Finance Assignment: Cost of Capital, Capital Budgeting, Risk & Return

VerifiedAdded on 2021/04/21

|13

|2405

|434

Homework Assignment

AI Summary

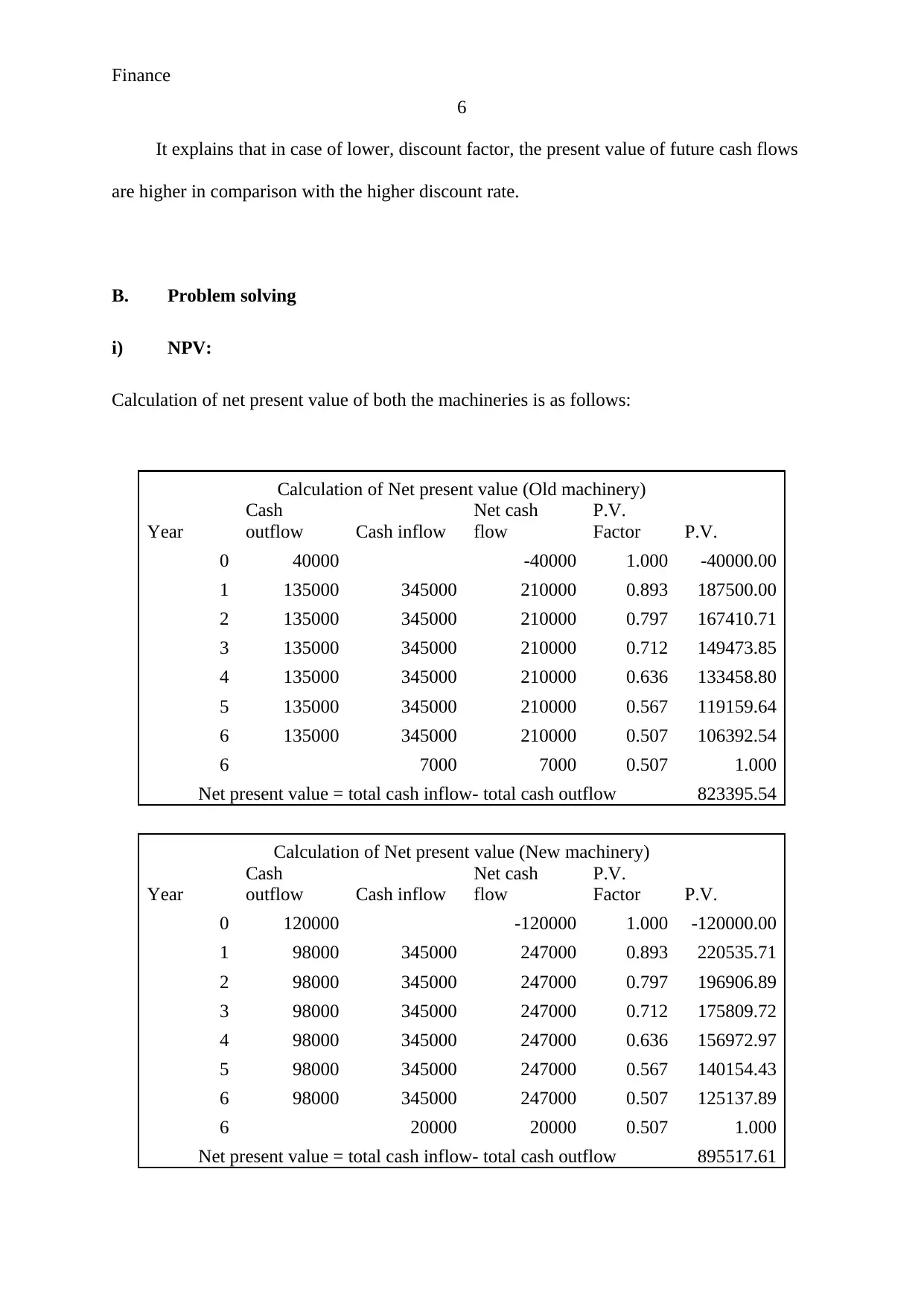

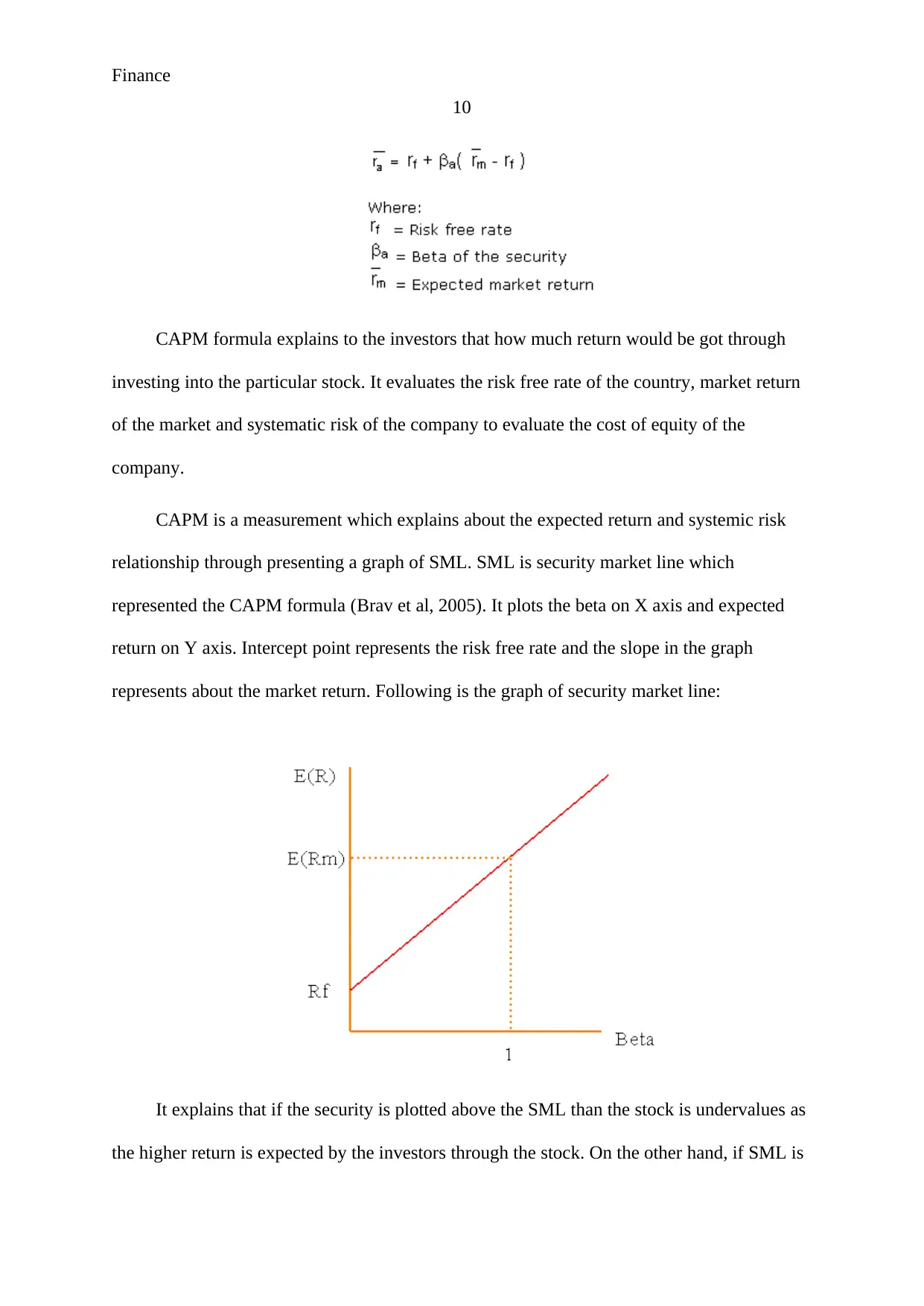

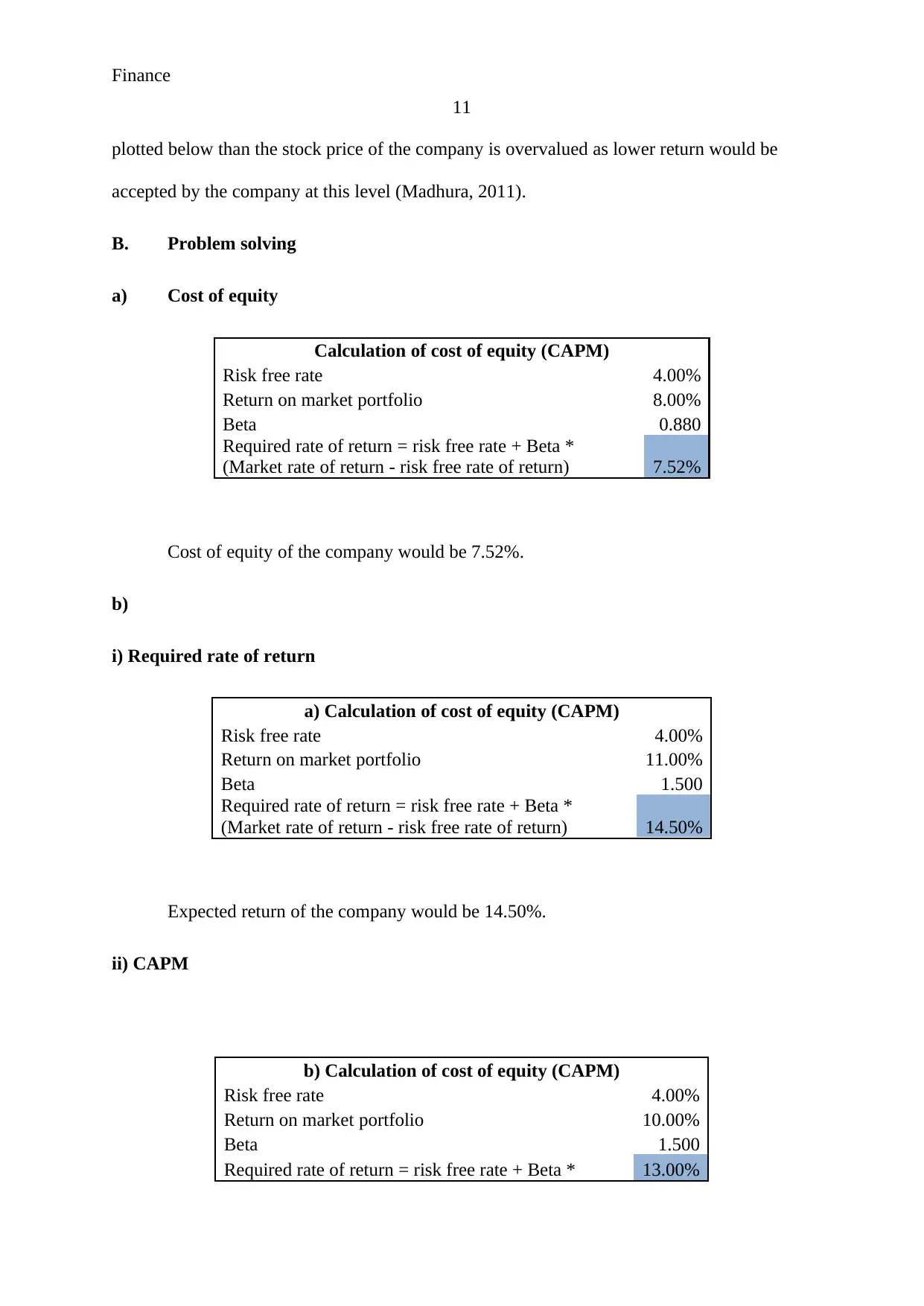

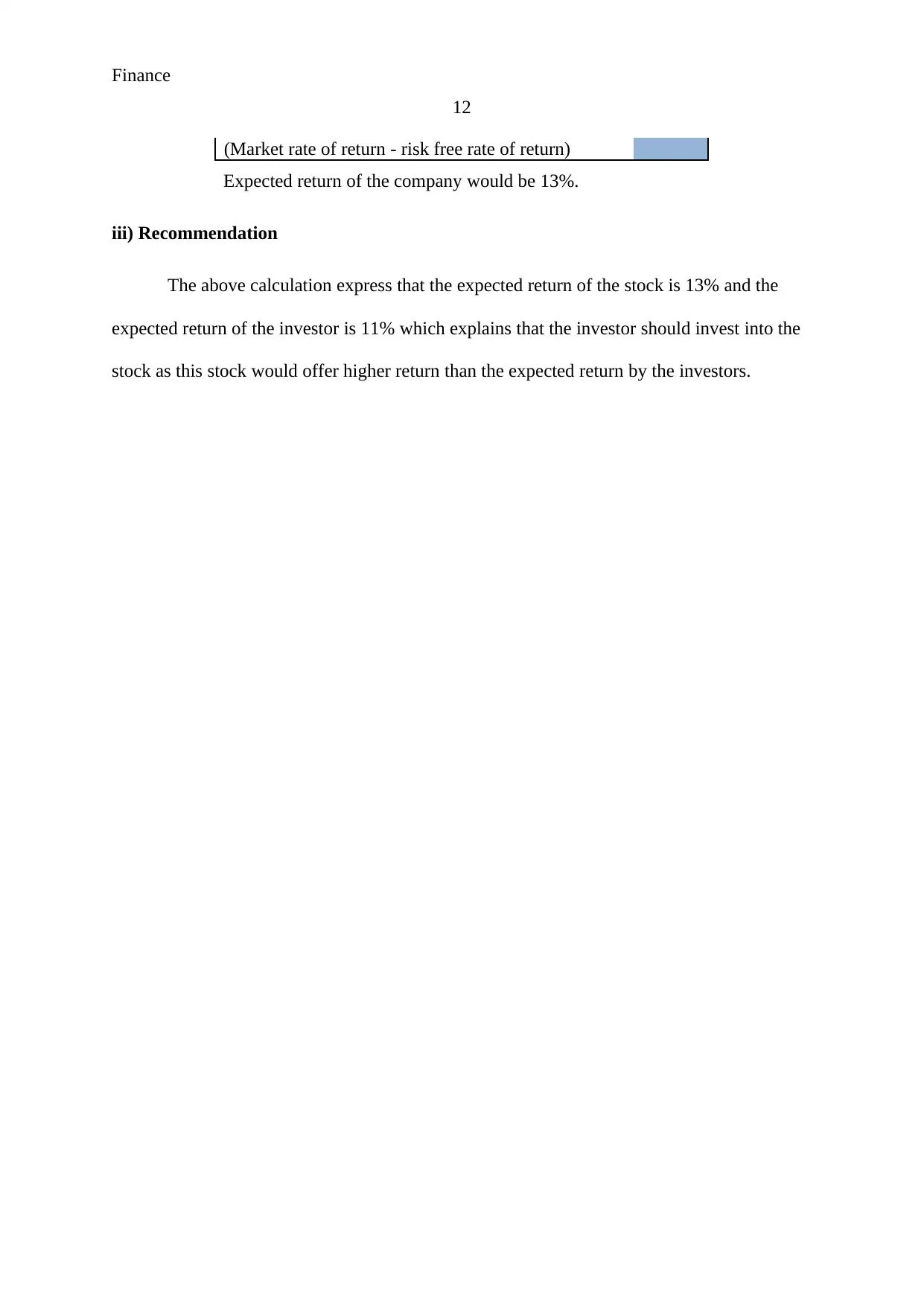

This assignment solution addresses key concepts in finance, including the cost of capital, capital budgeting, and risk and return analysis. The first section delves into capital structure, target capital structure, and the importance of evaluating the weighted average cost of capital (WACC) for different business units. It also provides a calculation of the cost of equity. The second section focuses on capital budgeting techniques, specifically the profitability index and net present value (NPV), with calculations for both. It analyzes how discount rates impact present values and discusses qualitative factors in machinery replacement decisions. The third section explores risk and return, differentiating between systematic and unsystematic risk and explaining the Capital Asset Pricing Model (CAPM). It includes calculations for the cost of equity using CAPM and provides investment recommendations based on expected returns. The assignment utilizes formulas, calculations, and theoretical explanations to provide a thorough understanding of financial management principles.

1 out of 13

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.