University of Sunderland Financial Management Assignment: APC308

VerifiedAdded on 2023/01/16

|16

|3907

|56

Homework Assignment

AI Summary

This financial management assignment analyzes key financial concepts and techniques. The first part evaluates equity finance options for Lexbel Plc, including right issues at different prices, and assesses the benefits and drawbacks of scrip dividends. The second part focuses on investment appraisal techniques for the Love-Well Ltd. Company, calculating payback period, accounting rate of return, net present value, and internal rate of return for a new machine purchase. The assignment provides detailed calculations and recommendations, offering a practical application of financial management principles.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 2 Equity finance as long term finance..........................................................................3

Question 3 Investment Appraisal techniques...............................................................................8

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 2 Equity finance as long term finance..........................................................................3

Question 3 Investment Appraisal techniques...............................................................................8

CONCLUSION..............................................................................................................................14

REFERENCES................................................................................................................................1

INTRODUCTION

Financial Management can be defined as that manner through which the financial

activities and decision-making in a company is regulated. It also monitors the fund procurement

methods that are used by the company and the utilization of these funds in the operations of the

company (Richard, Kirby and Chadwick, 2018). In the present report, an analysis will be made

that whether the right issue is a correct equity raising option for the Lexbel Company and further

the concept of scrip dividend will be evaluated. Further, the current research will also evaluate

the different investment options that are available to the Love Well Company and advantages as

well as disadvantages that are associated with all the investment techniques will also be

ascertained in the report.

MAIN BODY

Question 2 Equity finance as long term finance

a) Determination of PAT

Right issue refers to raising additional capital for the company by issuing the right of subscribing

to these newly issued shared to existing shareholders only (Yu and et.al., 2015). Currently,

Lexbel Plc is planning to raise £180000 by the means of right issue shares so that current

operations can be expanded. The existing financial data can be listed as follows:

The market price of current ex-dividend of Lexbel Plc = £1.90

Three recommended right issue prices: £1.80, £1.60 or £1.40

Ordinary shares issued at 50p each = £300000

+ Reserves = £400000

Total = £700000

Amount to be raised is £180000

Therefore, Profit after tax (PAT) = £700000* 20%

= £140000

b) Determination of:

i. Number of right shares to be issued.

Nos. of shares required to be issued = Funds required to be raised/ Right issue price

Particular Amount (in terms of

£)

Amount (in terms

of £)

Amount (in terms

of £)

Financial Management can be defined as that manner through which the financial

activities and decision-making in a company is regulated. It also monitors the fund procurement

methods that are used by the company and the utilization of these funds in the operations of the

company (Richard, Kirby and Chadwick, 2018). In the present report, an analysis will be made

that whether the right issue is a correct equity raising option for the Lexbel Company and further

the concept of scrip dividend will be evaluated. Further, the current research will also evaluate

the different investment options that are available to the Love Well Company and advantages as

well as disadvantages that are associated with all the investment techniques will also be

ascertained in the report.

MAIN BODY

Question 2 Equity finance as long term finance

a) Determination of PAT

Right issue refers to raising additional capital for the company by issuing the right of subscribing

to these newly issued shared to existing shareholders only (Yu and et.al., 2015). Currently,

Lexbel Plc is planning to raise £180000 by the means of right issue shares so that current

operations can be expanded. The existing financial data can be listed as follows:

The market price of current ex-dividend of Lexbel Plc = £1.90

Three recommended right issue prices: £1.80, £1.60 or £1.40

Ordinary shares issued at 50p each = £300000

+ Reserves = £400000

Total = £700000

Amount to be raised is £180000

Therefore, Profit after tax (PAT) = £700000* 20%

= £140000

b) Determination of:

i. Number of right shares to be issued.

Nos. of shares required to be issued = Funds required to be raised/ Right issue price

Particular Amount (in terms of

£)

Amount (in terms

of £)

Amount (in terms

of £)

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Existing number of shares 600000 600000 600000

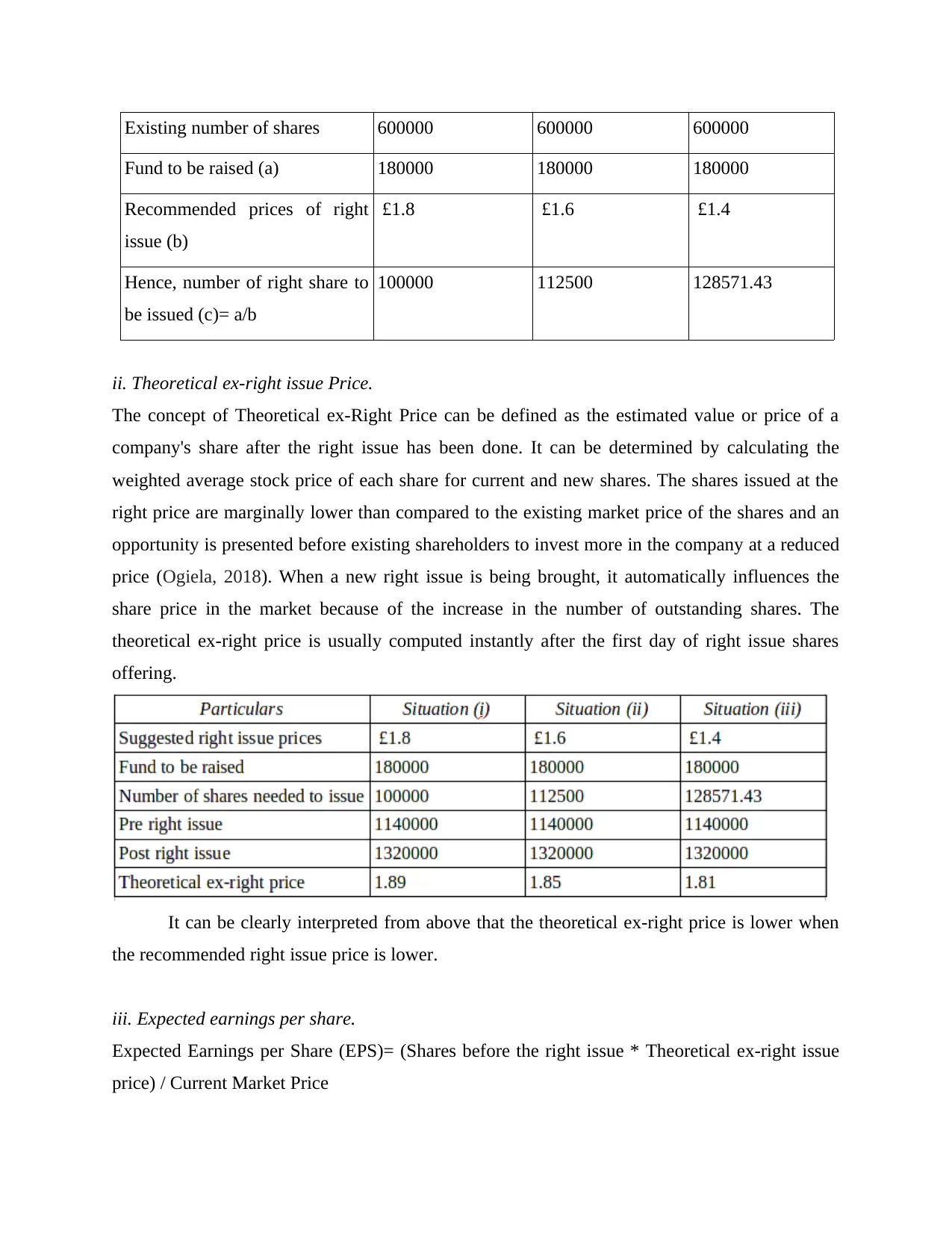

Fund to be raised (a) 180000 180000 180000

Recommended prices of right

issue (b)

£1.8 £1.6 £1.4

Hence, number of right share to

be issued (c)= a/b

100000 112500 128571.43

ii. Theoretical ex-right issue Price.

The concept of Theoretical ex-Right Price can be defined as the estimated value or price of a

company's share after the right issue has been done. It can be determined by calculating the

weighted average stock price of each share for current and new shares. The shares issued at the

right price are marginally lower than compared to the existing market price of the shares and an

opportunity is presented before existing shareholders to invest more in the company at a reduced

price (Ogiela, 2018). When a new right issue is being brought, it automatically influences the

share price in the market because of the increase in the number of outstanding shares. The

theoretical ex-right price is usually computed instantly after the first day of right issue shares

offering.

It can be clearly interpreted from above that the theoretical ex-right price is lower when

the recommended right issue price is lower.

iii. Expected earnings per share.

Expected Earnings per Share (EPS)= (Shares before the right issue * Theoretical ex-right issue

price) / Current Market Price

Fund to be raised (a) 180000 180000 180000

Recommended prices of right

issue (b)

£1.8 £1.6 £1.4

Hence, number of right share to

be issued (c)= a/b

100000 112500 128571.43

ii. Theoretical ex-right issue Price.

The concept of Theoretical ex-Right Price can be defined as the estimated value or price of a

company's share after the right issue has been done. It can be determined by calculating the

weighted average stock price of each share for current and new shares. The shares issued at the

right price are marginally lower than compared to the existing market price of the shares and an

opportunity is presented before existing shareholders to invest more in the company at a reduced

price (Ogiela, 2018). When a new right issue is being brought, it automatically influences the

share price in the market because of the increase in the number of outstanding shares. The

theoretical ex-right price is usually computed instantly after the first day of right issue shares

offering.

It can be clearly interpreted from above that the theoretical ex-right price is lower when

the recommended right issue price is lower.

iii. Expected earnings per share.

Expected Earnings per Share (EPS)= (Shares before the right issue * Theoretical ex-right issue

price) / Current Market Price

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

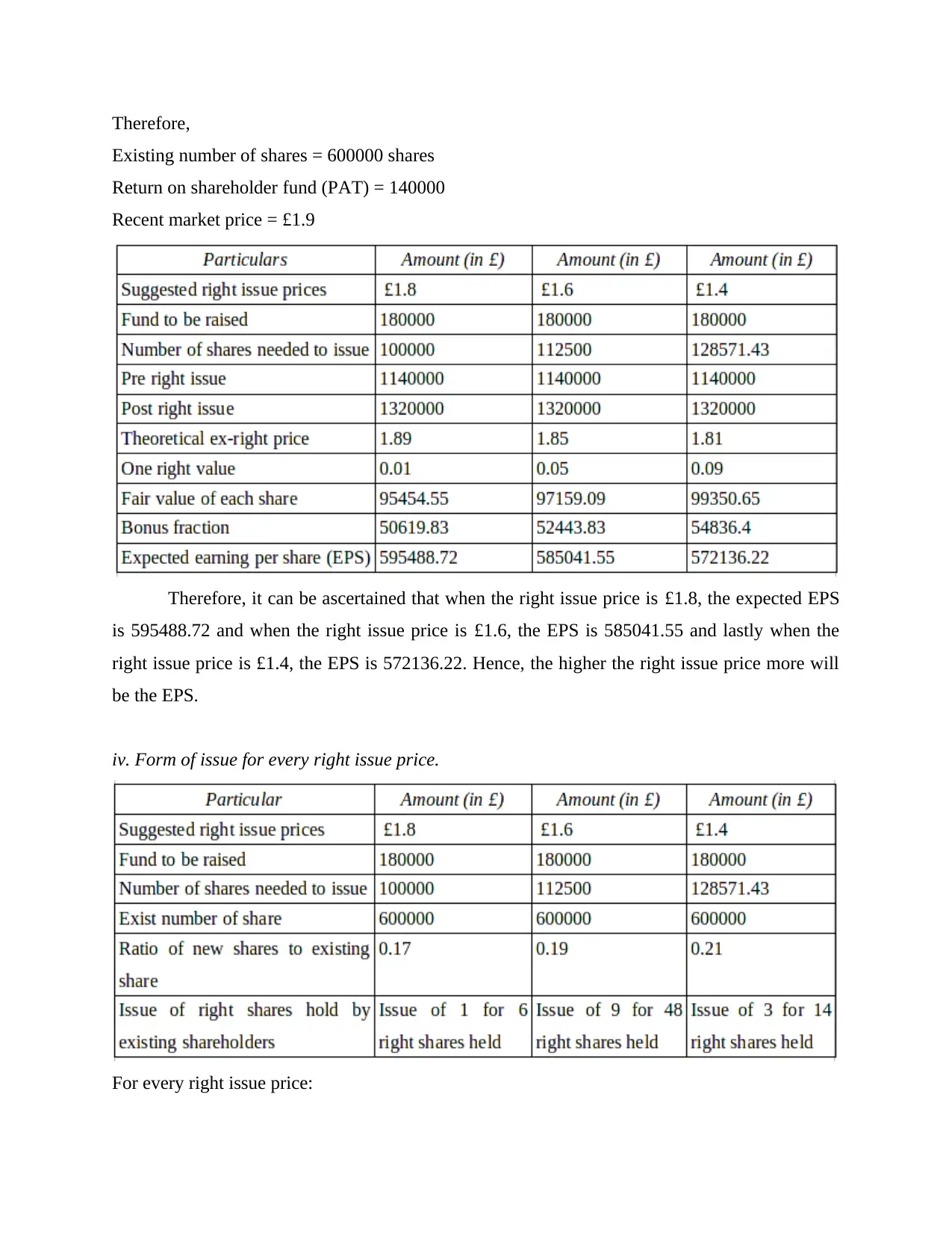

Therefore,

Existing number of shares = 600000 shares

Return on shareholder fund (PAT) = 140000

Recent market price = £1.9

Therefore, it can be ascertained that when the right issue price is £1.8, the expected EPS

is 595488.72 and when the right issue price is £1.6, the EPS is 585041.55 and lastly when the

right issue price is £1.4, the EPS is 572136.22. Hence, the higher the right issue price more will

be the EPS.

iv. Form of issue for every right issue price.

For every right issue price:

Existing number of shares = 600000 shares

Return on shareholder fund (PAT) = 140000

Recent market price = £1.9

Therefore, it can be ascertained that when the right issue price is £1.8, the expected EPS

is 595488.72 and when the right issue price is £1.6, the EPS is 585041.55 and lastly when the

right issue price is £1.4, the EPS is 572136.22. Hence, the higher the right issue price more will

be the EPS.

iv. Form of issue for every right issue price.

For every right issue price:

For the every share issued at the right issue price of £1.80., the number of shares that will

be collectively issued amounts to 100000 shares and hence on a pro-rata basis, the

shareholders will be assigned 1 share for every 6 shares that they hold in the company.

For every right share that is issued at the price of £1.60, the total number of shares that

will be issued are 112500 and therefore, while calculating on pro-rata basis, it can be

ascertained that for every 48 shares held by the shareholders in the company, they will be

issued 9 shares. Lastly, when the right issue s carried at £1.40, the company i.e. Lexbel Plc, will issue

128571 shares collectively and therefore, the pro-rata rate can be ascertained as issue of 3

shares for every 14 shares that are held by the existing shareholders.

v. Presentation and critical evaluation of the best option amongst the three.

The above calculation can therefore help in concluding that the best option amongst the

three right issue prices that have been suggested to the Lexbel Plc, the most profitable and

rewarding option would be to select the right issue at £1.80 (Kober, Subraamanniam and

Watson, 2017). The calculations above show that this is the most profitable situation for the

company as the earning per share would be highest at this price when they are compared to the

other two prices that have been suggested for the right issue for Lexbel Plc.

c) Evaluation of Scrip Dividend as an option for companies

Scrip Dividend: Scrip Dividend can be defined as that term or concept where the company or the

issuer does not simply or directly give the cash dividend to the shareholders of the company but

instead they are given an option where they can either take the cash dividend as an appropriate

option or they are given the choice to take additional shares in the company that are worth of an

amount equivalent to the cash dividend that they have been offered. This option is generally

presented to the shareholders by the company when they do not have adequate cash to pay the

dividend in form of cash but as an alternative, they try to sell more shares to them. The term

scrip signifies any substitute or an alternative currency for a legal tender (Sparrow and et.al,

2018). There are various benefits that are associated with such scrip dividend where both

shareholders and the company can get equally benefited and simultaneously there are some

drawbacks as well that can be discussed as follows:

Benefits for Shareholders:

be collectively issued amounts to 100000 shares and hence on a pro-rata basis, the

shareholders will be assigned 1 share for every 6 shares that they hold in the company.

For every right share that is issued at the price of £1.60, the total number of shares that

will be issued are 112500 and therefore, while calculating on pro-rata basis, it can be

ascertained that for every 48 shares held by the shareholders in the company, they will be

issued 9 shares. Lastly, when the right issue s carried at £1.40, the company i.e. Lexbel Plc, will issue

128571 shares collectively and therefore, the pro-rata rate can be ascertained as issue of 3

shares for every 14 shares that are held by the existing shareholders.

v. Presentation and critical evaluation of the best option amongst the three.

The above calculation can therefore help in concluding that the best option amongst the

three right issue prices that have been suggested to the Lexbel Plc, the most profitable and

rewarding option would be to select the right issue at £1.80 (Kober, Subraamanniam and

Watson, 2017). The calculations above show that this is the most profitable situation for the

company as the earning per share would be highest at this price when they are compared to the

other two prices that have been suggested for the right issue for Lexbel Plc.

c) Evaluation of Scrip Dividend as an option for companies

Scrip Dividend: Scrip Dividend can be defined as that term or concept where the company or the

issuer does not simply or directly give the cash dividend to the shareholders of the company but

instead they are given an option where they can either take the cash dividend as an appropriate

option or they are given the choice to take additional shares in the company that are worth of an

amount equivalent to the cash dividend that they have been offered. This option is generally

presented to the shareholders by the company when they do not have adequate cash to pay the

dividend in form of cash but as an alternative, they try to sell more shares to them. The term

scrip signifies any substitute or an alternative currency for a legal tender (Sparrow and et.al,

2018). There are various benefits that are associated with such scrip dividend where both

shareholders and the company can get equally benefited and simultaneously there are some

drawbacks as well that can be discussed as follows:

Benefits for Shareholders:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The scrip dividend helps the shareholders in increasing their investment in the company

and increase the total number of holding of such investors in the company. This is

usually a much profitable option when the company has a goodwill in the market and is

mostly in profit which makes the investors sure that they will earn higher amount when

they sell such shares.

The time value concept can be associated and concluded that the yield of the scrip

dividend is more than that of cash dividend. Additionally, it is much easier to handle

scrip dividends as compared to the cash dividends. This can help the shareholders in increasing their equity share holding in the company

without incurring any additional cost of paying commissions to any intermediary parties

or paying stamp duty (Persakis and Iatridis, 2015).

Drawbacks for the Shareholders:

Here the price of the share is dependent on it s movement and profitability which is

affected by the state of economy and there are chances that the shareholder might incur

significant losses rather than earning profits.

When the shareholders are in need of cash they might not be able to utilize full benefits

of the scrip dividend and it might be time-consuming process to get returns in exchange

for the shares thus amassed through scrip dividend. The shareholders can even incur taxes on the dividends thus given to them and this

taxation amount is not covered in the scrip dividends that are being issued.

Benefits for Companies:

This helps the companies in saving the capital and retaining it in the company thus

increasing the cash and cash equivalents' balance in the company (Yunus, 2018).

It helps the companies in addressing the risk associated with the liquidity position of the

company. Additionally, when the number of shareholders of the company increases, the

market capitalization of the company also increases. Another major advantage is that there is no additional requirement to pay cash to the

shareholders and this helps the company in tax saving as well.

Drawbacks for the Company:

and increase the total number of holding of such investors in the company. This is

usually a much profitable option when the company has a goodwill in the market and is

mostly in profit which makes the investors sure that they will earn higher amount when

they sell such shares.

The time value concept can be associated and concluded that the yield of the scrip

dividend is more than that of cash dividend. Additionally, it is much easier to handle

scrip dividends as compared to the cash dividends. This can help the shareholders in increasing their equity share holding in the company

without incurring any additional cost of paying commissions to any intermediary parties

or paying stamp duty (Persakis and Iatridis, 2015).

Drawbacks for the Shareholders:

Here the price of the share is dependent on it s movement and profitability which is

affected by the state of economy and there are chances that the shareholder might incur

significant losses rather than earning profits.

When the shareholders are in need of cash they might not be able to utilize full benefits

of the scrip dividend and it might be time-consuming process to get returns in exchange

for the shares thus amassed through scrip dividend. The shareholders can even incur taxes on the dividends thus given to them and this

taxation amount is not covered in the scrip dividends that are being issued.

Benefits for Companies:

This helps the companies in saving the capital and retaining it in the company thus

increasing the cash and cash equivalents' balance in the company (Yunus, 2018).

It helps the companies in addressing the risk associated with the liquidity position of the

company. Additionally, when the number of shareholders of the company increases, the

market capitalization of the company also increases. Another major advantage is that there is no additional requirement to pay cash to the

shareholders and this helps the company in tax saving as well.

Drawbacks for the Company:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

When the performance of the company is not profitable, there are chances that they might

earn losses i.e. there stock might not perform so well and this can lead to the company

not being able to give adequate return (Karpoff, Lee and Martin, 2017).

Though scrip dividend might seem a better option as compared to the cash dividends but

there is a higher or greater requirement of time and cost and it might not be a better

option after for the company as well.

The analysis of the various advantages and disadvantages that are associated with the companies

and shareholders can be hence concluded and appropriate decision can be taken accordingly.

Question 3 Investment Appraisal techniques

Investment Appraisal techniques can be defined as that technique where the decision regarding

the investment that is to be made is taken after evaluating different options that are available for

such investments that are to be made. These strategies such as payback period, NPV, ARR etc. is

used to make the choice regarding whether investment should be made or not (Mihai Yiannaki,

2017). Here the benefits for drawbacks of different investment options that are available is

evaluated and then the expenses against such benefits are compared calculating the net profit for

each investment that is to be made.

a) Calculations

In the following section, different techniques would be evaluated in context of the new machine

that the Love-Well Ltd. Company intends to buy:

i. The Payback Period.

The formula is Investment/ Cash Flows. Here,

Initial Investment = £275000

Cash Flow = Inflow- outflow

= £85000- £12500

= £72500

Therefore, payback period = £275000/ £72500

= 3.79 years.

It can be ascertained on the basis of calculation above that the company will be able to recover

the investment that it is making in approximately 4 years and the total expected life of the

machineries for 6 years. Therefore, the company should go forward with the investment because

it is a profitable venture.

earn losses i.e. there stock might not perform so well and this can lead to the company

not being able to give adequate return (Karpoff, Lee and Martin, 2017).

Though scrip dividend might seem a better option as compared to the cash dividends but

there is a higher or greater requirement of time and cost and it might not be a better

option after for the company as well.

The analysis of the various advantages and disadvantages that are associated with the companies

and shareholders can be hence concluded and appropriate decision can be taken accordingly.

Question 3 Investment Appraisal techniques

Investment Appraisal techniques can be defined as that technique where the decision regarding

the investment that is to be made is taken after evaluating different options that are available for

such investments that are to be made. These strategies such as payback period, NPV, ARR etc. is

used to make the choice regarding whether investment should be made or not (Mihai Yiannaki,

2017). Here the benefits for drawbacks of different investment options that are available is

evaluated and then the expenses against such benefits are compared calculating the net profit for

each investment that is to be made.

a) Calculations

In the following section, different techniques would be evaluated in context of the new machine

that the Love-Well Ltd. Company intends to buy:

i. The Payback Period.

The formula is Investment/ Cash Flows. Here,

Initial Investment = £275000

Cash Flow = Inflow- outflow

= £85000- £12500

= £72500

Therefore, payback period = £275000/ £72500

= 3.79 years.

It can be ascertained on the basis of calculation above that the company will be able to recover

the investment that it is making in approximately 4 years and the total expected life of the

machineries for 6 years. Therefore, the company should go forward with the investment because

it is a profitable venture.

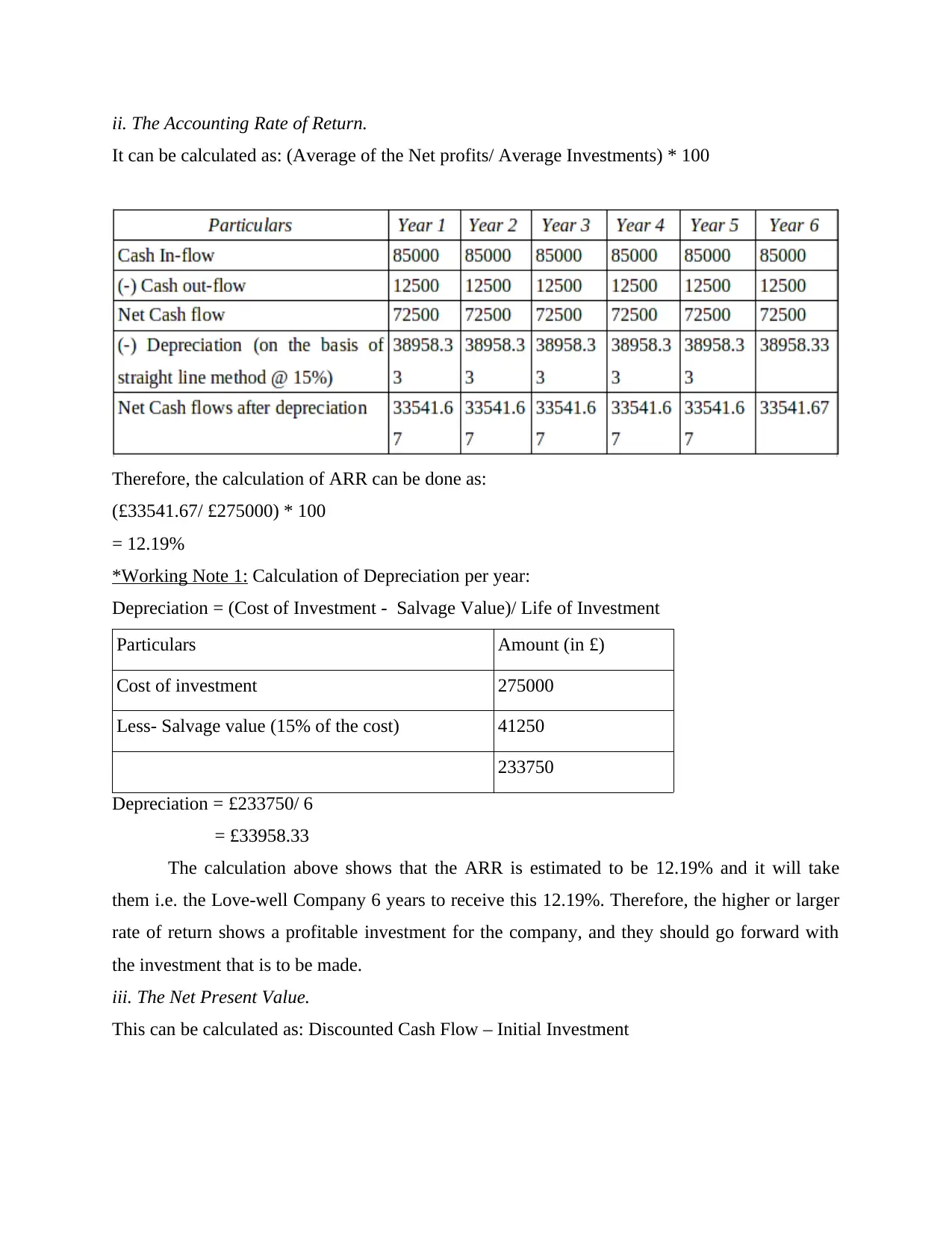

ii. The Accounting Rate of Return.

It can be calculated as: (Average of the Net profits/ Average Investments) * 100

Therefore, the calculation of ARR can be done as:

(£33541.67/ £275000) * 100

= 12.19%

*Working Note 1: Calculation of Depreciation per year:

Depreciation = (Cost of Investment - Salvage Value)/ Life of Investment

Particulars Amount (in £)

Cost of investment 275000

Less- Salvage value (15% of the cost) 41250

233750

Depreciation = £233750/ 6

= £33958.33

The calculation above shows that the ARR is estimated to be 12.19% and it will take

them i.e. the Love-well Company 6 years to receive this 12.19%. Therefore, the higher or larger

rate of return shows a profitable investment for the company, and they should go forward with

the investment that is to be made.

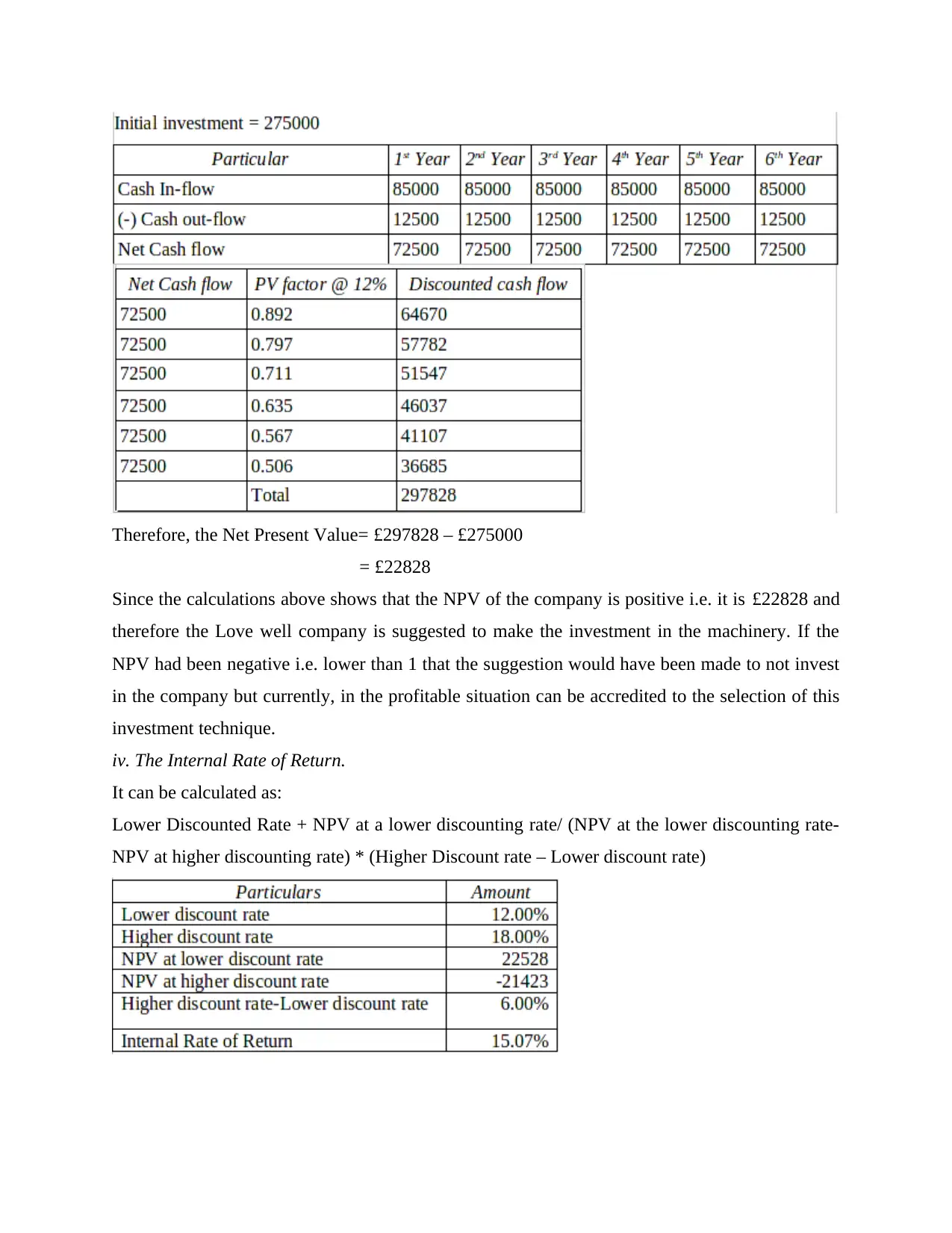

iii. The Net Present Value.

This can be calculated as: Discounted Cash Flow – Initial Investment

It can be calculated as: (Average of the Net profits/ Average Investments) * 100

Therefore, the calculation of ARR can be done as:

(£33541.67/ £275000) * 100

= 12.19%

*Working Note 1: Calculation of Depreciation per year:

Depreciation = (Cost of Investment - Salvage Value)/ Life of Investment

Particulars Amount (in £)

Cost of investment 275000

Less- Salvage value (15% of the cost) 41250

233750

Depreciation = £233750/ 6

= £33958.33

The calculation above shows that the ARR is estimated to be 12.19% and it will take

them i.e. the Love-well Company 6 years to receive this 12.19%. Therefore, the higher or larger

rate of return shows a profitable investment for the company, and they should go forward with

the investment that is to be made.

iii. The Net Present Value.

This can be calculated as: Discounted Cash Flow – Initial Investment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Therefore, the Net Present Value= £297828 – £275000

= £22828

Since the calculations above shows that the NPV of the company is positive i.e. it is £22828 and

therefore the Love well company is suggested to make the investment in the machinery. If the

NPV had been negative i.e. lower than 1 that the suggestion would have been made to not invest

in the company but currently, in the profitable situation can be accredited to the selection of this

investment technique.

iv. The Internal Rate of Return.

It can be calculated as:

Lower Discounted Rate + NPV at a lower discounting rate/ (NPV at the lower discounting rate-

NPV at higher discounting rate) * (Higher Discount rate – Lower discount rate)

= £22828

Since the calculations above shows that the NPV of the company is positive i.e. it is £22828 and

therefore the Love well company is suggested to make the investment in the machinery. If the

NPV had been negative i.e. lower than 1 that the suggestion would have been made to not invest

in the company but currently, in the profitable situation can be accredited to the selection of this

investment technique.

iv. The Internal Rate of Return.

It can be calculated as:

Lower Discounted Rate + NPV at a lower discounting rate/ (NPV at the lower discounting rate-

NPV at higher discounting rate) * (Higher Discount rate – Lower discount rate)

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

*Working Note: NPV Calculations

NPV at a lower interest rate i.e. @ 12%

NPV= £297828 – £275000

= £22828

NPV at a higher interest rate i.e. @18%

NPV= £253576- £275000

= -£21424

On the basis of above calculated IRR, it can be ascertained that the company should go

further with the acquisition of the machinery. Currently it is, 15.07% and it is relatively much

higher and can lead to higher revenue generation for the company.

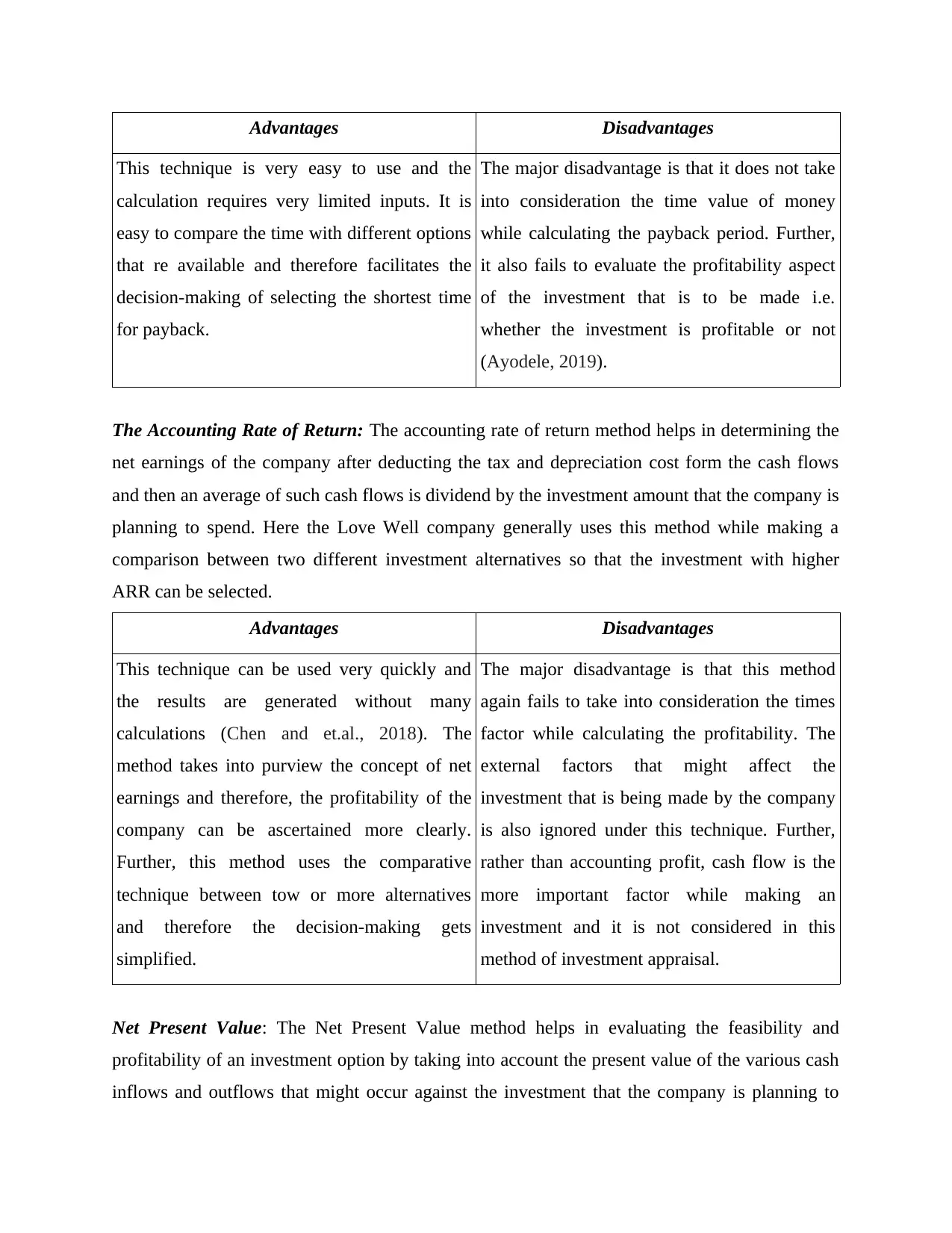

b) Advantages and Disadvantages of different appraisal techniques

The Payback Period:

The Payback Period technique is used to ascertain the approximate time that the company will

take to recover the expenditure that it is making on the investment. Under this technique, the

investments that have smaller cash flows in the earlier duration are ranked in a better way as

compared to the projects where the cash flows are greater in the later periods.

NPV at a lower interest rate i.e. @ 12%

NPV= £297828 – £275000

= £22828

NPV at a higher interest rate i.e. @18%

NPV= £253576- £275000

= -£21424

On the basis of above calculated IRR, it can be ascertained that the company should go

further with the acquisition of the machinery. Currently it is, 15.07% and it is relatively much

higher and can lead to higher revenue generation for the company.

b) Advantages and Disadvantages of different appraisal techniques

The Payback Period:

The Payback Period technique is used to ascertain the approximate time that the company will

take to recover the expenditure that it is making on the investment. Under this technique, the

investments that have smaller cash flows in the earlier duration are ranked in a better way as

compared to the projects where the cash flows are greater in the later periods.

Advantages Disadvantages

This technique is very easy to use and the

calculation requires very limited inputs. It is

easy to compare the time with different options

that re available and therefore facilitates the

decision-making of selecting the shortest time

for payback.

The major disadvantage is that it does not take

into consideration the time value of money

while calculating the payback period. Further,

it also fails to evaluate the profitability aspect

of the investment that is to be made i.e.

whether the investment is profitable or not

(Ayodele, 2019).

The Accounting Rate of Return: The accounting rate of return method helps in determining the

net earnings of the company after deducting the tax and depreciation cost form the cash flows

and then an average of such cash flows is dividend by the investment amount that the company is

planning to spend. Here the Love Well company generally uses this method while making a

comparison between two different investment alternatives so that the investment with higher

ARR can be selected.

Advantages Disadvantages

This technique can be used very quickly and

the results are generated without many

calculations (Chen and et.al., 2018). The

method takes into purview the concept of net

earnings and therefore, the profitability of the

company can be ascertained more clearly.

Further, this method uses the comparative

technique between tow or more alternatives

and therefore the decision-making gets

simplified.

The major disadvantage is that this method

again fails to take into consideration the times

factor while calculating the profitability. The

external factors that might affect the

investment that is being made by the company

is also ignored under this technique. Further,

rather than accounting profit, cash flow is the

more important factor while making an

investment and it is not considered in this

method of investment appraisal.

Net Present Value: The Net Present Value method helps in evaluating the feasibility and

profitability of an investment option by taking into account the present value of the various cash

inflows and outflows that might occur against the investment that the company is planning to

This technique is very easy to use and the

calculation requires very limited inputs. It is

easy to compare the time with different options

that re available and therefore facilitates the

decision-making of selecting the shortest time

for payback.

The major disadvantage is that it does not take

into consideration the time value of money

while calculating the payback period. Further,

it also fails to evaluate the profitability aspect

of the investment that is to be made i.e.

whether the investment is profitable or not

(Ayodele, 2019).

The Accounting Rate of Return: The accounting rate of return method helps in determining the

net earnings of the company after deducting the tax and depreciation cost form the cash flows

and then an average of such cash flows is dividend by the investment amount that the company is

planning to spend. Here the Love Well company generally uses this method while making a

comparison between two different investment alternatives so that the investment with higher

ARR can be selected.

Advantages Disadvantages

This technique can be used very quickly and

the results are generated without many

calculations (Chen and et.al., 2018). The

method takes into purview the concept of net

earnings and therefore, the profitability of the

company can be ascertained more clearly.

Further, this method uses the comparative

technique between tow or more alternatives

and therefore the decision-making gets

simplified.

The major disadvantage is that this method

again fails to take into consideration the times

factor while calculating the profitability. The

external factors that might affect the

investment that is being made by the company

is also ignored under this technique. Further,

rather than accounting profit, cash flow is the

more important factor while making an

investment and it is not considered in this

method of investment appraisal.

Net Present Value: The Net Present Value method helps in evaluating the feasibility and

profitability of an investment option by taking into account the present value of the various cash

inflows and outflows that might occur against the investment that the company is planning to

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.