Financial Management: Valuation and Investment Appraisal Assignment

VerifiedAdded on 2023/01/06

|14

|4117

|100

Homework Assignment

AI Summary

This assignment solution addresses key concepts in financial management, focusing on valuation techniques and investment appraisal. It begins by explaining and calculating the Price Earnings Ratio (PER), Dividend Valuation Method (DVM), and Discounted Cash Flow (DCF) methods, providing formulas and examples to illustrate each. The solution then critically discusses the limitations and problems associated with each valuation technique, providing a balanced perspective on their practical applications. Furthermore, the assignment explores investment appraisal techniques, including payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR), with detailed calculations and interpretations to assess the viability of a potential investment in new machinery for Lovewell Ltd. The solution concludes with a critical evaluation of these techniques, comparing their strengths and weaknesses to provide a comprehensive understanding of financial decision-making.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

QUESTION 2

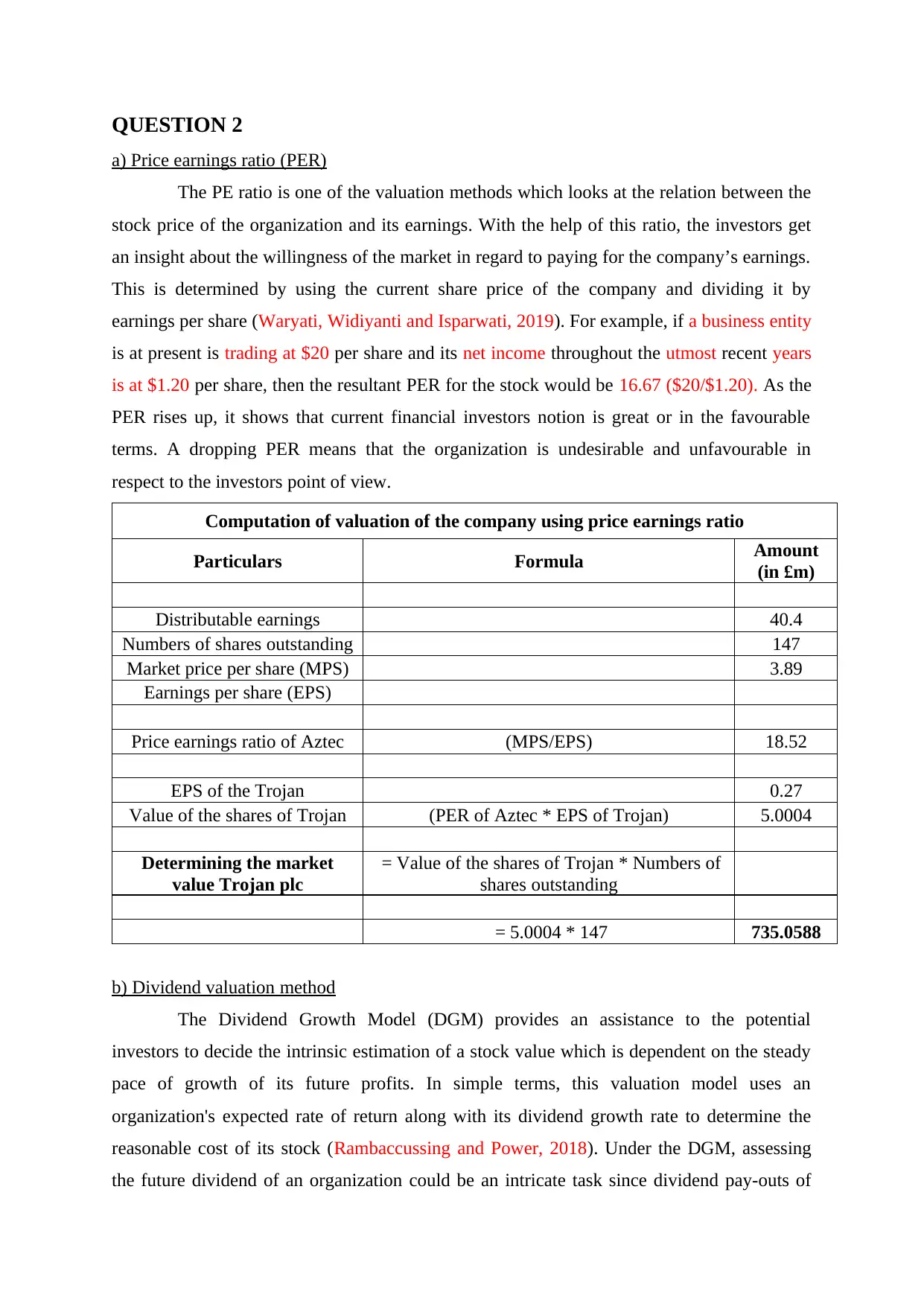

a) Price earnings ratio (PER)

The PE ratio is one of the valuation methods which looks at the relation between the

stock price of the organization and its earnings. With the help of this ratio, the investors get

an insight about the willingness of the market in regard to paying for the company’s earnings.

This is determined by using the current share price of the company and dividing it by

earnings per share (Waryati, Widiyanti and Isparwati, 2019). For example, if a business entity

is at present is trading at $20 per share and its net income throughout the utmost recent years

is at $1.20 per share, then the resultant PER for the stock would be 16.67 ($20/$1.20). As the

PER rises up, it shows that current financial investors notion is great or in the favourable

terms. A dropping PER means that the organization is undesirable and unfavourable in

respect to the investors point of view.

Computation of valuation of the company using price earnings ratio

Particulars Formula Amount

(in £m)

Distributable earnings 40.4

Numbers of shares outstanding 147

Market price per share (MPS) 3.89

Earnings per share (EPS)

Price earnings ratio of Aztec (MPS/EPS) 18.52

EPS of the Trojan 0.27

Value of the shares of Trojan (PER of Aztec * EPS of Trojan) 5.0004

Determining the market

value Trojan plc

= Value of the shares of Trojan * Numbers of

shares outstanding

= 5.0004 * 147 735.0588

b) Dividend valuation method

The Dividend Growth Model (DGM) provides an assistance to the potential

investors to decide the intrinsic estimation of a stock value which is dependent on the steady

pace of growth of its future profits. In simple terms, this valuation model uses an

organization's expected rate of return along with its dividend growth rate to determine the

reasonable cost of its stock (Rambaccussing and Power, 2018). Under the DGM, assessing

the future dividend of an organization could be an intricate task since dividend pay-outs of

a) Price earnings ratio (PER)

The PE ratio is one of the valuation methods which looks at the relation between the

stock price of the organization and its earnings. With the help of this ratio, the investors get

an insight about the willingness of the market in regard to paying for the company’s earnings.

This is determined by using the current share price of the company and dividing it by

earnings per share (Waryati, Widiyanti and Isparwati, 2019). For example, if a business entity

is at present is trading at $20 per share and its net income throughout the utmost recent years

is at $1.20 per share, then the resultant PER for the stock would be 16.67 ($20/$1.20). As the

PER rises up, it shows that current financial investors notion is great or in the favourable

terms. A dropping PER means that the organization is undesirable and unfavourable in

respect to the investors point of view.

Computation of valuation of the company using price earnings ratio

Particulars Formula Amount

(in £m)

Distributable earnings 40.4

Numbers of shares outstanding 147

Market price per share (MPS) 3.89

Earnings per share (EPS)

Price earnings ratio of Aztec (MPS/EPS) 18.52

EPS of the Trojan 0.27

Value of the shares of Trojan (PER of Aztec * EPS of Trojan) 5.0004

Determining the market

value Trojan plc

= Value of the shares of Trojan * Numbers of

shares outstanding

= 5.0004 * 147 735.0588

b) Dividend valuation method

The Dividend Growth Model (DGM) provides an assistance to the potential

investors to decide the intrinsic estimation of a stock value which is dependent on the steady

pace of growth of its future profits. In simple terms, this valuation model uses an

organization's expected rate of return along with its dividend growth rate to determine the

reasonable cost of its stock (Rambaccussing and Power, 2018). Under the DGM, assessing

the future dividend of an organization could be an intricate task since dividend pay-outs of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

organizations may change because of different factors, for example, economic situations,

benefit, etc. The DGM varies from the DDM in that it accepts a steady and constant rate of

growth of dividend. DGM is helpful in investigating the estimation of stable organizations

with great income and consistent profit growth rates. Yet, truly, it is hard for organizations to

accomplish a consistent growth rate because of different extraneous elements that influence

their gainfulness and growth.

Computation of valuation of the company using Dividend valuation

method

Particulars Formula Amount (in

£m)

Information provided:

Latest dividend payment (Current dividend) 0.13

Growth rate (GR)

= 0.10(1+g)

^5 = 0.13 5.00%

0.05

Risk free rate (Rf) 5.00%

Beta (β) 1.10%

Number of shares 147

Return on market (Rm) 11.00%

For determining expected rate of return (K),

CAPM model will be used

According to CAPM, K is = Rf + (Rm-

Rf) β

=5% + (11%

- 5%) * 1.1% 5.07%

Market value per share

= 0.13 *

(1+5%)/

(5.07%-5%)

195

Evaluating the market value Trojan plc

= Market

price per

share *

Number of

shares

28665

benefit, etc. The DGM varies from the DDM in that it accepts a steady and constant rate of

growth of dividend. DGM is helpful in investigating the estimation of stable organizations

with great income and consistent profit growth rates. Yet, truly, it is hard for organizations to

accomplish a consistent growth rate because of different extraneous elements that influence

their gainfulness and growth.

Computation of valuation of the company using Dividend valuation

method

Particulars Formula Amount (in

£m)

Information provided:

Latest dividend payment (Current dividend) 0.13

Growth rate (GR)

= 0.10(1+g)

^5 = 0.13 5.00%

0.05

Risk free rate (Rf) 5.00%

Beta (β) 1.10%

Number of shares 147

Return on market (Rm) 11.00%

For determining expected rate of return (K),

CAPM model will be used

According to CAPM, K is = Rf + (Rm-

Rf) β

=5% + (11%

- 5%) * 1.1% 5.07%

Market value per share

= 0.13 *

(1+5%)/

(5.07%-5%)

195

Evaluating the market value Trojan plc

= Market

price per

share *

Number of

shares

28665

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

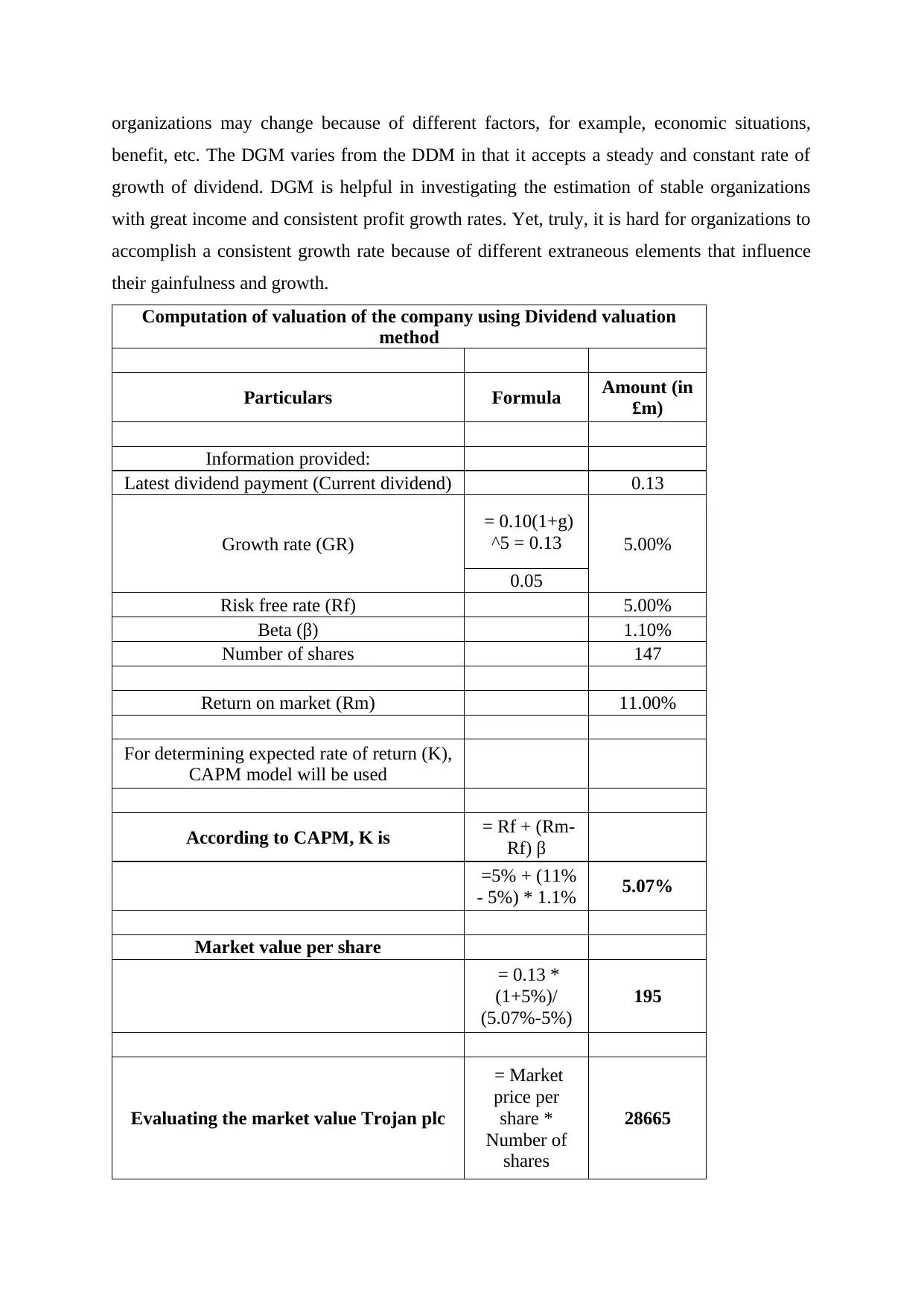

c) Discounted cash flow method (DCF)

The DCF valuation approach involves the net present worth (NPV) of the projected

incomes which is made available to the prospected investors who is willing to provide

capital, actual amount which is needed to be contributed creating the projected growth. The

idea of DCF approach of valuing the business depends on the concept that the estimation of a

corporate or resource is intrinsically dependent on its ability to create incomes for the

investors of the funds (Bayar and Liu, 2020). Along with that, the DCF model relied more on

the principal desires for the corporate than on open market factors or historical base for

reference, and it is a more in the context of the theoretical aspect which is relied upon

assumptions. A DCF investigation produces the general assessment of a corporate (for

example enterprise value), including both obligation and value.

Computation of valuation of the company using Discounted cash flow

method

Particulars Formula Amount (in

£m)

Evaluating the free cash flow

Net income (NI) 40.4

Less: Increase in working capital -

Less: Capital expenditure -

Add: Non-cash expenses -

Free cash flow (FCF) 40.4

Discounting rate or WACC 9.00%

MPS = Free cash

flow /

Discounting

rate

448.89

Market value of Trojan plc

= MPS *

Number of

shares

= 448.89 *

147 65986.67

The DCF valuation approach involves the net present worth (NPV) of the projected

incomes which is made available to the prospected investors who is willing to provide

capital, actual amount which is needed to be contributed creating the projected growth. The

idea of DCF approach of valuing the business depends on the concept that the estimation of a

corporate or resource is intrinsically dependent on its ability to create incomes for the

investors of the funds (Bayar and Liu, 2020). Along with that, the DCF model relied more on

the principal desires for the corporate than on open market factors or historical base for

reference, and it is a more in the context of the theoretical aspect which is relied upon

assumptions. A DCF investigation produces the general assessment of a corporate (for

example enterprise value), including both obligation and value.

Computation of valuation of the company using Discounted cash flow

method

Particulars Formula Amount (in

£m)

Evaluating the free cash flow

Net income (NI) 40.4

Less: Increase in working capital -

Less: Capital expenditure -

Add: Non-cash expenses -

Free cash flow (FCF) 40.4

Discounting rate or WACC 9.00%

MPS = Free cash

flow /

Discounting

rate

448.89

Market value of Trojan plc

= MPS *

Number of

shares

= 448.89 *

147 65986.67

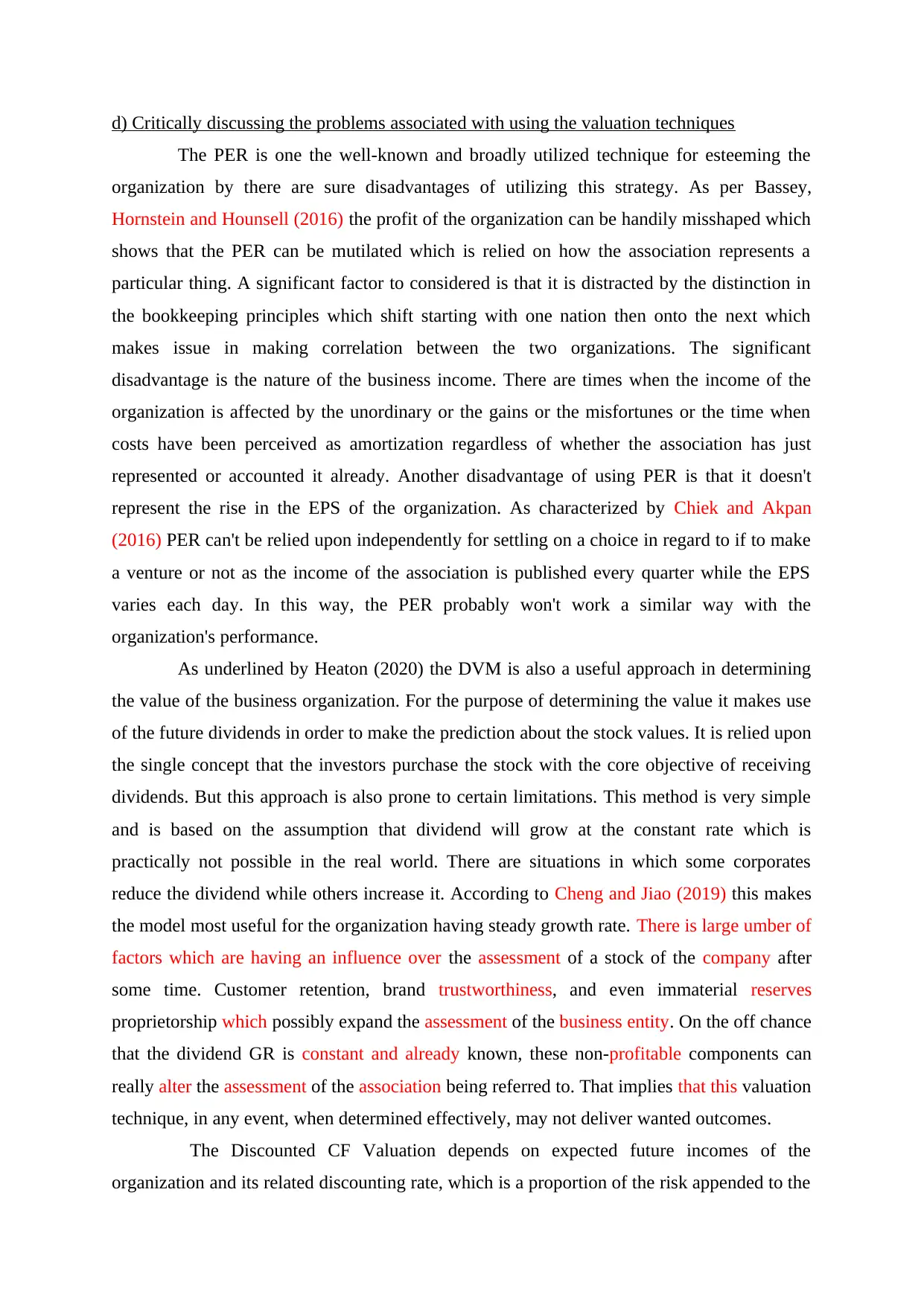

d) Critically discussing the problems associated with using the valuation techniques

The PER is one the well-known and broadly utilized technique for esteeming the

organization by there are sure disadvantages of utilizing this strategy. As per Bassey,

Hornstein and Hounsell (2016) the profit of the organization can be handily misshaped which

shows that the PER can be mutilated which is relied on how the association represents a

particular thing. A significant factor to considered is that it is distracted by the distinction in

the bookkeeping principles which shift starting with one nation then onto the next which

makes issue in making correlation between the two organizations. The significant

disadvantage is the nature of the business income. There are times when the income of the

organization is affected by the unordinary or the gains or the misfortunes or the time when

costs have been perceived as amortization regardless of whether the association has just

represented or accounted it already. Another disadvantage of using PER is that it doesn't

represent the rise in the EPS of the organization. As characterized by Chiek and Akpan

(2016) PER can't be relied upon independently for settling on a choice in regard to if to make

a venture or not as the income of the association is published every quarter while the EPS

varies each day. In this way, the PER probably won't work a similar way with the

organization's performance.

As underlined by Heaton (2020) the DVM is also a useful approach in determining

the value of the business organization. For the purpose of determining the value it makes use

of the future dividends in order to make the prediction about the stock values. It is relied upon

the single concept that the investors purchase the stock with the core objective of receiving

dividends. But this approach is also prone to certain limitations. This method is very simple

and is based on the assumption that dividend will grow at the constant rate which is

practically not possible in the real world. There are situations in which some corporates

reduce the dividend while others increase it. According to Cheng and Jiao (2019) this makes

the model most useful for the organization having steady growth rate. There is large umber of

factors which are having an influence over the assessment of a stock of the company after

some time. Customer retention, brand trustworthiness, and even immaterial reserves

proprietorship which possibly expand the assessment of the business entity. On the off chance

that the dividend GR is constant and already known, these non-profitable components can

really alter the assessment of the association being referred to. That implies that this valuation

technique, in any event, when determined effectively, may not deliver wanted outcomes.

The Discounted CF Valuation depends on expected future incomes of the

organization and its related discounting rate, which is a proportion of the risk appended to the

The PER is one the well-known and broadly utilized technique for esteeming the

organization by there are sure disadvantages of utilizing this strategy. As per Bassey,

Hornstein and Hounsell (2016) the profit of the organization can be handily misshaped which

shows that the PER can be mutilated which is relied on how the association represents a

particular thing. A significant factor to considered is that it is distracted by the distinction in

the bookkeeping principles which shift starting with one nation then onto the next which

makes issue in making correlation between the two organizations. The significant

disadvantage is the nature of the business income. There are times when the income of the

organization is affected by the unordinary or the gains or the misfortunes or the time when

costs have been perceived as amortization regardless of whether the association has just

represented or accounted it already. Another disadvantage of using PER is that it doesn't

represent the rise in the EPS of the organization. As characterized by Chiek and Akpan

(2016) PER can't be relied upon independently for settling on a choice in regard to if to make

a venture or not as the income of the association is published every quarter while the EPS

varies each day. In this way, the PER probably won't work a similar way with the

organization's performance.

As underlined by Heaton (2020) the DVM is also a useful approach in determining

the value of the business organization. For the purpose of determining the value it makes use

of the future dividends in order to make the prediction about the stock values. It is relied upon

the single concept that the investors purchase the stock with the core objective of receiving

dividends. But this approach is also prone to certain limitations. This method is very simple

and is based on the assumption that dividend will grow at the constant rate which is

practically not possible in the real world. There are situations in which some corporates

reduce the dividend while others increase it. According to Cheng and Jiao (2019) this makes

the model most useful for the organization having steady growth rate. There is large umber of

factors which are having an influence over the assessment of a stock of the company after

some time. Customer retention, brand trustworthiness, and even immaterial reserves

proprietorship which possibly expand the assessment of the business entity. On the off chance

that the dividend GR is constant and already known, these non-profitable components can

really alter the assessment of the association being referred to. That implies that this valuation

technique, in any event, when determined effectively, may not deliver wanted outcomes.

The Discounted CF Valuation depends on expected future incomes of the

organization and its related discounting rate, which is a proportion of the risk appended to the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

business in general way and specifically to the organization. As defined by Neaxie and

Hendrawan (2017) DCF Valuation, this methodology is simplest to use for resources,

organizations, and so forth whose sources of income are at present certain and can be

estimated with some dependability, and where an intermediary for risk that can be utilized to

get the discounting rates is accessible. DCF Valuation is incredibly sensitive to the

presumptions identified with the perpetual GR and the discounting rate. Any minor mistake

in the assumption, and the DCF Valuation will vary uncontrollably and the reasonable worth

of the organization will not be accurate.

As defined by Komikov (2020) the DCF model works good and well when there is a

serious extent of certainty in regard to the future incomes. However, in the event that the

administration's activities require perceivability, it gets complex to forecast the sales,

employed costs and capital investment with conviction. While estimating incomes for the

upcoming years is not an easy task. In that capacity, DCF strategy is increases the chances of

blunder if not appropriately represented these information sources. One of the major

drawbacks of this valuation method is that the terminal values involves nearly 65% to 75% of

the total value and in case there is a minor error in making these assumptions in respect to the

terminal values then it would have a significant influence over the organization’s valuation.

In light of the basic examination, it very well may be stated that the PER is the most

reasonable technique for valuation reason which is on the grounds that despite the fact that it

is inclined to certain downsides yet it is not a risky attempt for valuing the business and this

methodology is generally utilized by the partners or the organizations. Alongside it, it is

exceptionally simple to figure out and comprehend.

QUESTION 3

1. Presenting investment appraisal techniques

Computation of cash inflows

Year Cash

inflow

Cash

outflow

Less:

Depreciation

Gross

Profit EBIT

1 85000 12500 38958.33 33541.

7 72500

2 85000 12500 38958.33 33541.

7 72500

3 85000 12500 38958.33 33541.

7 72500

4 85000 12500 38958.33 33541.

7 72500

Hendrawan (2017) DCF Valuation, this methodology is simplest to use for resources,

organizations, and so forth whose sources of income are at present certain and can be

estimated with some dependability, and where an intermediary for risk that can be utilized to

get the discounting rates is accessible. DCF Valuation is incredibly sensitive to the

presumptions identified with the perpetual GR and the discounting rate. Any minor mistake

in the assumption, and the DCF Valuation will vary uncontrollably and the reasonable worth

of the organization will not be accurate.

As defined by Komikov (2020) the DCF model works good and well when there is a

serious extent of certainty in regard to the future incomes. However, in the event that the

administration's activities require perceivability, it gets complex to forecast the sales,

employed costs and capital investment with conviction. While estimating incomes for the

upcoming years is not an easy task. In that capacity, DCF strategy is increases the chances of

blunder if not appropriately represented these information sources. One of the major

drawbacks of this valuation method is that the terminal values involves nearly 65% to 75% of

the total value and in case there is a minor error in making these assumptions in respect to the

terminal values then it would have a significant influence over the organization’s valuation.

In light of the basic examination, it very well may be stated that the PER is the most

reasonable technique for valuation reason which is on the grounds that despite the fact that it

is inclined to certain downsides yet it is not a risky attempt for valuing the business and this

methodology is generally utilized by the partners or the organizations. Alongside it, it is

exceptionally simple to figure out and comprehend.

QUESTION 3

1. Presenting investment appraisal techniques

Computation of cash inflows

Year Cash

inflow

Cash

outflow

Less:

Depreciation

Gross

Profit EBIT

1 85000 12500 38958.33 33541.

7 72500

2 85000 12500 38958.33 33541.

7 72500

3 85000 12500 38958.33 33541.

7 72500

4 85000 12500 38958.33 33541.

7 72500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

5 85000 12500 38958.33 33541.

7 72500

6 85000 12500 38958.33 33541.

7 72500

Calculating amount of depreciation

Cost of asset 275000

Useful life of the asset 6

Estimated salvage value 275000*15%

41250

Depreciation

(cost of asset - estimated salvage value) /

Useful of the asset

(275000-41250)/6

38958.33

a. Payback Period

Year

Net

Cash

flow

Cumulative cash

flow

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 11375

0 476250

Payback

Period

3 + (275000 –

217500)

= 3 + (57500 /

72500)

3.8 years

b. Accounting Rate of return

Year Cash

flow

Depreciati

on

Annual

profit

1 72500 38958.3 33541.6

7

2 72500 38958.3 33541.6

7

3 72500 38958.3 33541.6

7

4 72500 38958.3 33541.6

7

5 72500 38958.3 33541.6

7

7 72500

6 85000 12500 38958.33 33541.

7 72500

Calculating amount of depreciation

Cost of asset 275000

Useful life of the asset 6

Estimated salvage value 275000*15%

41250

Depreciation

(cost of asset - estimated salvage value) /

Useful of the asset

(275000-41250)/6

38958.33

a. Payback Period

Year

Net

Cash

flow

Cumulative cash

flow

1 72500 72500

2 72500 145000

3 72500 217500

4 72500 290000

5 72500 362500

6 11375

0 476250

Payback

Period

3 + (275000 –

217500)

= 3 + (57500 /

72500)

3.8 years

b. Accounting Rate of return

Year Cash

flow

Depreciati

on

Annual

profit

1 72500 38958.3 33541.6

7

2 72500 38958.3 33541.6

7

3 72500 38958.3 33541.6

7

4 72500 38958.3 33541.6

7

5 72500 38958.3 33541.6

7

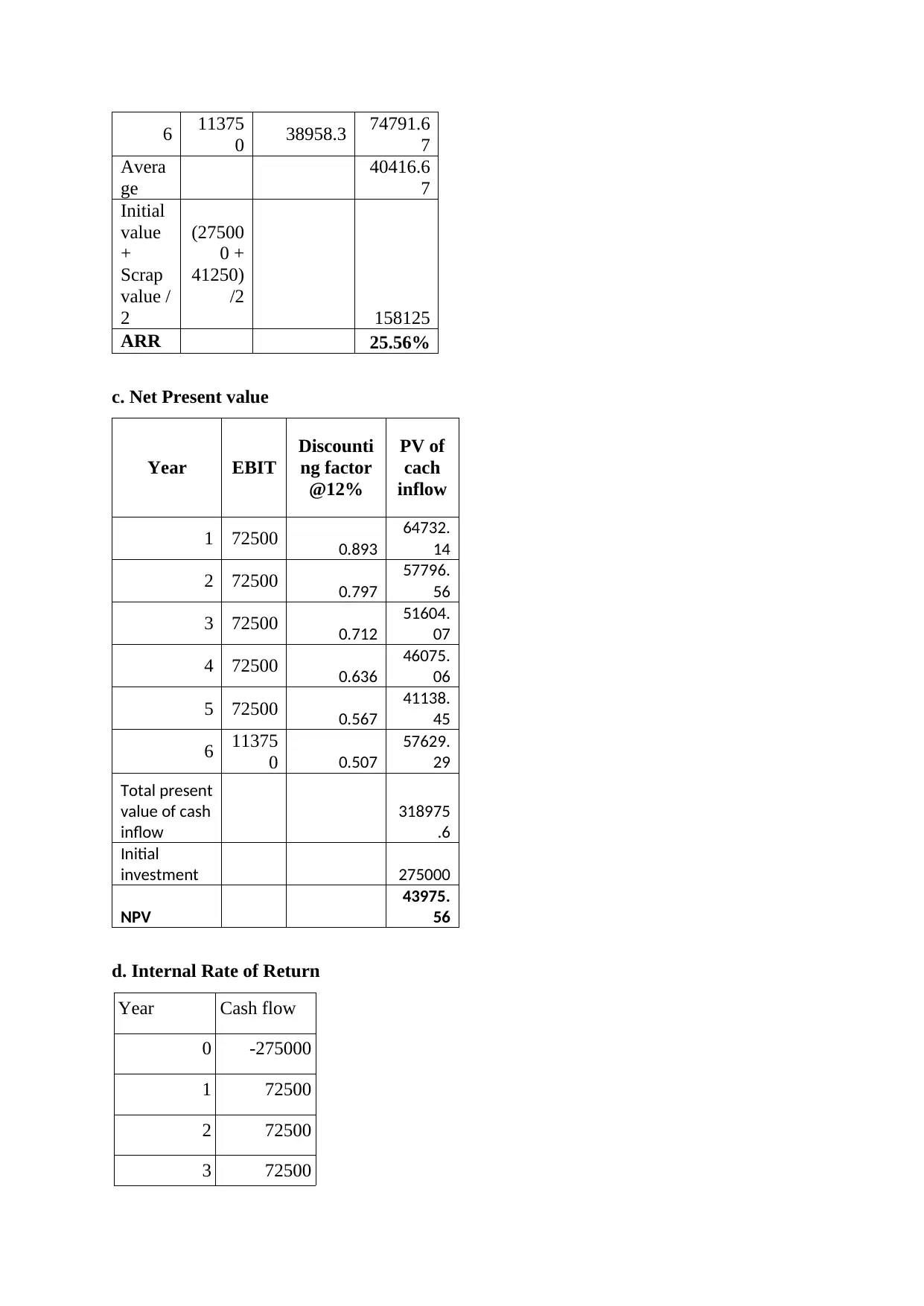

6 11375

0 38958.3 74791.6

7

Avera

ge

40416.6

7

Initial

value

+

Scrap

value /

2

(27500

0 +

41250)

/2

158125

ARR 25.56%

c. Net Present value

Year EBIT

Discounti

ng factor

@12%

PV of

cach

inflow

1 72500 0.893

64732.

14

2 72500 0.797

57796.

56

3 72500 0.712

51604.

07

4 72500 0.636

46075.

06

5 72500 0.567

41138.

45

6 11375

0 0.507

57629.

29

Total present

value of cash

inflow

318975

.6

Initial

investment 275000

NPV

43975.

56

d. Internal Rate of Return

Year Cash flow

0 -275000

1 72500

2 72500

3 72500

0 38958.3 74791.6

7

Avera

ge

40416.6

7

Initial

value

+

Scrap

value /

2

(27500

0 +

41250)

/2

158125

ARR 25.56%

c. Net Present value

Year EBIT

Discounti

ng factor

@12%

PV of

cach

inflow

1 72500 0.893

64732.

14

2 72500 0.797

57796.

56

3 72500 0.712

51604.

07

4 72500 0.636

46075.

06

5 72500 0.567

41138.

45

6 11375

0 0.507

57629.

29

Total present

value of cash

inflow

318975

.6

Initial

investment 275000

NPV

43975.

56

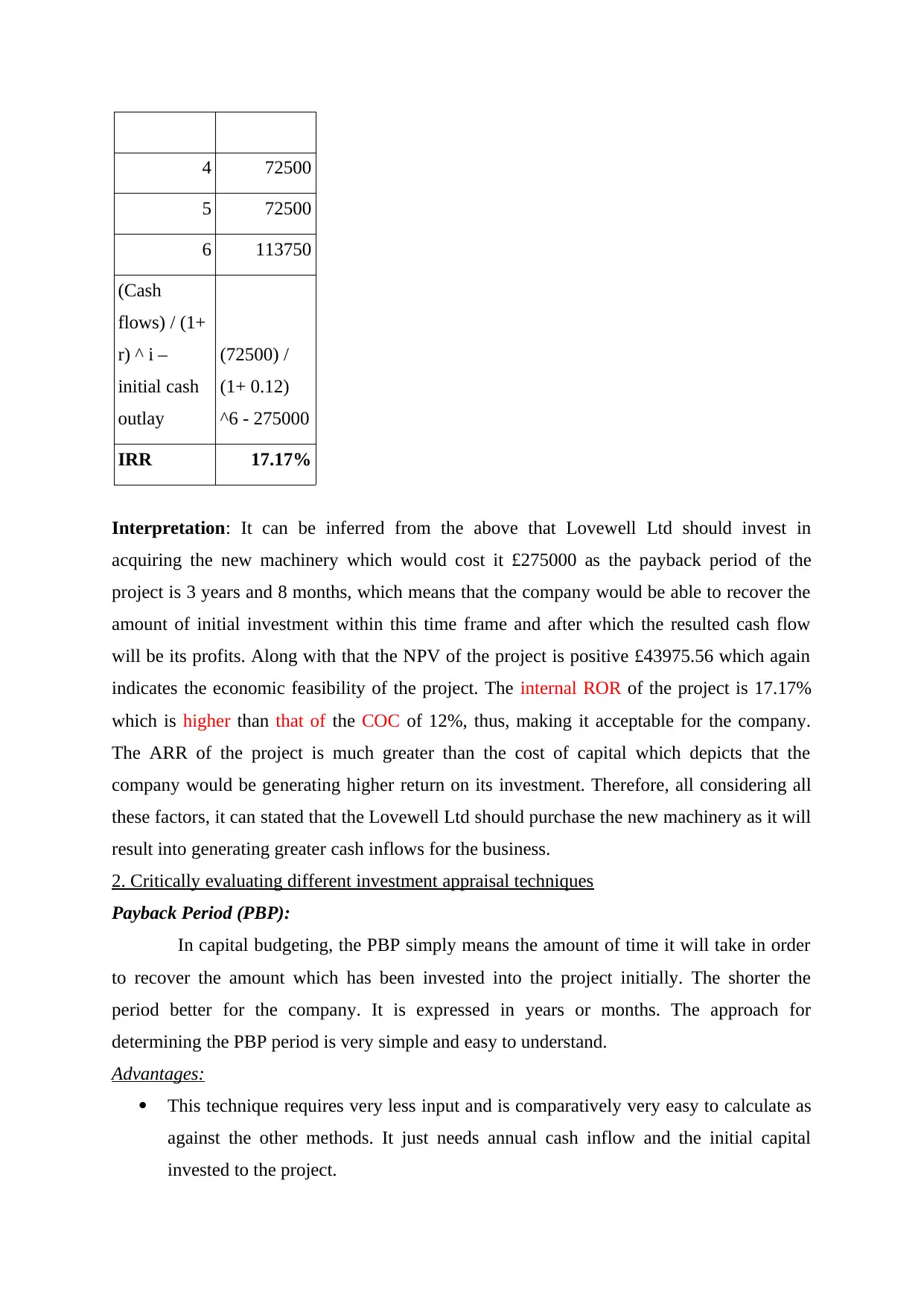

d. Internal Rate of Return

Year Cash flow

0 -275000

1 72500

2 72500

3 72500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

4 72500

5 72500

6 113750

(Cash

flows) / (1+

r) ^ i –

initial cash

outlay

(72500) /

(1+ 0.12)

^6 - 275000

IRR 17.17%

Interpretation: It can be inferred from the above that Lovewell Ltd should invest in

acquiring the new machinery which would cost it £275000 as the payback period of the

project is 3 years and 8 months, which means that the company would be able to recover the

amount of initial investment within this time frame and after which the resulted cash flow

will be its profits. Along with that the NPV of the project is positive £43975.56 which again

indicates the economic feasibility of the project. The internal ROR of the project is 17.17%

which is higher than that of the COC of 12%, thus, making it acceptable for the company.

The ARR of the project is much greater than the cost of capital which depicts that the

company would be generating higher return on its investment. Therefore, all considering all

these factors, it can stated that the Lovewell Ltd should purchase the new machinery as it will

result into generating greater cash inflows for the business.

2. Critically evaluating different investment appraisal techniques

Payback Period (PBP):

In capital budgeting, the PBP simply means the amount of time it will take in order

to recover the amount which has been invested into the project initially. The shorter the

period better for the company. It is expressed in years or months. The approach for

determining the PBP period is very simple and easy to understand.

Advantages:

This technique requires very less input and is comparatively very easy to calculate as

against the other methods. It just needs annual cash inflow and the initial capital

invested to the project.

5 72500

6 113750

(Cash

flows) / (1+

r) ^ i –

initial cash

outlay

(72500) /

(1+ 0.12)

^6 - 275000

IRR 17.17%

Interpretation: It can be inferred from the above that Lovewell Ltd should invest in

acquiring the new machinery which would cost it £275000 as the payback period of the

project is 3 years and 8 months, which means that the company would be able to recover the

amount of initial investment within this time frame and after which the resulted cash flow

will be its profits. Along with that the NPV of the project is positive £43975.56 which again

indicates the economic feasibility of the project. The internal ROR of the project is 17.17%

which is higher than that of the COC of 12%, thus, making it acceptable for the company.

The ARR of the project is much greater than the cost of capital which depicts that the

company would be generating higher return on its investment. Therefore, all considering all

these factors, it can stated that the Lovewell Ltd should purchase the new machinery as it will

result into generating greater cash inflows for the business.

2. Critically evaluating different investment appraisal techniques

Payback Period (PBP):

In capital budgeting, the PBP simply means the amount of time it will take in order

to recover the amount which has been invested into the project initially. The shorter the

period better for the company. It is expressed in years or months. The approach for

determining the PBP period is very simple and easy to understand.

Advantages:

This technique requires very less input and is comparatively very easy to calculate as

against the other methods. It just needs annual cash inflow and the initial capital

invested to the project.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

It provides crucial information which other methods fails to provide. Under this,

usually projects having a shorter PBP is also carrying lower risk (Ali and Hashlamun,

2019). This is important to the businesses which are having limited resources and

requires to quickly recover the amount invested.

This is beneficial in the industries which are uncertain and faces rapid change in

technology. These uncertainty results into making future cash inflows difficult. Thus,

focusing on projects with lower PBP helps in reducing the chances of loss.

Disadvantages:

The key downside of it is that it does not account for the time value of money and

therefore, affecting the actual value of the cash flow.

This method only considers the cash flows until the amount initially invested is

recovered. It does not consider cash flow generating after that time frame (Kim, Park

and Sawng, 2018). This cause looking the true potential of the project as there are

times when the lucrative cash flow s generated later on years.

It does not account for the profits as the shorter PBP does not provide any guarantee

the profitability. There are times when the cash flow from the project stops or reduces

after the PBP making the project not feasible.

Accounting rate of return (ARR):

The ARR provides the rate of return from the amount invested in the project. In

other words, it gives the accounting profits which is being arisen from the investment made in

the form of a percentage.

Advantages

Just like PBP it is very simple and easy to determine the value. It just requires the

total profits over the entire life of the venture (Torabi, Giahi and Sahebjamnia, 2016).

This approach undertakes the concept of net earnings after tax and depreciation. This

is considered as a crucial factor in capital budgeting.

This technique encourages the comparison of new project venture with that of cost

diminishing undertaking or other different investment proposals of similar nature.

This technique provides a clear depiction of the gainfulness of a task and is valuable

to quantify current performance level of the company.

Disadvantages:

It creates a problem if one calculates the ROI and others ARR as it will make the

situation complex in carrying out the decision.

usually projects having a shorter PBP is also carrying lower risk (Ali and Hashlamun,

2019). This is important to the businesses which are having limited resources and

requires to quickly recover the amount invested.

This is beneficial in the industries which are uncertain and faces rapid change in

technology. These uncertainty results into making future cash inflows difficult. Thus,

focusing on projects with lower PBP helps in reducing the chances of loss.

Disadvantages:

The key downside of it is that it does not account for the time value of money and

therefore, affecting the actual value of the cash flow.

This method only considers the cash flows until the amount initially invested is

recovered. It does not consider cash flow generating after that time frame (Kim, Park

and Sawng, 2018). This cause looking the true potential of the project as there are

times when the lucrative cash flow s generated later on years.

It does not account for the profits as the shorter PBP does not provide any guarantee

the profitability. There are times when the cash flow from the project stops or reduces

after the PBP making the project not feasible.

Accounting rate of return (ARR):

The ARR provides the rate of return from the amount invested in the project. In

other words, it gives the accounting profits which is being arisen from the investment made in

the form of a percentage.

Advantages

Just like PBP it is very simple and easy to determine the value. It just requires the

total profits over the entire life of the venture (Torabi, Giahi and Sahebjamnia, 2016).

This approach undertakes the concept of net earnings after tax and depreciation. This

is considered as a crucial factor in capital budgeting.

This technique encourages the comparison of new project venture with that of cost

diminishing undertaking or other different investment proposals of similar nature.

This technique provides a clear depiction of the gainfulness of a task and is valuable

to quantify current performance level of the company.

Disadvantages:

It creates a problem if one calculates the ROI and others ARR as it will make the

situation complex in carrying out the decision.

This approach ignores time value of money which is its biggest weakness. Along with

that, the fair rate cannot be determined by using ARR.

It does not take into account the outside aspects which has a higher influence on the

profitability of the business entity (Ejoh, Okpa and Ibanga, 2016).

It does not consider the time period in which profit is earned, such as, 18% ROR in 10

years would be more favorable than the 14% ROR which is for 6 years. This is not

correct as the longer is the time frame, greater is the risk involved.

Net Present Value (NPV):

This technique of investment appraisal provides information on whether the total

cash flow that will be generated by the investment will exceed the cost involved in it. The

resulting outcome can be either positive or negative. The positive means that project is

generating positive cash flow while negative means that the project won’t be able to exceed

the cost.

Advantages:

This method can be implemented very easily if the discounting rate and annual cash

inflow is provided. Under this, the discounting rate is decided by the management

which can be adjusted with the risk prevailing within the industry along with the other

important factors which are essential for getting the desired output.

NPV also considers the inflation rate in order to determine the right future

profitability and cash inflow (Michalkova and Spuchlakova, 2017). Thus, it considers

the time factor for determining the present value of future cash flow.

Through this, multiple projects can be compared with the same expected life under the

situation of mutually exclusive projects. This helps in selecting the most appropriate

and economically feasible project.

Disadvantages:

There are chances that it becomes difficult to calculate the opportunity which is

mainly considered in the initial outlay and thus, underestimating the initial cash

outflow would might distort the end result. Along with that, the sunk cost is also not

included which mainly includes the research and development cost incurred before

initiating the project.

The rate at which the cash flows are to be discounted is very difficult to determine.

Many a times firms make use of the WACC as the discount rate but it should be the

projects ROR and therefore, the wrong discounting rate might result into making

wrong estimation causing incorrect NPV value (Baker, Jabbouri and Dyaz, 2017). The

that, the fair rate cannot be determined by using ARR.

It does not take into account the outside aspects which has a higher influence on the

profitability of the business entity (Ejoh, Okpa and Ibanga, 2016).

It does not consider the time period in which profit is earned, such as, 18% ROR in 10

years would be more favorable than the 14% ROR which is for 6 years. This is not

correct as the longer is the time frame, greater is the risk involved.

Net Present Value (NPV):

This technique of investment appraisal provides information on whether the total

cash flow that will be generated by the investment will exceed the cost involved in it. The

resulting outcome can be either positive or negative. The positive means that project is

generating positive cash flow while negative means that the project won’t be able to exceed

the cost.

Advantages:

This method can be implemented very easily if the discounting rate and annual cash

inflow is provided. Under this, the discounting rate is decided by the management

which can be adjusted with the risk prevailing within the industry along with the other

important factors which are essential for getting the desired output.

NPV also considers the inflation rate in order to determine the right future

profitability and cash inflow (Michalkova and Spuchlakova, 2017). Thus, it considers

the time factor for determining the present value of future cash flow.

Through this, multiple projects can be compared with the same expected life under the

situation of mutually exclusive projects. This helps in selecting the most appropriate

and economically feasible project.

Disadvantages:

There are chances that it becomes difficult to calculate the opportunity which is

mainly considered in the initial outlay and thus, underestimating the initial cash

outflow would might distort the end result. Along with that, the sunk cost is also not

included which mainly includes the research and development cost incurred before

initiating the project.

The rate at which the cash flows are to be discounted is very difficult to determine.

Many a times firms make use of the WACC as the discount rate but it should be the

projects ROR and therefore, the wrong discounting rate might result into making

wrong estimation causing incorrect NPV value (Baker, Jabbouri and Dyaz, 2017). The

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.