Evaluating Valuation and Capital Appraisal Techniques in Finance

VerifiedAdded on 2023/06/18

|16

|4063

|458

Report

AI Summary

This report provides a comprehensive analysis of financial valuation and capital appraisal techniques. It begins by valuing a company using the price/earnings ratio, dividend valuation method, and discounted cash flow (DCF) method, discussing the problems associated with each. The report then evaluates capital appraisal techniques, including payback period (PP), accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR), highlighting the benefits and drawbacks of each method. The analysis includes calculations and interpretations to determine the economic feasibility of investment decisions, offering insights into how companies can effectively assess and manage their financial strategies. The solutions are provided by students on Desklib, a website providing necessary AI based study tools.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

QUESTION 2..................................................................................................................................3

a) Calculation of valuation of company by using price/ earning ratio.......................................3

b) Computation of valuation of Trojan plc by Dividend valuation method................................4

c) Estimation of organization's value via Discounted cash flow method...................................5

d) Discussing the problem associated with valuation techniques..............................................6

QUESTION 3..................................................................................................................................8

a) Payback Period (PP)................................................................................................................8

b) Accounting Rate of Return (ARR)..........................................................................................9

c) Net present value (NPV)..........................................................................................................9

d) Internal Rate of return (IRR)................................................................................................10

Evaluating the benefits and drawbacks of capital appraisal techniques....................................12

REFERENCES..............................................................................................................................15

QUESTION 2..................................................................................................................................3

a) Calculation of valuation of company by using price/ earning ratio.......................................3

b) Computation of valuation of Trojan plc by Dividend valuation method................................4

c) Estimation of organization's value via Discounted cash flow method...................................5

d) Discussing the problem associated with valuation techniques..............................................6

QUESTION 3..................................................................................................................................8

a) Payback Period (PP)................................................................................................................8

b) Accounting Rate of Return (ARR)..........................................................................................9

c) Net present value (NPV)..........................................................................................................9

d) Internal Rate of return (IRR)................................................................................................10

Evaluating the benefits and drawbacks of capital appraisal techniques....................................12

REFERENCES..............................................................................................................................15

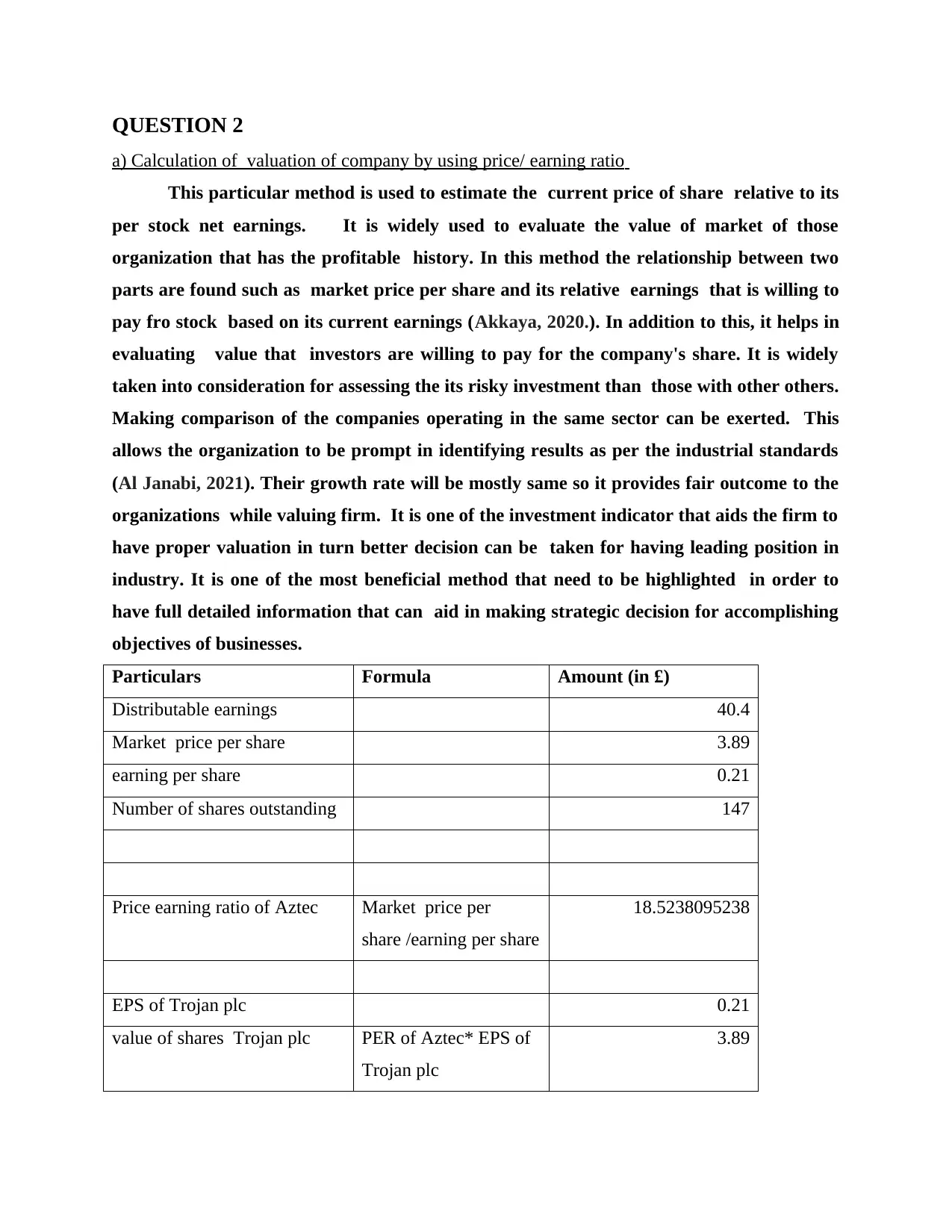

QUESTION 2

a) Calculation of valuation of company by using price/ earning ratio

This particular method is used to estimate the current price of share relative to its

per stock net earnings. It is widely used to evaluate the value of market of those

organization that has the profitable history. In this method the relationship between two

parts are found such as market price per share and its relative earnings that is willing to

pay fro stock based on its current earnings (Akkaya, 2020.). In addition to this, it helps in

evaluating value that investors are willing to pay for the company's share. It is widely

taken into consideration for assessing the its risky investment than those with other others.

Making comparison of the companies operating in the same sector can be exerted. This

allows the organization to be prompt in identifying results as per the industrial standards

(Al Janabi, 2021). Their growth rate will be mostly same so it provides fair outcome to the

organizations while valuing firm. It is one of the investment indicator that aids the firm to

have proper valuation in turn better decision can be taken for having leading position in

industry. It is one of the most beneficial method that need to be highlighted in order to

have full detailed information that can aid in making strategic decision for accomplishing

objectives of businesses.

Particulars Formula Amount (in £)

Distributable earnings 40.4

Market price per share 3.89

earning per share 0.21

Number of shares outstanding 147

Price earning ratio of Aztec Market price per

share /earning per share

18.5238095238

EPS of Trojan plc 0.21

value of shares Trojan plc PER of Aztec* EPS of

Trojan plc

3.89

a) Calculation of valuation of company by using price/ earning ratio

This particular method is used to estimate the current price of share relative to its

per stock net earnings. It is widely used to evaluate the value of market of those

organization that has the profitable history. In this method the relationship between two

parts are found such as market price per share and its relative earnings that is willing to

pay fro stock based on its current earnings (Akkaya, 2020.). In addition to this, it helps in

evaluating value that investors are willing to pay for the company's share. It is widely

taken into consideration for assessing the its risky investment than those with other others.

Making comparison of the companies operating in the same sector can be exerted. This

allows the organization to be prompt in identifying results as per the industrial standards

(Al Janabi, 2021). Their growth rate will be mostly same so it provides fair outcome to the

organizations while valuing firm. It is one of the investment indicator that aids the firm to

have proper valuation in turn better decision can be taken for having leading position in

industry. It is one of the most beneficial method that need to be highlighted in order to

have full detailed information that can aid in making strategic decision for accomplishing

objectives of businesses.

Particulars Formula Amount (in £)

Distributable earnings 40.4

Market price per share 3.89

earning per share 0.21

Number of shares outstanding 147

Price earning ratio of Aztec Market price per

share /earning per share

18.5238095238

EPS of Trojan plc 0.21

value of shares Trojan plc PER of Aztec* EPS of

Trojan plc

3.89

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Estimating the market value of

Trojan plc

value of shares of

Trojan plc* number of

outstanding share

571.83

From the above calculation it can be identified that market value of Trojan Plc is

£571.83 as per the price earning ratio method.

b) Computation of valuation of Trojan plc by Dividend valuation method

Dividend valuation is another method sued by company to accomplish the purpose

of making proper estimation of market price of specific organization. It is based on the

theory that it present day price is worth of all of sum of future dividends payments when

they are discounted to their present worth. This basically focus on determining the fair

value irrespective of taking the market based components into consideration. The time

when the stock should be buy is evaluated by value obtained from the dividend valuation

method. Basically large emphasis is given on valuing company by considering the time

value of money. It is one of the major method that can be taken into consideration by

organization for having market value of company on the basis of dividend providing of

company.

Particulars Formula Amount (in £)

latest dividend payment 0.13

Growth rate 2.00%

free rate 5.00%

Beta 1.10%

Number of shares

outstanding

147

Return on market 11.00%

For determining

expected rate of return

CAPM model will be

Trojan plc

value of shares of

Trojan plc* number of

outstanding share

571.83

From the above calculation it can be identified that market value of Trojan Plc is

£571.83 as per the price earning ratio method.

b) Computation of valuation of Trojan plc by Dividend valuation method

Dividend valuation is another method sued by company to accomplish the purpose

of making proper estimation of market price of specific organization. It is based on the

theory that it present day price is worth of all of sum of future dividends payments when

they are discounted to their present worth. This basically focus on determining the fair

value irrespective of taking the market based components into consideration. The time

when the stock should be buy is evaluated by value obtained from the dividend valuation

method. Basically large emphasis is given on valuing company by considering the time

value of money. It is one of the major method that can be taken into consideration by

organization for having market value of company on the basis of dividend providing of

company.

Particulars Formula Amount (in £)

latest dividend payment 0.13

Growth rate 2.00%

free rate 5.00%

Beta 1.10%

Number of shares

outstanding

147

Return on market 11.00%

For determining

expected rate of return

CAPM model will be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

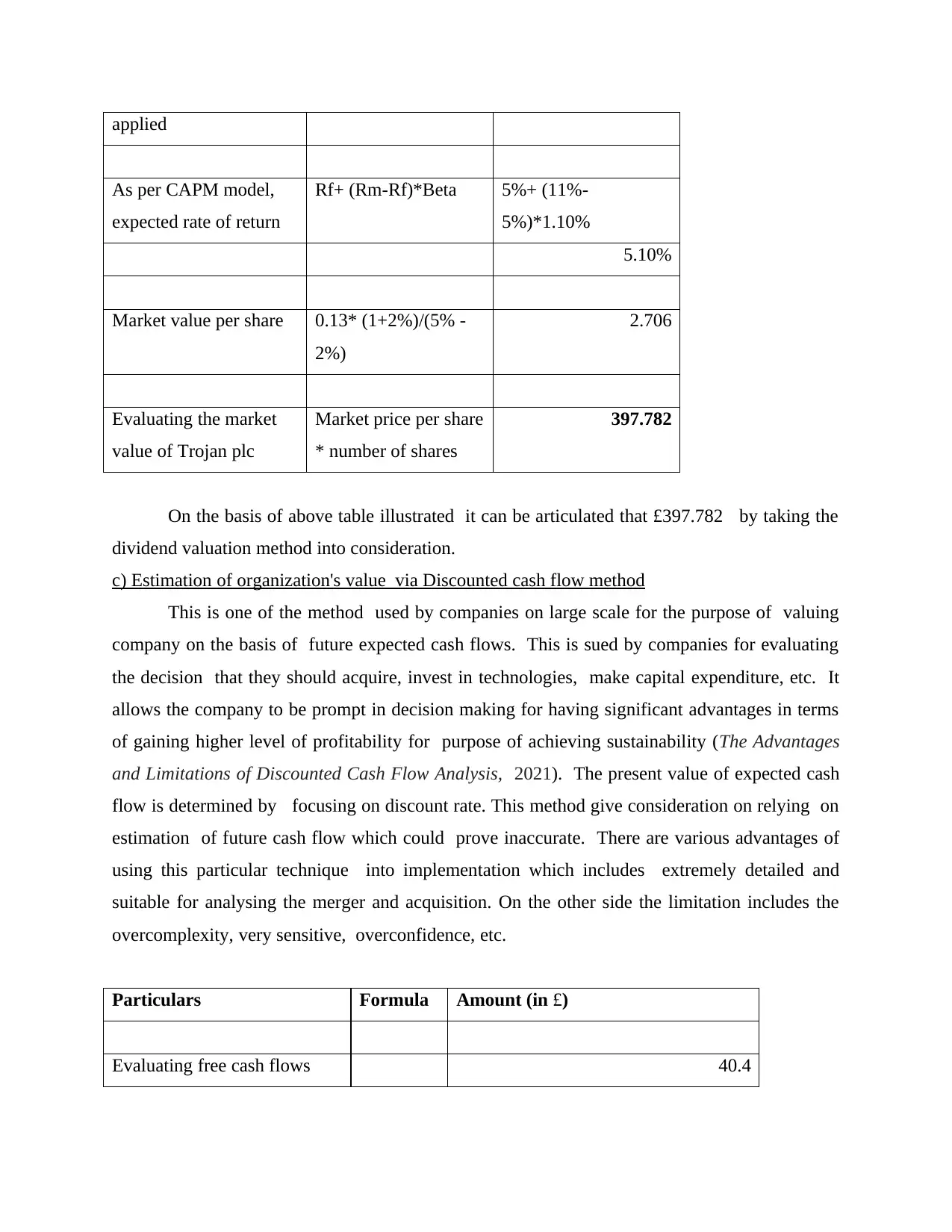

applied

As per CAPM model,

expected rate of return

Rf+ (Rm-Rf)*Beta 5%+ (11%-

5%)*1.10%

5.10%

Market value per share 0.13* (1+2%)/(5% -

2%)

2.706

Evaluating the market

value of Trojan plc

Market price per share

* number of shares

397.782

On the basis of above table illustrated it can be articulated that £397.782 by taking the

dividend valuation method into consideration.

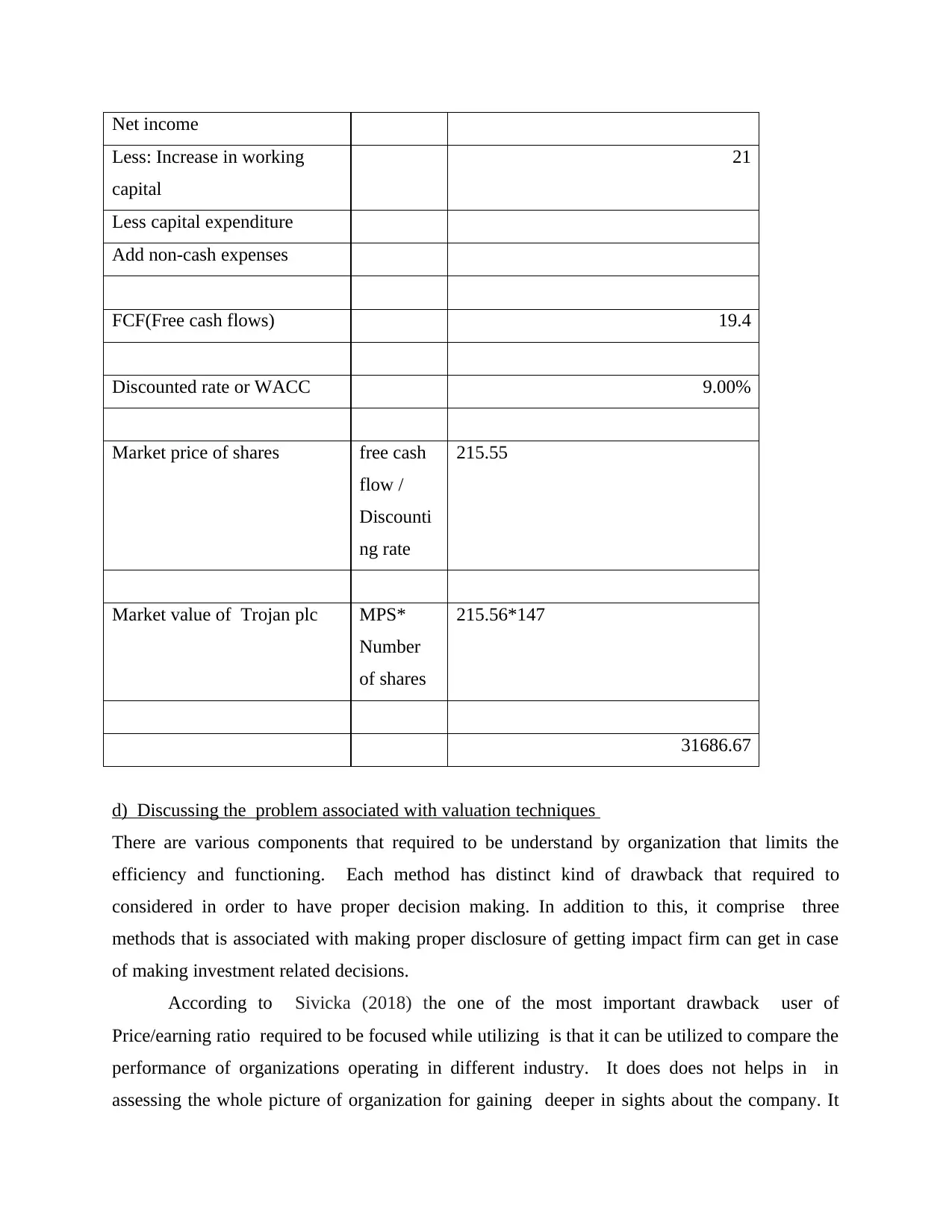

c) Estimation of organization's value via Discounted cash flow method

This is one of the method used by companies on large scale for the purpose of valuing

company on the basis of future expected cash flows. This is sued by companies for evaluating

the decision that they should acquire, invest in technologies, make capital expenditure, etc. It

allows the company to be prompt in decision making for having significant advantages in terms

of gaining higher level of profitability for purpose of achieving sustainability (The Advantages

and Limitations of Discounted Cash Flow Analysis, 2021). The present value of expected cash

flow is determined by focusing on discount rate. This method give consideration on relying on

estimation of future cash flow which could prove inaccurate. There are various advantages of

using this particular technique into implementation which includes extremely detailed and

suitable for analysing the merger and acquisition. On the other side the limitation includes the

overcomplexity, very sensitive, overconfidence, etc.

Particulars Formula Amount (in £)

Evaluating free cash flows 40.4

As per CAPM model,

expected rate of return

Rf+ (Rm-Rf)*Beta 5%+ (11%-

5%)*1.10%

5.10%

Market value per share 0.13* (1+2%)/(5% -

2%)

2.706

Evaluating the market

value of Trojan plc

Market price per share

* number of shares

397.782

On the basis of above table illustrated it can be articulated that £397.782 by taking the

dividend valuation method into consideration.

c) Estimation of organization's value via Discounted cash flow method

This is one of the method used by companies on large scale for the purpose of valuing

company on the basis of future expected cash flows. This is sued by companies for evaluating

the decision that they should acquire, invest in technologies, make capital expenditure, etc. It

allows the company to be prompt in decision making for having significant advantages in terms

of gaining higher level of profitability for purpose of achieving sustainability (The Advantages

and Limitations of Discounted Cash Flow Analysis, 2021). The present value of expected cash

flow is determined by focusing on discount rate. This method give consideration on relying on

estimation of future cash flow which could prove inaccurate. There are various advantages of

using this particular technique into implementation which includes extremely detailed and

suitable for analysing the merger and acquisition. On the other side the limitation includes the

overcomplexity, very sensitive, overconfidence, etc.

Particulars Formula Amount (in £)

Evaluating free cash flows 40.4

Net income

Less: Increase in working

capital

21

Less capital expenditure

Add non-cash expenses

FCF(Free cash flows) 19.4

Discounted rate or WACC 9.00%

Market price of shares free cash

flow /

Discounti

ng rate

215.55

Market value of Trojan plc MPS*

Number

of shares

215.56*147

31686.67

d) Discussing the problem associated with valuation techniques

There are various components that required to be understand by organization that limits the

efficiency and functioning. Each method has distinct kind of drawback that required to

considered in order to have proper decision making. In addition to this, it comprise three

methods that is associated with making proper disclosure of getting impact firm can get in case

of making investment related decisions.

According to Sivicka (2018) the one of the most important drawback user of

Price/earning ratio required to be focused while utilizing is that it can be utilized to compare the

performance of organizations operating in different industry. It does does not helps in in

assessing the whole picture of organization for gaining deeper in sights about the company. It

Less: Increase in working

capital

21

Less capital expenditure

Add non-cash expenses

FCF(Free cash flows) 19.4

Discounted rate or WACC 9.00%

Market price of shares free cash

flow /

Discounti

ng rate

215.55

Market value of Trojan plc MPS*

Number

of shares

215.56*147

31686.67

d) Discussing the problem associated with valuation techniques

There are various components that required to be understand by organization that limits the

efficiency and functioning. Each method has distinct kind of drawback that required to

considered in order to have proper decision making. In addition to this, it comprise three

methods that is associated with making proper disclosure of getting impact firm can get in case

of making investment related decisions.

According to Sivicka (2018) the one of the most important drawback user of

Price/earning ratio required to be focused while utilizing is that it can be utilized to compare the

performance of organizations operating in different industry. It does does not helps in in

assessing the whole picture of organization for gaining deeper in sights about the company. It

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

uses the earning per share which can be misleading in way of decision formulation which needs

to be included while making crucial decision. In against to this, Mellen and Evans, (2018)

depicted that there is no single metric which can provide assistance in analysing that particular

investment looking is good in terms of profitability and stability. There is way in which

organization provides the wrong singles that includes s its information regarding growth rate

that does not always tell that given data is accurate in context of company or not. In against to

this, AYDIN, (2017) articulated that this method of valuing company can not be used for those

organization that are constantly making profits. This makes difficult to take decision in respect

of merger & acquisition and does not accomplish objective of investors concerned with

utilizing valuing method.

In the views of Schueler (2021) organization while utilizing the limitations of dividend

valuation method can obtain distinct kind of drawbacks but one of the significant disadvantage

is that small organization can not utilize it accurately. There is ignorance of non dividend factor

which does not allow to have p[roper decision as all aspects are not considered. The effect of

stock buyback can is as well ignored while valuing the company which is another component

needs to be considered fro avoiding adverse impact on firm. On the other side Tkachenko and

et.al., (2019) articulated that there is large variation in earnings & maintenance of stable

dividend payouts which r helps in analysing assumptions which makes it worthless. There are

are certain personal bias which are sued by investors to make their personal assumptions and

experience. If an investor has the good point of view that they valuation of stock can be exerted

by him in positive manner and vice versa. Most of the assumptions are not in control of

investors which declines the validity of this particular valuation model. In contrast to this, Li

(2020) stated that Taxation rules re a swell not taken into practice while making calculation

which reduces the reliability and efficiency of interpreting values derived. This may not relate

to the earnings which allows it to implicit assumption that is one of the most important

drawback of this action.

From the opinion of Fujiwara and et.al., (2020) there are various types of disadvantages

of discounted cash flow method which highly impact the decision making procedure o

companies. The one of the significant aspect that need to be concentrated by organization is

that relies on large number of assumptions. It decline its accuracy and reliability which mainly

leads to make it complex procedure in turn negative impact on functioning of company can be

to be included while making crucial decision. In against to this, Mellen and Evans, (2018)

depicted that there is no single metric which can provide assistance in analysing that particular

investment looking is good in terms of profitability and stability. There is way in which

organization provides the wrong singles that includes s its information regarding growth rate

that does not always tell that given data is accurate in context of company or not. In against to

this, AYDIN, (2017) articulated that this method of valuing company can not be used for those

organization that are constantly making profits. This makes difficult to take decision in respect

of merger & acquisition and does not accomplish objective of investors concerned with

utilizing valuing method.

In the views of Schueler (2021) organization while utilizing the limitations of dividend

valuation method can obtain distinct kind of drawbacks but one of the significant disadvantage

is that small organization can not utilize it accurately. There is ignorance of non dividend factor

which does not allow to have p[roper decision as all aspects are not considered. The effect of

stock buyback can is as well ignored while valuing the company which is another component

needs to be considered fro avoiding adverse impact on firm. On the other side Tkachenko and

et.al., (2019) articulated that there is large variation in earnings & maintenance of stable

dividend payouts which r helps in analysing assumptions which makes it worthless. There are

are certain personal bias which are sued by investors to make their personal assumptions and

experience. If an investor has the good point of view that they valuation of stock can be exerted

by him in positive manner and vice versa. Most of the assumptions are not in control of

investors which declines the validity of this particular valuation model. In contrast to this, Li

(2020) stated that Taxation rules re a swell not taken into practice while making calculation

which reduces the reliability and efficiency of interpreting values derived. This may not relate

to the earnings which allows it to implicit assumption that is one of the most important

drawback of this action.

From the opinion of Fujiwara and et.al., (2020) there are various types of disadvantages

of discounted cash flow method which highly impact the decision making procedure o

companies. The one of the significant aspect that need to be concentrated by organization is

that relies on large number of assumptions. It decline its accuracy and reliability which mainly

leads to make it complex procedure in turn negative impact on functioning of company can be

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

derived. On the other side, Akkaya (2020) said that there is presence of prone to errors which

leads to result sin higher complexity that tend to give unrealistic assumptions. The reason

behind this can be considered its sensitivity and resistance to change assumptions. On the basis

of these assumptions investors become over confident that ultimately leads to bring

Irrelevance factor provides the decision inappropriately. In contrast to this, Susanto and

Rahadian (2021) articulated that organization may look at company valuation in isolation that

is not appropriate and significant while making comparison among the competitors. Its

challenging to estimate the weighted average cost of capital (WACC) as well terminal value is

difficult to reflect large portion of total components.

QUESTION 3

Particular amount

cash inflow 85000

Less: outflow 12500

Less: depreciation 38958.33

cash inflow after

depreciation

33541.67

Add: depreciation 38958.33

Net cash inflows 72500

a) Payback Period (PP)

Years cash inflows Cumulative cash inflows

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 72500 435000

leads to result sin higher complexity that tend to give unrealistic assumptions. The reason

behind this can be considered its sensitivity and resistance to change assumptions. On the basis

of these assumptions investors become over confident that ultimately leads to bring

Irrelevance factor provides the decision inappropriately. In contrast to this, Susanto and

Rahadian (2021) articulated that organization may look at company valuation in isolation that

is not appropriate and significant while making comparison among the competitors. Its

challenging to estimate the weighted average cost of capital (WACC) as well terminal value is

difficult to reflect large portion of total components.

QUESTION 3

Particular amount

cash inflow 85000

Less: outflow 12500

Less: depreciation 38958.33

cash inflow after

depreciation

33541.67

Add: depreciation 38958.33

Net cash inflows 72500

a) Payback Period (PP)

Years cash inflows Cumulative cash inflows

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 72500 435000

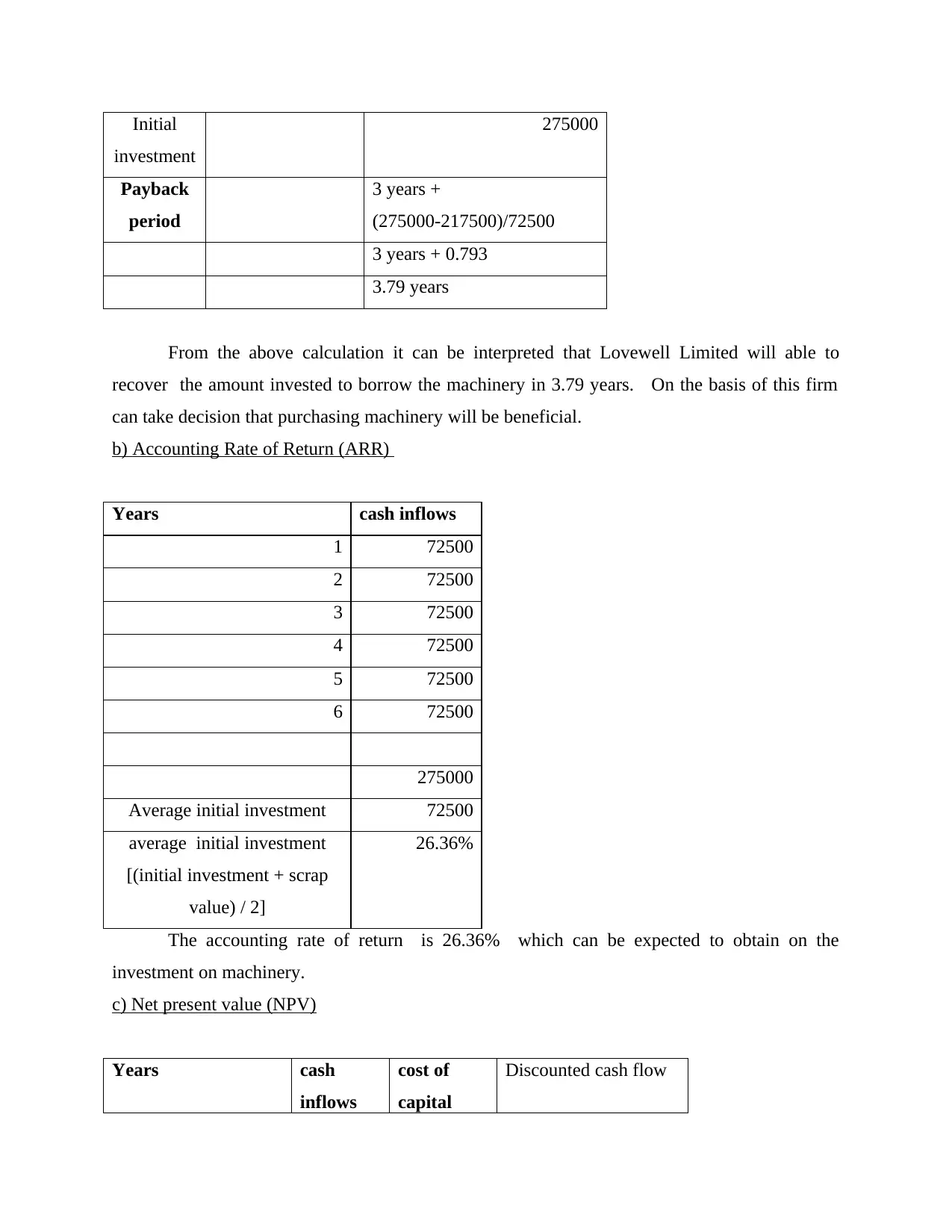

Initial

investment

275000

Payback

period

3 years +

(275000-217500)/72500

3 years + 0.793

3.79 years

From the above calculation it can be interpreted that Lovewell Limited will able to

recover the amount invested to borrow the machinery in 3.79 years. On the basis of this firm

can take decision that purchasing machinery will be beneficial.

b) Accounting Rate of Return (ARR)

Years cash inflows

1 72500

2 72500

3 72500

4 72500

5 72500

6 72500

275000

Average initial investment 72500

average initial investment

[(initial investment + scrap

value) / 2]

26.36%

The accounting rate of return is 26.36% which can be expected to obtain on the

investment on machinery.

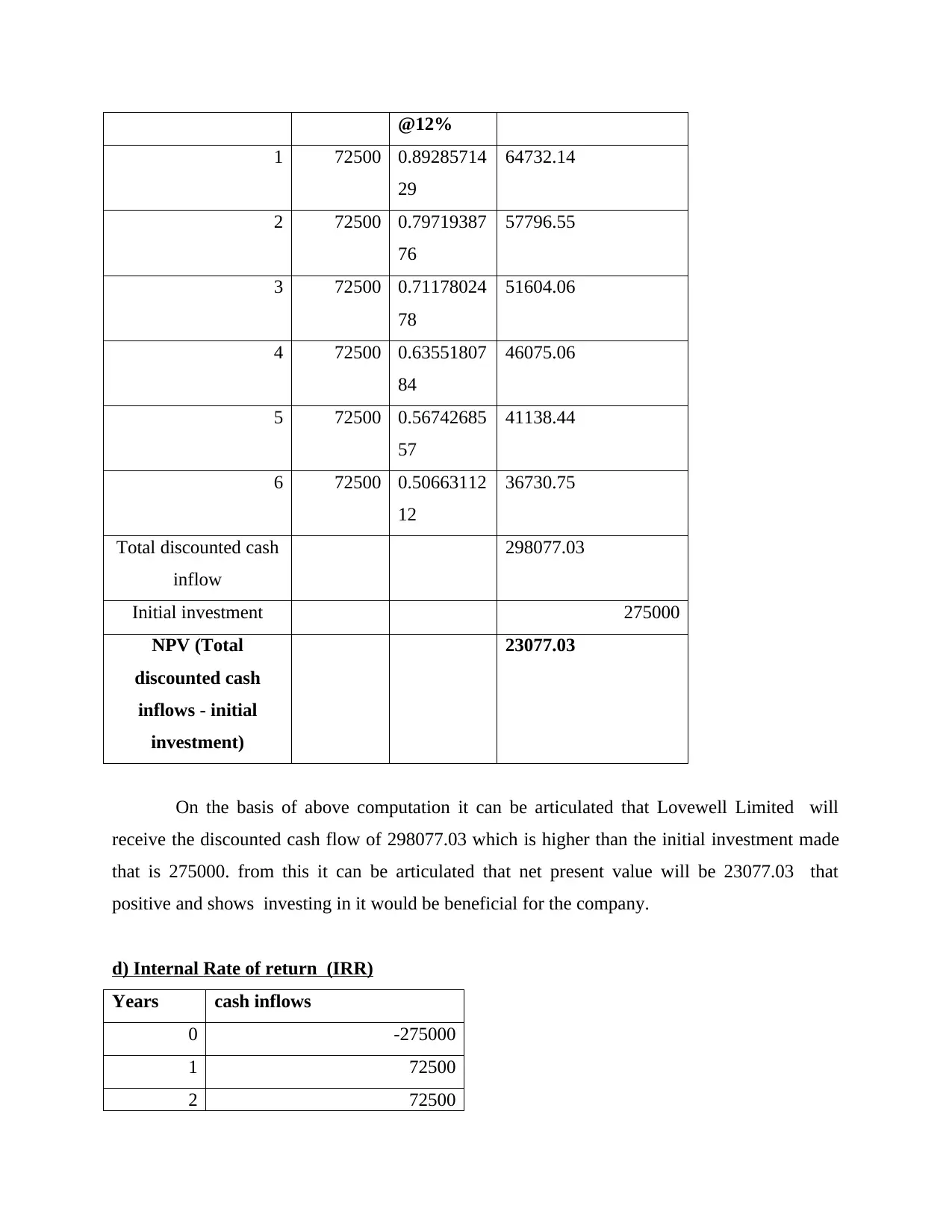

c) Net present value (NPV)

Years cash

inflows

cost of

capital

Discounted cash flow

investment

275000

Payback

period

3 years +

(275000-217500)/72500

3 years + 0.793

3.79 years

From the above calculation it can be interpreted that Lovewell Limited will able to

recover the amount invested to borrow the machinery in 3.79 years. On the basis of this firm

can take decision that purchasing machinery will be beneficial.

b) Accounting Rate of Return (ARR)

Years cash inflows

1 72500

2 72500

3 72500

4 72500

5 72500

6 72500

275000

Average initial investment 72500

average initial investment

[(initial investment + scrap

value) / 2]

26.36%

The accounting rate of return is 26.36% which can be expected to obtain on the

investment on machinery.

c) Net present value (NPV)

Years cash

inflows

cost of

capital

Discounted cash flow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

@12%

1 72500 0.89285714

29

64732.14

2 72500 0.79719387

76

57796.55

3 72500 0.71178024

78

51604.06

4 72500 0.63551807

84

46075.06

5 72500 0.56742685

57

41138.44

6 72500 0.50663112

12

36730.75

Total discounted cash

inflow

298077.03

Initial investment 275000

NPV (Total

discounted cash

inflows - initial

investment)

23077.03

On the basis of above computation it can be articulated that Lovewell Limited will

receive the discounted cash flow of 298077.03 which is higher than the initial investment made

that is 275000. from this it can be articulated that net present value will be 23077.03 that

positive and shows investing in it would be beneficial for the company.

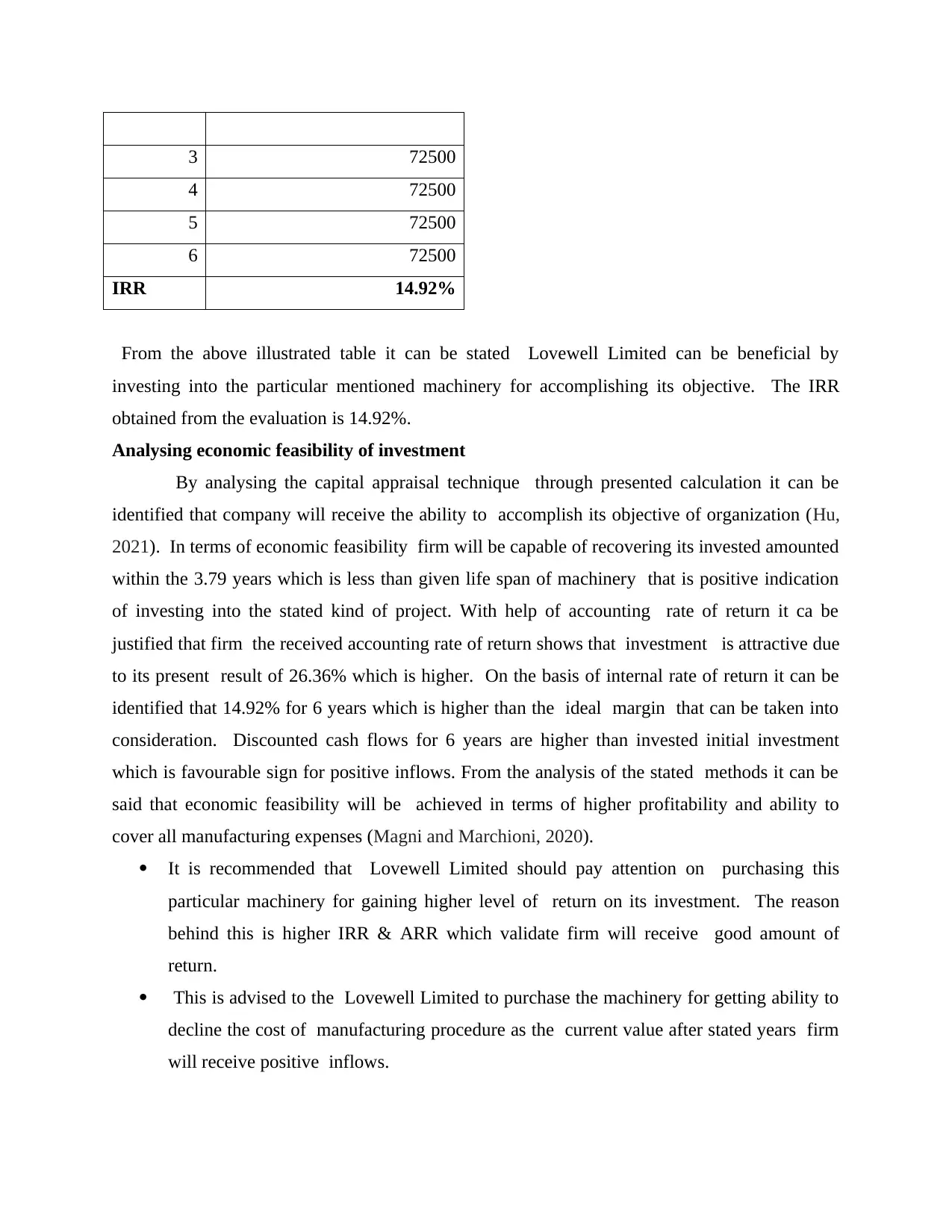

d) Internal Rate of return (IRR)

Years cash inflows

0 -275000

1 72500

2 72500

1 72500 0.89285714

29

64732.14

2 72500 0.79719387

76

57796.55

3 72500 0.71178024

78

51604.06

4 72500 0.63551807

84

46075.06

5 72500 0.56742685

57

41138.44

6 72500 0.50663112

12

36730.75

Total discounted cash

inflow

298077.03

Initial investment 275000

NPV (Total

discounted cash

inflows - initial

investment)

23077.03

On the basis of above computation it can be articulated that Lovewell Limited will

receive the discounted cash flow of 298077.03 which is higher than the initial investment made

that is 275000. from this it can be articulated that net present value will be 23077.03 that

positive and shows investing in it would be beneficial for the company.

d) Internal Rate of return (IRR)

Years cash inflows

0 -275000

1 72500

2 72500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3 72500

4 72500

5 72500

6 72500

IRR 14.92%

From the above illustrated table it can be stated Lovewell Limited can be beneficial by

investing into the particular mentioned machinery for accomplishing its objective. The IRR

obtained from the evaluation is 14.92%.

Analysing economic feasibility of investment

By analysing the capital appraisal technique through presented calculation it can be

identified that company will receive the ability to accomplish its objective of organization (Hu,

2021). In terms of economic feasibility firm will be capable of recovering its invested amounted

within the 3.79 years which is less than given life span of machinery that is positive indication

of investing into the stated kind of project. With help of accounting rate of return it ca be

justified that firm the received accounting rate of return shows that investment is attractive due

to its present result of 26.36% which is higher. On the basis of internal rate of return it can be

identified that 14.92% for 6 years which is higher than the ideal margin that can be taken into

consideration. Discounted cash flows for 6 years are higher than invested initial investment

which is favourable sign for positive inflows. From the analysis of the stated methods it can be

said that economic feasibility will be achieved in terms of higher profitability and ability to

cover all manufacturing expenses (Magni and Marchioni, 2020).

It is recommended that Lovewell Limited should pay attention on purchasing this

particular machinery for gaining higher level of return on its investment. The reason

behind this is higher IRR & ARR which validate firm will receive good amount of

return.

This is advised to the Lovewell Limited to purchase the machinery for getting ability to

decline the cost of manufacturing procedure as the current value after stated years firm

will receive positive inflows.

4 72500

5 72500

6 72500

IRR 14.92%

From the above illustrated table it can be stated Lovewell Limited can be beneficial by

investing into the particular mentioned machinery for accomplishing its objective. The IRR

obtained from the evaluation is 14.92%.

Analysing economic feasibility of investment

By analysing the capital appraisal technique through presented calculation it can be

identified that company will receive the ability to accomplish its objective of organization (Hu,

2021). In terms of economic feasibility firm will be capable of recovering its invested amounted

within the 3.79 years which is less than given life span of machinery that is positive indication

of investing into the stated kind of project. With help of accounting rate of return it ca be

justified that firm the received accounting rate of return shows that investment is attractive due

to its present result of 26.36% which is higher. On the basis of internal rate of return it can be

identified that 14.92% for 6 years which is higher than the ideal margin that can be taken into

consideration. Discounted cash flows for 6 years are higher than invested initial investment

which is favourable sign for positive inflows. From the analysis of the stated methods it can be

said that economic feasibility will be achieved in terms of higher profitability and ability to

cover all manufacturing expenses (Magni and Marchioni, 2020).

It is recommended that Lovewell Limited should pay attention on purchasing this

particular machinery for gaining higher level of return on its investment. The reason

behind this is higher IRR & ARR which validate firm will receive good amount of

return.

This is advised to the Lovewell Limited to purchase the machinery for getting ability to

decline the cost of manufacturing procedure as the current value after stated years firm

will receive positive inflows.

Evaluating the benefits and drawbacks of capital appraisal techniques

Capital appraisal is one of the important tool that can be used by organization for analysing the

each aspects that can influence processing of company. It comprises four methods which affect

both positively & negatively.

Net Present Value

This method is concerned with analysing the current value of the money after selected

life span of particular project (Moro Visconti, 2019). There are certain advantages and

disadvantages that organization can achieve are as follows:

Advantages:

The foremost benefit of utilizing this approach is that it accepts conventional cash flows

pattern that allows the firm to get accurate knowledge regarding the future outcomes.

There is possibility of having good measure of profitability that can permit enterprise to

make strategic decision for having leading position in the industry (Idehen, 2021).

Net present value can provide assistance in analysing the risk factors which can hinder

the performance of business. There is assumption of reinvestment which allows the firm

to take full picture of potential results.

Disadvantages

This method is not capable of determining the required rate of return which does not

provide the convenience in having proper analysis of investment. If there is difference in

size of projects can not give accurate outcomes.

It might not boost the EPS & return on equity that can lead to inappropriate decision

formulation of decision (Tastulekova, Satova and Shalbolova, 2018.). Higher chances

are seen in optimistic projection which does not allow the estimation of opportunity

cost.

Internal Rate of Return

It is the interest rate where NPV of all cash flows from investment equal to needed

capital investment if the it falls below the required margin of return than indicates that project

should be avoided and vice versa. Enterprise can get different kinds of pros and cons by

applying this particular kind of capital appraisal technique.

Pros

Capital appraisal is one of the important tool that can be used by organization for analysing the

each aspects that can influence processing of company. It comprises four methods which affect

both positively & negatively.

Net Present Value

This method is concerned with analysing the current value of the money after selected

life span of particular project (Moro Visconti, 2019). There are certain advantages and

disadvantages that organization can achieve are as follows:

Advantages:

The foremost benefit of utilizing this approach is that it accepts conventional cash flows

pattern that allows the firm to get accurate knowledge regarding the future outcomes.

There is possibility of having good measure of profitability that can permit enterprise to

make strategic decision for having leading position in the industry (Idehen, 2021).

Net present value can provide assistance in analysing the risk factors which can hinder

the performance of business. There is assumption of reinvestment which allows the firm

to take full picture of potential results.

Disadvantages

This method is not capable of determining the required rate of return which does not

provide the convenience in having proper analysis of investment. If there is difference in

size of projects can not give accurate outcomes.

It might not boost the EPS & return on equity that can lead to inappropriate decision

formulation of decision (Tastulekova, Satova and Shalbolova, 2018.). Higher chances

are seen in optimistic projection which does not allow the estimation of opportunity

cost.

Internal Rate of Return

It is the interest rate where NPV of all cash flows from investment equal to needed

capital investment if the it falls below the required margin of return than indicates that project

should be avoided and vice versa. Enterprise can get different kinds of pros and cons by

applying this particular kind of capital appraisal technique.

Pros

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.