Financial Management Report: Unit 7003V1 Financial Management Analysis

VerifiedAdded on 2023/06/07

|23

|5426

|396

Report

AI Summary

This report, submitted by a student, provides a comprehensive analysis of financial management principles. It begins by outlining the sources of financial data, both internal and external, emphasizing the importance of accurate and reliable information for decision-making. The report then delves into the financial performance of Crawford Healthcare, calculating and analyzing various financial ratios such as gross profit ratio, net profit ratio, gearing ratio, asset turnover ratio, current ratio, acid test ratio, and return on capital employed. Through comparative analysis, the report identifies strengths and weaknesses in the company's financial position, offering recommendations for improvement, particularly in areas like liquidity management. Furthermore, the report addresses budgeting, explaining how a budget can be produced considering financial constraints, targets, legal requirements, and accounting conventions. Finally, the report examines investment proposals, identifying criteria for judgment, analyzing viability, and evaluating their impact on organizational objectives, concluding with recommendations for financial strategy.

DistanceLearningCollege and Training – Submission Sheet

NAME STUDENT NO. If known

DATE

INSTITUTE

COURSE

UNIT TITLE

TOPIC

TASK REF

THE TASK

FINANCIAL MANAGEMENT

NAME STUDENT NO. If known

DATE

INSTITUTE

COURSE

UNIT TITLE

TOPIC

TASK REF

THE TASK

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DistanceLearningCollege and Training – Submission Sheet

TABLE OF CONTENTS

Introduction...................................................................................................................6

Task 1:..........................................................................................................................6

A.C. 1.1 - Determine how to obtain financial data and assess its validity................6

A.C. 1.4 - Review and question financial data..........................................................7

Task 2...........................................................................................................................8

A.C. 1.2 - Apply different types of analytical tools and techniques to a range of

financial documents, formulating conclusions about performance levels and needs

of stakeholders..........................................................................................................8

A.C. 1.3 - Conduct comparative analysis of financial data.....................................10

Task 3:........................................................................................................................12

A.C. 2.1 - Identify how a budget can be produced taking into account financial

constraints and achievement of targets, legal requirements and accounting

conventions.............................................................................................................12

Task 4:........................................................................................................................15

A.C. 2.2 - Analyse the budget outcomes against organisational objectives

identifying alternatives.............................................................................................15

Task 5:........................................................................................................................16

A.C. 3.1 - Identify criteria by which proposals are judged.......................................16

A.C. 3.2 - Analyzing the viability of the proposal for expenditure...........................17

A.C. 3.3 - Identify the strengths and weaknesses and give feedback on the

financial proposal....................................................................................................18

A.C. 3.4 - Evaluate the impact of the proposal on the strategic objectives of the

organisation.............................................................................................................19

Conclusion and Recommendations............................................................................19

TABLE OF CONTENTS

Introduction...................................................................................................................6

Task 1:..........................................................................................................................6

A.C. 1.1 - Determine how to obtain financial data and assess its validity................6

A.C. 1.4 - Review and question financial data..........................................................7

Task 2...........................................................................................................................8

A.C. 1.2 - Apply different types of analytical tools and techniques to a range of

financial documents, formulating conclusions about performance levels and needs

of stakeholders..........................................................................................................8

A.C. 1.3 - Conduct comparative analysis of financial data.....................................10

Task 3:........................................................................................................................12

A.C. 2.1 - Identify how a budget can be produced taking into account financial

constraints and achievement of targets, legal requirements and accounting

conventions.............................................................................................................12

Task 4:........................................................................................................................15

A.C. 2.2 - Analyse the budget outcomes against organisational objectives

identifying alternatives.............................................................................................15

Task 5:........................................................................................................................16

A.C. 3.1 - Identify criteria by which proposals are judged.......................................16

A.C. 3.2 - Analyzing the viability of the proposal for expenditure...........................17

A.C. 3.3 - Identify the strengths and weaknesses and give feedback on the

financial proposal....................................................................................................18

A.C. 3.4 - Evaluate the impact of the proposal on the strategic objectives of the

organisation.............................................................................................................19

Conclusion and Recommendations............................................................................19

DistanceLearningCollege and Training – Submission Sheet

References.................................................................................................................21

List of Tables

Table 1: Calculation of Ratios of Crawford Healthcare................................................5

References.................................................................................................................21

List of Tables

Table 1: Calculation of Ratios of Crawford Healthcare................................................5

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DistanceLearningCollege and Training – Submission Sheet

List of Figures

Figure 1 : Approaches of Budgeting.............................................................................8

List of Figures

Figure 1 : Approaches of Budgeting.............................................................................8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DistanceLearningCollege and Training – Submission Sheet

Introduction

Accurate information has a significant role in the decision-making process as an

organization can make a sound decision only in case accurate information is

supplied to the correct people at the right time in a comprehensibleformat.As per the

assertions of Mimura, et al. (2015), external as well as internal information is

considered by an investor to make a decision relating to investment or to assess the

efficiency of an organization. Present report emphasis on assessment of the external

as well as internal sources from which appropriate financial data can be attained.

Further assessment of the various ratios of Crawford Healthcare has been done in

order to evaluate its financial performance. Discussion relating to methods of

evaluating investment proposals will also be provided in order to ascertain the best

method for the company.

A.C. 1.1 Source of financial data that is HM revenue and customs.

A.C.1.4 include a profit and loss account or other financial data within your

organization (no names need to be disclosed), then as per the Task examine this

data (maybe comparing 2 or 3 previous years) and identify areas that you consider

deserve further investigation/analysis explaining how and why you consider this to

be necessary. Is it profitable?

You then need to refer to the task again and describe the types of data on other

organisations that you may require from time to time, such as competitors, suppliers

(to ensure they are financially sound in order to provide a constant supply chain).

You then need to go on to explain briefly how you would test the validity of the data.

A.C. 1.2 you need to apply these to the financial data provided in AC1.4. Giving

actual calculations of the ratios.

A.C.1.3 calculate the ratios for previous year’s data and referring to the task

compare them to the current year, drawing your own conclusions on your findings,

identifying strengths and weaknesses and making recommendations of ways in

which any shortcomings could be addressed.

Introduction

Accurate information has a significant role in the decision-making process as an

organization can make a sound decision only in case accurate information is

supplied to the correct people at the right time in a comprehensibleformat.As per the

assertions of Mimura, et al. (2015), external as well as internal information is

considered by an investor to make a decision relating to investment or to assess the

efficiency of an organization. Present report emphasis on assessment of the external

as well as internal sources from which appropriate financial data can be attained.

Further assessment of the various ratios of Crawford Healthcare has been done in

order to evaluate its financial performance. Discussion relating to methods of

evaluating investment proposals will also be provided in order to ascertain the best

method for the company.

A.C. 1.1 Source of financial data that is HM revenue and customs.

A.C.1.4 include a profit and loss account or other financial data within your

organization (no names need to be disclosed), then as per the Task examine this

data (maybe comparing 2 or 3 previous years) and identify areas that you consider

deserve further investigation/analysis explaining how and why you consider this to

be necessary. Is it profitable?

You then need to refer to the task again and describe the types of data on other

organisations that you may require from time to time, such as competitors, suppliers

(to ensure they are financially sound in order to provide a constant supply chain).

You then need to go on to explain briefly how you would test the validity of the data.

A.C. 1.2 you need to apply these to the financial data provided in AC1.4. Giving

actual calculations of the ratios.

A.C.1.3 calculate the ratios for previous year’s data and referring to the task

compare them to the current year, drawing your own conclusions on your findings,

identifying strengths and weaknesses and making recommendations of ways in

which any shortcomings could be addressed.

DistanceLearningCollege and Training – Submission Sheet

Task 1:

A.C. 1.1 - Determine how to obtain financial data and assess its validity

Types of data required

Internal Sources

DefensiveData: The specified relates to activities which assure compliance with

regulations. It comprises the integrity of the financial report and governing data. The

same is presented in financial reports.The yearly report is considered extremely

significant in comparison to several companies issue to their shareholders. The

reason behind the same is that the annual report provides shareholders with a

holistic view related to the organisation’s performance and reputation during the

preceding financial year (Laudon and Laudon, 2016). Apart from this, there are other

sources from which information can be assured that it is valid and they are an interim

financial statement, prospectus of the securities, internal account reports, annual

statement and financial reports. Furthermore, as per the study of Petty, et al. (2015),

the financial report comprises financial reports and other pertinent financial

information, whether or not it is in fiscal terms.

Offensive Data: Offensive activities relates to other business functions such as sales

and marketing, legal compliance, IT concern, supply management etc. It also

comprises information relating to competitiveness in the industry in order to assess

the existing trend. Moreover, data relating to suppliers of the product is also required

for assessing the effectiveness of the supply chain (West and Bogers, 2014). In

order to assure the validity of data the source from which information relating to

above-specified variant is assessed that whether the same can be trusted or not.

External Sources:

Revenue and Custom department are believed to be appropriate external resources

as the information provided by them is valid. Thus, decision taken on the basis of

same is appropriate. They are a helpful source of financial information. However,

share prices are affected by other factors; theyreplicate not only information on the

market’s evaluation of the growth and investment risk connected to future dividends,

Task 1:

A.C. 1.1 - Determine how to obtain financial data and assess its validity

Types of data required

Internal Sources

DefensiveData: The specified relates to activities which assure compliance with

regulations. It comprises the integrity of the financial report and governing data. The

same is presented in financial reports.The yearly report is considered extremely

significant in comparison to several companies issue to their shareholders. The

reason behind the same is that the annual report provides shareholders with a

holistic view related to the organisation’s performance and reputation during the

preceding financial year (Laudon and Laudon, 2016). Apart from this, there are other

sources from which information can be assured that it is valid and they are an interim

financial statement, prospectus of the securities, internal account reports, annual

statement and financial reports. Furthermore, as per the study of Petty, et al. (2015),

the financial report comprises financial reports and other pertinent financial

information, whether or not it is in fiscal terms.

Offensive Data: Offensive activities relates to other business functions such as sales

and marketing, legal compliance, IT concern, supply management etc. It also

comprises information relating to competitiveness in the industry in order to assess

the existing trend. Moreover, data relating to suppliers of the product is also required

for assessing the effectiveness of the supply chain (West and Bogers, 2014). In

order to assure the validity of data the source from which information relating to

above-specified variant is assessed that whether the same can be trusted or not.

External Sources:

Revenue and Custom department are believed to be appropriate external resources

as the information provided by them is valid. Thus, decision taken on the basis of

same is appropriate. They are a helpful source of financial information. However,

share prices are affected by other factors; theyreplicate not only information on the

market’s evaluation of the growth and investment risk connected to future dividends,

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DistanceLearningCollege and Training – Submission Sheet

but also on the probability of insolvency. It order to assess same other external

variants should also be assessed in detail.

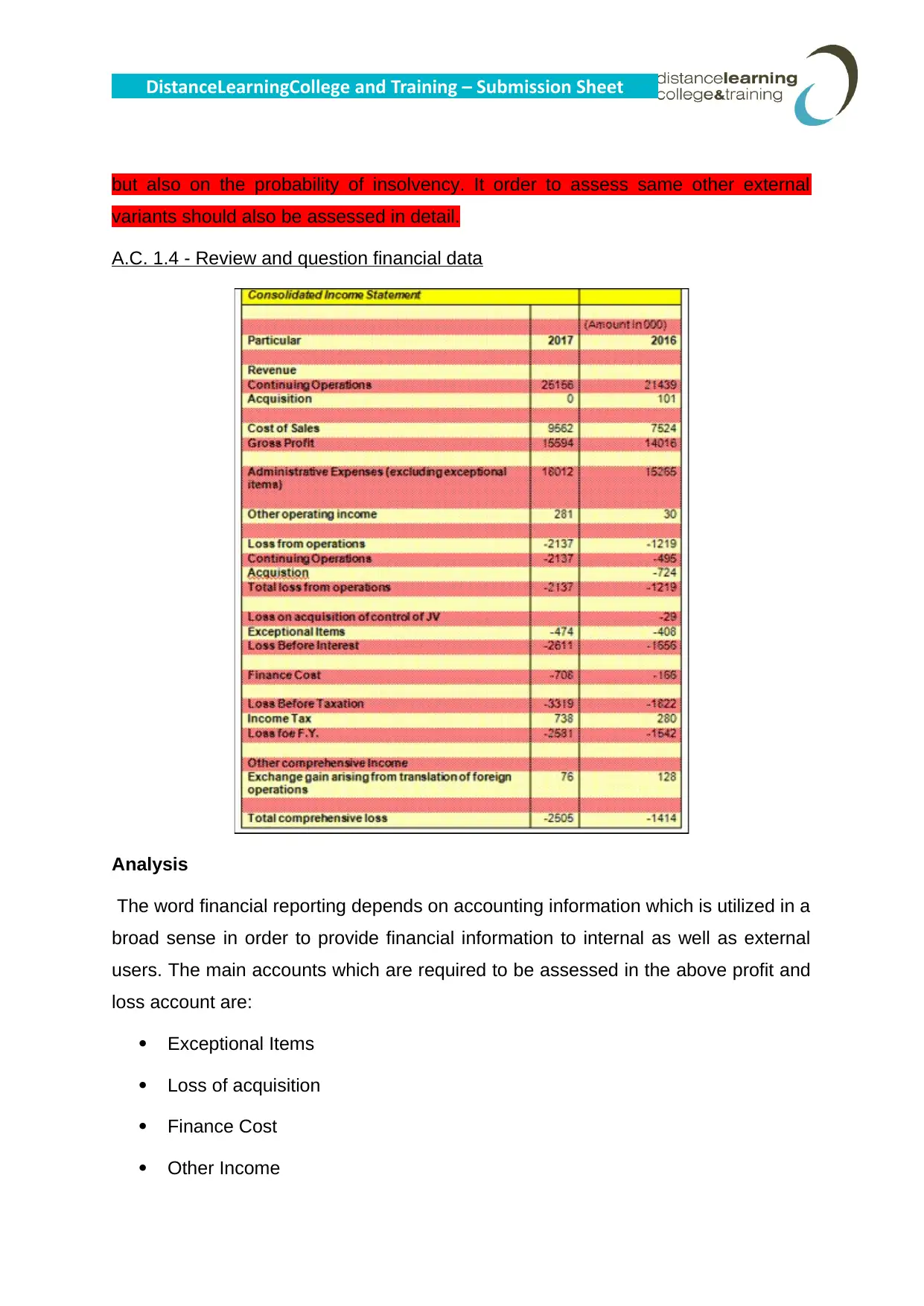

A.C. 1.4 - Review and question financial data

Analysis

The word financial reporting depends on accounting information which is utilized in a

broad sense in order to provide financial information to internal as well as external

users. The main accounts which are required to be assessed in the above profit and

loss account are:

Exceptional Items

Loss of acquisition

Finance Cost

Other Income

but also on the probability of insolvency. It order to assess same other external

variants should also be assessed in detail.

A.C. 1.4 - Review and question financial data

Analysis

The word financial reporting depends on accounting information which is utilized in a

broad sense in order to provide financial information to internal as well as external

users. The main accounts which are required to be assessed in the above profit and

loss account are:

Exceptional Items

Loss of acquisition

Finance Cost

Other Income

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DistanceLearningCollege and Training – Submission Sheet

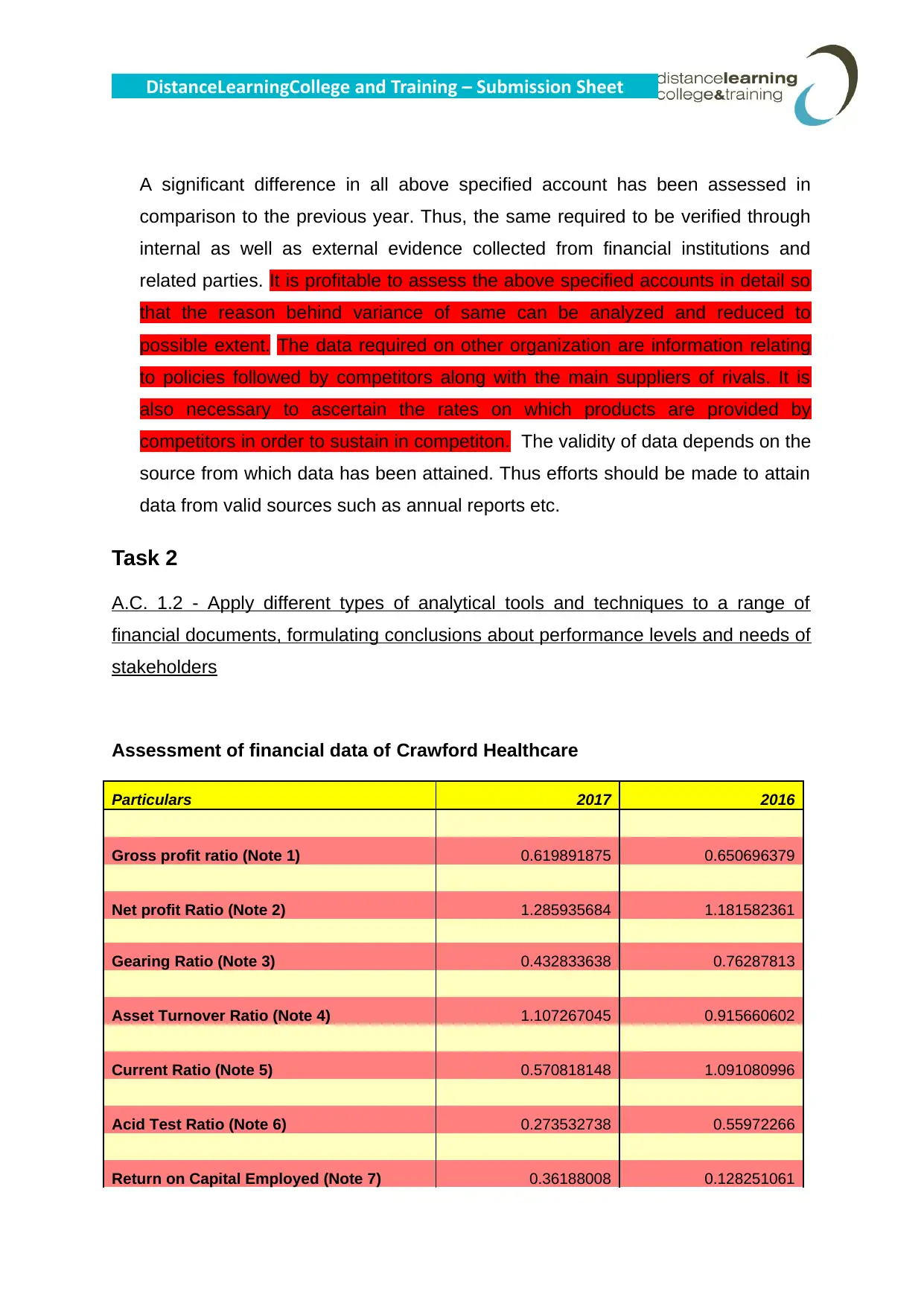

A significant difference in all above specified account has been assessed in

comparison to the previous year. Thus, the same required to be verified through

internal as well as external evidence collected from financial institutions and

related parties. It is profitable to assess the above specified accounts in detail so

that the reason behind variance of same can be analyzed and reduced to

possible extent. The data required on other organization are information relating

to policies followed by competitors along with the main suppliers of rivals. It is

also necessary to ascertain the rates on which products are provided by

competitors in order to sustain in competiton. The validity of data depends on the

source from which data has been attained. Thus efforts should be made to attain

data from valid sources such as annual reports etc.

Task 2

A.C. 1.2 - Apply different types of analytical tools and techniques to a range of

financial documents, formulating conclusions about performance levels and needs of

stakeholders

Assessment of financial data of Crawford Healthcare

Particulars 2017 2016

Gross profit ratio (Note 1) 0.619891875 0.650696379

Net profit Ratio (Note 2) 1.285935684 1.181582361

Gearing Ratio (Note 3) 0.432833638 0.76287813

Asset Turnover Ratio (Note 4) 1.107267045 0.915660602

Current Ratio (Note 5) 0.570818148 1.091080996

Acid Test Ratio (Note 6) 0.273532738 0.55972266

Return on Capital Employed (Note 7) 0.36188008 0.128251061

A significant difference in all above specified account has been assessed in

comparison to the previous year. Thus, the same required to be verified through

internal as well as external evidence collected from financial institutions and

related parties. It is profitable to assess the above specified accounts in detail so

that the reason behind variance of same can be analyzed and reduced to

possible extent. The data required on other organization are information relating

to policies followed by competitors along with the main suppliers of rivals. It is

also necessary to ascertain the rates on which products are provided by

competitors in order to sustain in competiton. The validity of data depends on the

source from which data has been attained. Thus efforts should be made to attain

data from valid sources such as annual reports etc.

Task 2

A.C. 1.2 - Apply different types of analytical tools and techniques to a range of

financial documents, formulating conclusions about performance levels and needs of

stakeholders

Assessment of financial data of Crawford Healthcare

Particulars 2017 2016

Gross profit ratio (Note 1) 0.619891875 0.650696379

Net profit Ratio (Note 2) 1.285935684 1.181582361

Gearing Ratio (Note 3) 0.432833638 0.76287813

Asset Turnover Ratio (Note 4) 1.107267045 0.915660602

Current Ratio (Note 5) 0.570818148 1.091080996

Acid Test Ratio (Note 6) 0.273532738 0.55972266

Return on Capital Employed (Note 7) 0.36188008 0.128251061

DistanceLearningCollege and Training – Submission Sheet

Table 1: Calculation of Ratios of Crawford Healthcare

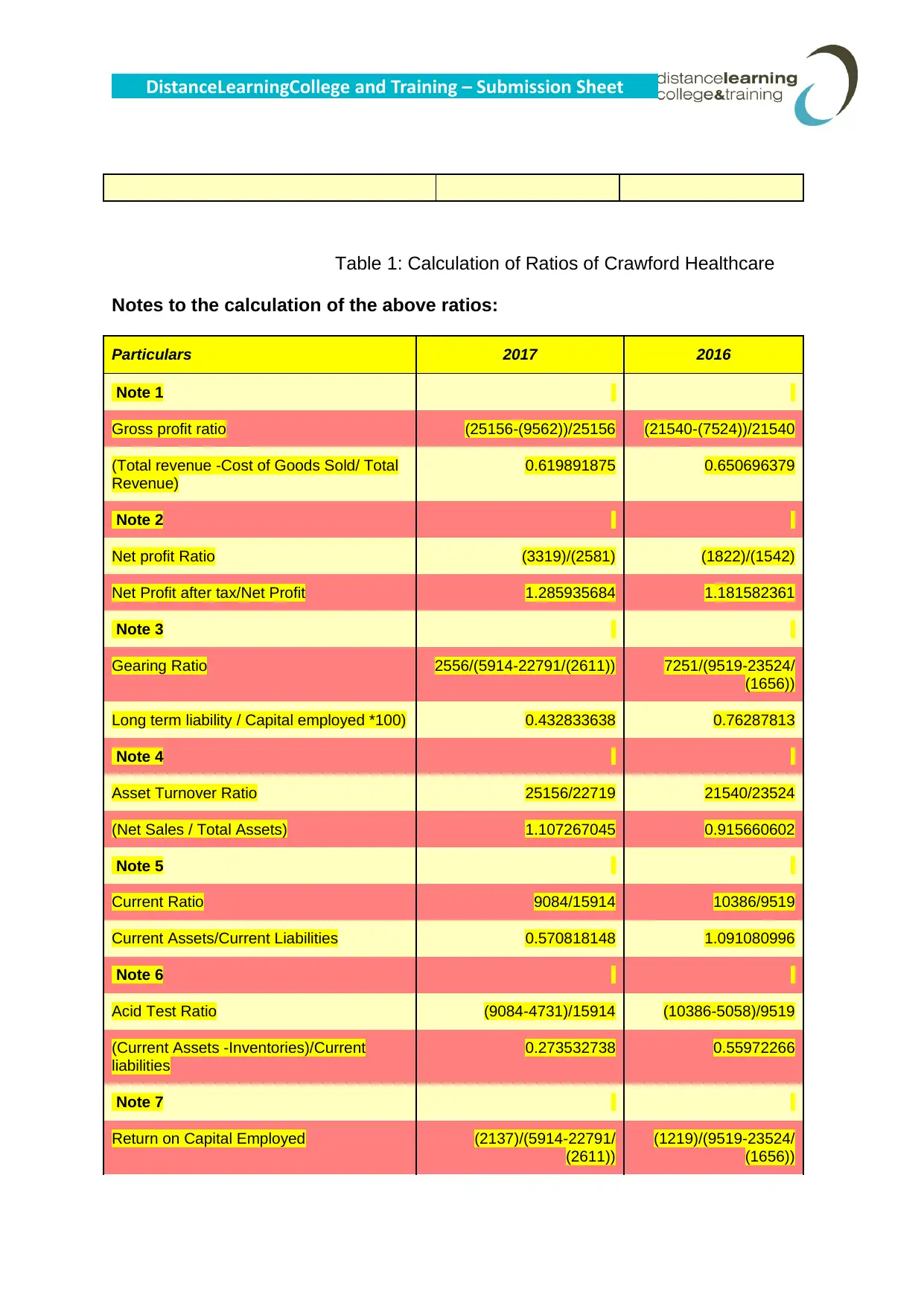

Notes to the calculation of the above ratios:

Particulars 2017 2016

Note 1

Gross profit ratio (25156-(9562))/25156 (21540-(7524))/21540

(Total revenue -Cost of Goods Sold/ Total

Revenue)

0.619891875 0.650696379

Note 2

Net profit Ratio (3319)/(2581) (1822)/(1542)

Net Profit after tax/Net Profit 1.285935684 1.181582361

Note 3

Gearing Ratio 2556/(5914-22791/(2611)) 7251/(9519-23524/

(1656))

Long term liability / Capital employed *100) 0.432833638 0.76287813

Note 4

Asset Turnover Ratio 25156/22719 21540/23524

(Net Sales / Total Assets) 1.107267045 0.915660602

Note 5

Current Ratio 9084/15914 10386/9519

Current Assets/Current Liabilities 0.570818148 1.091080996

Note 6

Acid Test Ratio (9084-4731)/15914 (10386-5058)/9519

(Current Assets -Inventories)/Current

liabilities

0.273532738 0.55972266

Note 7

Return on Capital Employed (2137)/(5914-22791/

(2611))

(1219)/(9519-23524/

(1656))

Table 1: Calculation of Ratios of Crawford Healthcare

Notes to the calculation of the above ratios:

Particulars 2017 2016

Note 1

Gross profit ratio (25156-(9562))/25156 (21540-(7524))/21540

(Total revenue -Cost of Goods Sold/ Total

Revenue)

0.619891875 0.650696379

Note 2

Net profit Ratio (3319)/(2581) (1822)/(1542)

Net Profit after tax/Net Profit 1.285935684 1.181582361

Note 3

Gearing Ratio 2556/(5914-22791/(2611)) 7251/(9519-23524/

(1656))

Long term liability / Capital employed *100) 0.432833638 0.76287813

Note 4

Asset Turnover Ratio 25156/22719 21540/23524

(Net Sales / Total Assets) 1.107267045 0.915660602

Note 5

Current Ratio 9084/15914 10386/9519

Current Assets/Current Liabilities 0.570818148 1.091080996

Note 6

Acid Test Ratio (9084-4731)/15914 (10386-5058)/9519

(Current Assets -Inventories)/Current

liabilities

0.273532738 0.55972266

Note 7

Return on Capital Employed (2137)/(5914-22791/

(2611))

(1219)/(9519-23524/

(1656))

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

DistanceLearningCollege and Training – Submission Sheet

Net Operating Profit/Capital Employed 0.36188008 0.128251061

A.C. 1.3 - Conduct comparative analysis of financial data

Net Operating Profit/Capital Employed 0.36188008 0.128251061

A.C. 1.3 - Conduct comparative analysis of financial data

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

DistanceLearningCollege and Training – Submission Sheet

Strength of company

Profitability

Gross profit (GP) ratio can be defined as a profitability ratio which demonstrates the

connection between gross profit and net sales income(Arkan, 2016). Further, the

gross profit of the company is low which indicates that an organisation is having

decreasing trend of gross profit which means products are under-priced. Thus, the

same can be improved through increasing the price of products. Net profit (NP) ratio

refers to profitability which illustrates the correlation of net profit after tax with net

sales. The net profit can be calculated by dividing the net profit after tax with net

sales of the company. Further, elevated net profit indicates that a Crawford

Healthcare is capableofchanging sales into real income. Thisthe same can be said to

be the strength of the company

Efficiency

Gearing ratio is used to calculate the fraction of the organisation’s borrowed funds to

its equity. Further, this ratio signifies the financial risk to which a company is

subjected to extreme debt can result in financial complexities. The gearing ratio of

the company is low, indicating that the proportion of debt is low than equity. The

asset turnover ratio calculates the value of an organisation’s sales or income

generated relative to the value of its assets. Further, higher asset turnover ratio of

Crawford Healthcare is a strength which indicates that of the companyperforming in

an efficient manner as it signifies that an organisation is producing more income.

Moreover the equity position also represents the efficiency of company in managing

required through its own resources (capital and retained earnings)

Return on capital employed (ROCE) refers to the financial ratio which estimates the

profitability of an organisation as well as the efficiency with which its capital is

utilized. Moreover, it is necessary that the company’s ROE is higher than the cost or

else it implies that the organisation is not employing its capital efficiently as well as it

is not producing shareholder value. Further, ROCE of Crawford Healthcare is

higher, andit is signifying that capital is utilised in an effective manner.

Strength of company

Profitability

Gross profit (GP) ratio can be defined as a profitability ratio which demonstrates the

connection between gross profit and net sales income(Arkan, 2016). Further, the

gross profit of the company is low which indicates that an organisation is having

decreasing trend of gross profit which means products are under-priced. Thus, the

same can be improved through increasing the price of products. Net profit (NP) ratio

refers to profitability which illustrates the correlation of net profit after tax with net

sales. The net profit can be calculated by dividing the net profit after tax with net

sales of the company. Further, elevated net profit indicates that a Crawford

Healthcare is capableofchanging sales into real income. Thisthe same can be said to

be the strength of the company

Efficiency

Gearing ratio is used to calculate the fraction of the organisation’s borrowed funds to

its equity. Further, this ratio signifies the financial risk to which a company is

subjected to extreme debt can result in financial complexities. The gearing ratio of

the company is low, indicating that the proportion of debt is low than equity. The

asset turnover ratio calculates the value of an organisation’s sales or income

generated relative to the value of its assets. Further, higher asset turnover ratio of

Crawford Healthcare is a strength which indicates that of the companyperforming in

an efficient manner as it signifies that an organisation is producing more income.

Moreover the equity position also represents the efficiency of company in managing

required through its own resources (capital and retained earnings)

Return on capital employed (ROCE) refers to the financial ratio which estimates the

profitability of an organisation as well as the efficiency with which its capital is

utilized. Moreover, it is necessary that the company’s ROE is higher than the cost or

else it implies that the organisation is not employing its capital efficiently as well as it

is not producing shareholder value. Further, ROCE of Crawford Healthcare is

higher, andit is signifying that capital is utilised in an effective manner.

DistanceLearningCollege and Training – Submission Sheet

Weakness

Liquidity

The current ratio can be defined as a liquidity and efficiency ratio which calculates

the capability of the company to recompense its short-term liabilities with its current

assets. Further, the current ratio of the company is low which implies that it is not

efficiently capable of paying off its debt and it represents the weakness of the

company. However even the ratio has decreased to a significant extent in

comparison to the previous year, butstill, it has not been lower in comparison to idol

ratio, i.e. 0.5:1. Acid test ratio can be defined as the strong indicator of whether the

company has adequate short-term assets or not. The same implies that whether the

company is capable of meeting its immediate liabilities. Further, the companyhas an

acid test ratio of less than 1, indicating that the company does not have sufficient

liquid assets to meet their current liabilities...

Conclusion and Recommendations

Ratio analysis are applied to assess the actual position of an organization on all

financial as well as non-financial metrics i.e. profitability, liquidity and efficiency.

Thus, in case of above company it can be assessed that it is not able to manage its

cash in appropriate manner as due to same reason it is weak at liquidity

parameters.The same can be improved through managing liquid funds and making

them available all the time. Further, it is recommended to develop appropriate

budget in structured manner so that regular monitoring against organisational or

departmental targets could be done. The required quantum of liquid assets can be

known from same and attempt could be made for their availability.

Weakness

Liquidity

The current ratio can be defined as a liquidity and efficiency ratio which calculates

the capability of the company to recompense its short-term liabilities with its current

assets. Further, the current ratio of the company is low which implies that it is not

efficiently capable of paying off its debt and it represents the weakness of the

company. However even the ratio has decreased to a significant extent in

comparison to the previous year, butstill, it has not been lower in comparison to idol

ratio, i.e. 0.5:1. Acid test ratio can be defined as the strong indicator of whether the

company has adequate short-term assets or not. The same implies that whether the

company is capable of meeting its immediate liabilities. Further, the companyhas an

acid test ratio of less than 1, indicating that the company does not have sufficient

liquid assets to meet their current liabilities...

Conclusion and Recommendations

Ratio analysis are applied to assess the actual position of an organization on all

financial as well as non-financial metrics i.e. profitability, liquidity and efficiency.

Thus, in case of above company it can be assessed that it is not able to manage its

cash in appropriate manner as due to same reason it is weak at liquidity

parameters.The same can be improved through managing liquid funds and making

them available all the time. Further, it is recommended to develop appropriate

budget in structured manner so that regular monitoring against organisational or

departmental targets could be done. The required quantum of liquid assets can be

known from same and attempt could be made for their availability.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 23

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.