Financial Management Report: Equity Finance and Appraisal Techniques

VerifiedAdded on 2021/02/20

|15

|3941

|144

Report

AI Summary

This financial management report provides a comprehensive overview of key concepts in financial management. The report begins with an introduction to financial management and its importance in business, followed by an analysis of long-term finance, specifically equity finance, including the calculation of theoretical ex-right price and earnings per share. The report then delves into investment appraisal techniques, such as payback period, accounting rate of return, net present value (NPV), and internal rate of return (IRR), with detailed calculations and evaluations. Additionally, the report explores the concept of dividends, differentiating between cash and scrip dividends, and discussing their advantages for both companies and shareholders. The report concludes with a summary of findings and recommendations for financial decision-making.

FINANCIAL MANAGEMENT

ASSESSMENT

ASSESSMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

INTRODUCTION...........................................................................................................................................3

SOLUTION 2.................................................................................................................................................3

Long term finance: Equity finance..........................................................................................................3

SOLUTION 3.................................................................................................................................................7

A) Calculation of investment appraisal techniques.................................................................................7

B) The benefits and limitation of investment appraisal techniques......................................................10

CONCLUSION.............................................................................................................................................13

REFERENCES ..............................................................................................................................................14

INTRODUCTION...........................................................................................................................................3

SOLUTION 2.................................................................................................................................................3

Long term finance: Equity finance..........................................................................................................3

SOLUTION 3.................................................................................................................................................7

A) Calculation of investment appraisal techniques.................................................................................7

B) The benefits and limitation of investment appraisal techniques......................................................10

CONCLUSION.............................................................................................................................................13

REFERENCES ..............................................................................................................................................14

INTRODUCTION

Financial management are broad principles and rules of management. It deals with the proper

management of the organisation's finance and ensures effective and efficient functioning of

business. It is defines as analysing investments and money in the business which is used in

decision making. Accounting department is responsible for managing the finance of the

company. Present report is based on financial management assessment where long term finance

such as equities are explained. Further report also includes investment appraisal techniques such

as payback period, accounting rate of return, net present value and internal rate of return.

Benefits and limitations of each technique is also mentioned in the report.

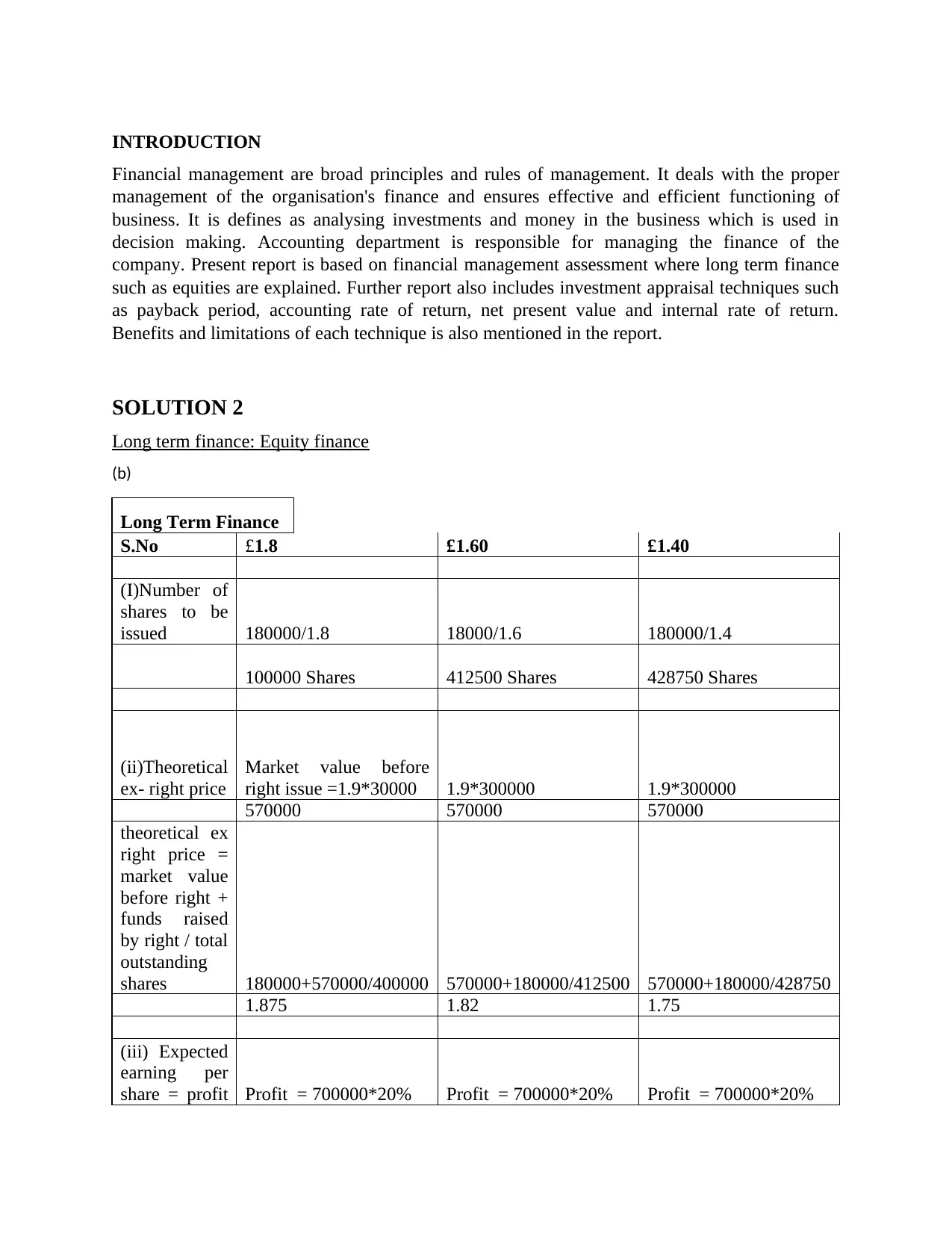

SOLUTION 2

Long term finance: Equity finance

(b)

Long Term Finance

S.No £1.8 £1.60 £1.40

(I)Number of

shares to be

issued 180000/1.8 18000/1.6 180000/1.4

100000 Shares 412500 Shares 428750 Shares

(ii)Theoretical

ex- right price

Market value before

right issue =1.9*30000 1.9*300000 1.9*300000

570000 570000 570000

theoretical ex

right price =

market value

before right +

funds raised

by right / total

outstanding

shares 180000+570000/400000 570000+180000/412500 570000+180000/428750

1.875 1.82 1.75

(iii) Expected

earning per

share = profit Profit = 700000*20% Profit = 700000*20% Profit = 700000*20%

Financial management are broad principles and rules of management. It deals with the proper

management of the organisation's finance and ensures effective and efficient functioning of

business. It is defines as analysing investments and money in the business which is used in

decision making. Accounting department is responsible for managing the finance of the

company. Present report is based on financial management assessment where long term finance

such as equities are explained. Further report also includes investment appraisal techniques such

as payback period, accounting rate of return, net present value and internal rate of return.

Benefits and limitations of each technique is also mentioned in the report.

SOLUTION 2

Long term finance: Equity finance

(b)

Long Term Finance

S.No £1.8 £1.60 £1.40

(I)Number of

shares to be

issued 180000/1.8 18000/1.6 180000/1.4

100000 Shares 412500 Shares 428750 Shares

(ii)Theoretical

ex- right price

Market value before

right issue =1.9*30000 1.9*300000 1.9*300000

570000 570000 570000

theoretical ex

right price =

market value

before right +

funds raised

by right / total

outstanding

shares 180000+570000/400000 570000+180000/412500 570000+180000/428750

1.875 1.82 1.75

(iii) Expected

earning per

share = profit Profit = 700000*20% Profit = 700000*20% Profit = 700000*20%

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

after tax/total

outstanding

shares

140000 140000 140000

EPS =140000/400000 140000/412500 140000/428750

0.35 0.34 0.32

(iv) Form of

issue for each

right price Direct issue Direct issue Insured issue

(v) Evaluation

company will not face

extra redundancy in this

issue as EPS is high

this option will also be

accepted by

shareholders as their

EPS is not changing at

very high rate

all shares might not be

accepted as eps has

gone down

outstanding

shares

140000 140000 140000

EPS =140000/400000 140000/412500 140000/428750

0.35 0.34 0.32

(iv) Form of

issue for each

right price Direct issue Direct issue Insured issue

(v) Evaluation

company will not face

extra redundancy in this

issue as EPS is high

this option will also be

accepted by

shareholders as their

EPS is not changing at

very high rate

all shares might not be

accepted as eps has

gone down

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Suggestion:

Company should issue

its right shares at £1.8

as issuing at this price

shares will not be issued

more which will protect

company from bearing

cost of underwriters for

its shares both other

options are not

beneficial as they are

reducing the eps and

increased number of

shares will reduce the

market value of shares,

evaluating above

scenarios it is suggested

that company should

issue its right at £1.8

(c) Dividend can be defined as that part of earnings of a company which is agreed to be

distributed by board of directors of company to its shareholders. It is known as reward from

company's earnings which is shared among shareholder of different class. Dividends of company

are decided and managed by its board of directors. Its approval is taken by shareholder in

meeting by voting. There are various forms of issuing dividends such as cash payments, stock

shares, property etc. in these dividends cash dividend are most commonly accepted by

shareholders. Purpose of paying dividend is to provide returns to investors on their shareholding

in company. Dividend are important as it will retain employees and its trust (Reifarth, 2019).

They are seen as growth of company, how well company is performing in market as shareholder

generally judge growth on the basis of returns they are getting on their investments. However it

is also essential for people to know that company does not distribute all of its profits to its

shareholder only agreed portion is distributed. The remaining portion of profits is retained by

company which will be used by company for its various operations and future expansion plans.

Some companies still pay dividend even when their profits are in adequate or no profits.

Company should issue

its right shares at £1.8

as issuing at this price

shares will not be issued

more which will protect

company from bearing

cost of underwriters for

its shares both other

options are not

beneficial as they are

reducing the eps and

increased number of

shares will reduce the

market value of shares,

evaluating above

scenarios it is suggested

that company should

issue its right at £1.8

(c) Dividend can be defined as that part of earnings of a company which is agreed to be

distributed by board of directors of company to its shareholders. It is known as reward from

company's earnings which is shared among shareholder of different class. Dividends of company

are decided and managed by its board of directors. Its approval is taken by shareholder in

meeting by voting. There are various forms of issuing dividends such as cash payments, stock

shares, property etc. in these dividends cash dividend are most commonly accepted by

shareholders. Purpose of paying dividend is to provide returns to investors on their shareholding

in company. Dividend are important as it will retain employees and its trust (Reifarth, 2019).

They are seen as growth of company, how well company is performing in market as shareholder

generally judge growth on the basis of returns they are getting on their investments. However it

is also essential for people to know that company does not distribute all of its profits to its

shareholder only agreed portion is distributed. The remaining portion of profits is retained by

company which will be used by company for its various operations and future expansion plans.

Some companies still pay dividend even when their profits are in adequate or no profits.

Companies are able to pay dividends even on inadequate dividends as they retain considerable

amount of profits for distributing dividends to shareholders(López, 2017).

Cash Dividend

Cash dividend can be defined as payments that are made by a company from its earnings

to shareholders who have invested their money in company in form of cash. Cash dividends are

also a form of dividend that are paid in cash. Cash dividends are most preferred form of dividend

the shareholders of company. Cash dividends affects the liquidity position of company as major

amount of money is to be distributed. There are situations where companies have enough

revenues but not in form of monetary terms at that time it becomes difficult for company to

distribute cash dividend to shareholder (Zelalem, 2018).

Scrip Dividend

Scrip dividend can be defined as a dividend program where company instead of giving

their shareholders cash dividend, gives them an option to receive dividend in form of equivalent

shares of company. They are also known as bonus issue or capitalization issue and it is known as

a secondary issue as existing cash reserves of company are converted to fresh shares and offerd

to existing shareholder of company or as an additional issue to existing shareholder in proportion

of their shareholding on pro-rata basis (Sweeting, 2017). Scrip dividend are becoming a trend in

modern times as companies want to use money in other operations of company by increasing

shareholding in company by providing shares to shareholders. Scrip issue is a method of creating

fresh shares that are distributed free of charge to existing shareholders of company and therefore

known as scrip dividend.

Issues are made considering existing holdings of company. Company issues for example

2 shares for every 5 shares which are currently held by shareholder. Scrips increase number of

shares without increasing value of company. In other words it can be defined that increased

number of shares reduces existing value per share of company. Shareholders are also having

right of selling new scrips to others in market. Scrips value are required to be disclosed I tax

returns like cash dividends. Scrips dividends are helping company to grow as they are able to

invest funds over more productive activities which will help company to generate mo re revenues

(Zelalem, 2018).

Advantages of Scrip dividend to company

Scrip dividends means shares rather than cash as dividends to shareholders of company.

Companies adopt scrip dividends for conserving their cash reserves. Another benefit that arise to

company by issue of scrip dividend is that they can avoid Advance Corporation Tax which they

have to pay every time they distribute dividends to shareholders. Companies issuing scrip

dividend do not have to arrange for cash for payments of dividends to shareholders that saves

their liquid funds. Company also issues scrip dividend as they help them to save their monetary

fund which they want to utilize for their future growth plans. Company is benefited by this

program as there are situations where company do not have adequate funds for payments so they

can issue shares to existing shareholders without paying cash (Ezeagba, 2017). It helps company

to preserve its monetary funds for reinvestment. More shares will help company to reduce its

amount of profits for distributing dividends to shareholders(López, 2017).

Cash Dividend

Cash dividend can be defined as payments that are made by a company from its earnings

to shareholders who have invested their money in company in form of cash. Cash dividends are

also a form of dividend that are paid in cash. Cash dividends are most preferred form of dividend

the shareholders of company. Cash dividends affects the liquidity position of company as major

amount of money is to be distributed. There are situations where companies have enough

revenues but not in form of monetary terms at that time it becomes difficult for company to

distribute cash dividend to shareholder (Zelalem, 2018).

Scrip Dividend

Scrip dividend can be defined as a dividend program where company instead of giving

their shareholders cash dividend, gives them an option to receive dividend in form of equivalent

shares of company. They are also known as bonus issue or capitalization issue and it is known as

a secondary issue as existing cash reserves of company are converted to fresh shares and offerd

to existing shareholder of company or as an additional issue to existing shareholder in proportion

of their shareholding on pro-rata basis (Sweeting, 2017). Scrip dividend are becoming a trend in

modern times as companies want to use money in other operations of company by increasing

shareholding in company by providing shares to shareholders. Scrip issue is a method of creating

fresh shares that are distributed free of charge to existing shareholders of company and therefore

known as scrip dividend.

Issues are made considering existing holdings of company. Company issues for example

2 shares for every 5 shares which are currently held by shareholder. Scrips increase number of

shares without increasing value of company. In other words it can be defined that increased

number of shares reduces existing value per share of company. Shareholders are also having

right of selling new scrips to others in market. Scrips value are required to be disclosed I tax

returns like cash dividends. Scrips dividends are helping company to grow as they are able to

invest funds over more productive activities which will help company to generate mo re revenues

(Zelalem, 2018).

Advantages of Scrip dividend to company

Scrip dividends means shares rather than cash as dividends to shareholders of company.

Companies adopt scrip dividends for conserving their cash reserves. Another benefit that arise to

company by issue of scrip dividend is that they can avoid Advance Corporation Tax which they

have to pay every time they distribute dividends to shareholders. Companies issuing scrip

dividend do not have to arrange for cash for payments of dividends to shareholders that saves

their liquid funds. Company also issues scrip dividend as they help them to save their monetary

fund which they want to utilize for their future growth plans. Company is benefited by this

program as there are situations where company do not have adequate funds for payments so they

can issue shares to existing shareholders without paying cash (Ezeagba, 2017). It helps company

to preserve its monetary funds for reinvestment. More shares will help company to reduce its

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

gearing ratio that will increase borrowing capacity of company in market (Johal, Roberts and

Sim, 2019).

Advantages of scrip dividend to shareholders

Scrip dividends are given as options to shareholders. Shareholders always prefer options

for making choices. Options give the investors chances to make right choice. Different

shareholders have different requirements and needs related to dividends. Scrip dividend are

mostly chosen by young and new investors as they have motive of increasing their holdings in

company so that they can get benefit from price appreciation. Scrip dividend allows shareholder

to get benefits without actually paying for shares (Iheduru and Okoro, 2018). Shareholders in

long run will get benefits from shares as the company will rise its operations and business that

will ultimately benefit shareholders as there share price will be increased over time. Shareholders

can sell shares in market at rates existing at that time and shareholder will be getting for shares

for which they have not paid. Investors will mostly choose scrip dividend as they would not be

required to pay transaction cost for shares they receive where they wold be required to pay if

those shares were brought by investors from market. Another advantage of scrip dividend to

shareholder is that they do not have to pay commissions, brokerage or stamp duty for purchasing

shares of company (Cannavan and Gray, 2017).

SOLUTION 3

A) Calculation of investment appraisal techniques

Calculation of Payback period

Payback period : The pay back period of the company is calculated to estimate the time

required to recover the cost of investment in the company. The shorter pay back period refers to

more interesting investment because company is able to recover the cost in shorter period of time

which present its efficiency and effectiveness. It can be calculated by average method and

subtraction method (How to calculate the payback period. 2019). The average method for

calculating pay back period is suitable when the cash flow are steady in the following years. It

can be calculated by adding all the cash inflow and divided it to the initial investment or cost of

the machinery. It help the finance and account manager to identify that whether they have to go

with the project or not. Here the pay back period is 1.96 year which indicate that Happy Meal

limited company cover the initial investment within 2 year which is quite good for them.

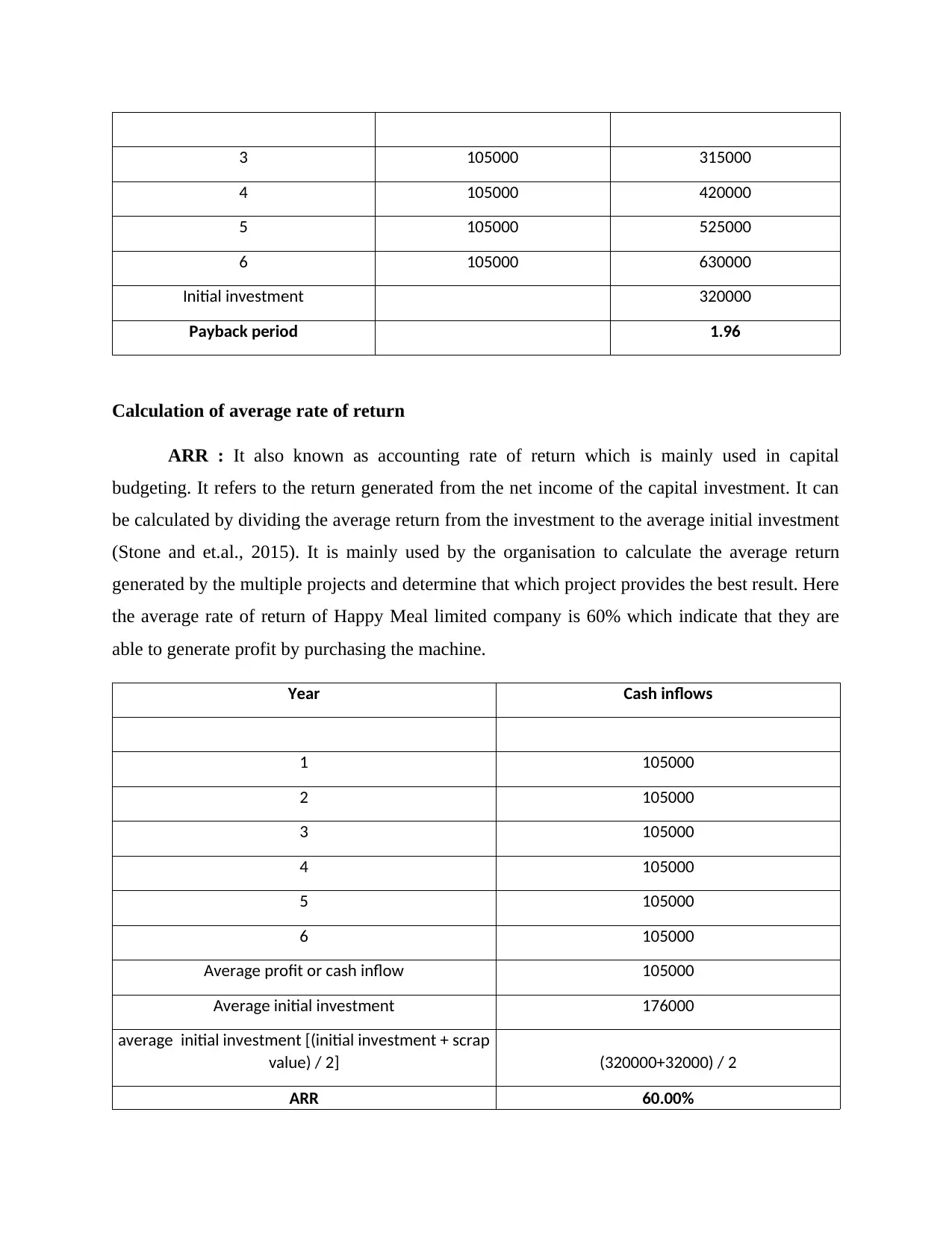

Year Cash inflows Cumulative cash inflows

1 105000 105000

2 105000 210000

Sim, 2019).

Advantages of scrip dividend to shareholders

Scrip dividends are given as options to shareholders. Shareholders always prefer options

for making choices. Options give the investors chances to make right choice. Different

shareholders have different requirements and needs related to dividends. Scrip dividend are

mostly chosen by young and new investors as they have motive of increasing their holdings in

company so that they can get benefit from price appreciation. Scrip dividend allows shareholder

to get benefits without actually paying for shares (Iheduru and Okoro, 2018). Shareholders in

long run will get benefits from shares as the company will rise its operations and business that

will ultimately benefit shareholders as there share price will be increased over time. Shareholders

can sell shares in market at rates existing at that time and shareholder will be getting for shares

for which they have not paid. Investors will mostly choose scrip dividend as they would not be

required to pay transaction cost for shares they receive where they wold be required to pay if

those shares were brought by investors from market. Another advantage of scrip dividend to

shareholder is that they do not have to pay commissions, brokerage or stamp duty for purchasing

shares of company (Cannavan and Gray, 2017).

SOLUTION 3

A) Calculation of investment appraisal techniques

Calculation of Payback period

Payback period : The pay back period of the company is calculated to estimate the time

required to recover the cost of investment in the company. The shorter pay back period refers to

more interesting investment because company is able to recover the cost in shorter period of time

which present its efficiency and effectiveness. It can be calculated by average method and

subtraction method (How to calculate the payback period. 2019). The average method for

calculating pay back period is suitable when the cash flow are steady in the following years. It

can be calculated by adding all the cash inflow and divided it to the initial investment or cost of

the machinery. It help the finance and account manager to identify that whether they have to go

with the project or not. Here the pay back period is 1.96 year which indicate that Happy Meal

limited company cover the initial investment within 2 year which is quite good for them.

Year Cash inflows Cumulative cash inflows

1 105000 105000

2 105000 210000

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

3 105000 315000

4 105000 420000

5 105000 525000

6 105000 630000

Initial investment 320000

Payback period 1.96

Calculation of average rate of return

ARR : It also known as accounting rate of return which is mainly used in capital

budgeting. It refers to the return generated from the net income of the capital investment. It can

be calculated by dividing the average return from the investment to the average initial investment

(Stone and et.al., 2015). It is mainly used by the organisation to calculate the average return

generated by the multiple projects and determine that which project provides the best result. Here

the average rate of return of Happy Meal limited company is 60% which indicate that they are

able to generate profit by purchasing the machine.

Year Cash inflows

1 105000

2 105000

3 105000

4 105000

5 105000

6 105000

Average profit or cash inflow 105000

Average initial investment 176000

average initial investment [(initial investment + scrap

value) / 2] (320000+32000) / 2

ARR 60.00%

4 105000 420000

5 105000 525000

6 105000 630000

Initial investment 320000

Payback period 1.96

Calculation of average rate of return

ARR : It also known as accounting rate of return which is mainly used in capital

budgeting. It refers to the return generated from the net income of the capital investment. It can

be calculated by dividing the average return from the investment to the average initial investment

(Stone and et.al., 2015). It is mainly used by the organisation to calculate the average return

generated by the multiple projects and determine that which project provides the best result. Here

the average rate of return of Happy Meal limited company is 60% which indicate that they are

able to generate profit by purchasing the machine.

Year Cash inflows

1 105000

2 105000

3 105000

4 105000

5 105000

6 105000

Average profit or cash inflow 105000

Average initial investment 176000

average initial investment [(initial investment + scrap

value) / 2] (320000+32000) / 2

ARR 60.00%

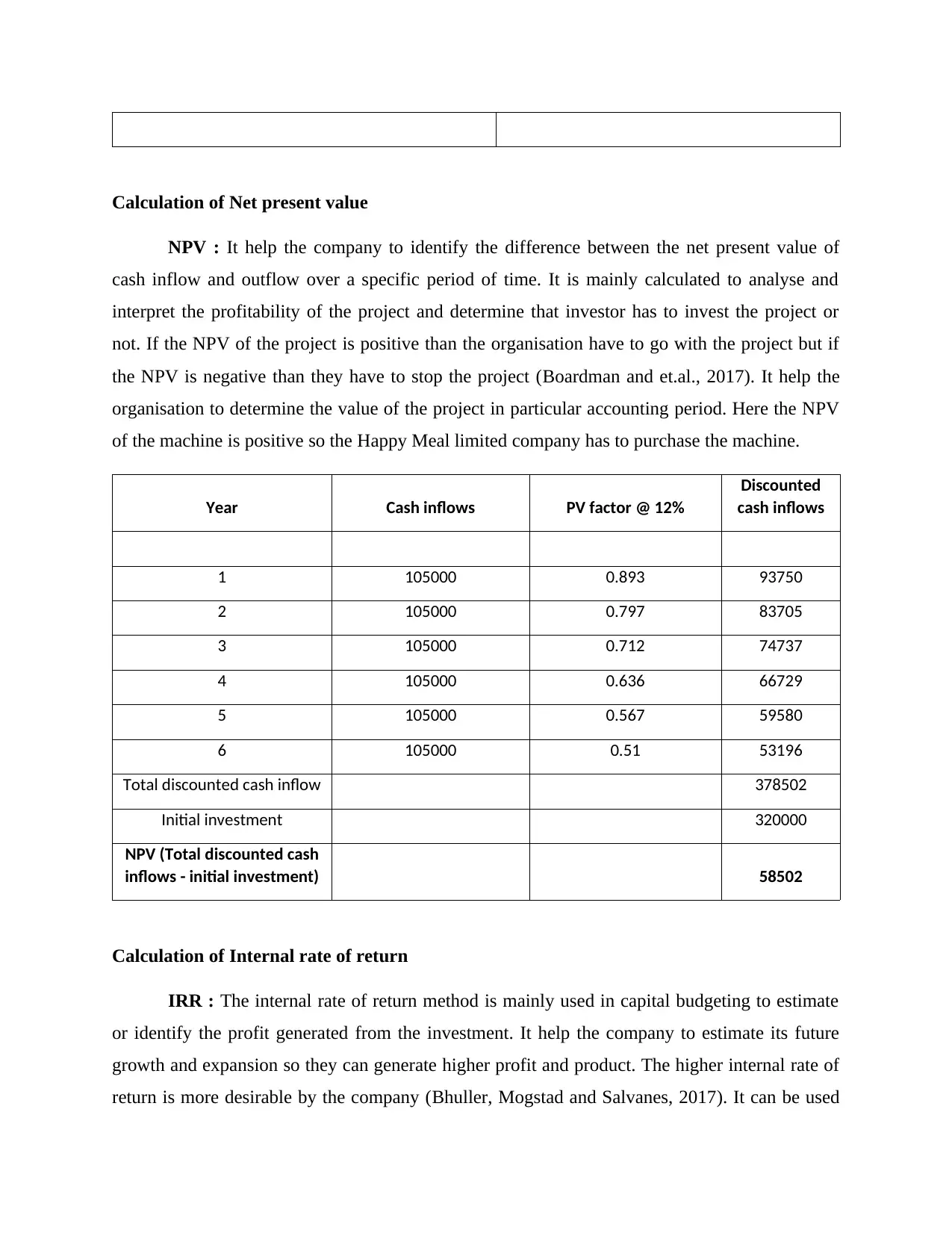

Calculation of Net present value

NPV : It help the company to identify the difference between the net present value of

cash inflow and outflow over a specific period of time. It is mainly calculated to analyse and

interpret the profitability of the project and determine that investor has to invest the project or

not. If the NPV of the project is positive than the organisation have to go with the project but if

the NPV is negative than they have to stop the project (Boardman and et.al., 2017). It help the

organisation to determine the value of the project in particular accounting period. Here the NPV

of the machine is positive so the Happy Meal limited company has to purchase the machine.

Year Cash inflows PV factor @ 12%

Discounted

cash inflows

1 105000 0.893 93750

2 105000 0.797 83705

3 105000 0.712 74737

4 105000 0.636 66729

5 105000 0.567 59580

6 105000 0.51 53196

Total discounted cash inflow 378502

Initial investment 320000

NPV (Total discounted cash

inflows - initial investment) 58502

Calculation of Internal rate of return

IRR : The internal rate of return method is mainly used in capital budgeting to estimate

or identify the profit generated from the investment. It help the company to estimate its future

growth and expansion so they can generate higher profit and product. The higher internal rate of

return is more desirable by the company (Bhuller, Mogstad and Salvanes, 2017). It can be used

NPV : It help the company to identify the difference between the net present value of

cash inflow and outflow over a specific period of time. It is mainly calculated to analyse and

interpret the profitability of the project and determine that investor has to invest the project or

not. If the NPV of the project is positive than the organisation have to go with the project but if

the NPV is negative than they have to stop the project (Boardman and et.al., 2017). It help the

organisation to determine the value of the project in particular accounting period. Here the NPV

of the machine is positive so the Happy Meal limited company has to purchase the machine.

Year Cash inflows PV factor @ 12%

Discounted

cash inflows

1 105000 0.893 93750

2 105000 0.797 83705

3 105000 0.712 74737

4 105000 0.636 66729

5 105000 0.567 59580

6 105000 0.51 53196

Total discounted cash inflow 378502

Initial investment 320000

NPV (Total discounted cash

inflows - initial investment) 58502

Calculation of Internal rate of return

IRR : The internal rate of return method is mainly used in capital budgeting to estimate

or identify the profit generated from the investment. It help the company to estimate its future

growth and expansion so they can generate higher profit and product. The higher internal rate of

return is more desirable by the company (Bhuller, Mogstad and Salvanes, 2017). It can be used

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

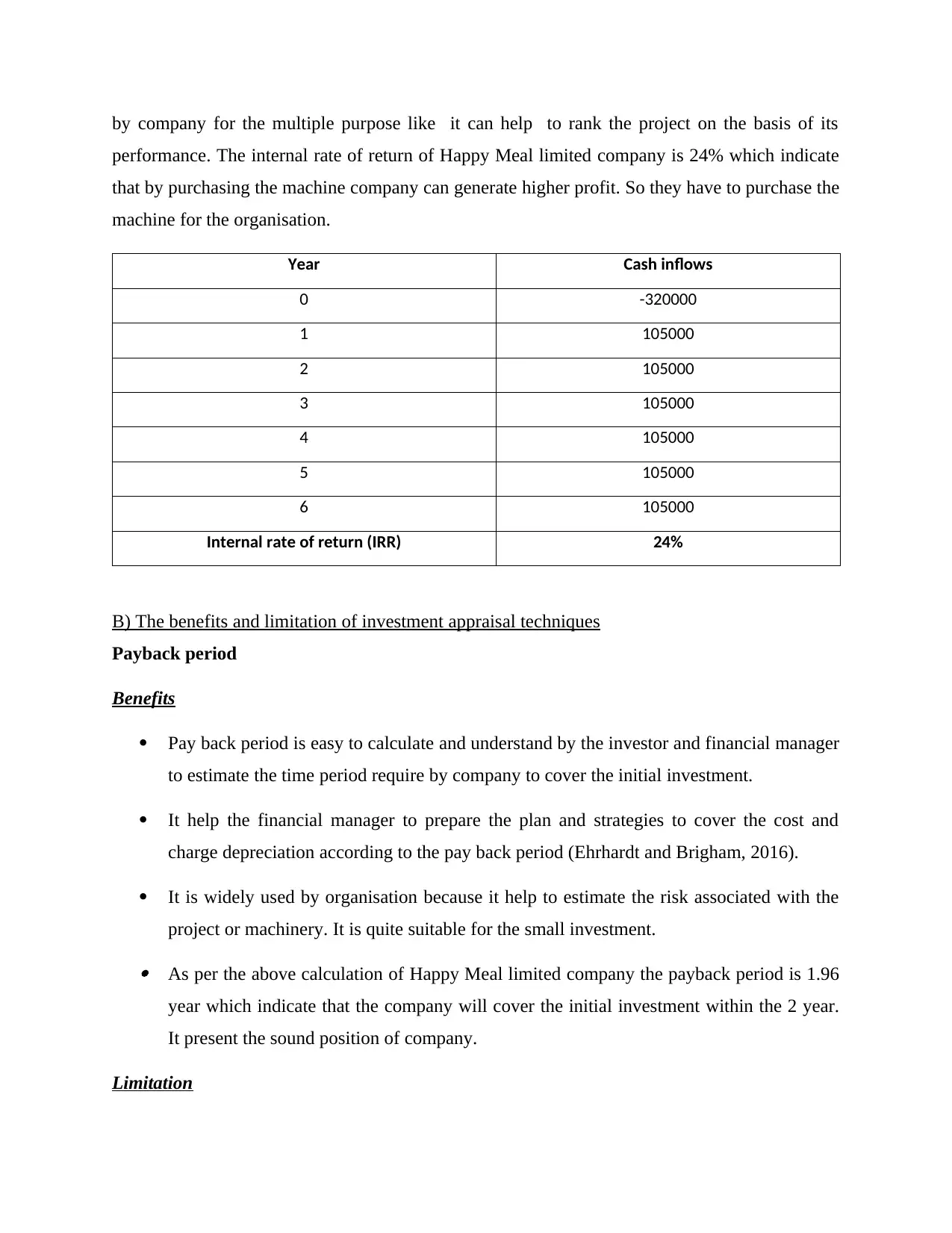

by company for the multiple purpose like it can help to rank the project on the basis of its

performance. The internal rate of return of Happy Meal limited company is 24% which indicate

that by purchasing the machine company can generate higher profit. So they have to purchase the

machine for the organisation.

Year Cash inflows

0 -320000

1 105000

2 105000

3 105000

4 105000

5 105000

6 105000

Internal rate of return (IRR) 24%

B) The benefits and limitation of investment appraisal techniques

Payback period

Benefits

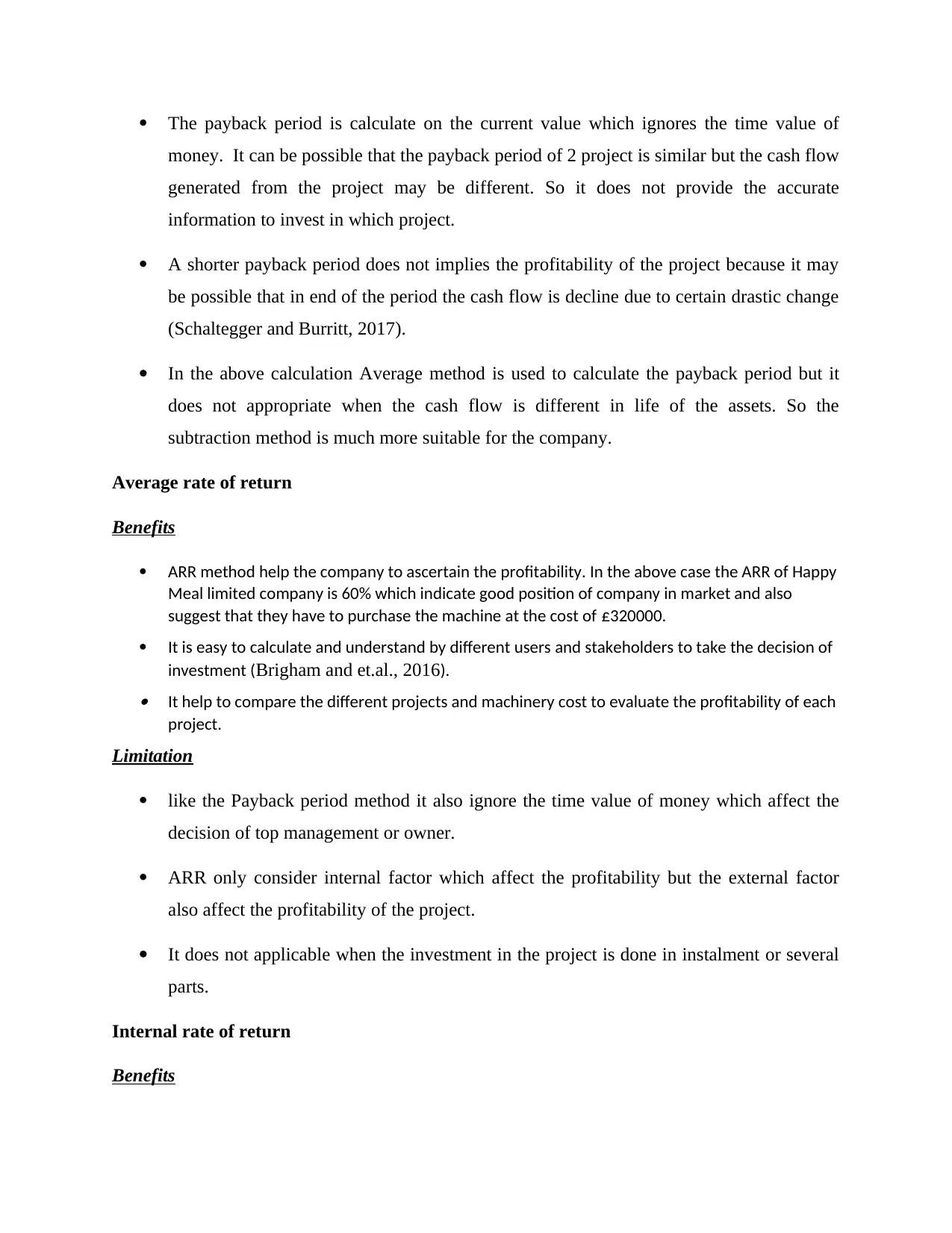

Pay back period is easy to calculate and understand by the investor and financial manager

to estimate the time period require by company to cover the initial investment.

It help the financial manager to prepare the plan and strategies to cover the cost and

charge depreciation according to the pay back period (Ehrhardt and Brigham, 2016).

It is widely used by organisation because it help to estimate the risk associated with the

project or machinery. It is quite suitable for the small investment. As per the above calculation of Happy Meal limited company the payback period is 1.96

year which indicate that the company will cover the initial investment within the 2 year.

It present the sound position of company.

Limitation

performance. The internal rate of return of Happy Meal limited company is 24% which indicate

that by purchasing the machine company can generate higher profit. So they have to purchase the

machine for the organisation.

Year Cash inflows

0 -320000

1 105000

2 105000

3 105000

4 105000

5 105000

6 105000

Internal rate of return (IRR) 24%

B) The benefits and limitation of investment appraisal techniques

Payback period

Benefits

Pay back period is easy to calculate and understand by the investor and financial manager

to estimate the time period require by company to cover the initial investment.

It help the financial manager to prepare the plan and strategies to cover the cost and

charge depreciation according to the pay back period (Ehrhardt and Brigham, 2016).

It is widely used by organisation because it help to estimate the risk associated with the

project or machinery. It is quite suitable for the small investment. As per the above calculation of Happy Meal limited company the payback period is 1.96

year which indicate that the company will cover the initial investment within the 2 year.

It present the sound position of company.

Limitation

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The payback period is calculate on the current value which ignores the time value of

money. It can be possible that the payback period of 2 project is similar but the cash flow

generated from the project may be different. So it does not provide the accurate

information to invest in which project.

A shorter payback period does not implies the profitability of the project because it may

be possible that in end of the period the cash flow is decline due to certain drastic change

(Schaltegger and Burritt, 2017).

In the above calculation Average method is used to calculate the payback period but it

does not appropriate when the cash flow is different in life of the assets. So the

subtraction method is much more suitable for the company.

Average rate of return

Benefits

ARR method help the company to ascertain the profitability. In the above case the ARR of Happy

Meal limited company is 60% which indicate good position of company in market and also

suggest that they have to purchase the machine at the cost of £320000.

It is easy to calculate and understand by different users and stakeholders to take the decision of

investment (Brigham and et.al., 2016). It help to compare the different projects and machinery cost to evaluate the profitability of each

project.

Limitation

like the Payback period method it also ignore the time value of money which affect the

decision of top management or owner.

ARR only consider internal factor which affect the profitability but the external factor

also affect the profitability of the project.

It does not applicable when the investment in the project is done in instalment or several

parts.

Internal rate of return

Benefits

money. It can be possible that the payback period of 2 project is similar but the cash flow

generated from the project may be different. So it does not provide the accurate

information to invest in which project.

A shorter payback period does not implies the profitability of the project because it may

be possible that in end of the period the cash flow is decline due to certain drastic change

(Schaltegger and Burritt, 2017).

In the above calculation Average method is used to calculate the payback period but it

does not appropriate when the cash flow is different in life of the assets. So the

subtraction method is much more suitable for the company.

Average rate of return

Benefits

ARR method help the company to ascertain the profitability. In the above case the ARR of Happy

Meal limited company is 60% which indicate good position of company in market and also

suggest that they have to purchase the machine at the cost of £320000.

It is easy to calculate and understand by different users and stakeholders to take the decision of

investment (Brigham and et.al., 2016). It help to compare the different projects and machinery cost to evaluate the profitability of each

project.

Limitation

like the Payback period method it also ignore the time value of money which affect the

decision of top management or owner.

ARR only consider internal factor which affect the profitability but the external factor

also affect the profitability of the project.

It does not applicable when the investment in the project is done in instalment or several

parts.

Internal rate of return

Benefits

The IRR method does not require the hurdle rate to calculate the return and easy to

calculate.

As per the above case the IRR is 24% which is higher to it cost of capital 12%. It present

that by purchasing the machine Happy Meal limited company is able to generate higher

return. It also include the time value of money which help to present the accurate information

regarding the financial position of company.

Limitation

The biggest disadvantage of the IRR method is that it does not consider the size of the

project. It is difficult to compare the two project on the basis of IRR with different time

period (Pandey, 2015).

The IRR method ignores the future cost and only focus on the projected cash flow which

is generated by capital injection.

Net present value

Benefits

The NPV method includes the time value of money which indicate true and accurate

position of the company.

As per the above method the NPV of machinery is positive £58502. The positive NPV

present that Happy Meal limited company has to purchase the machinery.

It help the company to estimate the profitability and make the decision of investment in

the project that whether they have to purchase the machinery or not. It also help to

estimate the risk associated with the project (Kieso, Weygandt and Warfield, 2016). It is used to compare the project and identify that which project is more suitable for the

organisation.

Limitation

calculate.

As per the above case the IRR is 24% which is higher to it cost of capital 12%. It present

that by purchasing the machine Happy Meal limited company is able to generate higher

return. It also include the time value of money which help to present the accurate information

regarding the financial position of company.

Limitation

The biggest disadvantage of the IRR method is that it does not consider the size of the

project. It is difficult to compare the two project on the basis of IRR with different time

period (Pandey, 2015).

The IRR method ignores the future cost and only focus on the projected cash flow which

is generated by capital injection.

Net present value

Benefits

The NPV method includes the time value of money which indicate true and accurate

position of the company.

As per the above method the NPV of machinery is positive £58502. The positive NPV

present that Happy Meal limited company has to purchase the machinery.

It help the company to estimate the profitability and make the decision of investment in

the project that whether they have to purchase the machinery or not. It also help to

estimate the risk associated with the project (Kieso, Weygandt and Warfield, 2016). It is used to compare the project and identify that which project is more suitable for the

organisation.

Limitation

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.