Financial Management Assignment: APC308, 2020/21, Solution

VerifiedAdded on 2022/12/29

|14

|3671

|27

Homework Assignment

AI Summary

This document presents a detailed solution to a Financial Management assignment, addressing key concepts such as equity finance and investment appraisal techniques. The assignment begins with an introduction to financial management, highlighting its role in planning, organizing, and controlling financial resources to achieve organizational objectives. The first question delves into long-term finance, specifically equity finance, explaining the process of raising funds through the issuance of shares. It includes calculations for the number of shares to be issued, the theoretical ex-rights price, and expected earnings per share, along with an evaluation of different rights issue prices. The advantages of cash dividends versus script dividends for both companies and shareholders are also discussed. The second question focuses on investment appraisal techniques, including the payback period, average rate of return, net present value, and internal rate of return. It provides calculations for each method and offers recommendations on the economic feasibility of acquiring machines, evaluating the benefits and limitations of each technique. The solution provides a comprehensive overview of financial management principles and practical application, offering valuable insights for students studying finance.

Financial

Management

Management

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Long term finance: Equity finance:.............................................................................................3

Advantage for the companies shareholders choice between the cash dividend, an equivalent

script dividend:.............................................................................................................................5

QUESTION 2...................................................................................................................................6

a) Calculation for the investment appraisal techniques, brief recommendations as to the

economic feasibility of acquiring the machines:.........................................................................6

Evaluate the benefits and limitations for the different investment appraisal techniques:..........10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

INTRODUCTION...........................................................................................................................3

QUESTION 1...................................................................................................................................3

Long term finance: Equity finance:.............................................................................................3

Advantage for the companies shareholders choice between the cash dividend, an equivalent

script dividend:.............................................................................................................................5

QUESTION 2...................................................................................................................................6

a) Calculation for the investment appraisal techniques, brief recommendations as to the

economic feasibility of acquiring the machines:.........................................................................6

Evaluate the benefits and limitations for the different investment appraisal techniques:..........10

CONCLUSION..............................................................................................................................11

REFERENCES..............................................................................................................................13

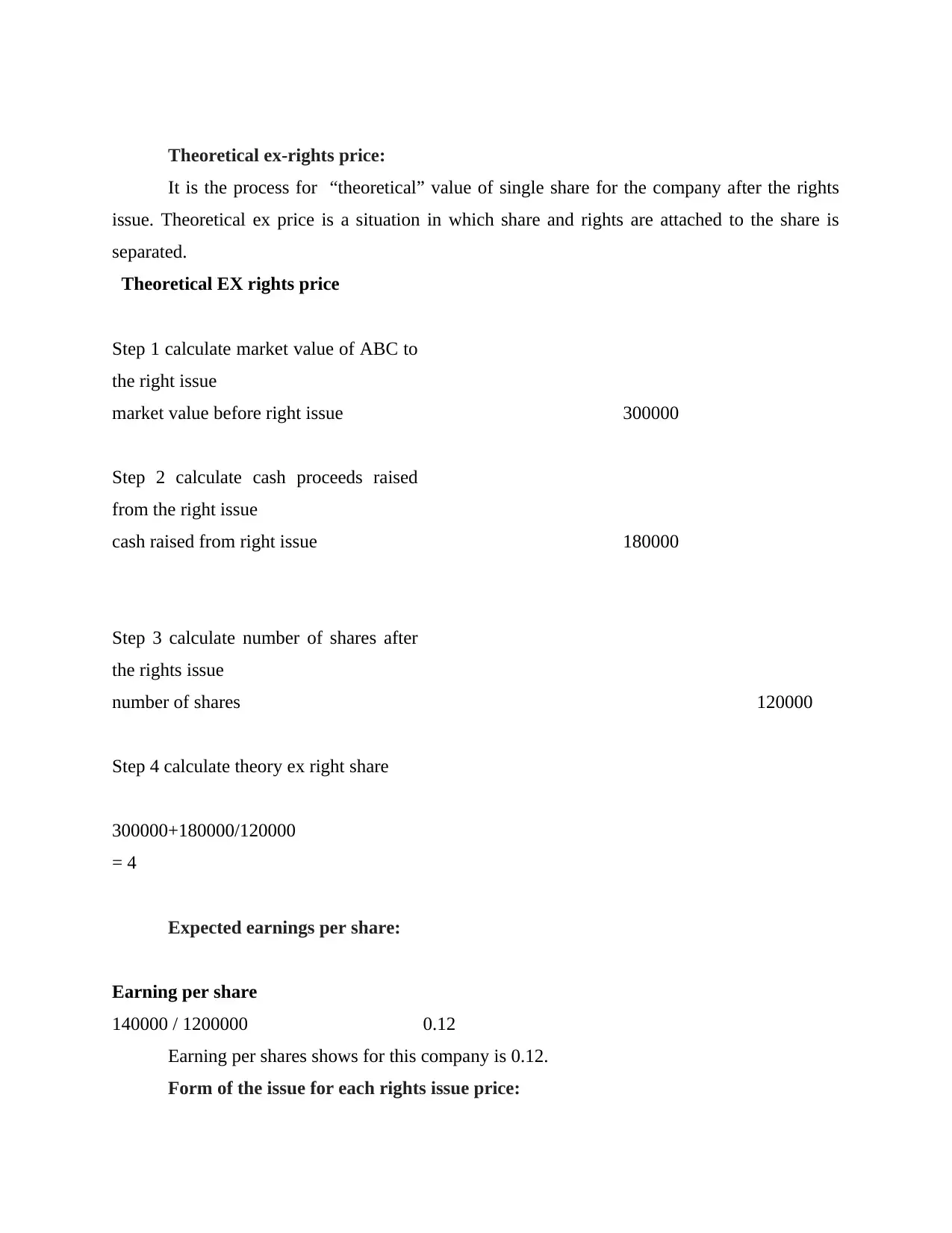

INTRODUCTION

Financial management is the process for planning, organising, managing, controlling,

budgeting financial resources in order to achieve organisations objectives. It defines as the

functions of organisation which are related to the profitability, expenses, cash credit etc. It refers

to the strategic planning, organising, directing financial activities for the organisations. Managers

prepares financial reports for the external parties which includes customers, shareholders etc.

financial management is all about planning, allocating, managing resources for the

organisations. Financial management is about acquiring, managing funds for the completing

financial needs for the organisation so that it can runs its activities (Shapiro and Hanouna, 2019).

It helps for financial decision making for the managers for taking efficient decisions. It means

applying general management rules for the financial resources of the organisations. Managers

making financial reports for the financial decision making they provides these information to

higher management so that they takes decisions regarding financial resources. This report is

based for financial resources, their techniques for managers decision making. This report covers

topics which includes equity finance, investment appraisal techniques etc.

QUESTION 1

Long term finance: Equity finance:

Equity finance: Equity finance is the process for raising funds by issuing shares for the

shareholders, financial institutions, investors. The persons who buy shares are known as

shareholders, they receives dividends for their funds. It is about sales for the shares in order to

raising funds for the companies. Equity finance takes place for when the owner of the company

sales their shares (Schill, 2017). The company gives dividends for shareholders as the interest for

their funds. Firms raising funds by issuing shares to the shareholders. This gives higher benefits

to the company for achieving money as it wants to expand its business. It helps firms for

acquiring funds which helps them for completing tasks which will gives higher profitability for

the company.

Number of shares to be issued:

Number of

shares

180000 /

0.25 720000

Financial management is the process for planning, organising, managing, controlling,

budgeting financial resources in order to achieve organisations objectives. It defines as the

functions of organisation which are related to the profitability, expenses, cash credit etc. It refers

to the strategic planning, organising, directing financial activities for the organisations. Managers

prepares financial reports for the external parties which includes customers, shareholders etc.

financial management is all about planning, allocating, managing resources for the

organisations. Financial management is about acquiring, managing funds for the completing

financial needs for the organisation so that it can runs its activities (Shapiro and Hanouna, 2019).

It helps for financial decision making for the managers for taking efficient decisions. It means

applying general management rules for the financial resources of the organisations. Managers

making financial reports for the financial decision making they provides these information to

higher management so that they takes decisions regarding financial resources. This report is

based for financial resources, their techniques for managers decision making. This report covers

topics which includes equity finance, investment appraisal techniques etc.

QUESTION 1

Long term finance: Equity finance:

Equity finance: Equity finance is the process for raising funds by issuing shares for the

shareholders, financial institutions, investors. The persons who buy shares are known as

shareholders, they receives dividends for their funds. It is about sales for the shares in order to

raising funds for the companies. Equity finance takes place for when the owner of the company

sales their shares (Schill, 2017). The company gives dividends for shareholders as the interest for

their funds. Firms raising funds by issuing shares to the shareholders. This gives higher benefits

to the company for achieving money as it wants to expand its business. It helps firms for

acquiring funds which helps them for completing tasks which will gives higher profitability for

the company.

Number of shares to be issued:

Number of

shares

180000 /

0.25 720000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Theoretical ex-rights price:

It is the process for “theoretical” value of single share for the company after the rights

issue. Theoretical ex price is a situation in which share and rights are attached to the share is

separated.

Theoretical EX rights price

Step 1 calculate market value of ABC to

the right issue

market value before right issue 300000

Step 2 calculate cash proceeds raised

from the right issue

cash raised from right issue 180000

Step 3 calculate number of shares after

the rights issue

number of shares 120000

Step 4 calculate theory ex right share

300000+180000/120000

= 4

Expected earnings per share:

Earning per share

140000 / 1200000 0.12

Earning per shares shows for this company is 0.12.

Form of the issue for each rights issue price:

It is the process for “theoretical” value of single share for the company after the rights

issue. Theoretical ex price is a situation in which share and rights are attached to the share is

separated.

Theoretical EX rights price

Step 1 calculate market value of ABC to

the right issue

market value before right issue 300000

Step 2 calculate cash proceeds raised

from the right issue

cash raised from right issue 180000

Step 3 calculate number of shares after

the rights issue

number of shares 120000

Step 4 calculate theory ex right share

300000+180000/120000

= 4

Expected earnings per share:

Earning per share

140000 / 1200000 0.12

Earning per shares shows for this company is 0.12.

Form of the issue for each rights issue price:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

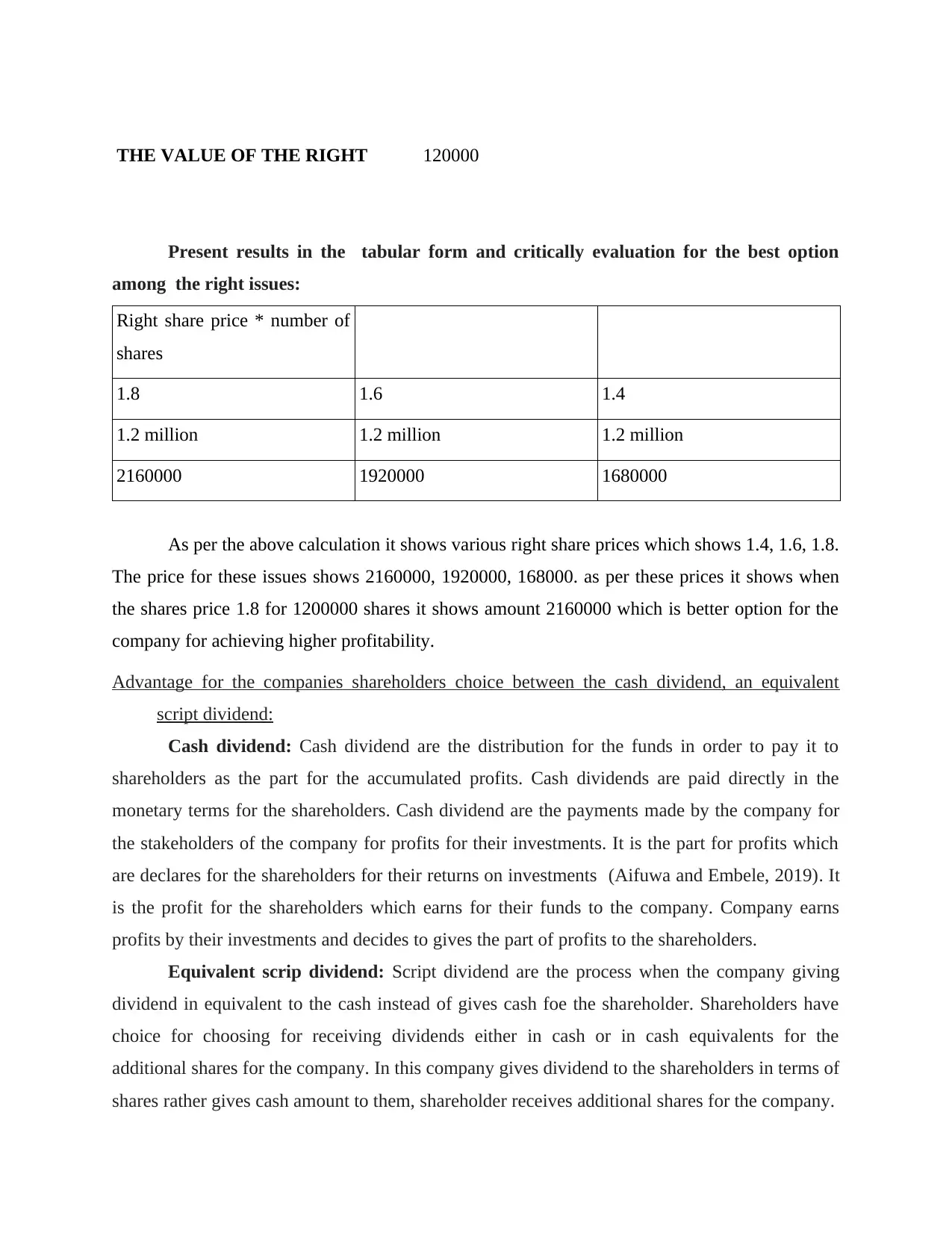

THE VALUE OF THE RIGHT 120000

Present results in the tabular form and critically evaluation for the best option

among the right issues:

Right share price * number of

shares

1.8 1.6 1.4

1.2 million 1.2 million 1.2 million

2160000 1920000 1680000

As per the above calculation it shows various right share prices which shows 1.4, 1.6, 1.8.

The price for these issues shows 2160000, 1920000, 168000. as per these prices it shows when

the shares price 1.8 for 1200000 shares it shows amount 2160000 which is better option for the

company for achieving higher profitability.

Advantage for the companies shareholders choice between the cash dividend, an equivalent

script dividend:

Cash dividend: Cash dividend are the distribution for the funds in order to pay it to

shareholders as the part for the accumulated profits. Cash dividends are paid directly in the

monetary terms for the shareholders. Cash dividend are the payments made by the company for

the stakeholders of the company for profits for their investments. It is the part for profits which

are declares for the shareholders for their returns on investments (Aifuwa and Embele, 2019). It

is the profit for the shareholders which earns for their funds to the company. Company earns

profits by their investments and decides to gives the part of profits to the shareholders.

Equivalent scrip dividend: Script dividend are the process when the company giving

dividend in equivalent to the cash instead of gives cash foe the shareholder. Shareholders have

choice for choosing for receiving dividends either in cash or in cash equivalents for the

additional shares for the company. In this company gives dividend to the shareholders in terms of

shares rather gives cash amount to them, shareholder receives additional shares for the company.

Present results in the tabular form and critically evaluation for the best option

among the right issues:

Right share price * number of

shares

1.8 1.6 1.4

1.2 million 1.2 million 1.2 million

2160000 1920000 1680000

As per the above calculation it shows various right share prices which shows 1.4, 1.6, 1.8.

The price for these issues shows 2160000, 1920000, 168000. as per these prices it shows when

the shares price 1.8 for 1200000 shares it shows amount 2160000 which is better option for the

company for achieving higher profitability.

Advantage for the companies shareholders choice between the cash dividend, an equivalent

script dividend:

Cash dividend: Cash dividend are the distribution for the funds in order to pay it to

shareholders as the part for the accumulated profits. Cash dividends are paid directly in the

monetary terms for the shareholders. Cash dividend are the payments made by the company for

the stakeholders of the company for profits for their investments. It is the part for profits which

are declares for the shareholders for their returns on investments (Aifuwa and Embele, 2019). It

is the profit for the shareholders which earns for their funds to the company. Company earns

profits by their investments and decides to gives the part of profits to the shareholders.

Equivalent scrip dividend: Script dividend are the process when the company giving

dividend in equivalent to the cash instead of gives cash foe the shareholder. Shareholders have

choice for choosing for receiving dividends either in cash or in cash equivalents for the

additional shares for the company. In this company gives dividend to the shareholders in terms of

shares rather gives cash amount to them, shareholder receives additional shares for the company.

Advantages for the scrip dividends: Scrip dividend are the dividends which helps

shareholders for the shareholding for the company. In this types of process shareholders purchase

shares without commission of broker. In this company provides dividend program for the

shareholders of the company for rights to take dividend in shares which increases shareholding

for that company. In this company has for issuing shares not in cash dividends. It provides better

way for financial constraints for the company. In this dividend shareholders has not pay to taxes

for shares value (Knight, 2017). Company receives money for investments in its activities by

issuing more shares for shareholders for the company.

For the company: The advantages for the company by the scrip dividend is it gives

investment money for the company by issuing shares to the shareholders. As it helps company

for expanding its business for the higher profitability (Mochkabadi and Volkmann, 2020). It is

better option for company as scrip dividend helps the company for cash saves. For every

shareholders which that elects shares it saves the company cash. The scrip dividend election

gives results which helps company for capital allocation decisions. In this company issuing

shares to shareholders as they see they are funding for the company's activities. The main thing is

the shareholders thinks that shares are attractive the company should too.

For the shareholders: The advantage for the shareholders for the company is

shareholders achieves higher dividend for their investments also more shareholding for the

company. Shareholders receives these shares for their dividend which gives higher profitability.

Its better for having choice as they takes better option for shareholders. Different shareholders

has various choices as investors who wants cash for paying its expenses they takes cash dividend

, who wants shares for their dividend they takes more shares for more shareholding for the

company. If the shares undervalued shareholders takes more shares. This gives better chance for

shareholders for acquiring funds (Ruggiero and Lehkonen, 2017).

QUESTION 2

a) Calculation for the investment appraisal techniques, brief recommendations as to the

economic feasibility of acquiring the machines:

Investment appraisal techniques are the process for finding better investment option from

more options it helps for choosing which option gives higher returns to the company for their

investments. There are various techniques for knowing which option is better for the company.

These techniques are payback period method, average rate of return method, internal rate of

shareholders for the shareholding for the company. In this types of process shareholders purchase

shares without commission of broker. In this company provides dividend program for the

shareholders of the company for rights to take dividend in shares which increases shareholding

for that company. In this company has for issuing shares not in cash dividends. It provides better

way for financial constraints for the company. In this dividend shareholders has not pay to taxes

for shares value (Knight, 2017). Company receives money for investments in its activities by

issuing more shares for shareholders for the company.

For the company: The advantages for the company by the scrip dividend is it gives

investment money for the company by issuing shares to the shareholders. As it helps company

for expanding its business for the higher profitability (Mochkabadi and Volkmann, 2020). It is

better option for company as scrip dividend helps the company for cash saves. For every

shareholders which that elects shares it saves the company cash. The scrip dividend election

gives results which helps company for capital allocation decisions. In this company issuing

shares to shareholders as they see they are funding for the company's activities. The main thing is

the shareholders thinks that shares are attractive the company should too.

For the shareholders: The advantage for the shareholders for the company is

shareholders achieves higher dividend for their investments also more shareholding for the

company. Shareholders receives these shares for their dividend which gives higher profitability.

Its better for having choice as they takes better option for shareholders. Different shareholders

has various choices as investors who wants cash for paying its expenses they takes cash dividend

, who wants shares for their dividend they takes more shares for more shareholding for the

company. If the shares undervalued shareholders takes more shares. This gives better chance for

shareholders for acquiring funds (Ruggiero and Lehkonen, 2017).

QUESTION 2

a) Calculation for the investment appraisal techniques, brief recommendations as to the

economic feasibility of acquiring the machines:

Investment appraisal techniques are the process for finding better investment option from

more options it helps for choosing which option gives higher returns to the company for their

investments. There are various techniques for knowing which option is better for the company.

These techniques are payback period method, average rate of return method, internal rate of

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

return method, net present value method etc. It helps company for choosing higher profitability

(Hunt and Terry, 2018).

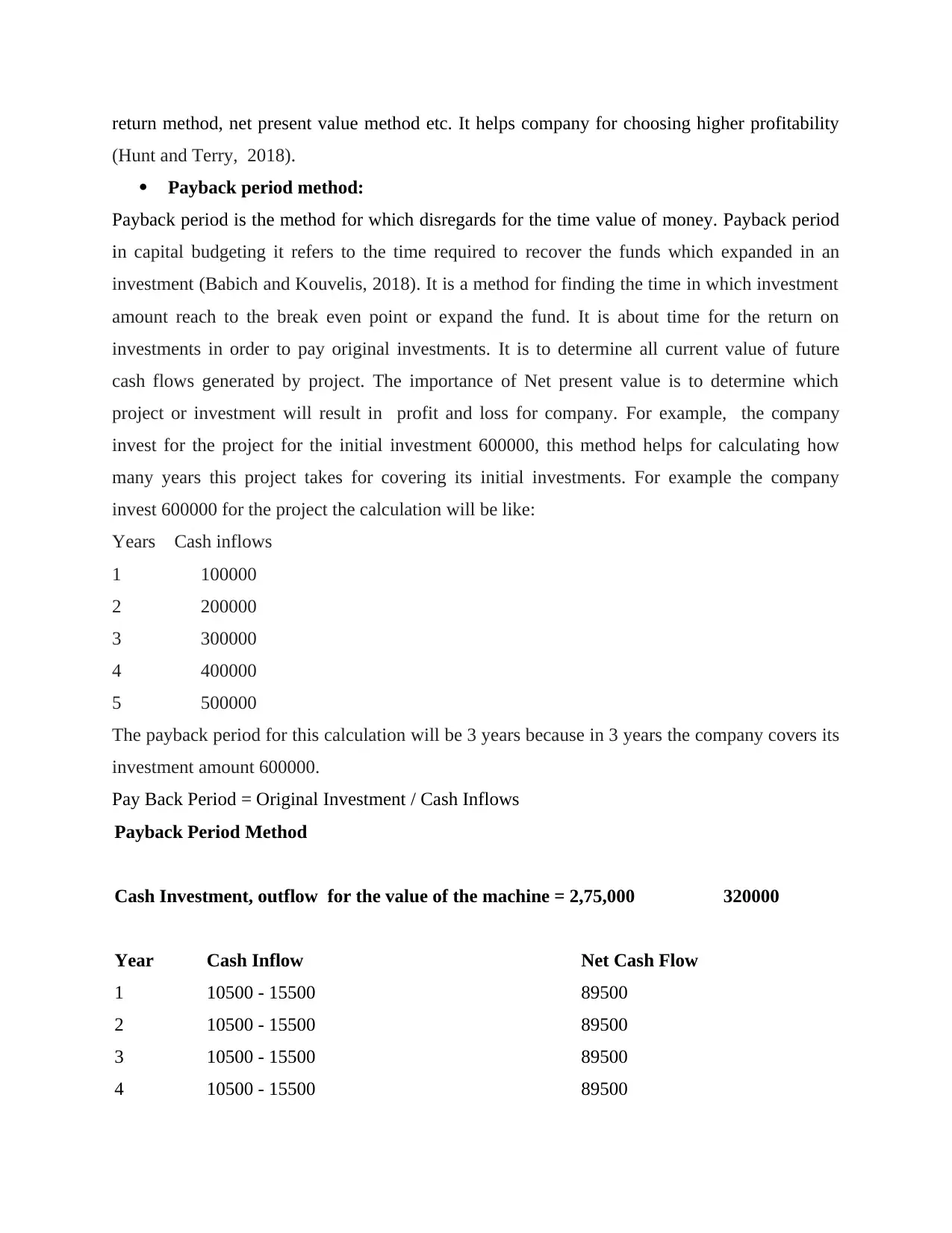

Payback period method:

Payback period is the method for which disregards for the time value of money. Payback period

in capital budgeting it refers to the time required to recover the funds which expanded in an

investment (Babich and Kouvelis, 2018). It is a method for finding the time in which investment

amount reach to the break even point or expand the fund. It is about time for the return on

investments in order to pay original investments. It is to determine all current value of future

cash flows generated by project. The importance of Net present value is to determine which

project or investment will result in profit and loss for company. For example, the company

invest for the project for the initial investment 600000, this method helps for calculating how

many years this project takes for covering its initial investments. For example the company

invest 600000 for the project the calculation will be like:

Years Cash inflows

1 100000

2 200000

3 300000

4 400000

5 500000

The payback period for this calculation will be 3 years because in 3 years the company covers its

investment amount 600000.

Pay Back Period = Original Investment / Cash Inflows

Payback Period Method

Cash Investment, outflow for the value of the machine = 2,75,000 320000

Year Cash Inflow Net Cash Flow

1 10500 - 15500 89500

2 10500 - 15500 89500

3 10500 - 15500 89500

4 10500 - 15500 89500

(Hunt and Terry, 2018).

Payback period method:

Payback period is the method for which disregards for the time value of money. Payback period

in capital budgeting it refers to the time required to recover the funds which expanded in an

investment (Babich and Kouvelis, 2018). It is a method for finding the time in which investment

amount reach to the break even point or expand the fund. It is about time for the return on

investments in order to pay original investments. It is to determine all current value of future

cash flows generated by project. The importance of Net present value is to determine which

project or investment will result in profit and loss for company. For example, the company

invest for the project for the initial investment 600000, this method helps for calculating how

many years this project takes for covering its initial investments. For example the company

invest 600000 for the project the calculation will be like:

Years Cash inflows

1 100000

2 200000

3 300000

4 400000

5 500000

The payback period for this calculation will be 3 years because in 3 years the company covers its

investment amount 600000.

Pay Back Period = Original Investment / Cash Inflows

Payback Period Method

Cash Investment, outflow for the value of the machine = 2,75,000 320000

Year Cash Inflow Net Cash Flow

1 10500 - 15500 89500

2 10500 - 15500 89500

3 10500 - 15500 89500

4 10500 - 15500 89500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

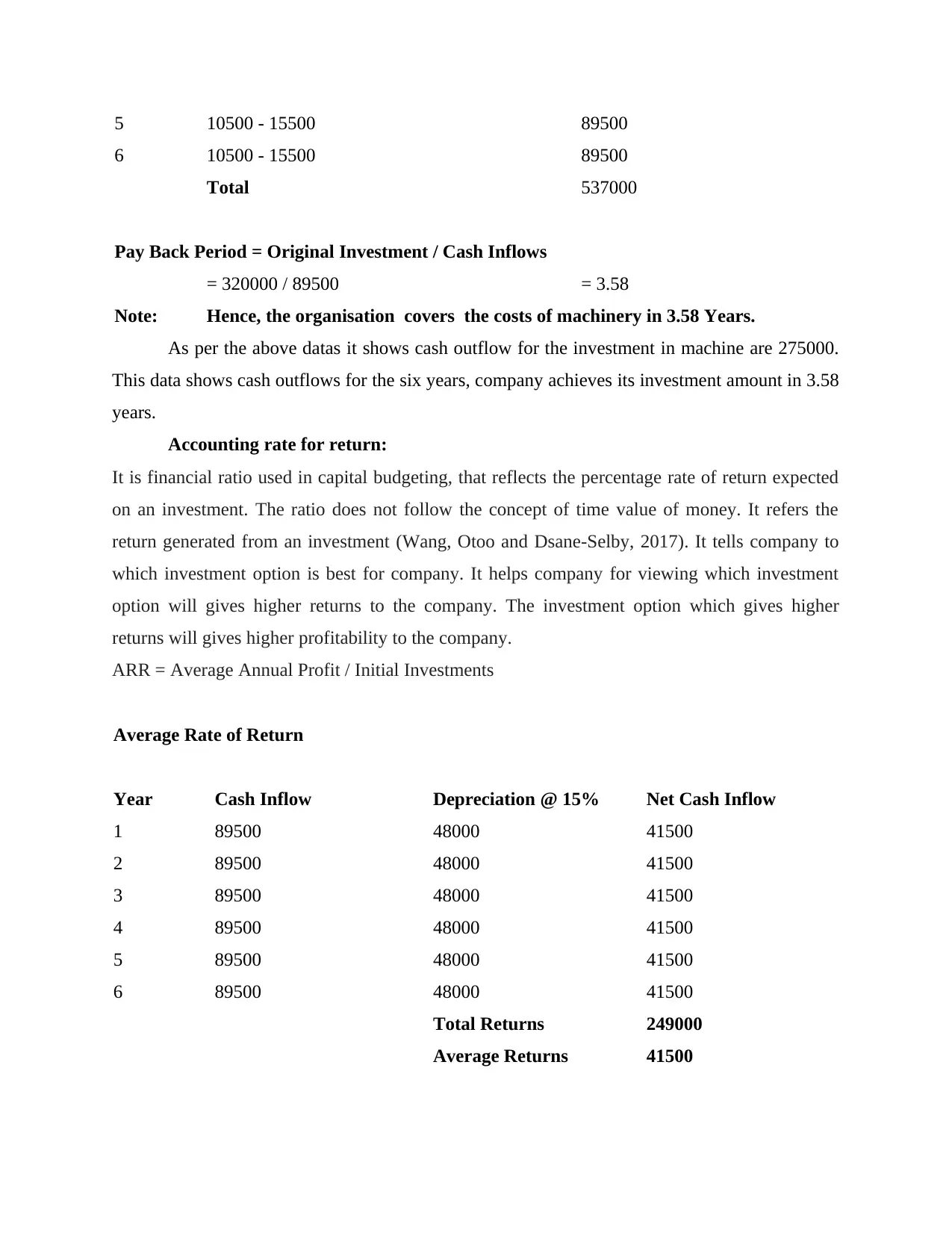

5 10500 - 15500 89500

6 10500 - 15500 89500

Total 537000

Pay Back Period = Original Investment / Cash Inflows

= 320000 / 89500 = 3.58

Note: Hence, the organisation covers the costs of machinery in 3.58 Years.

As per the above datas it shows cash outflow for the investment in machine are 275000.

This data shows cash outflows for the six years, company achieves its investment amount in 3.58

years.

Accounting rate for return:

It is financial ratio used in capital budgeting, that reflects the percentage rate of return expected

on an investment. The ratio does not follow the concept of time value of money. It refers the

return generated from an investment (Wang, Otoo and Dsane-Selby, 2017). It tells company to

which investment option is best for company. It helps company for viewing which investment

option will gives higher returns to the company. The investment option which gives higher

returns will gives higher profitability to the company.

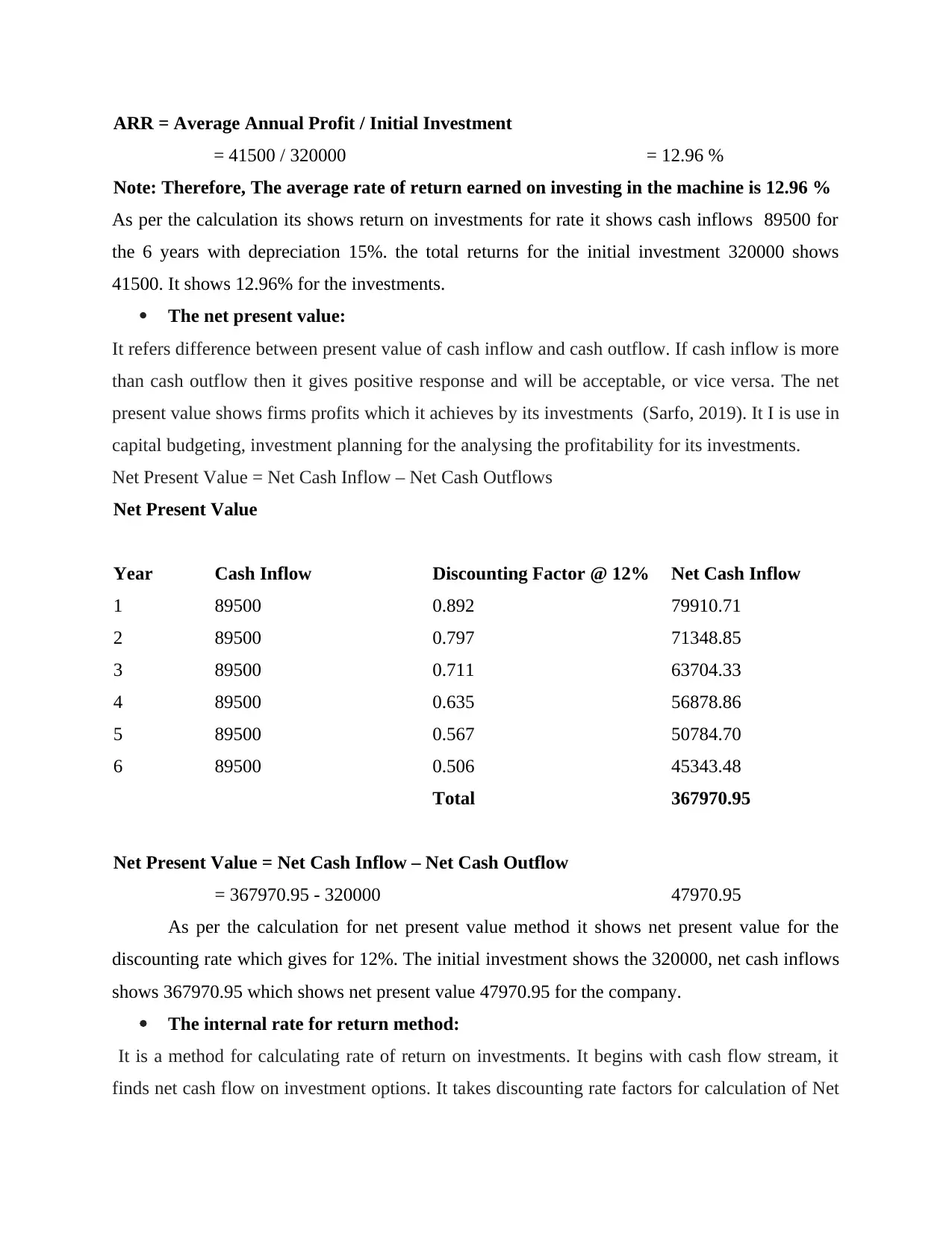

ARR = Average Annual Profit / Initial Investments

Average Rate of Return

Year Cash Inflow Depreciation @ 15% Net Cash Inflow

1 89500 48000 41500

2 89500 48000 41500

3 89500 48000 41500

4 89500 48000 41500

5 89500 48000 41500

6 89500 48000 41500

Total Returns 249000

Average Returns 41500

6 10500 - 15500 89500

Total 537000

Pay Back Period = Original Investment / Cash Inflows

= 320000 / 89500 = 3.58

Note: Hence, the organisation covers the costs of machinery in 3.58 Years.

As per the above datas it shows cash outflow for the investment in machine are 275000.

This data shows cash outflows for the six years, company achieves its investment amount in 3.58

years.

Accounting rate for return:

It is financial ratio used in capital budgeting, that reflects the percentage rate of return expected

on an investment. The ratio does not follow the concept of time value of money. It refers the

return generated from an investment (Wang, Otoo and Dsane-Selby, 2017). It tells company to

which investment option is best for company. It helps company for viewing which investment

option will gives higher returns to the company. The investment option which gives higher

returns will gives higher profitability to the company.

ARR = Average Annual Profit / Initial Investments

Average Rate of Return

Year Cash Inflow Depreciation @ 15% Net Cash Inflow

1 89500 48000 41500

2 89500 48000 41500

3 89500 48000 41500

4 89500 48000 41500

5 89500 48000 41500

6 89500 48000 41500

Total Returns 249000

Average Returns 41500

ARR = Average Annual Profit / Initial Investment

= 41500 / 320000 = 12.96 %

Note: Therefore, The average rate of return earned on investing in the machine is 12.96 %

As per the calculation its shows return on investments for rate it shows cash inflows 89500 for

the 6 years with depreciation 15%. the total returns for the initial investment 320000 shows

41500. It shows 12.96% for the investments.

The net present value:

It refers difference between present value of cash inflow and cash outflow. If cash inflow is more

than cash outflow then it gives positive response and will be acceptable, or vice versa. The net

present value shows firms profits which it achieves by its investments (Sarfo, 2019). It I is use in

capital budgeting, investment planning for the analysing the profitability for its investments.

Net Present Value = Net Cash Inflow – Net Cash Outflows

Net Present Value

Year Cash Inflow Discounting Factor @ 12% Net Cash Inflow

1 89500 0.892 79910.71

2 89500 0.797 71348.85

3 89500 0.711 63704.33

4 89500 0.635 56878.86

5 89500 0.567 50784.70

6 89500 0.506 45343.48

Total 367970.95

Net Present Value = Net Cash Inflow – Net Cash Outflow

= 367970.95 - 320000 47970.95

As per the calculation for net present value method it shows net present value for the

discounting rate which gives for 12%. The initial investment shows the 320000, net cash inflows

shows 367970.95 which shows net present value 47970.95 for the company.

The internal rate for return method:

It is a method for calculating rate of return on investments. It begins with cash flow stream, it

finds net cash flow on investment options. It takes discounting rate factors for calculation of Net

= 41500 / 320000 = 12.96 %

Note: Therefore, The average rate of return earned on investing in the machine is 12.96 %

As per the calculation its shows return on investments for rate it shows cash inflows 89500 for

the 6 years with depreciation 15%. the total returns for the initial investment 320000 shows

41500. It shows 12.96% for the investments.

The net present value:

It refers difference between present value of cash inflow and cash outflow. If cash inflow is more

than cash outflow then it gives positive response and will be acceptable, or vice versa. The net

present value shows firms profits which it achieves by its investments (Sarfo, 2019). It I is use in

capital budgeting, investment planning for the analysing the profitability for its investments.

Net Present Value = Net Cash Inflow – Net Cash Outflows

Net Present Value

Year Cash Inflow Discounting Factor @ 12% Net Cash Inflow

1 89500 0.892 79910.71

2 89500 0.797 71348.85

3 89500 0.711 63704.33

4 89500 0.635 56878.86

5 89500 0.567 50784.70

6 89500 0.506 45343.48

Total 367970.95

Net Present Value = Net Cash Inflow – Net Cash Outflow

= 367970.95 - 320000 47970.95

As per the calculation for net present value method it shows net present value for the

discounting rate which gives for 12%. The initial investment shows the 320000, net cash inflows

shows 367970.95 which shows net present value 47970.95 for the company.

The internal rate for return method:

It is a method for calculating rate of return on investments. It begins with cash flow stream, it

finds net cash flow on investment options. It takes discounting rate factors for calculation of Net

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

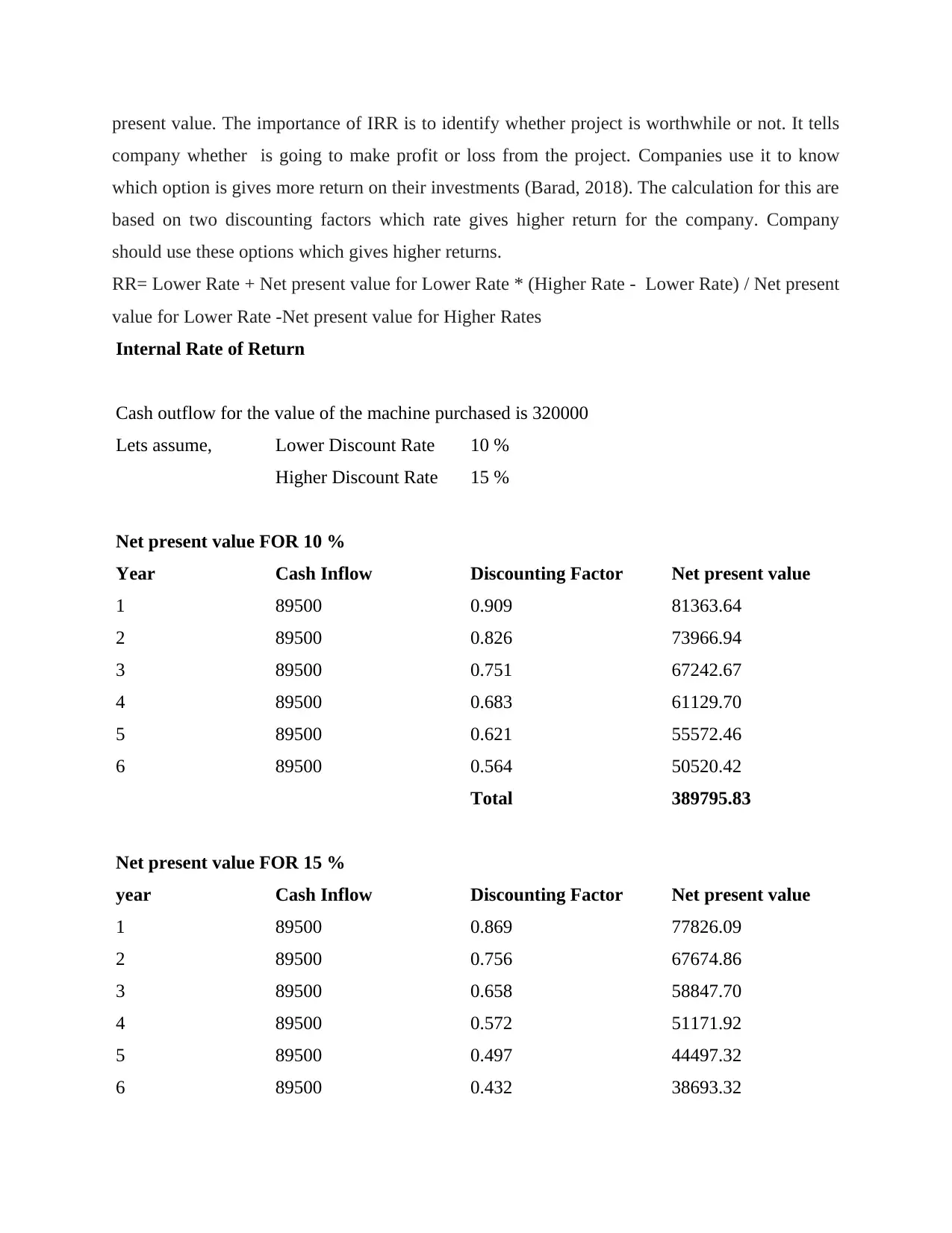

present value. The importance of IRR is to identify whether project is worthwhile or not. It tells

company whether is going to make profit or loss from the project. Companies use it to know

which option is gives more return on their investments (Barad, 2018). The calculation for this are

based on two discounting factors which rate gives higher return for the company. Company

should use these options which gives higher returns.

RR= Lower Rate + Net present value for Lower Rate * (Higher Rate - Lower Rate) / Net present

value for Lower Rate -Net present value for Higher Rates

Internal Rate of Return

Cash outflow for the value of the machine purchased is 320000

Lets assume, Lower Discount Rate 10 %

Higher Discount Rate 15 %

Net present value FOR 10 %

Year Cash Inflow Discounting Factor Net present value

1 89500 0.909 81363.64

2 89500 0.826 73966.94

3 89500 0.751 67242.67

4 89500 0.683 61129.70

5 89500 0.621 55572.46

6 89500 0.564 50520.42

Total 389795.83

Net present value FOR 15 %

year Cash Inflow Discounting Factor Net present value

1 89500 0.869 77826.09

2 89500 0.756 67674.86

3 89500 0.658 58847.70

4 89500 0.572 51171.92

5 89500 0.497 44497.32

6 89500 0.432 38693.32

company whether is going to make profit or loss from the project. Companies use it to know

which option is gives more return on their investments (Barad, 2018). The calculation for this are

based on two discounting factors which rate gives higher return for the company. Company

should use these options which gives higher returns.

RR= Lower Rate + Net present value for Lower Rate * (Higher Rate - Lower Rate) / Net present

value for Lower Rate -Net present value for Higher Rates

Internal Rate of Return

Cash outflow for the value of the machine purchased is 320000

Lets assume, Lower Discount Rate 10 %

Higher Discount Rate 15 %

Net present value FOR 10 %

Year Cash Inflow Discounting Factor Net present value

1 89500 0.909 81363.64

2 89500 0.826 73966.94

3 89500 0.751 67242.67

4 89500 0.683 61129.70

5 89500 0.621 55572.46

6 89500 0.564 50520.42

Total 389795.83

Net present value FOR 15 %

year Cash Inflow Discounting Factor Net present value

1 89500 0.869 77826.09

2 89500 0.756 67674.86

3 89500 0.658 58847.70

4 89500 0.572 51171.92

5 89500 0.497 44497.32

6 89500 0.432 38693.32

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

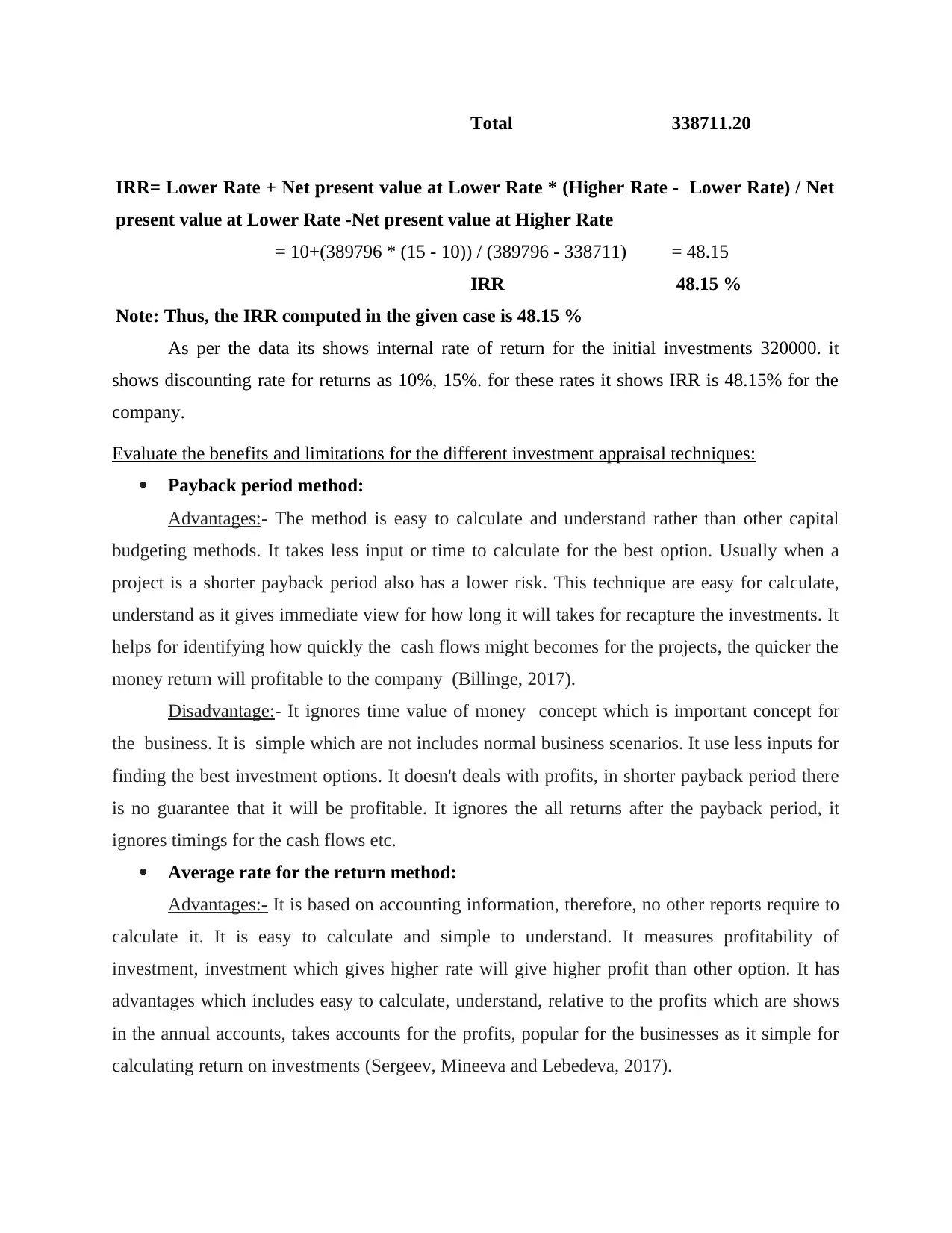

Total 338711.20

IRR= Lower Rate + Net present value at Lower Rate * (Higher Rate - Lower Rate) / Net

present value at Lower Rate -Net present value at Higher Rate

= 10+(389796 * (15 - 10)) / (389796 - 338711) = 48.15

IRR 48.15 %

Note: Thus, the IRR computed in the given case is 48.15 %

As per the data its shows internal rate of return for the initial investments 320000. it

shows discounting rate for returns as 10%, 15%. for these rates it shows IRR is 48.15% for the

company.

Evaluate the benefits and limitations for the different investment appraisal techniques:

Payback period method:

Advantages:- The method is easy to calculate and understand rather than other capital

budgeting methods. It takes less input or time to calculate for the best option. Usually when a

project is a shorter payback period also has a lower risk. This technique are easy for calculate,

understand as it gives immediate view for how long it will takes for recapture the investments. It

helps for identifying how quickly the cash flows might becomes for the projects, the quicker the

money return will profitable to the company (Billinge, 2017).

Disadvantage:- It ignores time value of money concept which is important concept for

the business. It is simple which are not includes normal business scenarios. It use less inputs for

finding the best investment options. It doesn't deals with profits, in shorter payback period there

is no guarantee that it will be profitable. It ignores the all returns after the payback period, it

ignores timings for the cash flows etc.

Average rate for the return method:

Advantages:- It is based on accounting information, therefore, no other reports require to

calculate it. It is easy to calculate and simple to understand. It measures profitability of

investment, investment which gives higher rate will give higher profit than other option. It has

advantages which includes easy to calculate, understand, relative to the profits which are shows

in the annual accounts, takes accounts for the profits, popular for the businesses as it simple for

calculating return on investments (Sergeev, Mineeva and Lebedeva, 2017).

IRR= Lower Rate + Net present value at Lower Rate * (Higher Rate - Lower Rate) / Net

present value at Lower Rate -Net present value at Higher Rate

= 10+(389796 * (15 - 10)) / (389796 - 338711) = 48.15

IRR 48.15 %

Note: Thus, the IRR computed in the given case is 48.15 %

As per the data its shows internal rate of return for the initial investments 320000. it

shows discounting rate for returns as 10%, 15%. for these rates it shows IRR is 48.15% for the

company.

Evaluate the benefits and limitations for the different investment appraisal techniques:

Payback period method:

Advantages:- The method is easy to calculate and understand rather than other capital

budgeting methods. It takes less input or time to calculate for the best option. Usually when a

project is a shorter payback period also has a lower risk. This technique are easy for calculate,

understand as it gives immediate view for how long it will takes for recapture the investments. It

helps for identifying how quickly the cash flows might becomes for the projects, the quicker the

money return will profitable to the company (Billinge, 2017).

Disadvantage:- It ignores time value of money concept which is important concept for

the business. It is simple which are not includes normal business scenarios. It use less inputs for

finding the best investment options. It doesn't deals with profits, in shorter payback period there

is no guarantee that it will be profitable. It ignores the all returns after the payback period, it

ignores timings for the cash flows etc.

Average rate for the return method:

Advantages:- It is based on accounting information, therefore, no other reports require to

calculate it. It is easy to calculate and simple to understand. It measures profitability of

investment, investment which gives higher rate will give higher profit than other option. It has

advantages which includes easy to calculate, understand, relative to the profits which are shows

in the annual accounts, takes accounts for the profits, popular for the businesses as it simple for

calculating return on investments (Sergeev, Mineeva and Lebedeva, 2017).

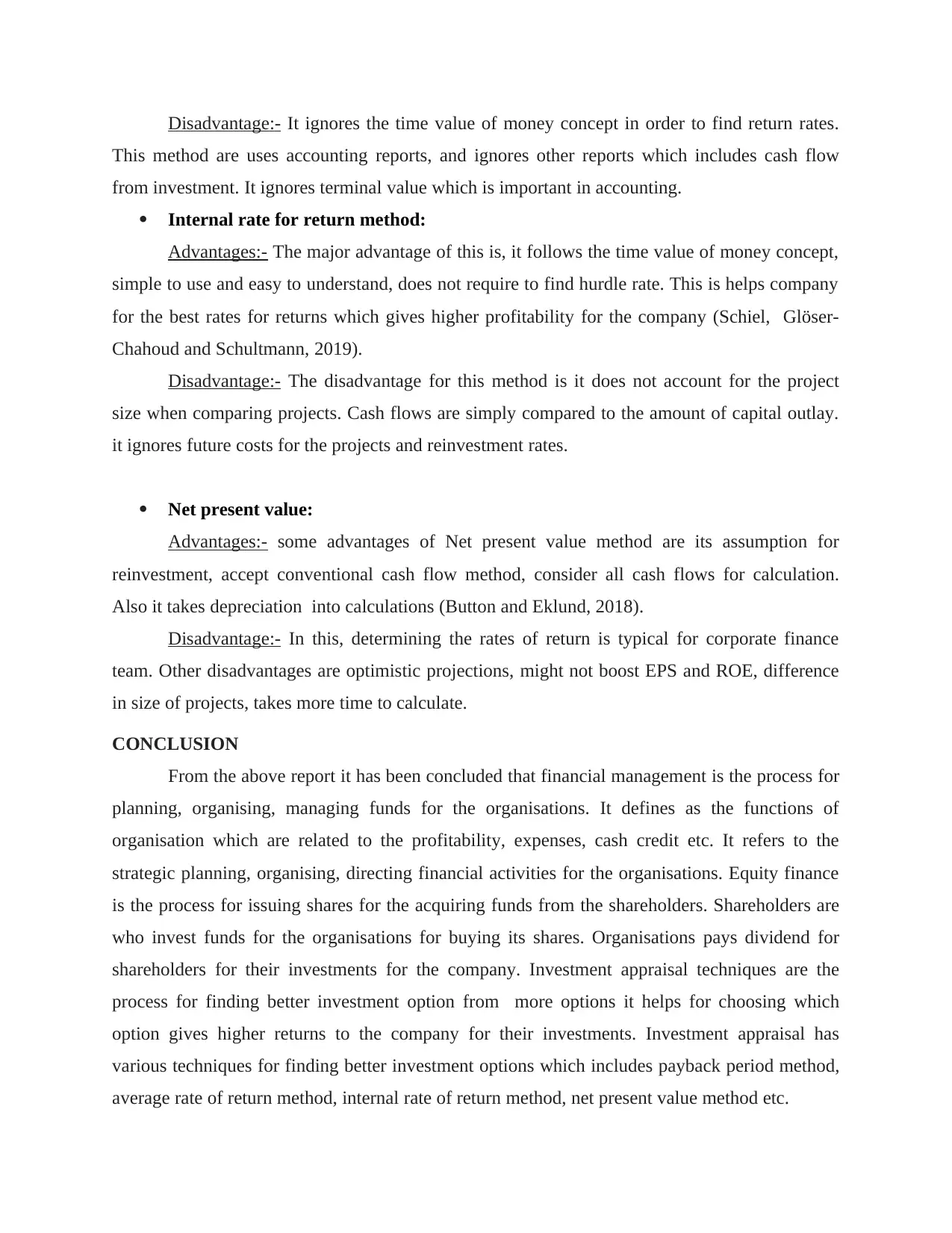

Disadvantage:- It ignores the time value of money concept in order to find return rates.

This method are uses accounting reports, and ignores other reports which includes cash flow

from investment. It ignores terminal value which is important in accounting.

Internal rate for return method:

Advantages:- The major advantage of this is, it follows the time value of money concept,

simple to use and easy to understand, does not require to find hurdle rate. This is helps company

for the best rates for returns which gives higher profitability for the company (Schiel, Glöser-

Chahoud and Schultmann, 2019).

Disadvantage:- The disadvantage for this method is it does not account for the project

size when comparing projects. Cash flows are simply compared to the amount of capital outlay.

it ignores future costs for the projects and reinvestment rates.

Net present value:

Advantages:- some advantages of Net present value method are its assumption for

reinvestment, accept conventional cash flow method, consider all cash flows for calculation.

Also it takes depreciation into calculations (Button and Eklund, 2018).

Disadvantage:- In this, determining the rates of return is typical for corporate finance

team. Other disadvantages are optimistic projections, might not boost EPS and ROE, difference

in size of projects, takes more time to calculate.

CONCLUSION

From the above report it has been concluded that financial management is the process for

planning, organising, managing funds for the organisations. It defines as the functions of

organisation which are related to the profitability, expenses, cash credit etc. It refers to the

strategic planning, organising, directing financial activities for the organisations. Equity finance

is the process for issuing shares for the acquiring funds from the shareholders. Shareholders are

who invest funds for the organisations for buying its shares. Organisations pays dividend for

shareholders for their investments for the company. Investment appraisal techniques are the

process for finding better investment option from more options it helps for choosing which

option gives higher returns to the company for their investments. Investment appraisal has

various techniques for finding better investment options which includes payback period method,

average rate of return method, internal rate of return method, net present value method etc.

This method are uses accounting reports, and ignores other reports which includes cash flow

from investment. It ignores terminal value which is important in accounting.

Internal rate for return method:

Advantages:- The major advantage of this is, it follows the time value of money concept,

simple to use and easy to understand, does not require to find hurdle rate. This is helps company

for the best rates for returns which gives higher profitability for the company (Schiel, Glöser-

Chahoud and Schultmann, 2019).

Disadvantage:- The disadvantage for this method is it does not account for the project

size when comparing projects. Cash flows are simply compared to the amount of capital outlay.

it ignores future costs for the projects and reinvestment rates.

Net present value:

Advantages:- some advantages of Net present value method are its assumption for

reinvestment, accept conventional cash flow method, consider all cash flows for calculation.

Also it takes depreciation into calculations (Button and Eklund, 2018).

Disadvantage:- In this, determining the rates of return is typical for corporate finance

team. Other disadvantages are optimistic projections, might not boost EPS and ROE, difference

in size of projects, takes more time to calculate.

CONCLUSION

From the above report it has been concluded that financial management is the process for

planning, organising, managing funds for the organisations. It defines as the functions of

organisation which are related to the profitability, expenses, cash credit etc. It refers to the

strategic planning, organising, directing financial activities for the organisations. Equity finance

is the process for issuing shares for the acquiring funds from the shareholders. Shareholders are

who invest funds for the organisations for buying its shares. Organisations pays dividend for

shareholders for their investments for the company. Investment appraisal techniques are the

process for finding better investment option from more options it helps for choosing which

option gives higher returns to the company for their investments. Investment appraisal has

various techniques for finding better investment options which includes payback period method,

average rate of return method, internal rate of return method, net present value method etc.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 14

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.