Financial Management Case Study: Develop Complex Broking Options

VerifiedAdded on 2021/05/31

|6

|1682

|31

Case Study

AI Summary

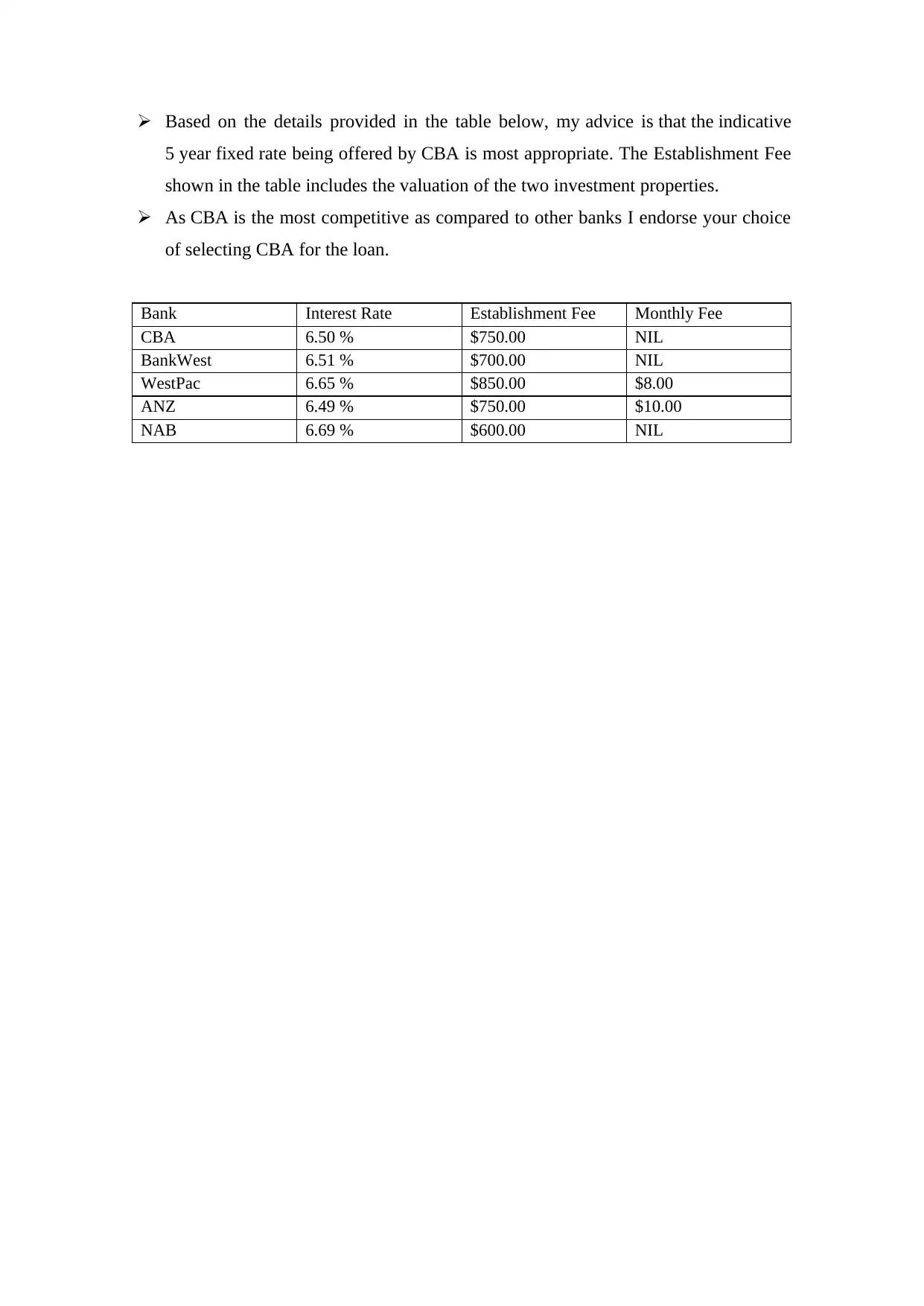

This case study presents a financial management scenario where a mortgage broker, Fred Broker, advises two brothers, Tom and Steve Broad, on purchasing two investment properties. The case begins with a detailed fact find, outlining the brothers' personal and financial situations, including their income, assets, liabilities, and investment experience. The proposed investment properties, their expected income, and expenses are also provided. A memo from Fred Broker to the brothers summarizes the discussion and outlines the process for obtaining finance, including required documentation, the application process, and recommendations on loan types, terms, and interest rates. The broker suggests a principal and interest loan with a 30-year term and recommends a 20% deposit. The case concludes with a comparison of interest rates from different banks, endorsing CBA as the most suitable option. The case provides a comprehensive overview of the steps involved in securing a mortgage for investment properties and the factors considered in financial planning.

1 out of 6

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.