Financial Accounts vs. Management Accounts: Detailed Business Report

VerifiedAdded on 2023/01/11

|7

|1440

|81

Report

AI Summary

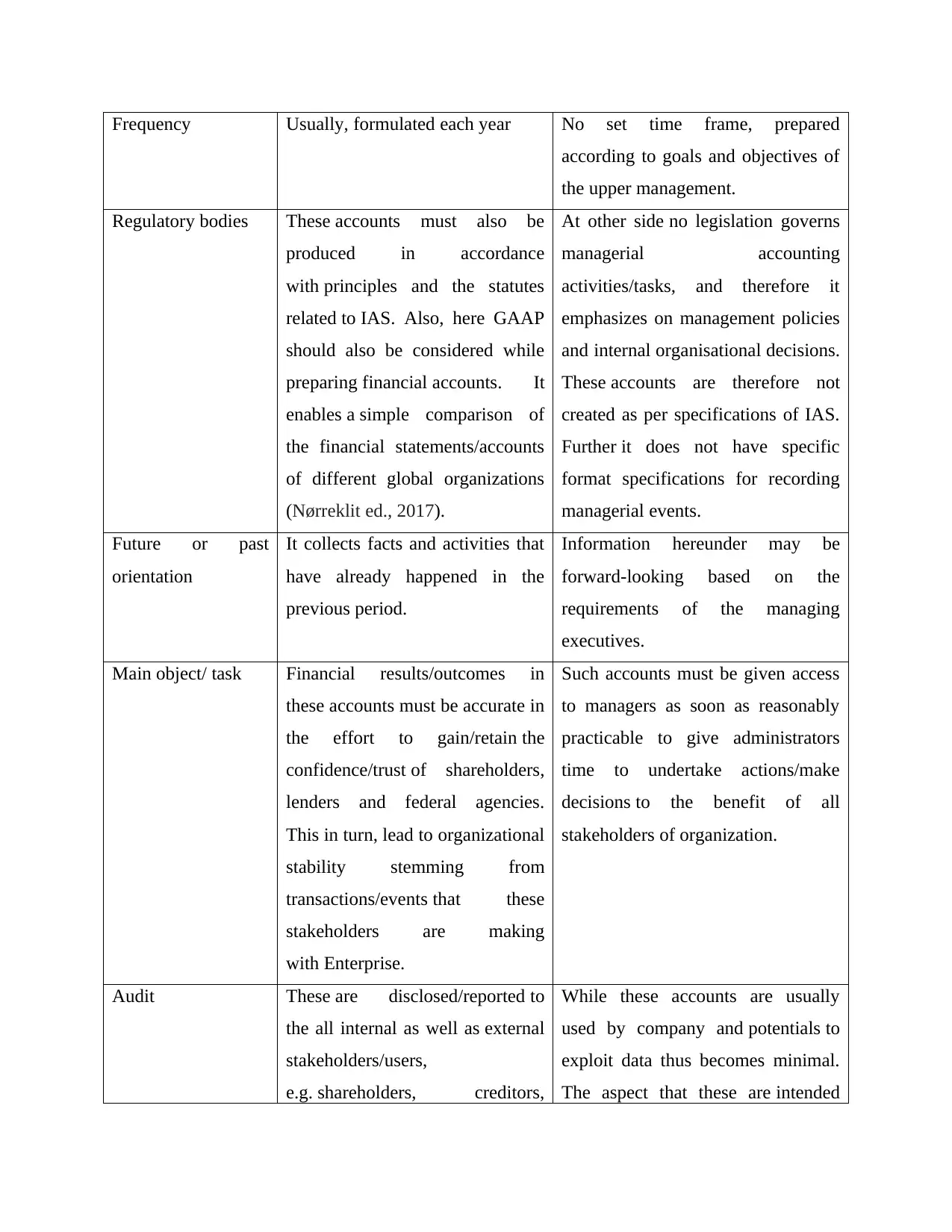

This report delves into the core differences between financial and management accounts, crucial components of business finance. It outlines the distinct characteristics of each, including their focus, frequency, regulatory bodies, information orientation, and primary objectives. Financial accounts, primarily for external reporting, document day-to-day business transactions, while management accounts, for internal use, capture both financial and non-financial data to aid managerial decision-making. The report further explores the usefulness of these accounts to various stakeholders, including managers, shareholders, investors, suppliers, government, and employees, highlighting how each group utilizes the information for their specific needs. This report emphasizes the importance of both types of accounts in enhancing organizational efficiency and stakeholder confidence.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.