Comprehensive Solution: Financial Management Assessment 2 - University

VerifiedAdded on 2023/06/05

|13

|1858

|443

Homework Assignment

AI Summary

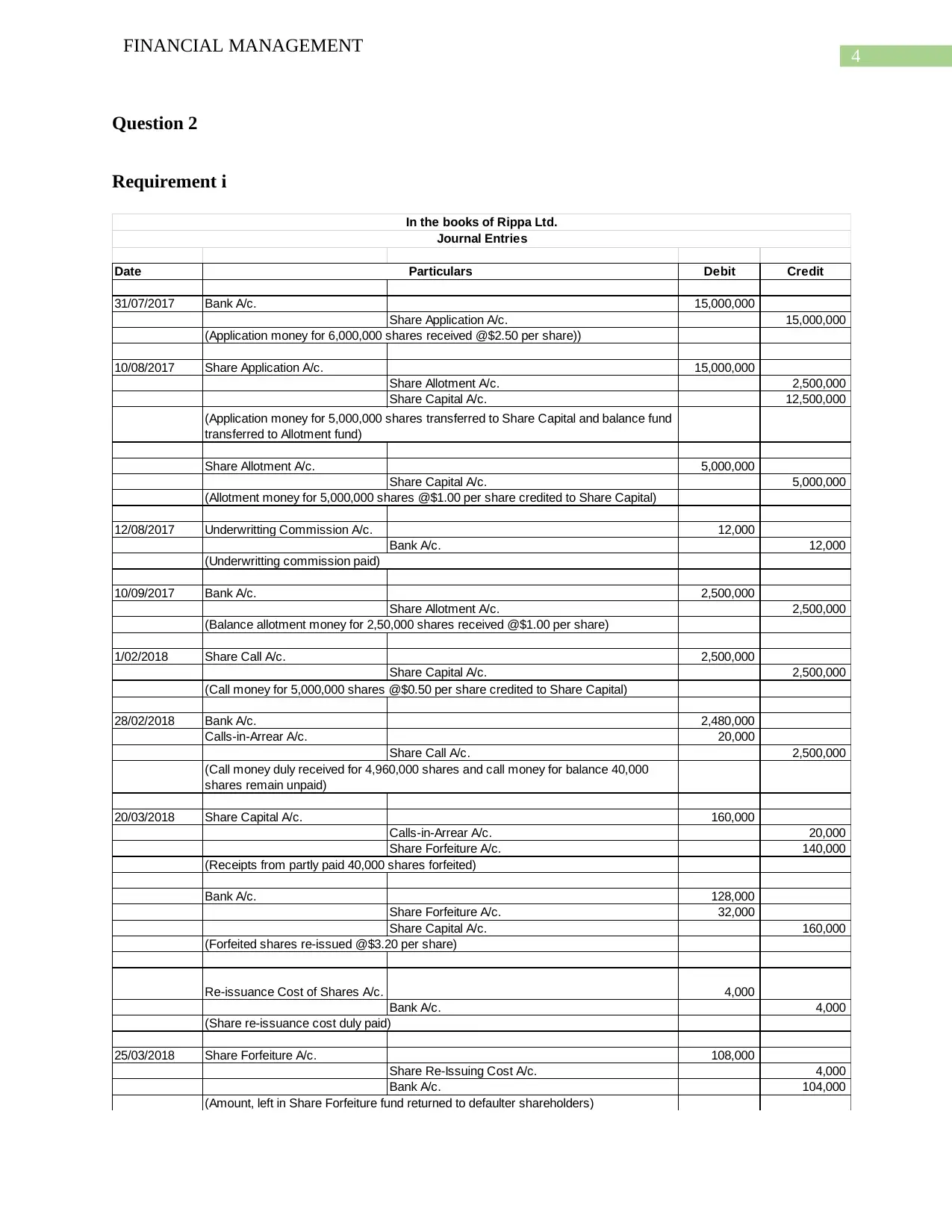

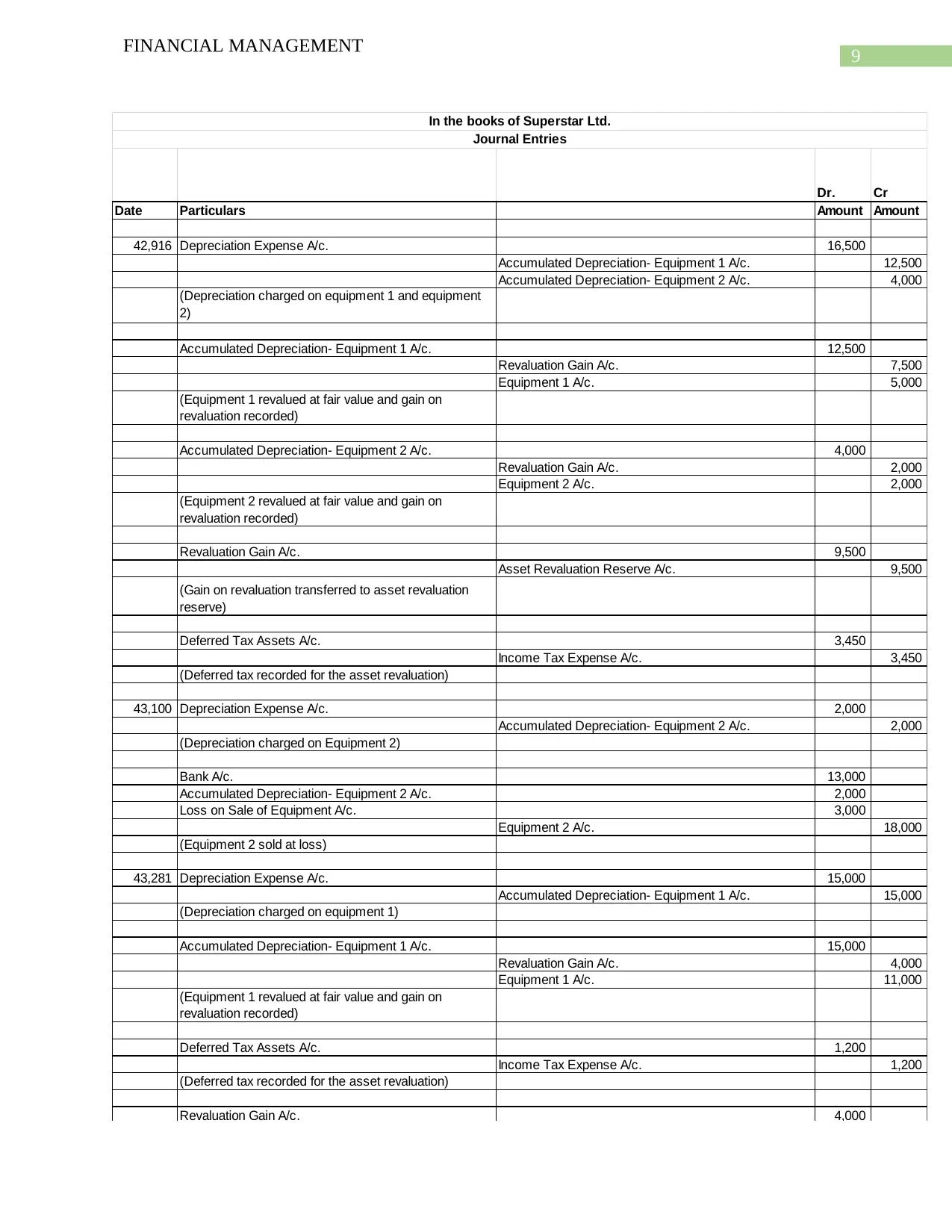

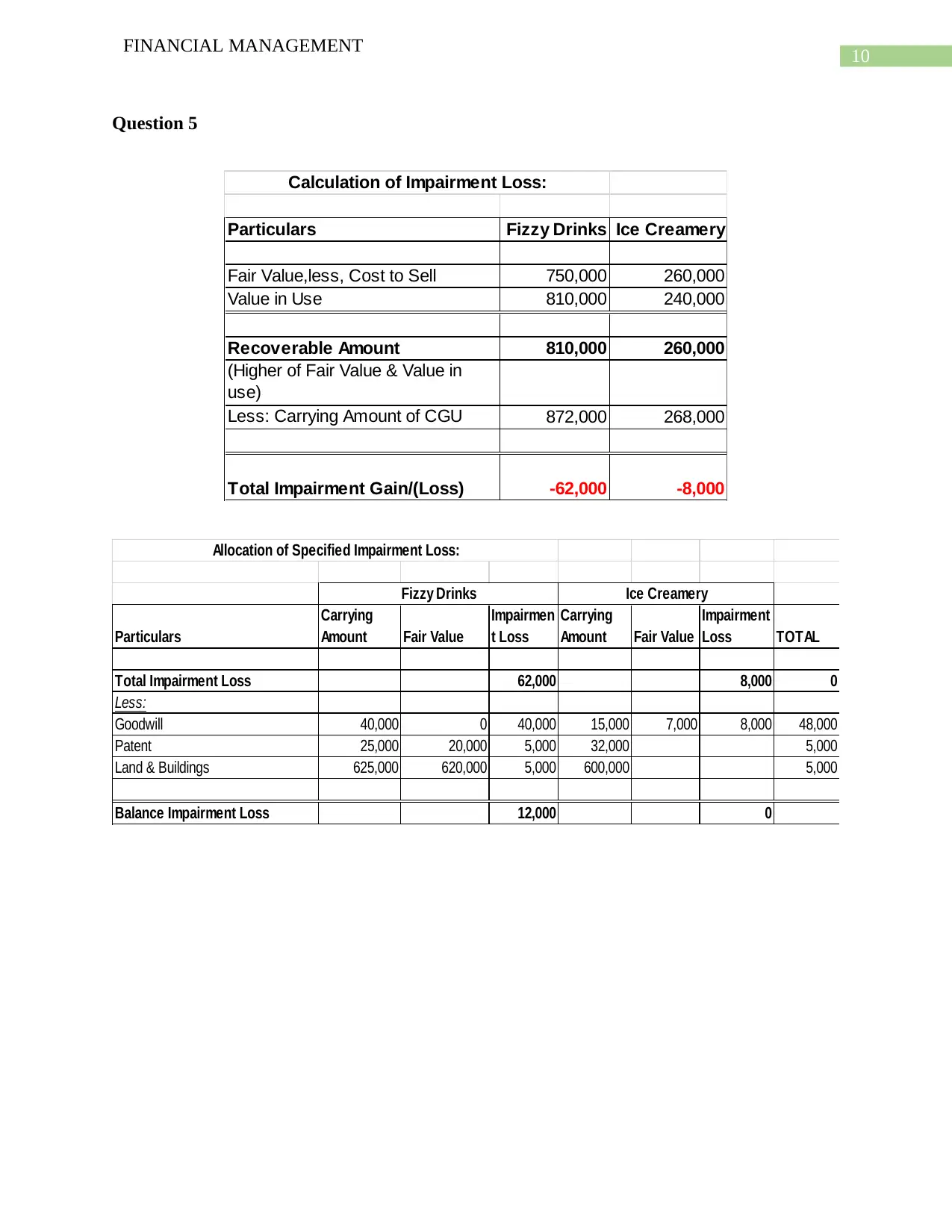

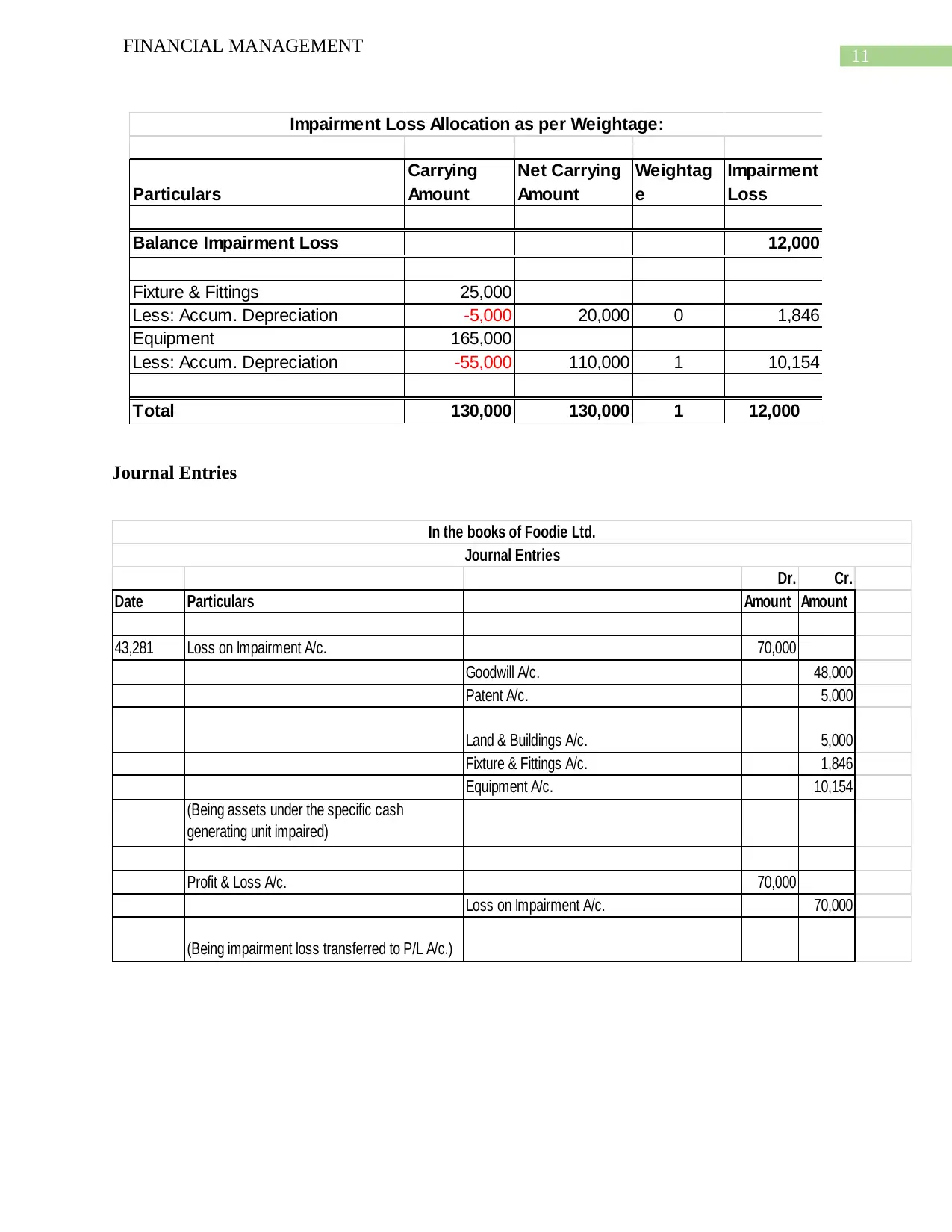

This document presents a comprehensive solution to a Financial Management assessment, addressing various accounting and financial reporting issues. The solution begins with an analysis of accounting estimates and the treatment of changes in useful asset life, followed by journal entries related to tax refunds, share price fluctuations, and incorrect expense recordings. It then delves into detailed journal entries for Rippa Ltd, covering share applications, allotments, underwriting commissions, and share forfeitures. The document further includes a current and deferred tax liability calculation, along with journal entries. It also provides a computation of revaluation gains/losses and deferred tax for Superstar Ltd, accompanied by the relevant journal entries. Finally, the solution concludes with an impairment loss calculation and allocation for Foodie Ltd, incorporating impairment loss journal entries.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.