Financial Management Assignment: Investment Appraisal & Equity Finance

VerifiedAdded on 2023/01/13

|17

|3949

|92

Homework Assignment

AI Summary

This financial management assignment solution addresses key concepts in long-term finance and investment appraisal. It begins by calculating profit after tax and analyzing right issues, including the determination of right shares to be issued and the theoretical ex-right price. The solution then evaluates different right issue price options and recommends the best choice for Lexbel Plc, based on earnings per share. The assignment also includes an evaluation of scrip dividends, outlining their benefits and drawbacks for both shareholders and the company. Furthermore, the solution calculates and interprets various investment appraisal techniques, such as the payback period, accounting rate of return (ARR), and net present value (NPV), providing a comprehensive analysis of investment viability.

Financial management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 2. Long term Finance i.e. Equity Finance....................................................................3

QUESTION 3: Investment Appraisal Techniques...........................................................................8

a.) Calculations............................................................................................................................8

b.) Critically evaluating the advantages and limitations of various investment appraisal

techniques..................................................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 2. Long term Finance i.e. Equity Finance....................................................................3

QUESTION 3: Investment Appraisal Techniques...........................................................................8

a.) Calculations............................................................................................................................8

b.) Critically evaluating the advantages and limitations of various investment appraisal

techniques..................................................................................................................................11

CONCLUSION..............................................................................................................................13

REFERENCES................................................................................................................................1

INTRODUCTION

Financial management is considered to be one of the most appropriate procedure which

helps in planning, organizing and effectively controlling the various financial operations related

with proper procurement of the funds and capital in an organization (Wambua and Koori, 2018).

It is considered to be very useful in taking business decision which is very useful for attainment

of organizational goals and objectives. Financial management is very crucial because it helps in

promoting the growth of the business enterprise. The present study will emphasize on examining

the long term finance of the company. It is very useful in properly managing the funds of the

company. Furthermore, this study also helps in determining the benefits of the scrip dividends to

the company and its stakeholders. This study also includes calculation of various investment

appraisal techniques and also critically evaluate benefits and limitations of different investment

appraisal techniques.

MAIN BODY

Question 2. Long term Finance i.e. Equity Finance

a) Calculation of Profit After Tax

The term right issue is mostly used to determine the act through which a company can

raise additional shares in the form of equity capital by issuing shares only to the existing

sahreho9lders of the company at a lower rate (Ogiela, 2018). The company Lexbel Plc intends to

generate £180000 through the right issue share price and for that the profit after tax needs to be

ascertained in a following manner:

The current ex-dividend's market price of Lexbel Plc = £1.90

Recommendation of right issue prices that Lexbel has been proposed: £1.80, £1.60 or £1.40

Ordinary shares which are issued at 50p each = £300000

+ Reserves = £400000

Total = £700000

Amount intended to be raised = £180000

Therefore, Profit after tax (PAT) = £700000* 20%

= £140000

b) Calculation of:

Right shares that are to be issued.

Rights shares that are to be issued: Funds amount that is to be raised/ price of right issue

Financial management is considered to be one of the most appropriate procedure which

helps in planning, organizing and effectively controlling the various financial operations related

with proper procurement of the funds and capital in an organization (Wambua and Koori, 2018).

It is considered to be very useful in taking business decision which is very useful for attainment

of organizational goals and objectives. Financial management is very crucial because it helps in

promoting the growth of the business enterprise. The present study will emphasize on examining

the long term finance of the company. It is very useful in properly managing the funds of the

company. Furthermore, this study also helps in determining the benefits of the scrip dividends to

the company and its stakeholders. This study also includes calculation of various investment

appraisal techniques and also critically evaluate benefits and limitations of different investment

appraisal techniques.

MAIN BODY

Question 2. Long term Finance i.e. Equity Finance

a) Calculation of Profit After Tax

The term right issue is mostly used to determine the act through which a company can

raise additional shares in the form of equity capital by issuing shares only to the existing

sahreho9lders of the company at a lower rate (Ogiela, 2018). The company Lexbel Plc intends to

generate £180000 through the right issue share price and for that the profit after tax needs to be

ascertained in a following manner:

The current ex-dividend's market price of Lexbel Plc = £1.90

Recommendation of right issue prices that Lexbel has been proposed: £1.80, £1.60 or £1.40

Ordinary shares which are issued at 50p each = £300000

+ Reserves = £400000

Total = £700000

Amount intended to be raised = £180000

Therefore, Profit after tax (PAT) = £700000* 20%

= £140000

b) Calculation of:

Right shares that are to be issued.

Rights shares that are to be issued: Funds amount that is to be raised/ price of right issue

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

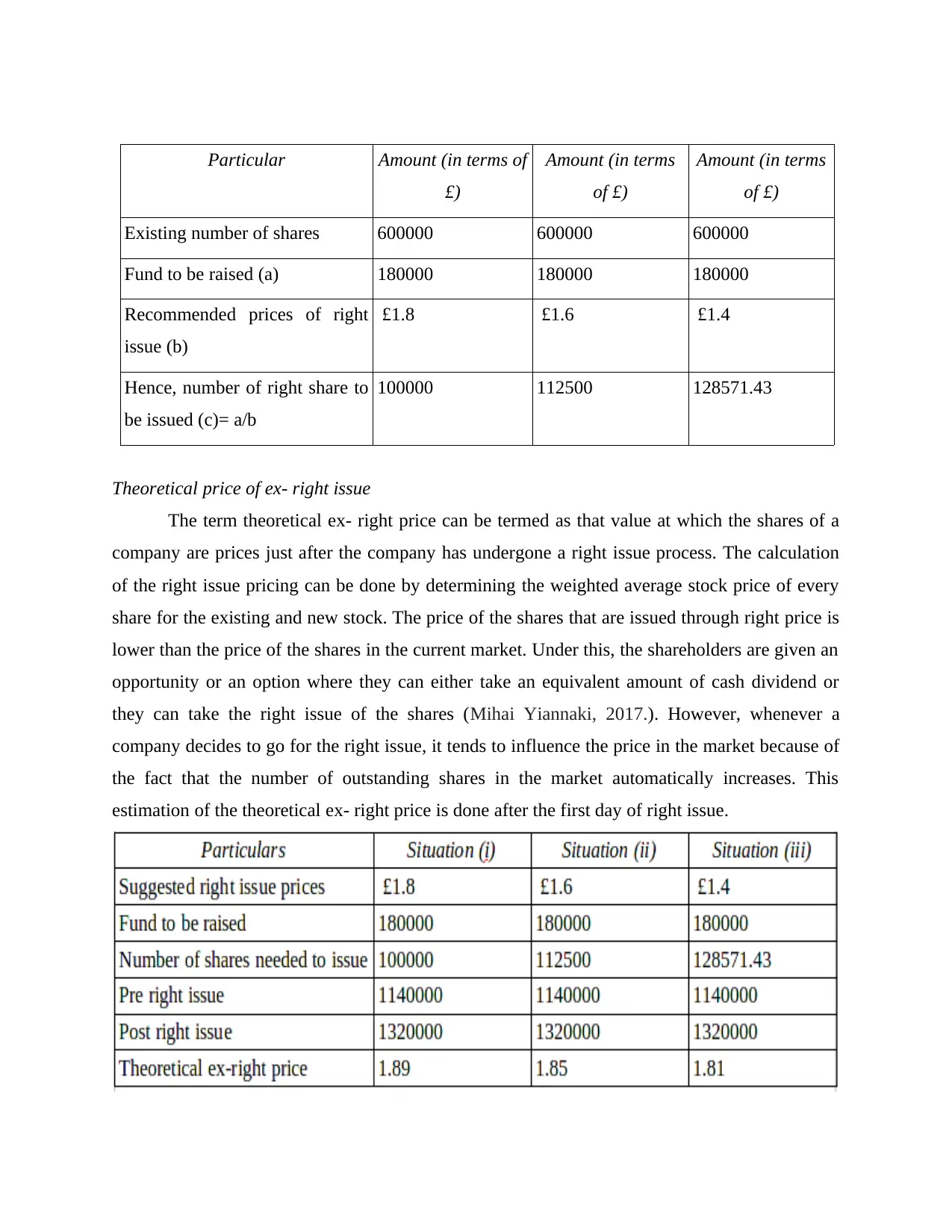

Particular Amount (in terms of

£)

Amount (in terms

of £)

Amount (in terms

of £)

Existing number of shares 600000 600000 600000

Fund to be raised (a) 180000 180000 180000

Recommended prices of right

issue (b)

£1.8 £1.6 £1.4

Hence, number of right share to

be issued (c)= a/b

100000 112500 128571.43

Theoretical price of ex- right issue

The term theoretical ex- right price can be termed as that value at which the shares of a

company are prices just after the company has undergone a right issue process. The calculation

of the right issue pricing can be done by determining the weighted average stock price of every

share for the existing and new stock. The price of the shares that are issued through right price is

lower than the price of the shares in the current market. Under this, the shareholders are given an

opportunity or an option where they can either take an equivalent amount of cash dividend or

they can take the right issue of the shares (Mihai Yiannaki, 2017.). However, whenever a

company decides to go for the right issue, it tends to influence the price in the market because of

the fact that the number of outstanding shares in the market automatically increases. This

estimation of the theoretical ex- right price is done after the first day of right issue.

£)

Amount (in terms

of £)

Amount (in terms

of £)

Existing number of shares 600000 600000 600000

Fund to be raised (a) 180000 180000 180000

Recommended prices of right

issue (b)

£1.8 £1.6 £1.4

Hence, number of right share to

be issued (c)= a/b

100000 112500 128571.43

Theoretical price of ex- right issue

The term theoretical ex- right price can be termed as that value at which the shares of a

company are prices just after the company has undergone a right issue process. The calculation

of the right issue pricing can be done by determining the weighted average stock price of every

share for the existing and new stock. The price of the shares that are issued through right price is

lower than the price of the shares in the current market. Under this, the shareholders are given an

opportunity or an option where they can either take an equivalent amount of cash dividend or

they can take the right issue of the shares (Mihai Yiannaki, 2017.). However, whenever a

company decides to go for the right issue, it tends to influence the price in the market because of

the fact that the number of outstanding shares in the market automatically increases. This

estimation of the theoretical ex- right price is done after the first day of right issue.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

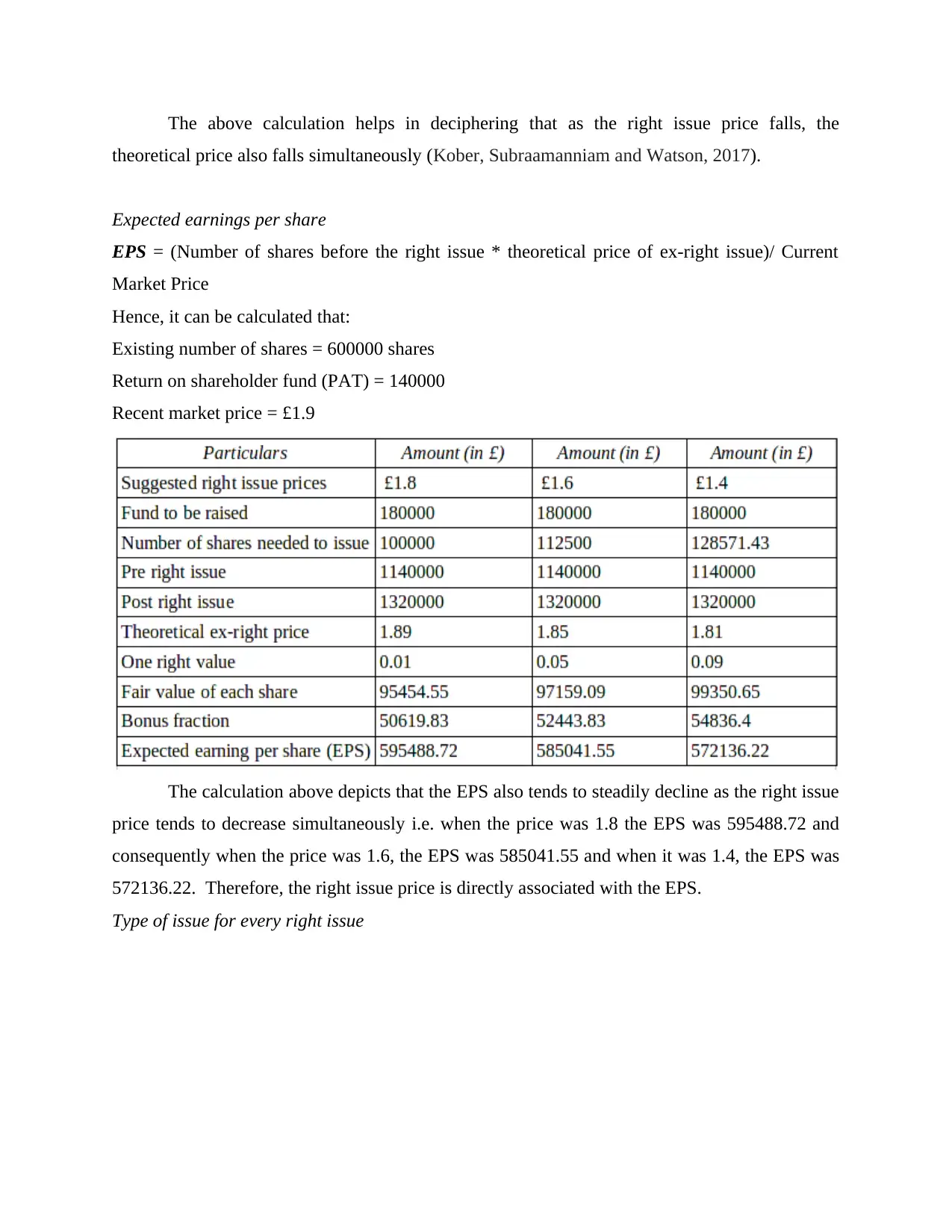

The above calculation helps in deciphering that as the right issue price falls, the

theoretical price also falls simultaneously (Kober, Subraamanniam and Watson, 2017).

Expected earnings per share

EPS = (Number of shares before the right issue * theoretical price of ex-right issue)/ Current

Market Price

Hence, it can be calculated that:

Existing number of shares = 600000 shares

Return on shareholder fund (PAT) = 140000

Recent market price = £1.9

The calculation above depicts that the EPS also tends to steadily decline as the right issue

price tends to decrease simultaneously i.e. when the price was 1.8 the EPS was 595488.72 and

consequently when the price was 1.6, the EPS was 585041.55 and when it was 1.4, the EPS was

572136.22. Therefore, the right issue price is directly associated with the EPS.

Type of issue for every right issue

theoretical price also falls simultaneously (Kober, Subraamanniam and Watson, 2017).

Expected earnings per share

EPS = (Number of shares before the right issue * theoretical price of ex-right issue)/ Current

Market Price

Hence, it can be calculated that:

Existing number of shares = 600000 shares

Return on shareholder fund (PAT) = 140000

Recent market price = £1.9

The calculation above depicts that the EPS also tends to steadily decline as the right issue

price tends to decrease simultaneously i.e. when the price was 1.8 the EPS was 595488.72 and

consequently when the price was 1.6, the EPS was 585041.55 and when it was 1.4, the EPS was

572136.22. Therefore, the right issue price is directly associated with the EPS.

Type of issue for every right issue

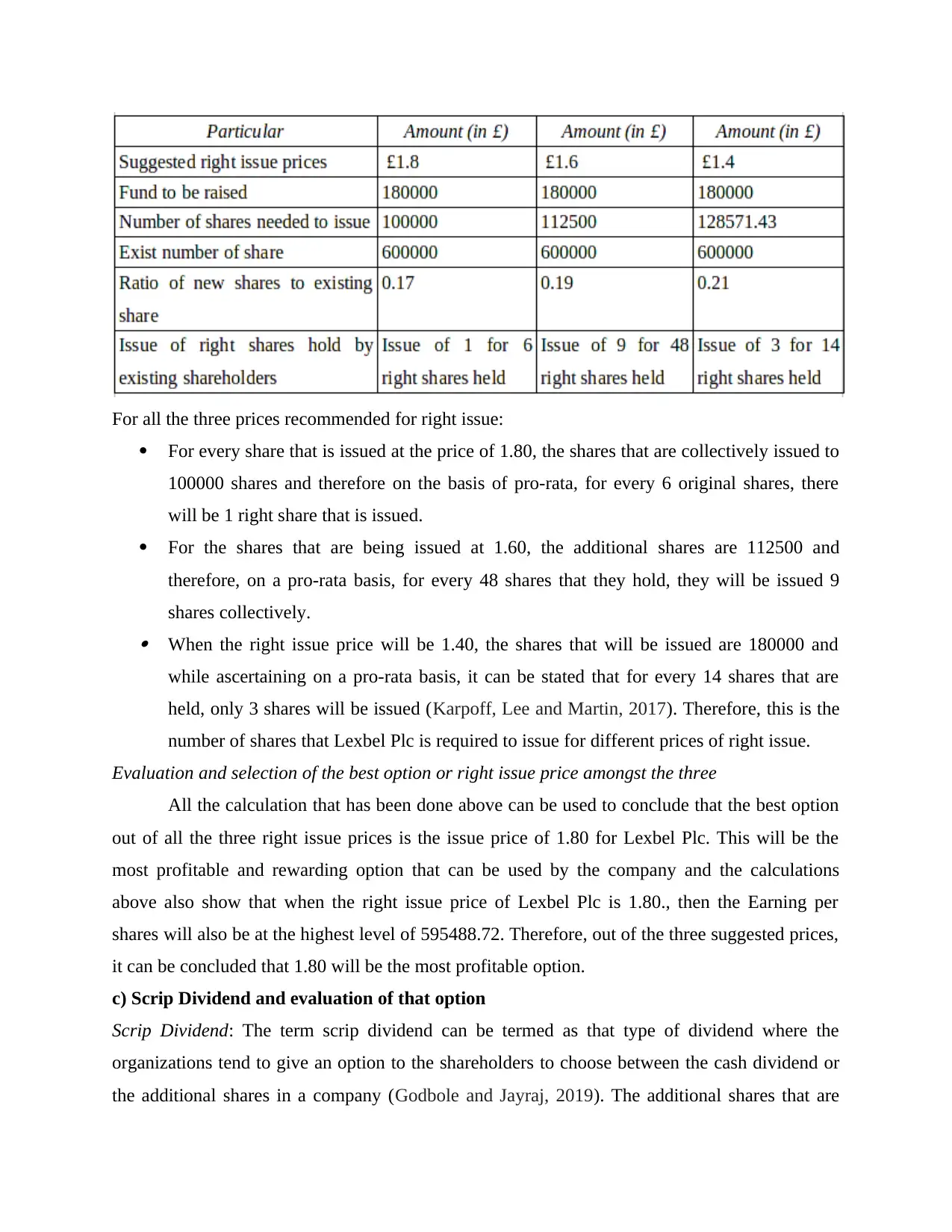

For all the three prices recommended for right issue:

For every share that is issued at the price of 1.80, the shares that are collectively issued to

100000 shares and therefore on the basis of pro-rata, for every 6 original shares, there

will be 1 right share that is issued.

For the shares that are being issued at 1.60, the additional shares are 112500 and

therefore, on a pro-rata basis, for every 48 shares that they hold, they will be issued 9

shares collectively. When the right issue price will be 1.40, the shares that will be issued are 180000 and

while ascertaining on a pro-rata basis, it can be stated that for every 14 shares that are

held, only 3 shares will be issued (Karpoff, Lee and Martin, 2017). Therefore, this is the

number of shares that Lexbel Plc is required to issue for different prices of right issue.

Evaluation and selection of the best option or right issue price amongst the three

All the calculation that has been done above can be used to conclude that the best option

out of all the three right issue prices is the issue price of 1.80 for Lexbel Plc. This will be the

most profitable and rewarding option that can be used by the company and the calculations

above also show that when the right issue price of Lexbel Plc is 1.80., then the Earning per

shares will also be at the highest level of 595488.72. Therefore, out of the three suggested prices,

it can be concluded that 1.80 will be the most profitable option.

c) Scrip Dividend and evaluation of that option

Scrip Dividend: The term scrip dividend can be termed as that type of dividend where the

organizations tend to give an option to the shareholders to choose between the cash dividend or

the additional shares in a company (Godbole and Jayraj, 2019). The additional shares that are

For every share that is issued at the price of 1.80, the shares that are collectively issued to

100000 shares and therefore on the basis of pro-rata, for every 6 original shares, there

will be 1 right share that is issued.

For the shares that are being issued at 1.60, the additional shares are 112500 and

therefore, on a pro-rata basis, for every 48 shares that they hold, they will be issued 9

shares collectively. When the right issue price will be 1.40, the shares that will be issued are 180000 and

while ascertaining on a pro-rata basis, it can be stated that for every 14 shares that are

held, only 3 shares will be issued (Karpoff, Lee and Martin, 2017). Therefore, this is the

number of shares that Lexbel Plc is required to issue for different prices of right issue.

Evaluation and selection of the best option or right issue price amongst the three

All the calculation that has been done above can be used to conclude that the best option

out of all the three right issue prices is the issue price of 1.80 for Lexbel Plc. This will be the

most profitable and rewarding option that can be used by the company and the calculations

above also show that when the right issue price of Lexbel Plc is 1.80., then the Earning per

shares will also be at the highest level of 595488.72. Therefore, out of the three suggested prices,

it can be concluded that 1.80 will be the most profitable option.

c) Scrip Dividend and evaluation of that option

Scrip Dividend: The term scrip dividend can be termed as that type of dividend where the

organizations tend to give an option to the shareholders to choose between the cash dividend or

the additional shares in a company (Godbole and Jayraj, 2019). The additional shares that are

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

given in the company are equivalent to the amount of cash dividend and are generally issued at a

lower price than the current market price of the shares. This option is generally more suitable

when the company is regularly performing profitably and the option to choose the option of

additional capital in the company is better than the option for cash dividend. There are various

benefits and drawbacks that are inherent to the shareholders as well as the company that has

decided to undergo the process of giving scrip dividend:

Benefit for Shareholders:

Scrip dividend offers the shareholders a chance to increase the investment that they hold

in the company and this is usually a much more profitable option for the company as

compared to the cash because the benefits that the company can offer here are higher in

the long term. Here, the concept of time value can be utilized stating that the yield of the scrip dividend

is much higher than that of the cash dividend and ultimately, another major benefit that

can be stated is that the shareholders will not incur any additional cost such as stamp duty

or any intermediate party charges.

Benefit for Company:

The benefit for the Lexbel Plc if they go for the option of scrip dividend is that it helps in

saving the cash and thus retain it in the company. This savings that the company is doing

in the form of cash payments can assist them in saving up the taxes as well that they

might have to pay (Chen and et.al., 2018). The scrip dividend also helps the company is minimizing the risk that is inherent to the

liquidity position in the company i.e. when there is an increased number of shareholders

in the company, the market capitalization of that company also increases automatically.

Disadvantages for Shareholders:

The major drawback is that the share price of the company issuing scrip dividend is

dependent on the movement of the economy i.e. the profitability of the company etc. and

therefore the risk exposure of the shareholder increases where they might incur losses

instead of profits.

Another disadvantage here is that the shareholders might face the requirement of cash

later and it is a time-consuming process for the shareholders to convert the scrip dividend

shares into the cash.

lower price than the current market price of the shares. This option is generally more suitable

when the company is regularly performing profitably and the option to choose the option of

additional capital in the company is better than the option for cash dividend. There are various

benefits and drawbacks that are inherent to the shareholders as well as the company that has

decided to undergo the process of giving scrip dividend:

Benefit for Shareholders:

Scrip dividend offers the shareholders a chance to increase the investment that they hold

in the company and this is usually a much more profitable option for the company as

compared to the cash because the benefits that the company can offer here are higher in

the long term. Here, the concept of time value can be utilized stating that the yield of the scrip dividend

is much higher than that of the cash dividend and ultimately, another major benefit that

can be stated is that the shareholders will not incur any additional cost such as stamp duty

or any intermediate party charges.

Benefit for Company:

The benefit for the Lexbel Plc if they go for the option of scrip dividend is that it helps in

saving the cash and thus retain it in the company. This savings that the company is doing

in the form of cash payments can assist them in saving up the taxes as well that they

might have to pay (Chen and et.al., 2018). The scrip dividend also helps the company is minimizing the risk that is inherent to the

liquidity position in the company i.e. when there is an increased number of shareholders

in the company, the market capitalization of that company also increases automatically.

Disadvantages for Shareholders:

The major drawback is that the share price of the company issuing scrip dividend is

dependent on the movement of the economy i.e. the profitability of the company etc. and

therefore the risk exposure of the shareholder increases where they might incur losses

instead of profits.

Another disadvantage here is that the shareholders might face the requirement of cash

later and it is a time-consuming process for the shareholders to convert the scrip dividend

shares into the cash.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

The shareholders might have to pay additional taxes on the dividend amount that they

receive and this tax amount is not covered up under the scrip dividend that the company

is issuing.

Disadvantages for Company:

The major disadvantages for the company going for scrip dividend is that they can earn

losses as well and if their stock does not perform as well as they expected it too, then the

loss that they might suffer double up (Ayodele, 2019).

Although, the scrip dividend option appears to be much more attractive than the option of

cash dividend yet the time and cost that is required is much more and therefore it might

not be the best option for the company since the cost overall increases.

Hence, the various advantages and disadvantages inherent to scrip dividend were evaluated for

the companies as well as their shareholders.

QUESTION 3: Investment Appraisal Techniques

Investment Appraisal Techniques is very useful in assessing the viability of the project

and portfolio which in turn is considered to be necessary for better decision making related to the

particular investment (Mayer and Schultmann, 2017). Investment Appraisal Techniques is useful

in evaluating the returns on the particular long term investment. It helps in selecting the

appropriate investment plan by analysing and predicting the results on the investment.

Investment Appraisal Techniques is important because it helps in maximization of the wealth of

the shareholders.

a.) Calculations

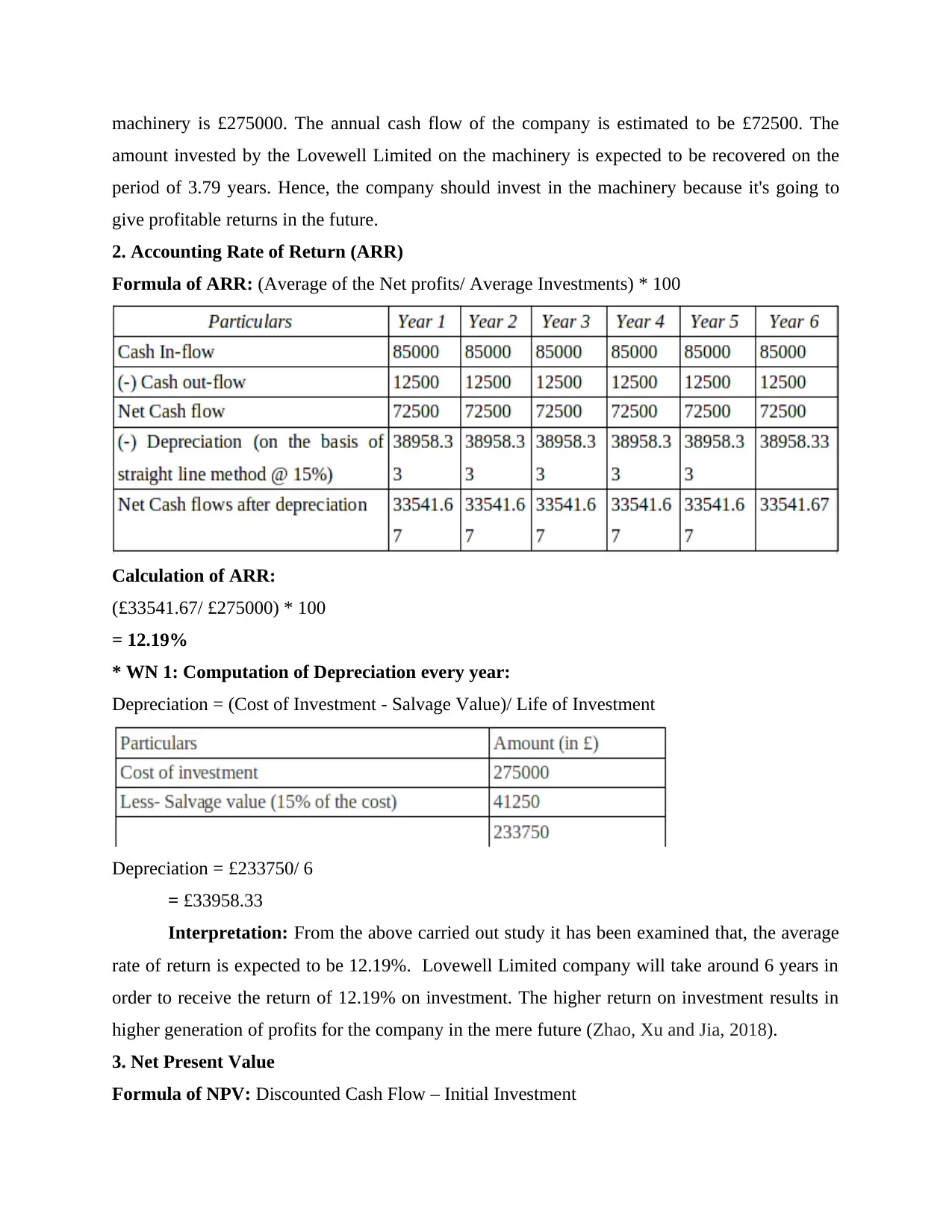

1. Payback Period

Formula of Payback period: Investment/ Cash Flows.

Initial Investment = £275000

Cash Flow = Inflow- outflow

= £85000- £12500

= £72500

Hence, Payback period = £275000/ £72500

= 3.79 years.

Interpretation: From the above carried out study it has been examined that, the life span

of the machinery is expected to be 6 years. On the other hand, the initial investment on

receive and this tax amount is not covered up under the scrip dividend that the company

is issuing.

Disadvantages for Company:

The major disadvantages for the company going for scrip dividend is that they can earn

losses as well and if their stock does not perform as well as they expected it too, then the

loss that they might suffer double up (Ayodele, 2019).

Although, the scrip dividend option appears to be much more attractive than the option of

cash dividend yet the time and cost that is required is much more and therefore it might

not be the best option for the company since the cost overall increases.

Hence, the various advantages and disadvantages inherent to scrip dividend were evaluated for

the companies as well as their shareholders.

QUESTION 3: Investment Appraisal Techniques

Investment Appraisal Techniques is very useful in assessing the viability of the project

and portfolio which in turn is considered to be necessary for better decision making related to the

particular investment (Mayer and Schultmann, 2017). Investment Appraisal Techniques is useful

in evaluating the returns on the particular long term investment. It helps in selecting the

appropriate investment plan by analysing and predicting the results on the investment.

Investment Appraisal Techniques is important because it helps in maximization of the wealth of

the shareholders.

a.) Calculations

1. Payback Period

Formula of Payback period: Investment/ Cash Flows.

Initial Investment = £275000

Cash Flow = Inflow- outflow

= £85000- £12500

= £72500

Hence, Payback period = £275000/ £72500

= 3.79 years.

Interpretation: From the above carried out study it has been examined that, the life span

of the machinery is expected to be 6 years. On the other hand, the initial investment on

machinery is £275000. The annual cash flow of the company is estimated to be £72500. The

amount invested by the Lovewell Limited on the machinery is expected to be recovered on the

period of 3.79 years. Hence, the company should invest in the machinery because it's going to

give profitable returns in the future.

2. Accounting Rate of Return (ARR)

Formula of ARR: (Average of the Net profits/ Average Investments) * 100

Calculation of ARR:

(£33541.67/ £275000) * 100

= 12.19%

* WN 1: Computation of Depreciation every year:

Depreciation = (Cost of Investment - Salvage Value)/ Life of Investment

Depreciation = £233750/ 6

= £33958.33

Interpretation: From the above carried out study it has been examined that, the average

rate of return is expected to be 12.19%. Lovewell Limited company will take around 6 years in

order to receive the return of 12.19% on investment. The higher return on investment results in

higher generation of profits for the company in the mere future (Zhao, Xu and Jia, 2018).

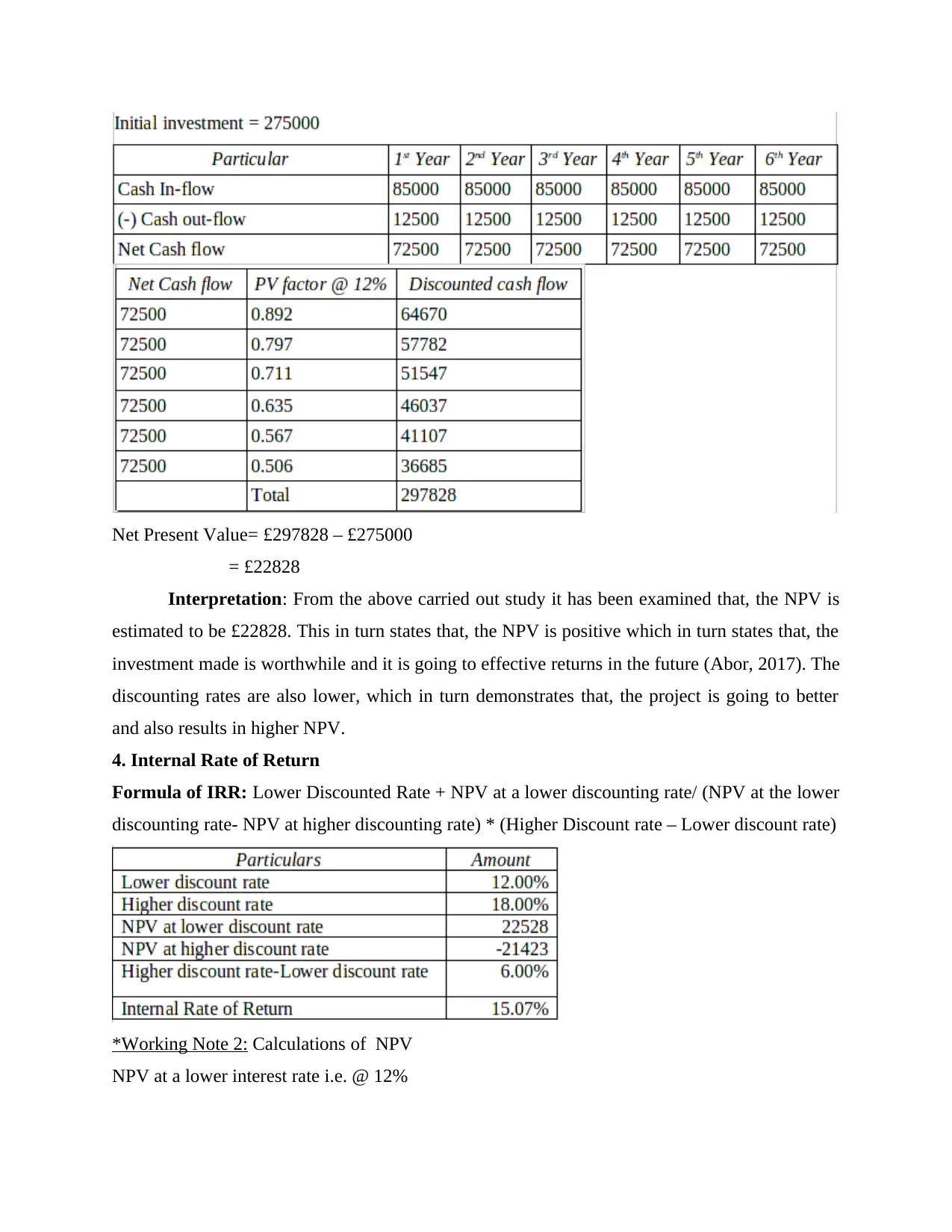

3. Net Present Value

Formula of NPV: Discounted Cash Flow – Initial Investment

amount invested by the Lovewell Limited on the machinery is expected to be recovered on the

period of 3.79 years. Hence, the company should invest in the machinery because it's going to

give profitable returns in the future.

2. Accounting Rate of Return (ARR)

Formula of ARR: (Average of the Net profits/ Average Investments) * 100

Calculation of ARR:

(£33541.67/ £275000) * 100

= 12.19%

* WN 1: Computation of Depreciation every year:

Depreciation = (Cost of Investment - Salvage Value)/ Life of Investment

Depreciation = £233750/ 6

= £33958.33

Interpretation: From the above carried out study it has been examined that, the average

rate of return is expected to be 12.19%. Lovewell Limited company will take around 6 years in

order to receive the return of 12.19% on investment. The higher return on investment results in

higher generation of profits for the company in the mere future (Zhao, Xu and Jia, 2018).

3. Net Present Value

Formula of NPV: Discounted Cash Flow – Initial Investment

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net Present Value= £297828 – £275000

= £22828

Interpretation: From the above carried out study it has been examined that, the NPV is

estimated to be £22828. This in turn states that, the NPV is positive which in turn states that, the

investment made is worthwhile and it is going to effective returns in the future (Abor, 2017). The

discounting rates are also lower, which in turn demonstrates that, the project is going to better

and also results in higher NPV.

4. Internal Rate of Return

Formula of IRR: Lower Discounted Rate + NPV at a lower discounting rate/ (NPV at the lower

discounting rate- NPV at higher discounting rate) * (Higher Discount rate – Lower discount rate)

*Working Note 2: Calculations of NPV

NPV at a lower interest rate i.e. @ 12%

= £22828

Interpretation: From the above carried out study it has been examined that, the NPV is

estimated to be £22828. This in turn states that, the NPV is positive which in turn states that, the

investment made is worthwhile and it is going to effective returns in the future (Abor, 2017). The

discounting rates are also lower, which in turn demonstrates that, the project is going to better

and also results in higher NPV.

4. Internal Rate of Return

Formula of IRR: Lower Discounted Rate + NPV at a lower discounting rate/ (NPV at the lower

discounting rate- NPV at higher discounting rate) * (Higher Discount rate – Lower discount rate)

*Working Note 2: Calculations of NPV

NPV at a lower interest rate i.e. @ 12%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

NPV= £297828 – £275000

= £22828

NPV at a higher interest rate i.e. @18%

NPV= £253576- £275000

= -£21424

Interpretation: From the above carried out study it has been examined that, the IRR is

estimated to be 15.07%. It has been evaluated that, the higher IRR of the project means higher

generation of cash and revenue into the company. It tends to add high degree of value to the

company in a long term.

b.) Critically evaluating the advantages and limitations of various investment appraisal

techniques.

The Payback Period

This investment accounting technique helps in recouping the funds which has been

expended in the particular investment project (Zativita and Chumaidiyah, 2019, May). Payback

period is the length of time which has been required in order to recover the cost on the particular

investment. Shorter pay back period is considered to be the most attractive investment plan. This

means the company will take short duration of time to recover the amount invested on the

= £22828

NPV at a higher interest rate i.e. @18%

NPV= £253576- £275000

= -£21424

Interpretation: From the above carried out study it has been examined that, the IRR is

estimated to be 15.07%. It has been evaluated that, the higher IRR of the project means higher

generation of cash and revenue into the company. It tends to add high degree of value to the

company in a long term.

b.) Critically evaluating the advantages and limitations of various investment appraisal

techniques.

The Payback Period

This investment accounting technique helps in recouping the funds which has been

expended in the particular investment project (Zativita and Chumaidiyah, 2019, May). Payback

period is the length of time which has been required in order to recover the cost on the particular

investment. Shorter pay back period is considered to be the most attractive investment plan. This

means the company will take short duration of time to recover the amount invested on the

particular project. On the other hand, longer pay back period is considered to be less attractive

investment plan.

Advantages of Payback Period

It is considered to be one of the most easy and simple way to compare several investment

projects and make necessary decision. It is considered to be one of the effective investment

appraisal technique which is useful in assessing the risk on particular investment project.

Limitations of Payback Period

One of the key disadvantage of the payback period is that, it tends to ignore the time

value of the money (Wijesuriya and et.al., 2017). It also tends to ignore the cash inflows after the

payback period and the profitability of the specific project. It also does not consider ROI on the

project.

The Accounting Rate of Return

This is the percentage return which is useful in measuring the anticipated profitability of

the investment project. It enables investors to effectively analyse the viability of the project by

analysing the risk involved in specific investment project.

Advantages of ARR

One of the key advantage of the ARR is that, it is useful in measuring the current

performance of the particular project (Accounting Rate of Return (ARR) Method | Advantages |

Disadvantages, 2020). It is a very easy approach and it also tends to consider total savings over

the economic life of the project.

Limitations of ARR

This method does not take into consideration increased risk and variability of the

prolonged project. This technique is not considered to be ideal for comparing two different

projects because of the variation in the variable and various other non- financial and time factors.

The major disadvantage is that, it tends to ignore the time value of the money.

Net Present Value

It is an effective procedure which helps in analysing the profit of a particular project

(Temizel and et.al., 2018, March). Positive NPV results in higher generation of cash inflows

within the company which leads to higher profitability. On the contrary, lower NPV states that,

project is not beneficial. NPV is considered to be an effective tool which is very useful in

maximizing the wealth by showing greater return on the investment.

investment plan.

Advantages of Payback Period

It is considered to be one of the most easy and simple way to compare several investment

projects and make necessary decision. It is considered to be one of the effective investment

appraisal technique which is useful in assessing the risk on particular investment project.

Limitations of Payback Period

One of the key disadvantage of the payback period is that, it tends to ignore the time

value of the money (Wijesuriya and et.al., 2017). It also tends to ignore the cash inflows after the

payback period and the profitability of the specific project. It also does not consider ROI on the

project.

The Accounting Rate of Return

This is the percentage return which is useful in measuring the anticipated profitability of

the investment project. It enables investors to effectively analyse the viability of the project by

analysing the risk involved in specific investment project.

Advantages of ARR

One of the key advantage of the ARR is that, it is useful in measuring the current

performance of the particular project (Accounting Rate of Return (ARR) Method | Advantages |

Disadvantages, 2020). It is a very easy approach and it also tends to consider total savings over

the economic life of the project.

Limitations of ARR

This method does not take into consideration increased risk and variability of the

prolonged project. This technique is not considered to be ideal for comparing two different

projects because of the variation in the variable and various other non- financial and time factors.

The major disadvantage is that, it tends to ignore the time value of the money.

Net Present Value

It is an effective procedure which helps in analysing the profit of a particular project

(Temizel and et.al., 2018, March). Positive NPV results in higher generation of cash inflows

within the company which leads to higher profitability. On the contrary, lower NPV states that,

project is not beneficial. NPV is considered to be an effective tool which is very useful in

maximizing the wealth by showing greater return on the investment.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.