Dr. 650

To cash 650

30th April Drawing A/c Dr. 1500

To cash A/c 1500

81670 81670

Ledger posting of the journal entries to the relevant accounts

LEDGER ACCOUNTS

Dr.

Cash a/c

Cr.

Date Particulars Amount Date Particulars Amount

1st April To capital 20000 2nd April

By rent

expense 1700

24th April

To commission

received 7900 3rd April

By office

supplies 1100

10th April

By prepaid

insurance 3600

28th April By salaries 1800

29th April

By repair

expense 250

30th April

By telephone

bill expense 650

30th April By Drawings 1500

30th April By balance c/d 17300

27900 27900

Dr.

Computer equipment A/c

Cr.

Date Particulars Amount Date Particulars Amount

1st April To capital 40000 30th April

By

depreciation 600

30th April By balance c/d 39400

40000 40000

Dr. Capital A/c Cr.

2

Date Particulars Amount Date Particulars Amount

30th April To balance c/d 60000 1st April By cash A/c 20000

By computer

equipment 40000

60000 60000

Dr.

Depreciation A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April

To computer

Equipment 600 30th April By balance c/d 600

600 600

Dr.

Rent expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

2nd April To cash 1700 30th April By balance c/d 1700

1700 1700

Dr.

Office supplies A/c

Cr.

Date Particulars Amount Date Particulars Amount

3rd April To cash 1100

By office

supplies

expense 400

30th April By balance c/d 700

1100 1100

Dr.

Office supplies expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

To Office

supplies 400 30th April By balance c/d 400

400 400

Dr.

Prepaid Insurance A/c

Cr.

Date Particulars Amount Date Particulars Amount

10th April To cash 3600 By insurance 200

30th April By balance c/d 3400

3

30th April To balance c/d 60000 1st April By cash A/c 20000

By computer

equipment 40000

60000 60000

Dr.

Depreciation A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April

To computer

Equipment 600 30th April By balance c/d 600

600 600

Dr.

Rent expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

2nd April To cash 1700 30th April By balance c/d 1700

1700 1700

Dr.

Office supplies A/c

Cr.

Date Particulars Amount Date Particulars Amount

3rd April To cash 1100

By office

supplies

expense 400

30th April By balance c/d 700

1100 1100

Dr.

Office supplies expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

To Office

supplies 400 30th April By balance c/d 400

400 400

Dr.

Prepaid Insurance A/c

Cr.

Date Particulars Amount Date Particulars Amount

10th April To cash 3600 By insurance 200

30th April By balance c/d 3400

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

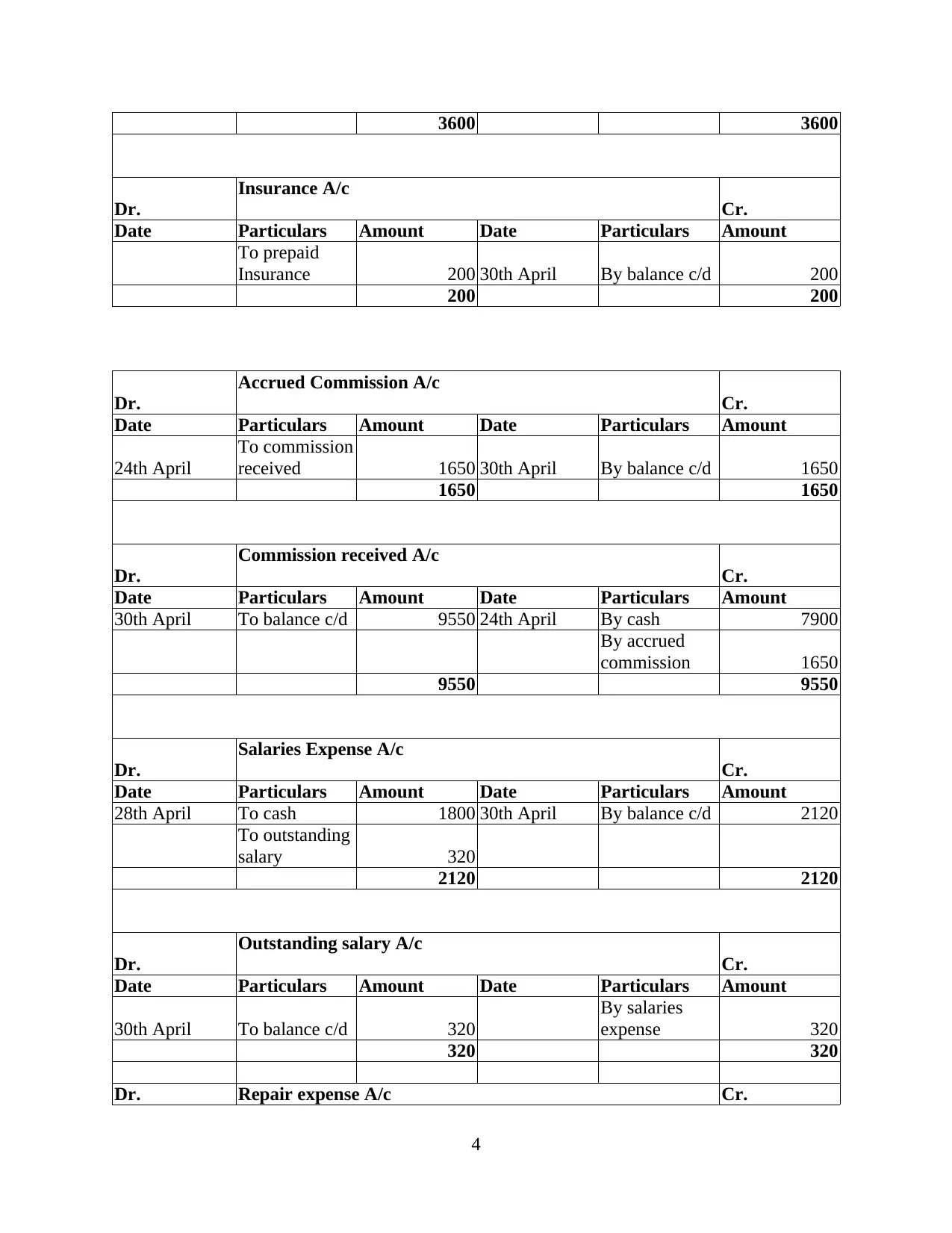

3600 3600

Dr.

Insurance A/c

Cr.

Date Particulars Amount Date Particulars Amount

To prepaid

Insurance 200 30th April By balance c/d 200

200 200

Dr.

Accrued Commission A/c

Cr.

Date Particulars Amount Date Particulars Amount

24th April

To commission

received 1650 30th April By balance c/d 1650

1650 1650

Dr.

Commission received A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To balance c/d 9550 24th April By cash 7900

By accrued

commission 1650

9550 9550

Dr.

Salaries Expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

28th April To cash 1800 30th April By balance c/d 2120

To outstanding

salary 320

2120 2120

Dr.

Outstanding salary A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To balance c/d 320

By salaries

expense 320

320 320

Dr. Repair expense A/c Cr.

4

Dr.

Insurance A/c

Cr.

Date Particulars Amount Date Particulars Amount

To prepaid

Insurance 200 30th April By balance c/d 200

200 200

Dr.

Accrued Commission A/c

Cr.

Date Particulars Amount Date Particulars Amount

24th April

To commission

received 1650 30th April By balance c/d 1650

1650 1650

Dr.

Commission received A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To balance c/d 9550 24th April By cash 7900

By accrued

commission 1650

9550 9550

Dr.

Salaries Expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

28th April To cash 1800 30th April By balance c/d 2120

To outstanding

salary 320

2120 2120

Dr.

Outstanding salary A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To balance c/d 320

By salaries

expense 320

320 320

Dr. Repair expense A/c Cr.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Date Particulars Amount Date Particulars Amount

29th April To cash 250 30th April By balance c/d 250

250 250

Dr.

Telephone bill expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To cash 650 30th April By balance c/d 650

650 650

Dr.

Drawings A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To cash 1500 30th April By balance c/d 1500

1500 1500

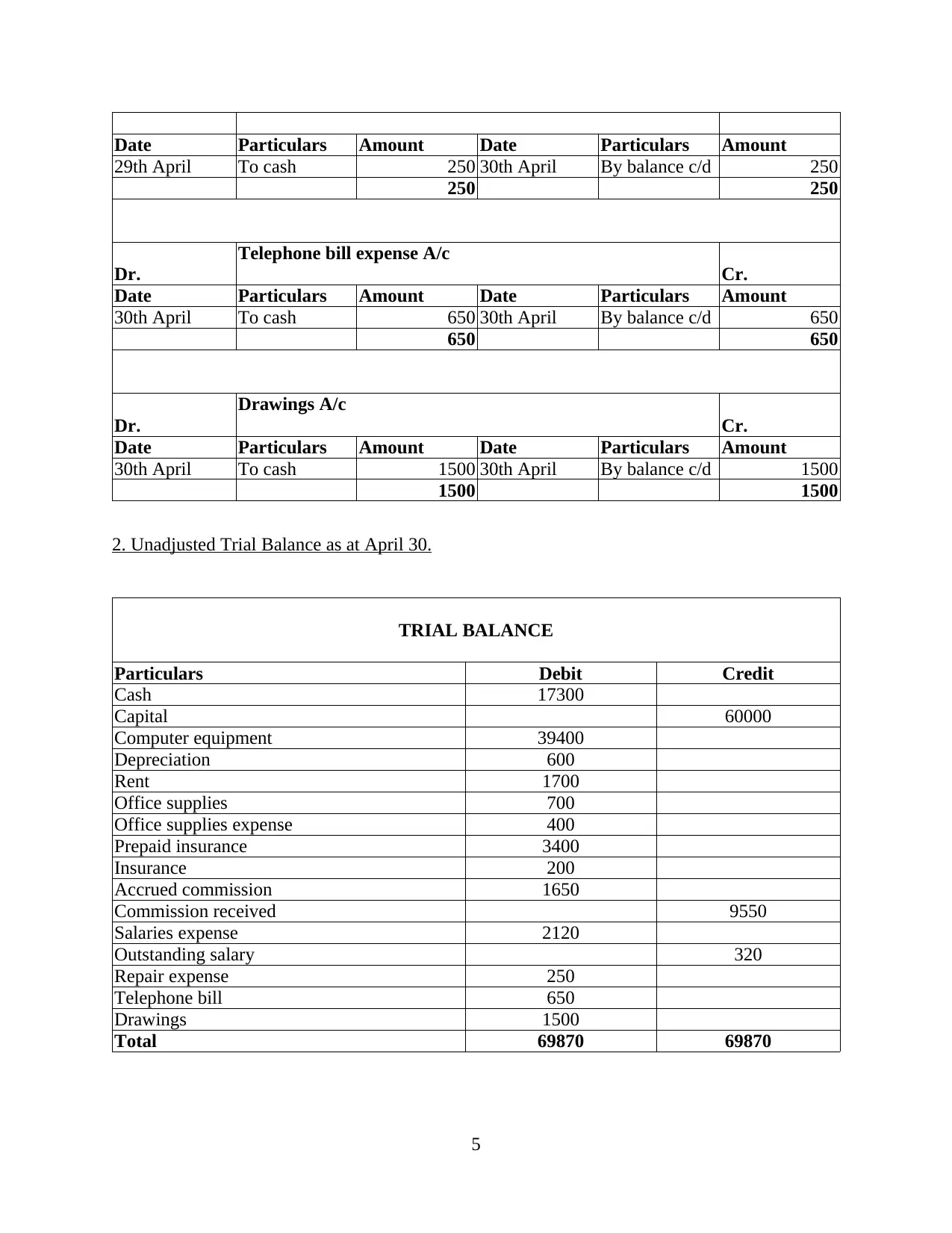

2. Unadjusted Trial Balance as at April 30.

TRIAL BALANCE

Particulars Debit Credit

Cash 17300

Capital 60000

Computer equipment 39400

Depreciation 600

Rent 1700

Office supplies 700

Office supplies expense 400

Prepaid insurance 3400

Insurance 200

Accrued commission 1650

Commission received 9550

Salaries expense 2120

Outstanding salary 320

Repair expense 250

Telephone bill 650

Drawings 1500

Total 69870 69870

5

29th April To cash 250 30th April By balance c/d 250

250 250

Dr.

Telephone bill expense A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To cash 650 30th April By balance c/d 650

650 650

Dr.

Drawings A/c

Cr.

Date Particulars Amount Date Particulars Amount

30th April To cash 1500 30th April By balance c/d 1500

1500 1500

2. Unadjusted Trial Balance as at April 30.

TRIAL BALANCE

Particulars Debit Credit

Cash 17300

Capital 60000

Computer equipment 39400

Depreciation 600

Rent 1700

Office supplies 700

Office supplies expense 400

Prepaid insurance 3400

Insurance 200

Accrued commission 1650

Commission received 9550

Salaries expense 2120

Outstanding salary 320

Repair expense 250

Telephone bill 650

Drawings 1500

Total 69870 69870

5

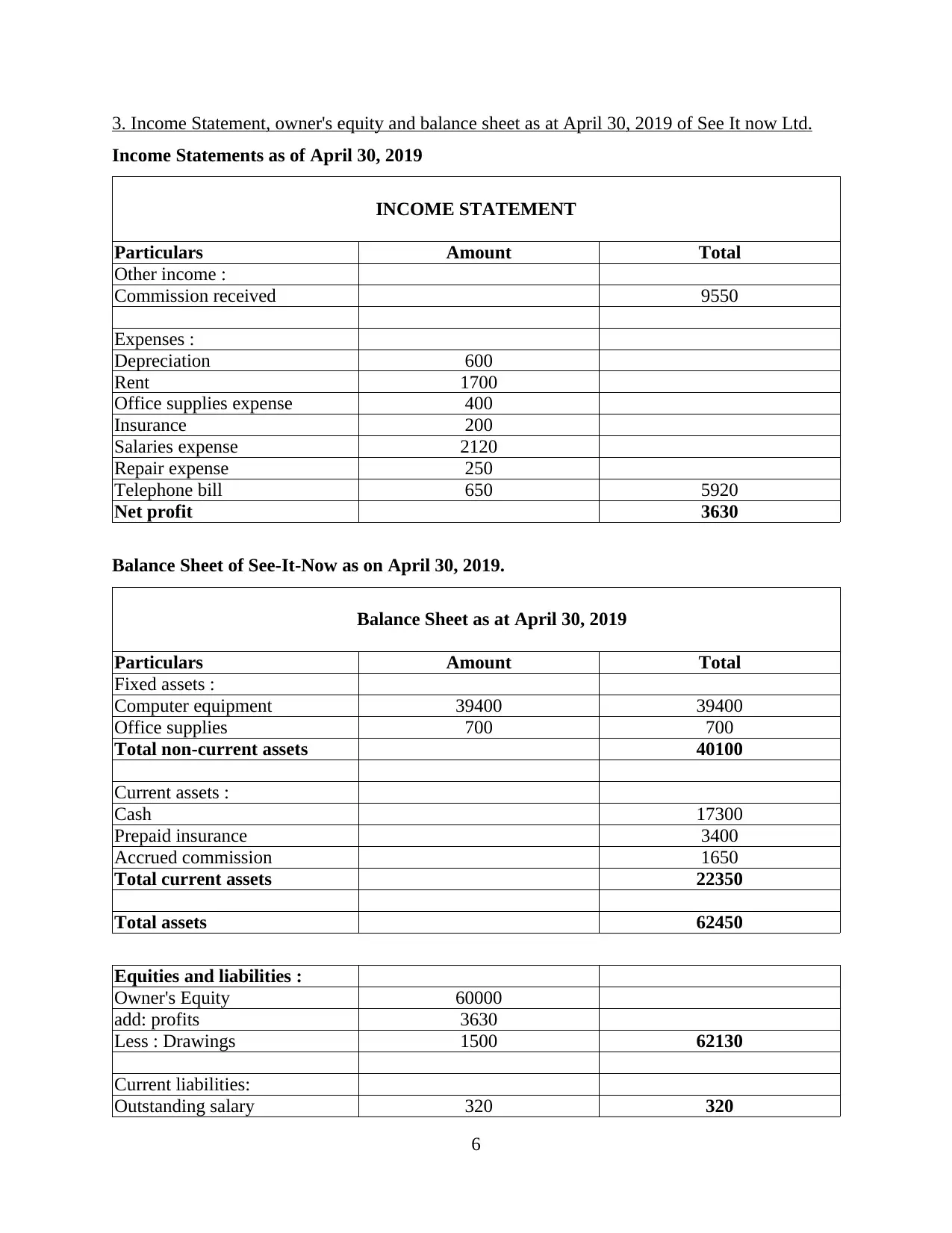

3. Income Statement, owner's equity and balance sheet as at April 30, 2019 of See It now Ltd.

Income Statements as of April 30, 2019

INCOME STATEMENT

Particulars Amount Total

Other income :

Commission received 9550

Expenses :

Depreciation 600

Rent 1700

Office supplies expense 400

Insurance 200

Salaries expense 2120

Repair expense 250

Telephone bill 650 5920

Net profit 3630

Balance Sheet of See-It-Now as on April 30, 2019.

Balance Sheet as at April 30, 2019

Particulars Amount Total

Fixed assets :

Computer equipment 39400 39400

Office supplies 700 700

Total non-current assets 40100

Current assets :

Cash 17300

Prepaid insurance 3400

Accrued commission 1650

Total current assets 22350

Total assets 62450

Equities and liabilities :

Owner's Equity 60000

add: profits 3630

Less : Drawings 1500 62130

Current liabilities:

Outstanding salary 320 320

6

Income Statements as of April 30, 2019

INCOME STATEMENT

Particulars Amount Total

Other income :

Commission received 9550

Expenses :

Depreciation 600

Rent 1700

Office supplies expense 400

Insurance 200

Salaries expense 2120

Repair expense 250

Telephone bill 650 5920

Net profit 3630

Balance Sheet of See-It-Now as on April 30, 2019.

Balance Sheet as at April 30, 2019

Particulars Amount Total

Fixed assets :

Computer equipment 39400 39400

Office supplies 700 700

Total non-current assets 40100

Current assets :

Cash 17300

Prepaid insurance 3400

Accrued commission 1650

Total current assets 22350

Total assets 62450

Equities and liabilities :

Owner's Equity 60000

add: profits 3630

Less : Drawings 1500 62130

Current liabilities:

Outstanding salary 320 320

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

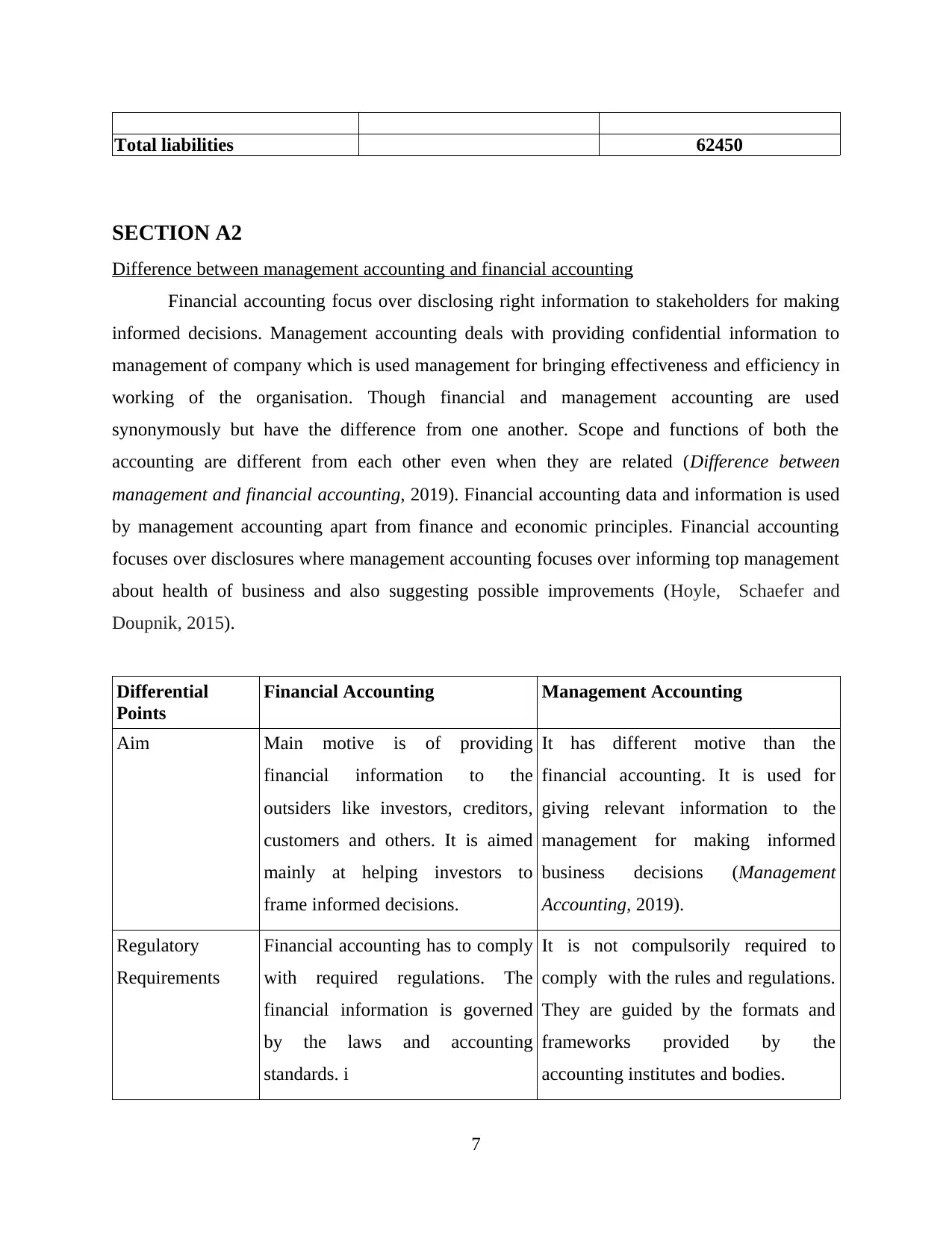

Total liabilities 62450

SECTION A2

Difference between management accounting and financial accounting

Financial accounting focus over disclosing right information to stakeholders for making

informed decisions. Management accounting deals with providing confidential information to

management of company which is used management for bringing effectiveness and efficiency in

working of the organisation. Though financial and management accounting are used

synonymously but have the difference from one another. Scope and functions of both the

accounting are different from each other even when they are related (Difference between

management and financial accounting, 2019). Financial accounting data and information is used

by management accounting apart from finance and economic principles. Financial accounting

focuses over disclosures where management accounting focuses over informing top management

about health of business and also suggesting possible improvements (Hoyle, Schaefer and

Doupnik, 2015).

Differential

Points

Financial Accounting Management Accounting

Aim Main motive is of providing

financial information to the

outsiders like investors, creditors,

customers and others. It is aimed

mainly at helping investors to

frame informed decisions.

It has different motive than the

financial accounting. It is used for

giving relevant information to the

management for making informed

business decisions (Management

Accounting, 2019).

Regulatory

Requirements

Financial accounting has to comply

with required regulations. The

financial information is governed

by the laws and accounting

standards. i

It is not compulsorily required to

comply with the rules and regulations.

They are guided by the formats and

frameworks provided by the

accounting institutes and bodies.

7

SECTION A2

Difference between management accounting and financial accounting

Financial accounting focus over disclosing right information to stakeholders for making

informed decisions. Management accounting deals with providing confidential information to

management of company which is used management for bringing effectiveness and efficiency in

working of the organisation. Though financial and management accounting are used

synonymously but have the difference from one another. Scope and functions of both the

accounting are different from each other even when they are related (Difference between

management and financial accounting, 2019). Financial accounting data and information is used

by management accounting apart from finance and economic principles. Financial accounting

focuses over disclosures where management accounting focuses over informing top management

about health of business and also suggesting possible improvements (Hoyle, Schaefer and

Doupnik, 2015).

Differential

Points

Financial Accounting Management Accounting

Aim Main motive is of providing

financial information to the

outsiders like investors, creditors,

customers and others. It is aimed

mainly at helping investors to

frame informed decisions.

It has different motive than the

financial accounting. It is used for

giving relevant information to the

management for making informed

business decisions (Management

Accounting, 2019).

Regulatory

Requirements

Financial accounting has to comply

with required regulations. The

financial information is governed

by the laws and accounting

standards. i

It is not compulsorily required to

comply with the rules and regulations.

They are guided by the formats and

frameworks provided by the

accounting institutes and bodies.

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

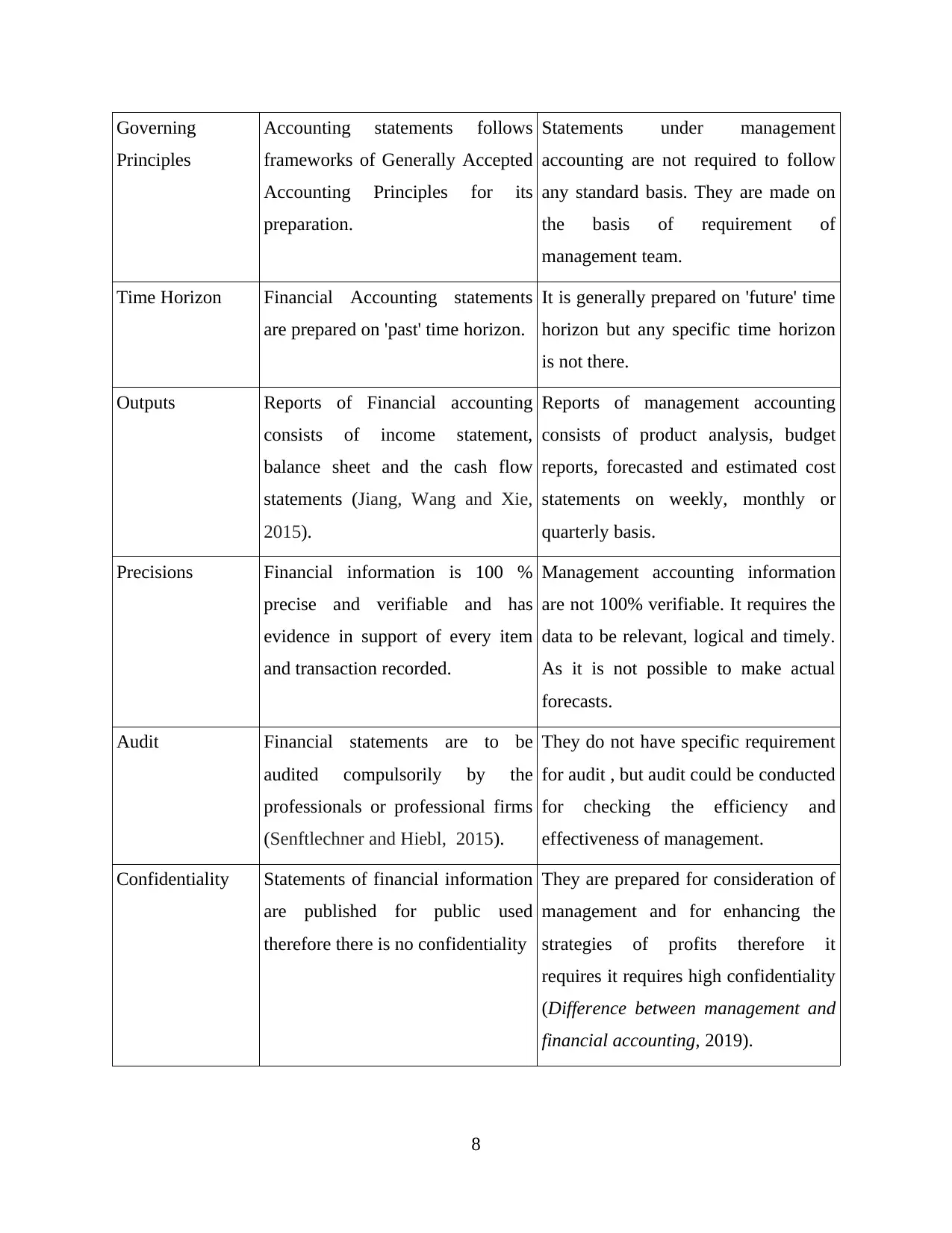

Governing

Principles

Accounting statements follows

frameworks of Generally Accepted

Accounting Principles for its

preparation.

Statements under management

accounting are not required to follow

any standard basis. They are made on

the basis of requirement of

management team.

Time Horizon Financial Accounting statements

are prepared on 'past' time horizon.

It is generally prepared on 'future' time

horizon but any specific time horizon

is not there.

Outputs Reports of Financial accounting

consists of income statement,

balance sheet and the cash flow

statements (Jiang, Wang and Xie,

2015).

Reports of management accounting

consists of product analysis, budget

reports, forecasted and estimated cost

statements on weekly, monthly or

quarterly basis.

Precisions Financial information is 100 %

precise and verifiable and has

evidence in support of every item

and transaction recorded.

Management accounting information

are not 100% verifiable. It requires the

data to be relevant, logical and timely.

As it is not possible to make actual

forecasts.

Audit Financial statements are to be

audited compulsorily by the

professionals or professional firms

(Senftlechner and Hiebl, 2015).

They do not have specific requirement

for audit , but audit could be conducted

for checking the efficiency and

effectiveness of management.

Confidentiality Statements of financial information

are published for public used

therefore there is no confidentiality

They are prepared for consideration of

management and for enhancing the

strategies of profits therefore it

requires it requires high confidentiality

(Difference between management and

financial accounting, 2019).

8

Principles

Accounting statements follows

frameworks of Generally Accepted

Accounting Principles for its

preparation.

Statements under management

accounting are not required to follow

any standard basis. They are made on

the basis of requirement of

management team.

Time Horizon Financial Accounting statements

are prepared on 'past' time horizon.

It is generally prepared on 'future' time

horizon but any specific time horizon

is not there.

Outputs Reports of Financial accounting

consists of income statement,

balance sheet and the cash flow

statements (Jiang, Wang and Xie,

2015).

Reports of management accounting

consists of product analysis, budget

reports, forecasted and estimated cost

statements on weekly, monthly or

quarterly basis.

Precisions Financial information is 100 %

precise and verifiable and has

evidence in support of every item

and transaction recorded.

Management accounting information

are not 100% verifiable. It requires the

data to be relevant, logical and timely.

As it is not possible to make actual

forecasts.

Audit Financial statements are to be

audited compulsorily by the

professionals or professional firms

(Senftlechner and Hiebl, 2015).

They do not have specific requirement

for audit , but audit could be conducted

for checking the efficiency and

effectiveness of management.

Confidentiality Statements of financial information

are published for public used

therefore there is no confidentiality

They are prepared for consideration of

management and for enhancing the

strategies of profits therefore it

requires it requires high confidentiality

(Difference between management and

financial accounting, 2019).

8

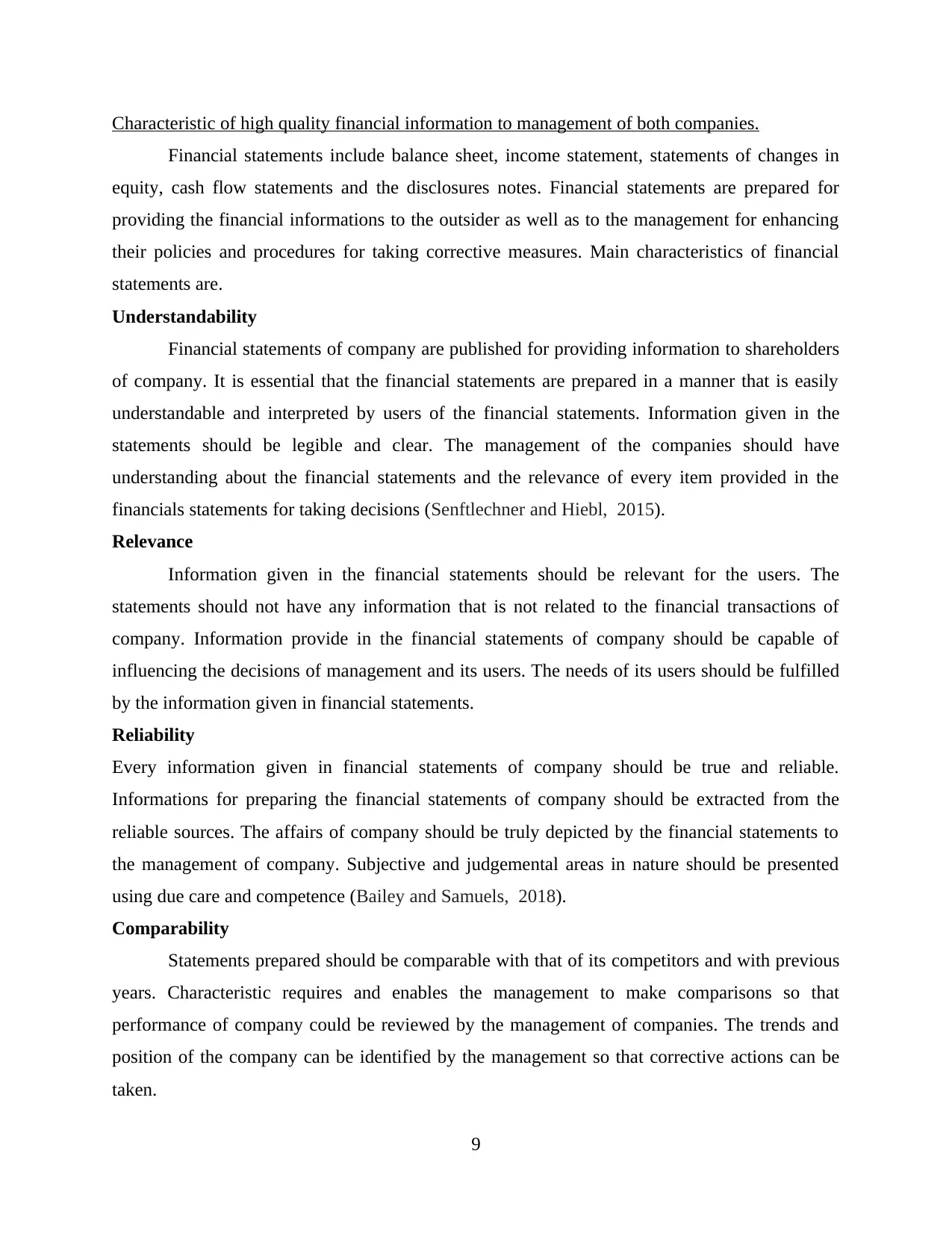

Characteristic of high quality financial information to management of both companies.

Financial statements include balance sheet, income statement, statements of changes in

equity, cash flow statements and the disclosures notes. Financial statements are prepared for

providing the financial informations to the outsider as well as to the management for enhancing

their policies and procedures for taking corrective measures. Main characteristics of financial

statements are.

Understandability

Financial statements of company are published for providing information to shareholders

of company. It is essential that the financial statements are prepared in a manner that is easily

understandable and interpreted by users of the financial statements. Information given in the

statements should be legible and clear. The management of the companies should have

understanding about the financial statements and the relevance of every item provided in the

financials statements for taking decisions (Senftlechner and Hiebl, 2015).

Relevance

Information given in the financial statements should be relevant for the users. The

statements should not have any information that is not related to the financial transactions of

company. Information provide in the financial statements of company should be capable of

influencing the decisions of management and its users. The needs of its users should be fulfilled

by the information given in financial statements.

Reliability

Every information given in financial statements of company should be true and reliable.

Informations for preparing the financial statements of company should be extracted from the

reliable sources. The affairs of company should be truly depicted by the financial statements to

the management of company. Subjective and judgemental areas in nature should be presented

using due care and competence (Bailey and Samuels, 2018).

Comparability

Statements prepared should be comparable with that of its competitors and with previous

years. Characteristic requires and enables the management to make comparisons so that

performance of company could be reviewed by the management of companies. The trends and

position of the company can be identified by the management so that corrective actions can be

taken.

9

Financial statements include balance sheet, income statement, statements of changes in

equity, cash flow statements and the disclosures notes. Financial statements are prepared for

providing the financial informations to the outsider as well as to the management for enhancing

their policies and procedures for taking corrective measures. Main characteristics of financial

statements are.

Understandability

Financial statements of company are published for providing information to shareholders

of company. It is essential that the financial statements are prepared in a manner that is easily

understandable and interpreted by users of the financial statements. Information given in the

statements should be legible and clear. The management of the companies should have

understanding about the financial statements and the relevance of every item provided in the

financials statements for taking decisions (Senftlechner and Hiebl, 2015).

Relevance

Information given in the financial statements should be relevant for the users. The

statements should not have any information that is not related to the financial transactions of

company. Information provide in the financial statements of company should be capable of

influencing the decisions of management and its users. The needs of its users should be fulfilled

by the information given in financial statements.

Reliability

Every information given in financial statements of company should be true and reliable.

Informations for preparing the financial statements of company should be extracted from the

reliable sources. The affairs of company should be truly depicted by the financial statements to

the management of company. Subjective and judgemental areas in nature should be presented

using due care and competence (Bailey and Samuels, 2018).

Comparability

Statements prepared should be comparable with that of its competitors and with previous

years. Characteristic requires and enables the management to make comparisons so that

performance of company could be reviewed by the management of companies. The trends and

position of the company can be identified by the management so that corrective actions can be

taken.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.