Financial Management: Cash Budget, NPV, and Payback Analysis

VerifiedAdded on 2022/08/21

|7

|878

|14

Homework Assignment

AI Summary

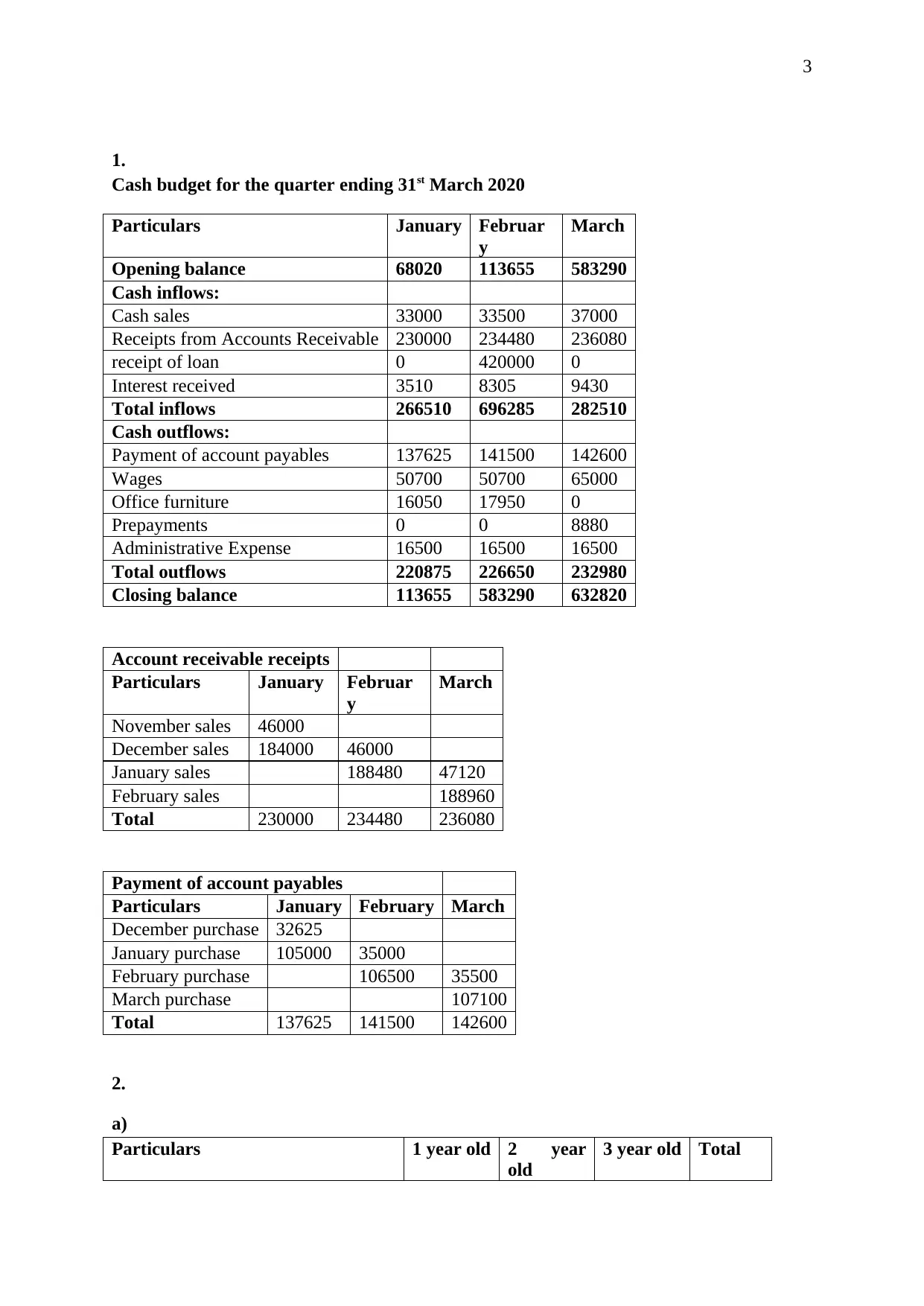

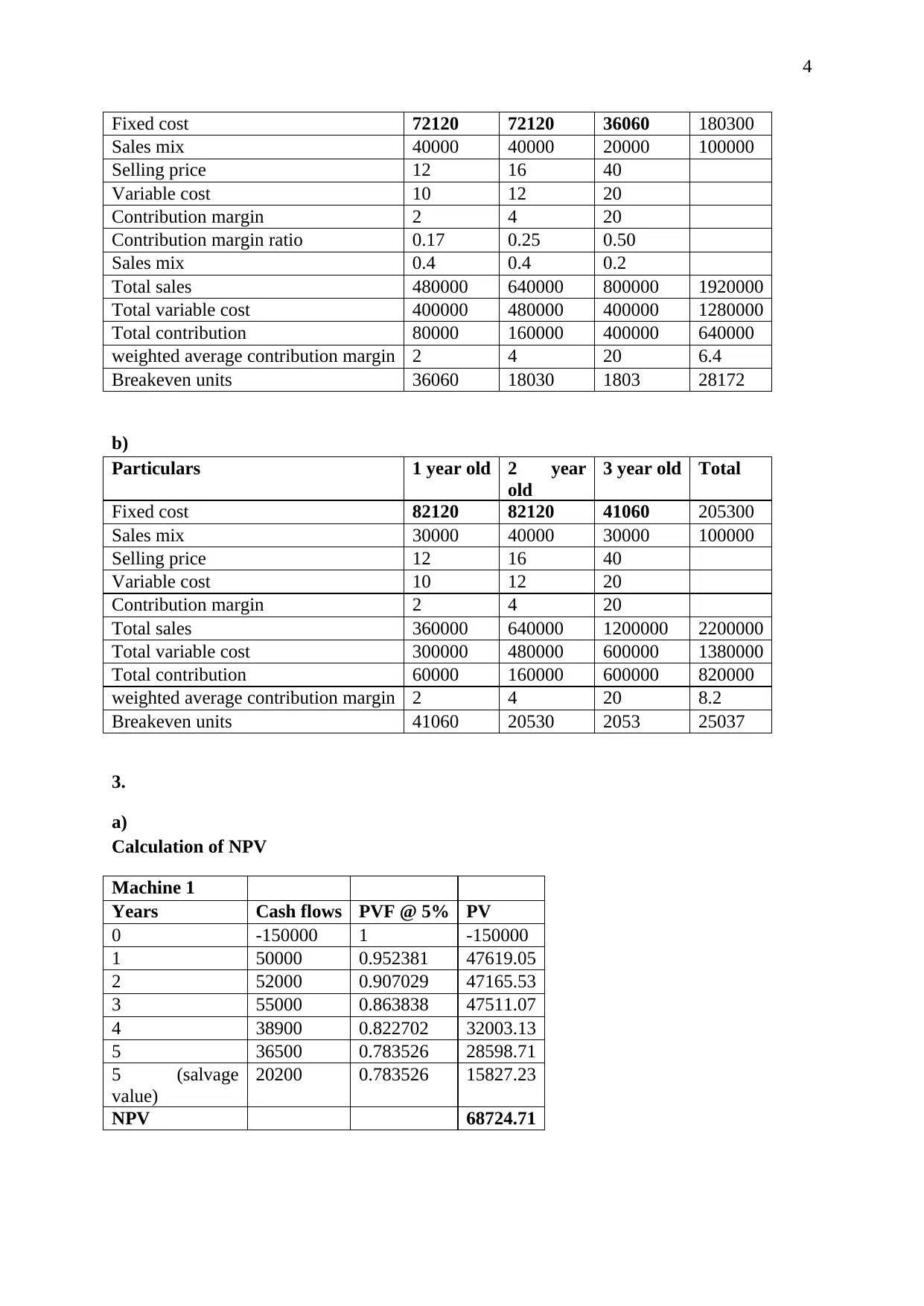

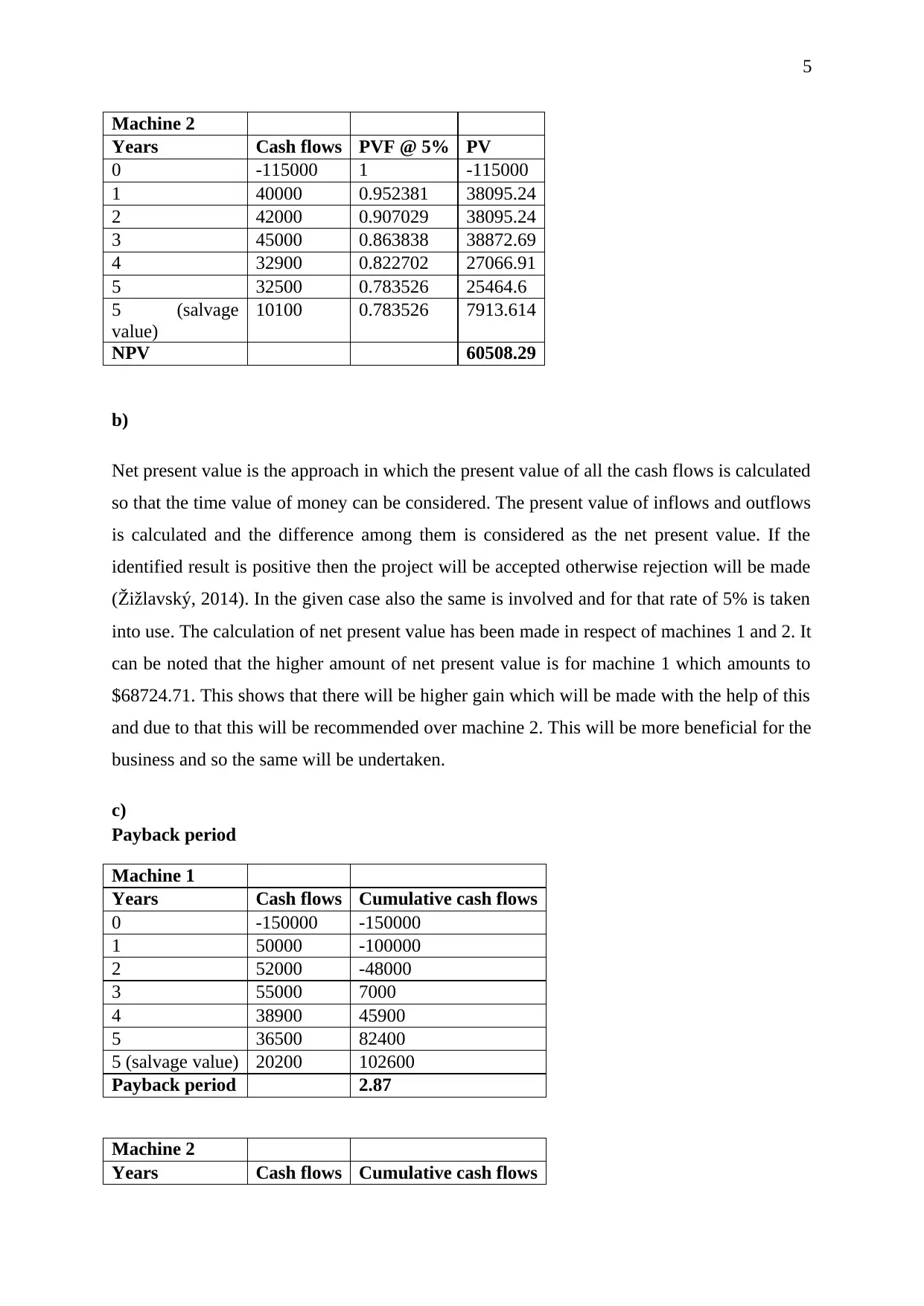

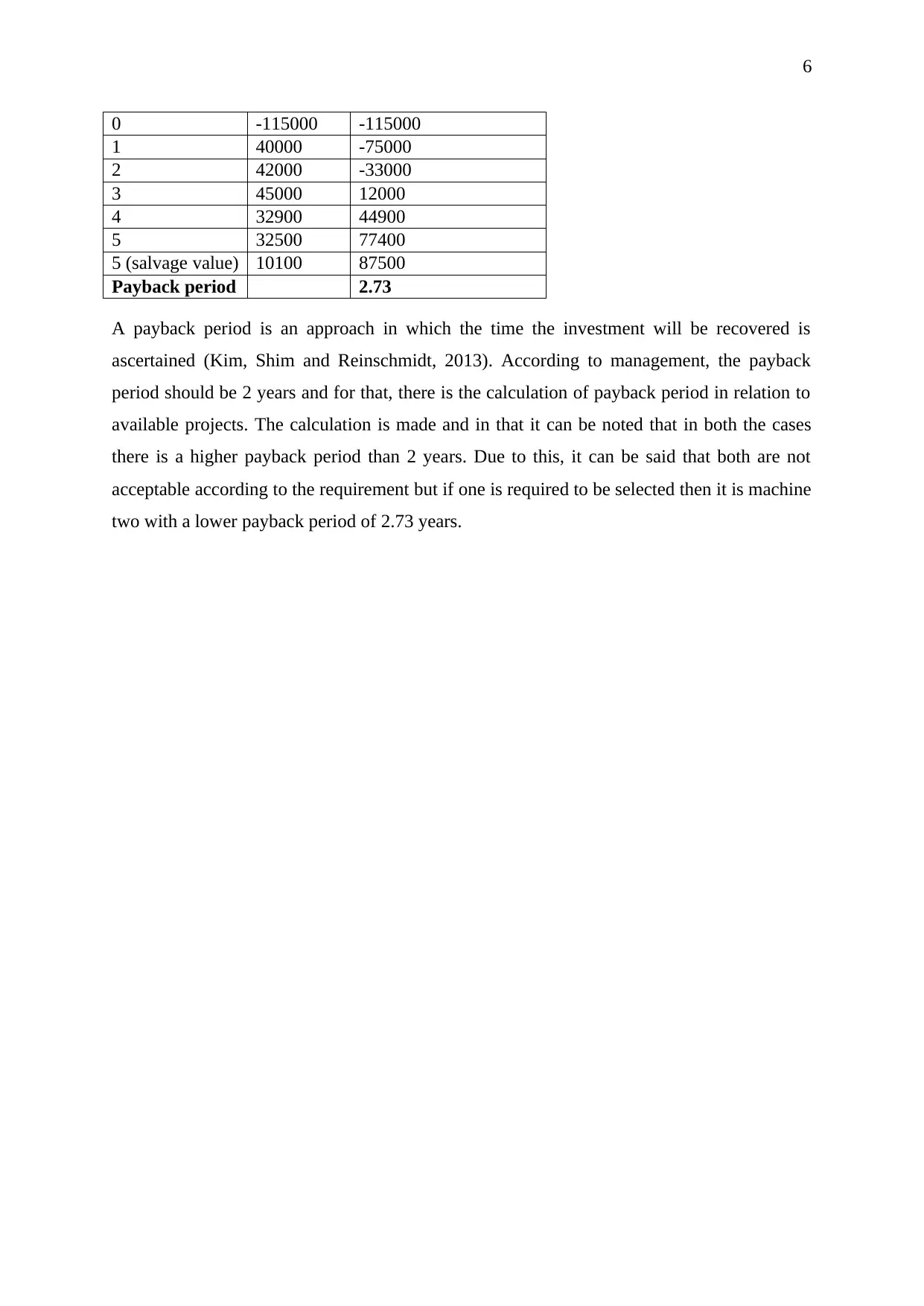

This document provides a comprehensive solution to a financial management assignment, demonstrating key concepts such as cash flow analysis, net present value (NPV), and payback period calculations. The assignment includes a detailed cash budget for the quarter ending March 31st, 2020, outlining cash inflows (cash sales, receipts from accounts receivable, receipt of loan, and interest received) and cash outflows (payment of accounts payables, wages, office furniture, prepayments, and administrative expenses). The document also analyzes the payment of accounts payables and account receivable receipts. Furthermore, the assignment explores breakeven analysis for different product scenarios, calculating fixed costs, sales mix, selling prices, variable costs, contribution margins, and breakeven units. Finally, the solution delves into investment appraisal, calculating the NPV and payback periods for two machines, considering cash flows, present values, and cumulative cash flows, and providing a recommendation based on the financial metrics. References to relevant academic sources are included.

1 out of 7

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.