APC308 Financial Management: Investment Appraisal and Valuation

VerifiedAdded on 2023/06/18

|15

|3812

|423

Report

AI Summary

This report provides a comprehensive analysis of investment appraisal techniques, including payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR), for Super Tasty Soup (STS) Limited. It evaluates the economic feasibility of investment proposals and discusses the impact of financial decisions, such as equity repurchase and dividend distribution. The report also examines the benefits and limitations of each investment appraisal technique. Furthermore, it delves into business valuation methods like the price-earnings ratio (PER) and discounted cash flow (DCF) for Dragon plc, highlighting their associated problems and suggesting the most suitable option for Kings plc. The analysis aims to provide insights into effective financial management and strategic decision-making.

INVESTMENT APPRAISAL

TECHNIQUES

TECHNIQUES

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENT

INTRODUCTION...........................................................................................................................3

QUESTION 2..................................................................................................................................3

(a) Recommendation to economic feasibility..............................................................................3

(b) Discussing the effect of proposal on Super Tasty Limited....................................................7

(c) Evaluation of benefits and limitations of investment appraisal techniques...........................8

QUESTION- 3...............................................................................................................................10

a) Valuation through the price earning ratio method.................................................................10

b) Valuation of Dragon plc by the discounted cash flow method.............................................11

c) Dividend valuation method for assessing the value of Dragon plc.......................................12

d) Problems associated with the valuation techniques and the most suitable option for Kings

plc..............................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

QUESTION 2..................................................................................................................................3

(a) Recommendation to economic feasibility..............................................................................3

(b) Discussing the effect of proposal on Super Tasty Limited....................................................7

(c) Evaluation of benefits and limitations of investment appraisal techniques...........................8

QUESTION- 3...............................................................................................................................10

a) Valuation through the price earning ratio method.................................................................10

b) Valuation of Dragon plc by the discounted cash flow method.............................................11

c) Dividend valuation method for assessing the value of Dragon plc.......................................12

d) Problems associated with the valuation techniques and the most suitable option for Kings

plc..............................................................................................................................................13

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION

Financial management is all about implementing the processes and procedures in place

which assists in effectively handling and managing the financial resources of the company. In

this report, an analysis of the various investment appraisal techniques is being carried out which

helps in determining the feasibility of the investment proposal for the purpose of investment. In

addition to this, a critical discussion of the various business valuation methods is being done

which helps in determining the pros and cons of each of the method and selecting the right one.

QUESTION 2

(a) Recommendation to economic feasibility

For Super Tasty Soup (STS) Limited which is a fast food organization following are the

recommendation it its investment appraisals techniques for improving the economic feasibility.

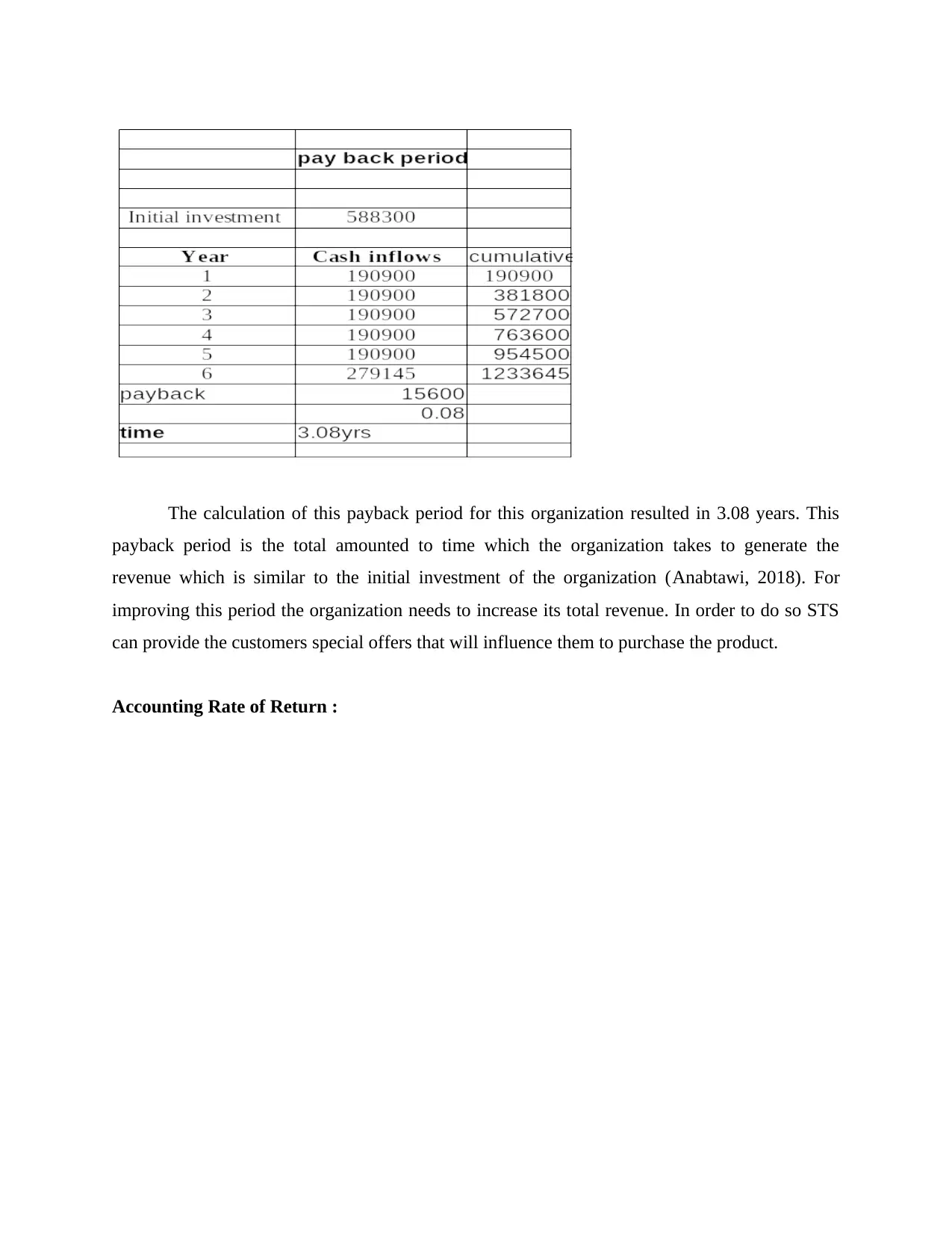

Payback period :

Financial management is all about implementing the processes and procedures in place

which assists in effectively handling and managing the financial resources of the company. In

this report, an analysis of the various investment appraisal techniques is being carried out which

helps in determining the feasibility of the investment proposal for the purpose of investment. In

addition to this, a critical discussion of the various business valuation methods is being done

which helps in determining the pros and cons of each of the method and selecting the right one.

QUESTION 2

(a) Recommendation to economic feasibility

For Super Tasty Soup (STS) Limited which is a fast food organization following are the

recommendation it its investment appraisals techniques for improving the economic feasibility.

Payback period :

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The calculation of this payback period for this organization resulted in 3.08 years. This

payback period is the total amounted to time which the organization takes to generate the

revenue which is similar to the initial investment of the organization (Anabtawi, 2018). For

improving this period the organization needs to increase its total revenue. In order to do so STS

can provide the customers special offers that will influence them to purchase the product.

Accounting Rate of Return :

payback period is the total amounted to time which the organization takes to generate the

revenue which is similar to the initial investment of the organization (Anabtawi, 2018). For

improving this period the organization needs to increase its total revenue. In order to do so STS

can provide the customers special offers that will influence them to purchase the product.

Accounting Rate of Return :

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

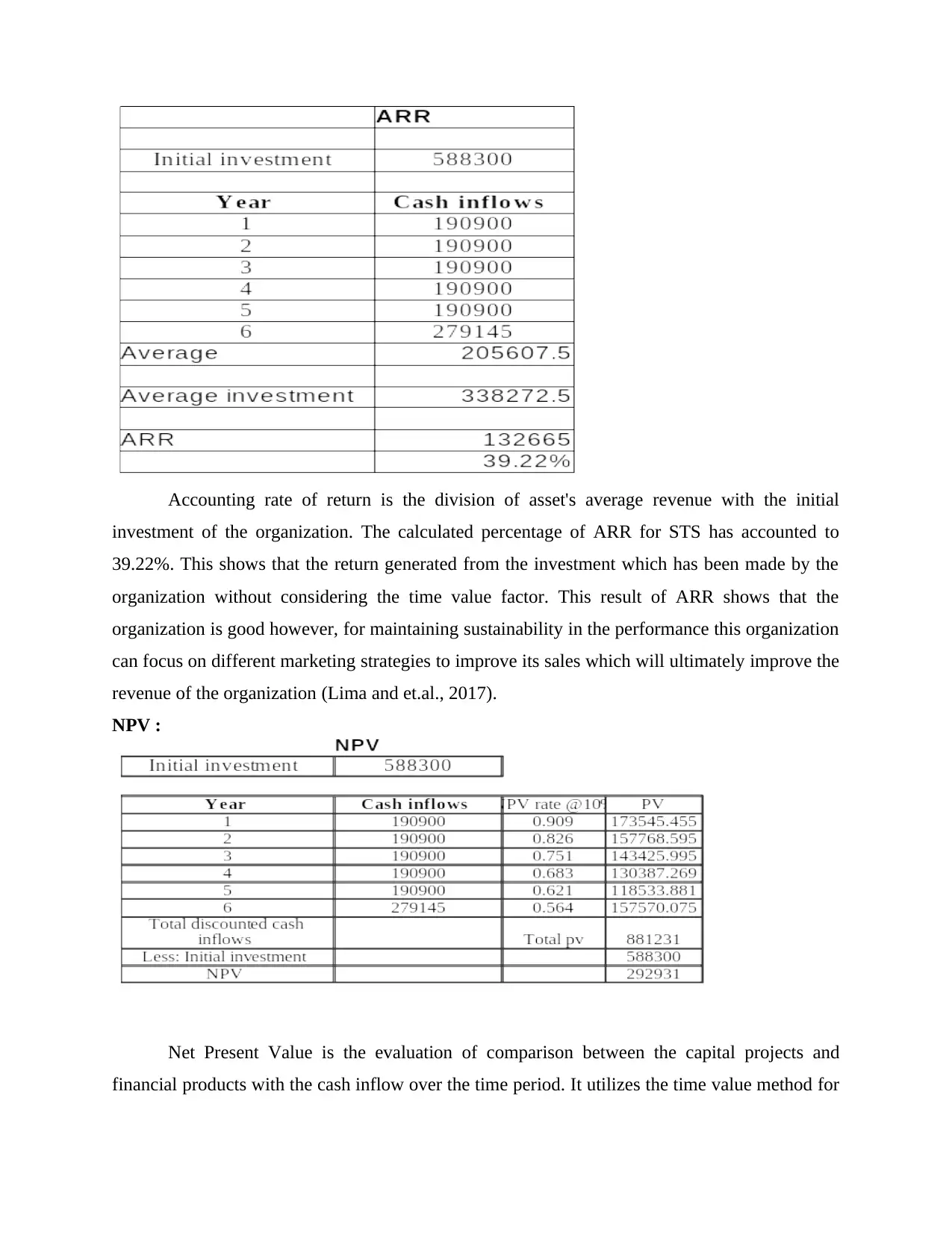

Accounting rate of return is the division of asset's average revenue with the initial

investment of the organization. The calculated percentage of ARR for STS has accounted to

39.22%. This shows that the return generated from the investment which has been made by the

organization without considering the time value factor. This result of ARR shows that the

organization is good however, for maintaining sustainability in the performance this organization

can focus on different marketing strategies to improve its sales which will ultimately improve the

revenue of the organization (Lima and et.al., 2017).

NPV :

Net Present Value is the evaluation of comparison between the capital projects and

financial products with the cash inflow over the time period. It utilizes the time value method for

investment of the organization. The calculated percentage of ARR for STS has accounted to

39.22%. This shows that the return generated from the investment which has been made by the

organization without considering the time value factor. This result of ARR shows that the

organization is good however, for maintaining sustainability in the performance this organization

can focus on different marketing strategies to improve its sales which will ultimately improve the

revenue of the organization (Lima and et.al., 2017).

NPV :

Net Present Value is the evaluation of comparison between the capital projects and

financial products with the cash inflow over the time period. It utilizes the time value method for

the calculation of the present value of the asset to better understand the return which it has

generated. In this calculation the NPV has been calculated as 292931. That shows the present

value of the machinery purchased 6 years ago that includes the scrap value of that machinery.

Due to this method considering the time value of money it is also successful in explaining the

actual profit or loss which the business has suffered. With the help of this evaluation it can be

concluded that, this organization needs to increase its total income by reducing the expenditure

and increasing the total revenue. This can be done by increasing the efficiency of its resources so

that with the same effort more revenue can be generated.

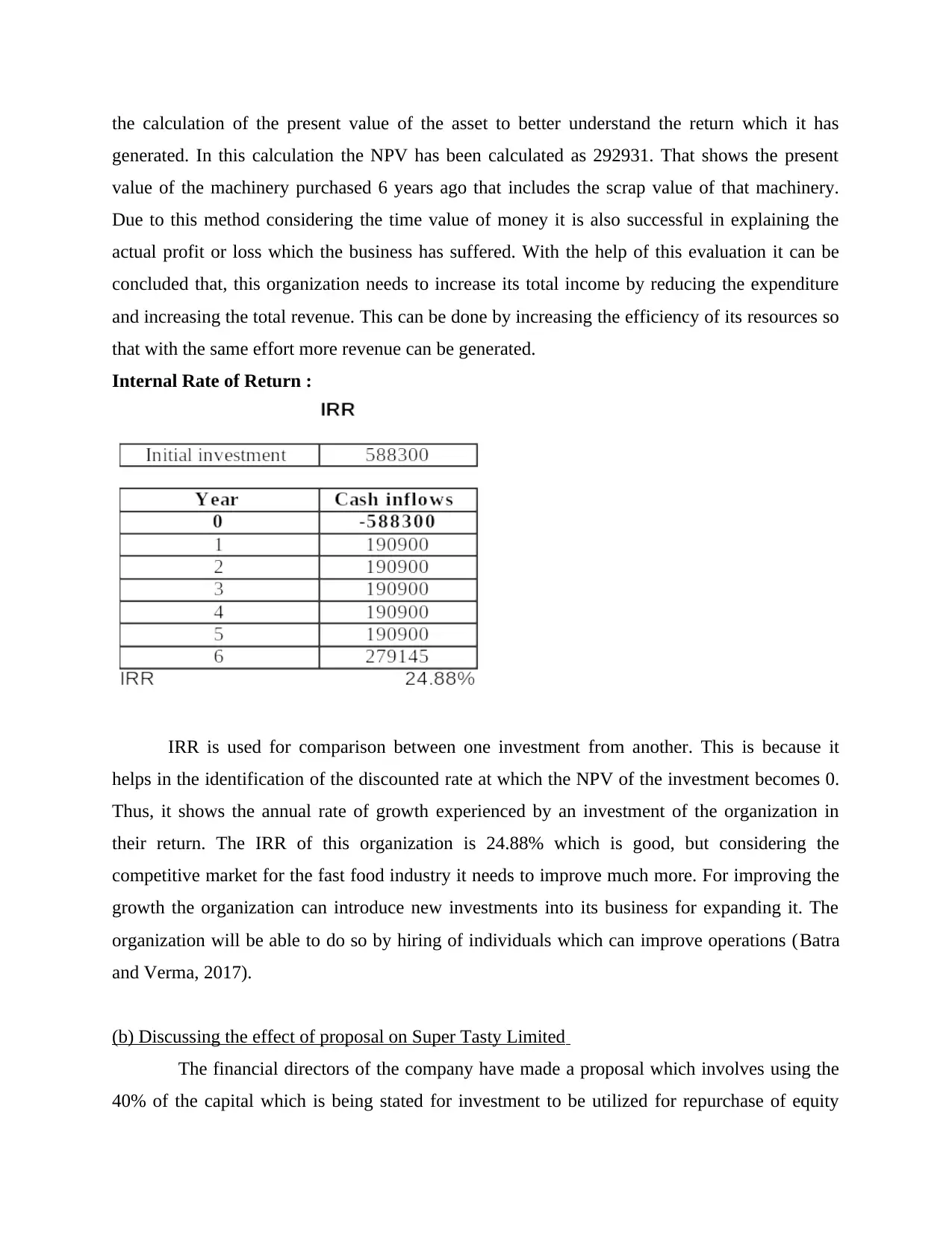

Internal Rate of Return :

IRR is used for comparison between one investment from another. This is because it

helps in the identification of the discounted rate at which the NPV of the investment becomes 0.

Thus, it shows the annual rate of growth experienced by an investment of the organization in

their return. The IRR of this organization is 24.88% which is good, but considering the

competitive market for the fast food industry it needs to improve much more. For improving the

growth the organization can introduce new investments into its business for expanding it. The

organization will be able to do so by hiring of individuals which can improve operations (Batra

and Verma, 2017).

(b) Discussing the effect of proposal on Super Tasty Limited

The financial directors of the company have made a proposal which involves using the

40% of the capital which is being stated for investment to be utilized for repurchase of equity

generated. In this calculation the NPV has been calculated as 292931. That shows the present

value of the machinery purchased 6 years ago that includes the scrap value of that machinery.

Due to this method considering the time value of money it is also successful in explaining the

actual profit or loss which the business has suffered. With the help of this evaluation it can be

concluded that, this organization needs to increase its total income by reducing the expenditure

and increasing the total revenue. This can be done by increasing the efficiency of its resources so

that with the same effort more revenue can be generated.

Internal Rate of Return :

IRR is used for comparison between one investment from another. This is because it

helps in the identification of the discounted rate at which the NPV of the investment becomes 0.

Thus, it shows the annual rate of growth experienced by an investment of the organization in

their return. The IRR of this organization is 24.88% which is good, but considering the

competitive market for the fast food industry it needs to improve much more. For improving the

growth the organization can introduce new investments into its business for expanding it. The

organization will be able to do so by hiring of individuals which can improve operations (Batra

and Verma, 2017).

(b) Discussing the effect of proposal on Super Tasty Limited

The financial directors of the company have made a proposal which involves using the

40% of the capital which is being stated for investment to be utilized for repurchase of equity

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

while the remaining funds for the purpose of paying of dividend. The main objective behind this

proposal is to make the business procedures effective. Organization get counsel from the

financial director of the company for accomplishing the business goals in useful way by

considering all the significant variables. Capitalization structure ought to be planned by

organization in such a way that it can satisfy its internal along with external monetary

necessities. The utilization of 40% of 588300 which is 235320 for the purpose of repurchasing

equity and spending 60% in respect to distributing it as dividends to the shareholders.

The principle objective of the company is to boost productivity alongside investors

abundance so better standing can be acquired in market. The rise in the satisfaction of the

shareholders results into enhancing the establishments' extent of development within industry

and empowers it to gain upper hands. Other reason behind doing this is that the company would

not be required to deliver profit on the value shares it repurchased which will help it in holding

more from the profits which can be additionally used in the further growth and development

projects of the firm (When Does It Benefit a Company to Buy Back Outstanding Shares? 2021).

Additionally, it will result into making it simple for the organization in delivering profit to its

financial investors in an effective manner or at higher rate which will develop great and positive

picture before them. This is the main factor which may make this proposition adequate as it is

useful for the organization. Subsequently, this progression results into acquiring different

advantages to the business which can't be abstained from prompting, leading it to making a

satisfactory and feasible deal. In other words, this proposition will prompt adequately dealing

with the income of the business as the organization will as of now not needed to distribute profit

as dividend on certain number of its equity shares.

The appropriate segregation of capital equity shares and retained earnings for giving

profits along with carrying out the business tasks to a great extent by way of making use of the

retained earnings. There are a few elements which drives business to acknowledge and accept the

given proposal or proposition which is relied upon the monetary situation of association that it

will be profited or not. The upsides of keeping 40% equity capital is that there will be no

reimbursement prerequisites, lower risk, and so forth. STP would have the option to draw in

more financial investors by offering them reliability and trust that the organization is taking care

of the shareholder’s growth in addition to the company’s development. Usefulness and

proposal is to make the business procedures effective. Organization get counsel from the

financial director of the company for accomplishing the business goals in useful way by

considering all the significant variables. Capitalization structure ought to be planned by

organization in such a way that it can satisfy its internal along with external monetary

necessities. The utilization of 40% of 588300 which is 235320 for the purpose of repurchasing

equity and spending 60% in respect to distributing it as dividends to the shareholders.

The principle objective of the company is to boost productivity alongside investors

abundance so better standing can be acquired in market. The rise in the satisfaction of the

shareholders results into enhancing the establishments' extent of development within industry

and empowers it to gain upper hands. Other reason behind doing this is that the company would

not be required to deliver profit on the value shares it repurchased which will help it in holding

more from the profits which can be additionally used in the further growth and development

projects of the firm (When Does It Benefit a Company to Buy Back Outstanding Shares? 2021).

Additionally, it will result into making it simple for the organization in delivering profit to its

financial investors in an effective manner or at higher rate which will develop great and positive

picture before them. This is the main factor which may make this proposition adequate as it is

useful for the organization. Subsequently, this progression results into acquiring different

advantages to the business which can't be abstained from prompting, leading it to making a

satisfactory and feasible deal. In other words, this proposition will prompt adequately dealing

with the income of the business as the organization will as of now not needed to distribute profit

as dividend on certain number of its equity shares.

The appropriate segregation of capital equity shares and retained earnings for giving

profits along with carrying out the business tasks to a great extent by way of making use of the

retained earnings. There are a few elements which drives business to acknowledge and accept the

given proposal or proposition which is relied upon the monetary situation of association that it

will be profited or not. The upsides of keeping 40% equity capital is that there will be no

reimbursement prerequisites, lower risk, and so forth. STP would have the option to draw in

more financial investors by offering them reliability and trust that the organization is taking care

of the shareholder’s growth in addition to the company’s development. Usefulness and

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

productivity of STP will be expanded by accepting and going forward with the proposed

proposal.

(c) Evaluation of benefits and limitations of investment appraisal techniques

The investment appraisal techniques are used for the organization overall strategy and

decision of capital investment. They have their own benefits and drawbacks.

Payback period

Benefits :

Its only useful in the certain situations like, rapid changes in technology and trying to

improve investment conditions.

The calculation of the payback period is made for the analysation of quick return on

investment.

It helps in understanding the growth of the company, minimization of the risk and

maximization of the liquidity.

Another benefit of this is that it utilizes the cash flow for its calculation which makes the

calculation very simple.

Limitations :

Its calculation ignores the return after the payback period. Due to which it gets limited to

the years which are mention in the calculation.

It also ignores the timing of the cash flow, for the calculation of which the discounted

payback periods is used.

It is very subjective as it does not provide any specific result to what needs to be done.

This method does explain what the ideal payback period should be. The calculation of this ignores the profitability of the project. Profitability is the most

important factor for the organization due to which it becomes very essential to be

considered (Tijjani, 2019).

Accounting Rate of Return :

Benefits :

The accounting rate of return is very easy to calculate as it involves division of asset's

average revenue with the initial investment of the organization. This makes it also very

easy to understand.

It shows relations with the profit which is shown in the accounts annually.

proposal.

(c) Evaluation of benefits and limitations of investment appraisal techniques

The investment appraisal techniques are used for the organization overall strategy and

decision of capital investment. They have their own benefits and drawbacks.

Payback period

Benefits :

Its only useful in the certain situations like, rapid changes in technology and trying to

improve investment conditions.

The calculation of the payback period is made for the analysation of quick return on

investment.

It helps in understanding the growth of the company, minimization of the risk and

maximization of the liquidity.

Another benefit of this is that it utilizes the cash flow for its calculation which makes the

calculation very simple.

Limitations :

Its calculation ignores the return after the payback period. Due to which it gets limited to

the years which are mention in the calculation.

It also ignores the timing of the cash flow, for the calculation of which the discounted

payback periods is used.

It is very subjective as it does not provide any specific result to what needs to be done.

This method does explain what the ideal payback period should be. The calculation of this ignores the profitability of the project. Profitability is the most

important factor for the organization due to which it becomes very essential to be

considered (Tijjani, 2019).

Accounting Rate of Return :

Benefits :

The accounting rate of return is very easy to calculate as it involves division of asset's

average revenue with the initial investment of the organization. This makes it also very

easy to understand.

It shows relations with the profit which is shown in the accounts annually.

It considers the entire life of the investment project and the profit earned.

Due to its simplicity it is very popular among some business organization for their

evaluation.

Limitations :

One of its biggest limitations is that it ignores the time value of money which is important

for understanding the actual return.

As it utilizes the average of the return it ignores the timing of the profits.

For the calculation of profit the another method is needed to be used after this, called

depreciation. There are different methods by which ARR can be calculated, nothing is fixed.

Net Present Value :

Benefits :

One of the primary benefit is that it considers the time value of money, which is

important because the value of money changes with time.

It is very essential for the decision-making process of the organization.

It explains the investors to understand whether the particular investment will make profit

or loss (Thakur and Vaidya, 2021).

Limitations :

For the calculation of the required rate of return there is no given calculation. People use

different method for its calculation. Due to this the rate of returns have different figures.

It is limited as it use can be only made with projects with similar sizes. Project with high

difference in size is a limit to its calculation. It fails in consideration of the hidden cost which are not the part of the calculation.

Internal rate of return :

Benefits :

This value does recognize the time value of money. Due to which it considered more

reliable.

It takes account of the cash flows for the whole life of the investment.

It is used for comparison of different alternative users which can potentially make easy

money.

Due to its simplicity it is very popular among some business organization for their

evaluation.

Limitations :

One of its biggest limitations is that it ignores the time value of money which is important

for understanding the actual return.

As it utilizes the average of the return it ignores the timing of the profits.

For the calculation of profit the another method is needed to be used after this, called

depreciation. There are different methods by which ARR can be calculated, nothing is fixed.

Net Present Value :

Benefits :

One of the primary benefit is that it considers the time value of money, which is

important because the value of money changes with time.

It is very essential for the decision-making process of the organization.

It explains the investors to understand whether the particular investment will make profit

or loss (Thakur and Vaidya, 2021).

Limitations :

For the calculation of the required rate of return there is no given calculation. People use

different method for its calculation. Due to this the rate of returns have different figures.

It is limited as it use can be only made with projects with similar sizes. Project with high

difference in size is a limit to its calculation. It fails in consideration of the hidden cost which are not the part of the calculation.

Internal rate of return :

Benefits :

This value does recognize the time value of money. Due to which it considered more

reliable.

It takes account of the cash flows for the whole life of the investment.

It is used for comparison of different alternative users which can potentially make easy

money.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Limitations :

It is a little difficult concept for the people to understand.

It is very dependent over ascertaining the correct cost of capital concept.

It has been noticed that the interest some times adversely changes.

QUESTION- 3

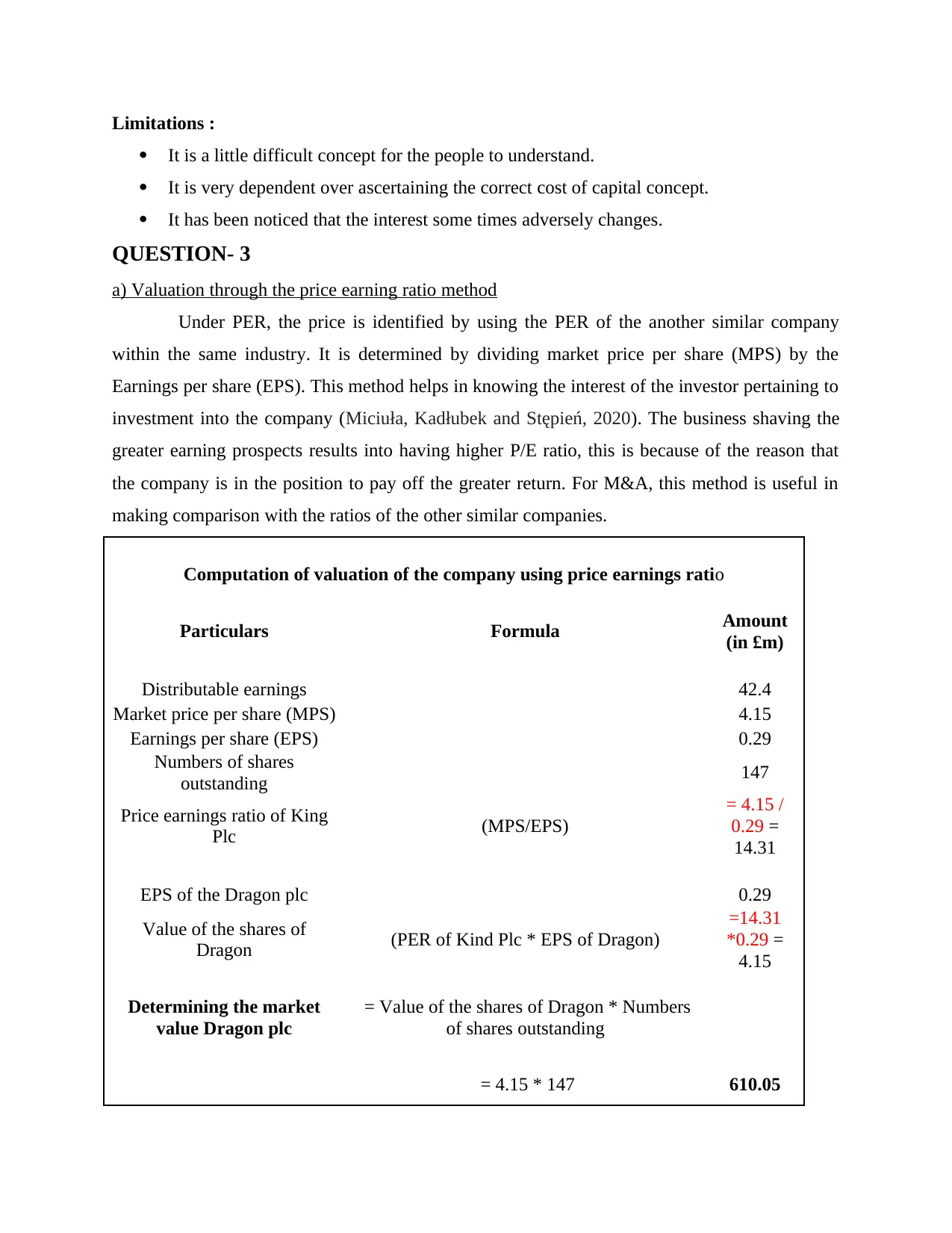

a) Valuation through the price earning ratio method

Under PER, the price is identified by using the PER of the another similar company

within the same industry. It is determined by dividing market price per share (MPS) by the

Earnings per share (EPS). This method helps in knowing the interest of the investor pertaining to

investment into the company (Miciuła, Kadłubek and Stępień, 2020). The business shaving the

greater earning prospects results into having higher P/E ratio, this is because of the reason that

the company is in the position to pay off the greater return. For M&A, this method is useful in

making comparison with the ratios of the other similar companies.

Computation of valuation of the company using price earnings ratio

Particulars Formula Amount

(in £m)

Distributable earnings 42.4

Market price per share (MPS) 4.15

Earnings per share (EPS) 0.29

Numbers of shares

outstanding 147

Price earnings ratio of King

Plc (MPS/EPS)

= 4.15 /

0.29 =

14.31

EPS of the Dragon plc 0.29

Value of the shares of

Dragon (PER of Kind Plc * EPS of Dragon)

=14.31

*0.29 =

4.15

Determining the market

value Dragon plc

= Value of the shares of Dragon * Numbers

of shares outstanding

= 4.15 * 147 610.05

It is a little difficult concept for the people to understand.

It is very dependent over ascertaining the correct cost of capital concept.

It has been noticed that the interest some times adversely changes.

QUESTION- 3

a) Valuation through the price earning ratio method

Under PER, the price is identified by using the PER of the another similar company

within the same industry. It is determined by dividing market price per share (MPS) by the

Earnings per share (EPS). This method helps in knowing the interest of the investor pertaining to

investment into the company (Miciuła, Kadłubek and Stępień, 2020). The business shaving the

greater earning prospects results into having higher P/E ratio, this is because of the reason that

the company is in the position to pay off the greater return. For M&A, this method is useful in

making comparison with the ratios of the other similar companies.

Computation of valuation of the company using price earnings ratio

Particulars Formula Amount

(in £m)

Distributable earnings 42.4

Market price per share (MPS) 4.15

Earnings per share (EPS) 0.29

Numbers of shares

outstanding 147

Price earnings ratio of King

Plc (MPS/EPS)

= 4.15 /

0.29 =

14.31

EPS of the Dragon plc 0.29

Value of the shares of

Dragon (PER of Kind Plc * EPS of Dragon)

=14.31

*0.29 =

4.15

Determining the market

value Dragon plc

= Value of the shares of Dragon * Numbers

of shares outstanding

= 4.15 * 147 610.05

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

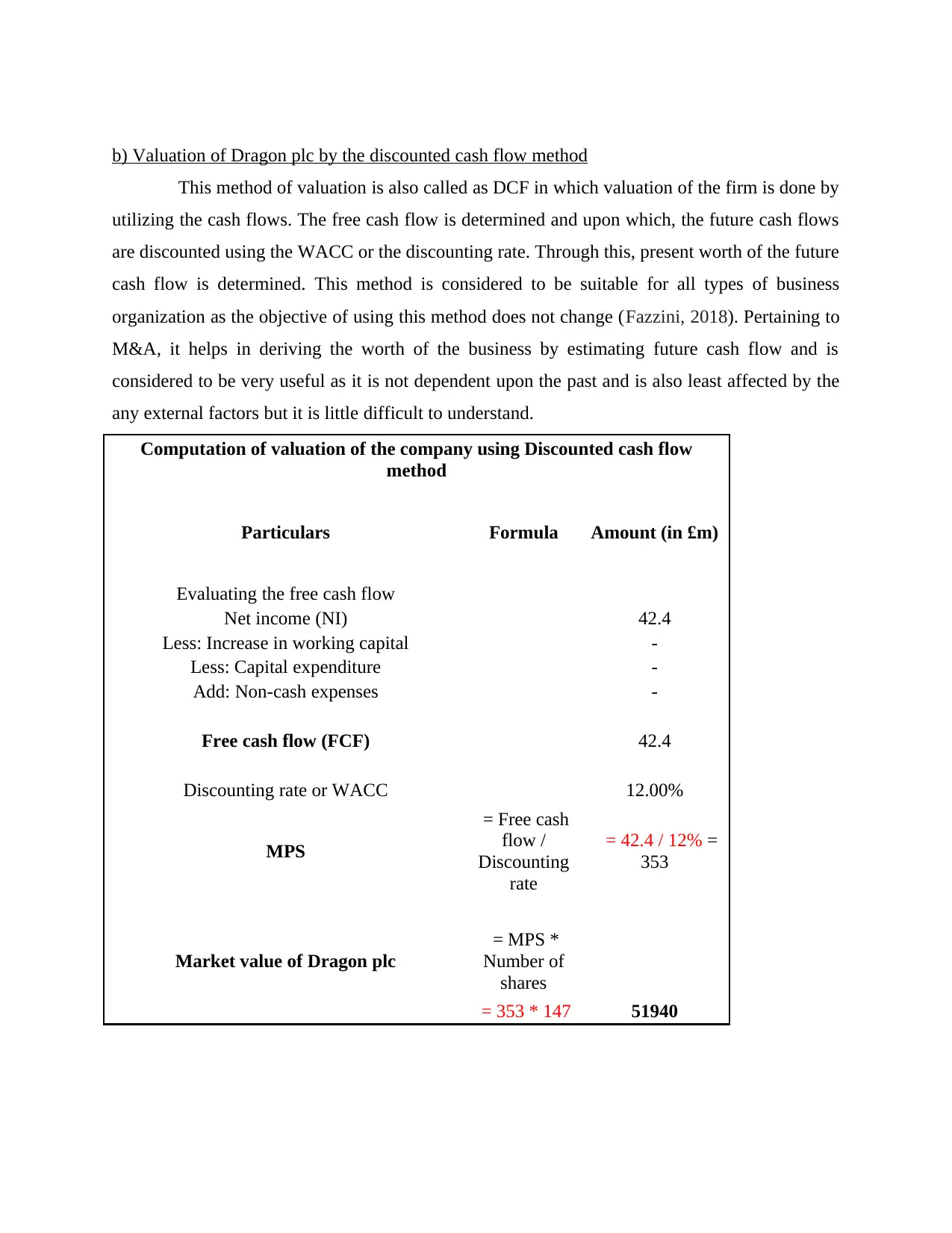

b) Valuation of Dragon plc by the discounted cash flow method

This method of valuation is also called as DCF in which valuation of the firm is done by

utilizing the cash flows. The free cash flow is determined and upon which, the future cash flows

are discounted using the WACC or the discounting rate. Through this, present worth of the future

cash flow is determined. This method is considered to be suitable for all types of business

organization as the objective of using this method does not change (Fazzini, 2018). Pertaining to

M&A, it helps in deriving the worth of the business by estimating future cash flow and is

considered to be very useful as it is not dependent upon the past and is also least affected by the

any external factors but it is little difficult to understand.

Computation of valuation of the company using Discounted cash flow

method

Particulars Formula Amount (in £m)

Evaluating the free cash flow

Net income (NI) 42.4

Less: Increase in working capital -

Less: Capital expenditure -

Add: Non-cash expenses -

Free cash flow (FCF) 42.4

Discounting rate or WACC 12.00%

MPS

= Free cash

flow /

Discounting

rate

= 42.4 / 12% =

353

Market value of Dragon plc

= MPS *

Number of

shares

= 353 * 147 51940

This method of valuation is also called as DCF in which valuation of the firm is done by

utilizing the cash flows. The free cash flow is determined and upon which, the future cash flows

are discounted using the WACC or the discounting rate. Through this, present worth of the future

cash flow is determined. This method is considered to be suitable for all types of business

organization as the objective of using this method does not change (Fazzini, 2018). Pertaining to

M&A, it helps in deriving the worth of the business by estimating future cash flow and is

considered to be very useful as it is not dependent upon the past and is also least affected by the

any external factors but it is little difficult to understand.

Computation of valuation of the company using Discounted cash flow

method

Particulars Formula Amount (in £m)

Evaluating the free cash flow

Net income (NI) 42.4

Less: Increase in working capital -

Less: Capital expenditure -

Add: Non-cash expenses -

Free cash flow (FCF) 42.4

Discounting rate or WACC 12.00%

MPS

= Free cash

flow /

Discounting

rate

= 42.4 / 12% =

353

Market value of Dragon plc

= MPS *

Number of

shares

= 353 * 147 51940

c) Dividend valuation method for assessing the value of Dragon plc

This method of valuation is based upon the assumption that the dividend will grow at

the constant rate. This method is considered right for those businesses where dividend payment

tends to rise at the fixed percentage annually. This approach is very easy to understand and to be

used in the organization which already has dividend pay-out ratios (Allee and et.al., 2020).

Through this model, comparison can also be drawn with other companies. This model requires

the usage of current profit which is paid as dividend, expected rate f return in addition to the

growth rate. There are few assumptions like steady growth rate, no internal or external factors is

accounted for and the free cash flow is given as dividend.

Dividend growth rate= Current year dividend – last year dividend / last year dividend *

100

Dividend growth rate= 0.14 – 0.12 / 0.12 * 100

Dividend growth rate= 0.02 / 0.12 * 100

Dividend growth rate= 16.67%

Year 1: The value of investments in the year 1 are:-

Current dividend / Expected rate of return on investments

= 0.14 / 1.12

= 0.125

Year 2: The value of investments in the year 2 are:-

Current dividend adjusted after growth rate / Expected rate of return ^ 2

= 0.16 / (1.12)^2

= 0.127

Constant growth rate: Constant growth value of a share of stock

= 0.16 / (0.12 – 0.167)

= -3.4

Value of share of Dragon plc

= 0.125 + 0.127 + -3.4

= -3.148

d) Problems associated with the valuation techniques and the most suitable option for Kings plc

There are several valuation techniques that can be applied by the company for

undertaking the business valuation so that the resultants can be used in the assessment of the

This method of valuation is based upon the assumption that the dividend will grow at

the constant rate. This method is considered right for those businesses where dividend payment

tends to rise at the fixed percentage annually. This approach is very easy to understand and to be

used in the organization which already has dividend pay-out ratios (Allee and et.al., 2020).

Through this model, comparison can also be drawn with other companies. This model requires

the usage of current profit which is paid as dividend, expected rate f return in addition to the

growth rate. There are few assumptions like steady growth rate, no internal or external factors is

accounted for and the free cash flow is given as dividend.

Dividend growth rate= Current year dividend – last year dividend / last year dividend *

100

Dividend growth rate= 0.14 – 0.12 / 0.12 * 100

Dividend growth rate= 0.02 / 0.12 * 100

Dividend growth rate= 16.67%

Year 1: The value of investments in the year 1 are:-

Current dividend / Expected rate of return on investments

= 0.14 / 1.12

= 0.125

Year 2: The value of investments in the year 2 are:-

Current dividend adjusted after growth rate / Expected rate of return ^ 2

= 0.16 / (1.12)^2

= 0.127

Constant growth rate: Constant growth value of a share of stock

= 0.16 / (0.12 – 0.167)

= -3.4

Value of share of Dragon plc

= 0.125 + 0.127 + -3.4

= -3.148

d) Problems associated with the valuation techniques and the most suitable option for Kings plc

There are several valuation techniques that can be applied by the company for

undertaking the business valuation so that the resultants can be used in the assessment of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.