University of Sunderland APC308 Financial Management Assignment 2019

VerifiedAdded on 2023/01/11

|14

|3220

|68

Homework Assignment

AI Summary

This financial management assignment addresses two key areas: long-term finance, specifically equity finance, and investment appraisal techniques. The assignment begins with a calculation of profit after tax on shareholders' funds, followed by an evaluation of various terms related to equity finance, including the calculation of the number of shares to be issued, theoretical ex-rights price, and expected earnings per share under different issue price scenarios. The assignment then assesses the benefits of scrip dividends for both shareholders and companies. The second part of the assignment focuses on investment appraisal techniques, including payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR), with calculations and interpretations for a hypothetical scenario. Finally, the assignment critically evaluates the benefits and drawbacks of each investment appraisal technique.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

Question 2 – Long term finance: Equity Finance............................................................................1

1. Calculate the profit after tax @ 20% on shareholders’ funds..................................................1

2. Evaluate the following terms which mentioned below............................................................2

3. Evaluate the benefits of scrip divided in context of shareholders or companies.....................4

Question 3 – Investment Appraisal Techniques..............................................................................5

1. Calculate the following aspect by using investment appraisal techniques..............................5

2. Critically evaluate the benefits and drawbacks of different investment appraisal technique..9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

MAIN BODY..................................................................................................................................1

Question 2 – Long term finance: Equity Finance............................................................................1

1. Calculate the profit after tax @ 20% on shareholders’ funds..................................................1

2. Evaluate the following terms which mentioned below............................................................2

3. Evaluate the benefits of scrip divided in context of shareholders or companies.....................4

Question 3 – Investment Appraisal Techniques..............................................................................5

1. Calculate the following aspect by using investment appraisal techniques..............................5

2. Critically evaluate the benefits and drawbacks of different investment appraisal technique..9

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................12

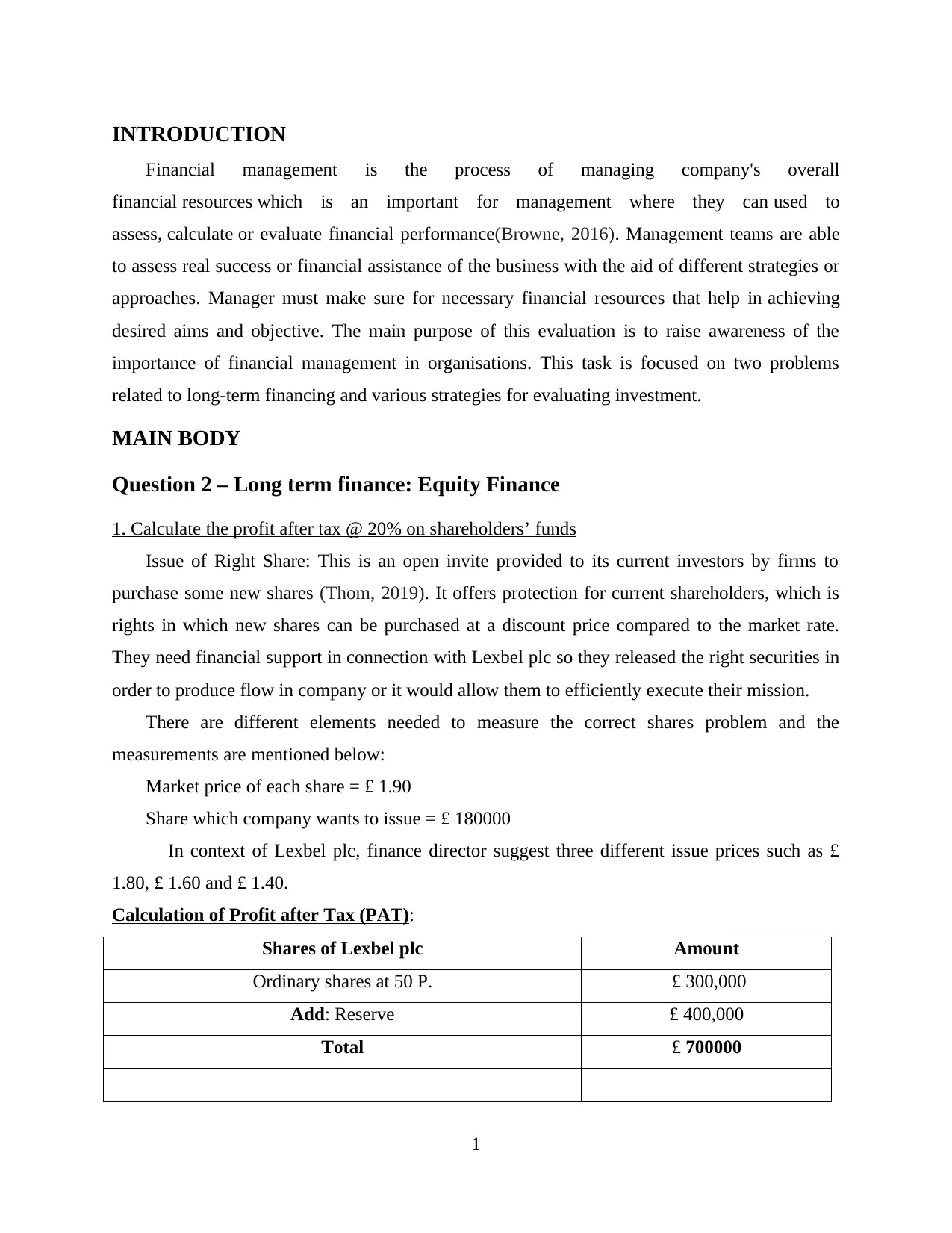

INTRODUCTION

Financial management is the process of managing company's overall

financial resources which is an important for management where they can used to

assess, calculate or evaluate financial performance(Browne, 2016). Management teams are able

to assess real success or financial assistance of the business with the aid of different strategies or

approaches. Manager must make sure for necessary financial resources that help in achieving

desired aims and objective. The main purpose of this evaluation is to raise awareness of the

importance of financial management in organisations. This task is focused on two problems

related to long-term financing and various strategies for evaluating investment.

MAIN BODY

Question 2 – Long term finance: Equity Finance

1. Calculate the profit after tax @ 20% on shareholders’ funds

Issue of Right Share: This is an open invite provided to its current investors by firms to

purchase some new shares (Thom, 2019). It offers protection for current shareholders, which is

rights in which new shares can be purchased at a discount price compared to the market rate.

They need financial support in connection with Lexbel plc so they released the right securities in

order to produce flow in company or it would allow them to efficiently execute their mission.

There are different elements needed to measure the correct shares problem and the

measurements are mentioned below:

Market price of each share = £ 1.90

Share which company wants to issue = £ 180000

In context of Lexbel plc, finance director suggest three different issue prices such as £

1.80, £ 1.60 and £ 1.40.

Calculation of Profit after Tax (PAT):

Shares of Lexbel plc Amount

Ordinary shares at 50 P. £ 300,000

Add: Reserve £ 400,000

Total £ 700000

1

Financial management is the process of managing company's overall

financial resources which is an important for management where they can used to

assess, calculate or evaluate financial performance(Browne, 2016). Management teams are able

to assess real success or financial assistance of the business with the aid of different strategies or

approaches. Manager must make sure for necessary financial resources that help in achieving

desired aims and objective. The main purpose of this evaluation is to raise awareness of the

importance of financial management in organisations. This task is focused on two problems

related to long-term financing and various strategies for evaluating investment.

MAIN BODY

Question 2 – Long term finance: Equity Finance

1. Calculate the profit after tax @ 20% on shareholders’ funds

Issue of Right Share: This is an open invite provided to its current investors by firms to

purchase some new shares (Thom, 2019). It offers protection for current shareholders, which is

rights in which new shares can be purchased at a discount price compared to the market rate.

They need financial support in connection with Lexbel plc so they released the right securities in

order to produce flow in company or it would allow them to efficiently execute their mission.

There are different elements needed to measure the correct shares problem and the

measurements are mentioned below:

Market price of each share = £ 1.90

Share which company wants to issue = £ 180000

In context of Lexbel plc, finance director suggest three different issue prices such as £

1.80, £ 1.60 and £ 1.40.

Calculation of Profit after Tax (PAT):

Shares of Lexbel plc Amount

Ordinary shares at 50 P. £ 300,000

Add: Reserve £ 400,000

Total £ 700000

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

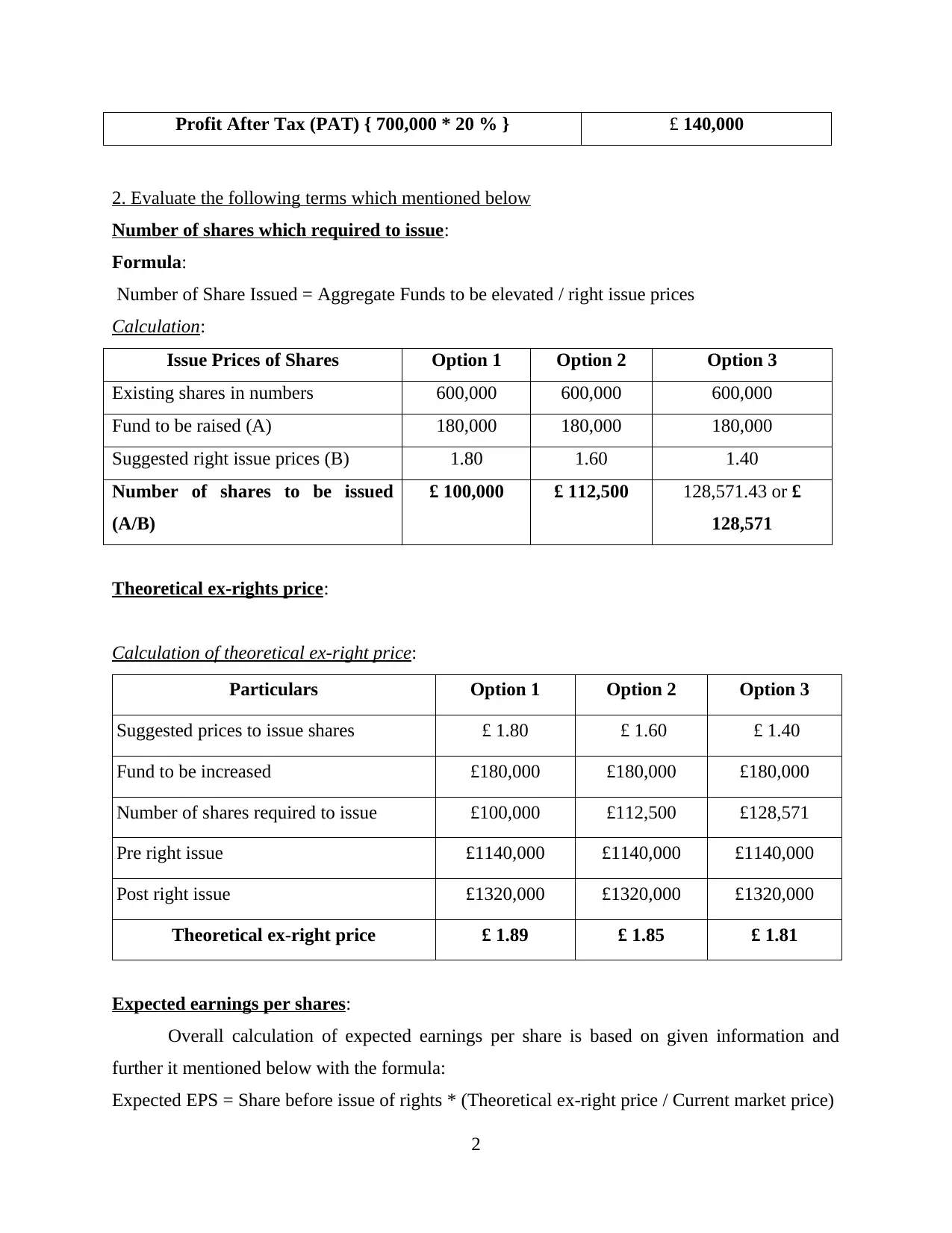

Profit After Tax (PAT) { 700,000 * 20 % } £ 140,000

2. Evaluate the following terms which mentioned below

Number of shares which required to issue:

Formula:

Number of Share Issued = Aggregate Funds to be elevated / right issue prices

Calculation:

Issue Prices of Shares Option 1 Option 2 Option 3

Existing shares in numbers 600,000 600,000 600,000

Fund to be raised (A) 180,000 180,000 180,000

Suggested right issue prices (B) 1.80 1.60 1.40

Number of shares to be issued

(A/B)

£ 100,000 £ 112,500 128,571.43 or £

128,571

Theoretical ex-rights price:

Calculation of theoretical ex-right price:

Particulars Option 1 Option 2 Option 3

Suggested prices to issue shares £ 1.80 £ 1.60 £ 1.40

Fund to be increased £180,000 £180,000 £180,000

Number of shares required to issue £100,000 £112,500 £128,571

Pre right issue £1140,000 £1140,000 £1140,000

Post right issue £1320,000 £1320,000 £1320,000

Theoretical ex-right price £ 1.89 £ 1.85 £ 1.81

Expected earnings per shares:

Overall calculation of expected earnings per share is based on given information and

further it mentioned below with the formula:

Expected EPS = Share before issue of rights * (Theoretical ex-right price / Current market price)

2

2. Evaluate the following terms which mentioned below

Number of shares which required to issue:

Formula:

Number of Share Issued = Aggregate Funds to be elevated / right issue prices

Calculation:

Issue Prices of Shares Option 1 Option 2 Option 3

Existing shares in numbers 600,000 600,000 600,000

Fund to be raised (A) 180,000 180,000 180,000

Suggested right issue prices (B) 1.80 1.60 1.40

Number of shares to be issued

(A/B)

£ 100,000 £ 112,500 128,571.43 or £

128,571

Theoretical ex-rights price:

Calculation of theoretical ex-right price:

Particulars Option 1 Option 2 Option 3

Suggested prices to issue shares £ 1.80 £ 1.60 £ 1.40

Fund to be increased £180,000 £180,000 £180,000

Number of shares required to issue £100,000 £112,500 £128,571

Pre right issue £1140,000 £1140,000 £1140,000

Post right issue £1320,000 £1320,000 £1320,000

Theoretical ex-right price £ 1.89 £ 1.85 £ 1.81

Expected earnings per shares:

Overall calculation of expected earnings per share is based on given information and

further it mentioned below with the formula:

Expected EPS = Share before issue of rights * (Theoretical ex-right price / Current market price)

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

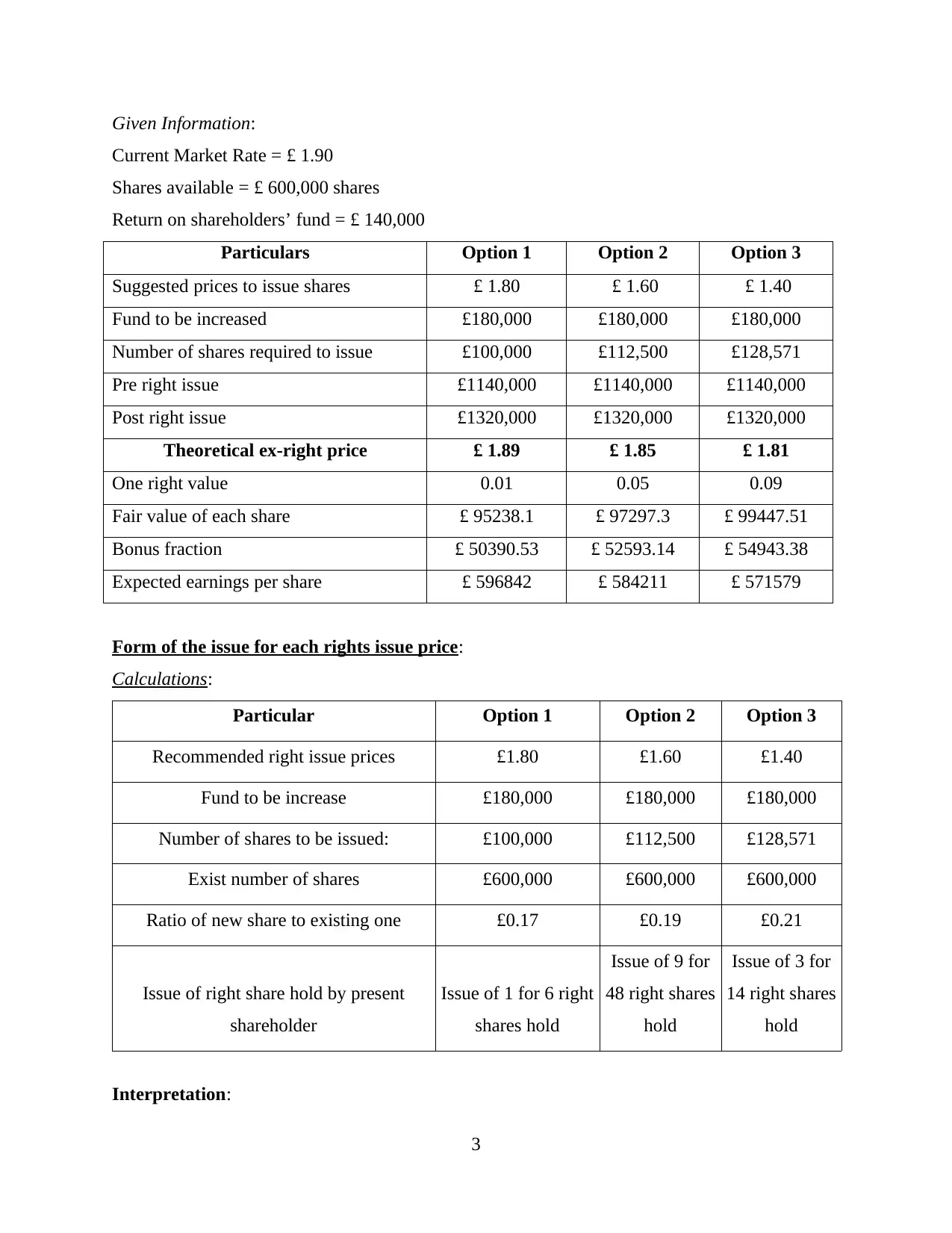

Given Information:

Current Market Rate = £ 1.90

Shares available = £ 600,000 shares

Return on shareholders’ fund = £ 140,000

Particulars Option 1 Option 2 Option 3

Suggested prices to issue shares £ 1.80 £ 1.60 £ 1.40

Fund to be increased £180,000 £180,000 £180,000

Number of shares required to issue £100,000 £112,500 £128,571

Pre right issue £1140,000 £1140,000 £1140,000

Post right issue £1320,000 £1320,000 £1320,000

Theoretical ex-right price £ 1.89 £ 1.85 £ 1.81

One right value 0.01 0.05 0.09

Fair value of each share £ 95238.1 £ 97297.3 £ 99447.51

Bonus fraction £ 50390.53 £ 52593.14 £ 54943.38

Expected earnings per share £ 596842 £ 584211 £ 571579

Form of the issue for each rights issue price:

Calculations:

Particular Option 1 Option 2 Option 3

Recommended right issue prices £1.80 £1.60 £1.40

Fund to be increase £180,000 £180,000 £180,000

Number of shares to be issued: £100,000 £112,500 £128,571

Exist number of shares £600,000 £600,000 £600,000

Ratio of new share to existing one £0.17 £0.19 £0.21

Issue of right share hold by present

shareholder

Issue of 1 for 6 right

shares hold

Issue of 9 for

48 right shares

hold

Issue of 3 for

14 right shares

hold

Interpretation:

3

Current Market Rate = £ 1.90

Shares available = £ 600,000 shares

Return on shareholders’ fund = £ 140,000

Particulars Option 1 Option 2 Option 3

Suggested prices to issue shares £ 1.80 £ 1.60 £ 1.40

Fund to be increased £180,000 £180,000 £180,000

Number of shares required to issue £100,000 £112,500 £128,571

Pre right issue £1140,000 £1140,000 £1140,000

Post right issue £1320,000 £1320,000 £1320,000

Theoretical ex-right price £ 1.89 £ 1.85 £ 1.81

One right value 0.01 0.05 0.09

Fair value of each share £ 95238.1 £ 97297.3 £ 99447.51

Bonus fraction £ 50390.53 £ 52593.14 £ 54943.38

Expected earnings per share £ 596842 £ 584211 £ 571579

Form of the issue for each rights issue price:

Calculations:

Particular Option 1 Option 2 Option 3

Recommended right issue prices £1.80 £1.60 £1.40

Fund to be increase £180,000 £180,000 £180,000

Number of shares to be issued: £100,000 £112,500 £128,571

Exist number of shares £600,000 £600,000 £600,000

Ratio of new share to existing one £0.17 £0.19 £0.21

Issue of right share hold by present

shareholder

Issue of 1 for 6 right

shares hold

Issue of 9 for

48 right shares

hold

Issue of 3 for

14 right shares

hold

Interpretation:

3

From the above calculation, there are three options recommended by the finance director

of Lexbel plc which is mentioned below:

Option 1: Issue of right shares @ £1.80 for £100,000 each. While shares allotted on pro -

rata basis and one share need to remained for 6 shares.

Option 2: Issue of rights @ £ 1.60 for £ 112,500 each. Shareholders allowed to allotting

on pro -rata basis and one share equal to 48 shares.

Option 3: Issue of rights @ £1.70 for £128,571 each. Shareholders should allocate on

pro -rata basis and 1 share should equal to 14 shares.

Critically evaluate the best option among the three right issues options:

By evaluating above three options, it has been observed that actual share price is £1.80 for

a single share. Lexbel plc will benefit from more generating revenue which allows it to perform

business activities (Vanauken, Ascigil and Carraher, 2017). Option one is better as it will yield

more profits relative too many other options.

3. Evaluate the benefits of scrip divided in context of shareholders or companies

Script dividend relates to the divided that is paid to its owners by organisations and is

separate from normal costing (Lytvynchenko, 2016). Such shares are corporate problems

because they lack the necessary cash. This is also given to creditors as cash dividend alternative.

Benefits of script dividend for organization:

Companies profit from maintaining a cash flow to carry out a operating operations.

Such securities offered by businesses that have a high market image or creditworthiness

to offer securities as they are unable to compensate their owners in cash (Yoshida, 2017).

It is one of the main sources of funding that allows companies to raise funds rather than

cash dividends.

This would contribute to the maximization of equity and gearing requirements for

companies at the time of issuance of scrip dividends.

Companies pay scrip dividends at low interest rates and do not impact business share

prices.

Benefits of script dividend for shareholders:

Companies profit from maintaining a cash flow to carry out a operating operations.

Such securities offered by businesses that have a high market image or creditworthiness

to offer securities as they are unable to compensate their owners in cash.

4

of Lexbel plc which is mentioned below:

Option 1: Issue of right shares @ £1.80 for £100,000 each. While shares allotted on pro -

rata basis and one share need to remained for 6 shares.

Option 2: Issue of rights @ £ 1.60 for £ 112,500 each. Shareholders allowed to allotting

on pro -rata basis and one share equal to 48 shares.

Option 3: Issue of rights @ £1.70 for £128,571 each. Shareholders should allocate on

pro -rata basis and 1 share should equal to 14 shares.

Critically evaluate the best option among the three right issues options:

By evaluating above three options, it has been observed that actual share price is £1.80 for

a single share. Lexbel plc will benefit from more generating revenue which allows it to perform

business activities (Vanauken, Ascigil and Carraher, 2017). Option one is better as it will yield

more profits relative too many other options.

3. Evaluate the benefits of scrip divided in context of shareholders or companies

Script dividend relates to the divided that is paid to its owners by organisations and is

separate from normal costing (Lytvynchenko, 2016). Such shares are corporate problems

because they lack the necessary cash. This is also given to creditors as cash dividend alternative.

Benefits of script dividend for organization:

Companies profit from maintaining a cash flow to carry out a operating operations.

Such securities offered by businesses that have a high market image or creditworthiness

to offer securities as they are unable to compensate their owners in cash (Yoshida, 2017).

It is one of the main sources of funding that allows companies to raise funds rather than

cash dividends.

This would contribute to the maximization of equity and gearing requirements for

companies at the time of issuance of scrip dividends.

Companies pay scrip dividends at low interest rates and do not impact business share

prices.

Benefits of script dividend for shareholders:

Companies profit from maintaining a cash flow to carry out a operating operations.

Such securities offered by businesses that have a high market image or creditworthiness

to offer securities as they are unable to compensate their owners in cash.

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is one of the main sources of funding that allows companies to raise funds rather than

cash dividends (Mwangi, Kiarie and Kiai, 2016).

This would contribute to the maximization of equity and gearing requirements for

companies at the time of issuance of scrip dividends.

Companies pay scrip dividends at low interest rates and do not impact business share

prices.

Question 3 – Investment Appraisal Techniques

Investment Appraisal Techniques are used by the organizations so that they are able to

find out whether a particular investment would be profitable or not in the future time period

(Investment Appraisal Techniques, 2020). Lovewell Ltd. can use these techniques to find out

whether the amount it is going to invest will yield it the desired returns or not. For this it can use

its various types of techniques. These techniques are explained as follows-

1. Calculate the following aspect by using investment appraisal techniques

Payback Period: Payback period refers to the time taken in order to recover the cost

incurred in an investment (Payback Period, 2020). The manager of Lovewell Ltd. can make use

of it to identify the cost incurred in investing and in order to recover it effectively so that they

can earn maximum profits.

Formula:

Payback Period = Initial Investment / Net Cash Flow per Period

= £ 275000 / £ 72500

= 3.79 years

Interpretation: It is found that; payback period is 3.79 years which means company will

recover their equipment costs within 4 years. Low recovery time is useful for small Lovewell and

the equipment has a life of six years. Business will invest in purchasing new machinery to

improve their productivity which further leads to increased profit margin.

Working Notes*:

Actual inflow of cash = Cash inflow – Annual Outflow

= £ 85,000 – £ 12,500

= £ 72,500

Initial Investment = £ 275000

5

cash dividends (Mwangi, Kiarie and Kiai, 2016).

This would contribute to the maximization of equity and gearing requirements for

companies at the time of issuance of scrip dividends.

Companies pay scrip dividends at low interest rates and do not impact business share

prices.

Question 3 – Investment Appraisal Techniques

Investment Appraisal Techniques are used by the organizations so that they are able to

find out whether a particular investment would be profitable or not in the future time period

(Investment Appraisal Techniques, 2020). Lovewell Ltd. can use these techniques to find out

whether the amount it is going to invest will yield it the desired returns or not. For this it can use

its various types of techniques. These techniques are explained as follows-

1. Calculate the following aspect by using investment appraisal techniques

Payback Period: Payback period refers to the time taken in order to recover the cost

incurred in an investment (Payback Period, 2020). The manager of Lovewell Ltd. can make use

of it to identify the cost incurred in investing and in order to recover it effectively so that they

can earn maximum profits.

Formula:

Payback Period = Initial Investment / Net Cash Flow per Period

= £ 275000 / £ 72500

= 3.79 years

Interpretation: It is found that; payback period is 3.79 years which means company will

recover their equipment costs within 4 years. Low recovery time is useful for small Lovewell and

the equipment has a life of six years. Business will invest in purchasing new machinery to

improve their productivity which further leads to increased profit margin.

Working Notes*:

Actual inflow of cash = Cash inflow – Annual Outflow

= £ 85,000 – £ 12,500

= £ 72,500

Initial Investment = £ 275000

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

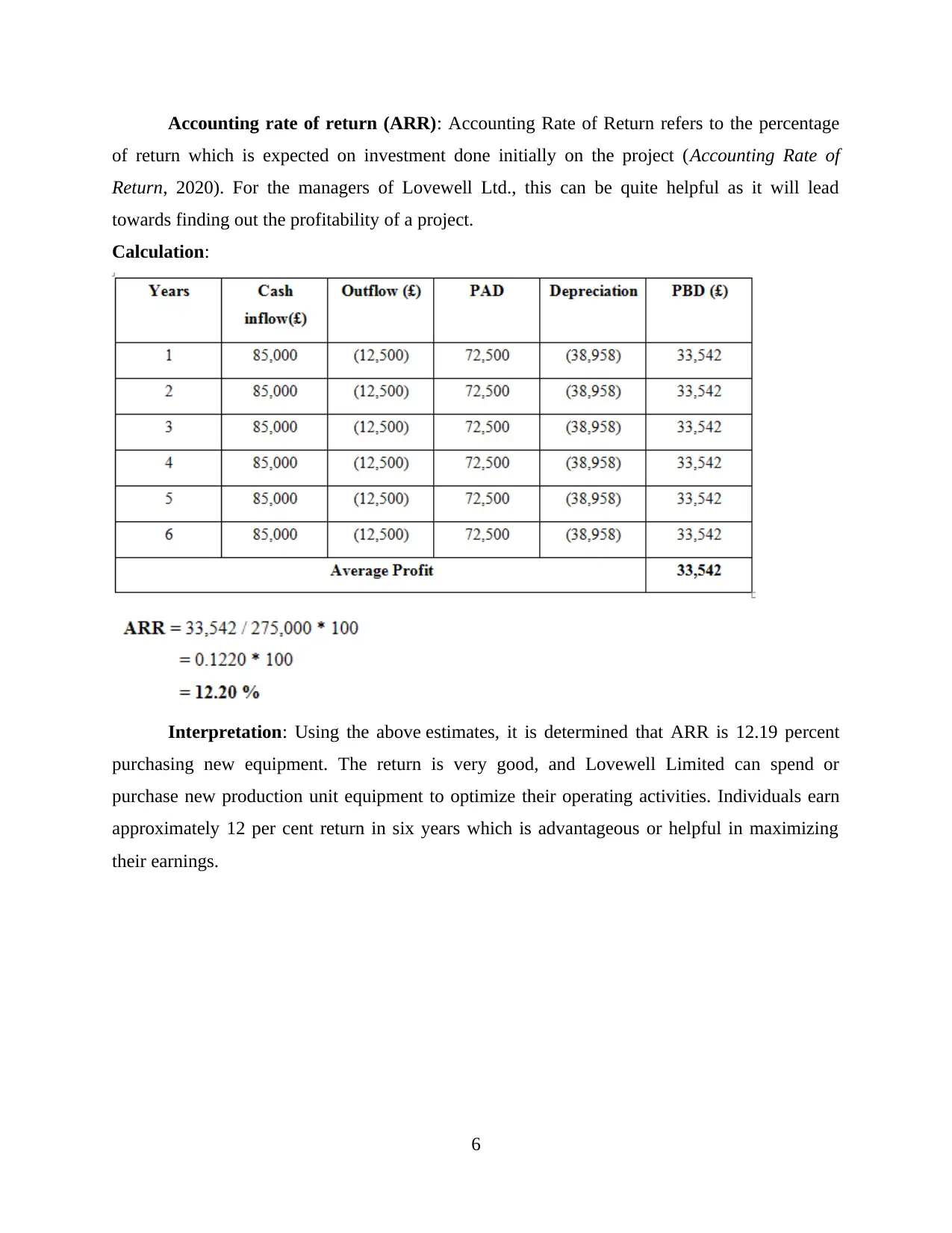

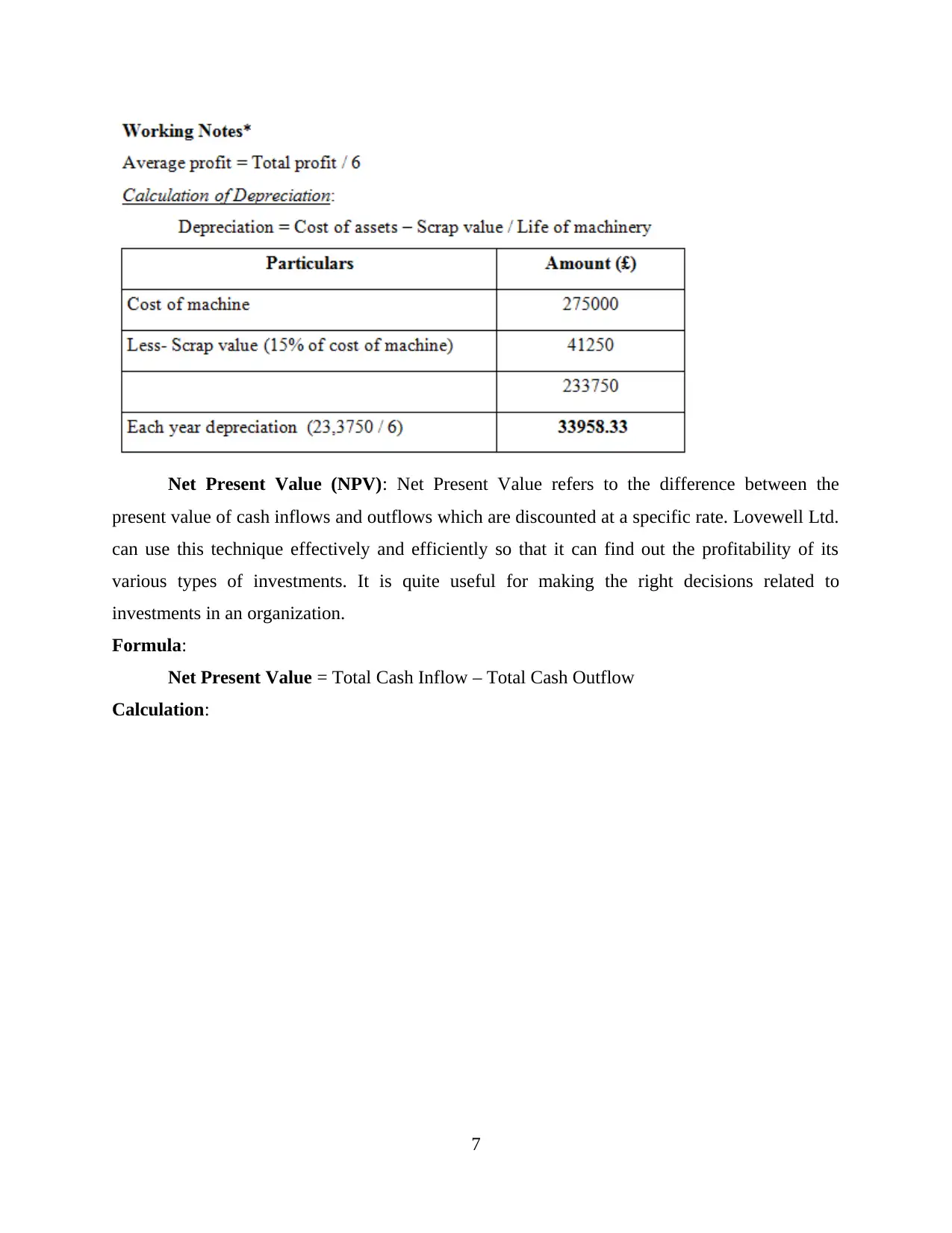

Accounting rate of return (ARR): Accounting Rate of Return refers to the percentage

of return which is expected on investment done initially on the project (Accounting Rate of

Return, 2020). For the managers of Lovewell Ltd., this can be quite helpful as it will lead

towards finding out the profitability of a project.

Calculation:

Interpretation: Using the above estimates, it is determined that ARR is 12.19 percent

purchasing new equipment. The return is very good, and Lovewell Limited can spend or

purchase new production unit equipment to optimize their operating activities. Individuals earn

approximately 12 per cent return in six years which is advantageous or helpful in maximizing

their earnings.

6

of return which is expected on investment done initially on the project (Accounting Rate of

Return, 2020). For the managers of Lovewell Ltd., this can be quite helpful as it will lead

towards finding out the profitability of a project.

Calculation:

Interpretation: Using the above estimates, it is determined that ARR is 12.19 percent

purchasing new equipment. The return is very good, and Lovewell Limited can spend or

purchase new production unit equipment to optimize their operating activities. Individuals earn

approximately 12 per cent return in six years which is advantageous or helpful in maximizing

their earnings.

6

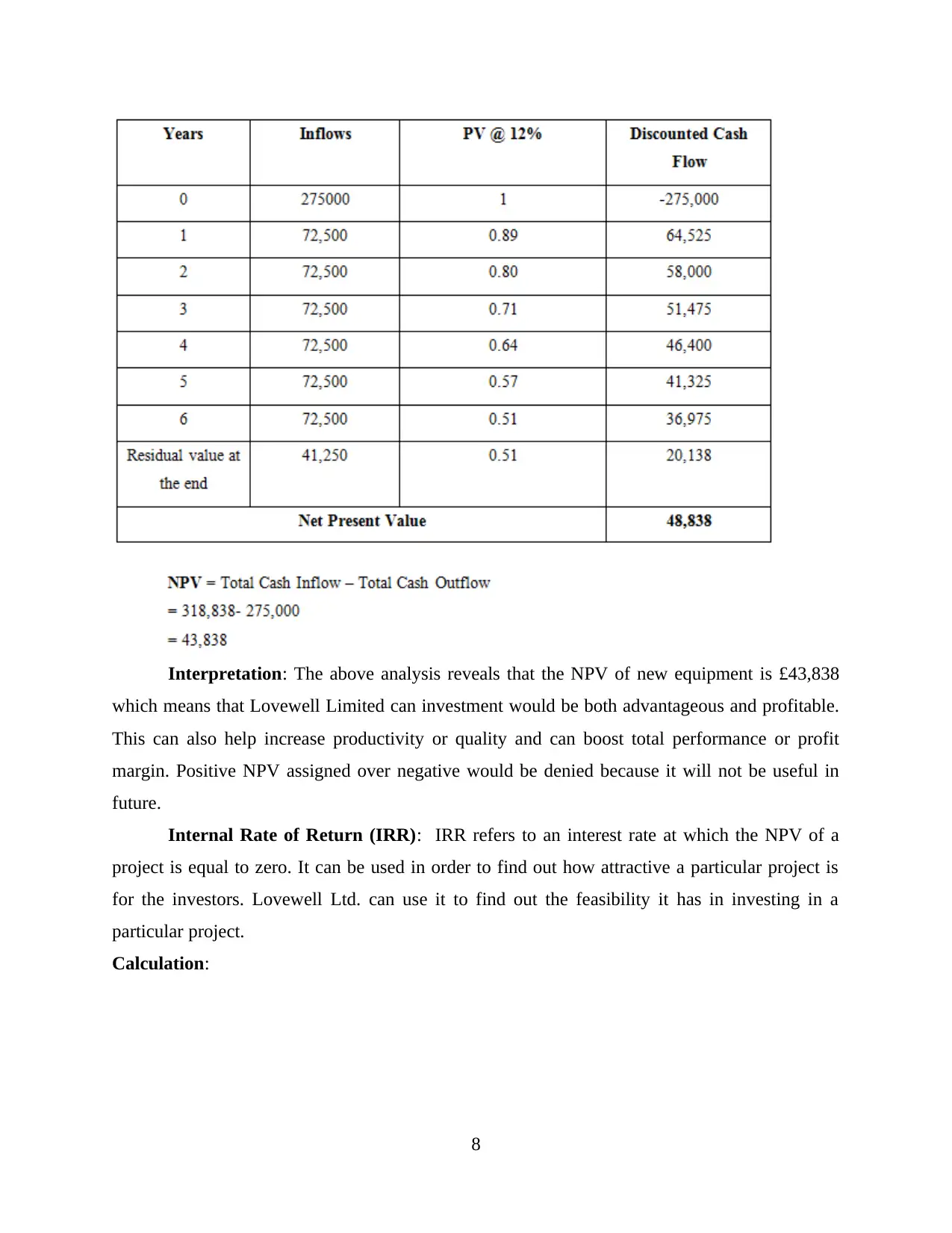

Net Present Value (NPV): Net Present Value refers to the difference between the

present value of cash inflows and outflows which are discounted at a specific rate. Lovewell Ltd.

can use this technique effectively and efficiently so that it can find out the profitability of its

various types of investments. It is quite useful for making the right decisions related to

investments in an organization.

Formula:

Net Present Value = Total Cash Inflow – Total Cash Outflow

Calculation:

7

present value of cash inflows and outflows which are discounted at a specific rate. Lovewell Ltd.

can use this technique effectively and efficiently so that it can find out the profitability of its

various types of investments. It is quite useful for making the right decisions related to

investments in an organization.

Formula:

Net Present Value = Total Cash Inflow – Total Cash Outflow

Calculation:

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: The above analysis reveals that the NPV of new equipment is £43,838

which means that Lovewell Limited can investment would be both advantageous and profitable.

This can also help increase productivity or quality and can boost total performance or profit

margin. Positive NPV assigned over negative would be denied because it will not be useful in

future.

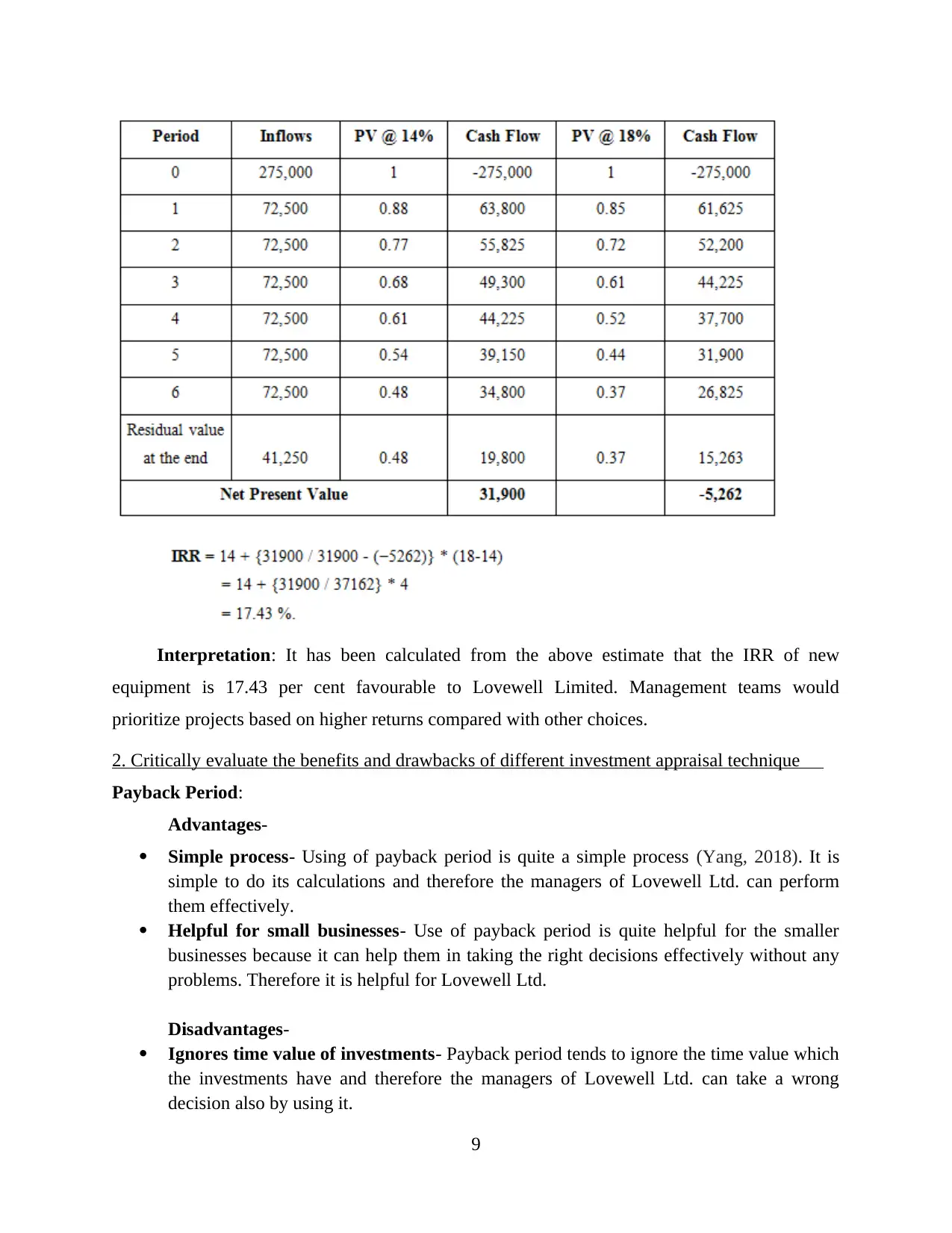

Internal Rate of Return (IRR): IRR refers to an interest rate at which the NPV of a

project is equal to zero. It can be used in order to find out how attractive a particular project is

for the investors. Lovewell Ltd. can use it to find out the feasibility it has in investing in a

particular project.

Calculation:

8

which means that Lovewell Limited can investment would be both advantageous and profitable.

This can also help increase productivity or quality and can boost total performance or profit

margin. Positive NPV assigned over negative would be denied because it will not be useful in

future.

Internal Rate of Return (IRR): IRR refers to an interest rate at which the NPV of a

project is equal to zero. It can be used in order to find out how attractive a particular project is

for the investors. Lovewell Ltd. can use it to find out the feasibility it has in investing in a

particular project.

Calculation:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Interpretation: It has been calculated from the above estimate that the IRR of new

equipment is 17.43 per cent favourable to Lovewell Limited. Management teams would

prioritize projects based on higher returns compared with other choices.

2. Critically evaluate the benefits and drawbacks of different investment appraisal technique

Payback Period:

Advantages-

Simple process- Using of payback period is quite a simple process (Yang, 2018). It is

simple to do its calculations and therefore the managers of Lovewell Ltd. can perform

them effectively.

Helpful for small businesses- Use of payback period is quite helpful for the smaller

businesses because it can help them in taking the right decisions effectively without any

problems. Therefore it is helpful for Lovewell Ltd.

Disadvantages-

Ignores time value of investments- Payback period tends to ignore the time value which

the investments have and therefore the managers of Lovewell Ltd. can take a wrong

decision also by using it.

9

equipment is 17.43 per cent favourable to Lovewell Limited. Management teams would

prioritize projects based on higher returns compared with other choices.

2. Critically evaluate the benefits and drawbacks of different investment appraisal technique

Payback Period:

Advantages-

Simple process- Using of payback period is quite a simple process (Yang, 2018). It is

simple to do its calculations and therefore the managers of Lovewell Ltd. can perform

them effectively.

Helpful for small businesses- Use of payback period is quite helpful for the smaller

businesses because it can help them in taking the right decisions effectively without any

problems. Therefore it is helpful for Lovewell Ltd.

Disadvantages-

Ignores time value of investments- Payback period tends to ignore the time value which

the investments have and therefore the managers of Lovewell Ltd. can take a wrong

decision also by using it.

9

Considers short-term cash flow- Payback period only considers short-term cash flow

for its calculations. Thus it creates a disadvantage for Lovewell Ltd.

Accounting rate of return (ARR):

Advantages-

Based on accounting information- ARR is based on accounting information and

therefore has accuracy in its results (Easton and Monahan, 2016). Therefore the managers

of Lovewell Ltd. can make the right decision related to investments using this technique

effectively.

Easy method- ARR method is quite easy to use. This is so because it allows simplicity

and ease in performing of the calculations and therefore is good for the company to use.

Thus, the managers of Lovewell Ltd. have an advantage here as they can perform the

calculations easily and can check the feasibility of investment without any problems and

issues.

Disadvantages-

Ignores the time value of money- ARR also ignores the time value of money which is

invested in a project. Therefore, for the managers of Lovewell Ltd. it can create a

problem.

Ignores the cash flow from investment- The ARR method completely ignores the cash

flow which is generated from the investments. This is quite important from the point of

view of investments. Thus this creates a disadvantage for the managers of Lovewell Ltd.

as it can lead towards taking of a wrong decision also which can create problems and

issues for the company in the future time period.

Net Present Value (NPV):

Advantages-

Assumption of reinvestment- It assumes that reinvestment will be done (Leyman and

Vanhoucke, 2016). Therefore it it’s advantageous for Lovewell Ltd.

Measurement of profitability- It is a measurement of the level of profitability and

therefore the managers of Lovewell Ltd. can easily find out the profits they can earn from

the investments through the use of this method.

Disadvantages-

Rate of return- With the use of this method it becomes quite difficult to determine the

rate of return. Therefore this can be disadvantageous for the managers of Lovewell Ltd.

Difference in size of projects- The use of this method can be disadvantageous for

Lovewell Ltd. because there is a difference in the size of projects where the investment is

done. Thus it may not give accurate information about the profitability of the projects.

Internal Rate of Return (IRR):

10

for its calculations. Thus it creates a disadvantage for Lovewell Ltd.

Accounting rate of return (ARR):

Advantages-

Based on accounting information- ARR is based on accounting information and

therefore has accuracy in its results (Easton and Monahan, 2016). Therefore the managers

of Lovewell Ltd. can make the right decision related to investments using this technique

effectively.

Easy method- ARR method is quite easy to use. This is so because it allows simplicity

and ease in performing of the calculations and therefore is good for the company to use.

Thus, the managers of Lovewell Ltd. have an advantage here as they can perform the

calculations easily and can check the feasibility of investment without any problems and

issues.

Disadvantages-

Ignores the time value of money- ARR also ignores the time value of money which is

invested in a project. Therefore, for the managers of Lovewell Ltd. it can create a

problem.

Ignores the cash flow from investment- The ARR method completely ignores the cash

flow which is generated from the investments. This is quite important from the point of

view of investments. Thus this creates a disadvantage for the managers of Lovewell Ltd.

as it can lead towards taking of a wrong decision also which can create problems and

issues for the company in the future time period.

Net Present Value (NPV):

Advantages-

Assumption of reinvestment- It assumes that reinvestment will be done (Leyman and

Vanhoucke, 2016). Therefore it it’s advantageous for Lovewell Ltd.

Measurement of profitability- It is a measurement of the level of profitability and

therefore the managers of Lovewell Ltd. can easily find out the profits they can earn from

the investments through the use of this method.

Disadvantages-

Rate of return- With the use of this method it becomes quite difficult to determine the

rate of return. Therefore this can be disadvantageous for the managers of Lovewell Ltd.

Difference in size of projects- The use of this method can be disadvantageous for

Lovewell Ltd. because there is a difference in the size of projects where the investment is

done. Thus it may not give accurate information about the profitability of the projects.

Internal Rate of Return (IRR):

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.