Financial Management Report: Decision Making & Stakeholders

VerifiedAdded on 2023/01/11

|13

|4479

|48

Report

AI Summary

This financial management report delves into the core principles and practices essential for sound financial decision-making within organizations. The report begins with an examination of various approaches, techniques, and critical factors influencing effective decision-making, including knowledge-based, formal, and informal approaches, alongside the significance of risk assessment and performance analysis. It then explores the intricacies of stakeholder management, addressing the complexities of managing conflicting objectives among diverse stakeholder groups. The value of management accounting techniques in cost control and maximizing stakeholder value is thoroughly discussed, including variance analysis, historical costing, and marginal costing. Furthermore, the report covers techniques for fraud detection and prevention, emphasizing the importance of ethical decision-making. The second part of the report focuses on applying these concepts to a case study, analyzing how data informs operational and strategic decisions, comparing investment appraisal techniques, and assessing how financial decision-making supports long-term sustainability, including recommendations for improvement. The report aims to enhance understanding of financial accounting and its importance for a business to improve financial sustainability.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

SCENARIO 1..................................................................................................................................1

1. Evaluation of range of approaches, techniques and factors which contribute to effective

decision making in an organisation.............................................................................................1

2. Stakeholder management and the management of conflicting objectives of different

stakeholder groups.......................................................................................................................3

3. The value of management accounting techniques in cost control and maximising

stakeholders value........................................................................................................................3

4. Techniques for fraud detection and prevention and the approach to ethical decision making4

5. Reflection about the learnings of above topics........................................................................5

SCENARIO 2..................................................................................................................................5

1. Identification of the way in which data obtained might help to inform operational and

strategic decisions for the company.............................................................................................5

2. Comparison and contrasting of three investment appraisal techniques and evaluation of their

effectiveness in helping to maximise return on investment.........................................................8

3. Demonstration of the value of techniques in helping to inform financial decision making....9

4. Analysis of the way in which financial decision making supports long-term sustainability...9

5. Recommendation for the way in which management accountant helps to improve financial

sustainability..............................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

Table of Contents.............................................................................................................................2

INTRODUCTION...........................................................................................................................1

SCENARIO 1..................................................................................................................................1

1. Evaluation of range of approaches, techniques and factors which contribute to effective

decision making in an organisation.............................................................................................1

2. Stakeholder management and the management of conflicting objectives of different

stakeholder groups.......................................................................................................................3

3. The value of management accounting techniques in cost control and maximising

stakeholders value........................................................................................................................3

4. Techniques for fraud detection and prevention and the approach to ethical decision making4

5. Reflection about the learnings of above topics........................................................................5

SCENARIO 2..................................................................................................................................5

1. Identification of the way in which data obtained might help to inform operational and

strategic decisions for the company.............................................................................................5

2. Comparison and contrasting of three investment appraisal techniques and evaluation of their

effectiveness in helping to maximise return on investment.........................................................8

3. Demonstration of the value of techniques in helping to inform financial decision making....9

4. Analysis of the way in which financial decision making supports long-term sustainability...9

5. Recommendation for the way in which management accountant helps to improve financial

sustainability..............................................................................................................................10

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial management is a process which is followed by companies when they are

willing to analyse the performance of company. While using it different types of final accounts

are formulated. These are profit and loss account, balance sheet and cash flow statement. For all

the accountants it is very important to make sure that the information which is used by them to

generate the financial statement is accurate. Apar from this they are also responsible to make sue

that are following all the essential principles and rules to generate accounts. It can help to retain

the investors and establish a good market image (Ashmarina, Zotova and Smolina, 2016). Main

aim of this report is to enhance understanding of financial accounting and its importance for a

business to improve financial sustainability. This assignment is segregated in two parts first one

is based upon analysis of key elements of financial accounting. Second part is based upon John

Lewis Partnership Plc which is one of the largest retailers of United Kingdom. It was founded in

year 1929 by John Spedan Lewis. The report covers various topics such as range of approaches,

techniques and factors that contribute in effective decision making, stakeholders management,

value of management accounting techniques, techniques for fraud detection and reflection upon

learning of them. Additionally, use of data to inform operational and strategic decision,

discussion of investment appraisal techniques, value of techniques helping to inform financial

decision making and they way in which it supports long-term sustainability etc. are also

discussed in this project.

SCENARIO 1

1. Evaluation of range of approaches, techniques and factors which contribute to effective

decision making in an organisation

Effective decision making is very important for all the companies as it helps to analyse

the ways in which all the predetermined goals of an organisation could be met. There are various

types of approaches, techniques and factors are used to support the decision making. All of them

are as follows:

Knowledge based approach: This approach is highly focused with quantitative

objective and factual information so that effective decisions could be formulated. In order to

make sure that highly efficient strategies are formed to improve the performance of business this

approach is used (Barr and McClellan, 2018). It is a form of system which is highly focused with

1

Financial management is a process which is followed by companies when they are

willing to analyse the performance of company. While using it different types of final accounts

are formulated. These are profit and loss account, balance sheet and cash flow statement. For all

the accountants it is very important to make sure that the information which is used by them to

generate the financial statement is accurate. Apar from this they are also responsible to make sue

that are following all the essential principles and rules to generate accounts. It can help to retain

the investors and establish a good market image (Ashmarina, Zotova and Smolina, 2016). Main

aim of this report is to enhance understanding of financial accounting and its importance for a

business to improve financial sustainability. This assignment is segregated in two parts first one

is based upon analysis of key elements of financial accounting. Second part is based upon John

Lewis Partnership Plc which is one of the largest retailers of United Kingdom. It was founded in

year 1929 by John Spedan Lewis. The report covers various topics such as range of approaches,

techniques and factors that contribute in effective decision making, stakeholders management,

value of management accounting techniques, techniques for fraud detection and reflection upon

learning of them. Additionally, use of data to inform operational and strategic decision,

discussion of investment appraisal techniques, value of techniques helping to inform financial

decision making and they way in which it supports long-term sustainability etc. are also

discussed in this project.

SCENARIO 1

1. Evaluation of range of approaches, techniques and factors which contribute to effective

decision making in an organisation

Effective decision making is very important for all the companies as it helps to analyse

the ways in which all the predetermined goals of an organisation could be met. There are various

types of approaches, techniques and factors are used to support the decision making. All of them

are as follows:

Knowledge based approach: This approach is highly focused with quantitative

objective and factual information so that effective decisions could be formulated. In order to

make sure that highly efficient strategies are formed to improve the performance of business this

approach is used (Barr and McClellan, 2018). It is a form of system which is highly focused with

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

the capturing of human intelligence so that decisions for future betterment of organisations could

be made. Main purpose of it is to analyse the actual position of business and then find effective

ways to deal with all the adverse impacts of operations which may take place in future.

Formal approach: It is the specific approach or technique which is used in effective

decision making so that performance of business could be improved. When it is applied by the

managers then they pay attention towards proper structure, processes and systems so that they

can assure that decisions taken by them are resulting positively for business. It helps in effective

decision making because with the help of it, the management can make sure that they have

formed specific strategies by keeping structure, processes and systems in mind. The types of

formal approaches which could be used by companies to form decisions are formal meetings,

video conferencing etc.

Informal approach: This approach is based upon relationships, personal networks and

unwritten rules. When it is used in companies then the decisions are formulated by taking help

with the individuals with whom the managers are having good relations. They guide them to

make highly effective and efficient decisions so that they can improve the performance of

business (Brusca, Gómez‐villegas and Montesinos, 2016). Some of the informal approaches to

make decisions are informal group discussion, asking staff to suggest their views for the

strategies etc.

Some of the key factors which are focused to formulate effective decisions for business

are as follows:

Risk for business: It is one of the key factors which are focused by managers while

planning to make effective decisions. With the help of it, such strategies could be formulated that

may result in enhancement of performance of business. It contributes in the effective decision

making because with the help of it, management will form such judgements which can help to

deal with all the risks which may take place in future.

Actual performance: It is also a factor which help to formulate effective decisions for

business. With the help of it, the managers determine the actual situation and position of business

so that effective strategies for dealing with all the negative aspects could be formed (Chandra,

2017).

The above factors facilitate the effective decision making which help to improve

performance of organisation and meet the desired aim.

2

be made. Main purpose of it is to analyse the actual position of business and then find effective

ways to deal with all the adverse impacts of operations which may take place in future.

Formal approach: It is the specific approach or technique which is used in effective

decision making so that performance of business could be improved. When it is applied by the

managers then they pay attention towards proper structure, processes and systems so that they

can assure that decisions taken by them are resulting positively for business. It helps in effective

decision making because with the help of it, the management can make sure that they have

formed specific strategies by keeping structure, processes and systems in mind. The types of

formal approaches which could be used by companies to form decisions are formal meetings,

video conferencing etc.

Informal approach: This approach is based upon relationships, personal networks and

unwritten rules. When it is used in companies then the decisions are formulated by taking help

with the individuals with whom the managers are having good relations. They guide them to

make highly effective and efficient decisions so that they can improve the performance of

business (Brusca, Gómez‐villegas and Montesinos, 2016). Some of the informal approaches to

make decisions are informal group discussion, asking staff to suggest their views for the

strategies etc.

Some of the key factors which are focused to formulate effective decisions for business

are as follows:

Risk for business: It is one of the key factors which are focused by managers while

planning to make effective decisions. With the help of it, such strategies could be formulated that

may result in enhancement of performance of business. It contributes in the effective decision

making because with the help of it, management will form such judgements which can help to

deal with all the risks which may take place in future.

Actual performance: It is also a factor which help to formulate effective decisions for

business. With the help of it, the managers determine the actual situation and position of business

so that effective strategies for dealing with all the negative aspects could be formed (Chandra,

2017).

The above factors facilitate the effective decision making which help to improve

performance of organisation and meet the desired aim.

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2. Stakeholder management and the management of conflicting objectives of different

stakeholder groups

Stakeholders management can be defined as the process which is followed by business

entities for the purpose of monitoring, organising and improving the relationship with the

stakeholders. Main purpose of it is to identify needs of all the stakeholders whether they are

internal or external. Internal stakeholders such as employees, manager etc. contribute in the

decision making as they are having detailed information about the perspective of customers and

their needs. The external stakeholders such as suppliers, investors etc. are having need of getting

higher returns and recovering the credit on time. They also contribute in decision making as their

perspectives are used by decisions makers to formulate policies for business.

All the internal as well as external stakeholders are having different objectives. It is very

important for the companies to manage the conflicting objectives of different stakeholder groups.

The internal group of stakeholders is interest in the good performance and attainment of business

objectives but the external group is highly focused with acquiring higher returns on their

investment or recovering credit on time (Ferguson and Morton-Huddleston, 2016). In order to

manage their conflicting objectives, it is very important for the entities to make sure that

organisational goals are formulated by keeping their objectives in mind. With the help of it,

objectives of all the groups of stakeholders could be met.

3. The value of management accounting techniques in cost control and maximising stakeholders

value

Management accounting can be defined as the process of controlling, managing and

monitoring performance of business so that strategic decisions for future could be formed. While

planning to meet the long-term business goals it is very important for all the companies to

conduct managing accounting on yearly basis. It helps managers to form strategies to reach the

predetermined goals and enhance the market image. There are various types of management

accounting techniques which are used by companies to control cost and enhance the shareholder

value. Discussion of all of them is as follows:

Variance analysis: This technique of management accounting is used to analyse the

variation between the actual and standard cost so that it could be analysed that the company is

able to meet the budget or not. While planning to control the cost it could be used by

organisations. It can help to analyse the difference between the planned and actual number so

3

stakeholder groups

Stakeholders management can be defined as the process which is followed by business

entities for the purpose of monitoring, organising and improving the relationship with the

stakeholders. Main purpose of it is to identify needs of all the stakeholders whether they are

internal or external. Internal stakeholders such as employees, manager etc. contribute in the

decision making as they are having detailed information about the perspective of customers and

their needs. The external stakeholders such as suppliers, investors etc. are having need of getting

higher returns and recovering the credit on time. They also contribute in decision making as their

perspectives are used by decisions makers to formulate policies for business.

All the internal as well as external stakeholders are having different objectives. It is very

important for the companies to manage the conflicting objectives of different stakeholder groups.

The internal group of stakeholders is interest in the good performance and attainment of business

objectives but the external group is highly focused with acquiring higher returns on their

investment or recovering credit on time (Ferguson and Morton-Huddleston, 2016). In order to

manage their conflicting objectives, it is very important for the entities to make sure that

organisational goals are formulated by keeping their objectives in mind. With the help of it,

objectives of all the groups of stakeholders could be met.

3. The value of management accounting techniques in cost control and maximising stakeholders

value

Management accounting can be defined as the process of controlling, managing and

monitoring performance of business so that strategic decisions for future could be formed. While

planning to meet the long-term business goals it is very important for all the companies to

conduct managing accounting on yearly basis. It helps managers to form strategies to reach the

predetermined goals and enhance the market image. There are various types of management

accounting techniques which are used by companies to control cost and enhance the shareholder

value. Discussion of all of them is as follows:

Variance analysis: This technique of management accounting is used to analyse the

variation between the actual and standard cost so that it could be analysed that the company is

able to meet the budget or not. While planning to control the cost it could be used by

organisations. It can help to analyse the difference between the planned and actual number so

3

that the managers can formulate strategies to control the cost which is not required. It is mainly

used to analyse cost and revenues for future so that effective decisions to improve business of the

enterprise could be formed.

Historical costing: This management accounting technique states that for all the business

entities it is very important to make sure that they are reflecting the assets and liabilities at the

actual cost rather than the market price. In order to enhance the value for shareholders it is used

by the companies. It will help to record all the elements of balance sheet on their actual cost so

that shareholders can determine actual position of business and can get good returns in the form

of dividend on their funds which are provided by them to the enterprise to carry out operations. It

will be beneficial to increase the value of shareholders so that their interest in business could be

retained for long run in future (Finkler, Smith and Calabrese, 2018).

Marginal costing: This technique is also known as variable costing because only

variable costs are charged to cost units under this approach of management accounting. Main

purpose of it is to determine the additional cost of the increased units which are produced by the

company so that possibility of facing losses could be reduced. With the help of it, objectives such

as cost controlling, increasing shareholder’s value could be achieved. It can guide the managers

to analyse the actual costs of each units so that they could be written off and controlled for

future. On the other hand, when all the costs will be written off properly then it will help the

shareholders to analyse that company is performing well and it will increase tehri value.

4. Techniques for fraud detection and prevention and the approach to ethical decision making

Fraud detection and prevention is very important for all the business entities as it helps to

reduce the errors in the reports. There are various types of techniques which could be used for

the purpose of identification and prevention of frauds. All of them are as follows:

Multiple reporting mechanism: It is one of the main approaches which is used for the

purpose of identification as well as prevention of frauds. According to this technique for all the

companies it is very important to use multiple reports to record the transactions so that when

there is a threat of fraud it could be identified and possibility of it could be prevented.

Proper training to employees: It is another technique which is used for fraud

prevention. When all the staff members will be trained properly then the possibility of frauds will

be very low as they will try to record accurate information in the books.

4

used to analyse cost and revenues for future so that effective decisions to improve business of the

enterprise could be formed.

Historical costing: This management accounting technique states that for all the business

entities it is very important to make sure that they are reflecting the assets and liabilities at the

actual cost rather than the market price. In order to enhance the value for shareholders it is used

by the companies. It will help to record all the elements of balance sheet on their actual cost so

that shareholders can determine actual position of business and can get good returns in the form

of dividend on their funds which are provided by them to the enterprise to carry out operations. It

will be beneficial to increase the value of shareholders so that their interest in business could be

retained for long run in future (Finkler, Smith and Calabrese, 2018).

Marginal costing: This technique is also known as variable costing because only

variable costs are charged to cost units under this approach of management accounting. Main

purpose of it is to determine the additional cost of the increased units which are produced by the

company so that possibility of facing losses could be reduced. With the help of it, objectives such

as cost controlling, increasing shareholder’s value could be achieved. It can guide the managers

to analyse the actual costs of each units so that they could be written off and controlled for

future. On the other hand, when all the costs will be written off properly then it will help the

shareholders to analyse that company is performing well and it will increase tehri value.

4. Techniques for fraud detection and prevention and the approach to ethical decision making

Fraud detection and prevention is very important for all the business entities as it helps to

reduce the errors in the reports. There are various types of techniques which could be used for

the purpose of identification and prevention of frauds. All of them are as follows:

Multiple reporting mechanism: It is one of the main approaches which is used for the

purpose of identification as well as prevention of frauds. According to this technique for all the

companies it is very important to use multiple reports to record the transactions so that when

there is a threat of fraud it could be identified and possibility of it could be prevented.

Proper training to employees: It is another technique which is used for fraud

prevention. When all the staff members will be trained properly then the possibility of frauds will

be very low as they will try to record accurate information in the books.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Ethical decision making: It can be defined as the process of formulating highly ethical

decisions for carrying out operations. It is focused by all the organisations as it can help to

establish a positive market image. While formulating decisions the managers are required to be

aware of all the actions which are taken by them They are required to analyse that whether they

are ethical or unethical (Karadag, 2017).

5. Reflection about the learnings of above topics

From the above discussion various elements are being learned. From the above four

questions it has been analysed that for all the companies it is very important to use effective

approaches for decision making. All the business entities are required to make sure that

objectives of all the stakeholder groups are met as it can help to meet business goals.

Management accounting plays a vital role in cost controlling and enhancement in stakeholder’s

values as it techniques are highly focused with it. Apart from this, the above discussion helped to

enhance knowledge about techniques which could eb used for fraud detection and prevention

purpose.

SCENARIO 2

1. Identification of the way in which data obtained might help to inform operational and strategic

decisions for the company

John Lewis Partnership Plc is one of the biggest retail firms of UK which is operating

business all around the world. In order to analyse the performance of company different ratios

are calculated which are as follows:

Return on equity ratio: It is used by companies to analyse the rate of return which is

provided by them to the shareholders for the shares which are owned by them within the

organisation. When it will be increased as compare to the previous year then it shows that the

entity is providing more value to the shareholders. If it will be decreased then the value of

shareholders will be decreased. While analysing performance of John Lewis Partnership it is also

used (Madura, 2020).

Gross profit margin ratio: It is one of the main profitability ratios which are analysed

by investors so that they can determine that the enterprise will be able to provide them higher

returns on the money which will be invested by them. With the help of it, it could be determined

that the company is able to generate appropriate profits to fulfil requirements of all the

5

decisions for carrying out operations. It is focused by all the organisations as it can help to

establish a positive market image. While formulating decisions the managers are required to be

aware of all the actions which are taken by them They are required to analyse that whether they

are ethical or unethical (Karadag, 2017).

5. Reflection about the learnings of above topics

From the above discussion various elements are being learned. From the above four

questions it has been analysed that for all the companies it is very important to use effective

approaches for decision making. All the business entities are required to make sure that

objectives of all the stakeholder groups are met as it can help to meet business goals.

Management accounting plays a vital role in cost controlling and enhancement in stakeholder’s

values as it techniques are highly focused with it. Apart from this, the above discussion helped to

enhance knowledge about techniques which could eb used for fraud detection and prevention

purpose.

SCENARIO 2

1. Identification of the way in which data obtained might help to inform operational and strategic

decisions for the company

John Lewis Partnership Plc is one of the biggest retail firms of UK which is operating

business all around the world. In order to analyse the performance of company different ratios

are calculated which are as follows:

Return on equity ratio: It is used by companies to analyse the rate of return which is

provided by them to the shareholders for the shares which are owned by them within the

organisation. When it will be increased as compare to the previous year then it shows that the

entity is providing more value to the shareholders. If it will be decreased then the value of

shareholders will be decreased. While analysing performance of John Lewis Partnership it is also

used (Madura, 2020).

Gross profit margin ratio: It is one of the main profitability ratios which are analysed

by investors so that they can determine that the enterprise will be able to provide them higher

returns on the money which will be invested by them. With the help of it, it could be determined

that the company is able to generate appropriate profits to fulfil requirements of all the

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

stakeholders. In order to analyse actual performance of John Lewis Partnership Plc it is used to

assess the profitability.

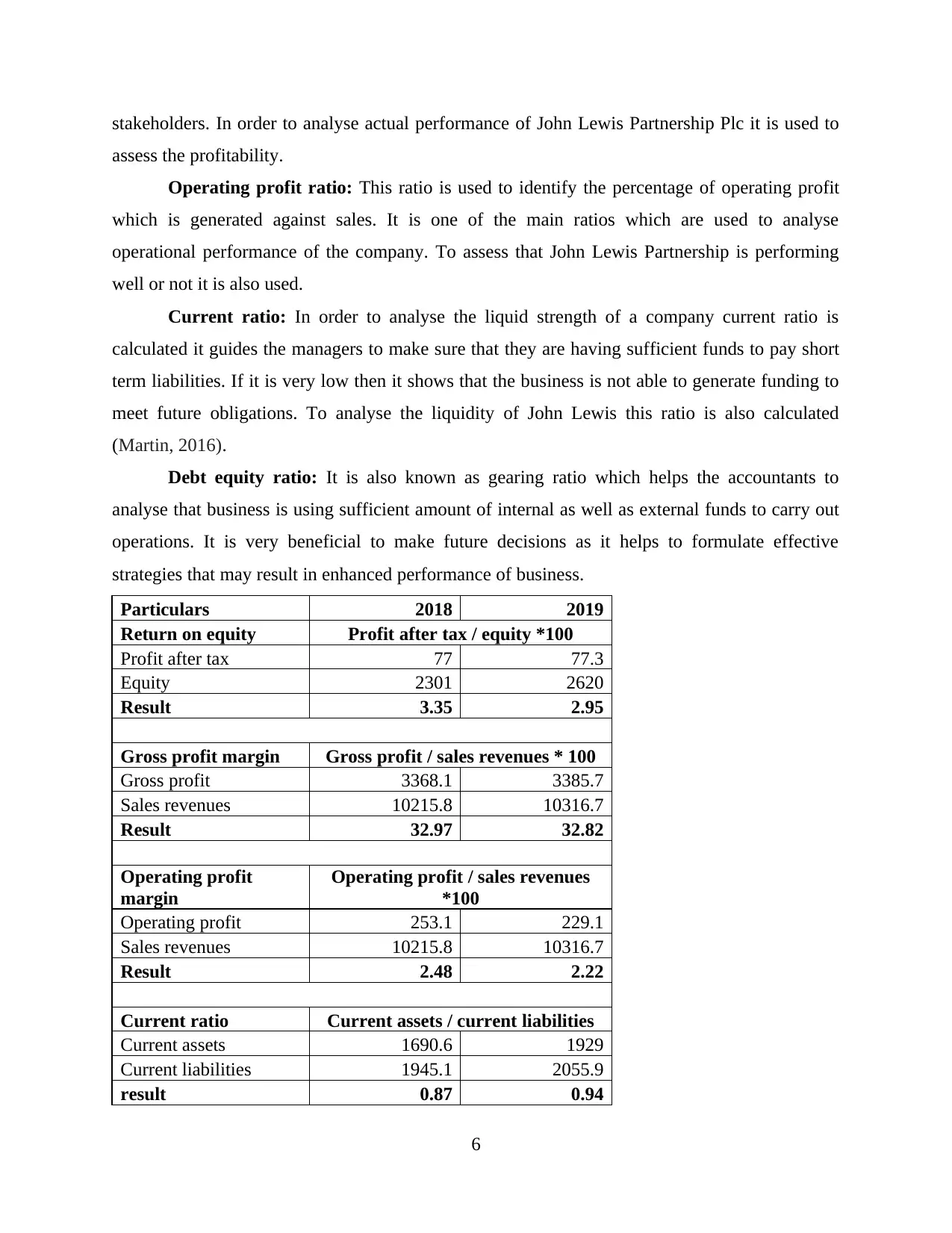

Operating profit ratio: This ratio is used to identify the percentage of operating profit

which is generated against sales. It is one of the main ratios which are used to analyse

operational performance of the company. To assess that John Lewis Partnership is performing

well or not it is also used.

Current ratio: In order to analyse the liquid strength of a company current ratio is

calculated it guides the managers to make sure that they are having sufficient funds to pay short

term liabilities. If it is very low then it shows that the business is not able to generate funding to

meet future obligations. To analyse the liquidity of John Lewis this ratio is also calculated

(Martin, 2016).

Debt equity ratio: It is also known as gearing ratio which helps the accountants to

analyse that business is using sufficient amount of internal as well as external funds to carry out

operations. It is very beneficial to make future decisions as it helps to formulate effective

strategies that may result in enhanced performance of business.

Particulars 2018 2019

Return on equity Profit after tax / equity *100

Profit after tax 77 77.3

Equity 2301 2620

Result 3.35 2.95

Gross profit margin Gross profit / sales revenues * 100

Gross profit 3368.1 3385.7

Sales revenues 10215.8 10316.7

Result 32.97 32.82

Operating profit

margin

Operating profit / sales revenues

*100

Operating profit 253.1 229.1

Sales revenues 10215.8 10316.7

Result 2.48 2.22

Current ratio Current assets / current liabilities

Current assets 1690.6 1929

Current liabilities 1945.1 2055.9

result 0.87 0.94

6

assess the profitability.

Operating profit ratio: This ratio is used to identify the percentage of operating profit

which is generated against sales. It is one of the main ratios which are used to analyse

operational performance of the company. To assess that John Lewis Partnership is performing

well or not it is also used.

Current ratio: In order to analyse the liquid strength of a company current ratio is

calculated it guides the managers to make sure that they are having sufficient funds to pay short

term liabilities. If it is very low then it shows that the business is not able to generate funding to

meet future obligations. To analyse the liquidity of John Lewis this ratio is also calculated

(Martin, 2016).

Debt equity ratio: It is also known as gearing ratio which helps the accountants to

analyse that business is using sufficient amount of internal as well as external funds to carry out

operations. It is very beneficial to make future decisions as it helps to formulate effective

strategies that may result in enhanced performance of business.

Particulars 2018 2019

Return on equity Profit after tax / equity *100

Profit after tax 77 77.3

Equity 2301 2620

Result 3.35 2.95

Gross profit margin Gross profit / sales revenues * 100

Gross profit 3368.1 3385.7

Sales revenues 10215.8 10316.7

Result 32.97 32.82

Operating profit

margin

Operating profit / sales revenues

*100

Operating profit 253.1 229.1

Sales revenues 10215.8 10316.7

Result 2.48 2.22

Current ratio Current assets / current liabilities

Current assets 1690.6 1929

Current liabilities 1945.1 2055.9

result 0.87 0.94

6

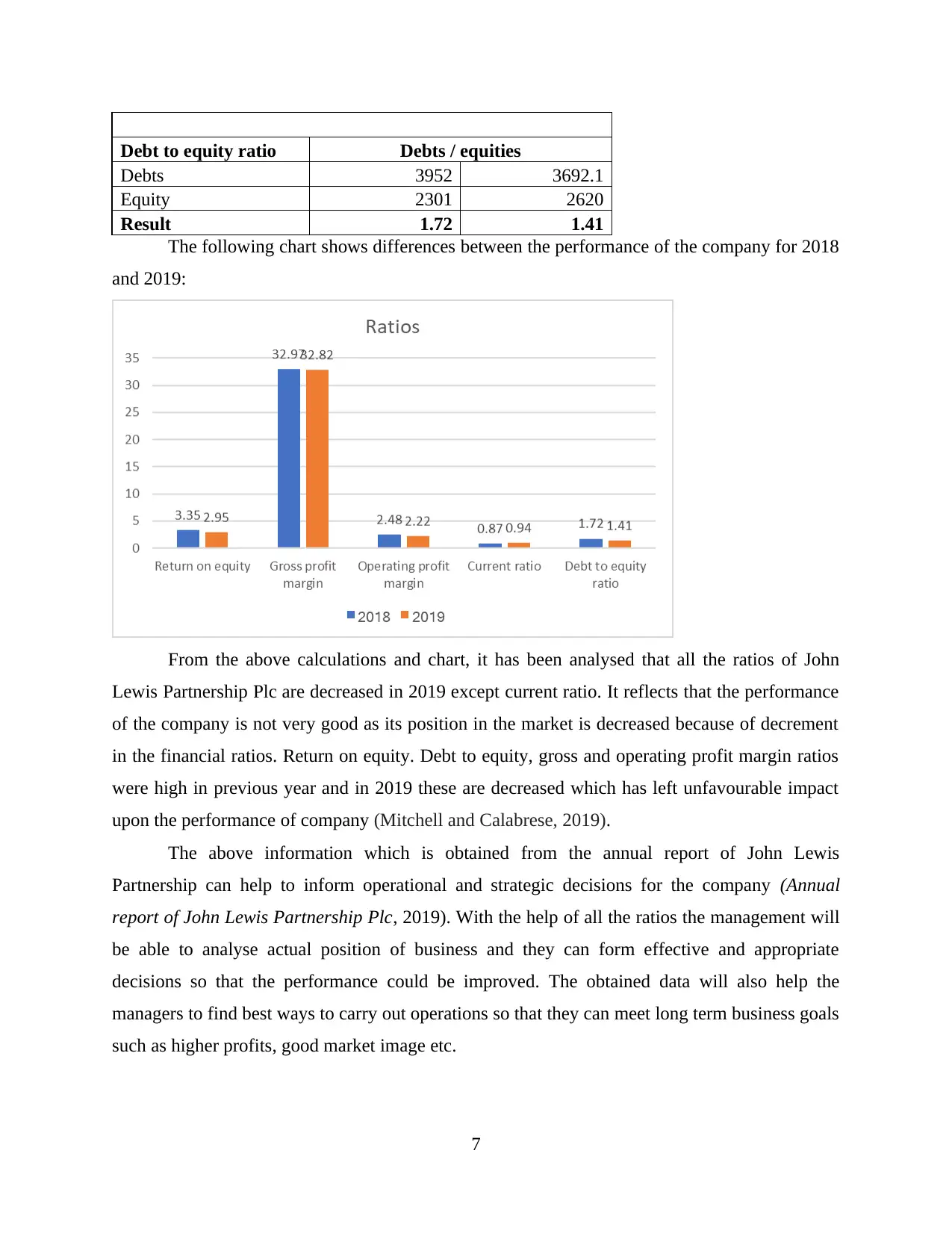

Debt to equity ratio Debts / equities

Debts 3952 3692.1

Equity 2301 2620

Result 1.72 1.41

The following chart shows differences between the performance of the company for 2018

and 2019:

From the above calculations and chart, it has been analysed that all the ratios of John

Lewis Partnership Plc are decreased in 2019 except current ratio. It reflects that the performance

of the company is not very good as its position in the market is decreased because of decrement

in the financial ratios. Return on equity. Debt to equity, gross and operating profit margin ratios

were high in previous year and in 2019 these are decreased which has left unfavourable impact

upon the performance of company (Mitchell and Calabrese, 2019).

The above information which is obtained from the annual report of John Lewis

Partnership can help to inform operational and strategic decisions for the company (Annual

report of John Lewis Partnership Plc, 2019). With the help of all the ratios the management will

be able to analyse actual position of business and they can form effective and appropriate

decisions so that the performance could be improved. The obtained data will also help the

managers to find best ways to carry out operations so that they can meet long term business goals

such as higher profits, good market image etc.

7

Debts 3952 3692.1

Equity 2301 2620

Result 1.72 1.41

The following chart shows differences between the performance of the company for 2018

and 2019:

From the above calculations and chart, it has been analysed that all the ratios of John

Lewis Partnership Plc are decreased in 2019 except current ratio. It reflects that the performance

of the company is not very good as its position in the market is decreased because of decrement

in the financial ratios. Return on equity. Debt to equity, gross and operating profit margin ratios

were high in previous year and in 2019 these are decreased which has left unfavourable impact

upon the performance of company (Mitchell and Calabrese, 2019).

The above information which is obtained from the annual report of John Lewis

Partnership can help to inform operational and strategic decisions for the company (Annual

report of John Lewis Partnership Plc, 2019). With the help of all the ratios the management will

be able to analyse actual position of business and they can form effective and appropriate

decisions so that the performance could be improved. The obtained data will also help the

managers to find best ways to carry out operations so that they can meet long term business goals

such as higher profits, good market image etc.

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

2. Comparison and contrasting of three investment appraisal techniques and evaluation of their

effectiveness in helping to maximise return on investment

Investment appraisal techniques are used in capital budgeting so that the management can

take right decision for business. It is very important for all the business entities to make sure that

they are using right approaches to formulate the decision of making investment in a business

project. There are various types of investment appraisal techniques differences among three of

them is as follows:

Basis Payback period Net present value Accounting rate of

return

Definition It is the time period which

will be required by an

investment project to

repay the value of initial

investment.

It can be defined as the

difference between initial

investment and the

discounted cash inflow of

the company.

It is a technique which is

used to analyse the return

or profits which could be

expected by the company

from the investment.

Results Its results are generated in

terms of time period.

The results which are

provided by it show the

currency or monetary

value.

The results of ARR show

the rate of return which

could be acquired by the

enterprise.

Time

value of

money

Pay back period does not

take time value of money

in to consideration so the

results could be

inaccurate.

Time value of money is

taken in to consideration

which calculating NPV so

that accurate results could

be generated.

In ARR time value of

money is not taken in to

consideration.

Contrasting: There are various types of investment appraisal techniques which are used

by companies to evaluate all the proposed projects that are selected to invest monetary resources.

Some of them are payback period, net present value and accounting rate of return. All of them

have various differences which could be analysed with the help of above table. On the other

hand, all of them have some similarities (Penner, 2016). One of them is facilitating the managers

in decision making. These techniques facilitate the managers to make decision regarding the

investment. Another similarity between them is evaluation of the feasibility of the proposed

8

effectiveness in helping to maximise return on investment

Investment appraisal techniques are used in capital budgeting so that the management can

take right decision for business. It is very important for all the business entities to make sure that

they are using right approaches to formulate the decision of making investment in a business

project. There are various types of investment appraisal techniques differences among three of

them is as follows:

Basis Payback period Net present value Accounting rate of

return

Definition It is the time period which

will be required by an

investment project to

repay the value of initial

investment.

It can be defined as the

difference between initial

investment and the

discounted cash inflow of

the company.

It is a technique which is

used to analyse the return

or profits which could be

expected by the company

from the investment.

Results Its results are generated in

terms of time period.

The results which are

provided by it show the

currency or monetary

value.

The results of ARR show

the rate of return which

could be acquired by the

enterprise.

Time

value of

money

Pay back period does not

take time value of money

in to consideration so the

results could be

inaccurate.

Time value of money is

taken in to consideration

which calculating NPV so

that accurate results could

be generated.

In ARR time value of

money is not taken in to

consideration.

Contrasting: There are various types of investment appraisal techniques which are used

by companies to evaluate all the proposed projects that are selected to invest monetary resources.

Some of them are payback period, net present value and accounting rate of return. All of them

have various differences which could be analysed with the help of above table. On the other

hand, all of them have some similarities (Penner, 2016). One of them is facilitating the managers

in decision making. These techniques facilitate the managers to make decision regarding the

investment. Another similarity between them is evaluation of the feasibility of the proposed

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

projects. All these approaches that are used in capital budgeting help to evaluate all the

investment options so that best one from them could be selected.

3. Demonstration of the value of techniques in helping to inform financial decision making

Financial decision making can be defined as the process of formulating decisions which

can help to attain benefits in future. While making strategies for betterment of business managers

analyse actual performance and then try to formulate effective and efficient decisions for

improvement in the position of business (Yuniningsih, Pertiwi and Purwanto, 2019). In all the

companies such as John Lewis Partnership Plc different types of techniques are used to inform

financial decision making. Some of them are cash flow statement, break even analysis etc.

Description of both of them along with their value in FDM is as follows:

Cash flow statement: It can be defined as a financial statement which is mainly

formulated to record all the cash related transactions that are made by an organisation during the

accounting period. With the help of it, the managers can determine that the company is

generating sufficient amount of cash or not from different types of activities. These are

operating, investing and financing (Renz, 2016). It is very valuable for financial decision making

because it can help to analyse the cash position of enterprise and determine that company is

having inflow or outflow of funds. By analysing all these facts for the entity, the managers will

be able to formulate effective financial decisions which may result positively for the business.

Break even analysis: It is a technique which is used by the organisations to determine

the break even point where cost and revenues are equal to each other. At this point the company

is in the position of no profit and no loss. In financial decision making it plays a vital role

because it guides the accounting professionals to formulate effective strategies so that the

possibility of loss could be ignored and the break-even point could be met.

4. Analysis of the way in which financial decision making supports long-term sustainability

Financial decision making is very important for all the business entities as it helps to find

ways to ignore the possibility of losses. If an entity such as John Lewis Partnership is able to

formulate effective and efficient decisions related to finance then it can help the company to

sustain in the market for long run (Shapiro and Hanouna, 2019). FDM supports the long-term

sustainability because it helps the external as well as internal parties to analyse that the business

is performing well or not. It helps to enhance the market image so that an entity can sustain in the

market successfully.

9

investment options so that best one from them could be selected.

3. Demonstration of the value of techniques in helping to inform financial decision making

Financial decision making can be defined as the process of formulating decisions which

can help to attain benefits in future. While making strategies for betterment of business managers

analyse actual performance and then try to formulate effective and efficient decisions for

improvement in the position of business (Yuniningsih, Pertiwi and Purwanto, 2019). In all the

companies such as John Lewis Partnership Plc different types of techniques are used to inform

financial decision making. Some of them are cash flow statement, break even analysis etc.

Description of both of them along with their value in FDM is as follows:

Cash flow statement: It can be defined as a financial statement which is mainly

formulated to record all the cash related transactions that are made by an organisation during the

accounting period. With the help of it, the managers can determine that the company is

generating sufficient amount of cash or not from different types of activities. These are

operating, investing and financing (Renz, 2016). It is very valuable for financial decision making

because it can help to analyse the cash position of enterprise and determine that company is

having inflow or outflow of funds. By analysing all these facts for the entity, the managers will

be able to formulate effective financial decisions which may result positively for the business.

Break even analysis: It is a technique which is used by the organisations to determine

the break even point where cost and revenues are equal to each other. At this point the company

is in the position of no profit and no loss. In financial decision making it plays a vital role

because it guides the accounting professionals to formulate effective strategies so that the

possibility of loss could be ignored and the break-even point could be met.

4. Analysis of the way in which financial decision making supports long-term sustainability

Financial decision making is very important for all the business entities as it helps to find

ways to ignore the possibility of losses. If an entity such as John Lewis Partnership is able to

formulate effective and efficient decisions related to finance then it can help the company to

sustain in the market for long run (Shapiro and Hanouna, 2019). FDM supports the long-term

sustainability because it helps the external as well as internal parties to analyse that the business

is performing well or not. It helps to enhance the market image so that an entity can sustain in the

market successfully.

9

5. Recommendation for the way in which management accountant helps to improve financial

sustainability

There are various types of recommendations which can help the management accountant to

improve financial sustainability. All of them are as follows:

The management accountant can improve the financial sustainability by guiding the

accounting professionals to analyse actual position of business (Spearman, 2019).

Management accountants can help to improve the financial sustainability by formulating

appropriate internal reports so that the accountants can use them to formulate future

decisions.

CONCLUSION

From the above project report, it has been concluded that financial management is a

technique which is required to be focused by all the organisations to make sure that the generate

final accounts in systematic manner. While planning to improve performance of business it is

very important for all the companies to make sure that they are focusing upon financial

performance. There are various types of approaches which are used to formulate effective

decisions. Apart from this, stakeholder management is also focused by companies so that all the

long-term business goals could be met. In order to analyse the performance different ratios such

as operating and gross profit margin, return on equity etc. are used. Different investment

appraisal techniques are also used by organisations to select best investment option and attain

sustainability for business.

10

sustainability

There are various types of recommendations which can help the management accountant to

improve financial sustainability. All of them are as follows:

The management accountant can improve the financial sustainability by guiding the

accounting professionals to analyse actual position of business (Spearman, 2019).

Management accountants can help to improve the financial sustainability by formulating

appropriate internal reports so that the accountants can use them to formulate future

decisions.

CONCLUSION

From the above project report, it has been concluded that financial management is a

technique which is required to be focused by all the organisations to make sure that the generate

final accounts in systematic manner. While planning to improve performance of business it is

very important for all the companies to make sure that they are focusing upon financial

performance. There are various types of approaches which are used to formulate effective

decisions. Apart from this, stakeholder management is also focused by companies so that all the

long-term business goals could be met. In order to analyse the performance different ratios such

as operating and gross profit margin, return on equity etc. are used. Different investment

appraisal techniques are also used by organisations to select best investment option and attain

sustainability for business.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.