APC308 Financial Management: Valuation, Investment Appraisal Analysis

VerifiedAdded on 2023/01/09

|18

|4975

|70

Homework Assignment

AI Summary

This assignment solution for a Financial Management course delves into key financial concepts, focusing on mergers and acquisitions, and investment appraisal techniques. The assignment begins with an introduction to financial management, highlighting its importance in efficient business operations. The main body addresses two primary questions. The first question involves calculating the value of Trojan Plc using various valuation methods, including the Price-Earnings Ratio, Dividend Valuation Model, and Discounted Cash Flow method, along with a discussion of their advantages and disadvantages. The second question focuses on investment appraisal techniques, calculating and providing recommendations for various methods. The assignment concludes with a summary of the findings and recommendations, along with a list of references used in the analysis.

Financial Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Contents

INTRODUCTION...........................................................................................................................................4

MAIN BODY.................................................................................................................................................4

Question 1- Merger and Takeovers.............................................................................................................4

1. Calculate the value for Trojan Plc by using various valuation method................................................4

Question 3. Investment Appraisal Techniques............................................................................................9

1. Calculate following investment appraisal technique and give brief recommendations........................9

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

INTRODUCTION...........................................................................................................................................4

MAIN BODY.................................................................................................................................................4

Question 1- Merger and Takeovers.............................................................................................................4

1. Calculate the value for Trojan Plc by using various valuation method................................................4

Question 3. Investment Appraisal Techniques............................................................................................9

1. Calculate following investment appraisal technique and give brief recommendations........................9

CONCLUSION.............................................................................................................................................16

REFERENCES..............................................................................................................................................17

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

The concept financial management basically means performing the business information of

the company in an efficient manner. Corporation's financial roles involve payroll, rules and

standards, record-keeping and order to move ahead, planning and scheduling activities, money

management protocols and responsibility for examine the economic. Strong financial

management aims at ensuring service is run as an economically viable company. Effective

financial management needs to achieve service is run as a fiscally viable company (Adrian,

Estrella and Shin, 2019). The key objective of the project research work is to reach conclusions

concerning wide range of financial definitions along with disbursements, expenditure evaluation

criteria, etc. The method of determining, reporting, analyzing and produced commercially about

the economic part of the economy is recognized as financial management that supports decision

making to increase the profitability of the employees.

There were 2 questions related to the project overview that are applicable to the concepts of

merger & acquisition and investment evaluation methodology. The analysis provides information

on the theoretical and empirical studies of the two mentioned concepts.

MAIN BODY

Question 1- Merger and Takeovers

1. Calculate the value for Trojan Plc by using various valuation method

This function entails the mergers and acquisitions that Aztec plc intends to acquire Trojan

plc through. To this end, financial information from both companies is given to decide either

Aztec plc can purchase so or not. A range of measures are used in conjunction with analyzes,

that are often performed in a way that makes the smart choices:

Price earnings ratio: This ratio is also named PER which represents the association between the

company's stock values and each shareholder's effectiveness. Employees use the formula to make

an estimate of equal value, so that they might determine whether they are priced up or down. The

main goal of using this approach is to conduct the analysis of a value - chain so that the stock

price can be accurately determined. Shareholders may find it beneficial when determining the

earnings market value of a business by contributing to results (Aymen, Alhamzah and Bilal,

The concept financial management basically means performing the business information of

the company in an efficient manner. Corporation's financial roles involve payroll, rules and

standards, record-keeping and order to move ahead, planning and scheduling activities, money

management protocols and responsibility for examine the economic. Strong financial

management aims at ensuring service is run as an economically viable company. Effective

financial management needs to achieve service is run as a fiscally viable company (Adrian,

Estrella and Shin, 2019). The key objective of the project research work is to reach conclusions

concerning wide range of financial definitions along with disbursements, expenditure evaluation

criteria, etc. The method of determining, reporting, analyzing and produced commercially about

the economic part of the economy is recognized as financial management that supports decision

making to increase the profitability of the employees.

There were 2 questions related to the project overview that are applicable to the concepts of

merger & acquisition and investment evaluation methodology. The analysis provides information

on the theoretical and empirical studies of the two mentioned concepts.

MAIN BODY

Question 1- Merger and Takeovers

1. Calculate the value for Trojan Plc by using various valuation method

This function entails the mergers and acquisitions that Aztec plc intends to acquire Trojan

plc through. To this end, financial information from both companies is given to decide either

Aztec plc can purchase so or not. A range of measures are used in conjunction with analyzes,

that are often performed in a way that makes the smart choices:

Price earnings ratio: This ratio is also named PER which represents the association between the

company's stock values and each shareholder's effectiveness. Employees use the formula to make

an estimate of equal value, so that they might determine whether they are priced up or down. The

main goal of using this approach is to conduct the analysis of a value - chain so that the stock

price can be accurately determined. Shareholders may find it beneficial when determining the

earnings market value of a business by contributing to results (Aymen, Alhamzah and Bilal,

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

2019). In addition to these attributes, there are certain drawbacks that are addressed during this

whole amount, as tries to follow:

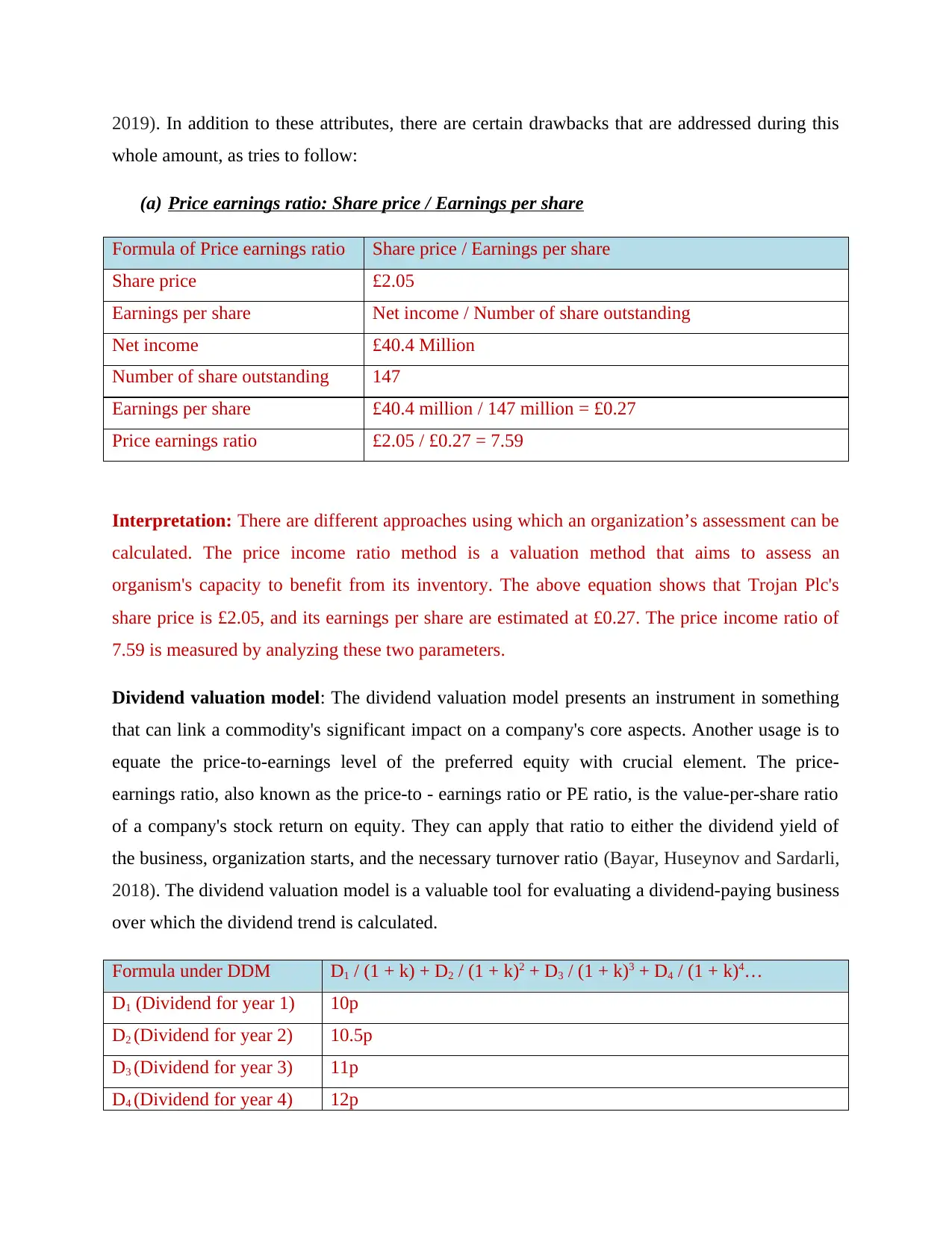

(a) Price earnings ratio: Share price / Earnings per share

Formula of Price earnings ratio Share price / Earnings per share

Share price £2.05

Earnings per share Net income / Number of share outstanding

Net income £40.4 Million

Number of share outstanding 147

Earnings per share £40.4 million / 147 million = £0.27

Price earnings ratio £2.05 / £0.27 = 7.59

Interpretation: There are different approaches using which an organization’s assessment can be

calculated. The price income ratio method is a valuation method that aims to assess an

organism's capacity to benefit from its inventory. The above equation shows that Trojan Plc's

share price is £2.05, and its earnings per share are estimated at £0.27. The price income ratio of

7.59 is measured by analyzing these two parameters.

Dividend valuation model: The dividend valuation model presents an instrument in something

that can link a commodity's significant impact on a company's core aspects. Another usage is to

equate the price-to-earnings level of the preferred equity with crucial element. The price-

earnings ratio, also known as the price-to - earnings ratio or PE ratio, is the value-per-share ratio

of a company's stock return on equity. They can apply that ratio to either the dividend yield of

the business, organization starts, and the necessary turnover ratio (Bayar, Huseynov and Sardarli,

2018). The dividend valuation model is a valuable tool for evaluating a dividend-paying business

over which the dividend trend is calculated.

Formula under DDM D1 / (1 + k) + D2 / (1 + k)2 + D3 / (1 + k)3 + D4 / (1 + k)4…

D1 (Dividend for year 1) 10p

D2 (Dividend for year 2) 10.5p

D3 (Dividend for year 3) 11p

D4 (Dividend for year 4) 12p

whole amount, as tries to follow:

(a) Price earnings ratio: Share price / Earnings per share

Formula of Price earnings ratio Share price / Earnings per share

Share price £2.05

Earnings per share Net income / Number of share outstanding

Net income £40.4 Million

Number of share outstanding 147

Earnings per share £40.4 million / 147 million = £0.27

Price earnings ratio £2.05 / £0.27 = 7.59

Interpretation: There are different approaches using which an organization’s assessment can be

calculated. The price income ratio method is a valuation method that aims to assess an

organism's capacity to benefit from its inventory. The above equation shows that Trojan Plc's

share price is £2.05, and its earnings per share are estimated at £0.27. The price income ratio of

7.59 is measured by analyzing these two parameters.

Dividend valuation model: The dividend valuation model presents an instrument in something

that can link a commodity's significant impact on a company's core aspects. Another usage is to

equate the price-to-earnings level of the preferred equity with crucial element. The price-

earnings ratio, also known as the price-to - earnings ratio or PE ratio, is the value-per-share ratio

of a company's stock return on equity. They can apply that ratio to either the dividend yield of

the business, organization starts, and the necessary turnover ratio (Bayar, Huseynov and Sardarli,

2018). The dividend valuation model is a valuable tool for evaluating a dividend-paying business

over which the dividend trend is calculated.

Formula under DDM D1 / (1 + k) + D2 / (1 + k)2 + D3 / (1 + k)3 + D4 / (1 + k)4…

D1 (Dividend for year 1) 10p

D2 (Dividend for year 2) 10.5p

D3 (Dividend for year 3) 11p

D4 (Dividend for year 4) 12p

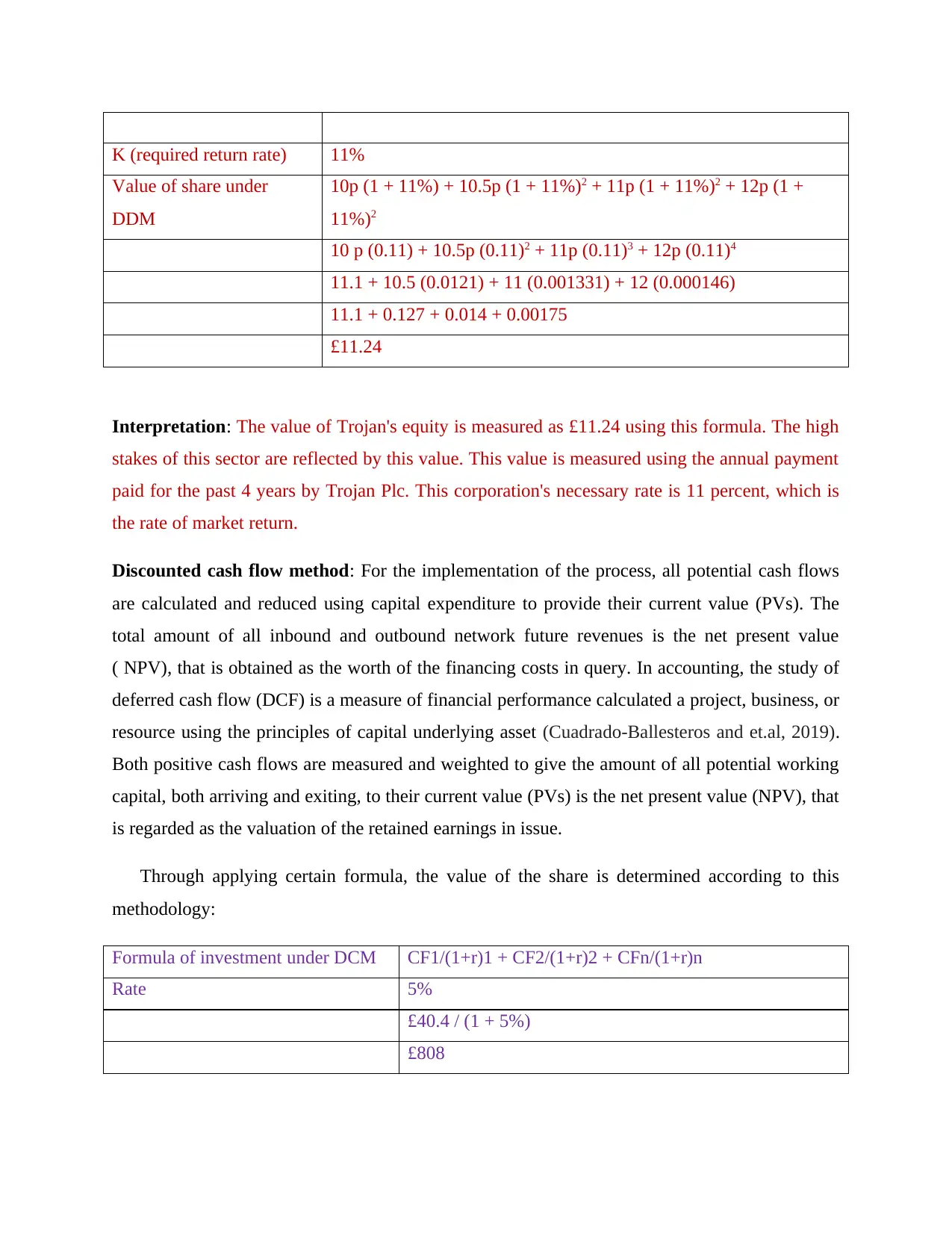

K (required return rate) 11%

Value of share under

DDM

10p (1 + 11%) + 10.5p (1 + 11%)2 + 11p (1 + 11%)2 + 12p (1 +

11%)2

10 p (0.11) + 10.5p (0.11)2 + 11p (0.11)3 + 12p (0.11)4

11.1 + 10.5 (0.0121) + 11 (0.001331) + 12 (0.000146)

11.1 + 0.127 + 0.014 + 0.00175

£11.24

Interpretation: The value of Trojan's equity is measured as £11.24 using this formula. The high

stakes of this sector are reflected by this value. This value is measured using the annual payment

paid for the past 4 years by Trojan Plc. This corporation's necessary rate is 11 percent, which is

the rate of market return.

Discounted cash flow method: For the implementation of the process, all potential cash flows

are calculated and reduced using capital expenditure to provide their current value (PVs). The

total amount of all inbound and outbound network future revenues is the net present value

( NPV), that is obtained as the worth of the financing costs in query. In accounting, the study of

deferred cash flow (DCF) is a measure of financial performance calculated a project, business, or

resource using the principles of capital underlying asset (Cuadrado-Ballesteros and et.al, 2019).

Both positive cash flows are measured and weighted to give the amount of all potential working

capital, both arriving and exiting, to their current value (PVs) is the net present value (NPV), that

is regarded as the valuation of the retained earnings in issue.

Through applying certain formula, the value of the share is determined according to this

methodology:

Formula of investment under DCM CF1/(1+r)1 + CF2/(1+r)2 + CFn/(1+r)n

Rate 5%

£40.4 / (1 + 5%)

£808

Value of share under

DDM

10p (1 + 11%) + 10.5p (1 + 11%)2 + 11p (1 + 11%)2 + 12p (1 +

11%)2

10 p (0.11) + 10.5p (0.11)2 + 11p (0.11)3 + 12p (0.11)4

11.1 + 10.5 (0.0121) + 11 (0.001331) + 12 (0.000146)

11.1 + 0.127 + 0.014 + 0.00175

£11.24

Interpretation: The value of Trojan's equity is measured as £11.24 using this formula. The high

stakes of this sector are reflected by this value. This value is measured using the annual payment

paid for the past 4 years by Trojan Plc. This corporation's necessary rate is 11 percent, which is

the rate of market return.

Discounted cash flow method: For the implementation of the process, all potential cash flows

are calculated and reduced using capital expenditure to provide their current value (PVs). The

total amount of all inbound and outbound network future revenues is the net present value

( NPV), that is obtained as the worth of the financing costs in query. In accounting, the study of

deferred cash flow (DCF) is a measure of financial performance calculated a project, business, or

resource using the principles of capital underlying asset (Cuadrado-Ballesteros and et.al, 2019).

Both positive cash flows are measured and weighted to give the amount of all potential working

capital, both arriving and exiting, to their current value (PVs) is the net present value (NPV), that

is regarded as the valuation of the retained earnings in issue.

Through applying certain formula, the value of the share is determined according to this

methodology:

Formula of investment under DCM CF1/(1+r)1 + CF2/(1+r)2 + CFn/(1+r)n

Rate 5%

£40.4 / (1 + 5%)

£808

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Interpretation: The net cash flow for the current year is estimated to be the income of this

business, that is £40.4, and the business's discount rate is estimated to be 5%, which seems to be

the corporation's Treasury bill yield. The present value of the Trojan 's financing under DCM is

measured as £808 using such parameters.

2. Discussed the problems associated with valuation models with the help of evaluating

advantages or disadvantages

Price earnings ratio

Advantages: The "price-to - earnings per equity" ratio, referred as P / E, is possibly the most

widespread was using ratio when the market price of equity is evaluated. Tom Copeland

characterizes P / E as wants to follow, "[P / E method] implies that in the persisting period

especially will also be good enough to justify some numerous of its potential profits. The high pe

ratio business is also seen as technology stocks (Cui and et.al, 2019). This implies high operating

margins, beneficial production in the long term and generally venture capitalists are ready to pay

as much for the shareholdings in this financial institution. If a company with a lower pe ratio

implies weak actual and potential growth in revenue, the inventory is underrated, etc. Looking to

invest in quite an undertaking could render a risky proposition.

Disadvantage: If there is an positive feeling in the overall market and economic climate, then

investors prefer to overpricing shares, thereby increasing P / E to a point that, yes technically, the

financial documents do not explain. This could cause a burst, enough that-called, with whom

prices and P / Es are so large that they can explode, or got a negative, that is, implosion at any

moment. The next downside comes from unemployment. During inflationary times, the money

of the particular country in which the measurement of the portion occurs. The issue of this is that

if we swap the company's profitability to a foreign exchange, assume from USD to EUR, the

corporation's profits can be devalued, which has in effect improves P / E, provided the equation.

Dividend valuation method

Advantage: There's no perfect valuation model. The personalized complexity of business

modern world also indicates that there is not one standard model to be used for share price either.

One of the benefits of the dividends investment strategy is that it still provides margins of

business, that is £40.4, and the business's discount rate is estimated to be 5%, which seems to be

the corporation's Treasury bill yield. The present value of the Trojan 's financing under DCM is

measured as £808 using such parameters.

2. Discussed the problems associated with valuation models with the help of evaluating

advantages or disadvantages

Price earnings ratio

Advantages: The "price-to - earnings per equity" ratio, referred as P / E, is possibly the most

widespread was using ratio when the market price of equity is evaluated. Tom Copeland

characterizes P / E as wants to follow, "[P / E method] implies that in the persisting period

especially will also be good enough to justify some numerous of its potential profits. The high pe

ratio business is also seen as technology stocks (Cui and et.al, 2019). This implies high operating

margins, beneficial production in the long term and generally venture capitalists are ready to pay

as much for the shareholdings in this financial institution. If a company with a lower pe ratio

implies weak actual and potential growth in revenue, the inventory is underrated, etc. Looking to

invest in quite an undertaking could render a risky proposition.

Disadvantage: If there is an positive feeling in the overall market and economic climate, then

investors prefer to overpricing shares, thereby increasing P / E to a point that, yes technically, the

financial documents do not explain. This could cause a burst, enough that-called, with whom

prices and P / Es are so large that they can explode, or got a negative, that is, implosion at any

moment. The next downside comes from unemployment. During inflationary times, the money

of the particular country in which the measurement of the portion occurs. The issue of this is that

if we swap the company's profitability to a foreign exchange, assume from USD to EUR, the

corporation's profits can be devalued, which has in effect improves P / E, provided the equation.

Dividend valuation method

Advantage: There's no perfect valuation model. The personalized complexity of business

modern world also indicates that there is not one standard model to be used for share price either.

One of the benefits of the dividends investment strategy is that it still provides margins of

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

protection. They should decide where the interest is, then allocate an asset location that functions

for expenditure. This involves having a grip on that when as well as how to spend (Dewanty and

Isbanah, 2018). Though its dividend valuation model relies on assumptions to generate results,

this model involves less rationality especially in comparison with other profitability ratios.

There's no ambiguity in defining a dividend. That means that and use this model to assess

interest, there will be less image features, increasing the likelihood that each shareholder will use

this model to produce a shared result. Furthermore, this methodology is too simple to use

because once the principle of measurement has been established by professionals, it can become

simple for them to apply it on any dividend-offering stock. Over this, shareholders can have

greater leverage over their financing options since they can verify the real value of share price

transactions.

Disadvantage: There are a number of variables that can affect a share value across period.

Satisfied customer, brand recognition as well as the possession of derivative instruments each

have the capacity to raise the corporation's worth. If the annual growth of the dividends is

constant and established, those non-dividend variables will potentially affect the stock profits.

Which implies the accounting method cannot yield optimal results, even though mainly

consisting. Here with this strategy, only certain stocks that give dividends can be added. This

cannot be generalised to those stock forms. Because of all this, it cannot be used in small

businesses because they cannot pay dividends on the inventory.

Discounted cash flow method

Advantage: The discounted cash flow model has a significant advantage that this really lowers a

capital expenditure to a single image. When the benefits outweigh the costs, it is assumed the

expenditure will be a source of money; if it is unfavourable, the transaction will be a losers. It

helps judgments on financial properties to be up-to-down. In addition, the approach helps in

making a decision between substantially different contributions. Measure cash flows with

expenditure, reduce them to discount rate, add these up and share them. The much more

attractive option is the one with the lowest average present-value (Dhole, Mishra and Pal, 2019).

It eliminates the problem and complexities for company managers in selecting one choice or

choice from a number of investment proposals that are almost equal in size. The reliability of the

for expenditure. This involves having a grip on that when as well as how to spend (Dewanty and

Isbanah, 2018). Though its dividend valuation model relies on assumptions to generate results,

this model involves less rationality especially in comparison with other profitability ratios.

There's no ambiguity in defining a dividend. That means that and use this model to assess

interest, there will be less image features, increasing the likelihood that each shareholder will use

this model to produce a shared result. Furthermore, this methodology is too simple to use

because once the principle of measurement has been established by professionals, it can become

simple for them to apply it on any dividend-offering stock. Over this, shareholders can have

greater leverage over their financing options since they can verify the real value of share price

transactions.

Disadvantage: There are a number of variables that can affect a share value across period.

Satisfied customer, brand recognition as well as the possession of derivative instruments each

have the capacity to raise the corporation's worth. If the annual growth of the dividends is

constant and established, those non-dividend variables will potentially affect the stock profits.

Which implies the accounting method cannot yield optimal results, even though mainly

consisting. Here with this strategy, only certain stocks that give dividends can be added. This

cannot be generalised to those stock forms. Because of all this, it cannot be used in small

businesses because they cannot pay dividends on the inventory.

Discounted cash flow method

Advantage: The discounted cash flow model has a significant advantage that this really lowers a

capital expenditure to a single image. When the benefits outweigh the costs, it is assumed the

expenditure will be a source of money; if it is unfavourable, the transaction will be a losers. It

helps judgments on financial properties to be up-to-down. In addition, the approach helps in

making a decision between substantially different contributions. Measure cash flows with

expenditure, reduce them to discount rate, add these up and share them. The much more

attractive option is the one with the lowest average present-value (Dhole, Mishra and Pal, 2019).

It eliminates the problem and complexities for company managers in selecting one choice or

choice from a number of investment proposals that are almost equal in size. The reliability of the

outcome generated helps businesses to make appropriate decisions pertaining to big capital

investments.

Disadvantage: The discounted cash flow method uses a variety in segregation. But you'd be

smart not to search at that quantity in separation. Think, there are going to comprehend a

business's worth. We will use the discounted cash flow approach to construct an asset value.

They could even evaluate how reasonable that percentage is by conducting a wakeup call,

examining how the profit generated from the net cash flows measures up with the share value of

the corporation; with the statement of financial position significance as seen on the income

statement; and with the significance of like businesses. Furthermore, this approach is solely

based on discounted cash flows that are measured on the assumption of capital costs. It is

believed that the pace of this capital cost renders outcomes uncertain and if businesses make

investments appropriately, they will face losses in the future.

RECOMMENDATION: Using the analysis described above, Aztec plc should follow the DDM

method. It's because a firm's stock price is calculated underneath it, which again is beneficial to

the organization. Although valuation of earnings and cash flow is carried out in the remaining

two ways, it cannot be effective for all parties in an organisation. Therefore, the business above

should choose the DDM process.

Question 3. Investment Appraisal Techniques

1. Calculate following investment appraisal technique and give brief recommendations

Investment evaluation approaches involve different tools that companies have used

measure any investor's profitability. These strategies are adopted by most companies and

calculate how effective and efficient it is, payback duration, internal rate of return (IRR), net

present value (NPV), rate of return accounting, etc. Such approaches evaluate a specific device

and then administrators pick the most relevant one (Tkachenko and et.al, 2019). The idea of this

method is to study the viability and success of the project and then to render additional financial

decisions. Love-well restricted administrators adopt this strategy to determine whether or not

expenditure is advantageous or competitive for enterprise. Suggest also that the organization

must and therefore should not be included in this and the further estimate underneath:

investments.

Disadvantage: The discounted cash flow method uses a variety in segregation. But you'd be

smart not to search at that quantity in separation. Think, there are going to comprehend a

business's worth. We will use the discounted cash flow approach to construct an asset value.

They could even evaluate how reasonable that percentage is by conducting a wakeup call,

examining how the profit generated from the net cash flows measures up with the share value of

the corporation; with the statement of financial position significance as seen on the income

statement; and with the significance of like businesses. Furthermore, this approach is solely

based on discounted cash flows that are measured on the assumption of capital costs. It is

believed that the pace of this capital cost renders outcomes uncertain and if businesses make

investments appropriately, they will face losses in the future.

RECOMMENDATION: Using the analysis described above, Aztec plc should follow the DDM

method. It's because a firm's stock price is calculated underneath it, which again is beneficial to

the organization. Although valuation of earnings and cash flow is carried out in the remaining

two ways, it cannot be effective for all parties in an organisation. Therefore, the business above

should choose the DDM process.

Question 3. Investment Appraisal Techniques

1. Calculate following investment appraisal technique and give brief recommendations

Investment evaluation approaches involve different tools that companies have used

measure any investor's profitability. These strategies are adopted by most companies and

calculate how effective and efficient it is, payback duration, internal rate of return (IRR), net

present value (NPV), rate of return accounting, etc. Such approaches evaluate a specific device

and then administrators pick the most relevant one (Tkachenko and et.al, 2019). The idea of this

method is to study the viability and success of the project and then to render additional financial

decisions. Love-well restricted administrators adopt this strategy to determine whether or not

expenditure is advantageous or competitive for enterprise. Suggest also that the organization

must and therefore should not be included in this and the further estimate underneath:

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

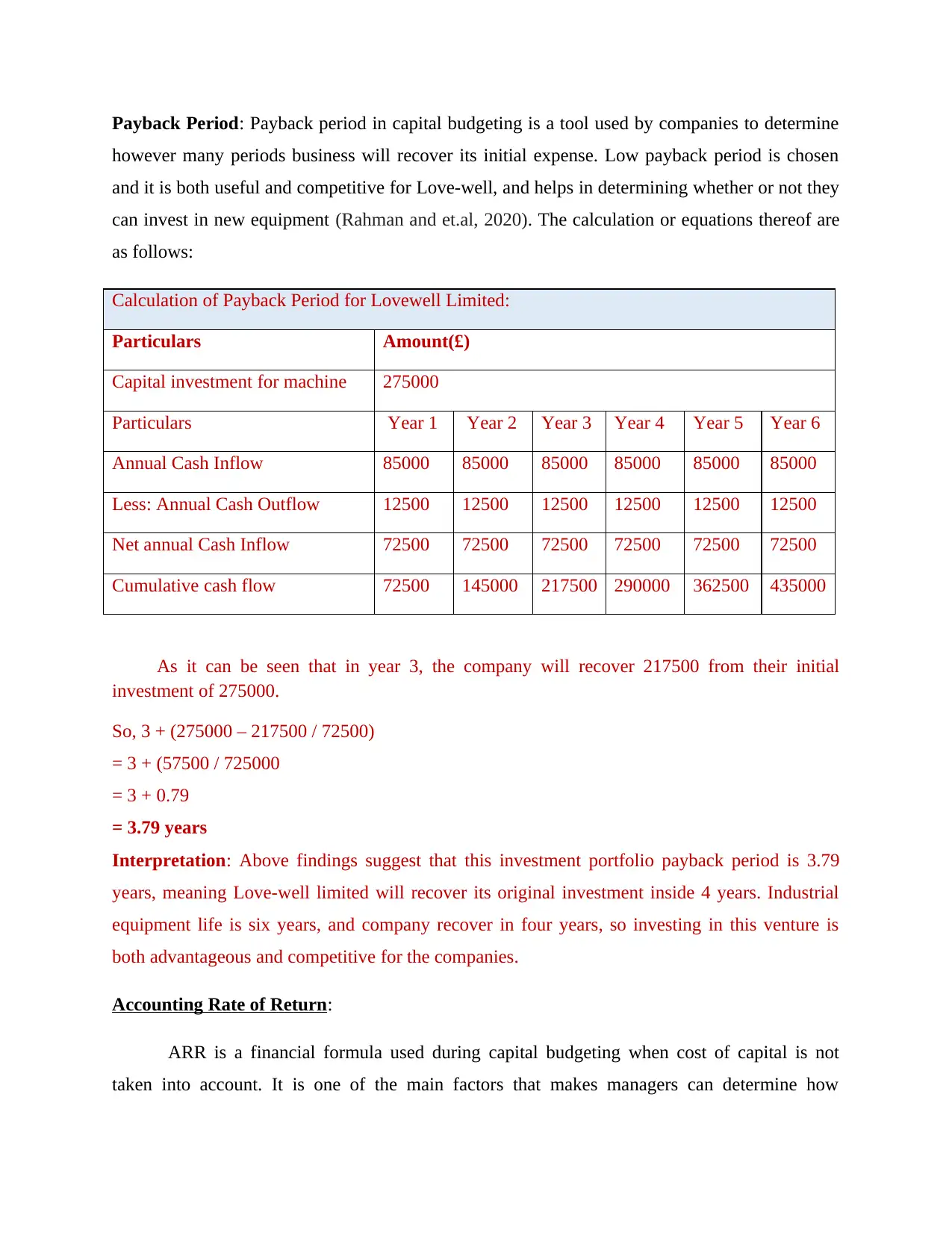

Payback Period: Payback period in capital budgeting is a tool used by companies to determine

however many periods business will recover its initial expense. Low payback period is chosen

and it is both useful and competitive for Love-well, and helps in determining whether or not they

can invest in new equipment (Rahman and et.al, 2020). The calculation or equations thereof are

as follows:

Calculation of Payback Period for Lovewell Limited:

Particulars Amount(£)

Capital investment for machine 275000

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Annual Cash Inflow 85000 85000 85000 85000 85000 85000

Less: Annual Cash Outflow 12500 12500 12500 12500 12500 12500

Net annual Cash Inflow 72500 72500 72500 72500 72500 72500

Cumulative cash flow 72500 145000 217500 290000 362500 435000

As it can be seen that in year 3, the company will recover 217500 from their initial

investment of 275000.

So, 3 + (275000 – 217500 / 72500)

= 3 + (57500 / 725000

= 3 + 0.79

= 3.79 years

Interpretation: Above findings suggest that this investment portfolio payback period is 3.79

years, meaning Love-well limited will recover its original investment inside 4 years. Industrial

equipment life is six years, and company recover in four years, so investing in this venture is

both advantageous and competitive for the companies.

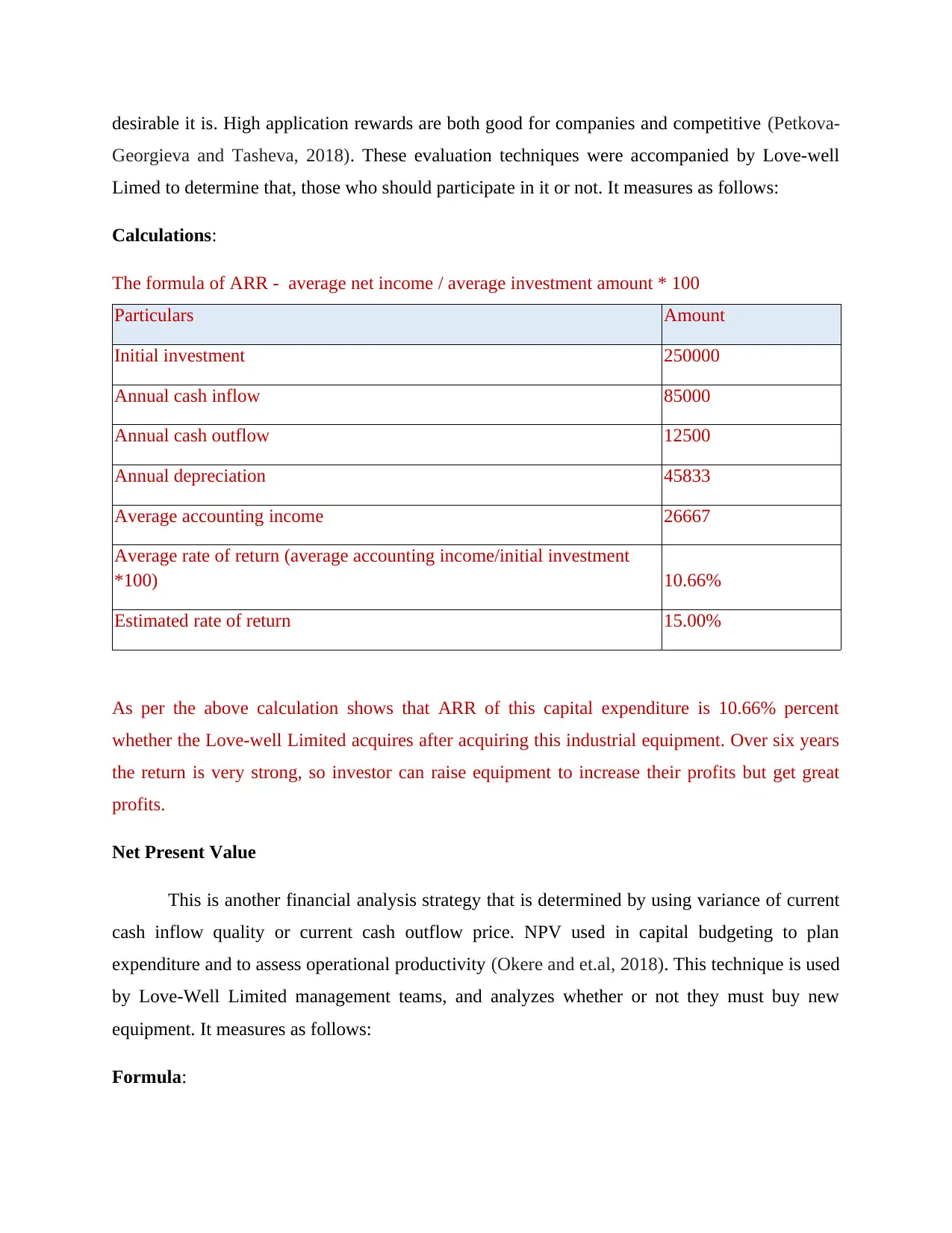

Accounting Rate of Return:

ARR is a financial formula used during capital budgeting when cost of capital is not

taken into account. It is one of the main factors that makes managers can determine how

however many periods business will recover its initial expense. Low payback period is chosen

and it is both useful and competitive for Love-well, and helps in determining whether or not they

can invest in new equipment (Rahman and et.al, 2020). The calculation or equations thereof are

as follows:

Calculation of Payback Period for Lovewell Limited:

Particulars Amount(£)

Capital investment for machine 275000

Particulars Year 1 Year 2 Year 3 Year 4 Year 5 Year 6

Annual Cash Inflow 85000 85000 85000 85000 85000 85000

Less: Annual Cash Outflow 12500 12500 12500 12500 12500 12500

Net annual Cash Inflow 72500 72500 72500 72500 72500 72500

Cumulative cash flow 72500 145000 217500 290000 362500 435000

As it can be seen that in year 3, the company will recover 217500 from their initial

investment of 275000.

So, 3 + (275000 – 217500 / 72500)

= 3 + (57500 / 725000

= 3 + 0.79

= 3.79 years

Interpretation: Above findings suggest that this investment portfolio payback period is 3.79

years, meaning Love-well limited will recover its original investment inside 4 years. Industrial

equipment life is six years, and company recover in four years, so investing in this venture is

both advantageous and competitive for the companies.

Accounting Rate of Return:

ARR is a financial formula used during capital budgeting when cost of capital is not

taken into account. It is one of the main factors that makes managers can determine how

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

desirable it is. High application rewards are both good for companies and competitive (Petkova-

Georgieva and Tasheva, 2018). These evaluation techniques were accompanied by Love-well

Limed to determine that, those who should participate in it or not. It measures as follows:

Calculations:

The formula of ARR - average net income / average investment amount * 100

Particulars Amount

Initial investment 250000

Annual cash inflow 85000

Annual cash outflow 12500

Annual depreciation 45833

Average accounting income 26667

Average rate of return (average accounting income/initial investment

*100) 10.66%

Estimated rate of return 15.00%

As per the above calculation shows that ARR of this capital expenditure is 10.66% percent

whether the Love-well Limited acquires after acquiring this industrial equipment. Over six years

the return is very strong, so investor can raise equipment to increase their profits but get great

profits.

Net Present Value

This is another financial analysis strategy that is determined by using variance of current

cash inflow quality or current cash outflow price. NPV used in capital budgeting to plan

expenditure and to assess operational productivity (Okere and et.al, 2018). This technique is used

by Love-Well Limited management teams, and analyzes whether or not they must buy new

equipment. It measures as follows:

Formula:

Georgieva and Tasheva, 2018). These evaluation techniques were accompanied by Love-well

Limed to determine that, those who should participate in it or not. It measures as follows:

Calculations:

The formula of ARR - average net income / average investment amount * 100

Particulars Amount

Initial investment 250000

Annual cash inflow 85000

Annual cash outflow 12500

Annual depreciation 45833

Average accounting income 26667

Average rate of return (average accounting income/initial investment

*100) 10.66%

Estimated rate of return 15.00%

As per the above calculation shows that ARR of this capital expenditure is 10.66% percent

whether the Love-well Limited acquires after acquiring this industrial equipment. Over six years

the return is very strong, so investor can raise equipment to increase their profits but get great

profits.

Net Present Value

This is another financial analysis strategy that is determined by using variance of current

cash inflow quality or current cash outflow price. NPV used in capital budgeting to plan

expenditure and to assess operational productivity (Okere and et.al, 2018). This technique is used

by Love-Well Limited management teams, and analyzes whether or not they must buy new

equipment. It measures as follows:

Formula:

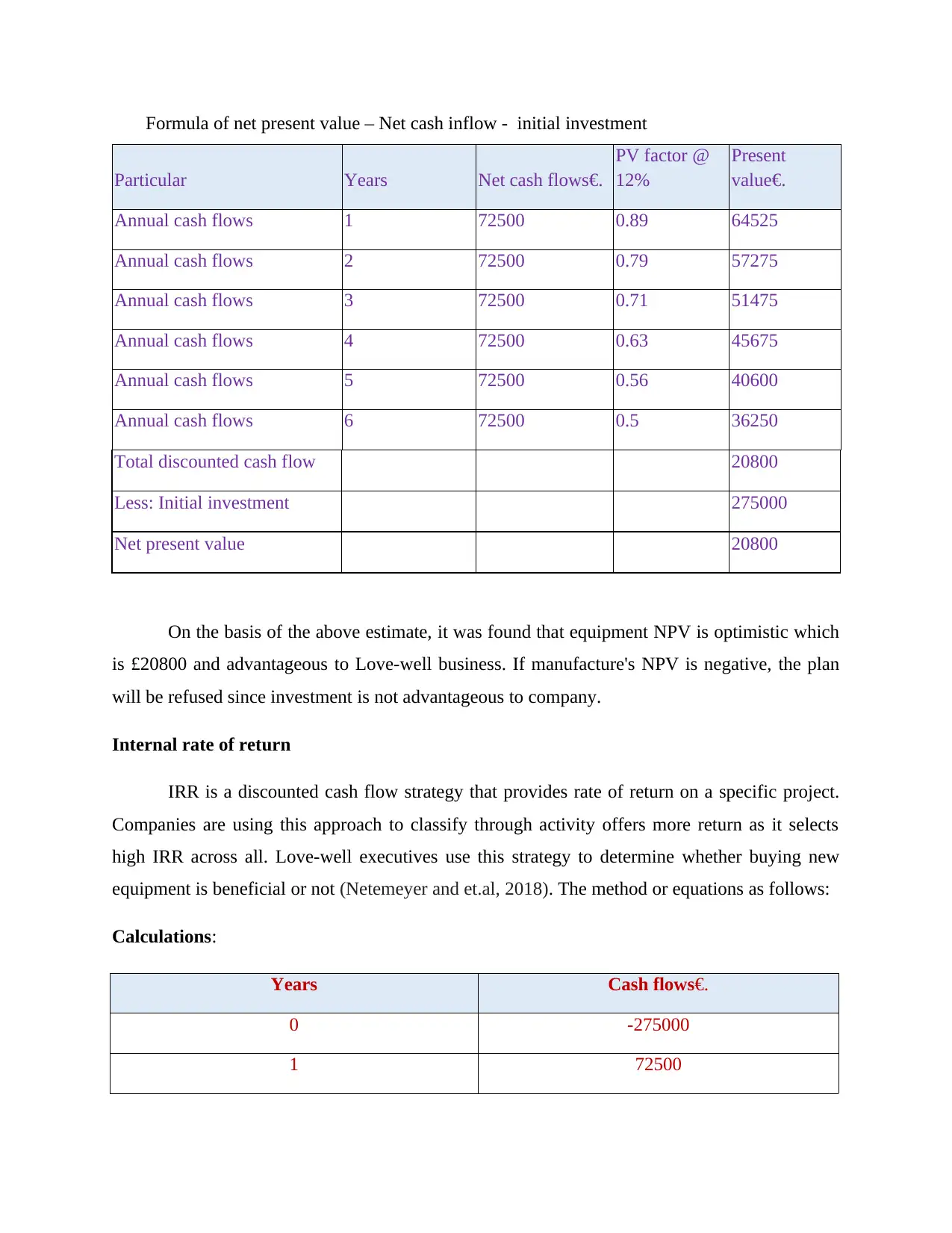

Formula of net present value – Net cash inflow - initial investment

Particular Years Net cash flows€.

PV factor @

12%

Present

value€.

Annual cash flows 1 72500 0.89 64525

Annual cash flows 2 72500 0.79 57275

Annual cash flows 3 72500 0.71 51475

Annual cash flows 4 72500 0.63 45675

Annual cash flows 5 72500 0.56 40600

Annual cash flows 6 72500 0.5 36250

Total discounted cash flow 20800

Less: Initial investment 275000

Net present value 20800

On the basis of the above estimate, it was found that equipment NPV is optimistic which

is £20800 and advantageous to Love-well business. If manufacture's NPV is negative, the plan

will be refused since investment is not advantageous to company.

Internal rate of return

IRR is a discounted cash flow strategy that provides rate of return on a specific project.

Companies are using this approach to classify through activity offers more return as it selects

high IRR across all. Love-well executives use this strategy to determine whether buying new

equipment is beneficial or not (Netemeyer and et.al, 2018). The method or equations as follows:

Calculations:

Years Cash flows€.

0 -275000

1 72500

Particular Years Net cash flows€.

PV factor @

12%

Present

value€.

Annual cash flows 1 72500 0.89 64525

Annual cash flows 2 72500 0.79 57275

Annual cash flows 3 72500 0.71 51475

Annual cash flows 4 72500 0.63 45675

Annual cash flows 5 72500 0.56 40600

Annual cash flows 6 72500 0.5 36250

Total discounted cash flow 20800

Less: Initial investment 275000

Net present value 20800

On the basis of the above estimate, it was found that equipment NPV is optimistic which

is £20800 and advantageous to Love-well business. If manufacture's NPV is negative, the plan

will be refused since investment is not advantageous to company.

Internal rate of return

IRR is a discounted cash flow strategy that provides rate of return on a specific project.

Companies are using this approach to classify through activity offers more return as it selects

high IRR across all. Love-well executives use this strategy to determine whether buying new

equipment is beneficial or not (Netemeyer and et.al, 2018). The method or equations as follows:

Calculations:

Years Cash flows€.

0 -275000

1 72500

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 18

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.