Financial Management Principles and Ratio Analysis Report

VerifiedAdded on 2023/01/11

|21

|5503

|48

Report

AI Summary

This report delves into the core principles of financial management, examining various approaches and methods for effective decision-making within organizations. It explores the significance of knowledge-based, formal, and informal approaches, emphasizing the role of stakeholders and the complexities of managing conflicting objectives among different stakeholder groups. The report further analyzes the value of management accounting techniques, including budgetary control and standard costing, in cost control and profit maximization. It also addresses fraud detection and prevention techniques, along with ethical decision-making processes. Scenario A evaluates decision-making, stakeholder management, and ethical considerations. Scenario B focuses on financial ratio analysis of Morrison Supermarkets PLC for the years 2020, 2019, and 2018, applying the data obtained in decision-making, evaluating investment appraisal techniques, and discussing long-term sustainability. The report concludes with recommendations for improving financial sustainability and the value of these techniques in informed decision making.

Principle of financial

management

management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION......................................................................................................................3

Scenario A..................................................................................................................................3

Evaluating approaches, methods and the factors that helps an organization in making

effective decisions .................................................................................................................3

Stakeholder management and managing conflicting purpose of different kind of the

stakeholder groups .................................................................................................................4

Value of management accounting techniques........................................................................5

Techniques for fraud detection and prevention and approach to ethical decision making....6

Reflection...............................................................................................................................6

Scenario B..................................................................................................................................7

Financial ratios analysis of Morrison Supermarkets PLC for the year 2020, 2019 & 2018. .7

Application of data obtained in decision making.................................................................14

Outcomes of investment appraisal techniques utilized in taking actions to maximise ROI 14

Value of the techniques that is used in informed decision making......................................15

Long term sustainability through financial decision making...............................................15

Recommendations to improve financial sustainability........................................................15

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................17

APPENDIX..............................................................................................................................19

INTRODUCTION......................................................................................................................3

Scenario A..................................................................................................................................3

Evaluating approaches, methods and the factors that helps an organization in making

effective decisions .................................................................................................................3

Stakeholder management and managing conflicting purpose of different kind of the

stakeholder groups .................................................................................................................4

Value of management accounting techniques........................................................................5

Techniques for fraud detection and prevention and approach to ethical decision making....6

Reflection...............................................................................................................................6

Scenario B..................................................................................................................................7

Financial ratios analysis of Morrison Supermarkets PLC for the year 2020, 2019 & 2018. .7

Application of data obtained in decision making.................................................................14

Outcomes of investment appraisal techniques utilized in taking actions to maximise ROI 14

Value of the techniques that is used in informed decision making......................................15

Long term sustainability through financial decision making...............................................15

Recommendations to improve financial sustainability........................................................15

CONCLUSION........................................................................................................................16

REFERENCES.........................................................................................................................17

APPENDIX..............................................................................................................................19

INTRODUCTION

Financial management is the process which focusses on all the management function

from the financial perspectives such as procurement and optimum utilization of the funds. It

mainly refers to the application of the principles of management to the financial resources.

This report presents about the importance of management accounting and its techniques in

making informed decisions which helps in sustainable growth along with the ratio analysis of

the Morrisons plc.

Scenario A

Evaluating approaches, methods and the factors that helps an organization in making

effective decisions

Knowledge based approach- The knowledge-based decision-making approach uses

a pre-determined criterion to measure and ensure that the outcome for the desired topic is

optimal. The main objective of this type of decision-making process is to ensure that strategic

decisions are made by using an effective approach and thought process. It also involves a

collective understanding of the background about the concerned topic (Valaskova, Bartosova

and Kubala, 2019). The key elements of knowledge-based approach include open

communication between leaders and members, equal information access and mutual trust

within the organization. By adequate implementation of these elements, an organization is

bound to make strategic business decisions that will help in its achievement of goals and

objectives.

Formal approach- Formal approach of decision making is said to be the most

balanced approach because it involves clarity in allocation of tasks and responsibilities which

means that all the employees are aware of their duties which further helps in the making of

strong and effective decisions (Shaofan and et.al., 2019). The formal approach is time

consuming but also has the highest success ratio as compared to other approaches. Also, it

helps in building equality and long-term trust within the members of the company that further

helps them in the accomplishment of assigned goals.

Informal approach- Informal approach includes making decisions on the basis of

subjective, holistic and past experience. Informal decisions are faster to implement and

require less efforts & coordination but at the same time these decisions are riskier (Reid and

Sanders, 2019). It is generally suitable for small scale organization as it gives the reward of

high risk, high rewards. However, every company should take informal decisions after heavy

research and planning. For instance- A member of staff or teh temporary employee hwho is

feeling that he is being treated in a wrong way.

Role of the stakeholders with respect to decision making- Stakeholders are the

group of people that are interested in the performance of the company, it includes

shareholders, investors, creditors, government and customers. Thus, it is important for an

organization to consider its stakeholders before taking the final decisions, the firm must

refrain itself from taking complex decisions as it can affect its stakeholders in a negative

manner and further reduce the revenue of the business. Furthermore, the company must

consider the issues raised by the people and should make appropriate decisions b keeping

those points in mind.

Making or buying decisions- The make or buy decision can be defined as an

approach of making strategic decision between manufacturing or producing an item internally

Financial management is the process which focusses on all the management function

from the financial perspectives such as procurement and optimum utilization of the funds. It

mainly refers to the application of the principles of management to the financial resources.

This report presents about the importance of management accounting and its techniques in

making informed decisions which helps in sustainable growth along with the ratio analysis of

the Morrisons plc.

Scenario A

Evaluating approaches, methods and the factors that helps an organization in making

effective decisions

Knowledge based approach- The knowledge-based decision-making approach uses

a pre-determined criterion to measure and ensure that the outcome for the desired topic is

optimal. The main objective of this type of decision-making process is to ensure that strategic

decisions are made by using an effective approach and thought process. It also involves a

collective understanding of the background about the concerned topic (Valaskova, Bartosova

and Kubala, 2019). The key elements of knowledge-based approach include open

communication between leaders and members, equal information access and mutual trust

within the organization. By adequate implementation of these elements, an organization is

bound to make strategic business decisions that will help in its achievement of goals and

objectives.

Formal approach- Formal approach of decision making is said to be the most

balanced approach because it involves clarity in allocation of tasks and responsibilities which

means that all the employees are aware of their duties which further helps in the making of

strong and effective decisions (Shaofan and et.al., 2019). The formal approach is time

consuming but also has the highest success ratio as compared to other approaches. Also, it

helps in building equality and long-term trust within the members of the company that further

helps them in the accomplishment of assigned goals.

Informal approach- Informal approach includes making decisions on the basis of

subjective, holistic and past experience. Informal decisions are faster to implement and

require less efforts & coordination but at the same time these decisions are riskier (Reid and

Sanders, 2019). It is generally suitable for small scale organization as it gives the reward of

high risk, high rewards. However, every company should take informal decisions after heavy

research and planning. For instance- A member of staff or teh temporary employee hwho is

feeling that he is being treated in a wrong way.

Role of the stakeholders with respect to decision making- Stakeholders are the

group of people that are interested in the performance of the company, it includes

shareholders, investors, creditors, government and customers. Thus, it is important for an

organization to consider its stakeholders before taking the final decisions, the firm must

refrain itself from taking complex decisions as it can affect its stakeholders in a negative

manner and further reduce the revenue of the business. Furthermore, the company must

consider the issues raised by the people and should make appropriate decisions b keeping

those points in mind.

Making or buying decisions- The make or buy decision can be defined as an

approach of making strategic decision between manufacturing or producing an item internally

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

or purchasing it from the external party like suppliers which is also referred to as outsourcing

(Ghazinoory and et.al., 2019). It is imperative for the business to analyze and interpret

whether it can achieve financial benefit through or making or purchasing and then take the

appropriate decision accordingly.

Limiting factor assessment- The limiting factor assessment involves the restriction

of an organization’s ability to increase its sales due to demand constraints or the availability

of production resources. Thus, an organization needs to take decisions on which factor should

it limit like raw materials, labor, money that would not affect its operations.

Key factor analysis- Key factor analysis is the method of decision making that

involves making strategic decision of using limited factors. It is concerned with the use of

limiting factors effectively and efficiently.

Stakeholder management and managing conflicting purpose of different kind of the

stakeholder groups

Effective management of stakeholder can be done by the company in complying or

considering various principles that are as follows-

Setting objective in order to achieve financial objectives- Setting of goals and

objectives is imperative for every organization to succeed as it helps the company in

developing a budget plan that it can follow to achieve financial success. The company must

make sure that it has set up SMART (specific, measurable, attainable, realistic, time bound)

goals and it can help in increasing their profitability.

Ethical FM- Ethical financial management means balancing, protecting and

preserving stakeholders’ interests. It is important to do so because ethics define what is right

and what is wrong which means that it I the duty of company to take care of its employees,

customers, government, investors and creditors, and to protect their interest within the

company. Moreover, the business should also follow its corporate social responsibility and

should not indulge in any unethical or illegal activities that cause harm to the society and its

stakeholders (Kostopoulos, 2019). It must not involve in forgery, manipulation and insiders

trading and should perform its financial/ business activities with complete honesty and

loyalty and should ensure complete transparency with its stakeholders by providing them

with accurate accounting information, financial reports and statements. This will be

beneficial for the business in long run as it will lead to building strong trust between both the

parties and help the firm in achieving long term success.

Maximizing wealth of the shareholders- It reflects that shareholders must provided

with maximum return and it is counted as the major objective of all the corporations. In

context of financial management, it means increasing the price or value of an entity’s

common stock. In order to achieve this objective, managers’ takes into account risk and the

timing attached with the expected earnings per share for maximizing price of company’s

shares. When this has been properly implemented, management would also leads to

maximizing dividends and the capital gains which accrue to its respective stakeholders. More

(Ghazinoory and et.al., 2019). It is imperative for the business to analyze and interpret

whether it can achieve financial benefit through or making or purchasing and then take the

appropriate decision accordingly.

Limiting factor assessment- The limiting factor assessment involves the restriction

of an organization’s ability to increase its sales due to demand constraints or the availability

of production resources. Thus, an organization needs to take decisions on which factor should

it limit like raw materials, labor, money that would not affect its operations.

Key factor analysis- Key factor analysis is the method of decision making that

involves making strategic decision of using limited factors. It is concerned with the use of

limiting factors effectively and efficiently.

Stakeholder management and managing conflicting purpose of different kind of the

stakeholder groups

Effective management of stakeholder can be done by the company in complying or

considering various principles that are as follows-

Setting objective in order to achieve financial objectives- Setting of goals and

objectives is imperative for every organization to succeed as it helps the company in

developing a budget plan that it can follow to achieve financial success. The company must

make sure that it has set up SMART (specific, measurable, attainable, realistic, time bound)

goals and it can help in increasing their profitability.

Ethical FM- Ethical financial management means balancing, protecting and

preserving stakeholders’ interests. It is important to do so because ethics define what is right

and what is wrong which means that it I the duty of company to take care of its employees,

customers, government, investors and creditors, and to protect their interest within the

company. Moreover, the business should also follow its corporate social responsibility and

should not indulge in any unethical or illegal activities that cause harm to the society and its

stakeholders (Kostopoulos, 2019). It must not involve in forgery, manipulation and insiders

trading and should perform its financial/ business activities with complete honesty and

loyalty and should ensure complete transparency with its stakeholders by providing them

with accurate accounting information, financial reports and statements. This will be

beneficial for the business in long run as it will lead to building strong trust between both the

parties and help the firm in achieving long term success.

Maximizing wealth of the shareholders- It reflects that shareholders must provided

with maximum return and it is counted as the major objective of all the corporations. In

context of financial management, it means increasing the price or value of an entity’s

common stock. In order to achieve this objective, managers’ takes into account risk and the

timing attached with the expected earnings per share for maximizing price of company’s

shares. When this has been properly implemented, management would also leads to

maximizing dividends and the capital gains which accrue to its respective stakeholders. More

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

defensible form of the shareholder wealth maximization looks for longer term instead of

shorter term increment.

Delivering sustainable growth in long run- It relates to protecting an entity’s capital

base which is counted as the well-accepted principle of business. Achieving sustainable

development helps in integrating measurement and the planning systems of the business

organization (Goodman and et.al., 2020). It means as adopting the suitable activities and the

business strategies that helps in meeting need of an enterprise and its respective stakeholders

at present along with protecting, enhancing & sustaining natural and the human resources

which would be required in future.

Value of management accounting techniques

There are mainly two types of standards which can be used for cost control, that is,

internal and external standards. The external standards are used for mainly used for

comparing the performance of the company with respect to the other firms within the industry

using the financial ratios. In contrast to it, internal standards are used for evaluating the infra

firm cost elements such as material, labour etc. Some of the internal control management

accounting techniques are stated below.

Budgetary control

It is derived from the budget as it uses budget for implementing the budgetary control

as a means of planning and controlling the various types of organizational activities. It

establishes the predetermined objectives which is further used as a basis for the purpose of

measuring the performance (Chand, 2019). Under budgetary control, actual outcome is

compared with the budgeted targets and in case any deviation is there, causes for the same is

identified and also remedial actions can be taken to rectify the mistakes. The budgetary

control helps in maximizing the utilization of limited resources in an effective way and

establishes proper coordination among the members. This helps in effective profit planning

and if implemented successfully will result into increase in profits which will lead to increase

in the shareholders’ value.

Standard costing

It is the most widely used system for exercising the cost control. Under this technique,

the aim is to establish the standards of performance along the target costs which the company

is required to achieve within the set working conditions. It is mainly the pre-determined cost

that determines the what each product would cost under the given set of conditions.It initiates

with the future estimate of the product with respect to its cost in a future period then standard

costs are set by gathering al the relevant information from different sources. This technique

establishes the yardstick based on which the performance of the company is measured that

helps in exercising the control which is means for cost reduction and this consequently leads

to increase in profits leading to increase in the shareholders value which is beneficial for both

the company and the shareholders.

shorter term increment.

Delivering sustainable growth in long run- It relates to protecting an entity’s capital

base which is counted as the well-accepted principle of business. Achieving sustainable

development helps in integrating measurement and the planning systems of the business

organization (Goodman and et.al., 2020). It means as adopting the suitable activities and the

business strategies that helps in meeting need of an enterprise and its respective stakeholders

at present along with protecting, enhancing & sustaining natural and the human resources

which would be required in future.

Value of management accounting techniques

There are mainly two types of standards which can be used for cost control, that is,

internal and external standards. The external standards are used for mainly used for

comparing the performance of the company with respect to the other firms within the industry

using the financial ratios. In contrast to it, internal standards are used for evaluating the infra

firm cost elements such as material, labour etc. Some of the internal control management

accounting techniques are stated below.

Budgetary control

It is derived from the budget as it uses budget for implementing the budgetary control

as a means of planning and controlling the various types of organizational activities. It

establishes the predetermined objectives which is further used as a basis for the purpose of

measuring the performance (Chand, 2019). Under budgetary control, actual outcome is

compared with the budgeted targets and in case any deviation is there, causes for the same is

identified and also remedial actions can be taken to rectify the mistakes. The budgetary

control helps in maximizing the utilization of limited resources in an effective way and

establishes proper coordination among the members. This helps in effective profit planning

and if implemented successfully will result into increase in profits which will lead to increase

in the shareholders’ value.

Standard costing

It is the most widely used system for exercising the cost control. Under this technique,

the aim is to establish the standards of performance along the target costs which the company

is required to achieve within the set working conditions. It is mainly the pre-determined cost

that determines the what each product would cost under the given set of conditions.It initiates

with the future estimate of the product with respect to its cost in a future period then standard

costs are set by gathering al the relevant information from different sources. This technique

establishes the yardstick based on which the performance of the company is measured that

helps in exercising the control which is means for cost reduction and this consequently leads

to increase in profits leading to increase in the shareholders value which is beneficial for both

the company and the shareholders.

Techniques for fraud detection and prevention and approach to ethical decision making

Fraud can be caused because of scams or fudging the financial reports or theft the

own employer. The businesses and government agencies all across the world have

sufferedthe loss of hundreds of billions in lost or the misused funds because of unethical

practices causing an irreversible damage to the company’s reputation and affecting the

customer trust (Kulikova and Satdarova, 2016). When the matter gets worse, it forces

organizations to force cut down it staff and stop the spending. The focus has been shifting to

internal audit departments who are now required to implement the fraud prevention and

detection measures. Some of the key techniques that can be used by the organizations for

preventing and detecting fraudare stated below.

Listing the potential areas of fraud

The most important thing that the organization should do is to list down the areas

where there are higher chances of detecting fraud along with the type (Halbouni, Obeid and

Garbou, 2016). Then quantify the risk associated with it with impact of it on the organization.

Also, company should focus that type of risk that has a direct connection with the shareholder

value.

Implementing continuous auditing and monitoring

By introducing continuous auditing and monitoring of the transaction will help in

checking the validity the same and also it will set up the scripts which will run against the

large volume of data with the purpose of identifying the any anomalies. This method will

improve the efficiency, consistency and the quality of the fraud detection.

Communicating the monitoring activity to all the members of the organization

For preventing fraud, the major step that can be taken is the communicating about

fraud detection system which may cause the alert in the organization which will reduce the

chances of breaching the controls system. this is the great preventive measure as people

already knows that if they will try, they will get caught.

For it to be successful it is essential to have encourage the approach of ethical

decision making in the top-down approach which will set an example for the organization.

Reflection

After evaluating all these 4 questions, I can say that management accounting is very

important from the business perspective. The wide range of techniques and tools it has will

assist the business organization in effective decision-making process. These approaches are

designed in such a way that it will meet the various business requirements. Taking into

consideration various aspects before taking decisions such as financial and non-financial

aspects. The role of stakeholders in an organization is also crucial and therefore, proper

management of the stakeholders is very essential for the organization. There are two types of

stakeholders internal and external each having their own aims and objective and on the other

side is organization which is having its own mission and vision. Thus, there are chances of

conflict of interest which is management is required to mitigate in order to run the

organization smoothly. I have learned that decisions should be taken by considering that the

interest of any particular group is not promoted or being decreased. Also, decisions are taken

by understanding the impact of it on the company’s stakeholders otherwise it will affect the

shareholders value. The various techniques that can be used for the purpose of managing the

cost and maximising the shareholders’ value which is beneficial for the company. Fraud

which is the major problem that every organization is facing can be reduced or mitigated by

Fraud can be caused because of scams or fudging the financial reports or theft the

own employer. The businesses and government agencies all across the world have

sufferedthe loss of hundreds of billions in lost or the misused funds because of unethical

practices causing an irreversible damage to the company’s reputation and affecting the

customer trust (Kulikova and Satdarova, 2016). When the matter gets worse, it forces

organizations to force cut down it staff and stop the spending. The focus has been shifting to

internal audit departments who are now required to implement the fraud prevention and

detection measures. Some of the key techniques that can be used by the organizations for

preventing and detecting fraudare stated below.

Listing the potential areas of fraud

The most important thing that the organization should do is to list down the areas

where there are higher chances of detecting fraud along with the type (Halbouni, Obeid and

Garbou, 2016). Then quantify the risk associated with it with impact of it on the organization.

Also, company should focus that type of risk that has a direct connection with the shareholder

value.

Implementing continuous auditing and monitoring

By introducing continuous auditing and monitoring of the transaction will help in

checking the validity the same and also it will set up the scripts which will run against the

large volume of data with the purpose of identifying the any anomalies. This method will

improve the efficiency, consistency and the quality of the fraud detection.

Communicating the monitoring activity to all the members of the organization

For preventing fraud, the major step that can be taken is the communicating about

fraud detection system which may cause the alert in the organization which will reduce the

chances of breaching the controls system. this is the great preventive measure as people

already knows that if they will try, they will get caught.

For it to be successful it is essential to have encourage the approach of ethical

decision making in the top-down approach which will set an example for the organization.

Reflection

After evaluating all these 4 questions, I can say that management accounting is very

important from the business perspective. The wide range of techniques and tools it has will

assist the business organization in effective decision-making process. These approaches are

designed in such a way that it will meet the various business requirements. Taking into

consideration various aspects before taking decisions such as financial and non-financial

aspects. The role of stakeholders in an organization is also crucial and therefore, proper

management of the stakeholders is very essential for the organization. There are two types of

stakeholders internal and external each having their own aims and objective and on the other

side is organization which is having its own mission and vision. Thus, there are chances of

conflict of interest which is management is required to mitigate in order to run the

organization smoothly. I have learned that decisions should be taken by considering that the

interest of any particular group is not promoted or being decreased. Also, decisions are taken

by understanding the impact of it on the company’s stakeholders otherwise it will affect the

shareholders value. The various techniques that can be used for the purpose of managing the

cost and maximising the shareholders’ value which is beneficial for the company. Fraud

which is the major problem that every organization is facing can be reduced or mitigated by

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the application of various techniques and tools and also it will help in detecting that would

have occurred. Apart from this, the busienss organization is also required to effectively

establish the internal control system for timely monitoring the busienss activities and

processes.

Scenario B

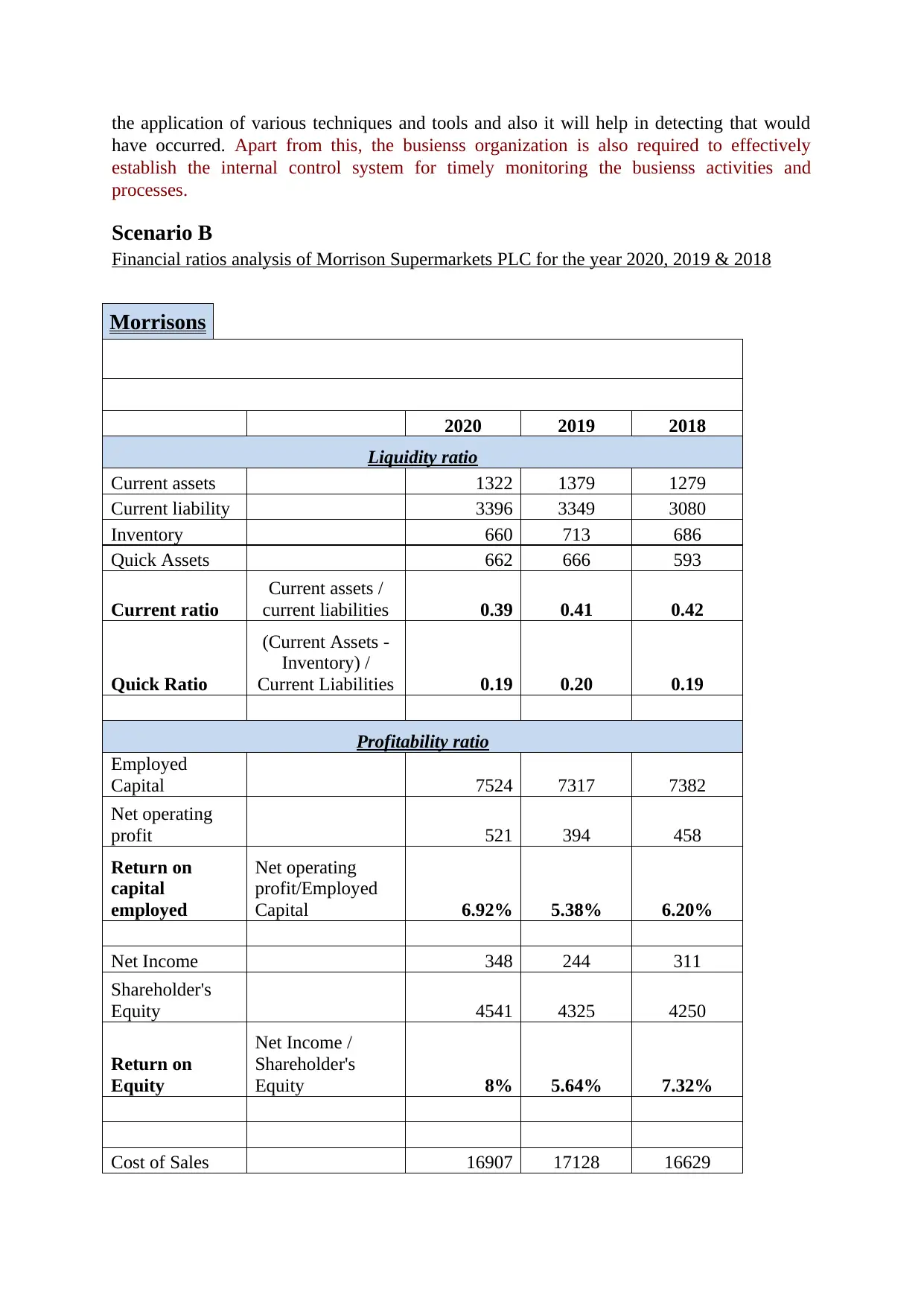

Financial ratios analysis of Morrison Supermarkets PLC for the year 2020, 2019 & 2018

Morrisons

2020 2019 2018

Liquidity ratio

Current assets 1322 1379 1279

Current liability 3396 3349 3080

Inventory 660 713 686

Quick Assets 662 666 593

Current ratio

Current assets /

current liabilities 0.39 0.41 0.42

Quick Ratio

(Current Assets -

Inventory) /

Current Liabilities 0.19 0.20 0.19

Profitability ratio

Employed

Capital 7524 7317 7382

Net operating

profit 521 394 458

Return on

capital

employed

Net operating

profit/Employed

Capital 6.92% 5.38% 6.20%

Net Income 348 244 311

Shareholder's

Equity 4541 4325 4250

Return on

Equity

Net Income /

Shareholder's

Equity 8% 5.64% 7.32%

Cost of Sales 16907 17128 16629

have occurred. Apart from this, the busienss organization is also required to effectively

establish the internal control system for timely monitoring the busienss activities and

processes.

Scenario B

Financial ratios analysis of Morrison Supermarkets PLC for the year 2020, 2019 & 2018

Morrisons

2020 2019 2018

Liquidity ratio

Current assets 1322 1379 1279

Current liability 3396 3349 3080

Inventory 660 713 686

Quick Assets 662 666 593

Current ratio

Current assets /

current liabilities 0.39 0.41 0.42

Quick Ratio

(Current Assets -

Inventory) /

Current Liabilities 0.19 0.20 0.19

Profitability ratio

Employed

Capital 7524 7317 7382

Net operating

profit 521 394 458

Return on

capital

employed

Net operating

profit/Employed

Capital 6.92% 5.38% 6.20%

Net Income 348 244 311

Shareholder's

Equity 4541 4325 4250

Return on

Equity

Net Income /

Shareholder's

Equity 8% 5.64% 7.32%

Cost of Sales 16907 17128 16629

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

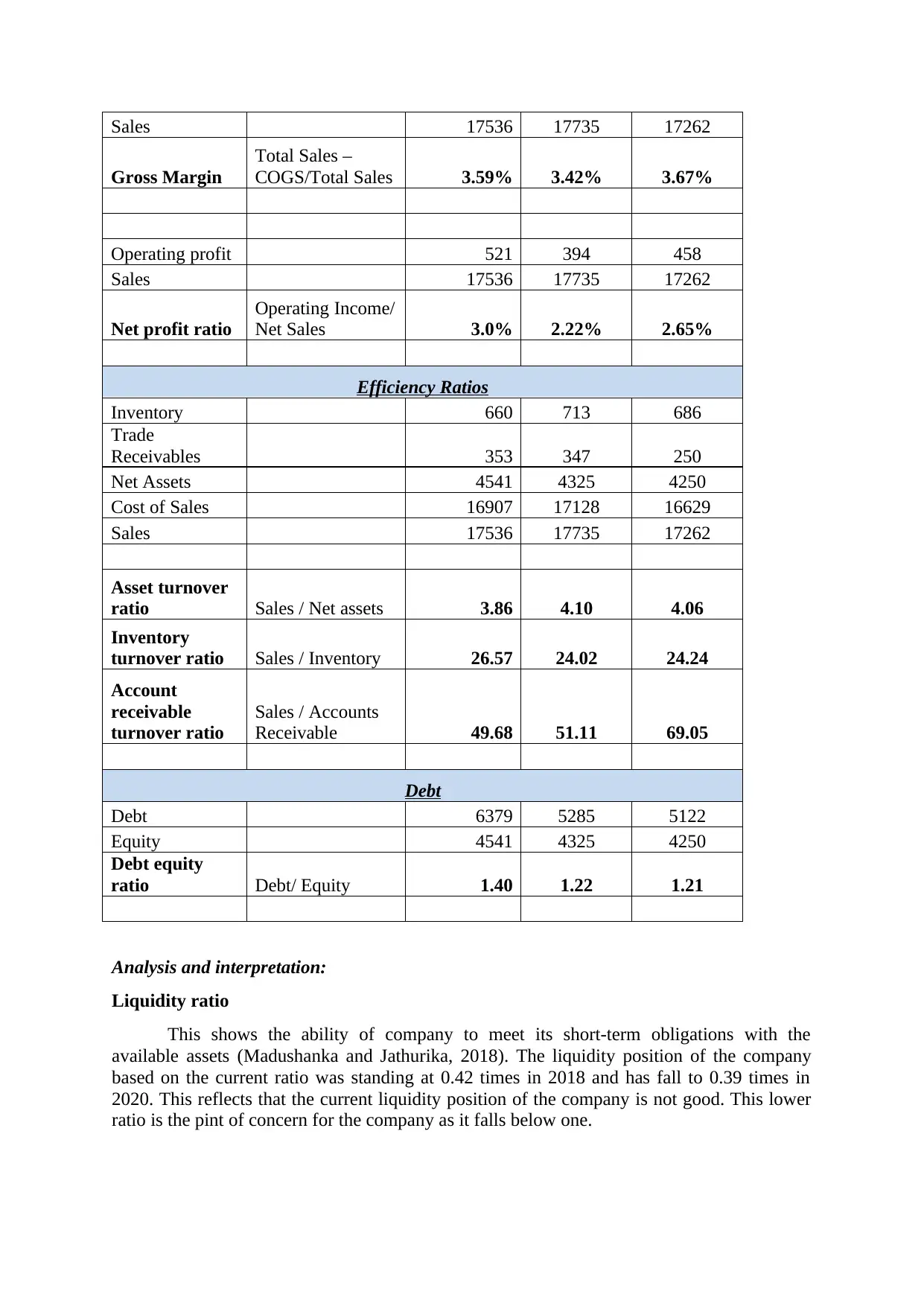

Sales 17536 17735 17262

Gross Margin

Total Sales –

COGS/Total Sales 3.59% 3.42% 3.67%

Operating profit 521 394 458

Sales 17536 17735 17262

Net profit ratio

Operating Income/

Net Sales 3.0% 2.22% 2.65%

Efficiency Ratios

Inventory 660 713 686

Trade

Receivables 353 347 250

Net Assets 4541 4325 4250

Cost of Sales 16907 17128 16629

Sales 17536 17735 17262

Asset turnover

ratio Sales / Net assets 3.86 4.10 4.06

Inventory

turnover ratio Sales / Inventory 26.57 24.02 24.24

Account

receivable

turnover ratio

Sales / Accounts

Receivable 49.68 51.11 69.05

Debt

Debt 6379 5285 5122

Equity 4541 4325 4250

Debt equity

ratio Debt/ Equity 1.40 1.22 1.21

Analysis and interpretation:

Liquidity ratio

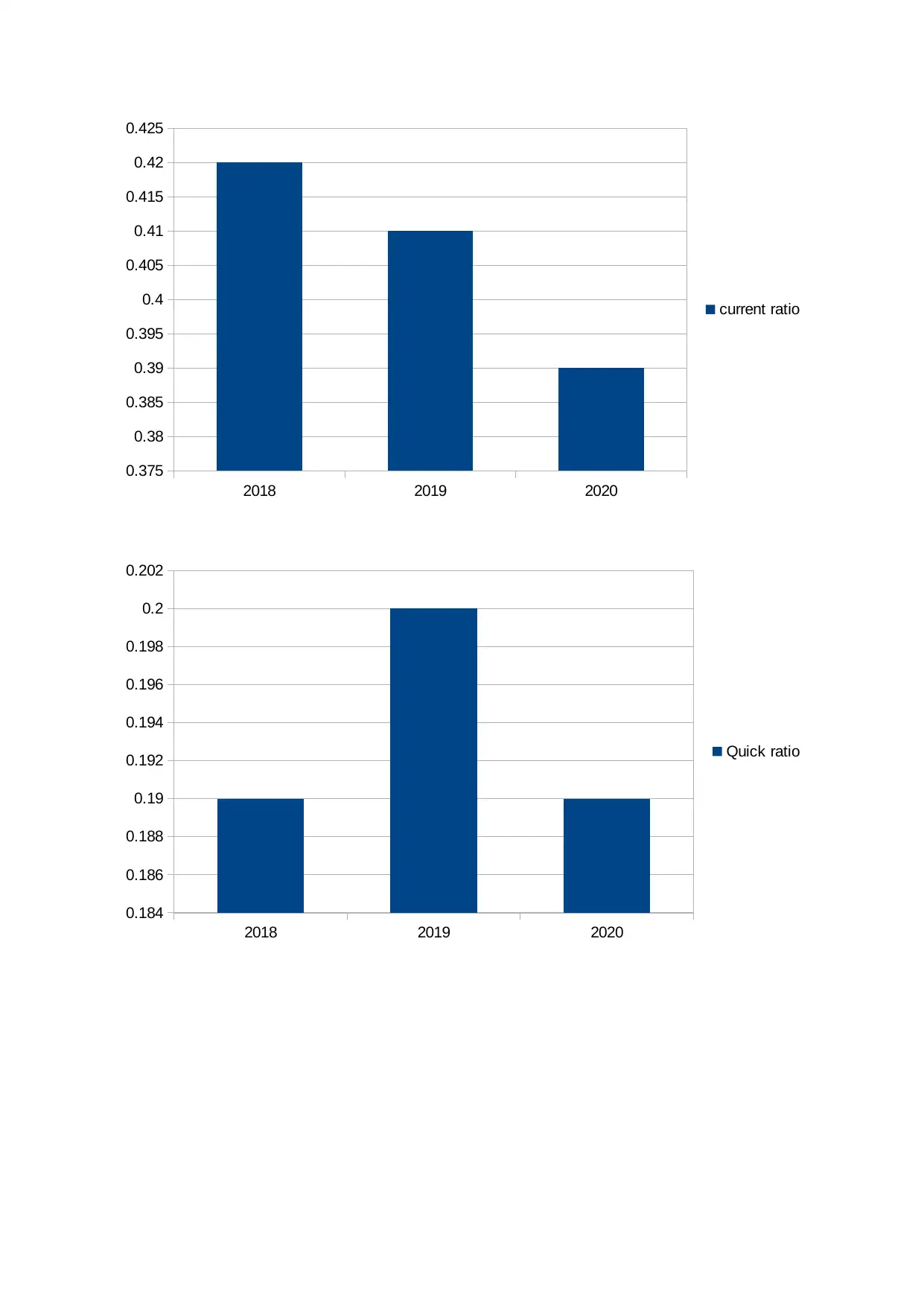

This shows the ability of company to meet its short-term obligations with the

available assets (Madushanka and Jathurika, 2018). The liquidity position of the company

based on the current ratio was standing at 0.42 times in 2018 and has fall to 0.39 times in

2020. This reflects that the current liquidity position of the company is not good. This lower

ratio is the pint of concern for the company as it falls below one.

Gross Margin

Total Sales –

COGS/Total Sales 3.59% 3.42% 3.67%

Operating profit 521 394 458

Sales 17536 17735 17262

Net profit ratio

Operating Income/

Net Sales 3.0% 2.22% 2.65%

Efficiency Ratios

Inventory 660 713 686

Trade

Receivables 353 347 250

Net Assets 4541 4325 4250

Cost of Sales 16907 17128 16629

Sales 17536 17735 17262

Asset turnover

ratio Sales / Net assets 3.86 4.10 4.06

Inventory

turnover ratio Sales / Inventory 26.57 24.02 24.24

Account

receivable

turnover ratio

Sales / Accounts

Receivable 49.68 51.11 69.05

Debt

Debt 6379 5285 5122

Equity 4541 4325 4250

Debt equity

ratio Debt/ Equity 1.40 1.22 1.21

Analysis and interpretation:

Liquidity ratio

This shows the ability of company to meet its short-term obligations with the

available assets (Madushanka and Jathurika, 2018). The liquidity position of the company

based on the current ratio was standing at 0.42 times in 2018 and has fall to 0.39 times in

2020. This reflects that the current liquidity position of the company is not good. This lower

ratio is the pint of concern for the company as it falls below one.

2018 2019 2020

0.375

0.38

0.385

0.39

0.395

0.4

0.405

0.41

0.415

0.42

0.425

current ratio

2018 2019 2020

0.184

0.186

0.188

0.19

0.192

0.194

0.196

0.198

0.2

0.202

Quick ratio

0.375

0.38

0.385

0.39

0.395

0.4

0.405

0.41

0.415

0.42

0.425

current ratio

2018 2019 2020

0.184

0.186

0.188

0.19

0.192

0.194

0.196

0.198

0.2

0.202

Quick ratio

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

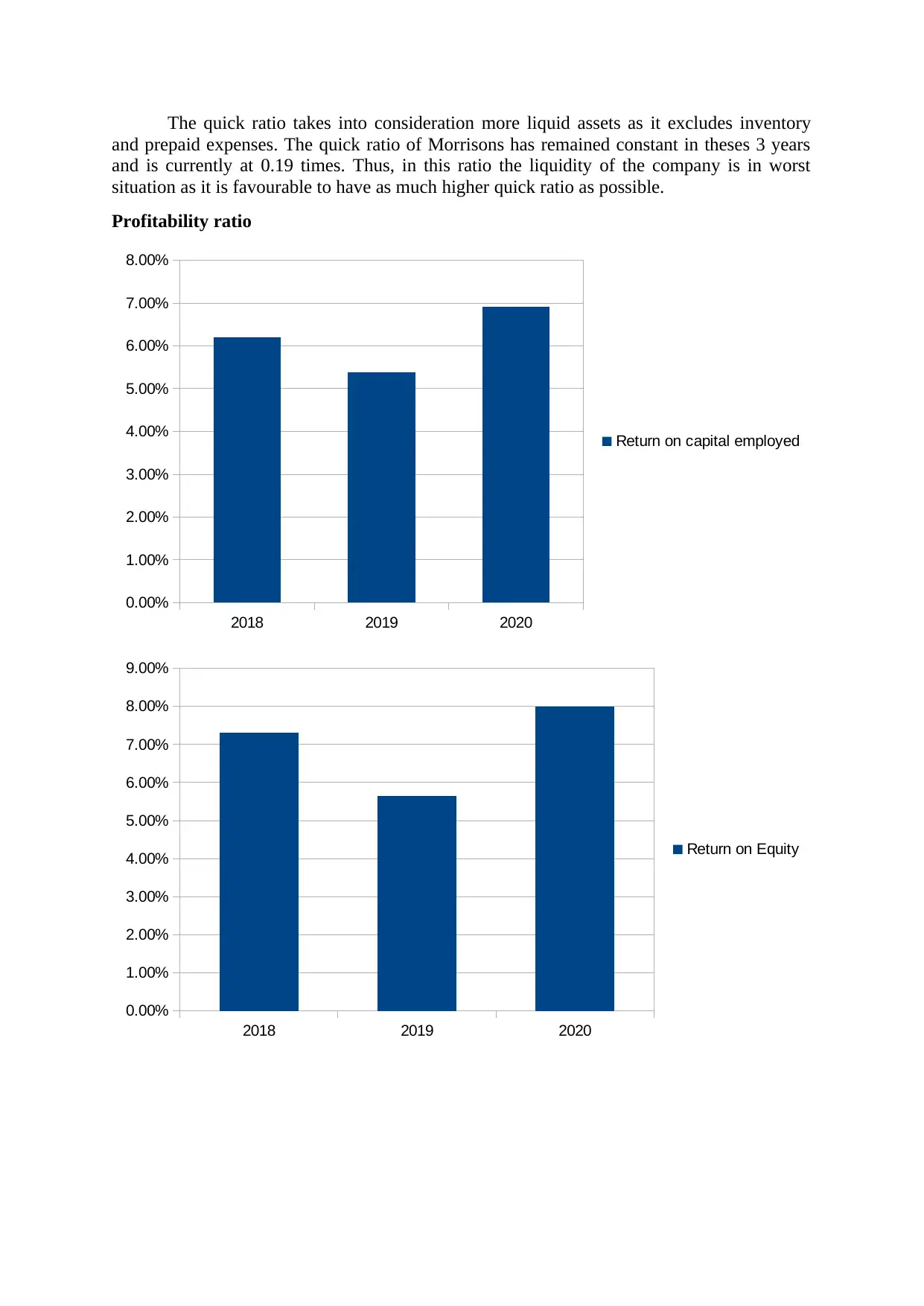

The quick ratio takes into consideration more liquid assets as it excludes inventory

and prepaid expenses. The quick ratio of Morrisons has remained constant in theses 3 years

and is currently at 0.19 times. Thus, in this ratio the liquidity of the company is in worst

situation as it is favourable to have as much higher quick ratio as possible.

Profitability ratio

2018 2019 2020

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

Return on capital employed

2018 2019 2020

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

Return on Equity

and prepaid expenses. The quick ratio of Morrisons has remained constant in theses 3 years

and is currently at 0.19 times. Thus, in this ratio the liquidity of the company is in worst

situation as it is favourable to have as much higher quick ratio as possible.

Profitability ratio

2018 2019 2020

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

Return on capital employed

2018 2019 2020

0.00%

1.00%

2.00%

3.00%

4.00%

5.00%

6.00%

7.00%

8.00%

9.00%

Return on Equity

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The above graphs states about the company’s earning in respect to the return on

capital employed and the equity. It can be seen that there is so much fluctuation in the return.

In case of ROCE, in 2018 it was 6.20% which then dropped to 5.38% in the year 2019 and

then again increased to 6.92%. Also, in ROC, it was 7.32%, which then reduced to 5.64%

then rose to 8%. Even though there are fluctuation, it indicates that the company is making

efforts for effectively managing its resources.

2018 2019 2020

3.25%

3.30%

3.35%

3.40%

3.45%

3.50%

3.55%

3.60%

3.65%

3.70%

Gross margin

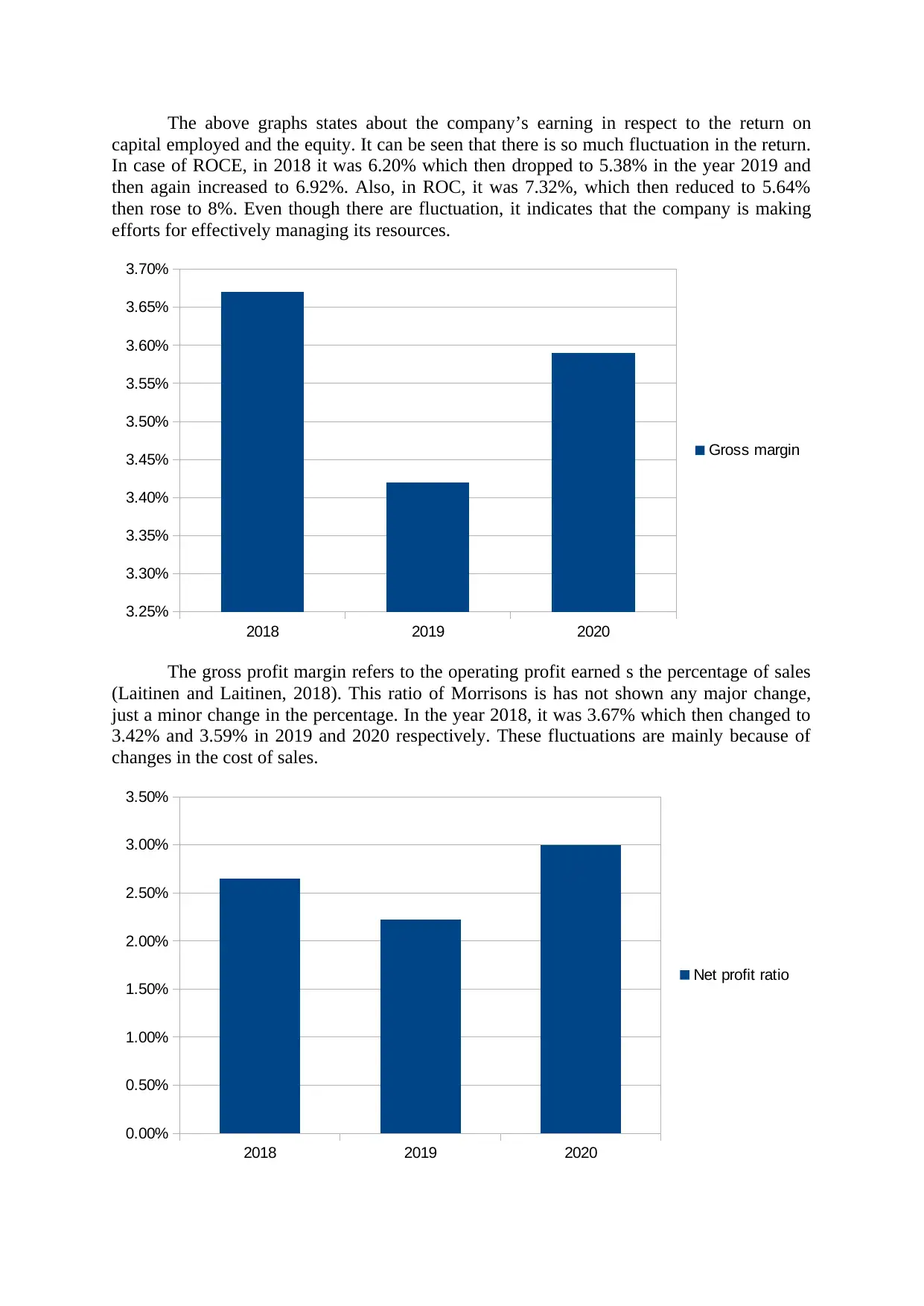

The gross profit margin refers to the operating profit earned s the percentage of sales

(Laitinen and Laitinen, 2018). This ratio of Morrisons is has not shown any major change,

just a minor change in the percentage. In the year 2018, it was 3.67% which then changed to

3.42% and 3.59% in 2019 and 2020 respectively. These fluctuations are mainly because of

changes in the cost of sales.

2018 2019 2020

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Net profit ratio

capital employed and the equity. It can be seen that there is so much fluctuation in the return.

In case of ROCE, in 2018 it was 6.20% which then dropped to 5.38% in the year 2019 and

then again increased to 6.92%. Also, in ROC, it was 7.32%, which then reduced to 5.64%

then rose to 8%. Even though there are fluctuation, it indicates that the company is making

efforts for effectively managing its resources.

2018 2019 2020

3.25%

3.30%

3.35%

3.40%

3.45%

3.50%

3.55%

3.60%

3.65%

3.70%

Gross margin

The gross profit margin refers to the operating profit earned s the percentage of sales

(Laitinen and Laitinen, 2018). This ratio of Morrisons is has not shown any major change,

just a minor change in the percentage. In the year 2018, it was 3.67% which then changed to

3.42% and 3.59% in 2019 and 2020 respectively. These fluctuations are mainly because of

changes in the cost of sales.

2018 2019 2020

0.00%

0.50%

1.00%

1.50%

2.00%

2.50%

3.00%

3.50%

Net profit ratio

This ratio shows the relationship of net profit with respect to net sales. The net profit

of Morrison has shown a decline in percentage from 2018 to 2019 from 2.65% to 2.22% and

then increased to 3%. This shows a steady level of profits in the company.

Efficiency ratio

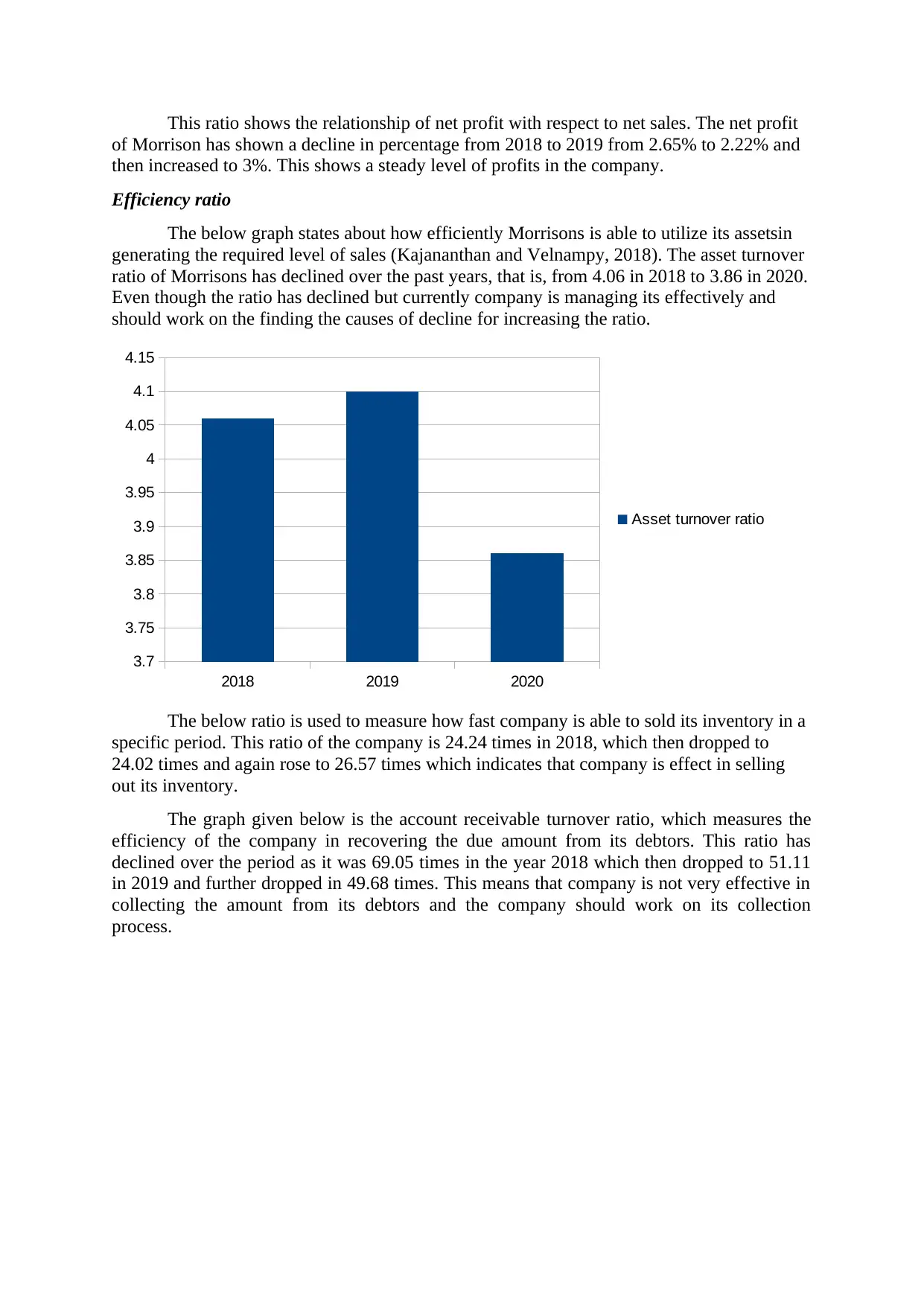

The below graph states about how efficiently Morrisons is able to utilize its assetsin

generating the required level of sales (Kajananthan and Velnampy, 2018). The asset turnover

ratio of Morrisons has declined over the past years, that is, from 4.06 in 2018 to 3.86 in 2020.

Even though the ratio has declined but currently company is managing its effectively and

should work on the finding the causes of decline for increasing the ratio.

2018 2019 2020

3.7

3.75

3.8

3.85

3.9

3.95

4

4.05

4.1

4.15

Asset turnover ratio

The below ratio is used to measure how fast company is able to sold its inventory in a

specific period. This ratio of the company is 24.24 times in 2018, which then dropped to

24.02 times and again rose to 26.57 times which indicates that company is effect in selling

out its inventory.

The graph given below is the account receivable turnover ratio, which measures the

efficiency of the company in recovering the due amount from its debtors. This ratio has

declined over the period as it was 69.05 times in the year 2018 which then dropped to 51.11

in 2019 and further dropped in 49.68 times. This means that company is not very effective in

collecting the amount from its debtors and the company should work on its collection

process.

of Morrison has shown a decline in percentage from 2018 to 2019 from 2.65% to 2.22% and

then increased to 3%. This shows a steady level of profits in the company.

Efficiency ratio

The below graph states about how efficiently Morrisons is able to utilize its assetsin

generating the required level of sales (Kajananthan and Velnampy, 2018). The asset turnover

ratio of Morrisons has declined over the past years, that is, from 4.06 in 2018 to 3.86 in 2020.

Even though the ratio has declined but currently company is managing its effectively and

should work on the finding the causes of decline for increasing the ratio.

2018 2019 2020

3.7

3.75

3.8

3.85

3.9

3.95

4

4.05

4.1

4.15

Asset turnover ratio

The below ratio is used to measure how fast company is able to sold its inventory in a

specific period. This ratio of the company is 24.24 times in 2018, which then dropped to

24.02 times and again rose to 26.57 times which indicates that company is effect in selling

out its inventory.

The graph given below is the account receivable turnover ratio, which measures the

efficiency of the company in recovering the due amount from its debtors. This ratio has

declined over the period as it was 69.05 times in the year 2018 which then dropped to 51.11

in 2019 and further dropped in 49.68 times. This means that company is not very effective in

collecting the amount from its debtors and the company should work on its collection

process.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 21

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.