Financial Management Assessment Week 2: Short Answer Responses

VerifiedAdded on 2020/06/04

|27

|7414

|76

Homework Assignment

AI Summary

This document presents a completed finance assignment, addressing key concepts in financial management. The assignment covers a range of topics, including an analysis of a profitable business, reasons for potential business failures, and explanations of fundamental accounting concepts such as the business entity concept, dual aspect concept, money measurement concept, objectivity concept, going concern concept, periodicity concept, cost concept, conservatism concept, materiality concept, realisation concept, matching concept, and full disclosure concept. Additionally, the assignment provides examples of investment and financing decisions. The student's responses demonstrate an understanding of financial principles and their application in various business contexts. The assignment is a valuable resource for students studying finance and accounting, and Desklib provides additional resources for academic success.

Student Name: Student ID:

Assessment Type: Project Other:

Assessor’s Name:

Assessment

Outcome:

☐ Satisfactory ☐ Not Yet Satisfactory

Student

Declaration:

By submitting this assessment via Moodle, I declare that this is my own work and had

not been copied or plagiarised from any other source. Please refer to the Student

Handbook for more information.

Assessment

Conditions:

Each assessment criteria is recorded as either Satisfactory (S) or Not Yet Satisfactory

(NYS). A student can only achieve a ‘Satisfactory’ Assessment Outcome for the entire

assessment when all assessment Criteria listed below are ‘Satisfactory’. A student who

is assessed as ‘Not Yet Satisfactory’ is eligible for re-assessment with their trainer.

All assessment answers must be typed, include this assessment cover sheet and

uploaded in ‘WORD’ version to module.

Assessment Criteria

Element Performance Criteria S

Develop and use emotional intelligence

1 Plan for financial

management 1.1 Review and analyse previous financial data to

establish areas which have generated a profit or loss

☐

1.2 Undertake research to review reasons for previous

profit and loss

☐

1.3 Review business plan to establish critical dates

and initiatives that will require or generate resources

in the next financial cycle

☐

1.4 Analyse cash flow trends

1.5 Review statutory requirements for compliance and

liabilities for tax

☐

1.6 Review existing software and its suitability for

financial management

☐

Assessment Type: Project Other:

Assessor’s Name:

Assessment

Outcome:

☐ Satisfactory ☐ Not Yet Satisfactory

Student

Declaration:

By submitting this assessment via Moodle, I declare that this is my own work and had

not been copied or plagiarised from any other source. Please refer to the Student

Handbook for more information.

Assessment

Conditions:

Each assessment criteria is recorded as either Satisfactory (S) or Not Yet Satisfactory

(NYS). A student can only achieve a ‘Satisfactory’ Assessment Outcome for the entire

assessment when all assessment Criteria listed below are ‘Satisfactory’. A student who

is assessed as ‘Not Yet Satisfactory’ is eligible for re-assessment with their trainer.

All assessment answers must be typed, include this assessment cover sheet and

uploaded in ‘WORD’ version to module.

Assessment Criteria

Element Performance Criteria S

Develop and use emotional intelligence

1 Plan for financial

management 1.1 Review and analyse previous financial data to

establish areas which have generated a profit or loss

☐

1.2 Undertake research to review reasons for previous

profit and loss

☐

1.3 Review business plan to establish critical dates

and initiatives that will require or generate resources

in the next financial cycle

☐

1.4 Analyse cash flow trends

1.5 Review statutory requirements for compliance and

liabilities for tax

☐

1.6 Review existing software and its suitability for

financial management

☐

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2 Establish budgets

and allocate

funds 2.1 Use previous financial data to determine

allocations for resources

☐

2.2 Make informed estimates of new items for

inclusion in budget

☐

2.3 Prepare budgets in accordance with organisational

requirements and statutory requirements

☐

3 Implement

budgets 3.1 Circulate budgets and ensure managers and

supervisors are clear about budgets, reporting

requirements and financial delegations

☐

3.2 Manage risks by checking there are no

opportunities for misappropriation of funds and that

systems are in place to properly record all financial

transactions

☐

3.3 Review profit and loss statements, cash flows and

ageing summaries

☐

3.4 Revise budgets, as required, to deal with

contingencies

3.5 Maintain audit trails to ensure accurate tracking

and to identify discrepancies between agreed and

actual allocations

3.6 Ensure compliance with due diligence

4 Report on

finances 4.1 Ensure structure and format of reports are clear

and conform to organisational and statutory

requirements

S

4.2 Identify and prioritise significant issues in

statements, including comparative financial

performances for review and decision making

and allocate

funds 2.1 Use previous financial data to determine

allocations for resources

☐

2.2 Make informed estimates of new items for

inclusion in budget

☐

2.3 Prepare budgets in accordance with organisational

requirements and statutory requirements

☐

3 Implement

budgets 3.1 Circulate budgets and ensure managers and

supervisors are clear about budgets, reporting

requirements and financial delegations

☐

3.2 Manage risks by checking there are no

opportunities for misappropriation of funds and that

systems are in place to properly record all financial

transactions

☐

3.3 Review profit and loss statements, cash flows and

ageing summaries

☐

3.4 Revise budgets, as required, to deal with

contingencies

3.5 Maintain audit trails to ensure accurate tracking

and to identify discrepancies between agreed and

actual allocations

3.6 Ensure compliance with due diligence

4 Report on

finances 4.1 Ensure structure and format of reports are clear

and conform to organisational and statutory

requirements

S

4.2 Identify and prioritise significant issues in

statements, including comparative financial

performances for review and decision making

4.3 Prepare recommendations to ensure financial

viability of the organisation

☐

4.4 Evaluate the effectiveness of financial

management processes

☐

☐

☐

☐

FINANCIAL MANAGEMENT: ASSESSMENT

WEEK 2 (20 marks)

ASSESSMENT ACTIVITY: SHORT ANSWER RESPONSES

1. Describe at least one (1) business that is profitable and explain why you think it is enjoying

financial success.

NAB (National Australian Banking): it is one of the successful banking and financial industry in

Australia.

viability of the organisation

☐

4.4 Evaluate the effectiveness of financial

management processes

☐

☐

☐

☐

FINANCIAL MANAGEMENT: ASSESSMENT

WEEK 2 (20 marks)

ASSESSMENT ACTIVITY: SHORT ANSWER RESPONSES

1. Describe at least one (1) business that is profitable and explain why you think it is enjoying

financial success.

NAB (National Australian Banking): it is one of the successful banking and financial industry in

Australia.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

It is 41st largest bank in the world operating financial and banking sector across the world.

It has a large capital structure which is helpful to enhance the scope the of NAB across the globe.

It has a large revenue share too. In Australia it has 74%, in Europe it has 12% in New Zealand it

has 10% in USA 3% and in Asia it has 1%.

Capital Structure: Organisation is enjoying its financial success with its strong financial and capital

structure. It is seen that the company is capable to build its market share at optimum level.

Technology: NAB uses late test technology and advanced tools. The Siebel and Teradata CRM

(Customer Relation Management) system is one of the technology used by the organisation.

It has launched “NextGen” program also to deal the financial problems and challenges.

2. While the evidence suggests otherwise, there is a common view that many new businesses fail

within the first year of operation. Why do you think a new business might not succeed?

There are some reasons that new business get fail to attain profit at initial stage.

Lake of goodwill

Low capital structure

Low number of investors and financiers

3. Explain the following fundamental accounting concepts:

Business Entity Concept

Concept of business is considered as separate from the owner. It is considered as simple that there

must be septate accounts to be recorded from the owner.

It is also considered as separate entity concept and economic entity concept.

Final accounts of the business are prepared separate from the owner.

Dual Aspect Concept

Dual concept indicates towards the double entry accounting system.

It has a large capital structure which is helpful to enhance the scope the of NAB across the globe.

It has a large revenue share too. In Australia it has 74%, in Europe it has 12% in New Zealand it

has 10% in USA 3% and in Asia it has 1%.

Capital Structure: Organisation is enjoying its financial success with its strong financial and capital

structure. It is seen that the company is capable to build its market share at optimum level.

Technology: NAB uses late test technology and advanced tools. The Siebel and Teradata CRM

(Customer Relation Management) system is one of the technology used by the organisation.

It has launched “NextGen” program also to deal the financial problems and challenges.

2. While the evidence suggests otherwise, there is a common view that many new businesses fail

within the first year of operation. Why do you think a new business might not succeed?

There are some reasons that new business get fail to attain profit at initial stage.

Lake of goodwill

Low capital structure

Low number of investors and financiers

3. Explain the following fundamental accounting concepts:

Business Entity Concept

Concept of business is considered as separate from the owner. It is considered as simple that there

must be septate accounts to be recorded from the owner.

It is also considered as separate entity concept and economic entity concept.

Final accounts of the business are prepared separate from the owner.

Dual Aspect Concept

Dual concept indicates towards the double entry accounting system.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It is a fundamental convention of accounting which is considered as essential accounting principle.

As per this transaction a transaction effect both side of account such as debit side and credit side.

Money Measurement Concept

This concept tells that only those transactions must be recorded in the books which are measurable

in money.

There should be a separate accounting system adopted by the organisation subject to record non

monetary transactions and events.

4. Explain the following fundamental accounting concepts:

Objectivity Concept

As per this concept the financial statements of an organisation must be prepared on the basis of

relevant and accurate information.

Estimated and assumption based information and dare are avoided while preparing financial

accounts

Going Concern Concept

It is considered that the business and organisation is established in subject to operating regular

working.

Operations and functions are deemed to be consistent for long term perspective.

Periodicity Concept

This concept defines the time duration of recording the transactions in books.

Accounts period are considered as quarter, month and year.

This concept is also known as the time period assumption concept.

31st march, 31st June, 31st September and 31st December are considered in periodicity concept.

As per this transaction a transaction effect both side of account such as debit side and credit side.

Money Measurement Concept

This concept tells that only those transactions must be recorded in the books which are measurable

in money.

There should be a separate accounting system adopted by the organisation subject to record non

monetary transactions and events.

4. Explain the following fundamental accounting concepts:

Objectivity Concept

As per this concept the financial statements of an organisation must be prepared on the basis of

relevant and accurate information.

Estimated and assumption based information and dare are avoided while preparing financial

accounts

Going Concern Concept

It is considered that the business and organisation is established in subject to operating regular

working.

Operations and functions are deemed to be consistent for long term perspective.

Periodicity Concept

This concept defines the time duration of recording the transactions in books.

Accounts period are considered as quarter, month and year.

This concept is also known as the time period assumption concept.

31st march, 31st June, 31st September and 31st December are considered in periodicity concept.

5. Explain the following fundamental accounting concepts:

Cost Concept

This concept provides a path to record the assets and liabilities in books.

As per this concept the assets and liabilities must be recorded on their original cost.

Depreciation and deficiency must be deducted from the cost of the assets while recording the

transactions.

This concept is basically implemented on fixed assets.

Conservatism Concept

This concept is based upon actual scenario and assumptions.

As per this concept estimated and predicted cost should not be considered in profit and loss

accounts.

There must be a provision made for losses and expenses.

Materiality Concept

As per this concept the all the important figures and material information to be recorded in the

books of accounts.

Irrelevant and non material information and data are not considered in books and records while

preparing financial statements.

6. Explain the following fundamental accounting concepts:

Realisation Concept

Realisation concept is related to goods and services.

This concept tells that the amount should be recorded in books when the services and goods are

rendered or provided to customers.

It is also called as accrual basis accounting system.

Matching Concept

Cost Concept

This concept provides a path to record the assets and liabilities in books.

As per this concept the assets and liabilities must be recorded on their original cost.

Depreciation and deficiency must be deducted from the cost of the assets while recording the

transactions.

This concept is basically implemented on fixed assets.

Conservatism Concept

This concept is based upon actual scenario and assumptions.

As per this concept estimated and predicted cost should not be considered in profit and loss

accounts.

There must be a provision made for losses and expenses.

Materiality Concept

As per this concept the all the important figures and material information to be recorded in the

books of accounts.

Irrelevant and non material information and data are not considered in books and records while

preparing financial statements.

6. Explain the following fundamental accounting concepts:

Realisation Concept

Realisation concept is related to goods and services.

This concept tells that the amount should be recorded in books when the services and goods are

rendered or provided to customers.

It is also called as accrual basis accounting system.

Matching Concept

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

This accounting concept defines the relationship between revenues and expenditures.

It is also considered as matching concept which is depended upon expressive.

Non recognised expenses and incomes are not considered in accounting

Expenses and income of current financial years are only considered in books of accounting.

Full Disclosure Concept

This is one of the basic concept adopted by the organisation and business entities.

It indicates towards defining the accounting principles and accrual concepts related to business

and organisation. It is important to define the concept focused upon presenting the essential

information related to making financial statements and final accounts.

Earnings and expenditures are recorded on Monmouth, quarterly and annual basis.

7. Provide four (4) examples of investment decisions

Investment decisions indicate towards providing effective and optimum option for financial growth

and development.

Investment decisions helps to determine the best options for purchasing of productivity capacity

and capital expenditure.

Working capital investment: Working capital is known as current assets less current liabilities. It

states for compensating the short term liability with the liquid assets.

Investment made in inventories, cash, saving accounts and inveiglement made for enhancing

current assets are considered as working capital investment.

Financial Investments: these type of investment decisions are remain focused upon capital

investments, small business enterprises, capital markets.

It is considered as decision making in respect of capital investments, experts to trade.

Capital expenditure: There are some expenses considered as capital expenditure which

contributes profitability for further years. There are various type of investment done by the

organisation such as purchase of new plant and machinery, investment made for bonds and

investments.

Investment in new business: this is also one of the capital expenditure. Investment decision

remain associated to establish new business entity and organisation.

Replacement Investment: these are the type of investment which are intended to replace existing

investment.

Strategic investment decision: investment which are made in skills and expertise subject to

It is also considered as matching concept which is depended upon expressive.

Non recognised expenses and incomes are not considered in accounting

Expenses and income of current financial years are only considered in books of accounting.

Full Disclosure Concept

This is one of the basic concept adopted by the organisation and business entities.

It indicates towards defining the accounting principles and accrual concepts related to business

and organisation. It is important to define the concept focused upon presenting the essential

information related to making financial statements and final accounts.

Earnings and expenditures are recorded on Monmouth, quarterly and annual basis.

7. Provide four (4) examples of investment decisions

Investment decisions indicate towards providing effective and optimum option for financial growth

and development.

Investment decisions helps to determine the best options for purchasing of productivity capacity

and capital expenditure.

Working capital investment: Working capital is known as current assets less current liabilities. It

states for compensating the short term liability with the liquid assets.

Investment made in inventories, cash, saving accounts and inveiglement made for enhancing

current assets are considered as working capital investment.

Financial Investments: these type of investment decisions are remain focused upon capital

investments, small business enterprises, capital markets.

It is considered as decision making in respect of capital investments, experts to trade.

Capital expenditure: There are some expenses considered as capital expenditure which

contributes profitability for further years. There are various type of investment done by the

organisation such as purchase of new plant and machinery, investment made for bonds and

investments.

Investment in new business: this is also one of the capital expenditure. Investment decision

remain associated to establish new business entity and organisation.

Replacement Investment: these are the type of investment which are intended to replace existing

investment.

Strategic investment decision: investment which are made in skills and expertise subject to

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

achieve core competence are considered in these type of investment decision.

8. Provide five (5) examples of financing decisions

Short term financing: Decisions which are made to respond short term finance problems are

considered as short term financing. Bank overdraft, short term credits, borrowings are the type of

short term financial resources.

It helps managers to find out best and effective option to generate short term finance requirement.

Long term financing: Long term investments such as purchase of fixed assets, investment made

in purchasing long term financial statements. Financing decisions are helps managers to determine

the better and effective long term decisions.

Working capital decision: these decisions are made to make a optimum structure of current

assets and liabilities. It helps the management to keep a minimum amount of cash and stock in

organisation to repay its liabilities. Devotes, cash, inventories and creditors are the essential

elements of working capital requirement.

Decisions related to debts and equity: it helps the managers of organisation that which option is

better to generate finance such as debts and equities. It helps to make relations between the debts

and equity.

9. Provide three (3) examples of financial management decisions.

Cost control

Identify investment opportunities

Improving accounting standards

10. Explain the difference between financial accounting and management accounting.

Financing accounting Management accounting

This accounting system remain focused to make

financial statements.

This accounting system provides helpful

information to managers subject to decision

making.

It provides only monetary information to

departmental managers and senior level

management.

It provides all the monetary and non monetary

informations to managers to make strategies

and plans.

Financial statements are prepared in the end of

financial year.

These reports are prepared monthly, quarterly

and yearly basis.

Financial information remain essential for both In this accounting system information remain

8. Provide five (5) examples of financing decisions

Short term financing: Decisions which are made to respond short term finance problems are

considered as short term financing. Bank overdraft, short term credits, borrowings are the type of

short term financial resources.

It helps managers to find out best and effective option to generate short term finance requirement.

Long term financing: Long term investments such as purchase of fixed assets, investment made

in purchasing long term financial statements. Financing decisions are helps managers to determine

the better and effective long term decisions.

Working capital decision: these decisions are made to make a optimum structure of current

assets and liabilities. It helps the management to keep a minimum amount of cash and stock in

organisation to repay its liabilities. Devotes, cash, inventories and creditors are the essential

elements of working capital requirement.

Decisions related to debts and equity: it helps the managers of organisation that which option is

better to generate finance such as debts and equities. It helps to make relations between the debts

and equity.

9. Provide three (3) examples of financial management decisions.

Cost control

Identify investment opportunities

Improving accounting standards

10. Explain the difference between financial accounting and management accounting.

Financing accounting Management accounting

This accounting system remain focused to make

financial statements.

This accounting system provides helpful

information to managers subject to decision

making.

It provides only monetary information to

departmental managers and senior level

management.

It provides all the monetary and non monetary

informations to managers to make strategies

and plans.

Financial statements are prepared in the end of

financial year.

These reports are prepared monthly, quarterly

and yearly basis.

Financial information remain essential for both In this accounting system information remain

the internal and external parties. essential subject to internal partied such as

management level.

These are the summarised information in

respect of classification of transactions.

These provides completed reports to purse the

decision making process.

All the information remain relevant to the

subject.

Projected information and details also remain

essential in this section.

11. Provide five (5) examples of ratios that can be used for analysis and what they mean

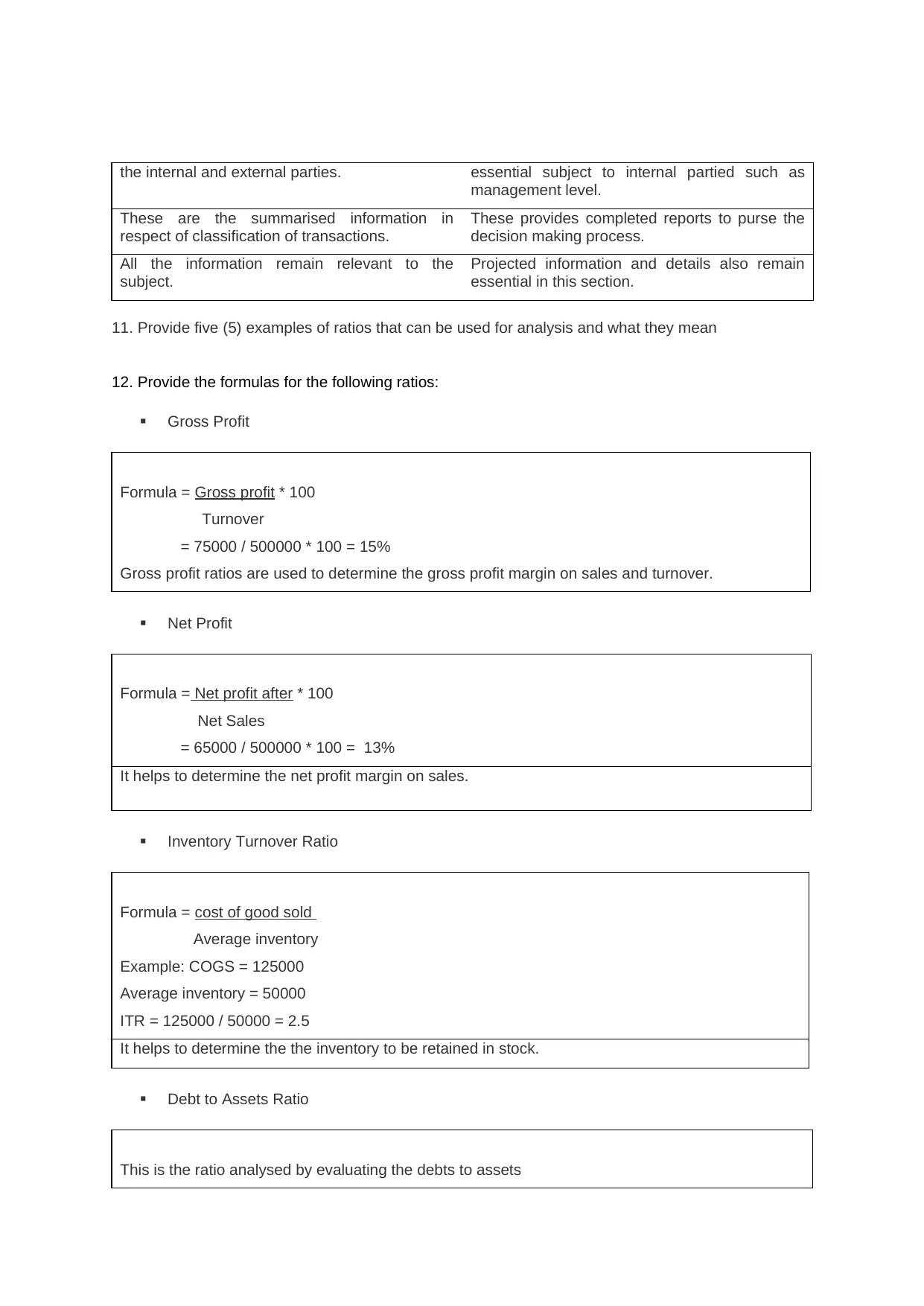

12. Provide the formulas for the following ratios:

Gross Profit

Formula = Gross profit * 100

Turnover

= 75000 / 500000 * 100 = 15%

Gross profit ratios are used to determine the gross profit margin on sales and turnover.

Net Profit

Formula = Net profit after * 100

Net Sales

= 65000 / 500000 * 100 = 13%

It helps to determine the net profit margin on sales.

Inventory Turnover Ratio

Formula = cost of good sold

Average inventory

Example: COGS = 125000

Average inventory = 50000

ITR = 125000 / 50000 = 2.5

It helps to determine the the inventory to be retained in stock.

Debt to Assets Ratio

This is the ratio analysed by evaluating the debts to assets

management level.

These are the summarised information in

respect of classification of transactions.

These provides completed reports to purse the

decision making process.

All the information remain relevant to the

subject.

Projected information and details also remain

essential in this section.

11. Provide five (5) examples of ratios that can be used for analysis and what they mean

12. Provide the formulas for the following ratios:

Gross Profit

Formula = Gross profit * 100

Turnover

= 75000 / 500000 * 100 = 15%

Gross profit ratios are used to determine the gross profit margin on sales and turnover.

Net Profit

Formula = Net profit after * 100

Net Sales

= 65000 / 500000 * 100 = 13%

It helps to determine the net profit margin on sales.

Inventory Turnover Ratio

Formula = cost of good sold

Average inventory

Example: COGS = 125000

Average inventory = 50000

ITR = 125000 / 50000 = 2.5

It helps to determine the the inventory to be retained in stock.

Debt to Assets Ratio

This is the ratio analysed by evaluating the debts to assets

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

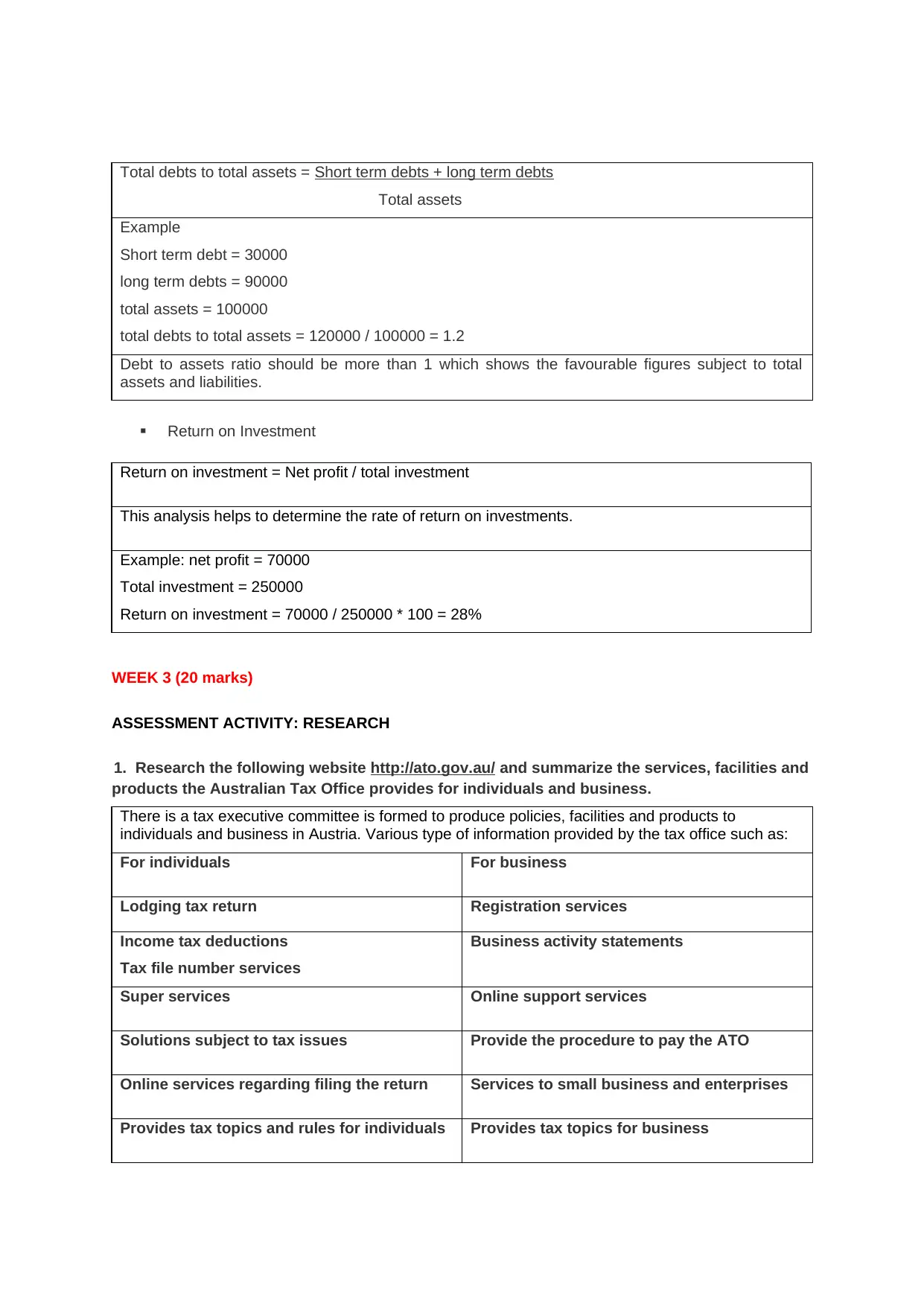

Total debts to total assets = Short term debts + long term debts

Total assets

Example

Short term debt = 30000

long term debts = 90000

total assets = 100000

total debts to total assets = 120000 / 100000 = 1.2

Debt to assets ratio should be more than 1 which shows the favourable figures subject to total

assets and liabilities.

Return on Investment

Return on investment = Net profit / total investment

This analysis helps to determine the rate of return on investments.

Example: net profit = 70000

Total investment = 250000

Return on investment = 70000 / 250000 * 100 = 28%

WEEK 3 (20 marks)

ASSESSMENT ACTIVITY: RESEARCH

1. Research the following website http://ato.gov.au/ and summarize the services, facilities and

products the Australian Tax Office provides for individuals and business.

There is a tax executive committee is formed to produce policies, facilities and products to

individuals and business in Austria. Various type of information provided by the tax office such as:

For individuals For business

Lodging tax return Registration services

Income tax deductions

Tax file number services

Business activity statements

Super services Online support services

Solutions subject to tax issues Provide the procedure to pay the ATO

Online services regarding filing the return Services to small business and enterprises

Provides tax topics and rules for individuals Provides tax topics for business

Total assets

Example

Short term debt = 30000

long term debts = 90000

total assets = 100000

total debts to total assets = 120000 / 100000 = 1.2

Debt to assets ratio should be more than 1 which shows the favourable figures subject to total

assets and liabilities.

Return on Investment

Return on investment = Net profit / total investment

This analysis helps to determine the rate of return on investments.

Example: net profit = 70000

Total investment = 250000

Return on investment = 70000 / 250000 * 100 = 28%

WEEK 3 (20 marks)

ASSESSMENT ACTIVITY: RESEARCH

1. Research the following website http://ato.gov.au/ and summarize the services, facilities and

products the Australian Tax Office provides for individuals and business.

There is a tax executive committee is formed to produce policies, facilities and products to

individuals and business in Austria. Various type of information provided by the tax office such as:

For individuals For business

Lodging tax return Registration services

Income tax deductions

Tax file number services

Business activity statements

Super services Online support services

Solutions subject to tax issues Provide the procedure to pay the ATO

Online services regarding filing the return Services to small business and enterprises

Provides tax topics and rules for individuals Provides tax topics for business

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

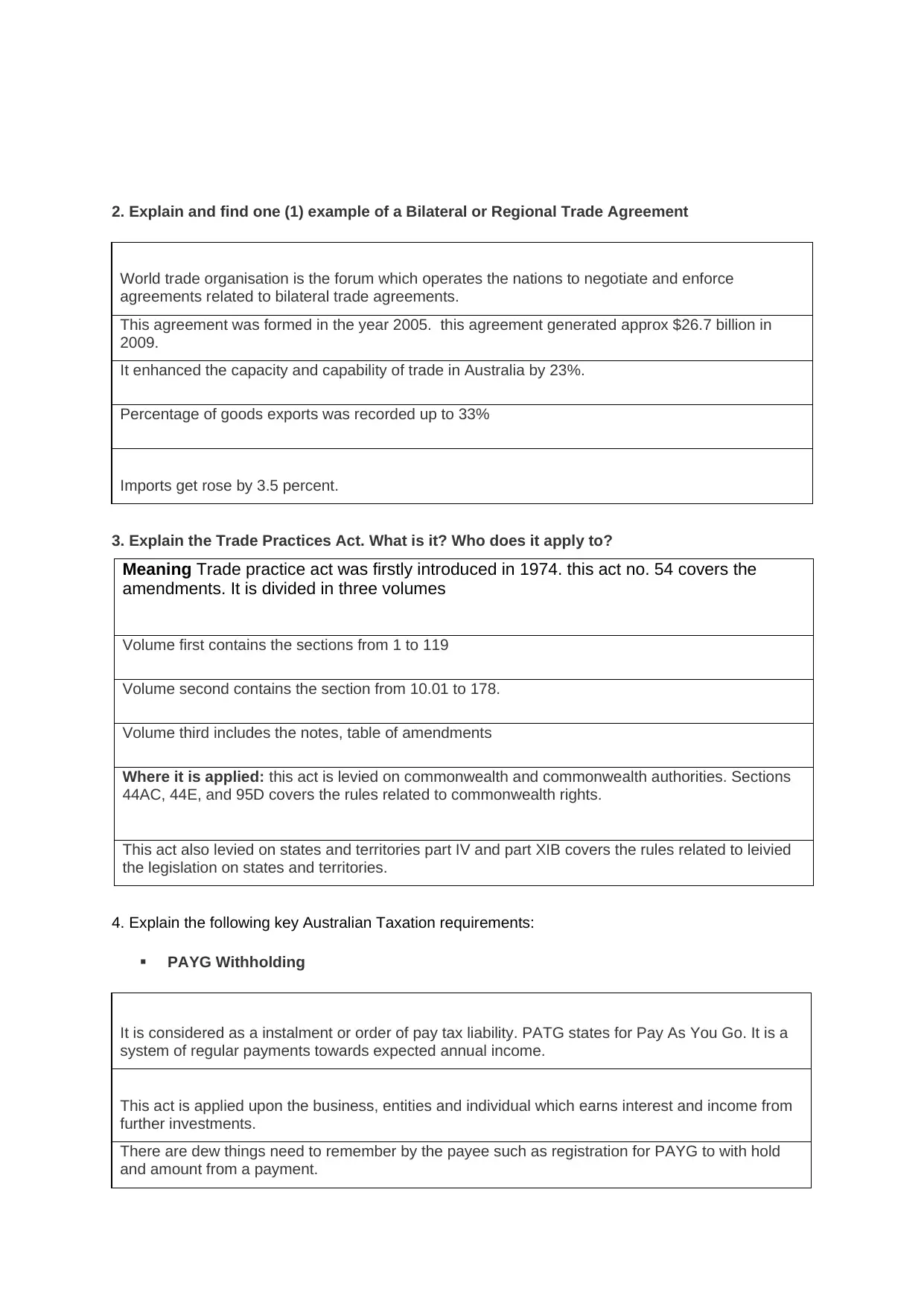

2. Explain and find one (1) example of a Bilateral or Regional Trade Agreement

World trade organisation is the forum which operates the nations to negotiate and enforce

agreements related to bilateral trade agreements.

This agreement was formed in the year 2005. this agreement generated approx $26.7 billion in

2009.

It enhanced the capacity and capability of trade in Australia by 23%.

Percentage of goods exports was recorded up to 33%

Imports get rose by 3.5 percent.

3. Explain the Trade Practices Act. What is it? Who does it apply to?

Meaning Trade practice act was firstly introduced in 1974. this act no. 54 covers the

amendments. It is divided in three volumes

Volume first contains the sections from 1 to 119

Volume second contains the section from 10.01 to 178.

Volume third includes the notes, table of amendments

Where it is applied: this act is levied on commonwealth and commonwealth authorities. Sections

44AC, 44E, and 95D covers the rules related to commonwealth rights.

This act also levied on states and territories part IV and part XIB covers the rules related to leivied

the legislation on states and territories.

4. Explain the following key Australian Taxation requirements:

PAYG Withholding

It is considered as a instalment or order of pay tax liability. PATG states for Pay As You Go. It is a

system of regular payments towards expected annual income.

This act is applied upon the business, entities and individual which earns interest and income from

further investments.

There are dew things need to remember by the payee such as registration for PAYG to with hold

and amount from a payment.

World trade organisation is the forum which operates the nations to negotiate and enforce

agreements related to bilateral trade agreements.

This agreement was formed in the year 2005. this agreement generated approx $26.7 billion in

2009.

It enhanced the capacity and capability of trade in Australia by 23%.

Percentage of goods exports was recorded up to 33%

Imports get rose by 3.5 percent.

3. Explain the Trade Practices Act. What is it? Who does it apply to?

Meaning Trade practice act was firstly introduced in 1974. this act no. 54 covers the

amendments. It is divided in three volumes

Volume first contains the sections from 1 to 119

Volume second contains the section from 10.01 to 178.

Volume third includes the notes, table of amendments

Where it is applied: this act is levied on commonwealth and commonwealth authorities. Sections

44AC, 44E, and 95D covers the rules related to commonwealth rights.

This act also levied on states and territories part IV and part XIB covers the rules related to leivied

the legislation on states and territories.

4. Explain the following key Australian Taxation requirements:

PAYG Withholding

It is considered as a instalment or order of pay tax liability. PATG states for Pay As You Go. It is a

system of regular payments towards expected annual income.

This act is applied upon the business, entities and individual which earns interest and income from

further investments.

There are dew things need to remember by the payee such as registration for PAYG to with hold

and amount from a payment.

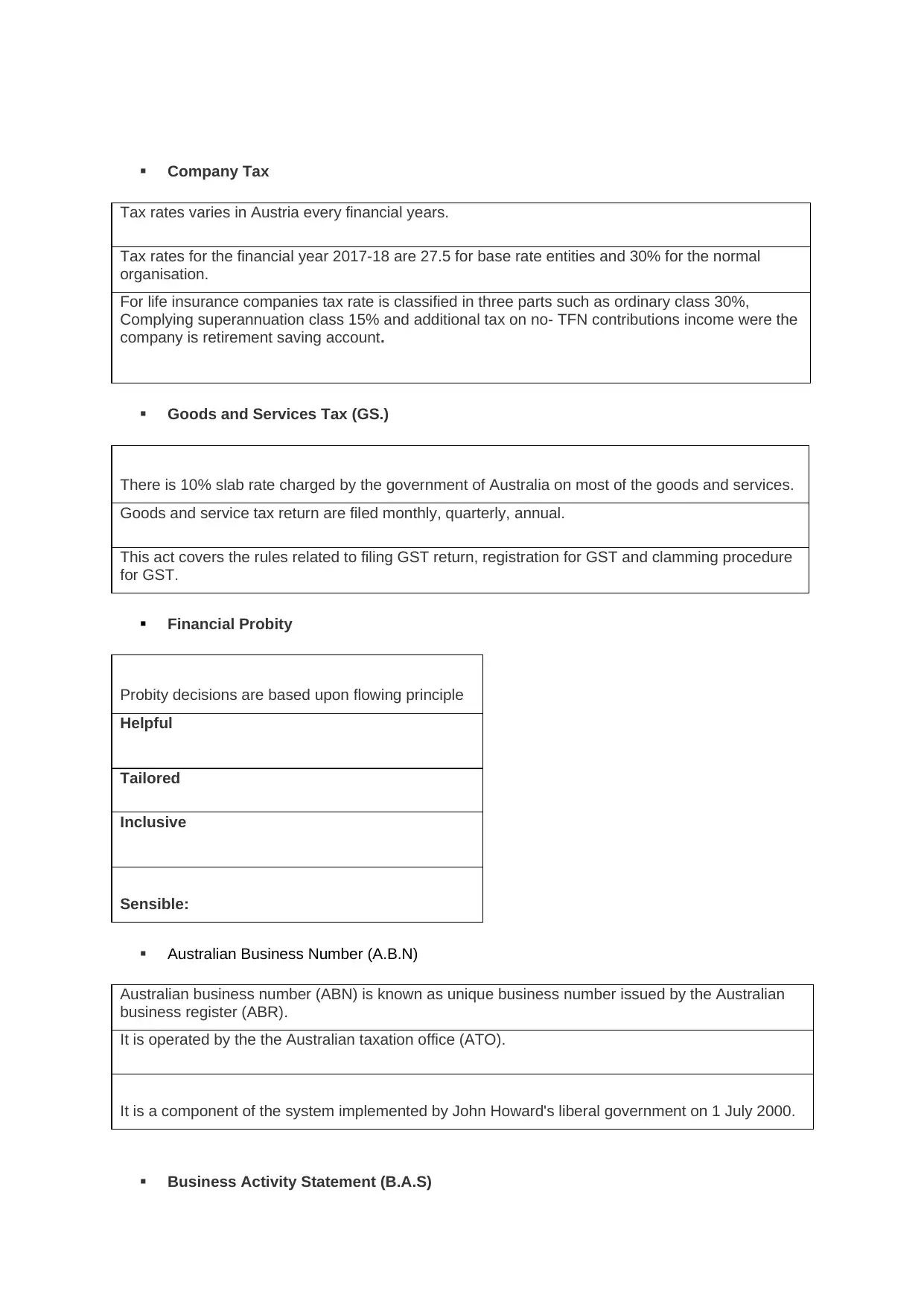

Company Tax

Tax rates varies in Austria every financial years.

Tax rates for the financial year 2017-18 are 27.5 for base rate entities and 30% for the normal

organisation.

For life insurance companies tax rate is classified in three parts such as ordinary class 30%,

Complying superannuation class 15% and additional tax on no- TFN contributions income were the

company is retirement saving account.

Goods and Services Tax (GS.)

There is 10% slab rate charged by the government of Australia on most of the goods and services.

Goods and service tax return are filed monthly, quarterly, annual.

This act covers the rules related to filing GST return, registration for GST and clamming procedure

for GST.

Financial Probity

Probity decisions are based upon flowing principle

Helpful

Tailored

Inclusive

Sensible:

Australian Business Number (A.B.N)

Australian business number (ABN) is known as unique business number issued by the Australian

business register (ABR).

It is operated by the the Australian taxation office (ATO).

It is a component of the system implemented by John Howard's liberal government on 1 July 2000.

Business Activity Statement (B.A.S)

Tax rates varies in Austria every financial years.

Tax rates for the financial year 2017-18 are 27.5 for base rate entities and 30% for the normal

organisation.

For life insurance companies tax rate is classified in three parts such as ordinary class 30%,

Complying superannuation class 15% and additional tax on no- TFN contributions income were the

company is retirement saving account.

Goods and Services Tax (GS.)

There is 10% slab rate charged by the government of Australia on most of the goods and services.

Goods and service tax return are filed monthly, quarterly, annual.

This act covers the rules related to filing GST return, registration for GST and clamming procedure

for GST.

Financial Probity

Probity decisions are based upon flowing principle

Helpful

Tailored

Inclusive

Sensible:

Australian Business Number (A.B.N)

Australian business number (ABN) is known as unique business number issued by the Australian

business register (ABR).

It is operated by the the Australian taxation office (ATO).

It is a component of the system implemented by John Howard's liberal government on 1 July 2000.

Business Activity Statement (B.A.S)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 27

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.