Financial Management Assessment Report for APC 308 Module

VerifiedAdded on 2023/01/16

|17

|3748

|96

Report

AI Summary

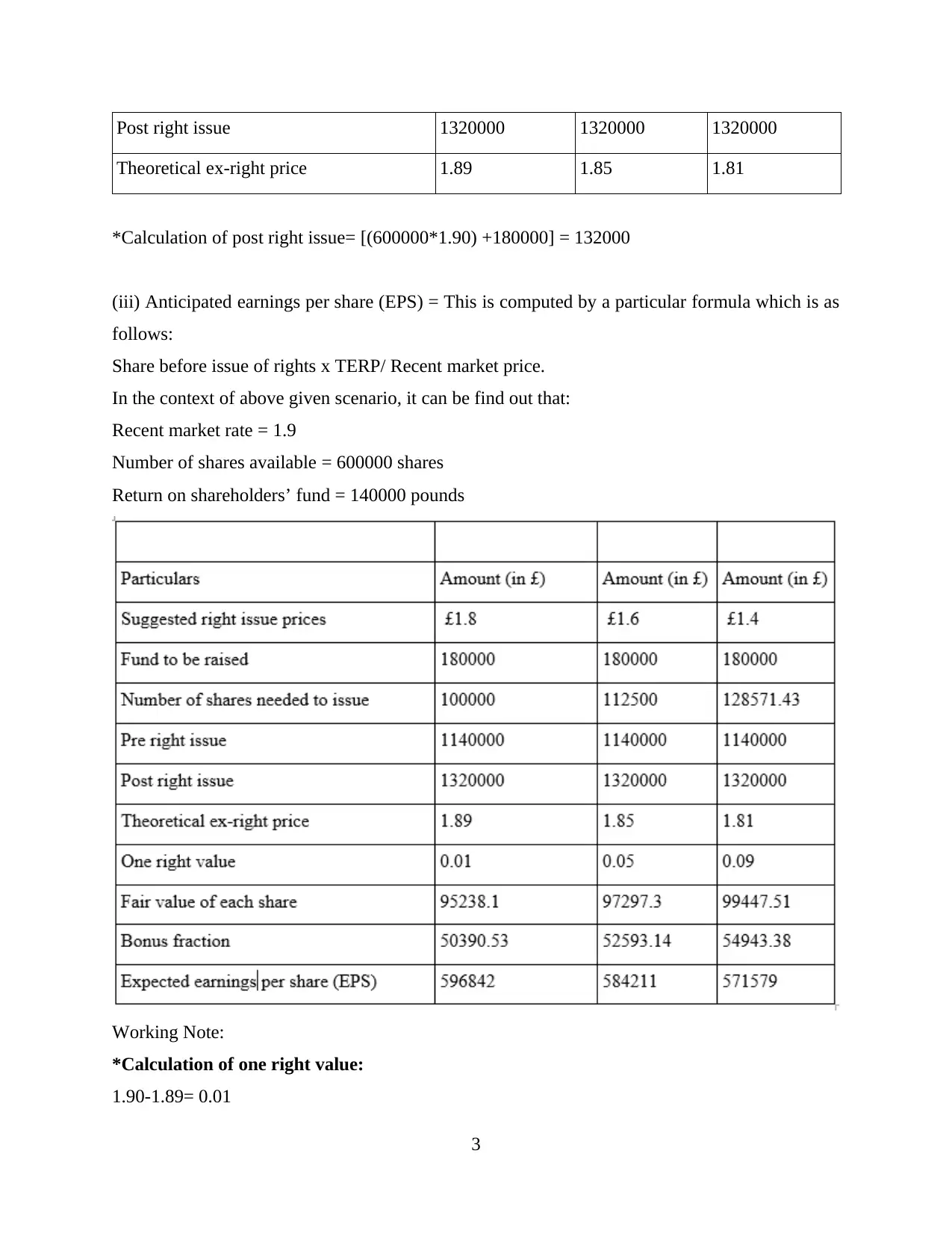

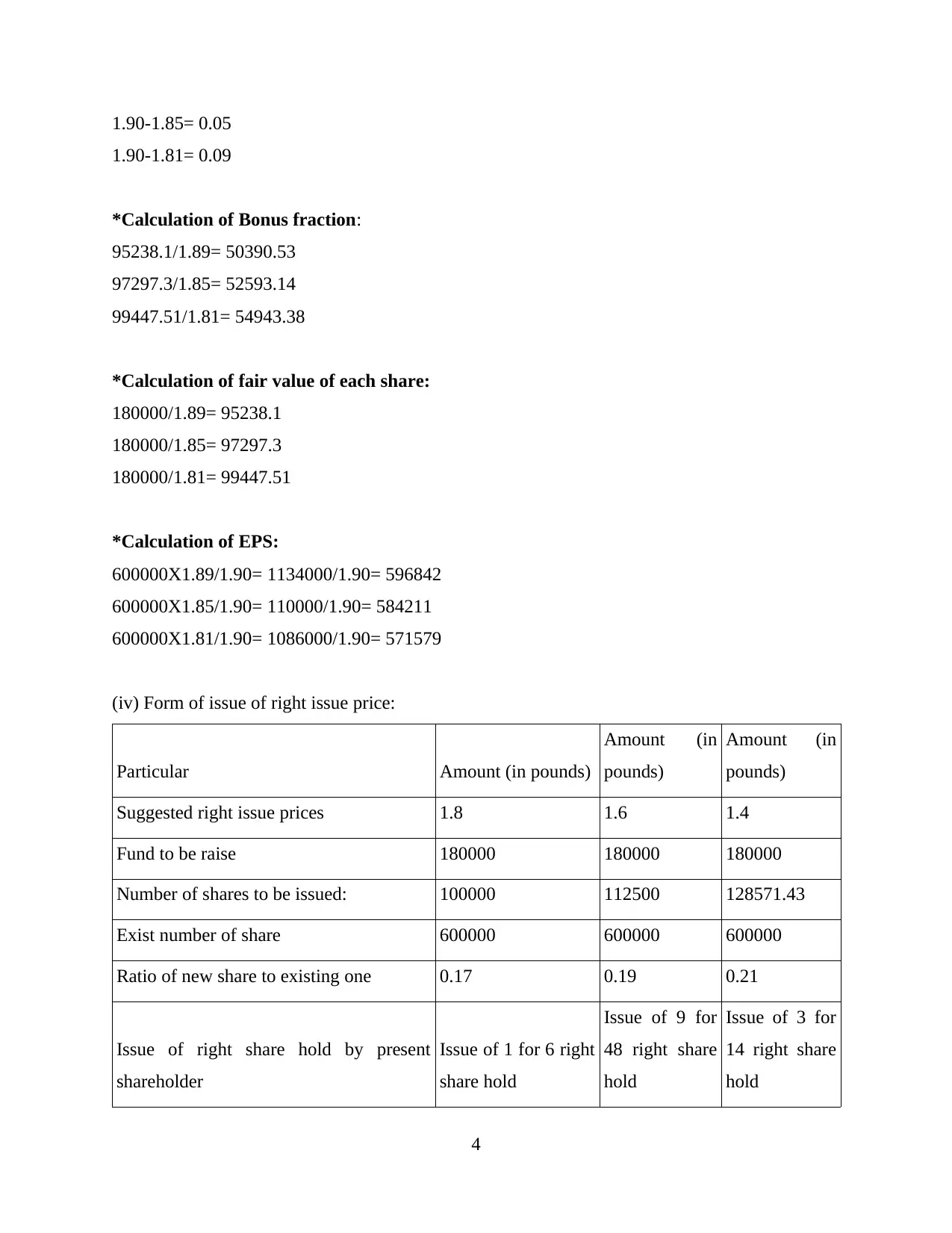

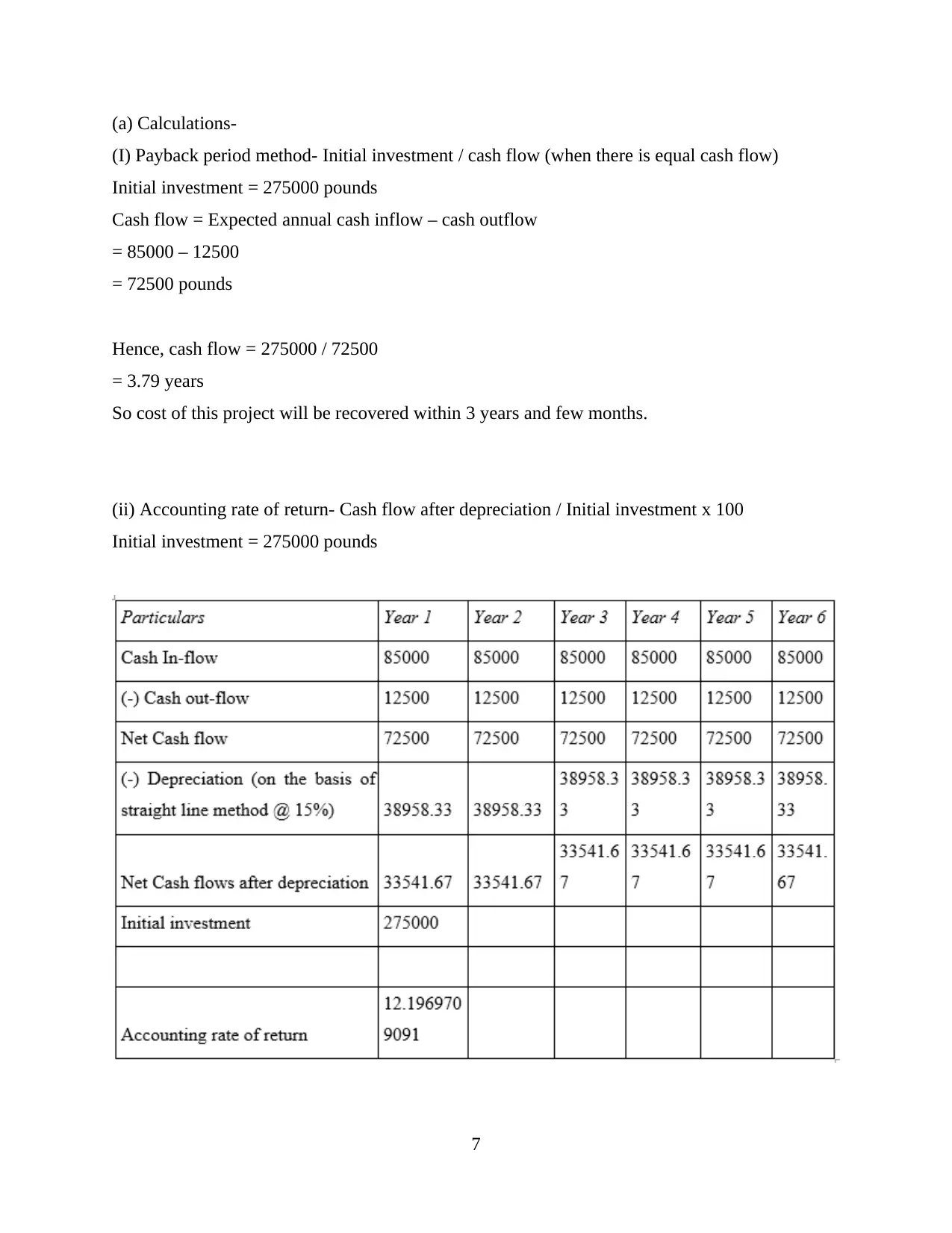

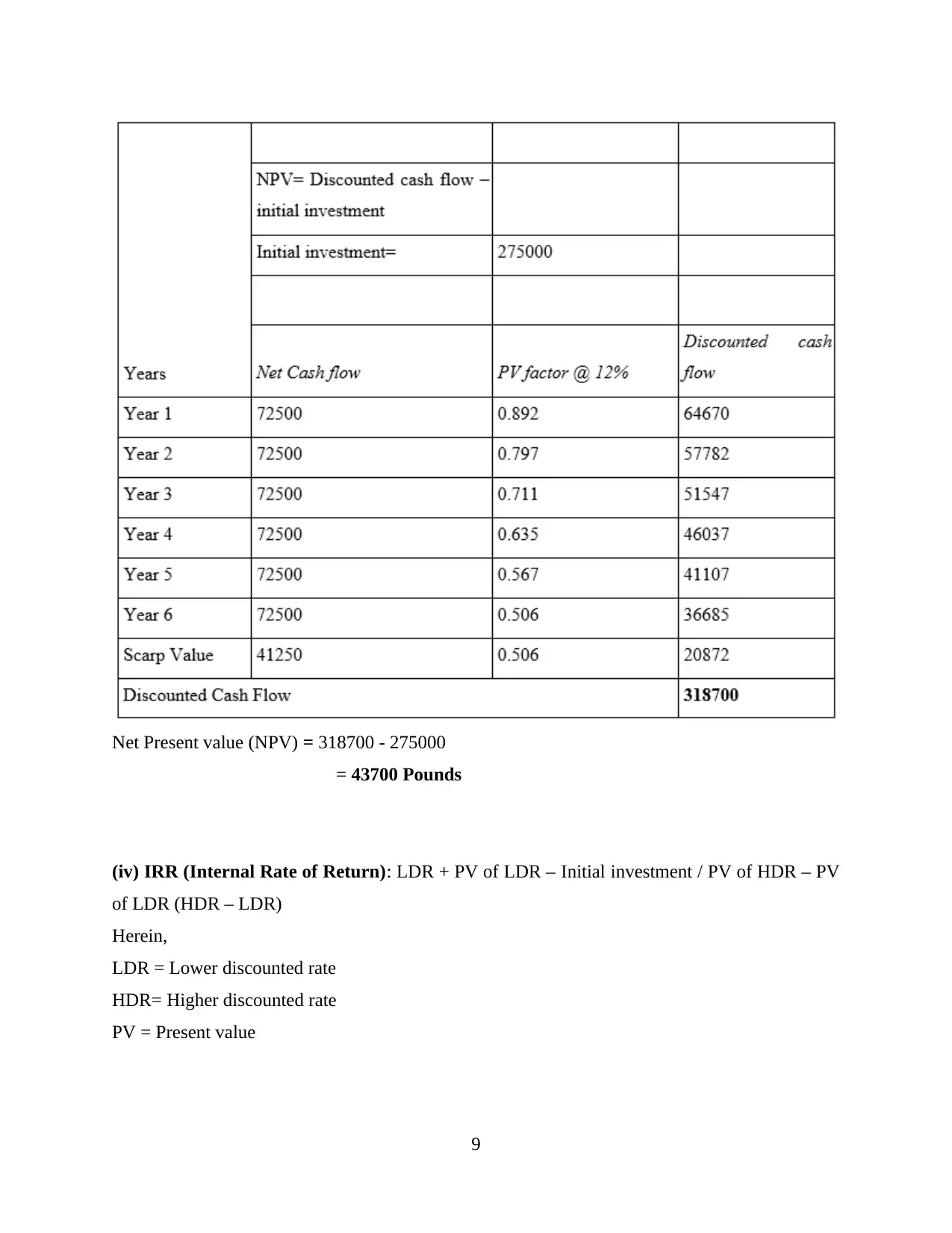

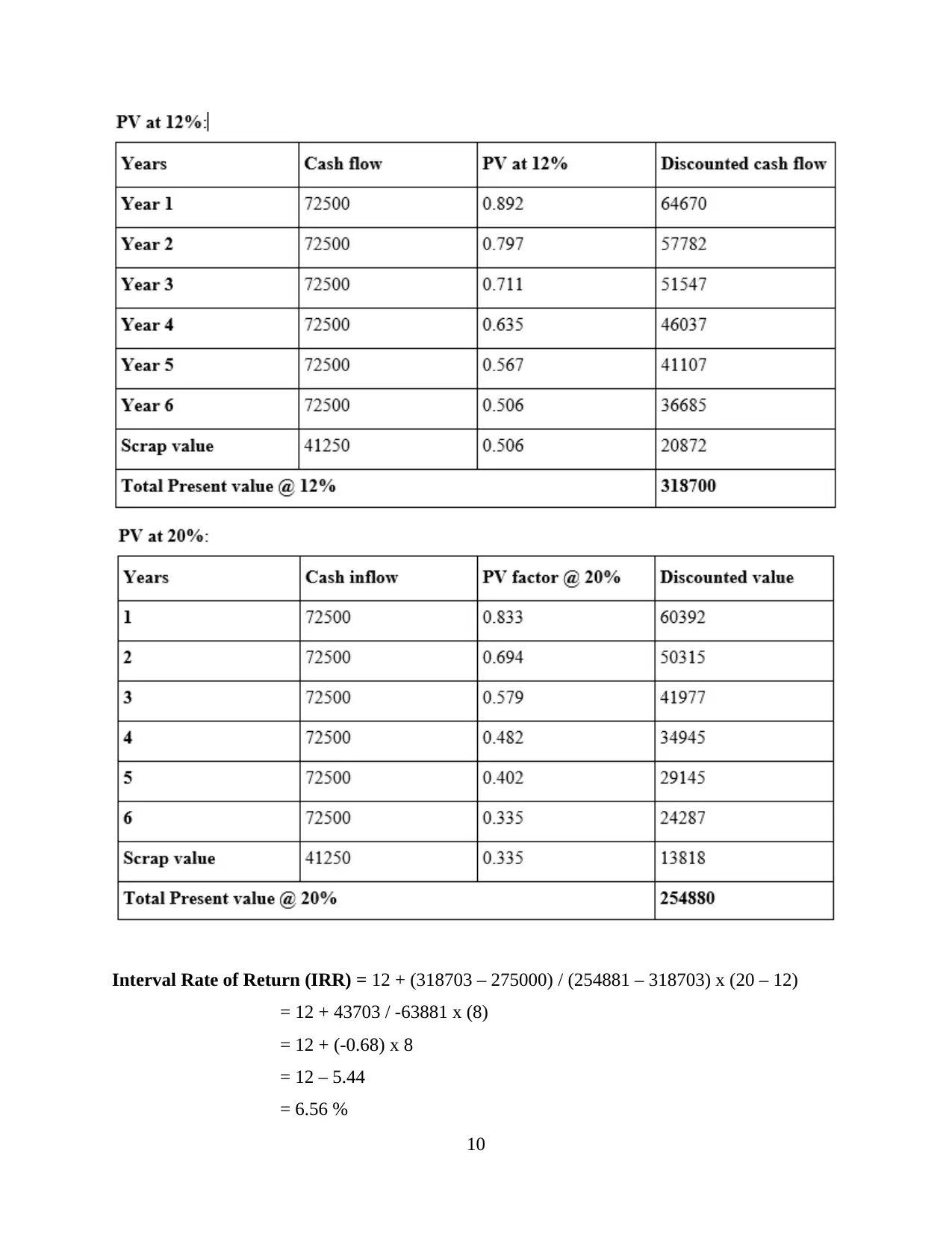

This report delves into key aspects of financial management, addressing long-term finance and investment appraisal techniques. It begins with an analysis of right share issues, including calculations of the number of shares to be issued, theoretical ex-right price, anticipated earnings per share, and the evaluation of different right issue price options. The report also examines the benefits of scrip dividends for both companies and shareholders. Furthermore, it applies and evaluates various investment appraisal techniques, such as the payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR), to assess the efficiency of a project. The report provides detailed calculations and recommendations based on these techniques, followed by a critical evaluation of the benefits and drawbacks of each investment appraisal method. This report provides a comprehensive overview of financial management concepts and their practical application in business decision-making.

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.