APC308 Financial Management Report: Investment Appraisal & Valuation

VerifiedAdded on 2023/01/11

|13

|3729

|35

Report

AI Summary

This report delves into financial management, addressing two key questions: mergers and acquisitions, and investment appraisal techniques. The first section analyzes valuation models such as price-earnings ratio, dividend valuation model, and discounted cash flow method, along with their associated problems, recommending the discounted valuation method for a company. The second section focuses on investment appraisal techniques, calculating and evaluating payback period, accounting rate of return (ARR), net present value (NPV), and internal rate of return (IRR) to aid in investment decisions. The report provides detailed calculations and critical evaluations of each method to assist managers in making strategic financial decisions, with the aim of maximizing market share and returns on investment.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

INTRODUCTION...........................................................................................................................1

MAIN BODY..................................................................................................................................1

QUESTION 2 - Mergers and Takeover...........................................................................................1

1. Price earnings ratio..................................................................................................................1

2. Dividend valuation model........................................................................................................2

3. Discounted cash flow method..................................................................................................3

4. Discuss the problems which associated with valuation model................................................3

Recommendation:........................................................................................................................4

QUESTION 3 – Investment appraisal techniques...........................................................................4

1. Calculate the following investment appraisal technique.........................................................4

2. Critically evaluate the benefits or limitations of different investment appraisal techniques:..9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

MAIN BODY..................................................................................................................................1

QUESTION 2 - Mergers and Takeover...........................................................................................1

1. Price earnings ratio..................................................................................................................1

2. Dividend valuation model........................................................................................................2

3. Discounted cash flow method..................................................................................................3

4. Discuss the problems which associated with valuation model................................................3

Recommendation:........................................................................................................................4

QUESTION 3 – Investment appraisal techniques...........................................................................4

1. Calculate the following investment appraisal technique.........................................................4

2. Critically evaluate the benefits or limitations of different investment appraisal techniques:..9

CONCLUSION..............................................................................................................................10

REFERENCES..............................................................................................................................11

INTRODUCTION

Financial management concentrates on ratio analysis, equity and debt. It is valuable for fund

management, income allocation, project finance, trying to hedge and monitoring foreign

exchange and commodity cycle volatility (Anthony, 2019). It is necessary for an company to

handle its funds effectively and it is vital that the funds it acquires are spent in such a way that

the returns on the project are greater than the funding costs. This report based on two different

questions which are about mergers and acquisition and investment appraisal techniques which

are used by the managers to identified best favourable project to invest. These concepts help the

managers to make strategic decisions to invest and what actions they should implement to

maximise their market share as well.

MAIN BODY

QUESTION 2 - Mergers and Takeover

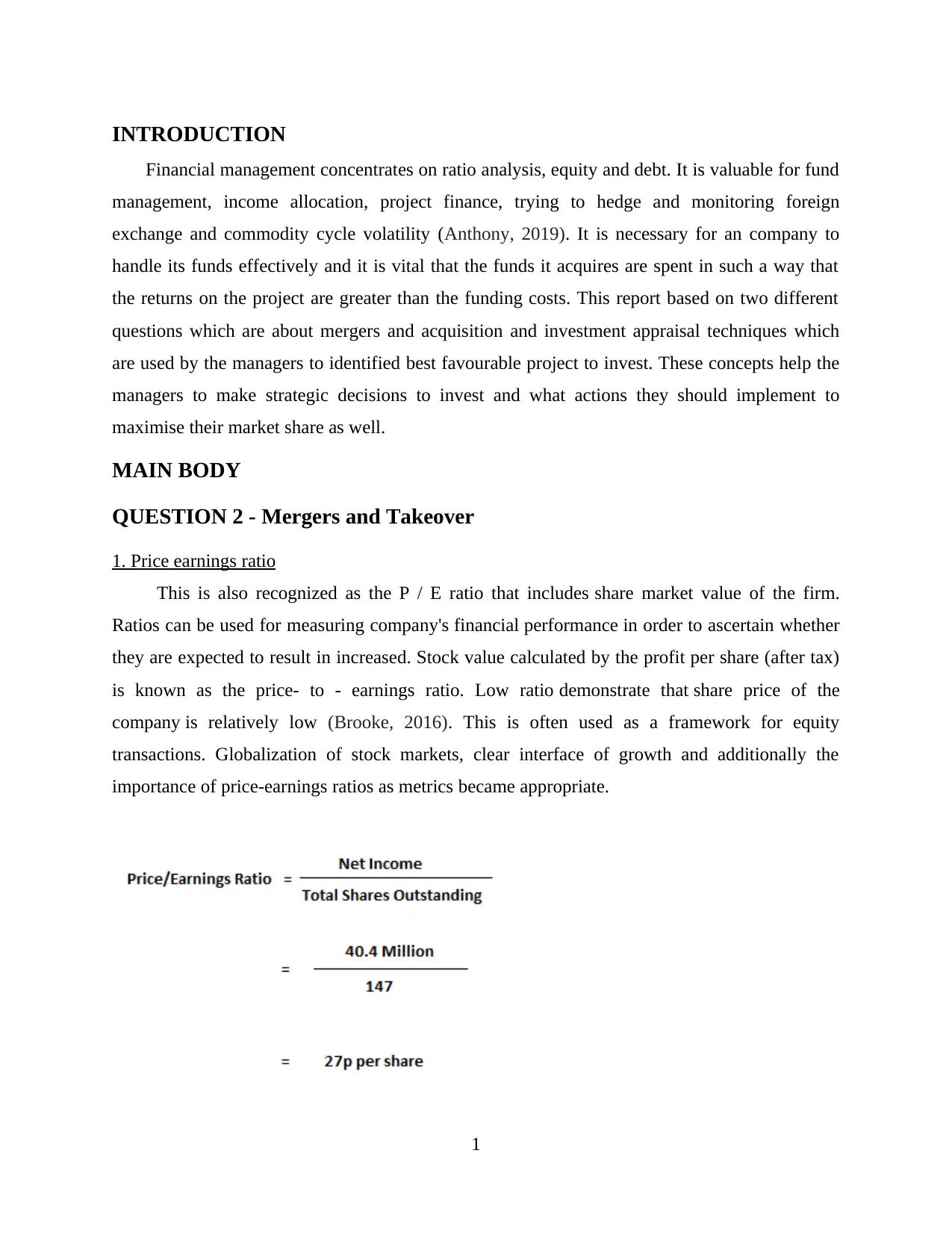

1. Price earnings ratio

This is also recognized as the P / E ratio that includes share market value of the firm.

Ratios can be used for measuring company's financial performance in order to ascertain whether

they are expected to result in increased. Stock value calculated by the profit per share (after tax)

is known as the price- to - earnings ratio. Low ratio demonstrate that share price of the

company is relatively low (Brooke, 2016). This is often used as a framework for equity

transactions. Globalization of stock markets, clear interface of growth and additionally the

importance of price-earnings ratios as metrics became appropriate.

1

Financial management concentrates on ratio analysis, equity and debt. It is valuable for fund

management, income allocation, project finance, trying to hedge and monitoring foreign

exchange and commodity cycle volatility (Anthony, 2019). It is necessary for an company to

handle its funds effectively and it is vital that the funds it acquires are spent in such a way that

the returns on the project are greater than the funding costs. This report based on two different

questions which are about mergers and acquisition and investment appraisal techniques which

are used by the managers to identified best favourable project to invest. These concepts help the

managers to make strategic decisions to invest and what actions they should implement to

maximise their market share as well.

MAIN BODY

QUESTION 2 - Mergers and Takeover

1. Price earnings ratio

This is also recognized as the P / E ratio that includes share market value of the firm.

Ratios can be used for measuring company's financial performance in order to ascertain whether

they are expected to result in increased. Stock value calculated by the profit per share (after tax)

is known as the price- to - earnings ratio. Low ratio demonstrate that share price of the

company is relatively low (Brooke, 2016). This is often used as a framework for equity

transactions. Globalization of stock markets, clear interface of growth and additionally the

importance of price-earnings ratios as metrics became appropriate.

1

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

The above calculation shows that owners of Trojan plc have earned a stake of 27 %. In

order to achieve the several benefits by using this P/E ratio, gross profit split into outstanding

shares or deal with organizations to issue the face of deduction of costs and expenses. average

payout of the company throughout the year is £ 40.4 million and the actual outstanding deals are

147 million.

2. Dividend valuation model

Main shareholders have the right to convert equity and dividend payments to equilibrium

shareholders. Actual investors of the company are borrowers to the association. When the

company earns taxable earnings, extra profits are collected and the dividend is not earned

because the revenue is not obtained, i.e. the dividend yield on the above-mentioned securities

remains constant whilst the payout ratio on equity shares is starting to shift.

This technique is used to identify the required return throughout the existing year as a

discount factor which is equal to the benefit cost at the bid’s expense (Dwiastanti, 2017). This

technique is referred to it as the model or DDM which restricts revenue. It's being used to

calculate the cost of Aztec’s shares depending on time spans. With the current contrast, all profit

is left to its existing qualities in order to know the potential. Under it, compensation assessment

using the discounted valuation model and its calculation is below:

Dividend Discount Model Fair Value: £4.774

Expected Dividends Next Year = {Dividends per Share × (1 + Expected Growth Rate)}

= {0.13 × (1 + 0.14)}

= 0.148

Expected Growth Rate = {(1 – Dividend Payout Ratio) × Return on Equity}

= {(1 – 0.48) × 0.27}

= 0.14

Cost of Equity = Risk Free Rate + Beta × Market Risk Premium

= 0.05 + 1.1 × 0.11

= 0.171

Fair Value = {Expected Dividends Next Year / (Cost of Equity – Expected Growth Rate)}

= {0.148 / (0.171 – 0.14)}

= 4.774

2

order to achieve the several benefits by using this P/E ratio, gross profit split into outstanding

shares or deal with organizations to issue the face of deduction of costs and expenses. average

payout of the company throughout the year is £ 40.4 million and the actual outstanding deals are

147 million.

2. Dividend valuation model

Main shareholders have the right to convert equity and dividend payments to equilibrium

shareholders. Actual investors of the company are borrowers to the association. When the

company earns taxable earnings, extra profits are collected and the dividend is not earned

because the revenue is not obtained, i.e. the dividend yield on the above-mentioned securities

remains constant whilst the payout ratio on equity shares is starting to shift.

This technique is used to identify the required return throughout the existing year as a

discount factor which is equal to the benefit cost at the bid’s expense (Dwiastanti, 2017). This

technique is referred to it as the model or DDM which restricts revenue. It's being used to

calculate the cost of Aztec’s shares depending on time spans. With the current contrast, all profit

is left to its existing qualities in order to know the potential. Under it, compensation assessment

using the discounted valuation model and its calculation is below:

Dividend Discount Model Fair Value: £4.774

Expected Dividends Next Year = {Dividends per Share × (1 + Expected Growth Rate)}

= {0.13 × (1 + 0.14)}

= 0.148

Expected Growth Rate = {(1 – Dividend Payout Ratio) × Return on Equity}

= {(1 – 0.48) × 0.27}

= 0.14

Cost of Equity = Risk Free Rate + Beta × Market Risk Premium

= 0.05 + 1.1 × 0.11

= 0.171

Fair Value = {Expected Dividends Next Year / (Cost of Equity – Expected Growth Rate)}

= {0.148 / (0.171 – 0.14)}

= 4.774

2

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Above calculation helps in estimate the specified profit is 4.774 p per share. Share price in

the market, free buoy rate and beta rating are known to be significant work to assess the

situation. Market rate is often related to as premium or risk rate as speculation brings this extra

incentive to the risk. Free buoy rates really aren't dangerous however, as there will be no chance

of losing the interest of the company.

3. Discounted cash flow method

It could be described as a measurement of the value of potential cash flows, seeking to

convey a discounted rate which reflects the expected uncertainties in market prices. It must be

taken not to equate discounted cash flow for income every month as cash flow is tracked by links

posted from predetermined maps.

Year Net Income £’ million Discounted cash flow @ 7 %

Year 1 £ 40.40 £ 37.76

Year 2 £ 41.21 £ 35.99

Year 3 £ 42.03 £ 34.31

Year 4 £ 42.87 £ 32.71

Year 5 £ 43.73 £ 31.18

£ 171.95

With the help of above calculation, figures show that limited income with distributable

payout is 2% per annum. It was found that the entity would receive the all-out money of £ 171.95

million (present value) towards the end of 5 years.

4. Discuss the problems which associated with valuation model

There are several problems that linked with the valuation methods, so before implementing

these methods managers should identified the issues which can affect the managerial decisions.

Further discussions are as follow:

At the time of buying securities, company can't be used to evaluate companies stock of

they does not pay dividends, irrespective of capital gains (Ehrhardt and Brigham, 2016).

Dividend Discount Model (DDM) is based on the mistaken presumption that the sole

interest of a asset is the return on capital by dividend distribution.

3

the market, free buoy rate and beta rating are known to be significant work to assess the

situation. Market rate is often related to as premium or risk rate as speculation brings this extra

incentive to the risk. Free buoy rates really aren't dangerous however, as there will be no chance

of losing the interest of the company.

3. Discounted cash flow method

It could be described as a measurement of the value of potential cash flows, seeking to

convey a discounted rate which reflects the expected uncertainties in market prices. It must be

taken not to equate discounted cash flow for income every month as cash flow is tracked by links

posted from predetermined maps.

Year Net Income £’ million Discounted cash flow @ 7 %

Year 1 £ 40.40 £ 37.76

Year 2 £ 41.21 £ 35.99

Year 3 £ 42.03 £ 34.31

Year 4 £ 42.87 £ 32.71

Year 5 £ 43.73 £ 31.18

£ 171.95

With the help of above calculation, figures show that limited income with distributable

payout is 2% per annum. It was found that the entity would receive the all-out money of £ 171.95

million (present value) towards the end of 5 years.

4. Discuss the problems which associated with valuation model

There are several problems that linked with the valuation methods, so before implementing

these methods managers should identified the issues which can affect the managerial decisions.

Further discussions are as follow:

At the time of buying securities, company can't be used to evaluate companies stock of

they does not pay dividends, irrespective of capital gains (Ehrhardt and Brigham, 2016).

Dividend Discount Model (DDM) is based on the mistaken presumption that the sole

interest of a asset is the return on capital by dividend distribution.

3

Another disadvantage is the reality that certain estimates on issues like the growth rate

and the expected cost of return are included in the price at the time of calculations.

Dividend yields significantly shift with time.

If all the observations or calculations taken in the estimation which are somewhat in

error. It may be outcome in an expert, who calculates the valuation for the product, being

undervalued or downsized dramatically. There are several variations in Closed DDM to

solve this disadvantage. However, most of these require making new assumptions and

measurements, which, over time, are often prone to expanded errors.

It ignores the impact of stock buybacks in respect to the return of share price to

shareholders that is very big difference. This model also ignoring stock buybacks

which represents challenge in DDM, being cautious, over share price forecasts.

Recommendation:

After observing the entire three valuation model and its calculation, it is recommended that

Aztec should follow discounted valuation method that is beneficial for Trojan Plc. In context of

the organization, every company work on their earning aspects to maximise it. Among the two

valuations model based on profit and the one is overlook the return or revenue which they can

generate by using it. In this case, discounted valuation model suggested evaluating the Trojan Plc

which provides them more benefits.

QUESTION 3 – Investment appraisal techniques

1. Calculate the following investment appraisal technique

Payback period:

It is one of the most usable methods of capital budgeting that help the organizations

ti evaluate recovery period of their investment (Greve and Man Zhang, 2017). Company gains

from short payback period which allowed regaining original investments as well as increasing

their returns. The firm's financial strategy executives will decide together on potential

acquisitions. Calculating the companies' total project risk is really necessary because

administrators choose the project that holds less risk than other projects. In addition, lower the

recovery time is acceptable or higher one is rejected when managers have multiple options, so

they can make investment decisions accordingly. Its calculation is mentioned below:

Formula:

4

and the expected cost of return are included in the price at the time of calculations.

Dividend yields significantly shift with time.

If all the observations or calculations taken in the estimation which are somewhat in

error. It may be outcome in an expert, who calculates the valuation for the product, being

undervalued or downsized dramatically. There are several variations in Closed DDM to

solve this disadvantage. However, most of these require making new assumptions and

measurements, which, over time, are often prone to expanded errors.

It ignores the impact of stock buybacks in respect to the return of share price to

shareholders that is very big difference. This model also ignoring stock buybacks

which represents challenge in DDM, being cautious, over share price forecasts.

Recommendation:

After observing the entire three valuation model and its calculation, it is recommended that

Aztec should follow discounted valuation method that is beneficial for Trojan Plc. In context of

the organization, every company work on their earning aspects to maximise it. Among the two

valuations model based on profit and the one is overlook the return or revenue which they can

generate by using it. In this case, discounted valuation model suggested evaluating the Trojan Plc

which provides them more benefits.

QUESTION 3 – Investment appraisal techniques

1. Calculate the following investment appraisal technique

Payback period:

It is one of the most usable methods of capital budgeting that help the organizations

ti evaluate recovery period of their investment (Greve and Man Zhang, 2017). Company gains

from short payback period which allowed regaining original investments as well as increasing

their returns. The firm's financial strategy executives will decide together on potential

acquisitions. Calculating the companies' total project risk is really necessary because

administrators choose the project that holds less risk than other projects. In addition, lower the

recovery time is acceptable or higher one is rejected when managers have multiple options, so

they can make investment decisions accordingly. Its calculation is mentioned below:

Formula:

4

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

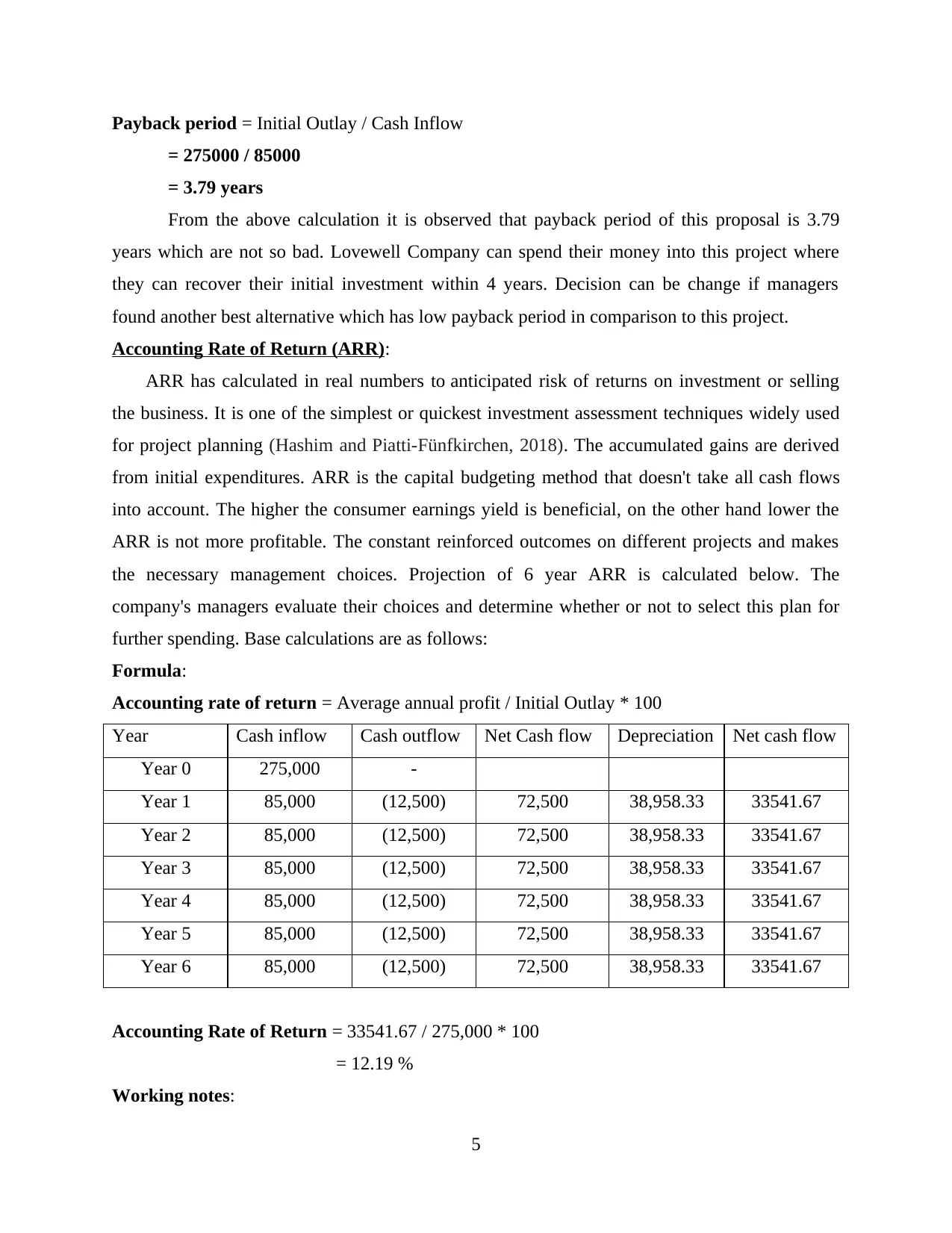

Payback period = Initial Outlay / Cash Inflow

= 275000 / 85000

= 3.79 years

From the above calculation it is observed that payback period of this proposal is 3.79

years which are not so bad. Lovewell Company can spend their money into this project where

they can recover their initial investment within 4 years. Decision can be change if managers

found another best alternative which has low payback period in comparison to this project.

Accounting Rate of Return (ARR):

ARR has calculated in real numbers to anticipated risk of returns on investment or selling

the business. It is one of the simplest or quickest investment assessment techniques widely used

for project planning (Hashim and Piatti-Fünfkirchen, 2018). The accumulated gains are derived

from initial expenditures. ARR is the capital budgeting method that doesn't take all cash flows

into account. The higher the consumer earnings yield is beneficial, on the other hand lower the

ARR is not more profitable. The constant reinforced outcomes on different projects and makes

the necessary management choices. Projection of 6 year ARR is calculated below. The

company's managers evaluate their choices and determine whether or not to select this plan for

further spending. Base calculations are as follows:

Formula:

Accounting rate of return = Average annual profit / Initial Outlay * 100

Year Cash inflow Cash outflow Net Cash flow Depreciation Net cash flow

Year 0 275,000 -

Year 1 85,000 (12,500) 72,500 38,958.33 33541.67

Year 2 85,000 (12,500) 72,500 38,958.33 33541.67

Year 3 85,000 (12,500) 72,500 38,958.33 33541.67

Year 4 85,000 (12,500) 72,500 38,958.33 33541.67

Year 5 85,000 (12,500) 72,500 38,958.33 33541.67

Year 6 85,000 (12,500) 72,500 38,958.33 33541.67

Accounting Rate of Return = 33541.67 / 275,000 * 100

= 12.19 %

Working notes:

5

= 275000 / 85000

= 3.79 years

From the above calculation it is observed that payback period of this proposal is 3.79

years which are not so bad. Lovewell Company can spend their money into this project where

they can recover their initial investment within 4 years. Decision can be change if managers

found another best alternative which has low payback period in comparison to this project.

Accounting Rate of Return (ARR):

ARR has calculated in real numbers to anticipated risk of returns on investment or selling

the business. It is one of the simplest or quickest investment assessment techniques widely used

for project planning (Hashim and Piatti-Fünfkirchen, 2018). The accumulated gains are derived

from initial expenditures. ARR is the capital budgeting method that doesn't take all cash flows

into account. The higher the consumer earnings yield is beneficial, on the other hand lower the

ARR is not more profitable. The constant reinforced outcomes on different projects and makes

the necessary management choices. Projection of 6 year ARR is calculated below. The

company's managers evaluate their choices and determine whether or not to select this plan for

further spending. Base calculations are as follows:

Formula:

Accounting rate of return = Average annual profit / Initial Outlay * 100

Year Cash inflow Cash outflow Net Cash flow Depreciation Net cash flow

Year 0 275,000 -

Year 1 85,000 (12,500) 72,500 38,958.33 33541.67

Year 2 85,000 (12,500) 72,500 38,958.33 33541.67

Year 3 85,000 (12,500) 72,500 38,958.33 33541.67

Year 4 85,000 (12,500) 72,500 38,958.33 33541.67

Year 5 85,000 (12,500) 72,500 38,958.33 33541.67

Year 6 85,000 (12,500) 72,500 38,958.33 33541.67

Accounting Rate of Return = 33541.67 / 275,000 * 100

= 12.19 %

Working notes:

5

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

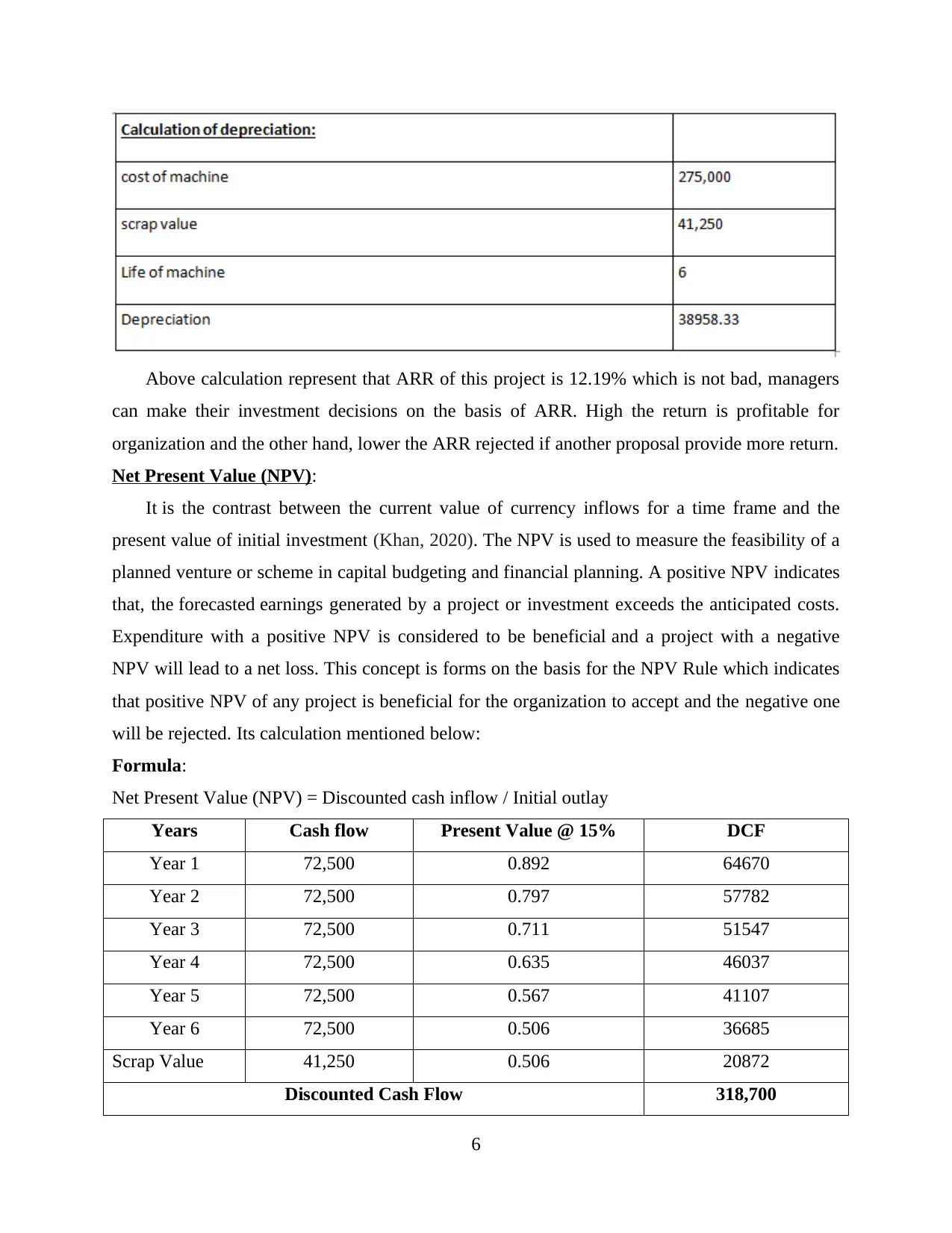

Above calculation represent that ARR of this project is 12.19% which is not bad, managers

can make their investment decisions on the basis of ARR. High the return is profitable for

organization and the other hand, lower the ARR rejected if another proposal provide more return.

Net Present Value (NPV):

It is the contrast between the current value of currency inflows for a time frame and the

present value of initial investment (Khan, 2020). The NPV is used to measure the feasibility of a

planned venture or scheme in capital budgeting and financial planning. A positive NPV indicates

that, the forecasted earnings generated by a project or investment exceeds the anticipated costs.

Expenditure with a positive NPV is considered to be beneficial and a project with a negative

NPV will lead to a net loss. This concept is forms on the basis for the NPV Rule which indicates

that positive NPV of any project is beneficial for the organization to accept and the negative one

will be rejected. Its calculation mentioned below:

Formula:

Net Present Value (NPV) = Discounted cash inflow / Initial outlay

Years Cash flow Present Value @ 15% DCF

Year 1 72,500 0.892 64670

Year 2 72,500 0.797 57782

Year 3 72,500 0.711 51547

Year 4 72,500 0.635 46037

Year 5 72,500 0.567 41107

Year 6 72,500 0.506 36685

Scrap Value 41,250 0.506 20872

Discounted Cash Flow 318,700

6

can make their investment decisions on the basis of ARR. High the return is profitable for

organization and the other hand, lower the ARR rejected if another proposal provide more return.

Net Present Value (NPV):

It is the contrast between the current value of currency inflows for a time frame and the

present value of initial investment (Khan, 2020). The NPV is used to measure the feasibility of a

planned venture or scheme in capital budgeting and financial planning. A positive NPV indicates

that, the forecasted earnings generated by a project or investment exceeds the anticipated costs.

Expenditure with a positive NPV is considered to be beneficial and a project with a negative

NPV will lead to a net loss. This concept is forms on the basis for the NPV Rule which indicates

that positive NPV of any project is beneficial for the organization to accept and the negative one

will be rejected. Its calculation mentioned below:

Formula:

Net Present Value (NPV) = Discounted cash inflow / Initial outlay

Years Cash flow Present Value @ 15% DCF

Year 1 72,500 0.892 64670

Year 2 72,500 0.797 57782

Year 3 72,500 0.711 51547

Year 4 72,500 0.635 46037

Year 5 72,500 0.567 41107

Year 6 72,500 0.506 36685

Scrap Value 41,250 0.506 20872

Discounted Cash Flow 318,700

6

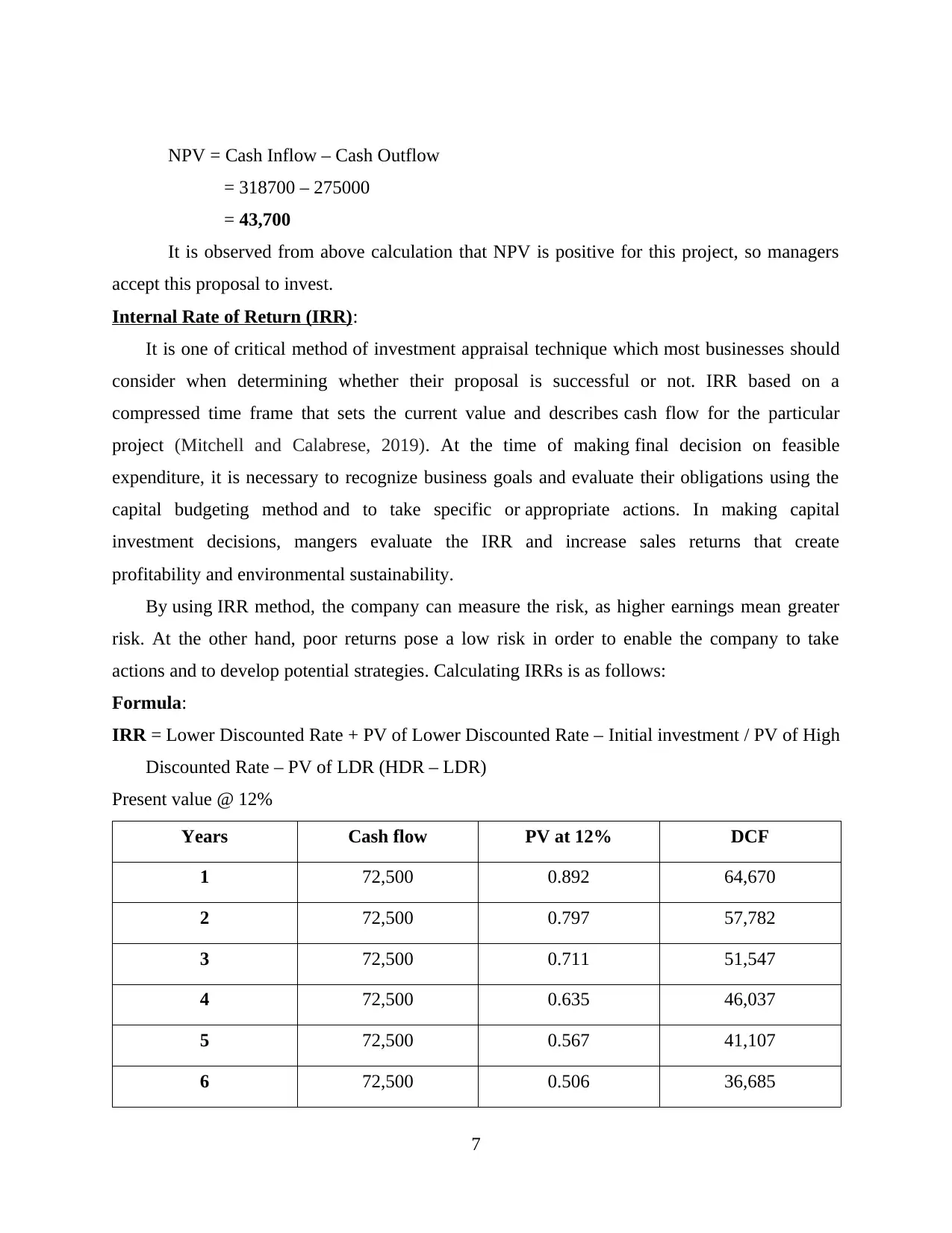

NPV = Cash Inflow – Cash Outflow

= 318700 – 275000

= 43,700

It is observed from above calculation that NPV is positive for this project, so managers

accept this proposal to invest.

Internal Rate of Return (IRR):

It is one of critical method of investment appraisal technique which most businesses should

consider when determining whether their proposal is successful or not. IRR based on a

compressed time frame that sets the current value and describes cash flow for the particular

project (Mitchell and Calabrese, 2019). At the time of making final decision on feasible

expenditure, it is necessary to recognize business goals and evaluate their obligations using the

capital budgeting method and to take specific or appropriate actions. In making capital

investment decisions, mangers evaluate the IRR and increase sales returns that create

profitability and environmental sustainability.

By using IRR method, the company can measure the risk, as higher earnings mean greater

risk. At the other hand, poor returns pose a low risk in order to enable the company to take

actions and to develop potential strategies. Calculating IRRs is as follows:

Formula:

IRR = Lower Discounted Rate + PV of Lower Discounted Rate – Initial investment / PV of High

Discounted Rate – PV of LDR (HDR – LDR)

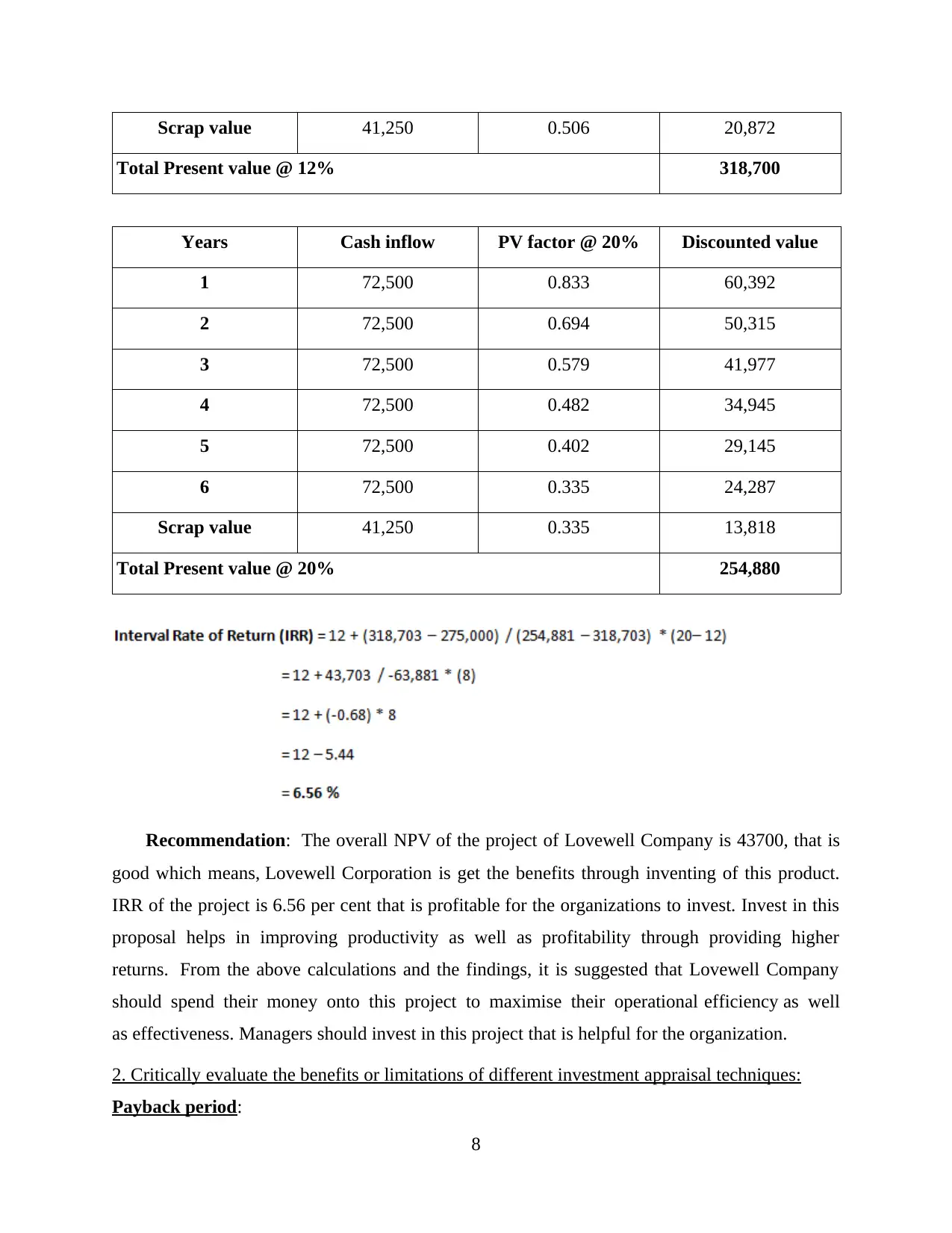

Present value @ 12%

Years Cash flow PV at 12% DCF

1 72,500 0.892 64,670

2 72,500 0.797 57,782

3 72,500 0.711 51,547

4 72,500 0.635 46,037

5 72,500 0.567 41,107

6 72,500 0.506 36,685

7

= 318700 – 275000

= 43,700

It is observed from above calculation that NPV is positive for this project, so managers

accept this proposal to invest.

Internal Rate of Return (IRR):

It is one of critical method of investment appraisal technique which most businesses should

consider when determining whether their proposal is successful or not. IRR based on a

compressed time frame that sets the current value and describes cash flow for the particular

project (Mitchell and Calabrese, 2019). At the time of making final decision on feasible

expenditure, it is necessary to recognize business goals and evaluate their obligations using the

capital budgeting method and to take specific or appropriate actions. In making capital

investment decisions, mangers evaluate the IRR and increase sales returns that create

profitability and environmental sustainability.

By using IRR method, the company can measure the risk, as higher earnings mean greater

risk. At the other hand, poor returns pose a low risk in order to enable the company to take

actions and to develop potential strategies. Calculating IRRs is as follows:

Formula:

IRR = Lower Discounted Rate + PV of Lower Discounted Rate – Initial investment / PV of High

Discounted Rate – PV of LDR (HDR – LDR)

Present value @ 12%

Years Cash flow PV at 12% DCF

1 72,500 0.892 64,670

2 72,500 0.797 57,782

3 72,500 0.711 51,547

4 72,500 0.635 46,037

5 72,500 0.567 41,107

6 72,500 0.506 36,685

7

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Scrap value 41,250 0.506 20,872

Total Present value @ 12% 318,700

Years Cash inflow PV factor @ 20% Discounted value

1 72,500 0.833 60,392

2 72,500 0.694 50,315

3 72,500 0.579 41,977

4 72,500 0.482 34,945

5 72,500 0.402 29,145

6 72,500 0.335 24,287

Scrap value 41,250 0.335 13,818

Total Present value @ 20% 254,880

Recommendation: The overall NPV of the project of Lovewell Company is 43700, that is

good which means, Lovewell Corporation is get the benefits through inventing of this product.

IRR of the project is 6.56 per cent that is profitable for the organizations to invest. Invest in this

proposal helps in improving productivity as well as profitability through providing higher

returns. From the above calculations and the findings, it is suggested that Lovewell Company

should spend their money onto this project to maximise their operational efficiency as well

as effectiveness. Managers should invest in this project that is helpful for the organization.

2. Critically evaluate the benefits or limitations of different investment appraisal techniques:

Payback period:

8

Total Present value @ 12% 318,700

Years Cash inflow PV factor @ 20% Discounted value

1 72,500 0.833 60,392

2 72,500 0.694 50,315

3 72,500 0.579 41,977

4 72,500 0.482 34,945

5 72,500 0.402 29,145

6 72,500 0.335 24,287

Scrap value 41,250 0.335 13,818

Total Present value @ 20% 254,880

Recommendation: The overall NPV of the project of Lovewell Company is 43700, that is

good which means, Lovewell Corporation is get the benefits through inventing of this product.

IRR of the project is 6.56 per cent that is profitable for the organizations to invest. Invest in this

proposal helps in improving productivity as well as profitability through providing higher

returns. From the above calculations and the findings, it is suggested that Lovewell Company

should spend their money onto this project to maximise their operational efficiency as well

as effectiveness. Managers should invest in this project that is helpful for the organization.

2. Critically evaluate the benefits or limitations of different investment appraisal techniques:

Payback period:

8

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Benefits: Payback period is highly helpful for a business owner which may not need to

make more difficult estimates trying to take care of some factors including marketing prices and

marketing impacts (Moortgat, Annaert and Deloof, 2017). The judgment whether to

select project or not is among the most critical decision which can be made easy through

following this capital budgeting technique. Managers may pick the correct investment

distribution, with the aid of this tool. It would allow for quick response, as it would allow the

company to recover their original cost in minimum time.

Drawbacks: One of the most critical drawbacks of payback period method is that time value

does not considered it. The cash balance is assigned higher significance in the initial years of the

project than in later life. Two enterprises refer to the same payback period. But, one spending

more cash to produces more cash flow in the first three years. In later years the second fund

provides more cash flows. This example does not specifically define which initiative they are

opting to reimburse for. Managers should avoid unpleasant NPVs because they make important

decisions that do little good. The policy does not understand the investments of money and

would rely on the average period, as each investment will have the same cash flow as other

choices.

Accounting rate of return:

Benefits: ARR allows companies to make investments. Strong revenues for the company are

safe and competitive. Management assesses the ARR proposal by selecting the right one before

making final decisions. This approach acknowledges the reporting significance that executives

often consider in the implementation period.

Drawbacks: This would not allow the time valuation of assets into account. The approach to

measuring capital expenditures is also unscientific (Siminica, Motoi and Dumitru, 2017)

(Valencia-Cárdenas and Restrepo-Morales, 2016) (Waxman, 2017). Typical return expectations

do not take into consideration the cash flow of assets, which relies on both disclosing income and

actual benefits. It will also affect the different activities that need to be carried out. Within this

methodology of analysis, the effect as well as the end outcome or viability of the proposal is

ignored.

Net Present Value (NPV):

Benefits: The lot of firms use the NPV to evaluate the commitment and evaluate whether the

company is spending in this project. The positive benefit of the preferred and unfavourable NPV

9

make more difficult estimates trying to take care of some factors including marketing prices and

marketing impacts (Moortgat, Annaert and Deloof, 2017). The judgment whether to

select project or not is among the most critical decision which can be made easy through

following this capital budgeting technique. Managers may pick the correct investment

distribution, with the aid of this tool. It would allow for quick response, as it would allow the

company to recover their original cost in minimum time.

Drawbacks: One of the most critical drawbacks of payback period method is that time value

does not considered it. The cash balance is assigned higher significance in the initial years of the

project than in later life. Two enterprises refer to the same payback period. But, one spending

more cash to produces more cash flow in the first three years. In later years the second fund

provides more cash flows. This example does not specifically define which initiative they are

opting to reimburse for. Managers should avoid unpleasant NPVs because they make important

decisions that do little good. The policy does not understand the investments of money and

would rely on the average period, as each investment will have the same cash flow as other

choices.

Accounting rate of return:

Benefits: ARR allows companies to make investments. Strong revenues for the company are

safe and competitive. Management assesses the ARR proposal by selecting the right one before

making final decisions. This approach acknowledges the reporting significance that executives

often consider in the implementation period.

Drawbacks: This would not allow the time valuation of assets into account. The approach to

measuring capital expenditures is also unscientific (Siminica, Motoi and Dumitru, 2017)

(Valencia-Cárdenas and Restrepo-Morales, 2016) (Waxman, 2017). Typical return expectations

do not take into consideration the cash flow of assets, which relies on both disclosing income and

actual benefits. It will also affect the different activities that need to be carried out. Within this

methodology of analysis, the effect as well as the end outcome or viability of the proposal is

ignored.

Net Present Value (NPV):

Benefits: The lot of firms use the NPV to evaluate the commitment and evaluate whether the

company is spending in this project. The positive benefit of the preferred and unfavourable NPV

9

will be rejected as the client is not supported by this effort. This financial valuation approach

takes into account the time value of money and provides new prospects for companies. Managers

should make choices that are focused on the value of the NPV.

Limitations: Managers may use these methods to assess the feasibility of their projects or to

equate them with other plans, but not just because all cash flows are equal in a project. They

need to check or claim if the initial expenditure is low, since it has no valid findings. When

modified net present value, determined by the decreased expense, avoids external variables such

as inflation.

Internal Rate of Return (IRR):

Benefits: IRR was being used primarily to describe the return that business received just

after investment, and to make more rational choices (Shakeel and Datta, 2020). Managerial

decisions which determine high yields but which project helps companies optimize their income

promotes the choice of its most efficient project leaders for the company.

Limitations: IRR doesn't really acknowledge economics of scale which affect efficiency. It

is determined by means of a system of effect & control which produces no accurate results.

Independent decision-taking processes are also affected. Additionally, there is no other

distinction in loans or borrowings. Similar to the decreased costs, each company has varying

returns, and investment decisions on executives are difficult.

CONCLUSION

From the above observation it has been concluded that, financial management play essential

role in the organization which help the managers to make operational decisions which maximise

the productivity as well as profitability. It further helps in increasing efficiency as well as

effectiveness after evaluating the above discussed findings. Managers select the best suitable

valuation method that is beneficial in context of the organization. On the other side, there are

several investment appraisal techniques which are used to evaluate the best proposal which helps

in selecting more favourable as well as profitable project.

10

takes into account the time value of money and provides new prospects for companies. Managers

should make choices that are focused on the value of the NPV.

Limitations: Managers may use these methods to assess the feasibility of their projects or to

equate them with other plans, but not just because all cash flows are equal in a project. They

need to check or claim if the initial expenditure is low, since it has no valid findings. When

modified net present value, determined by the decreased expense, avoids external variables such

as inflation.

Internal Rate of Return (IRR):

Benefits: IRR was being used primarily to describe the return that business received just

after investment, and to make more rational choices (Shakeel and Datta, 2020). Managerial

decisions which determine high yields but which project helps companies optimize their income

promotes the choice of its most efficient project leaders for the company.

Limitations: IRR doesn't really acknowledge economics of scale which affect efficiency. It

is determined by means of a system of effect & control which produces no accurate results.

Independent decision-taking processes are also affected. Additionally, there is no other

distinction in loans or borrowings. Similar to the decreased costs, each company has varying

returns, and investment decisions on executives are difficult.

CONCLUSION

From the above observation it has been concluded that, financial management play essential

role in the organization which help the managers to make operational decisions which maximise

the productivity as well as profitability. It further helps in increasing efficiency as well as

effectiveness after evaluating the above discussed findings. Managers select the best suitable

valuation method that is beneficial in context of the organization. On the other side, there are

several investment appraisal techniques which are used to evaluate the best proposal which helps

in selecting more favourable as well as profitable project.

10

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.