Financial Management: Project Evaluation, WACC, and Financing

VerifiedAdded on 2021/06/15

|9

|1728

|37

Homework Assignment

AI Summary

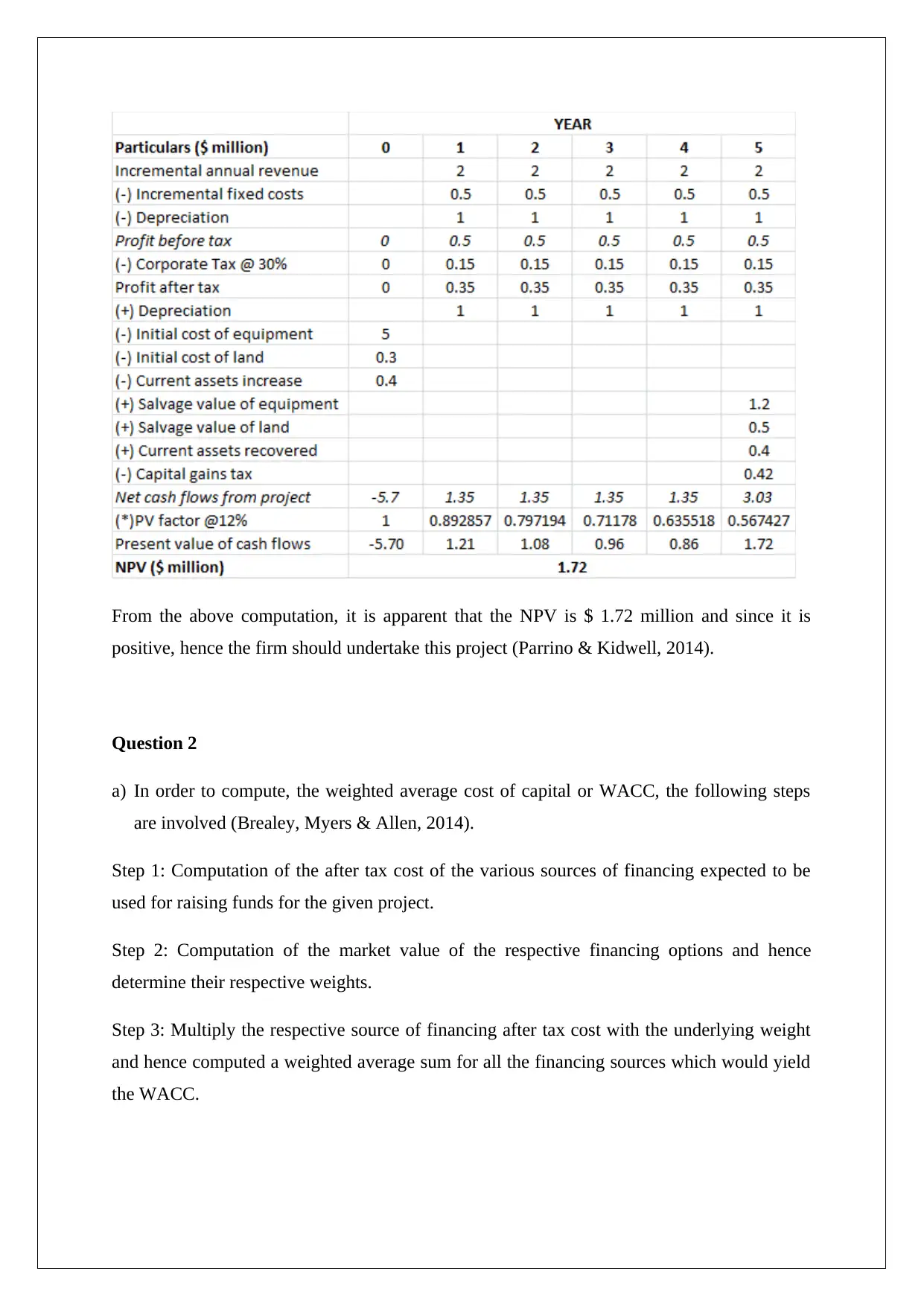

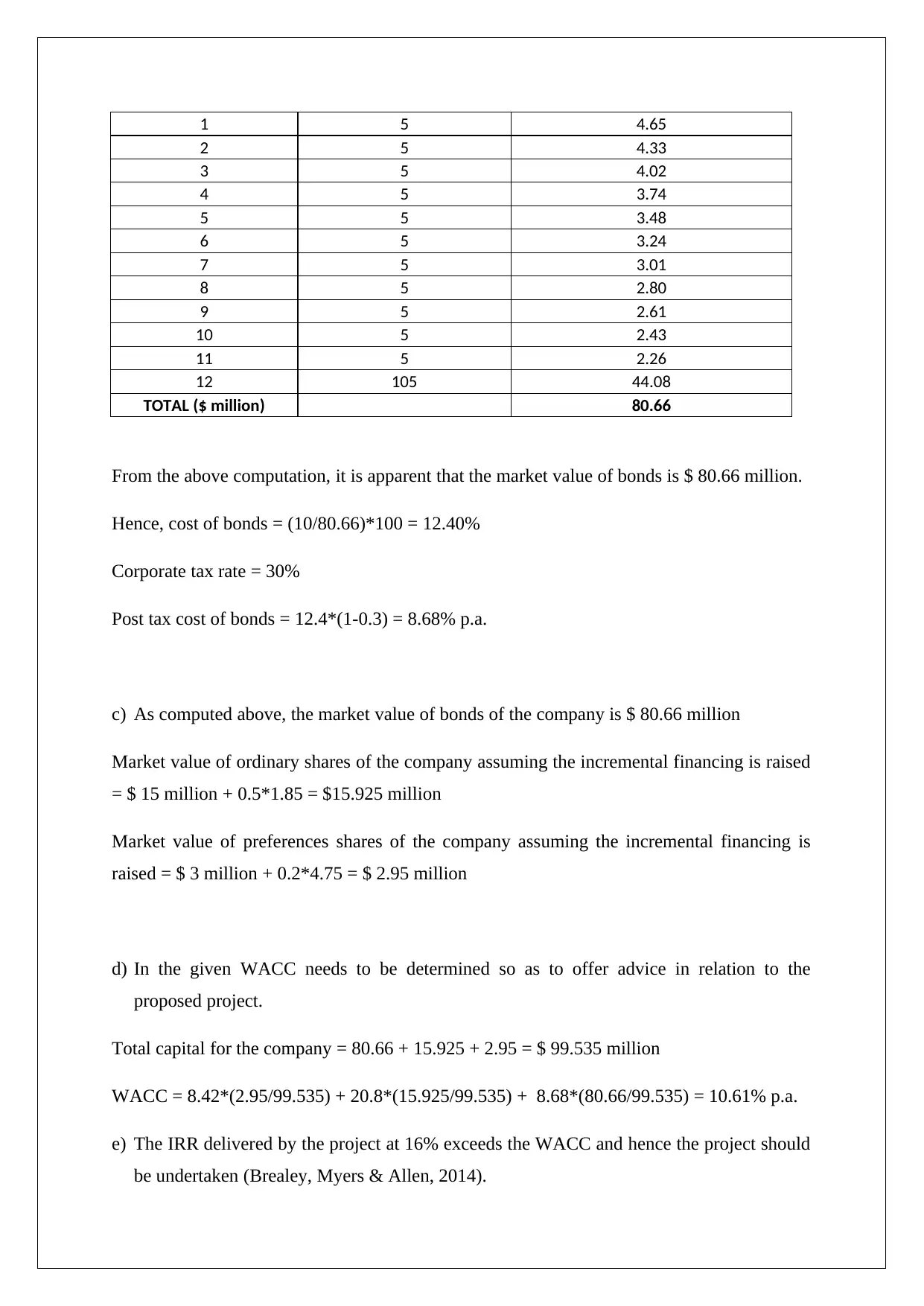

This financial management assignment addresses three key questions. The first involves a Net Present Value (NPV) analysis of a project, considering revenue, costs, initial investments, salvage values, depreciation, capital gains, and tax implications to determine project feasibility. The second question focuses on calculating the Weighted Average Cost of Capital (WACC), requiring the determination of after-tax costs for various financing sources (preference shares, ordinary shares using CAPM, and bonds) and their respective market values to arrive at the WACC. The final question explores factors a company should consider when selecting short-term financing, including the cost of financing, collateral requirements, and the overhead costs associated with raising funds, providing a comprehensive understanding of financial decision-making. The solution utilizes formulas and calculations to support the analysis and includes references from financial management textbooks.

1 out of 9

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.