Report: Comparative Analysis of Financial and Management Accounting

VerifiedAdded on 2023/01/12

|3

|575

|54

Report

AI Summary

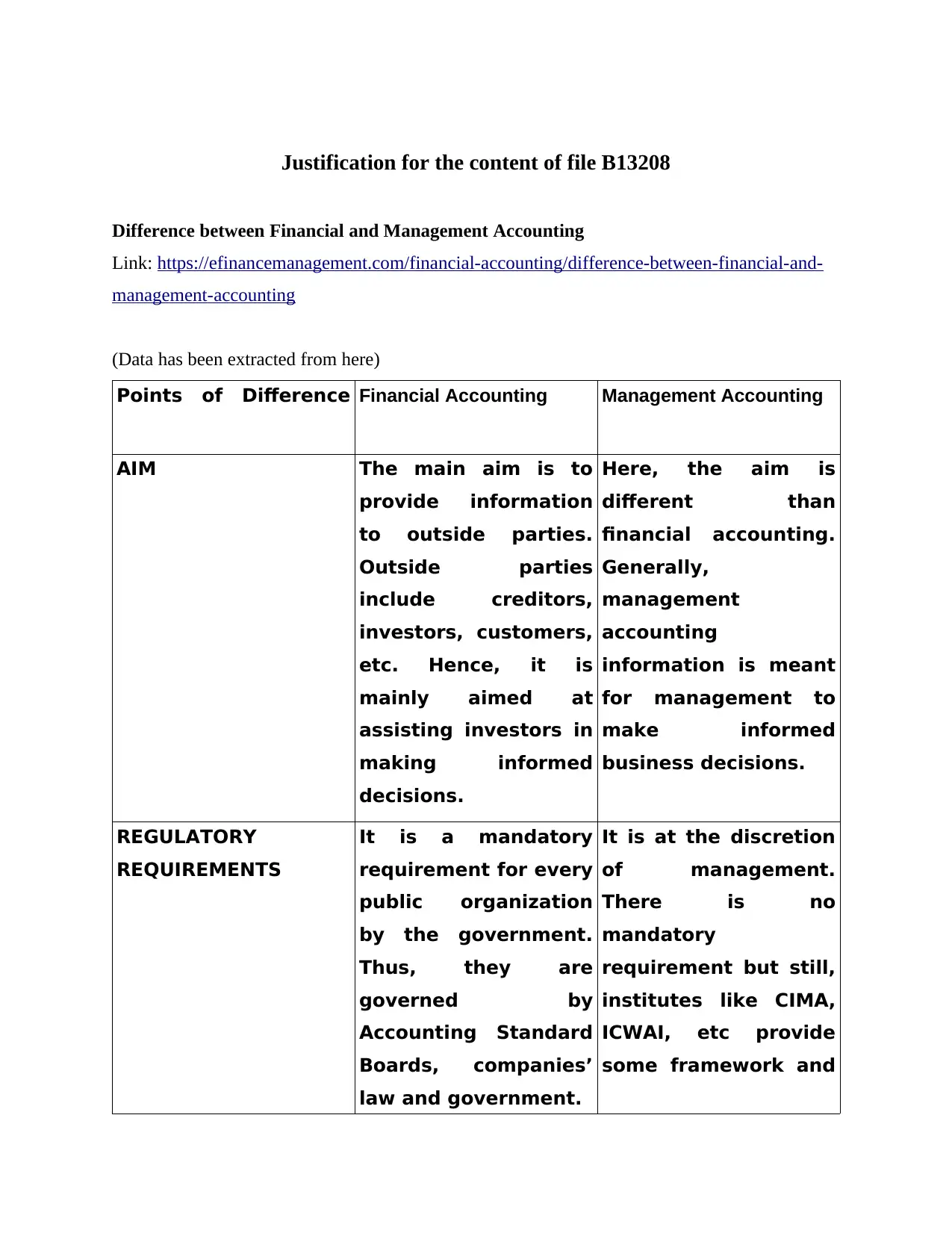

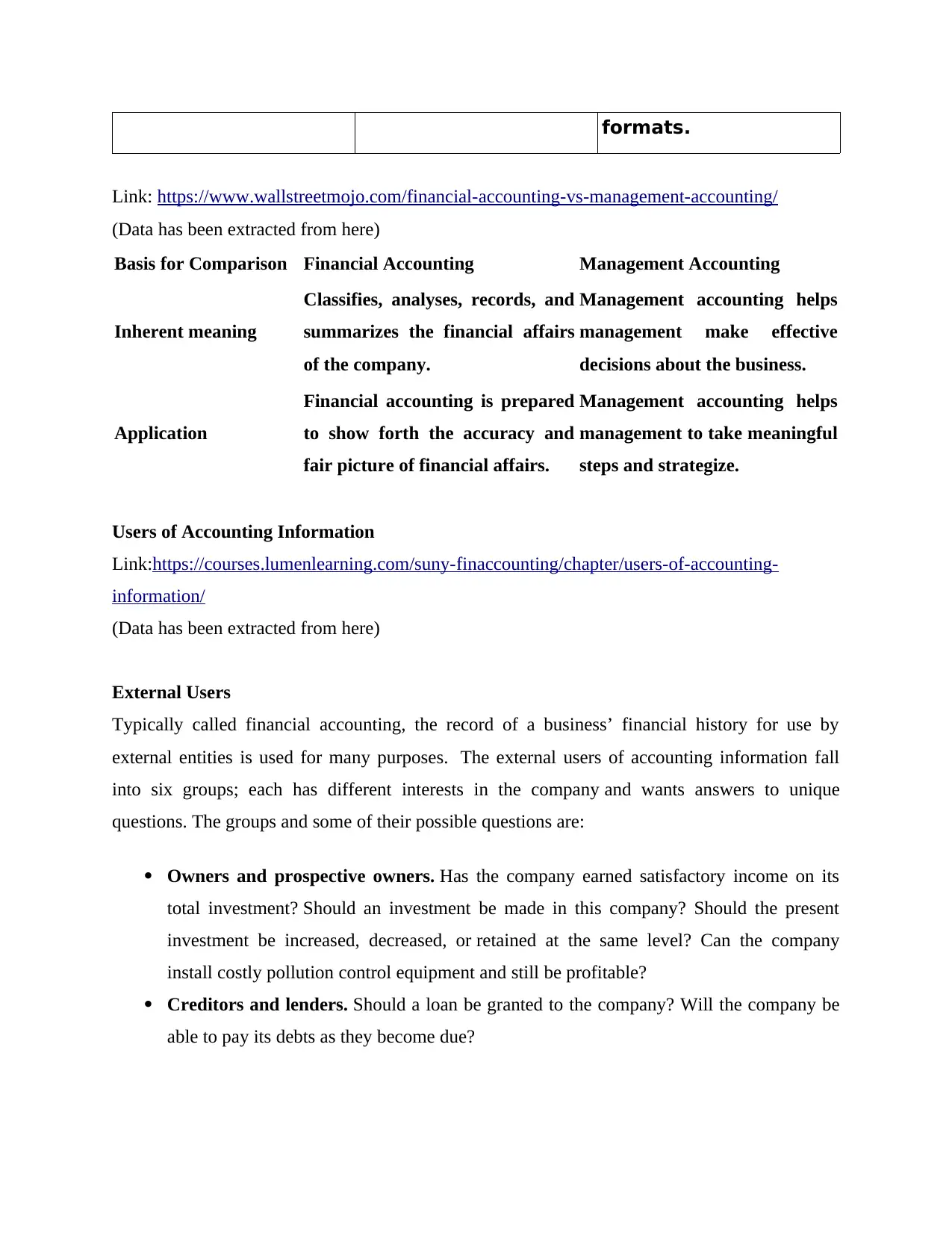

This report provides a comparative analysis of financial and management accounting, detailing their distinct purposes, users, and regulatory requirements. Financial accounting is designed for external stakeholders, such as investors and creditors, and adheres to established standards. Management accounting, on the other hand, is geared towards internal decision-making, offering insights for optimizing business operations. The report highlights the users of financial information, including owners, creditors, and employees, emphasizing their varied interests and needs. The report also explores the differences in the information provided by each accounting method, the data sources, and the objectives of each. The report aims to clarify the differences between the two fields and make it easier to understand the information provided by each accounting method.

1 out of 3

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.