University of Sunderland Financial Management Report

VerifiedAdded on 2022/12/23

|14

|3924

|90

Report

AI Summary

This report provides a comprehensive analysis of financial management principles, focusing on investment appraisal techniques and market efficiency. It begins with an introduction to financial management and its importance in business, defining key concepts and objectives. The main body of the report is divided into two parts. Part A delves into the application of various investment appraisal methods, including the payback period, net present value (NPV), accounting rate of return (ARR), and internal rate of return (IRR), with detailed calculations for Project X and Project Y. The report evaluates the benefits and limitations of each method, offering insights into their practical applications and implications for decision-making. Part B assesses the strengths of market efficiency, supported by relevant academic evidence. The report concludes by summarizing the key findings and emphasizing the significance of financial management in achieving organizational goals. The report includes tables with calculations for payback period, NPV, ARR, and IRR for two projects, and references relevant academic sources to support its analysis. This report is a detailed analysis of financial management concepts, investment appraisal, and market efficiency, designed to provide a comprehensive understanding of the topic.

Financial management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part A...........................................................................................................................................3

Part B ..........................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Part A...........................................................................................................................................3

Part B ..........................................................................................................................................8

CONCLUSION..............................................................................................................................10

REFERENCES................................................................................................................................1

INTRODUCTION

Financial management is most important aspect in the business that include the excellent

knowledge in financial terms and also refers to planning, organising, directing and controlling of

financial undertakings (Akbasheva and Yaitskaya, 2021). It is refers as essential form of

determining and allocation of the objectives of the company. In this report, it is being discussed

about the different forms of investment appraisal such as Payback period, Accounting rate of

return, Net present value and IRR and discussed their limitation and benefits in the organisation.

Apart from that it is being evaluated the three differing strengths of market efficiency with the

support of relevant academic evidence.

MAIN BODY

Part A

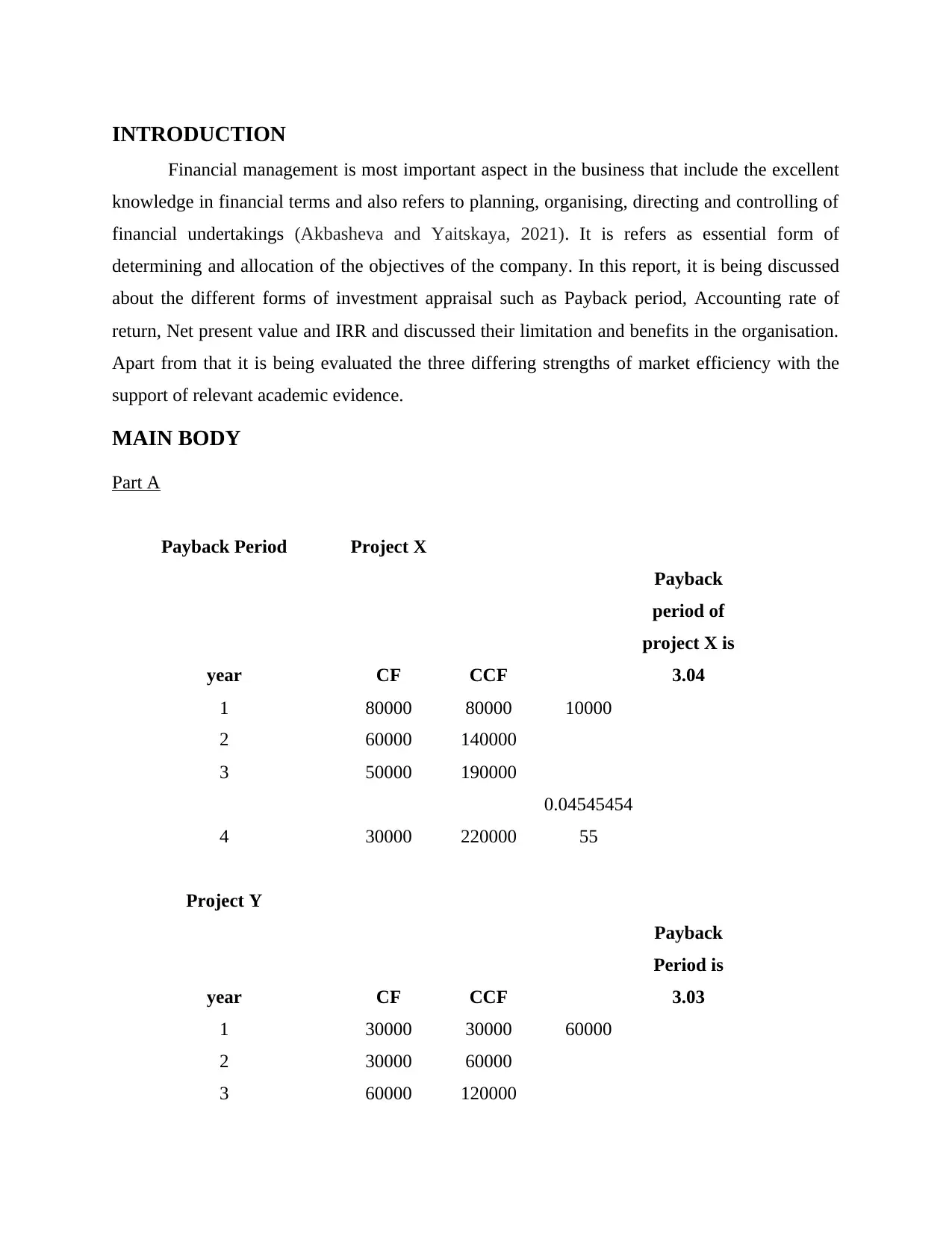

Payback Period Project X

year CF CCF

Payback

period of

project X is

3.04

1 80000 80000 10000

2 60000 140000

3 50000 190000

4 30000 220000

0.04545454

55

Project Y

year CF CCF

Payback

Period is

3.03

1 30000 30000 60000

2 30000 60000

3 60000 120000

Financial management is most important aspect in the business that include the excellent

knowledge in financial terms and also refers to planning, organising, directing and controlling of

financial undertakings (Akbasheva and Yaitskaya, 2021). It is refers as essential form of

determining and allocation of the objectives of the company. In this report, it is being discussed

about the different forms of investment appraisal such as Payback period, Accounting rate of

return, Net present value and IRR and discussed their limitation and benefits in the organisation.

Apart from that it is being evaluated the three differing strengths of market efficiency with the

support of relevant academic evidence.

MAIN BODY

Part A

Payback Period Project X

year CF CCF

Payback

period of

project X is

3.04

1 80000 80000 10000

2 60000 140000

3 50000 190000

4 30000 220000

0.04545454

55

Project Y

year CF CCF

Payback

Period is

3.03

1 30000 30000 60000

2 30000 60000

3 60000 120000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

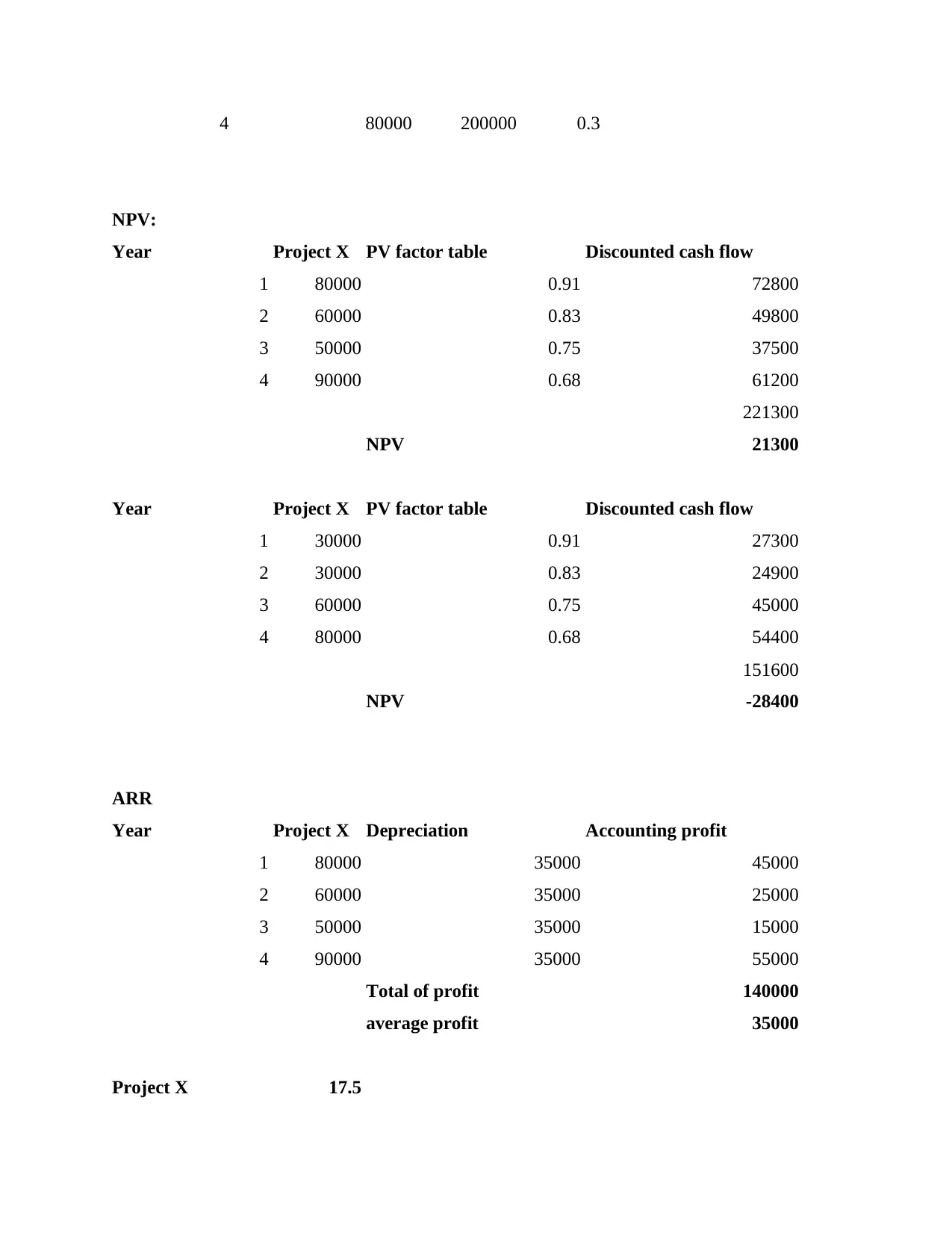

4 80000 200000 0.3

NPV:

Year Project X PV factor table Discounted cash flow

1 80000 0.91 72800

2 60000 0.83 49800

3 50000 0.75 37500

4 90000 0.68 61200

221300

NPV 21300

Year Project X PV factor table Discounted cash flow

1 30000 0.91 27300

2 30000 0.83 24900

3 60000 0.75 45000

4 80000 0.68 54400

151600

NPV -28400

ARR

Year Project X Depreciation Accounting profit

1 80000 35000 45000

2 60000 35000 25000

3 50000 35000 15000

4 90000 35000 55000

Total of profit 140000

average profit 35000

Project X 17.5

NPV:

Year Project X PV factor table Discounted cash flow

1 80000 0.91 72800

2 60000 0.83 49800

3 50000 0.75 37500

4 90000 0.68 61200

221300

NPV 21300

Year Project X PV factor table Discounted cash flow

1 30000 0.91 27300

2 30000 0.83 24900

3 60000 0.75 45000

4 80000 0.68 54400

151600

NPV -28400

ARR

Year Project X Depreciation Accounting profit

1 80000 35000 45000

2 60000 35000 25000

3 50000 35000 15000

4 90000 35000 55000

Total of profit 140000

average profit 35000

Project X 17.5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

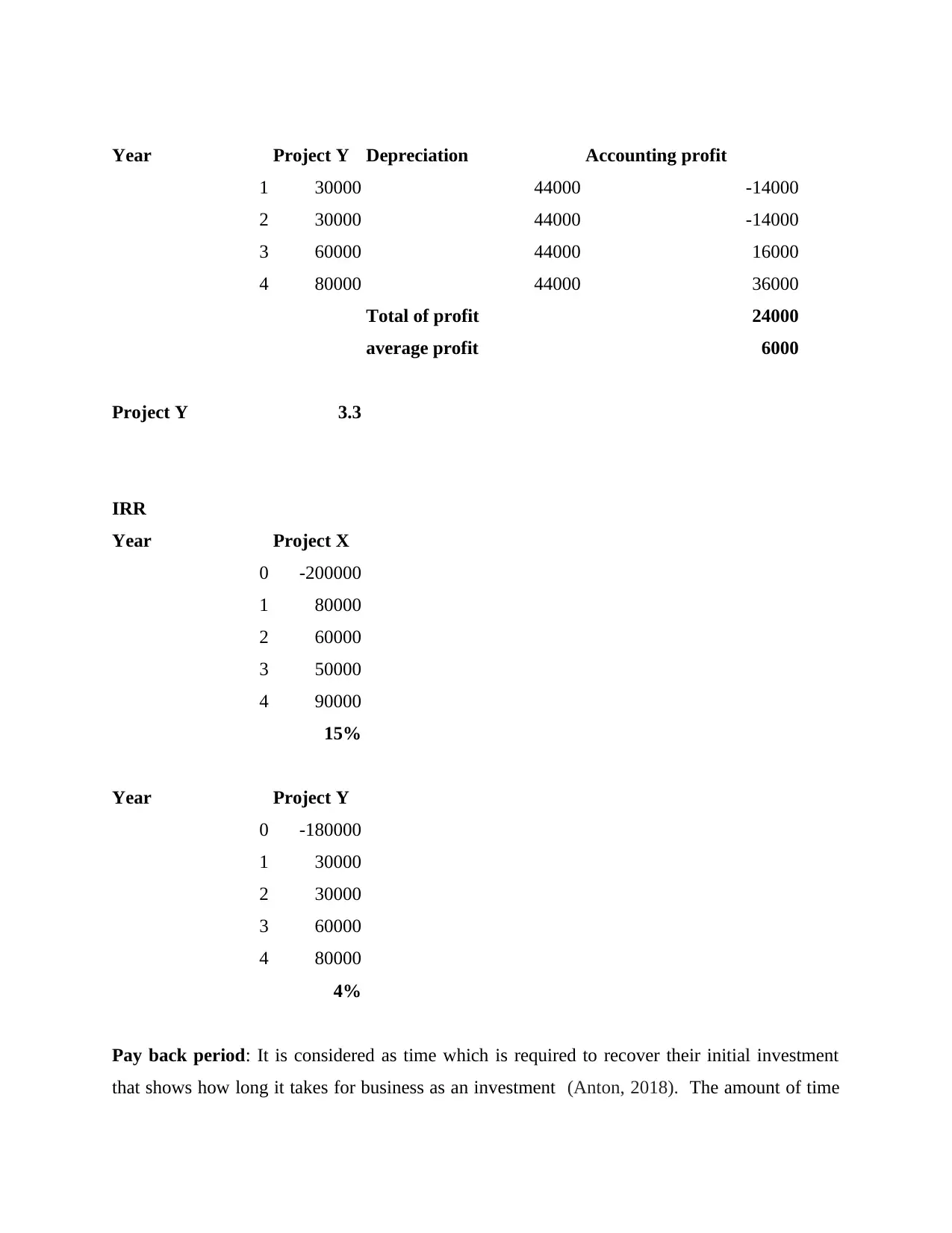

Year Project Y Depreciation Accounting profit

1 30000 44000 -14000

2 30000 44000 -14000

3 60000 44000 16000

4 80000 44000 36000

Total of profit 24000

average profit 6000

Project Y 3.3

IRR

Year Project X

0 -200000

1 80000

2 60000

3 50000

4 90000

15%

Year Project Y

0 -180000

1 30000

2 30000

3 60000

4 80000

4%

Pay back period: It is considered as time which is required to recover their initial investment

that shows how long it takes for business as an investment (Anton, 2018). The amount of time

1 30000 44000 -14000

2 30000 44000 -14000

3 60000 44000 16000

4 80000 44000 36000

Total of profit 24000

average profit 6000

Project Y 3.3

IRR

Year Project X

0 -200000

1 80000

2 60000

3 50000

4 90000

15%

Year Project Y

0 -180000

1 30000

2 30000

3 60000

4 80000

4%

Pay back period: It is considered as time which is required to recover their initial investment

that shows how long it takes for business as an investment (Anton, 2018). The amount of time

that requires initial cash inflows which are generated by project to beginning from initial cash

outflow. It is simply a way that evaluate which risk is related with proposed project and is

divided amount of investment by annual cash flow. With context to Blue Ltd, it is an effective

measures for risk of investment and it is mainly used in firm for liquidity criteria to choose a

various project. It is an appropriate for firm that they should investment in small projects and

spend much more time. This helps the manager to take the help from the project that have to

choose between project and helps in taking the effective decision which help in minimising the

cost and maximisation of profit to increase the efficiency. This payback period helps in revealing

the payback period of the investment and takes into the consideration of cash flow of incomes

from the particular project to cover the initial investment. In this case the project X payback is

more than the project Y and that indicate that it was more profitable and leads to many advantage

and profit to deal with the future circumstances.

Benefits of pay back period:

Easy to understand: This method is very simple and easily to understand and needs to

calculate pay back period in project initial cost and annual cash flows. This ratio is helpful in

determined the profitability of an organisation through analysing the effectiveness in the selected

organisation. This gives better method to check the efficiency so that company able to choose the

most appropriate form of project.

Focus on risk: This type of analysis mainly focus on how firm can managed their risk

and how they can quickly and easily returned on investment which is crucial part for measure

their risk in an enterprise. Pay back period should be used as comparison of relative risk of

projects with varying of various payback periods.

Quick solution- It helps in calculate and it just fewer inputs, managers are quickly able

to calculate the payback project and easy to get the decision with better manner and leads to

many advantages and provides many other benefits to the organisation. This is useful for those

who has the limited resources and require to find the effectiveness of the company and help in

building the efficiency.

Useful in uncertainty- They were useful for the company who has witness the

uncertainty and face rapid changes in the technology and will leads to many difficulties. So, from

this it helps in making the relevant use of the project that reduces the chances of loss through the

outflow. It is simply a way that evaluate which risk is related with proposed project and is

divided amount of investment by annual cash flow. With context to Blue Ltd, it is an effective

measures for risk of investment and it is mainly used in firm for liquidity criteria to choose a

various project. It is an appropriate for firm that they should investment in small projects and

spend much more time. This helps the manager to take the help from the project that have to

choose between project and helps in taking the effective decision which help in minimising the

cost and maximisation of profit to increase the efficiency. This payback period helps in revealing

the payback period of the investment and takes into the consideration of cash flow of incomes

from the particular project to cover the initial investment. In this case the project X payback is

more than the project Y and that indicate that it was more profitable and leads to many advantage

and profit to deal with the future circumstances.

Benefits of pay back period:

Easy to understand: This method is very simple and easily to understand and needs to

calculate pay back period in project initial cost and annual cash flows. This ratio is helpful in

determined the profitability of an organisation through analysing the effectiveness in the selected

organisation. This gives better method to check the efficiency so that company able to choose the

most appropriate form of project.

Focus on risk: This type of analysis mainly focus on how firm can managed their risk

and how they can quickly and easily returned on investment which is crucial part for measure

their risk in an enterprise. Pay back period should be used as comparison of relative risk of

projects with varying of various payback periods.

Quick solution- It helps in calculate and it just fewer inputs, managers are quickly able

to calculate the payback project and easy to get the decision with better manner and leads to

many advantages and provides many other benefits to the organisation. This is useful for those

who has the limited resources and require to find the effectiveness of the company and help in

building the efficiency.

Useful in uncertainty- They were useful for the company who has witness the

uncertainty and face rapid changes in the technology and will leads to many difficulties. So, from

this it helps in making the relevant use of the project that reduces the chances of loss through the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

obsolescence. They help in increasing the efficiency that will help in selecting the project which

is more preferable.

Disadvantages of pay back period:

Time value of money: They ignore time value if money because cash flow are received

during this time where they get a higher part of project than cash flows received. The money

received is worth more than one upcoming later if its potential to earn an additional return if they

are invested (Archer-Brown and Kietzmann, 2018).

Ignored profitability: This type demerits focused on liquidity and recovery of speed of

investment but they are completely ignore all profitability. If a project is short pay back period

that doesn't mean it is profitable and if cash flows are end up then it is forceful decreased.

Not all cash flows covered- Payback period method consider cash flows only until time

the initial investment is recovered. It fails to consider the cash flows that come in subsequent

years. This create the inefficiency and limited view of cash flows might force you to overlook

the project that could generate the lucrative cash flows in latest years.

Not realistic- The payback period is so simple that it does not involve the normal

business scenarios. Capital investment are not just one-time investment and rather such project

need the further investment and also have irregular cash inflows.

Accounting rate of return: This rate of return is expected which is to be earned

investment in respect of initial investment is calculated by dividing the average annual profit

where these profits are calculated by sum of book value. It is that percentage rate of return which

is expected from initial investment or compared initial cost of investment. In case of Blue Ltd, it

is important for organisation when accounting rate of return are compare doubled projects to be

ascertain that expected rate of return which helps to decide an investments or any acquisition of

firm (Betaneli, Nikitina and Zhelev, 2020). This uses to expect net operating income to be

generated by the investment proposal rather than focusing on cash flows to evaluate the

investment proposal. It refers to that if asset expected accounting rate of return is greater than or

equal to the management’s desired rate of return.

Benefits of accounting rate of return:

They should focused on most profitable project: It will recommend that they invest in

high project where profits are also high and best use of investment fund if they are invested in

any fund or any activity of business so which will help to maximise rate of return. That's why

is more preferable.

Disadvantages of pay back period:

Time value of money: They ignore time value if money because cash flow are received

during this time where they get a higher part of project than cash flows received. The money

received is worth more than one upcoming later if its potential to earn an additional return if they

are invested (Archer-Brown and Kietzmann, 2018).

Ignored profitability: This type demerits focused on liquidity and recovery of speed of

investment but they are completely ignore all profitability. If a project is short pay back period

that doesn't mean it is profitable and if cash flows are end up then it is forceful decreased.

Not all cash flows covered- Payback period method consider cash flows only until time

the initial investment is recovered. It fails to consider the cash flows that come in subsequent

years. This create the inefficiency and limited view of cash flows might force you to overlook

the project that could generate the lucrative cash flows in latest years.

Not realistic- The payback period is so simple that it does not involve the normal

business scenarios. Capital investment are not just one-time investment and rather such project

need the further investment and also have irregular cash inflows.

Accounting rate of return: This rate of return is expected which is to be earned

investment in respect of initial investment is calculated by dividing the average annual profit

where these profits are calculated by sum of book value. It is that percentage rate of return which

is expected from initial investment or compared initial cost of investment. In case of Blue Ltd, it

is important for organisation when accounting rate of return are compare doubled projects to be

ascertain that expected rate of return which helps to decide an investments or any acquisition of

firm (Betaneli, Nikitina and Zhelev, 2020). This uses to expect net operating income to be

generated by the investment proposal rather than focusing on cash flows to evaluate the

investment proposal. It refers to that if asset expected accounting rate of return is greater than or

equal to the management’s desired rate of return.

Benefits of accounting rate of return:

They should focused on most profitable project: It will recommend that they invest in

high project where profits are also high and best use of investment fund if they are invested in

any fund or any activity of business so which will help to maximise rate of return. That's why

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

they should focused on profitable project that will impact on profitability an productivity in an

organisation. It can gives clear picture of project.

Simple method: This method is very easy to understand and simple because it does not

require any complicated situation. It considers total profits and savings over time period for

various economic life of project. ARR is a technique for comparing actual capital projects that

would be easily understood by everyone.

Facilitates decision rules- It is easy to take the decision regarding the suitable capital

project. As, project with higher ARR is selected and project with lower ARR is ignored. This

helps the manager to take fast decision as compared to others as it is easy to understand and also

to select the project.

Limitations of accounting rate of return:

Ignores time factors: It is a method which does not require time value of money and

long time project will be highly selected on basis of accounting rate of return. The main primary

weakness that average return method selection of alternative use of funds is that time of funds

which is being ignored (Klimek and Jędrych, 2021).

Ignore whole project team: It is mainly focused on each and every year profits instead

of entire return of project. In fact, most of the project have low returns because of it has long

useful life. It ignores that period of profits which have to be earned in 20% rate of return on 10

years and it is not no longer term of project and risk is also involved.

Inconsistence- Accounting rate of return does not remain constant over useful life for

many projects and thus look desirable in one period but undesirable in another period. This leads

to confusion among the manager about profitability and accuracy of the project and leads to

many problems.

Net present value: It is a difference between net present value of cash inflow and net

present value of cash outflow over a specific period of time. The value of net present is required

that rate of return where project are compared to initial investment of other project. In case of

Blue Ltd, it is useful for managers that need to compare of initial spending of cash against the net

present value of return. It can also consider time value of money for upcoming cash flows. It is

helpful to determine capital budgeting for analyse main profitability of an investment projected.

This helps in let you know whether the value of all cash flows that project generates will exceed

organisation. It can gives clear picture of project.

Simple method: This method is very easy to understand and simple because it does not

require any complicated situation. It considers total profits and savings over time period for

various economic life of project. ARR is a technique for comparing actual capital projects that

would be easily understood by everyone.

Facilitates decision rules- It is easy to take the decision regarding the suitable capital

project. As, project with higher ARR is selected and project with lower ARR is ignored. This

helps the manager to take fast decision as compared to others as it is easy to understand and also

to select the project.

Limitations of accounting rate of return:

Ignores time factors: It is a method which does not require time value of money and

long time project will be highly selected on basis of accounting rate of return. The main primary

weakness that average return method selection of alternative use of funds is that time of funds

which is being ignored (Klimek and Jędrych, 2021).

Ignore whole project team: It is mainly focused on each and every year profits instead

of entire return of project. In fact, most of the project have low returns because of it has long

useful life. It ignores that period of profits which have to be earned in 20% rate of return on 10

years and it is not no longer term of project and risk is also involved.

Inconsistence- Accounting rate of return does not remain constant over useful life for

many projects and thus look desirable in one period but undesirable in another period. This leads

to confusion among the manager about profitability and accuracy of the project and leads to

many problems.

Net present value: It is a difference between net present value of cash inflow and net

present value of cash outflow over a specific period of time. The value of net present is required

that rate of return where project are compared to initial investment of other project. In case of

Blue Ltd, it is useful for managers that need to compare of initial spending of cash against the net

present value of return. It can also consider time value of money for upcoming cash flows. It is

helpful to determine capital budgeting for analyse main profitability of an investment projected.

This helps in let you know whether the value of all cash flows that project generates will exceed

the cost of starting the particular project and tells whether that project is positive or negative

outlook.

Benefits of Net present value:

Time value of money: Net present value consider time value of money because it takes

into consideration for the effect on inflation on future profitability of project. The calculation of

net present value considers discounted cash flow of investment that understand how present

value can determine their capital budgeting.

Decision making: This method enables that decision making procedures of firms and

also it helps to evaluate the same size of project but they can helps to identifying whether it is a

particular investment is loss or profit making. It will be helpful for taking decision in an

business enterprise (Koval, Prymush and Popova, 2017).

Good measure of profitability- This help in choosing the project which is has good

profitability and will leads to many advantages to the managers and shareholder also to facilitates

the efficiency and effectiveness of the project that has been chosen.

Limitations of net present value:

Difficulty in determine required rate of return: They can determine required rate of

return where cash flows are to be discounted factor and firm should not use as this rate but it

might be use of any project rate which is a discount rate of return and estimation which may

lead to higher or lower net present value.

It cannot used to compare different sizes of projects: The main disadvantages is that

they do not compare this type of projects with different sizes. It can be calculated is an absolute

figure not an percentage pattern. Net present value consist of larger projects as compare of higher

than a smaller size of project.

Might not boost EPS and ROE- As, this is its disadvantage of using sometimes that

short-term projects having higher NPV will not going to boost the EPS and Return on equity that

might upset the shareholder due to lack of return. Short-term projects with higher NPV might not

work in the favour of shareholder and leads to ignorance of the investors.

Internal rate of return: It is used as financial analysis to determine and estimate their

profitability of certain investments. This rate of return consist of that present value of all cash

flows are equal to zero in discounted cash flow analysis. With context to Blue Ltd, this firm used

internal rate of return whether they can determine investment or expense. They will show that

outlook.

Benefits of Net present value:

Time value of money: Net present value consider time value of money because it takes

into consideration for the effect on inflation on future profitability of project. The calculation of

net present value considers discounted cash flow of investment that understand how present

value can determine their capital budgeting.

Decision making: This method enables that decision making procedures of firms and

also it helps to evaluate the same size of project but they can helps to identifying whether it is a

particular investment is loss or profit making. It will be helpful for taking decision in an

business enterprise (Koval, Prymush and Popova, 2017).

Good measure of profitability- This help in choosing the project which is has good

profitability and will leads to many advantages to the managers and shareholder also to facilitates

the efficiency and effectiveness of the project that has been chosen.

Limitations of net present value:

Difficulty in determine required rate of return: They can determine required rate of

return where cash flows are to be discounted factor and firm should not use as this rate but it

might be use of any project rate which is a discount rate of return and estimation which may

lead to higher or lower net present value.

It cannot used to compare different sizes of projects: The main disadvantages is that

they do not compare this type of projects with different sizes. It can be calculated is an absolute

figure not an percentage pattern. Net present value consist of larger projects as compare of higher

than a smaller size of project.

Might not boost EPS and ROE- As, this is its disadvantage of using sometimes that

short-term projects having higher NPV will not going to boost the EPS and Return on equity that

might upset the shareholder due to lack of return. Short-term projects with higher NPV might not

work in the favour of shareholder and leads to ignorance of the investors.

Internal rate of return: It is used as financial analysis to determine and estimate their

profitability of certain investments. This rate of return consist of that present value of all cash

flows are equal to zero in discounted cash flow analysis. With context to Blue Ltd, this firm used

internal rate of return whether they can determine investment or expense. They will show that

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

firm made money or lost money in project and it is easy to measure their profitability and

compare one profits to another (Li, 2021) (Li, 2019). This technique helps in conducting the

proper analysis and interpretation of most of the project and proof as the well-known method of

evaluation and selection of investment projects.

Benefits of internal rate of return:

Required rate of return is not required: In this internal rate of return, there is no

requirement to find out hurdle of IRR or required rate of return. It is not dependent of hurdle rate

so it is risk that wrong determination of hurdle rate is decreased.

Time value of money: This benefit consist of most important things is internal rate of

return are considered time value of money because when they evaluating their project. This is

huge failure in ARR and payback period and one can measure to calculate their interest in which

present value is equal to capital investment so which is required.

Simplicity- The main advantage is that it is so simple to interpret after the calculation. If

IRR exceeds the cost of capital, then accept the project but not otherwise. This becomes easy for

the managers to visualize and helps in taking the in informed decision. It facilitates in taking the

project which is more preferable and profitable.

Limitations of internal rate of return:

Ignores size of project: Major demerit of internal rate of return is does not account for

those projects when comparing other projects. It is simply compared that amount of capital are

generate with cash flows and when consist of two projects are significantly different amount of

capital (Ptak-Chmielewska, 2019).

Part B

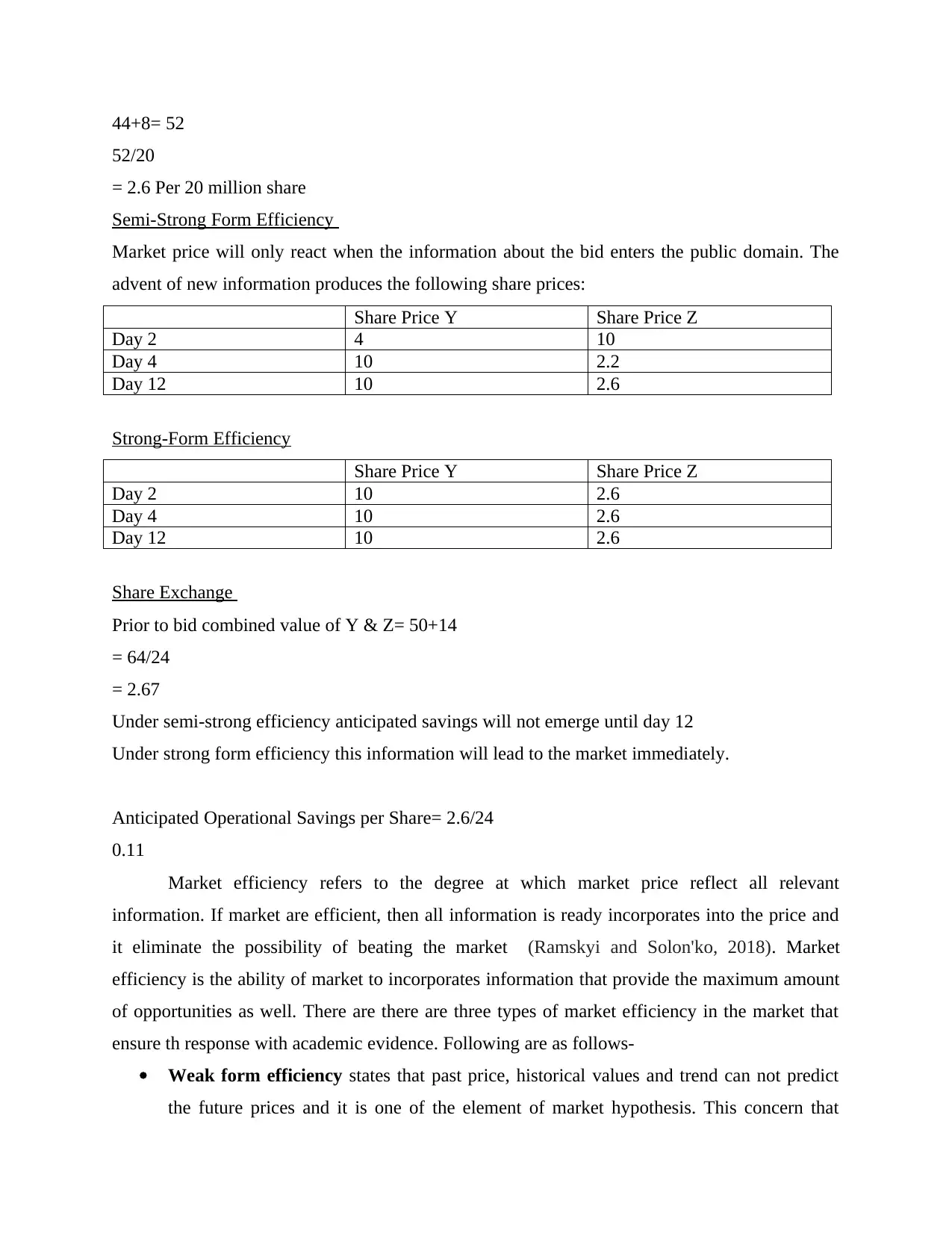

On Day 1 the total value of each firm is:

Y: (4*3.50) = 14

Z: (10*5) = 50

Company Z is making an offer of £20 million for Company Y which is apparently worth only

£14 million.

This will reduce the market value of B by £6million, therefore market value per share becomes:

44 Million/20

= 2.2 per share

Anticipated Operating Savings would raise Z’s value to:

compare one profits to another (Li, 2021) (Li, 2019). This technique helps in conducting the

proper analysis and interpretation of most of the project and proof as the well-known method of

evaluation and selection of investment projects.

Benefits of internal rate of return:

Required rate of return is not required: In this internal rate of return, there is no

requirement to find out hurdle of IRR or required rate of return. It is not dependent of hurdle rate

so it is risk that wrong determination of hurdle rate is decreased.

Time value of money: This benefit consist of most important things is internal rate of

return are considered time value of money because when they evaluating their project. This is

huge failure in ARR and payback period and one can measure to calculate their interest in which

present value is equal to capital investment so which is required.

Simplicity- The main advantage is that it is so simple to interpret after the calculation. If

IRR exceeds the cost of capital, then accept the project but not otherwise. This becomes easy for

the managers to visualize and helps in taking the in informed decision. It facilitates in taking the

project which is more preferable and profitable.

Limitations of internal rate of return:

Ignores size of project: Major demerit of internal rate of return is does not account for

those projects when comparing other projects. It is simply compared that amount of capital are

generate with cash flows and when consist of two projects are significantly different amount of

capital (Ptak-Chmielewska, 2019).

Part B

On Day 1 the total value of each firm is:

Y: (4*3.50) = 14

Z: (10*5) = 50

Company Z is making an offer of £20 million for Company Y which is apparently worth only

£14 million.

This will reduce the market value of B by £6million, therefore market value per share becomes:

44 Million/20

= 2.2 per share

Anticipated Operating Savings would raise Z’s value to:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

44+8= 52

52/20

= 2.6 Per 20 million share

Semi-Strong Form Efficiency

Market price will only react when the information about the bid enters the public domain. The

advent of new information produces the following share prices:

Share Price Y Share Price Z

Day 2 4 10

Day 4 10 2.2

Day 12 10 2.6

Strong-Form Efficiency

Share Price Y Share Price Z

Day 2 10 2.6

Day 4 10 2.6

Day 12 10 2.6

Share Exchange

Prior to bid combined value of Y & Z= 50+14

= 64/24

= 2.67

Under semi-strong efficiency anticipated savings will not emerge until day 12

Under strong form efficiency this information will lead to the market immediately.

Anticipated Operational Savings per Share= 2.6/24

0.11

Market efficiency refers to the degree at which market price reflect all relevant

information. If market are efficient, then all information is ready incorporates into the price and

it eliminate the possibility of beating the market (Ramskyi and Solon'ko, 2018). Market

efficiency is the ability of market to incorporates information that provide the maximum amount

of opportunities as well. There are there are three types of market efficiency in the market that

ensure th response with academic evidence. Following are as follows-

Weak form efficiency states that past price, historical values and trend can not predict

the future prices and it is one of the element of market hypothesis. This concern that

52/20

= 2.6 Per 20 million share

Semi-Strong Form Efficiency

Market price will only react when the information about the bid enters the public domain. The

advent of new information produces the following share prices:

Share Price Y Share Price Z

Day 2 4 10

Day 4 10 2.2

Day 12 10 2.6

Strong-Form Efficiency

Share Price Y Share Price Z

Day 2 10 2.6

Day 4 10 2.6

Day 12 10 2.6

Share Exchange

Prior to bid combined value of Y & Z= 50+14

= 64/24

= 2.67

Under semi-strong efficiency anticipated savings will not emerge until day 12

Under strong form efficiency this information will lead to the market immediately.

Anticipated Operational Savings per Share= 2.6/24

0.11

Market efficiency refers to the degree at which market price reflect all relevant

information. If market are efficient, then all information is ready incorporates into the price and

it eliminate the possibility of beating the market (Ramskyi and Solon'ko, 2018). Market

efficiency is the ability of market to incorporates information that provide the maximum amount

of opportunities as well. There are there are three types of market efficiency in the market that

ensure th response with academic evidence. Following are as follows-

Weak form efficiency states that past price, historical values and trend can not predict

the future prices and it is one of the element of market hypothesis. This concern that

stock prices reflect all current information. It is extremely difficult for the weak form

efficiency to outperform in the market. The basis of theory of weak form efficiency is

that investor are rational, capable and intelligent. The use of this market efficiency is in

short term profit higher than market average one to correctly pick up the stocks that were

undervalued and overvalued by the fundamental analysis. This does not consider the

technical analysis to be accurate and asserts that fundamental analysis can be flawed and

investor advocate weak from the efficiency assume they can randomly pick investment or

portfolios that gives them similar returns. The use of efficient this market is to be define

the proper weak form of efficiency in the company and leads to many issues in the

company.

Semi-strong form efficiency is an aspect of the efficient market hypothesis (EMH) that

refers to current stock price that adjusted rapidly to release the new public information.

This refers to understand the effectiveness of the investor and will help in taking decision

in fundamental and technical analysis that will be useless in the predicting the stock

future price movement and only material non- public information consider useful for the

trading the market. Apart from that it exist where security prices already prices reflect all

publicly that used to available information that is not possible to earn the excess return.

This helps in maintaining the effective relationship with that give used to give results to

the investor and other kind of trading facility (Shrestha, 2018). This help in analysing the

importance of fundamental and technical that does not use for the predicting the future

price movement. This generally helps in analysing the fact which is usually help in

finding the efficiency in the market.

Strong form efficiency is most stringent version of the efficient market that all

information in the market, where public or private is accounted to stock price and it is

believe that even insider information cannot give the advantages to the investor. The

degree in the market implies that profit exceeding the normal returns that could be

realized regardless of the amount of information investor that has access too. Economist

has designed that this estimate the investment advisory services as the useless that is not

able to give the relevant information. This is important components that also consider as

the random walk theory and states that overall market are randomly influence by the past

efficiency to outperform in the market. The basis of theory of weak form efficiency is

that investor are rational, capable and intelligent. The use of this market efficiency is in

short term profit higher than market average one to correctly pick up the stocks that were

undervalued and overvalued by the fundamental analysis. This does not consider the

technical analysis to be accurate and asserts that fundamental analysis can be flawed and

investor advocate weak from the efficiency assume they can randomly pick investment or

portfolios that gives them similar returns. The use of efficient this market is to be define

the proper weak form of efficiency in the company and leads to many issues in the

company.

Semi-strong form efficiency is an aspect of the efficient market hypothesis (EMH) that

refers to current stock price that adjusted rapidly to release the new public information.

This refers to understand the effectiveness of the investor and will help in taking decision

in fundamental and technical analysis that will be useless in the predicting the stock

future price movement and only material non- public information consider useful for the

trading the market. Apart from that it exist where security prices already prices reflect all

publicly that used to available information that is not possible to earn the excess return.

This helps in maintaining the effective relationship with that give used to give results to

the investor and other kind of trading facility (Shrestha, 2018). This help in analysing the

importance of fundamental and technical that does not use for the predicting the future

price movement. This generally helps in analysing the fact which is usually help in

finding the efficiency in the market.

Strong form efficiency is most stringent version of the efficient market that all

information in the market, where public or private is accounted to stock price and it is

believe that even insider information cannot give the advantages to the investor. The

degree in the market implies that profit exceeding the normal returns that could be

realized regardless of the amount of information investor that has access too. Economist

has designed that this estimate the investment advisory services as the useless that is not

able to give the relevant information. This is important components that also consider as

the random walk theory and states that overall market are randomly influence by the past

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.