Semester 1 Financial Management and Decision Making Assignment

VerifiedAdded on 2022/11/29

|15

|2884

|388

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial management and decision-making assignment. The assignment covers several key areas, including capital budgeting techniques like payback period and net present value (NPV), with detailed calculations and recommendations. It analyzes financial ratios, such as gross profit margin, operating profit margin, and liquidity ratios, to assess a company's performance over two years. The solution also involves variance analysis, calculating sales, material, labor, and overhead variances, along with an operating statement. Additionally, it includes break-even point analysis for two products, determining contribution margins and break-even points in units. The assignment emphasizes the application of financial concepts to real-world scenarios, providing a thorough understanding of financial management principles.

SEMESTER 1, EXAMINATION 2021/22

FINANCIAL MANAGEMENT AND DECISION

MAKING

MODULE NO: BMP5006

Date: 05 June 2021 Exam Start Time: 10:00 am

(Submit by 10:00 pm on 05 June

2021)

ANSWER BOOKLET

All the pages of the answer booklet should be submitted including blank ones.

Please type your answers in the spaces provided.

Insert additional pages where required.

Student Name

ID Number

Question 1

(a)

Calculation of Payback Period for each product:

FINANCIAL MANAGEMENT AND DECISION

MAKING

MODULE NO: BMP5006

Date: 05 June 2021 Exam Start Time: 10:00 am

(Submit by 10:00 pm on 05 June

2021)

ANSWER BOOKLET

All the pages of the answer booklet should be submitted including blank ones.

Please type your answers in the spaces provided.

Insert additional pages where required.

Student Name

ID Number

Question 1

(a)

Calculation of Payback Period for each product:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

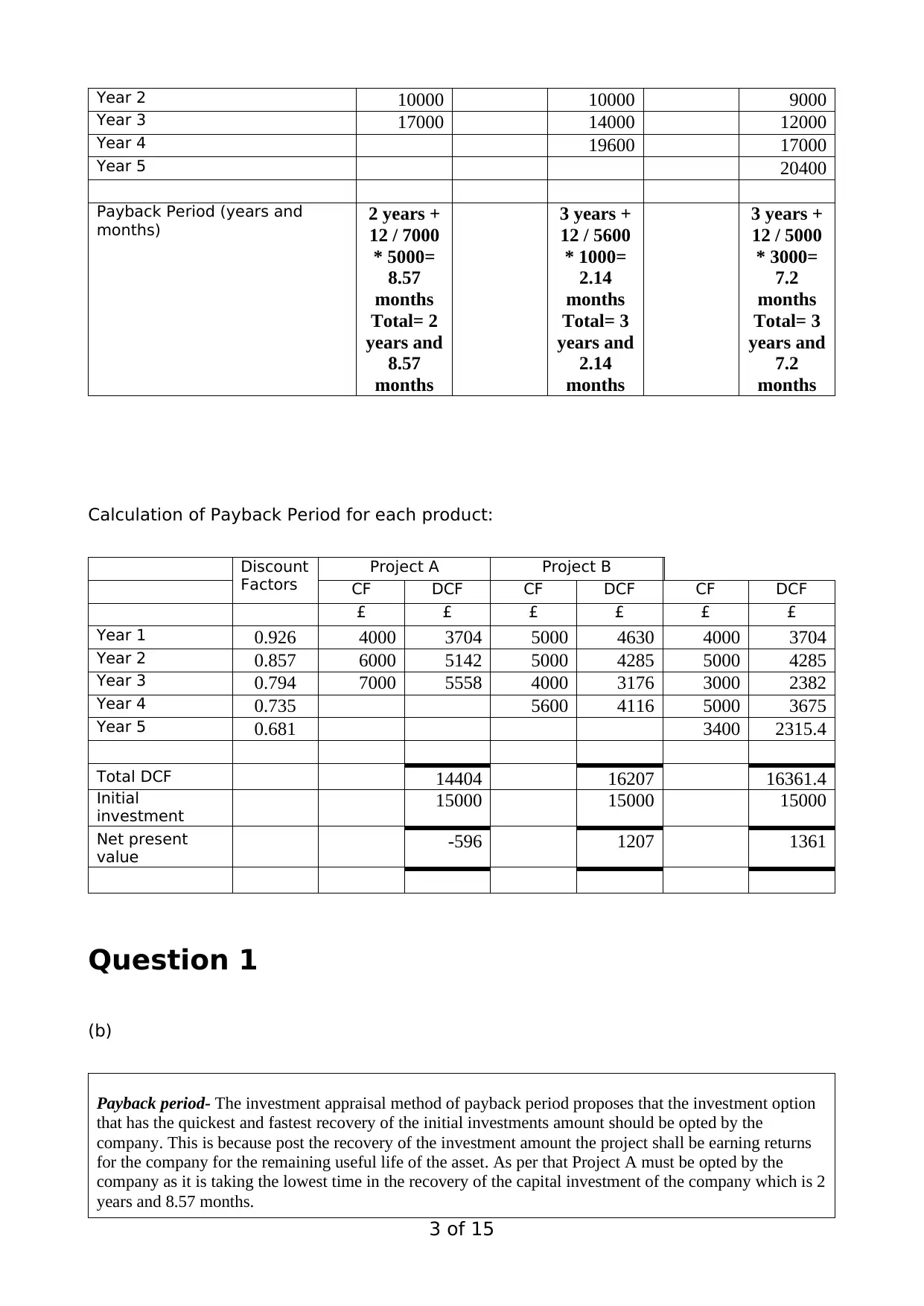

Project A Project B Project C

£ £ £

Year 1 4000 5000 4000

2 of 15

£ £ £

Year 1 4000 5000 4000

2 of 15

Year 2 10000 10000 9000

Year 3 17000 14000 12000

Year 4 19600 17000

Year 5 20400

Payback Period (years and

months) 2 years +

12 / 7000

* 5000=

8.57

months

Total= 2

years and

8.57

months

3 years +

12 / 5600

* 1000=

2.14

months

Total= 3

years and

2.14

months

3 years +

12 / 5000

* 3000=

7.2

months

Total= 3

years and

7.2

months

Calculation of Payback Period for each product:

Discount

Factors

Project A Project B

CF DCF CF DCF CF DCF

£ £ £ £ £ £

Year 1 0.926 4000 3704 5000 4630 4000 3704

Year 2 0.857 6000 5142 5000 4285 5000 4285

Year 3 0.794 7000 5558 4000 3176 3000 2382

Year 4 0.735 5600 4116 5000 3675

Year 5 0.681 3400 2315.4

Total DCF 14404 16207 16361.4

Initial

investment 15000 15000 15000

Net present

value -596 1207 1361

Question 1

(b)

Payback period- The investment appraisal method of payback period proposes that the investment option

that has the quickest and fastest recovery of the initial investments amount should be opted by the

company. This is because post the recovery of the investment amount the project shall be earning returns

for the company for the remaining useful life of the asset. As per that Project A must be opted by the

company as it is taking the lowest time in the recovery of the capital investment of the company which is 2

years and 8.57 months.

3 of 15

Year 3 17000 14000 12000

Year 4 19600 17000

Year 5 20400

Payback Period (years and

months) 2 years +

12 / 7000

* 5000=

8.57

months

Total= 2

years and

8.57

months

3 years +

12 / 5600

* 1000=

2.14

months

Total= 3

years and

2.14

months

3 years +

12 / 5000

* 3000=

7.2

months

Total= 3

years and

7.2

months

Calculation of Payback Period for each product:

Discount

Factors

Project A Project B

CF DCF CF DCF CF DCF

£ £ £ £ £ £

Year 1 0.926 4000 3704 5000 4630 4000 3704

Year 2 0.857 6000 5142 5000 4285 5000 4285

Year 3 0.794 7000 5558 4000 3176 3000 2382

Year 4 0.735 5600 4116 5000 3675

Year 5 0.681 3400 2315.4

Total DCF 14404 16207 16361.4

Initial

investment 15000 15000 15000

Net present

value -596 1207 1361

Question 1

(b)

Payback period- The investment appraisal method of payback period proposes that the investment option

that has the quickest and fastest recovery of the initial investments amount should be opted by the

company. This is because post the recovery of the investment amount the project shall be earning returns

for the company for the remaining useful life of the asset. As per that Project A must be opted by the

company as it is taking the lowest time in the recovery of the capital investment of the company which is 2

years and 8.57 months.

3 of 15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Net present value- This is the other most commonly used investment appraisal method in the company

which shall be discounting the future cash flows of the company to the present value and find the

difference between the present value of cash inflows and present value of cash outflows. This shall make

the choice based on the maximization of the returns by the various investment proposals, the option with

the highest net present value is to be selected by the company. In the current scenario the company shall

be choosing Project C as it is having the highest NPV which is 1361 as compared to the other projects.

This means that it shall be providing the maximum returns to the company.

(c)

I would recommend the company must go for making the capital investments in the Project C which is generating the

maximum returns for the company over the life of the asset. If the amount of investments is similar and also the life

of the asset is constant then in that case the investment proposal with the highest profitability must be opted by the

company. Also, another significant factor is that the company must be choosing an investment alternative which has

the constant and regular returns over the life of the asset so that the working capital cycle of the company keeps

moving smoothly and the operational efficiency is maintained in the business. The payback period as an capital

budgeting technique has criticisms like it does not consider the time value of money and also it does not see the post

payback profitability of any company and this is the reason that net present value as the appraisal technique is

considered superior. So I would suggest that suggestion of the net present value must be followed and the Project C

must be opted by the company.

(d)

Uses

Payback period- The payback period can be used to determine the time period that shall be taken to recover the

initial cost of investment of the company. It can be utilized in the determination of the proposal that shall be getting

back the investments at the quickest time possible. It is the simplest method to apply and can be used in the

combination of other techniques as well.

Net present value- The net present value is used to determine the profitability or the generation of the returns by the

various investment proposals and based on that the decision regarding the selection can be done in the company. It

can be utilized to know the present value of the stream of cash flows that are to be generated in the future for the

business.

Merits

Payback period- The major advantages of this method are that it is very simple and easy to apply on any investment

proposal to derive on the required result. The other significant benefit is that it is highly focused on the liquidity that

shall be generated over the life of the asset. It meets the requirement of the regular working capital needs of the

business. Apart from that the risk assessment can also be done regarding the receiving of the money.

Net present value- The most significant advantage of the method is that it shall be considering the time value of

money for the investments and based on that it shall be calculating the net returns on the capital investments. It

considers the wealth creation potential of the various investments which is the most essential factor that needs to be

counted upon by the financial analysts.

Limitation

Payback period- The limitations pertaining to the payback period of the company are that it does not consider the

time value of money and that is the reason the discounting factor part is skipped. Apart from that it can also be

analysed that the payback method does not see the post payback profitability of the company.

Net present value- The net present value method also has some limitations that the cost of capital that is considered

4 of 15

which shall be discounting the future cash flows of the company to the present value and find the

difference between the present value of cash inflows and present value of cash outflows. This shall make

the choice based on the maximization of the returns by the various investment proposals, the option with

the highest net present value is to be selected by the company. In the current scenario the company shall

be choosing Project C as it is having the highest NPV which is 1361 as compared to the other projects.

This means that it shall be providing the maximum returns to the company.

(c)

I would recommend the company must go for making the capital investments in the Project C which is generating the

maximum returns for the company over the life of the asset. If the amount of investments is similar and also the life

of the asset is constant then in that case the investment proposal with the highest profitability must be opted by the

company. Also, another significant factor is that the company must be choosing an investment alternative which has

the constant and regular returns over the life of the asset so that the working capital cycle of the company keeps

moving smoothly and the operational efficiency is maintained in the business. The payback period as an capital

budgeting technique has criticisms like it does not consider the time value of money and also it does not see the post

payback profitability of any company and this is the reason that net present value as the appraisal technique is

considered superior. So I would suggest that suggestion of the net present value must be followed and the Project C

must be opted by the company.

(d)

Uses

Payback period- The payback period can be used to determine the time period that shall be taken to recover the

initial cost of investment of the company. It can be utilized in the determination of the proposal that shall be getting

back the investments at the quickest time possible. It is the simplest method to apply and can be used in the

combination of other techniques as well.

Net present value- The net present value is used to determine the profitability or the generation of the returns by the

various investment proposals and based on that the decision regarding the selection can be done in the company. It

can be utilized to know the present value of the stream of cash flows that are to be generated in the future for the

business.

Merits

Payback period- The major advantages of this method are that it is very simple and easy to apply on any investment

proposal to derive on the required result. The other significant benefit is that it is highly focused on the liquidity that

shall be generated over the life of the asset. It meets the requirement of the regular working capital needs of the

business. Apart from that the risk assessment can also be done regarding the receiving of the money.

Net present value- The most significant advantage of the method is that it shall be considering the time value of

money for the investments and based on that it shall be calculating the net returns on the capital investments. It

considers the wealth creation potential of the various investments which is the most essential factor that needs to be

counted upon by the financial analysts.

Limitation

Payback period- The limitations pertaining to the payback period of the company are that it does not consider the

time value of money and that is the reason the discounting factor part is skipped. Apart from that it can also be

analysed that the payback method does not see the post payback profitability of the company.

Net present value- The net present value method also has some limitations that the cost of capital that is considered

4 of 15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

is used on the estimated basis by the company. Apart from that it can be assessed that this method is not applicable

on the projects having different investment amounts as they do not stand comparable.

Question 2

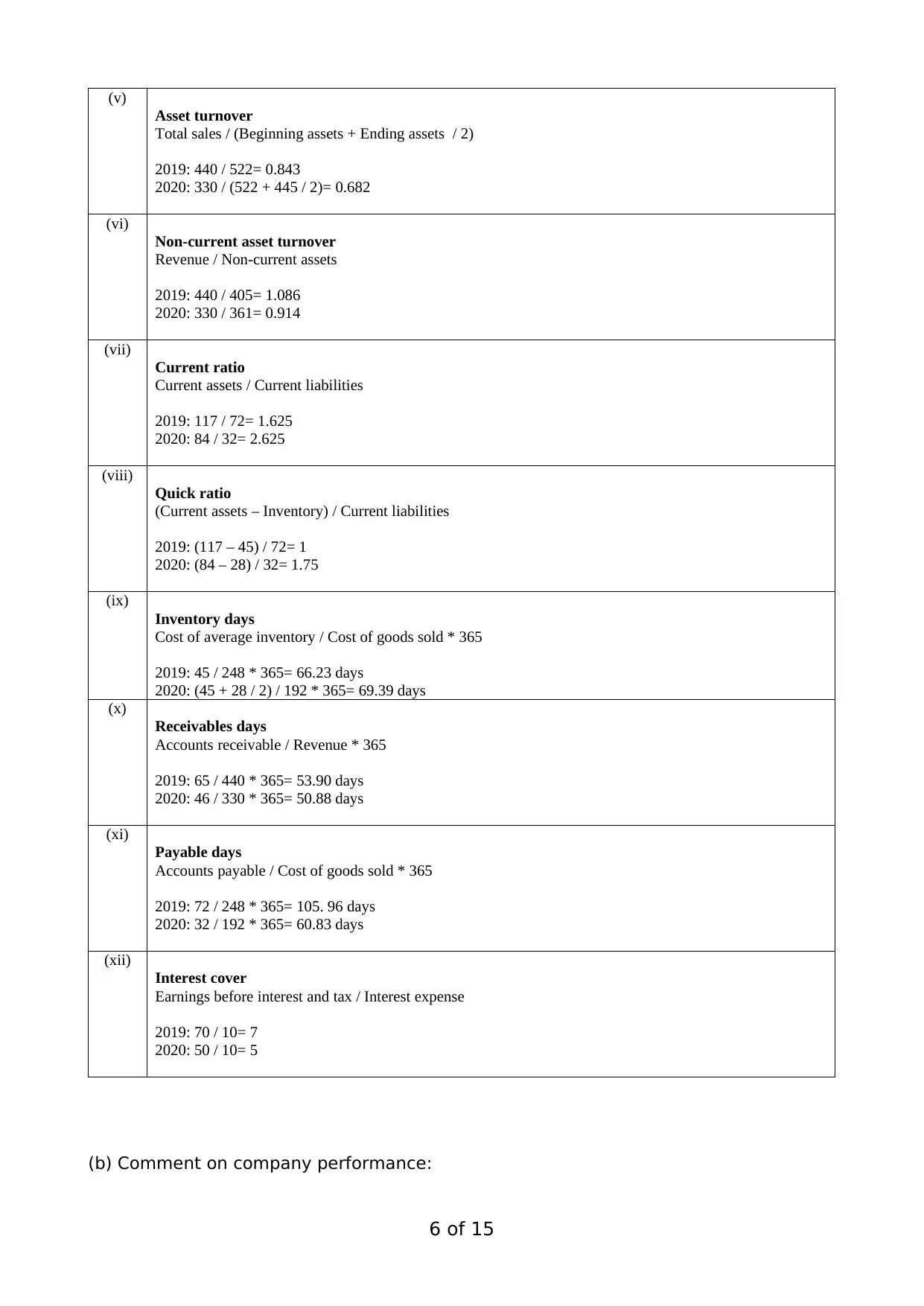

(a) Calculation of ratios:

(i)

Gross profit margin

Gross profit / Revenue * 100

2019: 192 / 440 * 100= 43.63%

2020: 138 / 330 * 100= 41.82%

(ii)

Operating profit margin

Operating profit / Revenue * 100

2019: 70 / 440 * 100= 15.91%

2020: 50 / 330 * 100= 15.15%

(iii)

Expenses to sales

Expenses / Revenue * 100

2019: 122 / 440 * 100= 27.73%

2020: 88 / 330 * 100= 26.67%

(iv)

Return on capital employed

Earnings before interest and tax / Capital employed * 100

Capital employed= Total assets – Current liabilities

2019: 70 / (522 – 72) * 100= 15.55%

2020: 50 / (445 – 32) * 100= 12.11%

5 of 15

on the projects having different investment amounts as they do not stand comparable.

Question 2

(a) Calculation of ratios:

(i)

Gross profit margin

Gross profit / Revenue * 100

2019: 192 / 440 * 100= 43.63%

2020: 138 / 330 * 100= 41.82%

(ii)

Operating profit margin

Operating profit / Revenue * 100

2019: 70 / 440 * 100= 15.91%

2020: 50 / 330 * 100= 15.15%

(iii)

Expenses to sales

Expenses / Revenue * 100

2019: 122 / 440 * 100= 27.73%

2020: 88 / 330 * 100= 26.67%

(iv)

Return on capital employed

Earnings before interest and tax / Capital employed * 100

Capital employed= Total assets – Current liabilities

2019: 70 / (522 – 72) * 100= 15.55%

2020: 50 / (445 – 32) * 100= 12.11%

5 of 15

(v)

Asset turnover

Total sales / (Beginning assets + Ending assets / 2)

2019: 440 / 522= 0.843

2020: 330 / (522 + 445 / 2)= 0.682

(vi)

Non-current asset turnover

Revenue / Non-current assets

2019: 440 / 405= 1.086

2020: 330 / 361= 0.914

(vii)

Current ratio

Current assets / Current liabilities

2019: 117 / 72= 1.625

2020: 84 / 32= 2.625

(viii)

Quick ratio

(Current assets – Inventory) / Current liabilities

2019: (117 – 45) / 72= 1

2020: (84 – 28) / 32= 1.75

(ix)

Inventory days

Cost of average inventory / Cost of goods sold * 365

2019: 45 / 248 * 365= 66.23 days

2020: (45 + 28 / 2) / 192 * 365= 69.39 days

(x)

Receivables days

Accounts receivable / Revenue * 365

2019: 65 / 440 * 365= 53.90 days

2020: 46 / 330 * 365= 50.88 days

(xi)

Payable days

Accounts payable / Cost of goods sold * 365

2019: 72 / 248 * 365= 105. 96 days

2020: 32 / 192 * 365= 60.83 days

(xii)

Interest cover

Earnings before interest and tax / Interest expense

2019: 70 / 10= 7

2020: 50 / 10= 5

(b) Comment on company performance:

6 of 15

Asset turnover

Total sales / (Beginning assets + Ending assets / 2)

2019: 440 / 522= 0.843

2020: 330 / (522 + 445 / 2)= 0.682

(vi)

Non-current asset turnover

Revenue / Non-current assets

2019: 440 / 405= 1.086

2020: 330 / 361= 0.914

(vii)

Current ratio

Current assets / Current liabilities

2019: 117 / 72= 1.625

2020: 84 / 32= 2.625

(viii)

Quick ratio

(Current assets – Inventory) / Current liabilities

2019: (117 – 45) / 72= 1

2020: (84 – 28) / 32= 1.75

(ix)

Inventory days

Cost of average inventory / Cost of goods sold * 365

2019: 45 / 248 * 365= 66.23 days

2020: (45 + 28 / 2) / 192 * 365= 69.39 days

(x)

Receivables days

Accounts receivable / Revenue * 365

2019: 65 / 440 * 365= 53.90 days

2020: 46 / 330 * 365= 50.88 days

(xi)

Payable days

Accounts payable / Cost of goods sold * 365

2019: 72 / 248 * 365= 105. 96 days

2020: 32 / 192 * 365= 60.83 days

(xii)

Interest cover

Earnings before interest and tax / Interest expense

2019: 70 / 10= 7

2020: 50 / 10= 5

(b) Comment on company performance:

6 of 15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

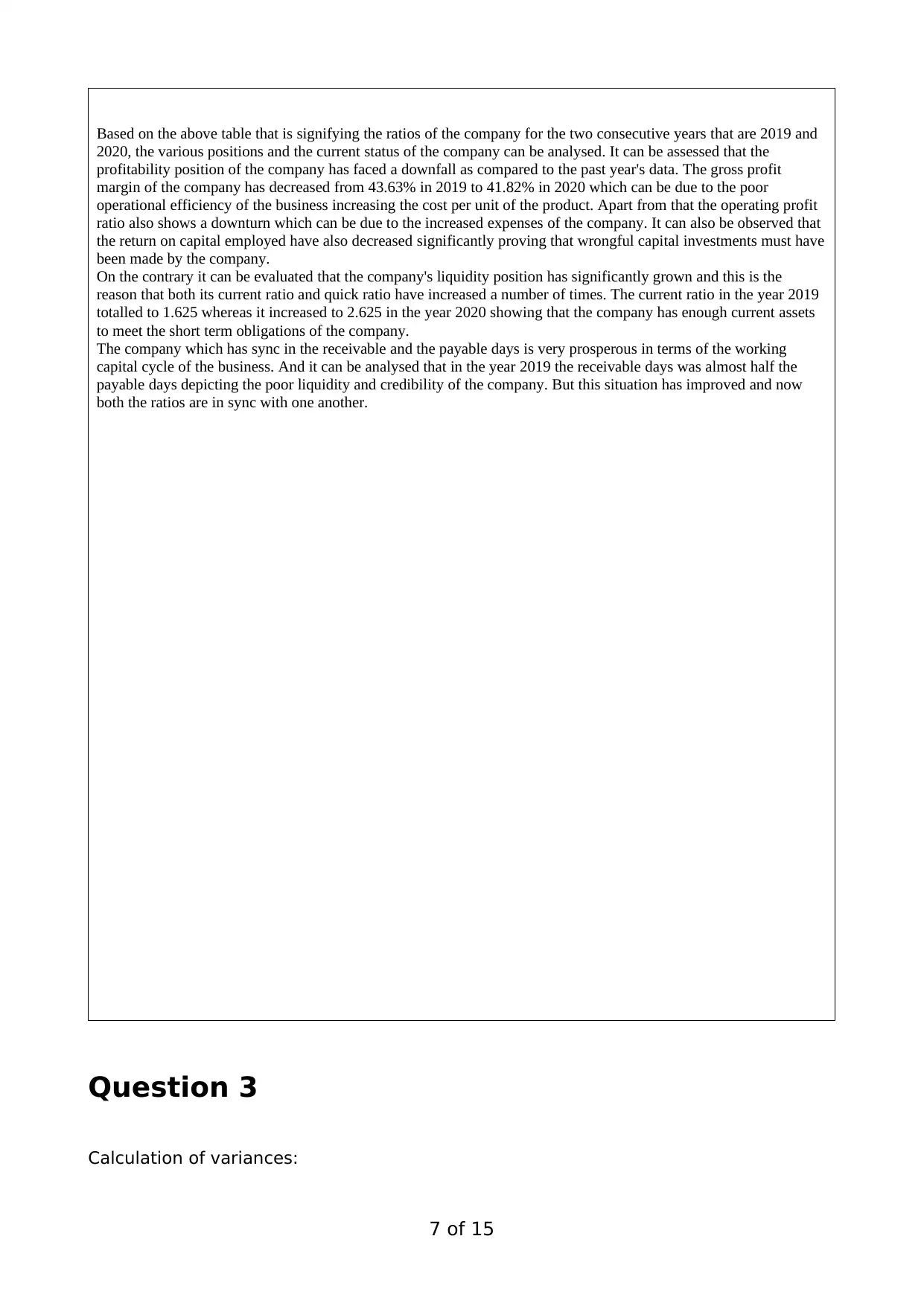

Based on the above table that is signifying the ratios of the company for the two consecutive years that are 2019 and

2020, the various positions and the current status of the company can be analysed. It can be assessed that the

profitability position of the company has faced a downfall as compared to the past year's data. The gross profit

margin of the company has decreased from 43.63% in 2019 to 41.82% in 2020 which can be due to the poor

operational efficiency of the business increasing the cost per unit of the product. Apart from that the operating profit

ratio also shows a downturn which can be due to the increased expenses of the company. It can also be observed that

the return on capital employed have also decreased significantly proving that wrongful capital investments must have

been made by the company.

On the contrary it can be evaluated that the company's liquidity position has significantly grown and this is the

reason that both its current ratio and quick ratio have increased a number of times. The current ratio in the year 2019

totalled to 1.625 whereas it increased to 2.625 in the year 2020 showing that the company has enough current assets

to meet the short term obligations of the company.

The company which has sync in the receivable and the payable days is very prosperous in terms of the working

capital cycle of the business. And it can be analysed that in the year 2019 the receivable days was almost half the

payable days depicting the poor liquidity and credibility of the company. But this situation has improved and now

both the ratios are in sync with one another.

Question 3

Calculation of variances:

7 of 15

2020, the various positions and the current status of the company can be analysed. It can be assessed that the

profitability position of the company has faced a downfall as compared to the past year's data. The gross profit

margin of the company has decreased from 43.63% in 2019 to 41.82% in 2020 which can be due to the poor

operational efficiency of the business increasing the cost per unit of the product. Apart from that the operating profit

ratio also shows a downturn which can be due to the increased expenses of the company. It can also be observed that

the return on capital employed have also decreased significantly proving that wrongful capital investments must have

been made by the company.

On the contrary it can be evaluated that the company's liquidity position has significantly grown and this is the

reason that both its current ratio and quick ratio have increased a number of times. The current ratio in the year 2019

totalled to 1.625 whereas it increased to 2.625 in the year 2020 showing that the company has enough current assets

to meet the short term obligations of the company.

The company which has sync in the receivable and the payable days is very prosperous in terms of the working

capital cycle of the business. And it can be analysed that in the year 2019 the receivable days was almost half the

payable days depicting the poor liquidity and credibility of the company. But this situation has improved and now

both the ratios are in sync with one another.

Question 3

Calculation of variances:

7 of 15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

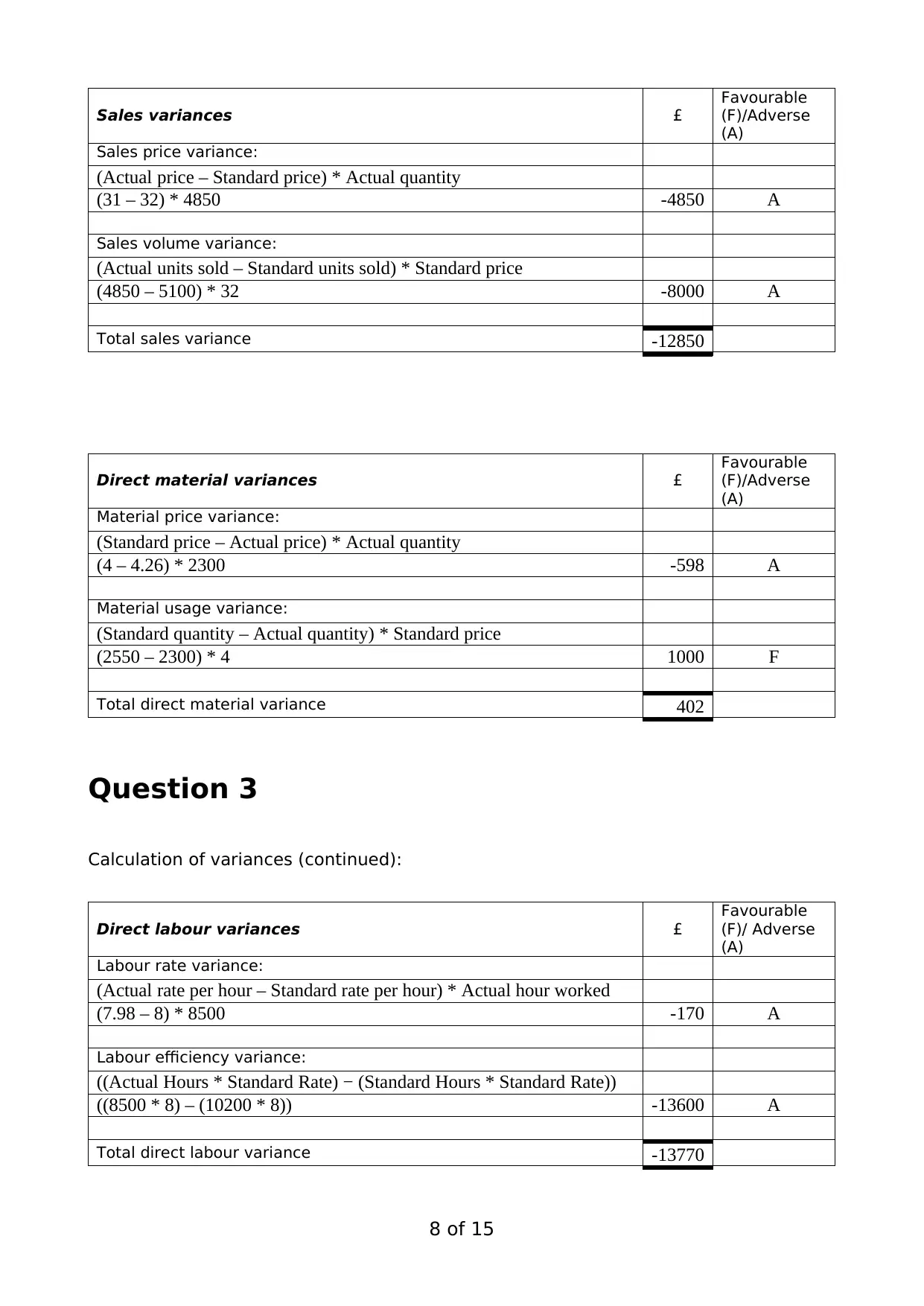

Sales variances £

Favourable

(F)/Adverse

(A)

Sales price variance:

(Actual price – Standard price) * Actual quantity

(31 – 32) * 4850 -4850 A

Sales volume variance:

(Actual units sold – Standard units sold) * Standard price

(4850 – 5100) * 32 -8000 A

Total sales variance -12850

Direct material variances £

Favourable

(F)/Adverse

(A)

Material price variance:

(Standard price – Actual price) * Actual quantity

(4 – 4.26) * 2300 -598 A

Material usage variance:

(Standard quantity – Actual quantity) * Standard price

(2550 – 2300) * 4 1000 F

Total direct material variance 402

Question 3

Calculation of variances (continued):

Direct labour variances £

Favourable

(F)/ Adverse

(A)

Labour rate variance:

(Actual rate per hour – Standard rate per hour) * Actual hour worked

(7.98 – 8) * 8500 -170 A

Labour efficiency variance:

((Actual Hours * Standard Rate) − (Standard Hours * Standard Rate))

((8500 * 8) – (10200 * 8)) -13600 A

Total direct labour variance -13770

8 of 15

Favourable

(F)/Adverse

(A)

Sales price variance:

(Actual price – Standard price) * Actual quantity

(31 – 32) * 4850 -4850 A

Sales volume variance:

(Actual units sold – Standard units sold) * Standard price

(4850 – 5100) * 32 -8000 A

Total sales variance -12850

Direct material variances £

Favourable

(F)/Adverse

(A)

Material price variance:

(Standard price – Actual price) * Actual quantity

(4 – 4.26) * 2300 -598 A

Material usage variance:

(Standard quantity – Actual quantity) * Standard price

(2550 – 2300) * 4 1000 F

Total direct material variance 402

Question 3

Calculation of variances (continued):

Direct labour variances £

Favourable

(F)/ Adverse

(A)

Labour rate variance:

(Actual rate per hour – Standard rate per hour) * Actual hour worked

(7.98 – 8) * 8500 -170 A

Labour efficiency variance:

((Actual Hours * Standard Rate) − (Standard Hours * Standard Rate))

((8500 * 8) – (10200 * 8)) -13600 A

Total direct labour variance -13770

8 of 15

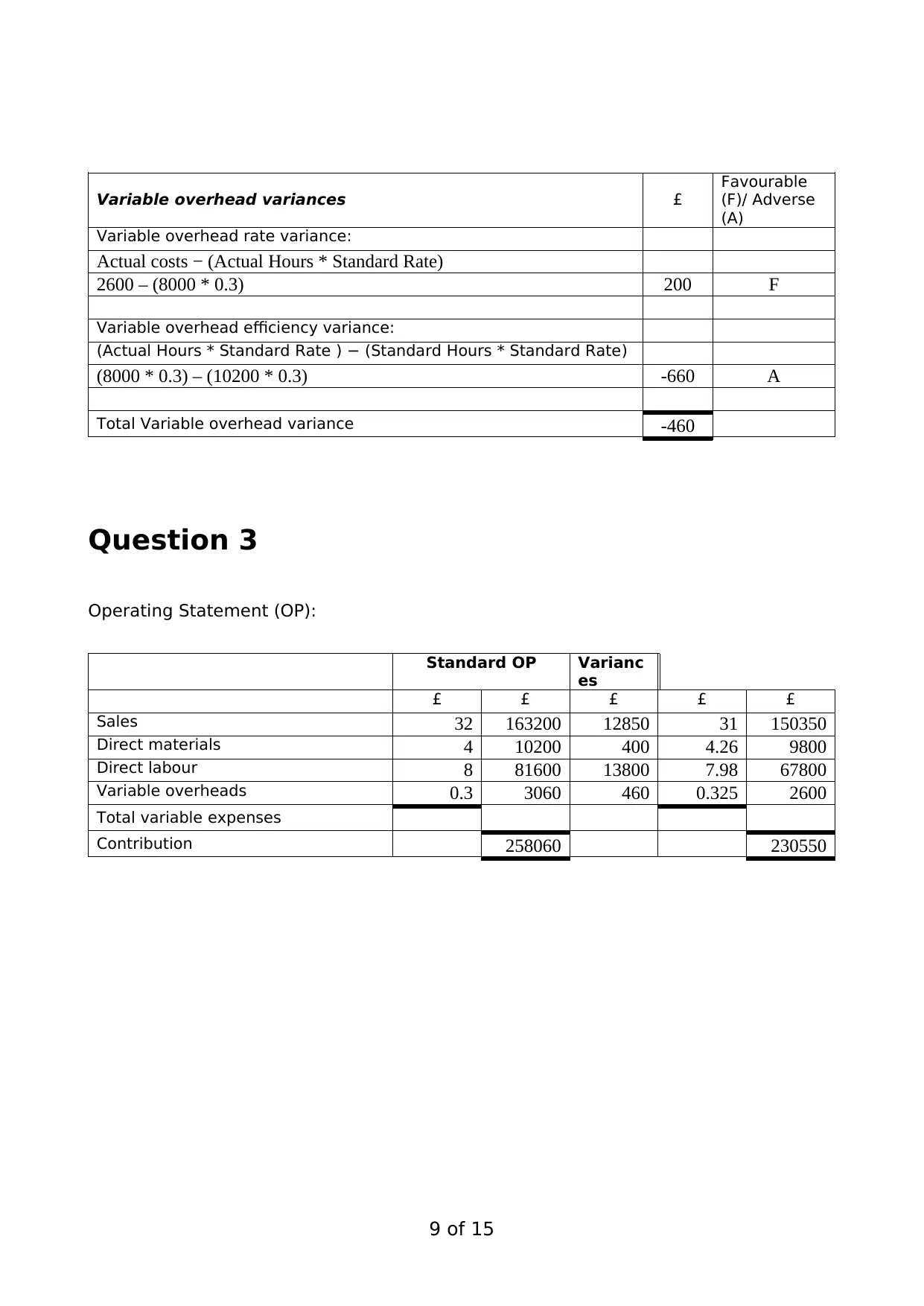

Variable overhead variances £

Favourable

(F)/ Adverse

(A)

Variable overhead rate variance:

Actual costs − (Actual Hours * Standard Rate)

2600 – (8000 * 0.3) 200 F

Variable overhead efficiency variance:

(Actual Hours * Standard Rate ) − (Standard Hours * Standard Rate)

(8000 * 0.3) – (10200 * 0.3) -660 A

Total Variable overhead variance -460

Question 3

Operating Statement (OP):

Standard OP Varianc

es

£ £ £ £ £

Sales 32 163200 12850 31 150350

Direct materials 4 10200 400 4.26 9800

Direct labour 8 81600 13800 7.98 67800

Variable overheads 0.3 3060 460 0.325 2600

Total variable expenses

Contribution 258060 230550

9 of 15

Favourable

(F)/ Adverse

(A)

Variable overhead rate variance:

Actual costs − (Actual Hours * Standard Rate)

2600 – (8000 * 0.3) 200 F

Variable overhead efficiency variance:

(Actual Hours * Standard Rate ) − (Standard Hours * Standard Rate)

(8000 * 0.3) – (10200 * 0.3) -660 A

Total Variable overhead variance -460

Question 3

Operating Statement (OP):

Standard OP Varianc

es

£ £ £ £ £

Sales 32 163200 12850 31 150350

Direct materials 4 10200 400 4.26 9800

Direct labour 8 81600 13800 7.98 67800

Variable overheads 0.3 3060 460 0.325 2600

Total variable expenses

Contribution 258060 230550

9 of 15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

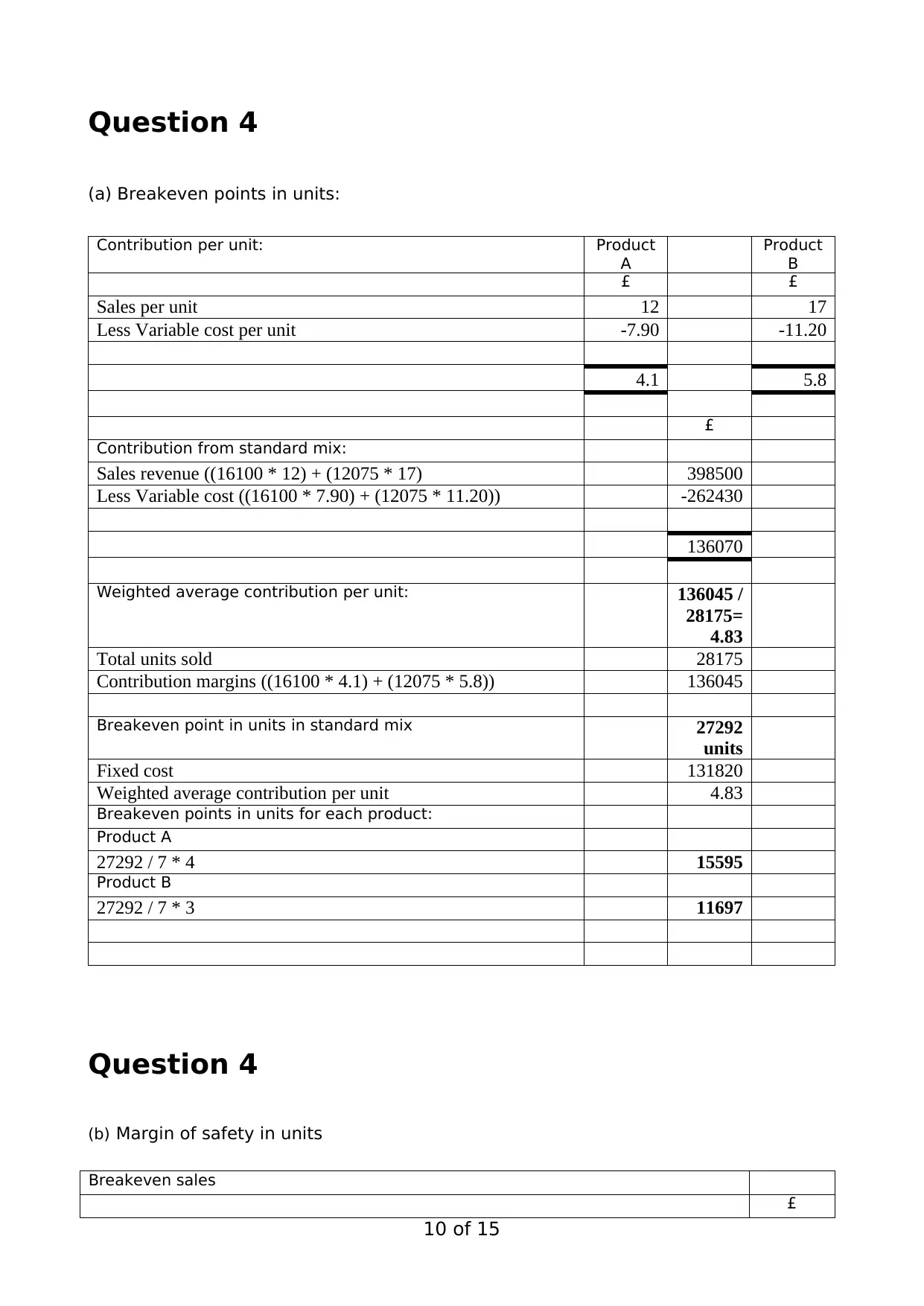

Question 4

(a) Breakeven points in units:

Contribution per unit: Product

A

Product

B

£ £

Sales per unit 12 17

Less Variable cost per unit -7.90 -11.20

4.1 5.8

£

Contribution from standard mix:

Sales revenue ((16100 * 12) + (12075 * 17) 398500

Less Variable cost ((16100 * 7.90) + (12075 * 11.20)) -262430

136070

Weighted average contribution per unit: 136045 /

28175=

4.83

Total units sold 28175

Contribution margins ((16100 * 4.1) + (12075 * 5.8)) 136045

Breakeven point in units in standard mix 27292

units

Fixed cost 131820

Weighted average contribution per unit 4.83

Breakeven points in units for each product:

Product A

27292 / 7 * 4 15595

Product B

27292 / 7 * 3 11697

Question 4

(b) Margin of safety in units

Breakeven sales

£

10 of 15

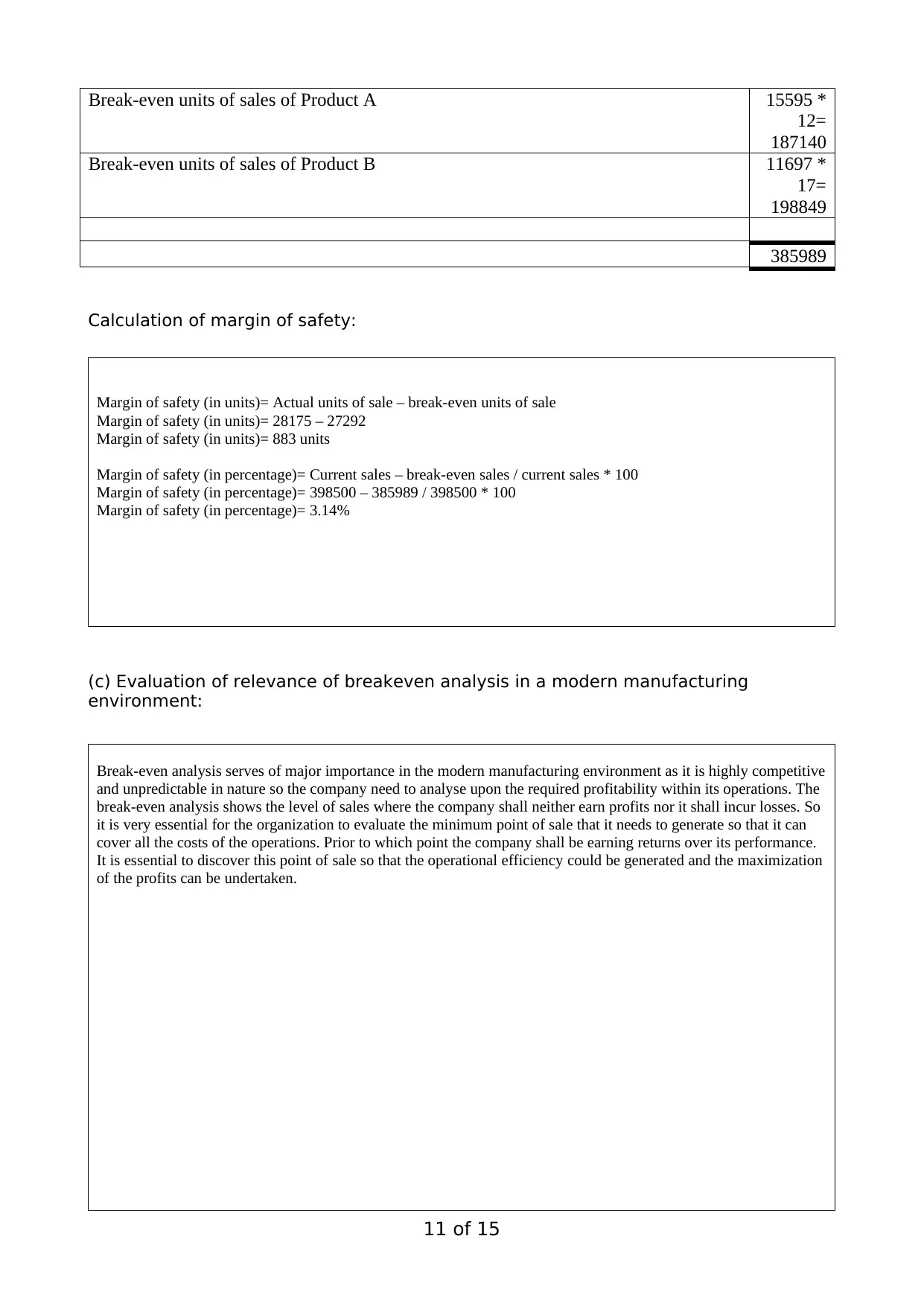

(a) Breakeven points in units:

Contribution per unit: Product

A

Product

B

£ £

Sales per unit 12 17

Less Variable cost per unit -7.90 -11.20

4.1 5.8

£

Contribution from standard mix:

Sales revenue ((16100 * 12) + (12075 * 17) 398500

Less Variable cost ((16100 * 7.90) + (12075 * 11.20)) -262430

136070

Weighted average contribution per unit: 136045 /

28175=

4.83

Total units sold 28175

Contribution margins ((16100 * 4.1) + (12075 * 5.8)) 136045

Breakeven point in units in standard mix 27292

units

Fixed cost 131820

Weighted average contribution per unit 4.83

Breakeven points in units for each product:

Product A

27292 / 7 * 4 15595

Product B

27292 / 7 * 3 11697

Question 4

(b) Margin of safety in units

Breakeven sales

£

10 of 15

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Break-even units of sales of Product A 15595 *

12=

187140

Break-even units of sales of Product B 11697 *

17=

198849

385989

Calculation of margin of safety:

Margin of safety (in units)= Actual units of sale – break-even units of sale

Margin of safety (in units)= 28175 – 27292

Margin of safety (in units)= 883 units

Margin of safety (in percentage)= Current sales – break-even sales / current sales * 100

Margin of safety (in percentage)= 398500 – 385989 / 398500 * 100

Margin of safety (in percentage)= 3.14%

(c) Evaluation of relevance of breakeven analysis in a modern manufacturing

environment:

Break-even analysis serves of major importance in the modern manufacturing environment as it is highly competitive

and unpredictable in nature so the company need to analyse upon the required profitability within its operations. The

break-even analysis shows the level of sales where the company shall neither earn profits nor it shall incur losses. So

it is very essential for the organization to evaluate the minimum point of sale that it needs to generate so that it can

cover all the costs of the operations. Prior to which point the company shall be earning returns over its performance.

It is essential to discover this point of sale so that the operational efficiency could be generated and the maximization

of the profits can be undertaken.

11 of 15

12=

187140

Break-even units of sales of Product B 11697 *

17=

198849

385989

Calculation of margin of safety:

Margin of safety (in units)= Actual units of sale – break-even units of sale

Margin of safety (in units)= 28175 – 27292

Margin of safety (in units)= 883 units

Margin of safety (in percentage)= Current sales – break-even sales / current sales * 100

Margin of safety (in percentage)= 398500 – 385989 / 398500 * 100

Margin of safety (in percentage)= 3.14%

(c) Evaluation of relevance of breakeven analysis in a modern manufacturing

environment:

Break-even analysis serves of major importance in the modern manufacturing environment as it is highly competitive

and unpredictable in nature so the company need to analyse upon the required profitability within its operations. The

break-even analysis shows the level of sales where the company shall neither earn profits nor it shall incur losses. So

it is very essential for the organization to evaluate the minimum point of sale that it needs to generate so that it can

cover all the costs of the operations. Prior to which point the company shall be earning returns over its performance.

It is essential to discover this point of sale so that the operational efficiency could be generated and the maximization

of the profits can be undertaken.

11 of 15

12 of 15

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.