Financial Management Report: Financial Techniques and Strategies

VerifiedAdded on 2023/01/06

|21

|5839

|90

Report

AI Summary

This financial management report provides a comprehensive analysis of key concepts and practices. It begins with an introduction to financial management, defining its role in organizational success. The report then delves into scenario-based analyses, evaluating various approaches, techniques, and factors that contribute to effective decision-making. It examines stakeholder management, addressing conflicting objectives and the roles of different stakeholder groups. The report also assesses the value of management accounting techniques, including budgetary control, break-even analysis, and capital budgeting, highlighting their importance in financial planning and operational efficiency. Furthermore, it explores techniques for fraud detection and prevention, along with key approaches to ethical decision-making within a business context. The report also provides a reflection on the learning experience and concludes with a discussion on financial decision-making in supporting long-term sustainability and recommendations to improve financial stability.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION ..........................................................................................................................1

SCENARIO A..................................................................................................................................1

1. Evaluating the range of approaches, techniques and the factors which contributes to

effective decision making............................................................................................................1

2. Evaluating the management of conflicting objectives and stakeholder management of

different stakeholder groups........................................................................................................3

3 Examining the value of management accounting techniques. .................................................3

4 Examining techniques detection and prevention of fraud and key approaches to ethical

decision making. .........................................................................................................................4

5. Reflection ................................................................................................................................5

SCENARIO B..................................................................................................................................6

1 & 2 Identifying how data obtained could help in informing operational and strategic

decisions of company. .................................................................................................................6

3. Comparing and contrasting investment appraisal techniques and evaluating their

effectiveness to maximise the return on investments. ..............................................................11

4. Value of techniques helping in financial decision making ...................................................15

5. Financial decision-making in supporting the long term sustainability .................................16

6. Recommendations for management accountant to help in improving financial stability .....16

CONCLUSION .............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION ..........................................................................................................................1

SCENARIO A..................................................................................................................................1

1. Evaluating the range of approaches, techniques and the factors which contributes to

effective decision making............................................................................................................1

2. Evaluating the management of conflicting objectives and stakeholder management of

different stakeholder groups........................................................................................................3

3 Examining the value of management accounting techniques. .................................................3

4 Examining techniques detection and prevention of fraud and key approaches to ethical

decision making. .........................................................................................................................4

5. Reflection ................................................................................................................................5

SCENARIO B..................................................................................................................................6

1 & 2 Identifying how data obtained could help in informing operational and strategic

decisions of company. .................................................................................................................6

3. Comparing and contrasting investment appraisal techniques and evaluating their

effectiveness to maximise the return on investments. ..............................................................11

4. Value of techniques helping in financial decision making ...................................................15

5. Financial decision-making in supporting the long term sustainability .................................16

6. Recommendations for management accountant to help in improving financial stability .....16

CONCLUSION .............................................................................................................................17

REFERENCES..............................................................................................................................18

INTRODUCTION

Financial management could be described as function or area in organization that is

concerned with the profitability, cash, expenses and credit so the organization is having means

for carrying out the objective as effectively as possible. It is also referred as dealing with money

investments of firm to help them in better decision-making (Erin and et.al., 2018). It involves

raising finance from various sources that is best suited for the organization and will bring

maximum benefits. Financial management ensures that there is adequate supply of the funds to

concern and ensuring adequate returns Report will provide about the range of techniques,

approaches and the factors that contribute to effective decision making. It will also discuss about

the different stakeholder groups and conflicts between shareholders and management. Further the

study will provide about the value of management accounting techniques and the different

techniques used for fraud detection.

SCENARIO A

1. Evaluating the range of approaches, techniques and the factors which contributes to effective

decision making

There are various types of approaches and techniques which assists the management of

the organization in taking relevant business related decisions. Some of these approaches and

techniques are stated below.

Knowledge based approach: In this, the management takes into account the pre-

determined criteria for the purpose of measuring and ensuring that the optimal outcome has been

achieved. It involves taking the advice from the expertise in the relevant for the purpose of

taking meaningful business decisions as it primarily focuses on the quantitative aspects and other

factual information for undertaking meaningful business decisions. For instance, the organization

can make use of its income statement to know its profitability and draw opinion on the same.

Formal and informal approaches: The formal decision-making processes takes much

longer time as compared to the informal approaches. In the formal approach, it is clear that who

will participate in the decision-making process and is also documented properly and it develops

trust and equality (Kyheröinen, 2020). In the informal approach, it is unclear who will be

participating in the discussion and it lacks transparency but in the situation requiring instant

decision then this approach is very useful for undertaking prompt decisions. There is a complete

1

Financial management could be described as function or area in organization that is

concerned with the profitability, cash, expenses and credit so the organization is having means

for carrying out the objective as effectively as possible. It is also referred as dealing with money

investments of firm to help them in better decision-making (Erin and et.al., 2018). It involves

raising finance from various sources that is best suited for the organization and will bring

maximum benefits. Financial management ensures that there is adequate supply of the funds to

concern and ensuring adequate returns Report will provide about the range of techniques,

approaches and the factors that contribute to effective decision making. It will also discuss about

the different stakeholder groups and conflicts between shareholders and management. Further the

study will provide about the value of management accounting techniques and the different

techniques used for fraud detection.

SCENARIO A

1. Evaluating the range of approaches, techniques and the factors which contributes to effective

decision making

There are various types of approaches and techniques which assists the management of

the organization in taking relevant business related decisions. Some of these approaches and

techniques are stated below.

Knowledge based approach: In this, the management takes into account the pre-

determined criteria for the purpose of measuring and ensuring that the optimal outcome has been

achieved. It involves taking the advice from the expertise in the relevant for the purpose of

taking meaningful business decisions as it primarily focuses on the quantitative aspects and other

factual information for undertaking meaningful business decisions. For instance, the organization

can make use of its income statement to know its profitability and draw opinion on the same.

Formal and informal approaches: The formal decision-making processes takes much

longer time as compared to the informal approaches. In the formal approach, it is clear that who

will participate in the decision-making process and is also documented properly and it develops

trust and equality (Kyheröinen, 2020). In the informal approach, it is unclear who will be

participating in the discussion and it lacks transparency but in the situation requiring instant

decision then this approach is very useful for undertaking prompt decisions. There is a complete

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

set of structure to be followed in the formal approach which is not so in case of the informal

approach.

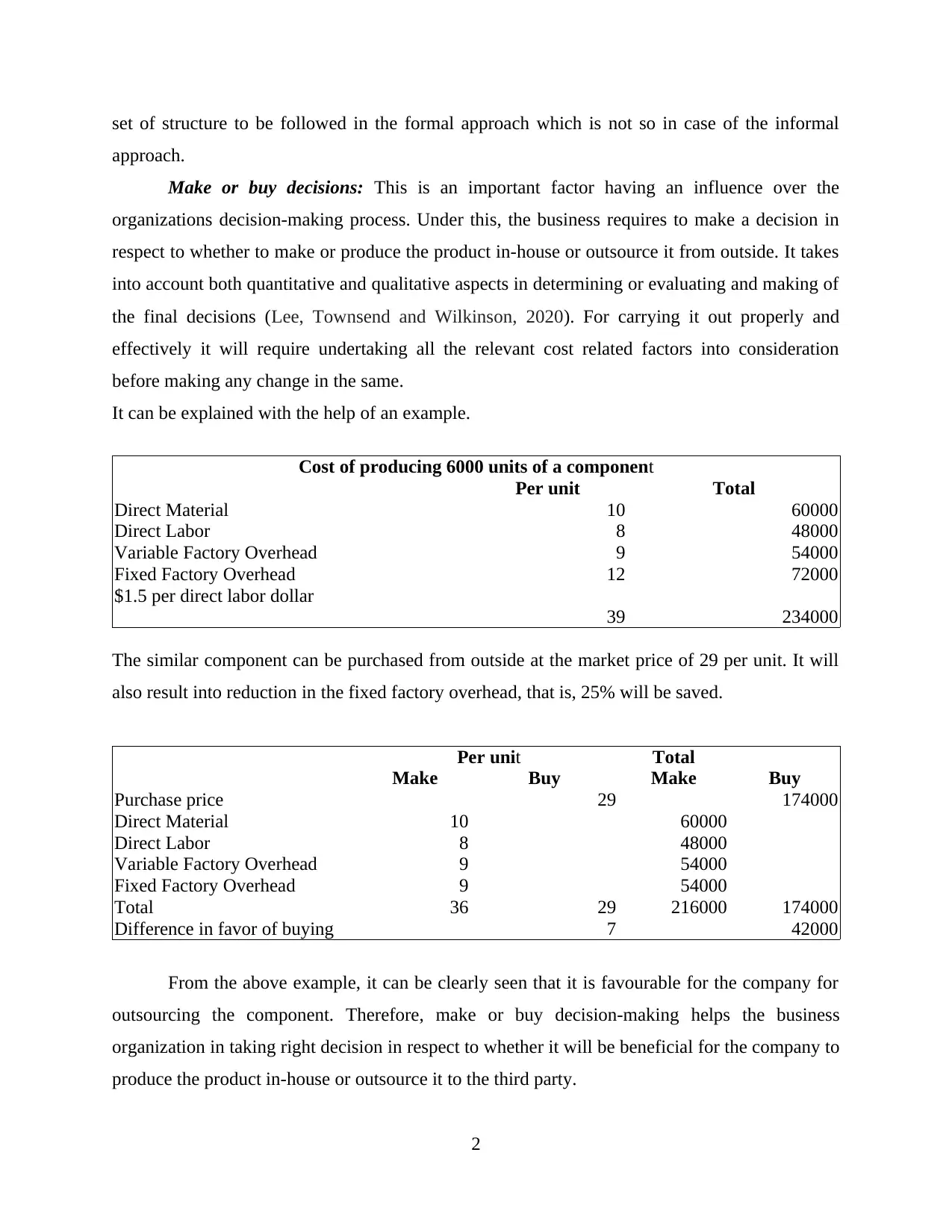

Make or buy decisions: This is an important factor having an influence over the

organizations decision-making process. Under this, the business requires to make a decision in

respect to whether to make or produce the product in-house or outsource it from outside. It takes

into account both quantitative and qualitative aspects in determining or evaluating and making of

the final decisions (Lee, Townsend and Wilkinson, 2020). For carrying it out properly and

effectively it will require undertaking all the relevant cost related factors into consideration

before making any change in the same.

It can be explained with the help of an example.

Cost of producing 6000 units of a component

Per unit Total

Direct Material 10 60000

Direct Labor 8 48000

Variable Factory Overhead 9 54000

Fixed Factory Overhead 12 72000

$1.5 per direct labor dollar

39 234000

The similar component can be purchased from outside at the market price of 29 per unit. It will

also result into reduction in the fixed factory overhead, that is, 25% will be saved.

Per unit Total

Make Buy Make Buy

Purchase price 29 174000

Direct Material 10 60000

Direct Labor 8 48000

Variable Factory Overhead 9 54000

Fixed Factory Overhead 9 54000

Total 36 29 216000 174000

Difference in favor of buying 7 42000

From the above example, it can be clearly seen that it is favourable for the company for

outsourcing the component. Therefore, make or buy decision-making helps the business

organization in taking right decision in respect to whether it will be beneficial for the company to

produce the product in-house or outsource it to the third party.

2

approach.

Make or buy decisions: This is an important factor having an influence over the

organizations decision-making process. Under this, the business requires to make a decision in

respect to whether to make or produce the product in-house or outsource it from outside. It takes

into account both quantitative and qualitative aspects in determining or evaluating and making of

the final decisions (Lee, Townsend and Wilkinson, 2020). For carrying it out properly and

effectively it will require undertaking all the relevant cost related factors into consideration

before making any change in the same.

It can be explained with the help of an example.

Cost of producing 6000 units of a component

Per unit Total

Direct Material 10 60000

Direct Labor 8 48000

Variable Factory Overhead 9 54000

Fixed Factory Overhead 12 72000

$1.5 per direct labor dollar

39 234000

The similar component can be purchased from outside at the market price of 29 per unit. It will

also result into reduction in the fixed factory overhead, that is, 25% will be saved.

Per unit Total

Make Buy Make Buy

Purchase price 29 174000

Direct Material 10 60000

Direct Labor 8 48000

Variable Factory Overhead 9 54000

Fixed Factory Overhead 9 54000

Total 36 29 216000 174000

Difference in favor of buying 7 42000

From the above example, it can be clearly seen that it is favourable for the company for

outsourcing the component. Therefore, make or buy decision-making helps the business

organization in taking right decision in respect to whether it will be beneficial for the company to

produce the product in-house or outsource it to the third party.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Evaluating the management of conflicting objectives and stakeholder management of different

stakeholder groups.

Stakeholders

Stakeholder management is a significant process which is useful in maintaining good set of

relationship with the key people of the organization. A stakeholder is considered to be as a party

who has wide degree of interest in the affairs of company and is also influenced by the working

of business. Creditors: They supply raw material, financial capital and other services to the company.

They are interested in the company because they want to be paid in full within the

stipulated time period. They seek to the financial statements of the company as it

provides comprehensive look upon the financial health of company. Managers and Employees: They want to company to thrive to earn high wages and

remain invested in the company for long period of time (Kaplan and Atkinson, 2015).

They seek to the financial statements of the company to know the financial health of

company. Shareholders: They are interested in the business operations and count on business to

remain profitable to gain valuable set of return on investment. They seek information

from cash flow statement and ratios to examine the earning growth of company.

Government: They need business to grow in order to gain taxes which supports various

government services.

Conflict between Management and Shareholders

The conflict between the shareholders and the managers of the company is mainly

referred to as the agency cost and has been borne by the shareholders. The agency theory tends to

state that, decision right of corporation has been given to mangers to effectively act in the

interest of the shareholders. The interest of the varied stakeholders group may conflict. For

example, the key goal of the owner or management of the company is to seek higher profits,

reduce business cost and pay optimum wages to the staff. On the other hand, the goal of the

shareholder is to gain higher returns from the investment they have made. This resulted in major

conflict of interest between the two parties.

3 Examining the value of management accounting techniques.

Management accounting

3

stakeholder groups.

Stakeholders

Stakeholder management is a significant process which is useful in maintaining good set of

relationship with the key people of the organization. A stakeholder is considered to be as a party

who has wide degree of interest in the affairs of company and is also influenced by the working

of business. Creditors: They supply raw material, financial capital and other services to the company.

They are interested in the company because they want to be paid in full within the

stipulated time period. They seek to the financial statements of the company as it

provides comprehensive look upon the financial health of company. Managers and Employees: They want to company to thrive to earn high wages and

remain invested in the company for long period of time (Kaplan and Atkinson, 2015).

They seek to the financial statements of the company to know the financial health of

company. Shareholders: They are interested in the business operations and count on business to

remain profitable to gain valuable set of return on investment. They seek information

from cash flow statement and ratios to examine the earning growth of company.

Government: They need business to grow in order to gain taxes which supports various

government services.

Conflict between Management and Shareholders

The conflict between the shareholders and the managers of the company is mainly

referred to as the agency cost and has been borne by the shareholders. The agency theory tends to

state that, decision right of corporation has been given to mangers to effectively act in the

interest of the shareholders. The interest of the varied stakeholders group may conflict. For

example, the key goal of the owner or management of the company is to seek higher profits,

reduce business cost and pay optimum wages to the staff. On the other hand, the goal of the

shareholder is to gain higher returns from the investment they have made. This resulted in major

conflict of interest between the two parties.

3 Examining the value of management accounting techniques.

Management accounting

3

Management accounting is considered to be as the branch of the accounting. It is

considered to be very useful for the financial managers of the Diageo Company because it helps

in taking long term as well as the short term decision to improve the financial health and

operational efficiency of the company. It is useful for the financial managers in carrying out

financial planning and effectively analyses the financial statements of the company. The

budgetary control technique is considered to be prominent because it helps the financial manger

to set specific budget and control cost to carry out business operations. The management

accounting techniques like break even analysis, marginal costing, standard costing, break even

analysis, capital budgeting, inventory valuation, trend analysis, etc. are of utmost value to the

financial manager because it helps in increasing the profit margins by effectively attaining

economies of scale and lowering operational expenses. It helps the financial manager in

evaluating the financial health of company and take necessary decision.

Role of management accountants

Management accountants in turn are referred to as the planners, risk managers,

strategists, budgeters and also the decision makers. They assess the key financial reports and

managerial reports of the company and engage in better decision making (Maas, Schaltegger and

Crutzen, 2016). They also focus on maintaining the effective financial health of the company for

greater sustainable success. Another key significant role of the management accountant is to

maintain optimum level of the capital structure. They analyses the accounts and also prepares

report for effective decision making. This way it is considered to be useful in contributing to the

greater success of the company.

Maximization of shareholder’s wealth

The shareholder’s wealth can be effectively maximized by considering those business

concern which helps in maximizing the market value of the shareholders. However, when the

company maximizes the wealth of the company then the individual shareholder can use the

wealth to maximize the individual utility. The market value of the share have been an effective

indicator associated with the key efficiency and effectiveness of the company.

4 Examining techniques detection and prevention of fraud and key approaches to ethical decision

making.

Fraud and detection of frauds

Any illegal activities and dishonest activities which has been carried out by the company or

4

considered to be very useful for the financial managers of the Diageo Company because it helps

in taking long term as well as the short term decision to improve the financial health and

operational efficiency of the company. It is useful for the financial managers in carrying out

financial planning and effectively analyses the financial statements of the company. The

budgetary control technique is considered to be prominent because it helps the financial manger

to set specific budget and control cost to carry out business operations. The management

accounting techniques like break even analysis, marginal costing, standard costing, break even

analysis, capital budgeting, inventory valuation, trend analysis, etc. are of utmost value to the

financial manager because it helps in increasing the profit margins by effectively attaining

economies of scale and lowering operational expenses. It helps the financial manager in

evaluating the financial health of company and take necessary decision.

Role of management accountants

Management accountants in turn are referred to as the planners, risk managers,

strategists, budgeters and also the decision makers. They assess the key financial reports and

managerial reports of the company and engage in better decision making (Maas, Schaltegger and

Crutzen, 2016). They also focus on maintaining the effective financial health of the company for

greater sustainable success. Another key significant role of the management accountant is to

maintain optimum level of the capital structure. They analyses the accounts and also prepares

report for effective decision making. This way it is considered to be useful in contributing to the

greater success of the company.

Maximization of shareholder’s wealth

The shareholder’s wealth can be effectively maximized by considering those business

concern which helps in maximizing the market value of the shareholders. However, when the

company maximizes the wealth of the company then the individual shareholder can use the

wealth to maximize the individual utility. The market value of the share have been an effective

indicator associated with the key efficiency and effectiveness of the company.

4 Examining techniques detection and prevention of fraud and key approaches to ethical decision

making.

Fraud and detection of frauds

Any illegal activities and dishonest activities which has been carried out by the company or

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the individual person to gain advantageous financial benefits. Detection of frauds is one of the

key significant measure which helps in improving the operations of the business. Segregating all

the accounting duties and maintaining the internal control is considered to be highly significant

measure for the prevention of fraud within the organization. Audit the books regularly and also

using encrypted software is considered to be as one of the key prominent measure which is

useful in prevention of the fraudulent set of activities within the company. Tampering of the data: the employee of the company alters the amount, payee or other

specific details to create unauthorized check. This fraud can be detected by conducting

random audits and implement check and balances. Inventory theft: Stealing of the products or diverting it to some other place. This can be

detected by implementing anonymous ethics and also encouraging employees to report

any wrongdoing within the organization.

Embezzlement: Such fraud is carried out on the part of the person who controls the funds

of the company. Implementation of the tight accounting functions and internal control

helps in the prevention of such fraud.

Ethics

Ethics is considered to be as carried out appropriate set of business practice and policies

within the whole organization. Ethical decision making is referred to as a process of choosing

and effectively evaluating the key alternatives in a significant and prominent manner. It is useful

in eliminating unethical practice and select the best ethical alternative. Utilitarian approach is

considered to be an effective ethical decision making approach which is useful in determining

the right and wrong doing by effectively focusing on the key relevant outcomes,

5. Reflection

The report belongs to my interest area finance. I have performed all the tasks and

questions taking deep interest and understanding the requirement in financial management. I

have found that financial management is the foundation of any business as cash flows are the

blood of organisation. Different approaches of decision-making are knowledge based, formal and

informal and make or buy decisions. These approaches help in effective decision making to run

the business efficiently. In critical situations where judgement could not be made effectively

different decision making techniques are used like decision tree, make or buy decisions. I have

found that even after using different approaches and techniques there are various factors that

5

key significant measure which helps in improving the operations of the business. Segregating all

the accounting duties and maintaining the internal control is considered to be highly significant

measure for the prevention of fraud within the organization. Audit the books regularly and also

using encrypted software is considered to be as one of the key prominent measure which is

useful in prevention of the fraudulent set of activities within the company. Tampering of the data: the employee of the company alters the amount, payee or other

specific details to create unauthorized check. This fraud can be detected by conducting

random audits and implement check and balances. Inventory theft: Stealing of the products or diverting it to some other place. This can be

detected by implementing anonymous ethics and also encouraging employees to report

any wrongdoing within the organization.

Embezzlement: Such fraud is carried out on the part of the person who controls the funds

of the company. Implementation of the tight accounting functions and internal control

helps in the prevention of such fraud.

Ethics

Ethics is considered to be as carried out appropriate set of business practice and policies

within the whole organization. Ethical decision making is referred to as a process of choosing

and effectively evaluating the key alternatives in a significant and prominent manner. It is useful

in eliminating unethical practice and select the best ethical alternative. Utilitarian approach is

considered to be an effective ethical decision making approach which is useful in determining

the right and wrong doing by effectively focusing on the key relevant outcomes,

5. Reflection

The report belongs to my interest area finance. I have performed all the tasks and

questions taking deep interest and understanding the requirement in financial management. I

have found that financial management is the foundation of any business as cash flows are the

blood of organisation. Different approaches of decision-making are knowledge based, formal and

informal and make or buy decisions. These approaches help in effective decision making to run

the business efficiently. In critical situations where judgement could not be made effectively

different decision making techniques are used like decision tree, make or buy decisions. I have

found that even after using different approaches and techniques there are various factors that

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

affect the decision-making process. Prior to this I was not aware about the fact that even

effective decisions could be influenced. Factors influencing the decisions are economic

scenarios, inflation rates, management effectiveness or other non financial issues. These factors

could significantly improve the financial condition of the business. Apart from this, I have also

noted that stakeholder management is essential for the management as it is not having single

standing and have various parties that are interested in business such as shareholders, employees,

suppliers and consumers. Management has to consider that the interest of one group is not

deprived due to other. It has to ensure that the decisions are taken which benefits all the

stakeholders and organisation as whole. I have learned that management accountant plays an

effective role in recording all the transactions and events of business. They have the role of

preparing budgets and variance analysis and taking measures for reducing variations. Along with

these company should also establish strong internal controls for preventing and detecting the

errors and frauds. The financial information provided by the company should present true and

fair of company and should not be misappropriated for presenting manipulated performance and

position.

SCENARIO B

1 & 2 Identifying how data obtained could help in informing operational and strategic decisions

of company.

Operational and Strategic decisions

The data provided by the financial statements enables the company to make decisions

that are essential for operating the business successfully. Operational decisions are taken for

optimum utilisation of the resources of the business to earn higher returns. Strategic decisions

based on financial information are taken to enhance the processes and procedures of business.

It is explained by financial analysis and interpretation of Diageo Company.

Profitability Ratios

Ratio Formulae 2020 2019

Profitability ratios

ROCE

Operating Profit

*100/ (Total Equity

+Total Non-current

liabilities)

7.97% 16.64%

6

effective decisions could be influenced. Factors influencing the decisions are economic

scenarios, inflation rates, management effectiveness or other non financial issues. These factors

could significantly improve the financial condition of the business. Apart from this, I have also

noted that stakeholder management is essential for the management as it is not having single

standing and have various parties that are interested in business such as shareholders, employees,

suppliers and consumers. Management has to consider that the interest of one group is not

deprived due to other. It has to ensure that the decisions are taken which benefits all the

stakeholders and organisation as whole. I have learned that management accountant plays an

effective role in recording all the transactions and events of business. They have the role of

preparing budgets and variance analysis and taking measures for reducing variations. Along with

these company should also establish strong internal controls for preventing and detecting the

errors and frauds. The financial information provided by the company should present true and

fair of company and should not be misappropriated for presenting manipulated performance and

position.

SCENARIO B

1 & 2 Identifying how data obtained could help in informing operational and strategic decisions

of company.

Operational and Strategic decisions

The data provided by the financial statements enables the company to make decisions

that are essential for operating the business successfully. Operational decisions are taken for

optimum utilisation of the resources of the business to earn higher returns. Strategic decisions

based on financial information are taken to enhance the processes and procedures of business.

It is explained by financial analysis and interpretation of Diageo Company.

Profitability Ratios

Ratio Formulae 2020 2019

Profitability ratios

ROCE

Operating Profit

*100/ (Total Equity

+Total Non-current

liabilities)

7.97% 16.64%

6

Gross Profit Margin Gross Profit*100

/Revenue (sales) 60.40% 62.18%

Operating Profit Margin

Operating

Profit*100 /Revenue

(sales)

18.18% 31.41%

Return on capital employed

It is the ratio used by the company to evaluate the efficiency of management in

generating returns over capital employed. It shows the ability of company in using the resources

in the best effective manner for the organisational growth and higher returns. ROCE of company

in year 2019 represents 16.64% that has moved downward to 7.97%. It shows significant decline

in the ratio causing serious concern for the management to look into the cause (Erin and et.al.,

2018). It is also seen due to the decreased profits or increase in capital employed. It could be

seen that management is losing efficiency in managing the resources.

Gross Profit Margin

It is the ratio reflecting different the performance of internal management by effectively

running the operations of business. It is the amount left with entity after covering all the direct

costs and expenditures associated with the business. Gross profit moves downward when firm is

not able to maintain control over costs of production (Husain and Sunardi, 2020). Gross profit

ratio was 62.18% that shows change of 1.78% downwards. Company is required to take steps for

controlling the costs due and to increase the revenues.

Net Profit Margin

Net profit margin of Diageo is 18.18% that has decreased with 13.32% from 31.41%. It

could be seen there has been significant decline in the profits of company. Net profit is an

important ration for both internal and external users of financial statements (Pivac, Barać and

Tadić, 2017). Such decline could have significant effect over the business and share prices.

Company is required to take steps to control the costs and expenditures and to promote sales of

business.

Liquidity ratios

Ratio Formulae 2020 2019

Working Capital

Ratio

Total Current Asset/

total current

Liabilities

1.77: 1 1.34 : 1

7

/Revenue (sales) 60.40% 62.18%

Operating Profit Margin

Operating

Profit*100 /Revenue

(sales)

18.18% 31.41%

Return on capital employed

It is the ratio used by the company to evaluate the efficiency of management in

generating returns over capital employed. It shows the ability of company in using the resources

in the best effective manner for the organisational growth and higher returns. ROCE of company

in year 2019 represents 16.64% that has moved downward to 7.97%. It shows significant decline

in the ratio causing serious concern for the management to look into the cause (Erin and et.al.,

2018). It is also seen due to the decreased profits or increase in capital employed. It could be

seen that management is losing efficiency in managing the resources.

Gross Profit Margin

It is the ratio reflecting different the performance of internal management by effectively

running the operations of business. It is the amount left with entity after covering all the direct

costs and expenditures associated with the business. Gross profit moves downward when firm is

not able to maintain control over costs of production (Husain and Sunardi, 2020). Gross profit

ratio was 62.18% that shows change of 1.78% downwards. Company is required to take steps for

controlling the costs due and to increase the revenues.

Net Profit Margin

Net profit margin of Diageo is 18.18% that has decreased with 13.32% from 31.41%. It

could be seen there has been significant decline in the profits of company. Net profit is an

important ration for both internal and external users of financial statements (Pivac, Barać and

Tadić, 2017). Such decline could have significant effect over the business and share prices.

Company is required to take steps to control the costs and expenditures and to promote sales of

business.

Liquidity ratios

Ratio Formulae 2020 2019

Working Capital

Ratio

Total Current Asset/

total current

Liabilities

1.77: 1 1.34 : 1

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

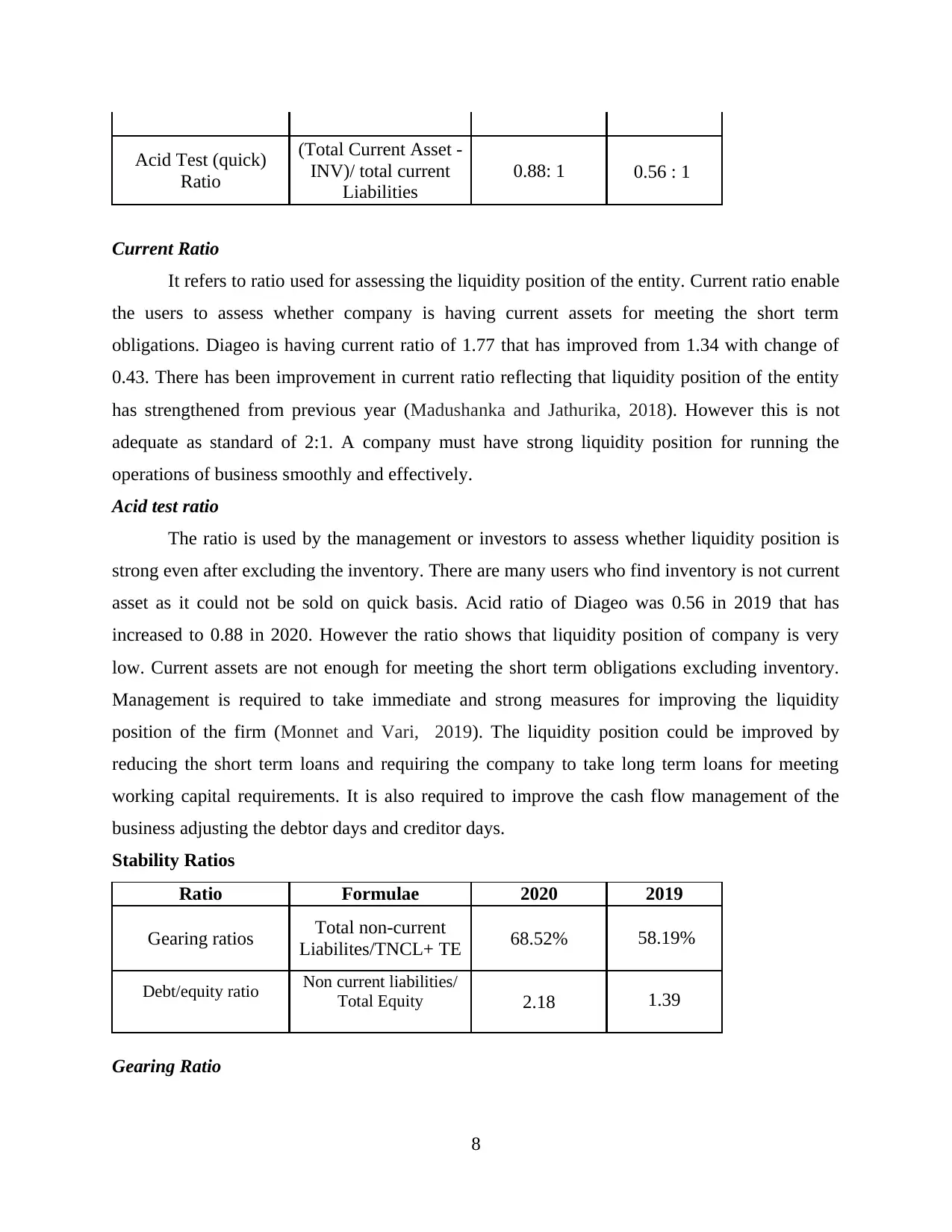

Acid Test (quick)

Ratio

(Total Current Asset -

INV)/ total current

Liabilities

0.88: 1 0.56 : 1

Current Ratio

It refers to ratio used for assessing the liquidity position of the entity. Current ratio enable

the users to assess whether company is having current assets for meeting the short term

obligations. Diageo is having current ratio of 1.77 that has improved from 1.34 with change of

0.43. There has been improvement in current ratio reflecting that liquidity position of the entity

has strengthened from previous year (Madushanka and Jathurika, 2018). However this is not

adequate as standard of 2:1. A company must have strong liquidity position for running the

operations of business smoothly and effectively.

Acid test ratio

The ratio is used by the management or investors to assess whether liquidity position is

strong even after excluding the inventory. There are many users who find inventory is not current

asset as it could not be sold on quick basis. Acid ratio of Diageo was 0.56 in 2019 that has

increased to 0.88 in 2020. However the ratio shows that liquidity position of company is very

low. Current assets are not enough for meeting the short term obligations excluding inventory.

Management is required to take immediate and strong measures for improving the liquidity

position of the firm (Monnet and Vari, 2019). The liquidity position could be improved by

reducing the short term loans and requiring the company to take long term loans for meeting

working capital requirements. It is also required to improve the cash flow management of the

business adjusting the debtor days and creditor days.

Stability Ratios

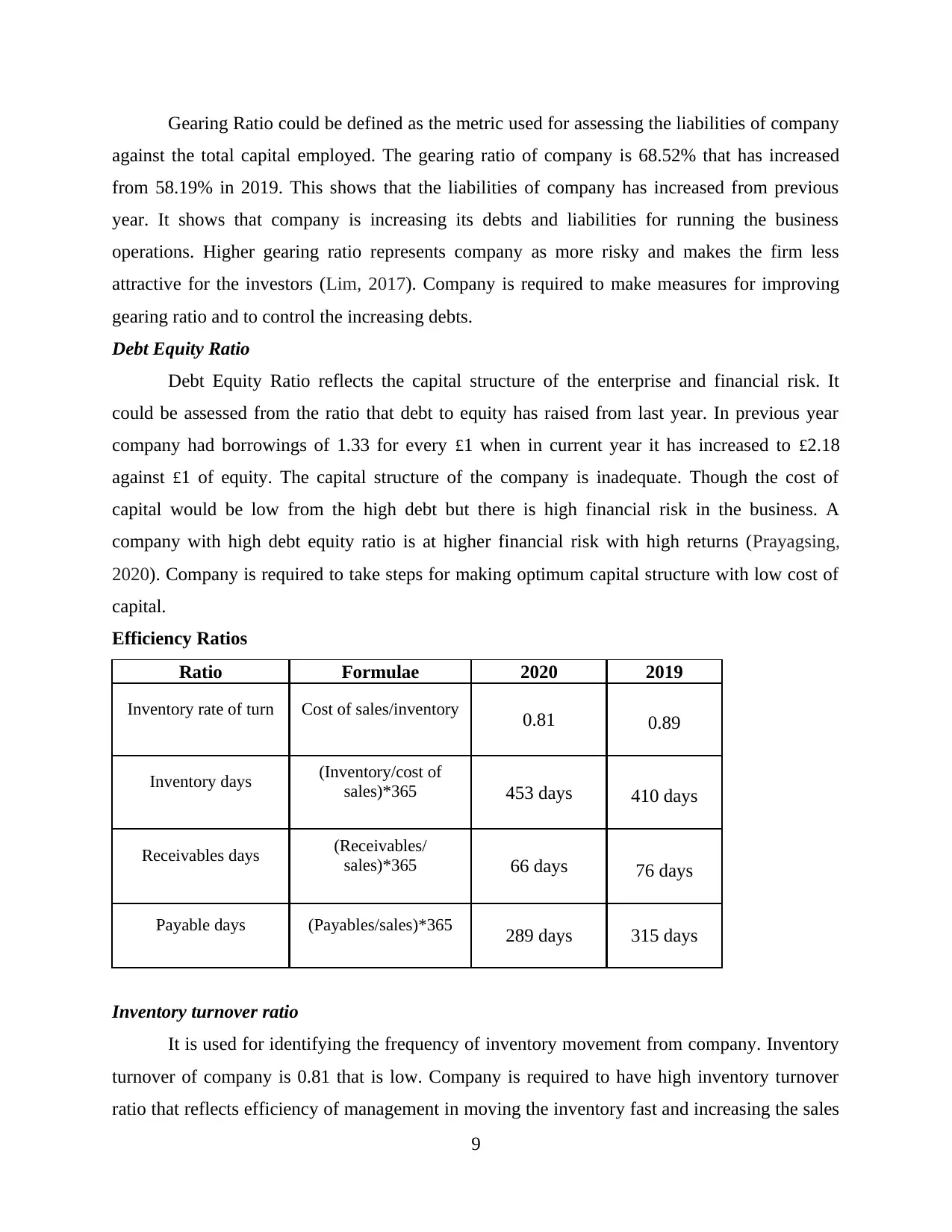

Ratio Formulae 2020 2019

Gearing ratios Total non-current

Liabilites/TNCL+ TE 68.52% 58.19%

Debt/equity ratio Non current liabilities/

Total Equity 2.18 1.39

Gearing Ratio

8

Ratio

(Total Current Asset -

INV)/ total current

Liabilities

0.88: 1 0.56 : 1

Current Ratio

It refers to ratio used for assessing the liquidity position of the entity. Current ratio enable

the users to assess whether company is having current assets for meeting the short term

obligations. Diageo is having current ratio of 1.77 that has improved from 1.34 with change of

0.43. There has been improvement in current ratio reflecting that liquidity position of the entity

has strengthened from previous year (Madushanka and Jathurika, 2018). However this is not

adequate as standard of 2:1. A company must have strong liquidity position for running the

operations of business smoothly and effectively.

Acid test ratio

The ratio is used by the management or investors to assess whether liquidity position is

strong even after excluding the inventory. There are many users who find inventory is not current

asset as it could not be sold on quick basis. Acid ratio of Diageo was 0.56 in 2019 that has

increased to 0.88 in 2020. However the ratio shows that liquidity position of company is very

low. Current assets are not enough for meeting the short term obligations excluding inventory.

Management is required to take immediate and strong measures for improving the liquidity

position of the firm (Monnet and Vari, 2019). The liquidity position could be improved by

reducing the short term loans and requiring the company to take long term loans for meeting

working capital requirements. It is also required to improve the cash flow management of the

business adjusting the debtor days and creditor days.

Stability Ratios

Ratio Formulae 2020 2019

Gearing ratios Total non-current

Liabilites/TNCL+ TE 68.52% 58.19%

Debt/equity ratio Non current liabilities/

Total Equity 2.18 1.39

Gearing Ratio

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Gearing Ratio could be defined as the metric used for assessing the liabilities of company

against the total capital employed. The gearing ratio of company is 68.52% that has increased

from 58.19% in 2019. This shows that the liabilities of company has increased from previous

year. It shows that company is increasing its debts and liabilities for running the business

operations. Higher gearing ratio represents company as more risky and makes the firm less

attractive for the investors (Lim, 2017). Company is required to make measures for improving

gearing ratio and to control the increasing debts.

Debt Equity Ratio

Debt Equity Ratio reflects the capital structure of the enterprise and financial risk. It

could be assessed from the ratio that debt to equity has raised from last year. In previous year

company had borrowings of 1.33 for every £1 when in current year it has increased to £2.18

against £1 of equity. The capital structure of the company is inadequate. Though the cost of

capital would be low from the high debt but there is high financial risk in the business. A

company with high debt equity ratio is at higher financial risk with high returns (Prayagsing,

2020). Company is required to take steps for making optimum capital structure with low cost of

capital.

Efficiency Ratios

Ratio Formulae 2020 2019

Inventory rate of turn Cost of sales/inventory 0.81 0.89

Inventory days (Inventory/cost of

sales)*365 453 days 410 days

Receivables days (Receivables/

sales)*365 66 days 76 days

Payable days (Payables/sales)*365 289 days 315 days

Inventory turnover ratio

It is used for identifying the frequency of inventory movement from company. Inventory

turnover of company is 0.81 that is low. Company is required to have high inventory turnover

ratio that reflects efficiency of management in moving the inventory fast and increasing the sales

9

against the total capital employed. The gearing ratio of company is 68.52% that has increased

from 58.19% in 2019. This shows that the liabilities of company has increased from previous

year. It shows that company is increasing its debts and liabilities for running the business

operations. Higher gearing ratio represents company as more risky and makes the firm less

attractive for the investors (Lim, 2017). Company is required to make measures for improving

gearing ratio and to control the increasing debts.

Debt Equity Ratio

Debt Equity Ratio reflects the capital structure of the enterprise and financial risk. It

could be assessed from the ratio that debt to equity has raised from last year. In previous year

company had borrowings of 1.33 for every £1 when in current year it has increased to £2.18

against £1 of equity. The capital structure of the company is inadequate. Though the cost of

capital would be low from the high debt but there is high financial risk in the business. A

company with high debt equity ratio is at higher financial risk with high returns (Prayagsing,

2020). Company is required to take steps for making optimum capital structure with low cost of

capital.

Efficiency Ratios

Ratio Formulae 2020 2019

Inventory rate of turn Cost of sales/inventory 0.81 0.89

Inventory days (Inventory/cost of

sales)*365 453 days 410 days

Receivables days (Receivables/

sales)*365 66 days 76 days

Payable days (Payables/sales)*365 289 days 315 days

Inventory turnover ratio

It is used for identifying the frequency of inventory movement from company. Inventory

turnover of company is 0.81 that is low. Company is required to have high inventory turnover

ratio that reflects efficiency of management in moving the inventory fast and increasing the sales

9

(Zimpel and et.al., 2017). Inventory turnover could be increased by taking effective sales

promotion steps to increased the sales.

Inventory days

It reflects the time within which inventory is converted into cash. Inventory days are 453

which were 410 in 2019. The inventory days are significantly high which reflects that the

management is facing issues in moving the inventory and converting them in cash.

Receivables days

It provides the days in which dues are collected from the customers. Above table shows

that receivables days are 66 which have reduced from 76 days last year (Njenga and Jagongo,

2019). Attempt have been made by management to reduce the collection period for improving

the cash flows.

Payable days

Payable days reflects the payment period of creditors. Diageo is having payable days of

289 days and have reduced from 315 days. Payable days are also reduced with receivable days

for effectively managing the cash cycle.

Management is taking active steps for improving the efficiency of entity which is currently very

weak.

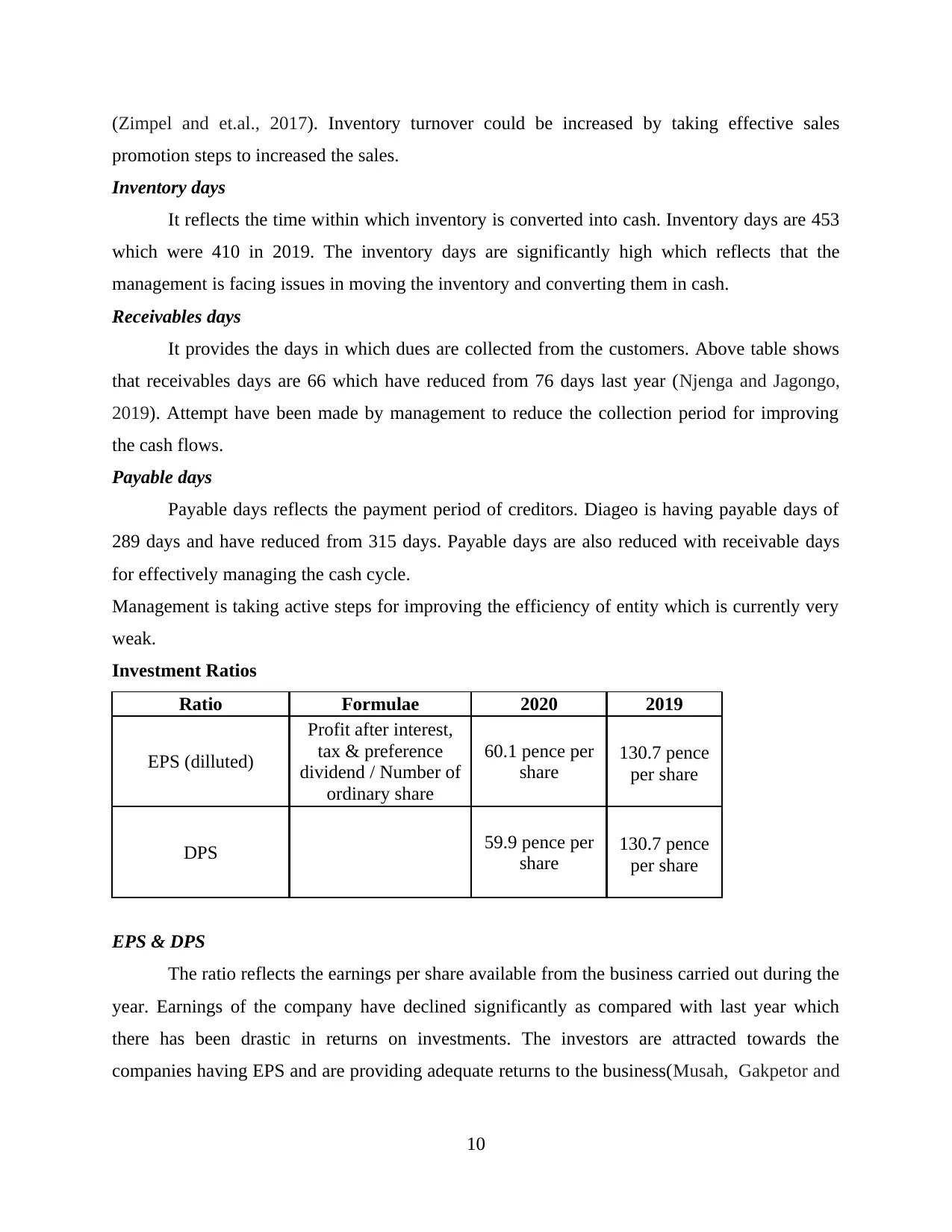

Investment Ratios

Ratio Formulae 2020 2019

EPS (dilluted)

Profit after interest,

tax & preference

dividend / Number of

ordinary share

60.1 pence per

share

130.7 pence

per share

DPS 59.9 pence per

share

130.7 pence

per share

EPS & DPS

The ratio reflects the earnings per share available from the business carried out during the

year. Earnings of the company have declined significantly as compared with last year which

there has been drastic in returns on investments. The investors are attracted towards the

companies having EPS and are providing adequate returns to the business(Musah, Gakpetor and

10

promotion steps to increased the sales.

Inventory days

It reflects the time within which inventory is converted into cash. Inventory days are 453

which were 410 in 2019. The inventory days are significantly high which reflects that the

management is facing issues in moving the inventory and converting them in cash.

Receivables days

It provides the days in which dues are collected from the customers. Above table shows

that receivables days are 66 which have reduced from 76 days last year (Njenga and Jagongo,

2019). Attempt have been made by management to reduce the collection period for improving

the cash flows.

Payable days

Payable days reflects the payment period of creditors. Diageo is having payable days of

289 days and have reduced from 315 days. Payable days are also reduced with receivable days

for effectively managing the cash cycle.

Management is taking active steps for improving the efficiency of entity which is currently very

weak.

Investment Ratios

Ratio Formulae 2020 2019

EPS (dilluted)

Profit after interest,

tax & preference

dividend / Number of

ordinary share

60.1 pence per

share

130.7 pence

per share

DPS 59.9 pence per

share

130.7 pence

per share

EPS & DPS

The ratio reflects the earnings per share available from the business carried out during the

year. Earnings of the company have declined significantly as compared with last year which

there has been drastic in returns on investments. The investors are attracted towards the

companies having EPS and are providing adequate returns to the business(Musah, Gakpetor and

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.