Financial Management Assignment: APC308 Valuation and Investment

VerifiedAdded on 2023/01/10

|14

|3293

|31

Homework Assignment

AI Summary

This assignment solution addresses key concepts in financial management, including valuation techniques and investment appraisal methods. The first section provides a detailed analysis of the Price Earning (P/E) ratio, Dividend Valuation Method, and Discounted Cash Flow (DCF) method, explaining their formulas, applications, and interpretations. It includes calculations for P/E ratio, return on equity, and the application of the dividend valuation method to determine share prices, alongside a WACC calculation. The second part of the solution discusses the limitations and problems associated with each valuation technique, such as the reliance on accounting standards in the P/E ratio, the inability of the dividend valuation method to value non-dividend-paying companies, and the uncertainties in forecasting cash flows in the DCF model. The assignment concludes with an examination of investment appraisal techniques like payback period, accounting rate of return, net present value (NPV), and internal rate of return (IRR) with associated calculations and interpretations, providing a comprehensive overview of financial analysis and decision-making.

FINANCIAL MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 2

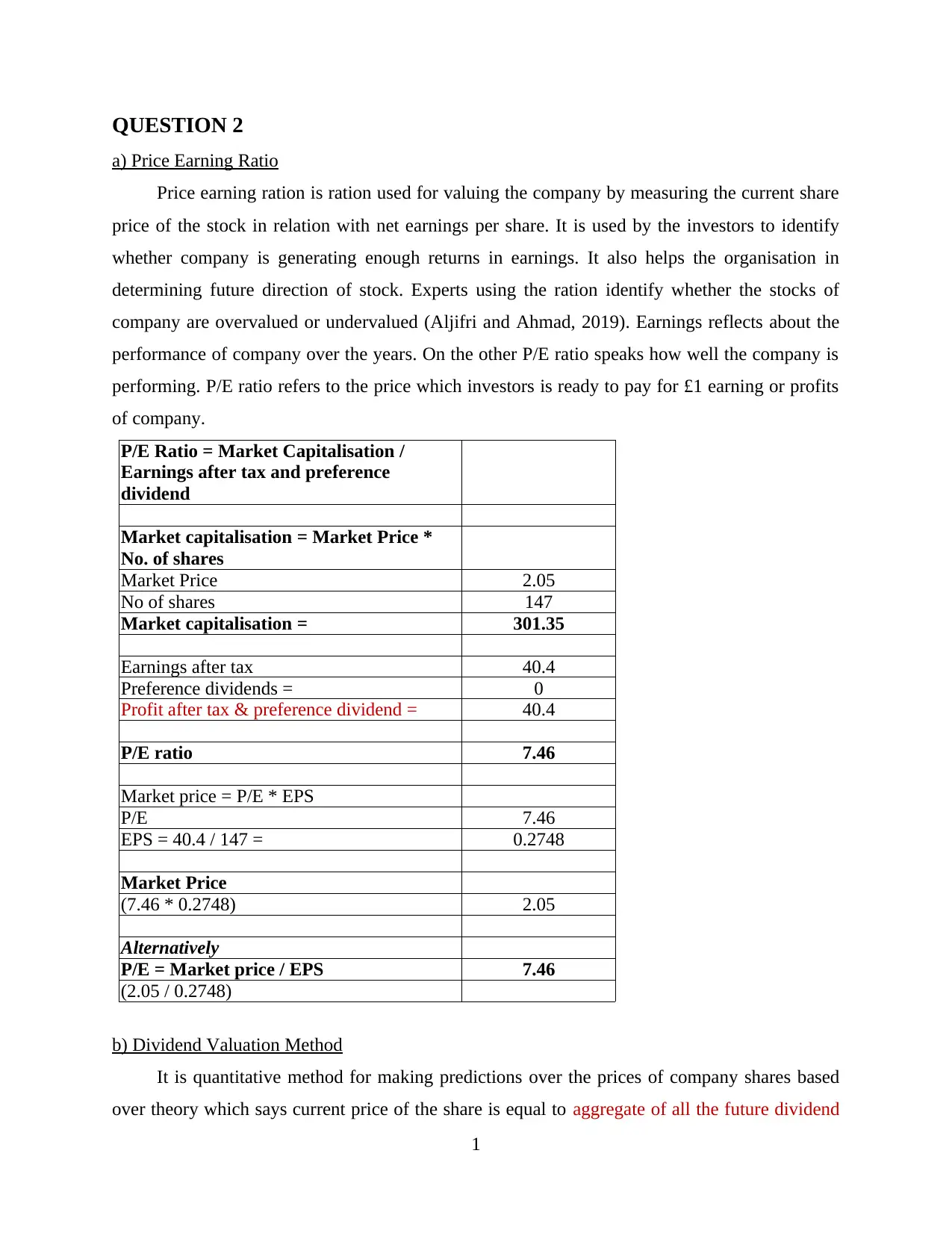

a) Price Earning Ratio

Price earning ration is ration used for valuing the company by measuring the current share

price of the stock in relation with net earnings per share. It is used by the investors to identify

whether company is generating enough returns in earnings. It also helps the organisation in

determining future direction of stock. Experts using the ration identify whether the stocks of

company are overvalued or undervalued (Aljifri and Ahmad, 2019). Earnings reflects about the

performance of company over the years. On the other P/E ratio speaks how well the company is

performing. P/E ratio refers to the price which investors is ready to pay for £1 earning or profits

of company.

P/E Ratio = Market Capitalisation /

Earnings after tax and preference

dividend

Market capitalisation = Market Price *

No. of shares

Market Price 2.05

No of shares 147

Market capitalisation = 301.35

Earnings after tax 40.4

Preference dividends = 0

Profit after tax & preference dividend = 40.4

P/E ratio 7.46

Market price = P/E * EPS

P/E 7.46

EPS = 40.4 / 147 = 0.2748

Market Price

(7.46 * 0.2748) 2.05

Alternatively

P/E = Market price / EPS 7.46

(2.05 / 0.2748)

b) Dividend Valuation Method

It is quantitative method for making predictions over the prices of company shares based

over theory which says current price of the share is equal to aggregate of all the future dividend

1

a) Price Earning Ratio

Price earning ration is ration used for valuing the company by measuring the current share

price of the stock in relation with net earnings per share. It is used by the investors to identify

whether company is generating enough returns in earnings. It also helps the organisation in

determining future direction of stock. Experts using the ration identify whether the stocks of

company are overvalued or undervalued (Aljifri and Ahmad, 2019). Earnings reflects about the

performance of company over the years. On the other P/E ratio speaks how well the company is

performing. P/E ratio refers to the price which investors is ready to pay for £1 earning or profits

of company.

P/E Ratio = Market Capitalisation /

Earnings after tax and preference

dividend

Market capitalisation = Market Price *

No. of shares

Market Price 2.05

No of shares 147

Market capitalisation = 301.35

Earnings after tax 40.4

Preference dividends = 0

Profit after tax & preference dividend = 40.4

P/E ratio 7.46

Market price = P/E * EPS

P/E 7.46

EPS = 40.4 / 147 = 0.2748

Market Price

(7.46 * 0.2748) 2.05

Alternatively

P/E = Market price / EPS 7.46

(2.05 / 0.2748)

b) Dividend Valuation Method

It is quantitative method for making predictions over the prices of company shares based

over theory which says current price of the share is equal to aggregate of all the future dividend

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

payments on discounting to the present value. This method attempts at calculating the value of

share irrespective of the prevailing conditions of the market & considers dividend payout factor

& the expected market return. Where values of the share using DDM is more than currently

trading prices of shares then stock is said to be undervalued. Investors tend to buy such securities

as these stocks have higher growth opportunities. The method is also known as dividend discount

model by the investors (Stancu, Ion and et.al.,). The method is highly effective in valuing the

stocks of firm to determine whether the investors should purchase or sell the securities.

Return on Equity 11.6

Re = Rf + (Rm – Rf) * Beta

5 + (11 – 5 ) * 1.1

Dividend Valuation method

Price = D1 / (Ke – g)

D1 0.1326

(0.13 +(0.13*2%))

Ke 11.60%

g 2.00%

Price = D1 / (Ke – g) 1.38

(0.1326 / (0.116 – 0.02)

c) Discounting cash flow method

It is valuation method used for estimating value of the investments based over future cash

flows. DCF calculates the current value of the investment based over future projections over the

future cash flows from firm. The method is used by investors for financial investments and also

by business owners that are planning to do changes to the business like purchase of new

equipment. PV of the expected future inflows is arrived using a discounting rate for calculating

the discounted cash flows. Under this method when discounted cash flows are higher than

current investment cost, opportunity will be resulting in the positive returns. Discounting rate is

taken as weighted average COC for discounting the cash flows considering expected returns by

the shareholders.

Discounted cash flow method

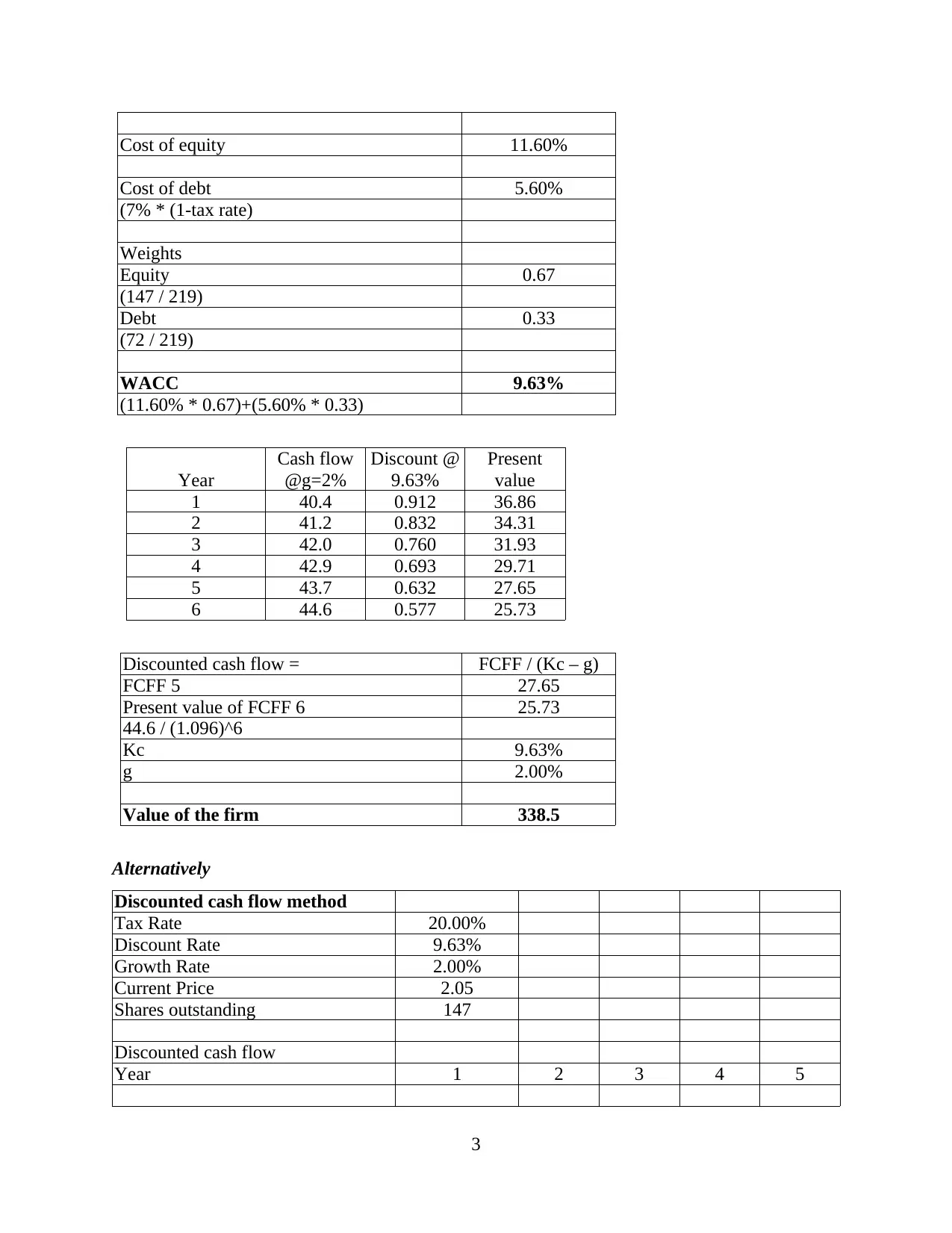

WACC

2

share irrespective of the prevailing conditions of the market & considers dividend payout factor

& the expected market return. Where values of the share using DDM is more than currently

trading prices of shares then stock is said to be undervalued. Investors tend to buy such securities

as these stocks have higher growth opportunities. The method is also known as dividend discount

model by the investors (Stancu, Ion and et.al.,). The method is highly effective in valuing the

stocks of firm to determine whether the investors should purchase or sell the securities.

Return on Equity 11.6

Re = Rf + (Rm – Rf) * Beta

5 + (11 – 5 ) * 1.1

Dividend Valuation method

Price = D1 / (Ke – g)

D1 0.1326

(0.13 +(0.13*2%))

Ke 11.60%

g 2.00%

Price = D1 / (Ke – g) 1.38

(0.1326 / (0.116 – 0.02)

c) Discounting cash flow method

It is valuation method used for estimating value of the investments based over future cash

flows. DCF calculates the current value of the investment based over future projections over the

future cash flows from firm. The method is used by investors for financial investments and also

by business owners that are planning to do changes to the business like purchase of new

equipment. PV of the expected future inflows is arrived using a discounting rate for calculating

the discounted cash flows. Under this method when discounted cash flows are higher than

current investment cost, opportunity will be resulting in the positive returns. Discounting rate is

taken as weighted average COC for discounting the cash flows considering expected returns by

the shareholders.

Discounted cash flow method

WACC

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Cost of equity 11.60%

Cost of debt 5.60%

(7% * (1-tax rate)

Weights

Equity 0.67

(147 / 219)

Debt 0.33

(72 / 219)

WACC 9.63%

(11.60% * 0.67)+(5.60% * 0.33)

Year

Cash flow

@g=2%

Discount @

9.63%

Present

value

1 40.4 0.912 36.86

2 41.2 0.832 34.31

3 42.0 0.760 31.93

4 42.9 0.693 29.71

5 43.7 0.632 27.65

6 44.6 0.577 25.73

Discounted cash flow = FCFF / (Kc – g)

FCFF 5 27.65

Present value of FCFF 6 25.73

44.6 / (1.096)^6

Kc 9.63%

g 2.00%

Value of the firm 338.5

Alternatively

Discounted cash flow method

Tax Rate 20.00%

Discount Rate 9.63%

Growth Rate 2.00%

Current Price 2.05

Shares outstanding 147

Discounted cash flow

Year 1 2 3 4 5

3

Cost of debt 5.60%

(7% * (1-tax rate)

Weights

Equity 0.67

(147 / 219)

Debt 0.33

(72 / 219)

WACC 9.63%

(11.60% * 0.67)+(5.60% * 0.33)

Year

Cash flow

@g=2%

Discount @

9.63%

Present

value

1 40.4 0.912 36.86

2 41.2 0.832 34.31

3 42.0 0.760 31.93

4 42.9 0.693 29.71

5 43.7 0.632 27.65

6 44.6 0.577 25.73

Discounted cash flow = FCFF / (Kc – g)

FCFF 5 27.65

Present value of FCFF 6 25.73

44.6 / (1.096)^6

Kc 9.63%

g 2.00%

Value of the firm 338.5

Alternatively

Discounted cash flow method

Tax Rate 20.00%

Discount Rate 9.63%

Growth Rate 2.00%

Current Price 2.05

Shares outstanding 147

Discounted cash flow

Year 1 2 3 4 5

3

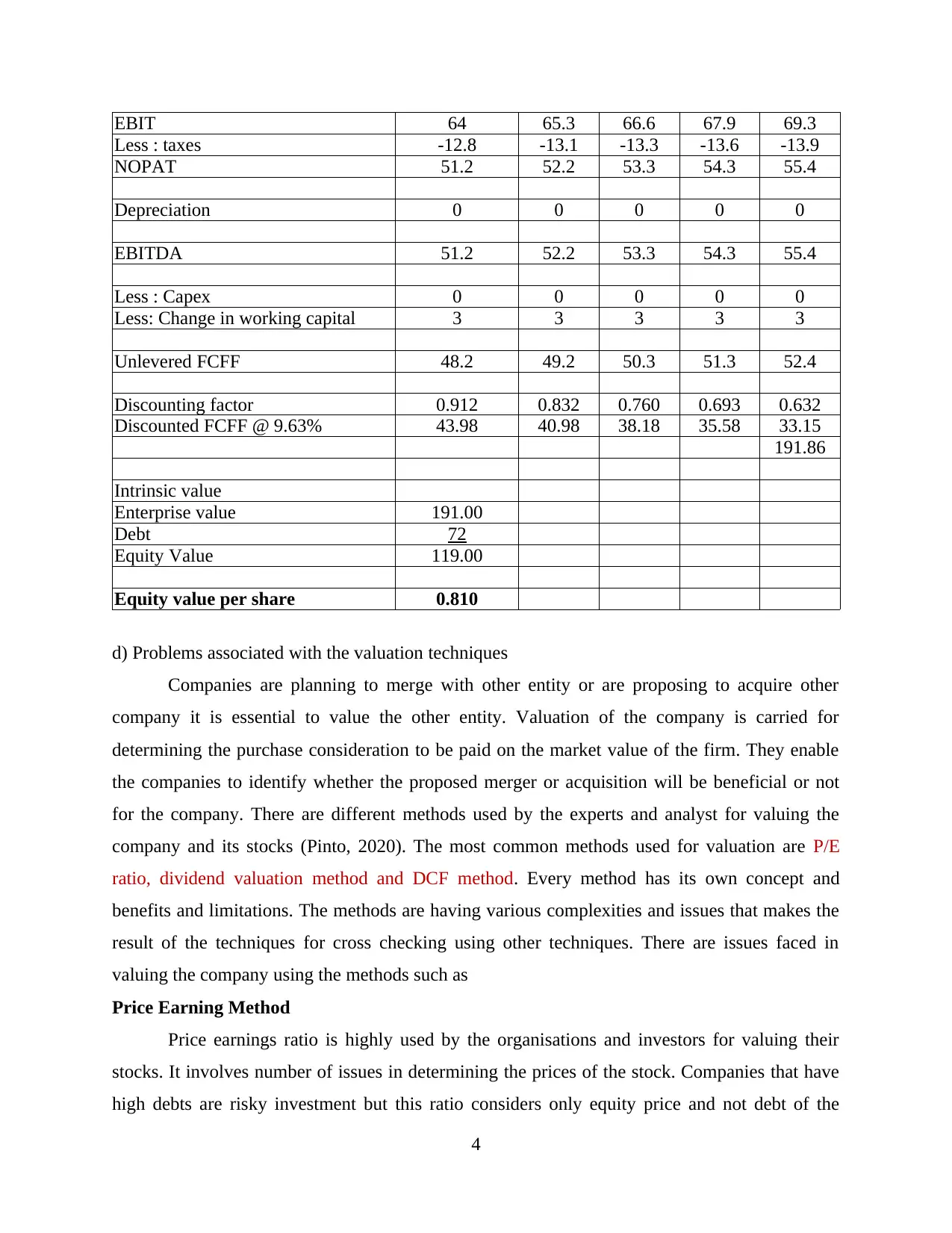

EBIT 64 65.3 66.6 67.9 69.3

Less : taxes -12.8 -13.1 -13.3 -13.6 -13.9

NOPAT 51.2 52.2 53.3 54.3 55.4

Depreciation 0 0 0 0 0

EBITDA 51.2 52.2 53.3 54.3 55.4

Less : Capex 0 0 0 0 0

Less: Change in working capital 3 3 3 3 3

Unlevered FCFF 48.2 49.2 50.3 51.3 52.4

Discounting factor 0.912 0.832 0.760 0.693 0.632

Discounted FCFF @ 9.63% 43.98 40.98 38.18 35.58 33.15

191.86

Intrinsic value

Enterprise value 191.00

Debt 72

Equity Value 119.00

Equity value per share 0.810

d) Problems associated with the valuation techniques

Companies are planning to merge with other entity or are proposing to acquire other

company it is essential to value the other entity. Valuation of the company is carried for

determining the purchase consideration to be paid on the market value of the firm. They enable

the companies to identify whether the proposed merger or acquisition will be beneficial or not

for the company. There are different methods used by the experts and analyst for valuing the

company and its stocks (Pinto, 2020). The most common methods used for valuation are P/E

ratio, dividend valuation method and DCF method. Every method has its own concept and

benefits and limitations. The methods are having various complexities and issues that makes the

result of the techniques for cross checking using other techniques. There are issues faced in

valuing the company using the methods such as

Price Earning Method

Price earnings ratio is highly used by the organisations and investors for valuing their

stocks. It involves number of issues in determining the prices of the stock. Companies that have

high debts are risky investment but this ratio considers only equity price and not debt of the

4

Less : taxes -12.8 -13.1 -13.3 -13.6 -13.9

NOPAT 51.2 52.2 53.3 54.3 55.4

Depreciation 0 0 0 0 0

EBITDA 51.2 52.2 53.3 54.3 55.4

Less : Capex 0 0 0 0 0

Less: Change in working capital 3 3 3 3 3

Unlevered FCFF 48.2 49.2 50.3 51.3 52.4

Discounting factor 0.912 0.832 0.760 0.693 0.632

Discounted FCFF @ 9.63% 43.98 40.98 38.18 35.58 33.15

191.86

Intrinsic value

Enterprise value 191.00

Debt 72

Equity Value 119.00

Equity value per share 0.810

d) Problems associated with the valuation techniques

Companies are planning to merge with other entity or are proposing to acquire other

company it is essential to value the other entity. Valuation of the company is carried for

determining the purchase consideration to be paid on the market value of the firm. They enable

the companies to identify whether the proposed merger or acquisition will be beneficial or not

for the company. There are different methods used by the experts and analyst for valuing the

company and its stocks (Pinto, 2020). The most common methods used for valuation are P/E

ratio, dividend valuation method and DCF method. Every method has its own concept and

benefits and limitations. The methods are having various complexities and issues that makes the

result of the techniques for cross checking using other techniques. There are issues faced in

valuing the company using the methods such as

Price Earning Method

Price earnings ratio is highly used by the organisations and investors for valuing their

stocks. It involves number of issues in determining the prices of the stock. Companies that have

high debts are risky investment but this ratio considers only equity price and not debt of the

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

company. It is the most serious issue is earnings of the company are defined by accounting

standards for specific country. It does not accounts cash earnings and company may show

earnings even they have no reporting profits. In this model future earnings of the company will

be remaining at least as that of current earnings. Estimating earnings of listed companies is very

difficult for more than one year. It is based over assumptions that current earnings will be earned

for next ten years and investors will be getting money back which is theoretical concept not

applying to the real world. It is not able to provide the reliable estimates about the future

earnings or stock prices of the entity. Earnings of the company could go significantly up or down

over the years and could not estimate the earnings accurately. Investors could not identify the

position of the company using P/E ratio it only tells about the profitability and nothing about

capital structure and risks involved in the company (Allee, and et.al., 2020). Companies may

seem profitable from the reported earnings but may be suffering liquidity issues. As companies

facing serious liquidity issues could go bankrupt in the future causing significant losses to the

investors. However the method is highly used by companies to make management decisions for

growth and performance of business.

Dividend Valuation

Downside of using dividend discount model involves difficulty of making accurate

projections and does not factor in buybacks. One of the significant limitations of the model is

that it could be used only for the companies that are paying dividend over the rising rate. It could

not make valuation for companies not paying dividends. The method is considered very

conservative as it does not takes into consideration buy back of the stocks. Value to the stock is

assigned in DDM using discounted cash flow method for determining current value of future

dividends. Where the value determined using the model is higher from current stock prices then

the share is considered undervalued from their actual worth and investors are suggested to make

buy decisions. It is helpful in estimating potential income from dividend despite of number of

drawbacks.

Discounted Cash Flow method

DCF model is powerful and have various benefits but also have shortcomings

Most essential part in DCF is estimating the future cash flows. Various issues are faced in

estimating the cash flows as various inherent problems are existing in the earnings and

forecasting of cash flows which could be generated by company. Uncertainty in the cash flows

5

standards for specific country. It does not accounts cash earnings and company may show

earnings even they have no reporting profits. In this model future earnings of the company will

be remaining at least as that of current earnings. Estimating earnings of listed companies is very

difficult for more than one year. It is based over assumptions that current earnings will be earned

for next ten years and investors will be getting money back which is theoretical concept not

applying to the real world. It is not able to provide the reliable estimates about the future

earnings or stock prices of the entity. Earnings of the company could go significantly up or down

over the years and could not estimate the earnings accurately. Investors could not identify the

position of the company using P/E ratio it only tells about the profitability and nothing about

capital structure and risks involved in the company (Allee, and et.al., 2020). Companies may

seem profitable from the reported earnings but may be suffering liquidity issues. As companies

facing serious liquidity issues could go bankrupt in the future causing significant losses to the

investors. However the method is highly used by companies to make management decisions for

growth and performance of business.

Dividend Valuation

Downside of using dividend discount model involves difficulty of making accurate

projections and does not factor in buybacks. One of the significant limitations of the model is

that it could be used only for the companies that are paying dividend over the rising rate. It could

not make valuation for companies not paying dividends. The method is considered very

conservative as it does not takes into consideration buy back of the stocks. Value to the stock is

assigned in DDM using discounted cash flow method for determining current value of future

dividends. Where the value determined using the model is higher from current stock prices then

the share is considered undervalued from their actual worth and investors are suggested to make

buy decisions. It is helpful in estimating potential income from dividend despite of number of

drawbacks.

Discounted Cash Flow method

DCF model is powerful and have various benefits but also have shortcomings

Most essential part in DCF is estimating the future cash flows. Various issues are faced in

estimating the cash flows as various inherent problems are existing in the earnings and

forecasting of cash flows which could be generated by company. Uncertainty in the cash flows

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

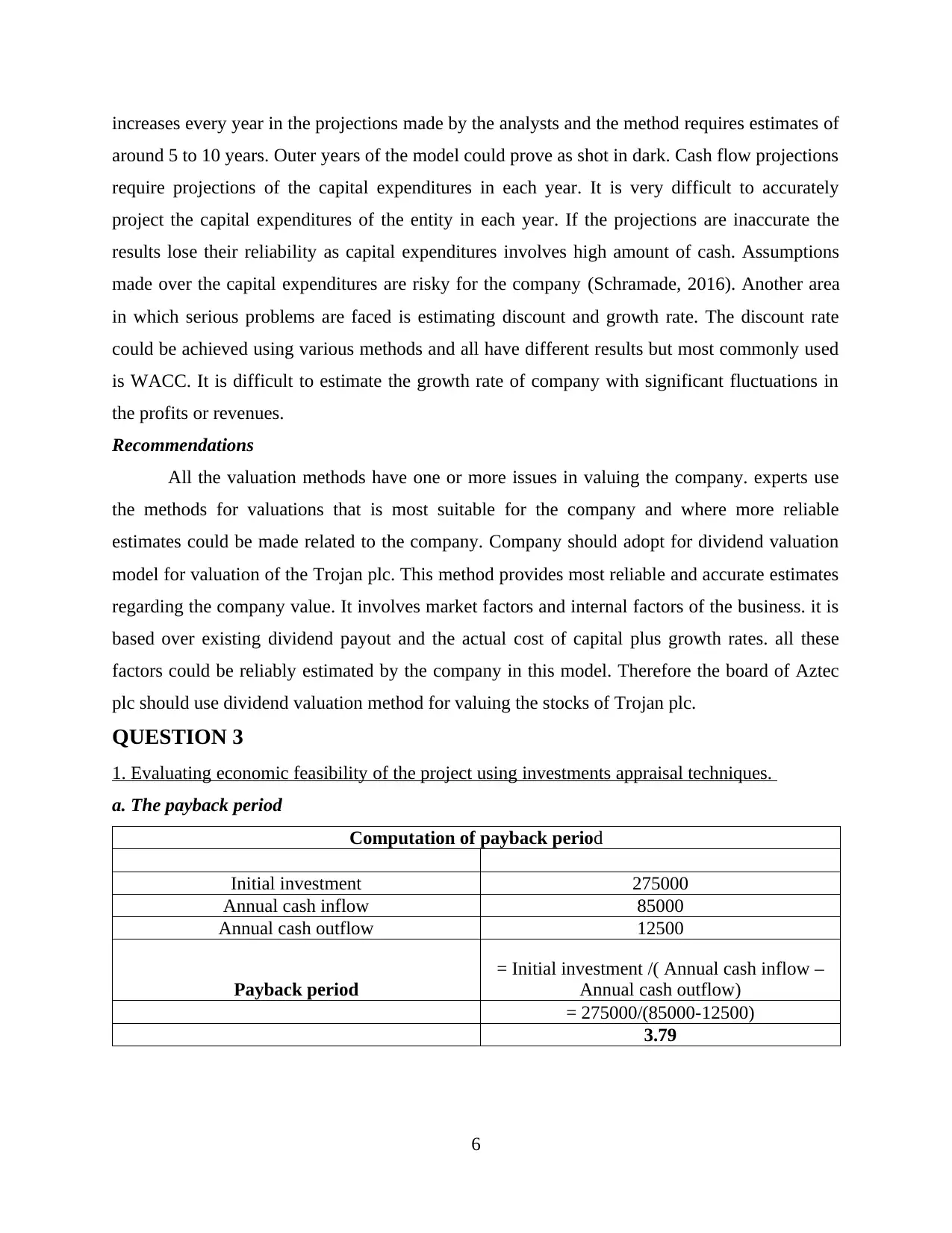

increases every year in the projections made by the analysts and the method requires estimates of

around 5 to 10 years. Outer years of the model could prove as shot in dark. Cash flow projections

require projections of the capital expenditures in each year. It is very difficult to accurately

project the capital expenditures of the entity in each year. If the projections are inaccurate the

results lose their reliability as capital expenditures involves high amount of cash. Assumptions

made over the capital expenditures are risky for the company (Schramade, 2016). Another area

in which serious problems are faced is estimating discount and growth rate. The discount rate

could be achieved using various methods and all have different results but most commonly used

is WACC. It is difficult to estimate the growth rate of company with significant fluctuations in

the profits or revenues.

Recommendations

All the valuation methods have one or more issues in valuing the company. experts use

the methods for valuations that is most suitable for the company and where more reliable

estimates could be made related to the company. Company should adopt for dividend valuation

model for valuation of the Trojan plc. This method provides most reliable and accurate estimates

regarding the company value. It involves market factors and internal factors of the business. it is

based over existing dividend payout and the actual cost of capital plus growth rates. all these

factors could be reliably estimated by the company in this model. Therefore the board of Aztec

plc should use dividend valuation method for valuing the stocks of Trojan plc.

QUESTION 3

1. Evaluating economic feasibility of the project using investments appraisal techniques.

a. The payback period

Computation of payback period

Initial investment 275000

Annual cash inflow 85000

Annual cash outflow 12500

Payback period

= Initial investment /( Annual cash inflow –

Annual cash outflow)

= 275000/(85000-12500)

3.79

6

around 5 to 10 years. Outer years of the model could prove as shot in dark. Cash flow projections

require projections of the capital expenditures in each year. It is very difficult to accurately

project the capital expenditures of the entity in each year. If the projections are inaccurate the

results lose their reliability as capital expenditures involves high amount of cash. Assumptions

made over the capital expenditures are risky for the company (Schramade, 2016). Another area

in which serious problems are faced is estimating discount and growth rate. The discount rate

could be achieved using various methods and all have different results but most commonly used

is WACC. It is difficult to estimate the growth rate of company with significant fluctuations in

the profits or revenues.

Recommendations

All the valuation methods have one or more issues in valuing the company. experts use

the methods for valuations that is most suitable for the company and where more reliable

estimates could be made related to the company. Company should adopt for dividend valuation

model for valuation of the Trojan plc. This method provides most reliable and accurate estimates

regarding the company value. It involves market factors and internal factors of the business. it is

based over existing dividend payout and the actual cost of capital plus growth rates. all these

factors could be reliably estimated by the company in this model. Therefore the board of Aztec

plc should use dividend valuation method for valuing the stocks of Trojan plc.

QUESTION 3

1. Evaluating economic feasibility of the project using investments appraisal techniques.

a. The payback period

Computation of payback period

Initial investment 275000

Annual cash inflow 85000

Annual cash outflow 12500

Payback period

= Initial investment /( Annual cash inflow –

Annual cash outflow)

= 275000/(85000-12500)

3.79

6

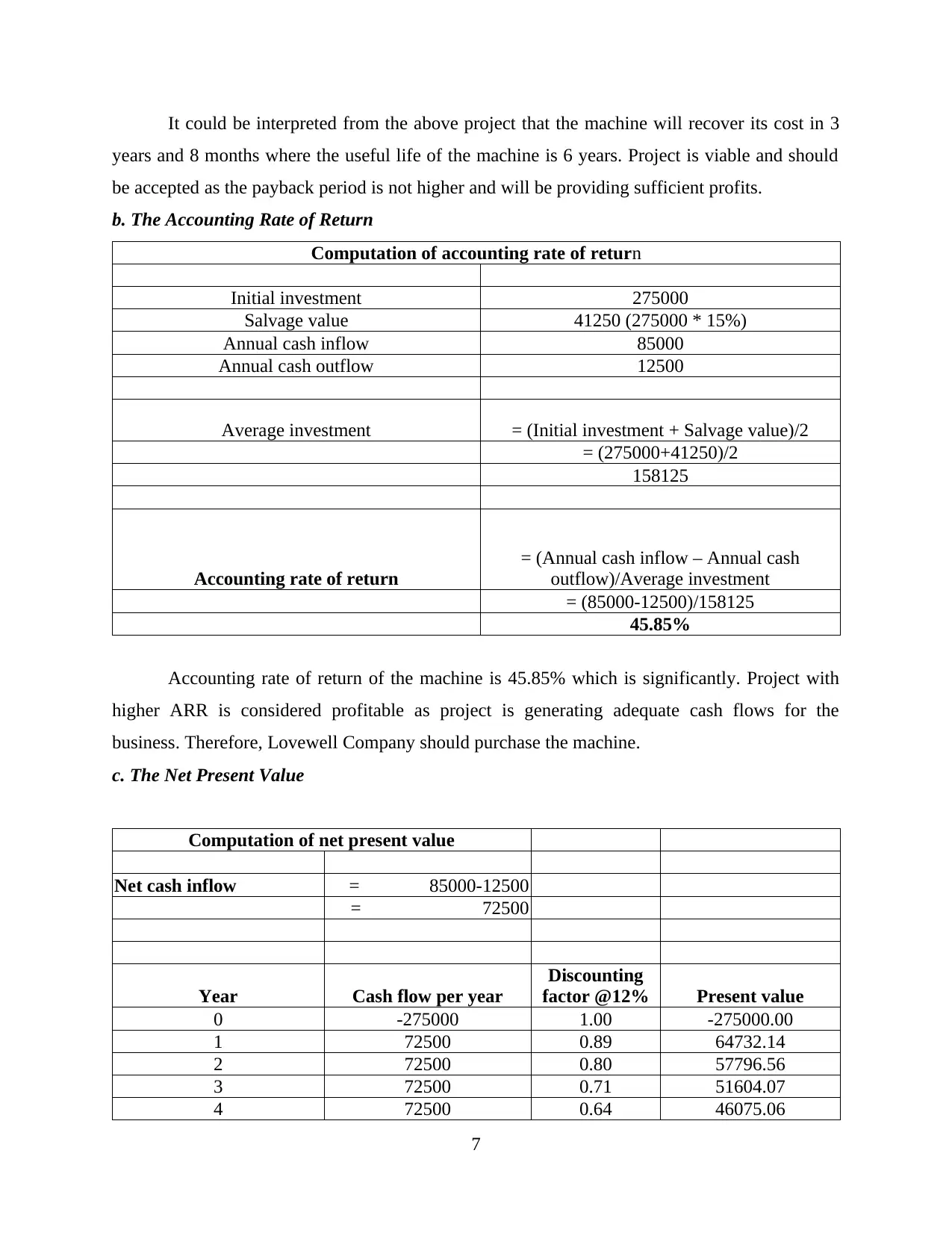

It could be interpreted from the above project that the machine will recover its cost in 3

years and 8 months where the useful life of the machine is 6 years. Project is viable and should

be accepted as the payback period is not higher and will be providing sufficient profits.

b. The Accounting Rate of Return

Computation of accounting rate of return

Initial investment 275000

Salvage value 41250 (275000 * 15%)

Annual cash inflow 85000

Annual cash outflow 12500

Average investment = (Initial investment + Salvage value)/2

= (275000+41250)/2

158125

Accounting rate of return

= (Annual cash inflow – Annual cash

outflow)/Average investment

= (85000-12500)/158125

45.85%

Accounting rate of return of the machine is 45.85% which is significantly. Project with

higher ARR is considered profitable as project is generating adequate cash flows for the

business. Therefore, Lovewell Company should purchase the machine.

c. The Net Present Value

Computation of net present value

Net cash inflow = 85000-12500

= 72500

Year Cash flow per year

Discounting

factor @12% Present value

0 -275000 1.00 -275000.00

1 72500 0.89 64732.14

2 72500 0.80 57796.56

3 72500 0.71 51604.07

4 72500 0.64 46075.06

7

years and 8 months where the useful life of the machine is 6 years. Project is viable and should

be accepted as the payback period is not higher and will be providing sufficient profits.

b. The Accounting Rate of Return

Computation of accounting rate of return

Initial investment 275000

Salvage value 41250 (275000 * 15%)

Annual cash inflow 85000

Annual cash outflow 12500

Average investment = (Initial investment + Salvage value)/2

= (275000+41250)/2

158125

Accounting rate of return

= (Annual cash inflow – Annual cash

outflow)/Average investment

= (85000-12500)/158125

45.85%

Accounting rate of return of the machine is 45.85% which is significantly. Project with

higher ARR is considered profitable as project is generating adequate cash flows for the

business. Therefore, Lovewell Company should purchase the machine.

c. The Net Present Value

Computation of net present value

Net cash inflow = 85000-12500

= 72500

Year Cash flow per year

Discounting

factor @12% Present value

0 -275000 1.00 -275000.00

1 72500 0.89 64732.14

2 72500 0.80 57796.56

3 72500 0.71 51604.07

4 72500 0.64 46075.06

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

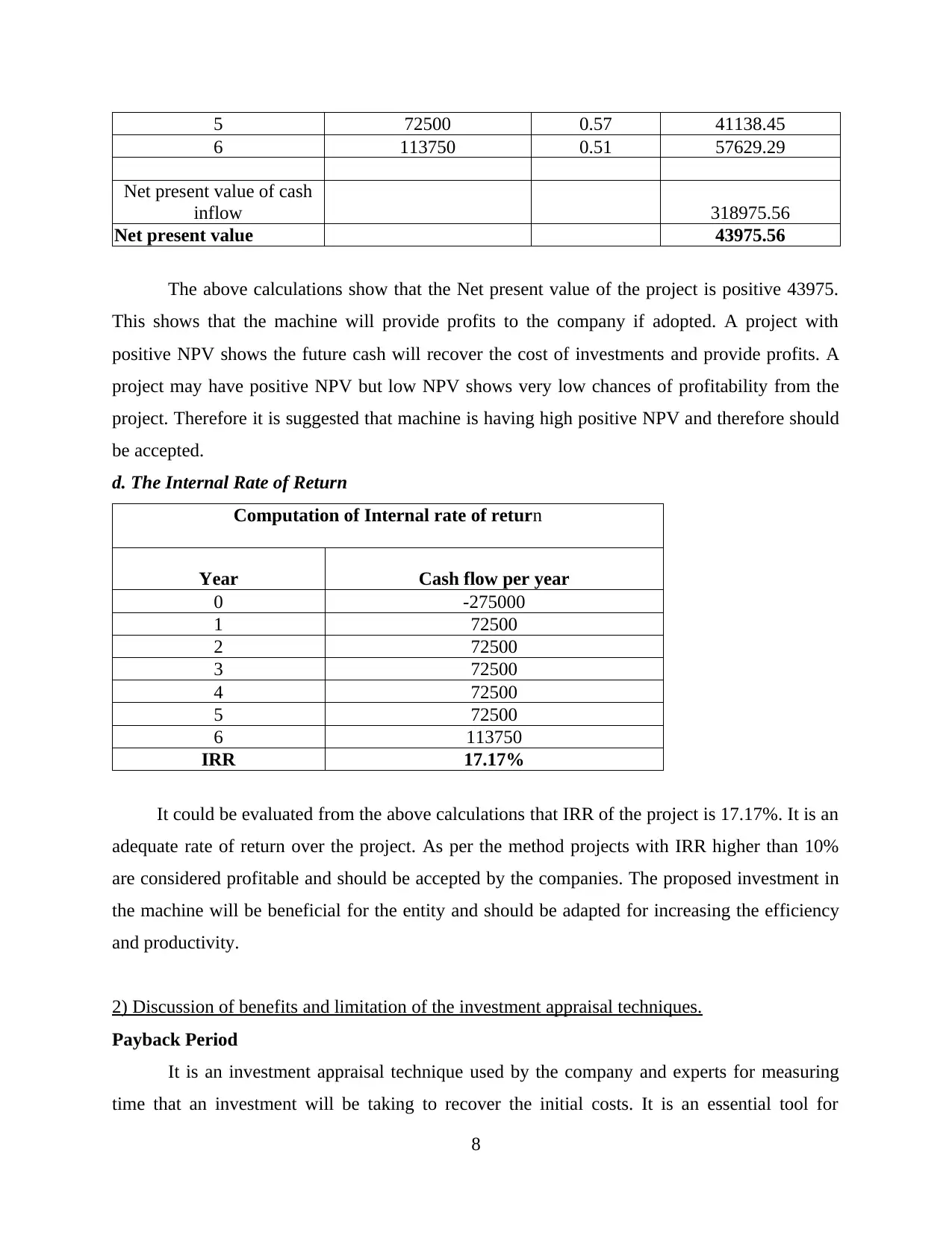

5 72500 0.57 41138.45

6 113750 0.51 57629.29

Net present value of cash

inflow 318975.56

Net present value 43975.56

The above calculations show that the Net present value of the project is positive 43975.

This shows that the machine will provide profits to the company if adopted. A project with

positive NPV shows the future cash will recover the cost of investments and provide profits. A

project may have positive NPV but low NPV shows very low chances of profitability from the

project. Therefore it is suggested that machine is having high positive NPV and therefore should

be accepted.

d. The Internal Rate of Return

Computation of Internal rate of return

Year Cash flow per year

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 113750

IRR 17.17%

It could be evaluated from the above calculations that IRR of the project is 17.17%. It is an

adequate rate of return over the project. As per the method projects with IRR higher than 10%

are considered profitable and should be accepted by the companies. The proposed investment in

the machine will be beneficial for the entity and should be adapted for increasing the efficiency

and productivity.

2) Discussion of benefits and limitation of the investment appraisal techniques.

Payback Period

It is an investment appraisal technique used by the company and experts for measuring

time that an investment will be taking to recover the initial costs. It is an essential tool for

8

6 113750 0.51 57629.29

Net present value of cash

inflow 318975.56

Net present value 43975.56

The above calculations show that the Net present value of the project is positive 43975.

This shows that the machine will provide profits to the company if adopted. A project with

positive NPV shows the future cash will recover the cost of investments and provide profits. A

project may have positive NPV but low NPV shows very low chances of profitability from the

project. Therefore it is suggested that machine is having high positive NPV and therefore should

be accepted.

d. The Internal Rate of Return

Computation of Internal rate of return

Year Cash flow per year

0 -275000

1 72500

2 72500

3 72500

4 72500

5 72500

6 113750

IRR 17.17%

It could be evaluated from the above calculations that IRR of the project is 17.17%. It is an

adequate rate of return over the project. As per the method projects with IRR higher than 10%

are considered profitable and should be accepted by the companies. The proposed investment in

the machine will be beneficial for the entity and should be adapted for increasing the efficiency

and productivity.

2) Discussion of benefits and limitation of the investment appraisal techniques.

Payback Period

It is an investment appraisal technique used by the company and experts for measuring

time that an investment will be taking to recover the initial costs. It is an essential tool for

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

identifying whether the investment will be covering the cost from within the useful life of assets.

Projects that have shorter payback period are considered acceptable by the business. It is also

known as the break even analysis that identifies the time after which it will be earning profits for

the business after recovering the costs of investments (Kengatharan and Nurullah, 2018).

Projects with higher projects should not be accepted as they do not allow the company to earn

adequate profits.

Benefits

This method uses very few inputs for calculating the profitability of investment. It could

identify the time within which it will be recovering the cost of investment. This provides the

management with more reliable estimate about the proposed investment project it is planning to

adopt. It is easy and simple method that does not requires complex calculations. It provides the

break even point after it will be earning the required profits.

Limitations

This method do not consider time factor in the calculation of payback period. Cash flows

of later years have higher weights which makes the decisions confusing. It does not cover the

cash flows after initial costs of the investment. This approach ignores profitability of the

investments.

ARR

It is an accounting ratio used by management for identifying the rate of return over

investments. This is also recognised as the average rate of return. It calculates the return

generated by the net income of proposed capital projects. This calculate return in percentage

terms. This is calculated for identifying whether the proposed investment is generating the

required rate of return on investments or not (Higham, Fortune and Boothman, 2016).

Management should not adopt the investments with lower rate of return as company will not be

able to earn sufficient profits after recovering cost of investments. It is a useful for identifying

the viability and comparing the rate of different investments.

Benefits

This is an easy method used for estimating the profitability of the investments it is

planning to adopt. Method facilitates comparison of the different projects on the basis of

competitive nature. It recognises net earnings which is vital aspect in the appraisal of the project.

9

Projects that have shorter payback period are considered acceptable by the business. It is also

known as the break even analysis that identifies the time after which it will be earning profits for

the business after recovering the costs of investments (Kengatharan and Nurullah, 2018).

Projects with higher projects should not be accepted as they do not allow the company to earn

adequate profits.

Benefits

This method uses very few inputs for calculating the profitability of investment. It could

identify the time within which it will be recovering the cost of investment. This provides the

management with more reliable estimate about the proposed investment project it is planning to

adopt. It is easy and simple method that does not requires complex calculations. It provides the

break even point after it will be earning the required profits.

Limitations

This method do not consider time factor in the calculation of payback period. Cash flows

of later years have higher weights which makes the decisions confusing. It does not cover the

cash flows after initial costs of the investment. This approach ignores profitability of the

investments.

ARR

It is an accounting ratio used by management for identifying the rate of return over

investments. This is also recognised as the average rate of return. It calculates the return

generated by the net income of proposed capital projects. This calculate return in percentage

terms. This is calculated for identifying whether the proposed investment is generating the

required rate of return on investments or not (Higham, Fortune and Boothman, 2016).

Management should not adopt the investments with lower rate of return as company will not be

able to earn sufficient profits after recovering cost of investments. It is a useful for identifying

the viability and comparing the rate of different investments.

Benefits

This is an easy method used for estimating the profitability of the investments it is

planning to adopt. Method facilitates comparison of the different projects on the basis of

competitive nature. It recognises net earnings which is vital aspect in the appraisal of the project.

9

This is the only method considering accounting profit for measuring the profitability of

investments.

Limitations

This method does not consider time value factor like IRR which is crucial in investment

appraisal techniques. The method do not considers cash inflows that are important for identifying

the viability of investments.

Net Present Value

This is a method used for checking the viability and feasibility of investments. It enables

the management to decide the investment or project with positive NPV and earn the desired

profits. It refers to the variation between present values of cash flows and PV of cash inflows. It

makes the company to identify whether cash flows generated from project are sufficient for

meeting cost of investment (Elmassri, Harris and Carter, 2016). This is used for comparing

different projects to choose project with high positive NPV. This approach is highly used by the

experts and analysts to analyse the profitability of project or investment. Project with negative

represents that cash flows are not enough to recover the cost of project and it may suffer losses

adopting the said technique.

Benefits

This method considers time value factor in calculating the profitability of investments

that provides current value of projected future CFs. This method accepts the conventional cash

flow patterns. The investment technique consider all the cash flows generated by project

(Nnamani, 2016). It provides more reliable estimate of the profitability of the investments

considering the factors risks associated with the project. If the NPV of the project is negative it

will not be providing required profits.

Limitations

The method though provides reliable estimates are difficult and time consuming. This

method does not provide any guidelines over calculation of the return rate required by the

investors. The technique could not be used for comparing the projects with different size. It does

not present profitability in terms of percentage which makes it difficult to make reliable

decisions from the outcomes.

IRR

10

investments.

Limitations

This method does not consider time value factor like IRR which is crucial in investment

appraisal techniques. The method do not considers cash inflows that are important for identifying

the viability of investments.

Net Present Value

This is a method used for checking the viability and feasibility of investments. It enables

the management to decide the investment or project with positive NPV and earn the desired

profits. It refers to the variation between present values of cash flows and PV of cash inflows. It

makes the company to identify whether cash flows generated from project are sufficient for

meeting cost of investment (Elmassri, Harris and Carter, 2016). This is used for comparing

different projects to choose project with high positive NPV. This approach is highly used by the

experts and analysts to analyse the profitability of project or investment. Project with negative

represents that cash flows are not enough to recover the cost of project and it may suffer losses

adopting the said technique.

Benefits

This method considers time value factor in calculating the profitability of investments

that provides current value of projected future CFs. This method accepts the conventional cash

flow patterns. The investment technique consider all the cash flows generated by project

(Nnamani, 2016). It provides more reliable estimate of the profitability of the investments

considering the factors risks associated with the project. If the NPV of the project is negative it

will not be providing required profits.

Limitations

The method though provides reliable estimates are difficult and time consuming. This

method does not provide any guidelines over calculation of the return rate required by the

investors. The technique could not be used for comparing the projects with different size. It does

not present profitability in terms of percentage which makes it difficult to make reliable

decisions from the outcomes.

IRR

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.