Financial Performance Analysis: Brentwood Plc and Griffin Plc Report

VerifiedAdded on 2019/12/03

|17

|4557

|176

Report

AI Summary

This report provides a comprehensive financial analysis of Brentwood Plc and Griffin Plc. Part A focuses on Brentwood Plc, evaluating its financial performance through profitability, liquidity, gearing, asset utilization, and investment ratios for 2013 and 2014, including a detailed analysis of its working capital cycle. Part B shifts to Griffin Plc, analyzing the optimal production quantities given scarce resources and considering the relevance of committed fixed costs. Part C critically evaluates investment appraisal techniques and examines the assumptions underlying the break-even model. The report utilizes financial ratios, calculations, and comparisons to assess the companies' financial positions and offers insights into their financial management practices, making it a valuable resource for understanding financial analysis and control.

Financial

management and

control

1

management and

control

1

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

TABLE OF CONTENTS

Introduction......................................................................................................................................3

Part a – Brentwood Plc....................................................................................................................3

Report on financial performance for the Board of Brentwood Plc..............................................3

Computation of working capital cycle.........................................................................................7

Part b – Griffin Plc...........................................................................................................................9

Computation of optimum quantities of products by making utilization of scarce resources.......9

Relevance to the committed fixed costs in determination of optimum mix for production......10

Part c..............................................................................................................................................11

Critical evaluation of investment appraisal techniques.............................................................11

Analysis of assumptions linked to the model of break even......................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

2

Introduction......................................................................................................................................3

Part a – Brentwood Plc....................................................................................................................3

Report on financial performance for the Board of Brentwood Plc..............................................3

Computation of working capital cycle.........................................................................................7

Part b – Griffin Plc...........................................................................................................................9

Computation of optimum quantities of products by making utilization of scarce resources.......9

Relevance to the committed fixed costs in determination of optimum mix for production......10

Part c..............................................................................................................................................11

Critical evaluation of investment appraisal techniques.............................................................11

Analysis of assumptions linked to the model of break even......................................................13

Conclusion.....................................................................................................................................14

References......................................................................................................................................15

2

INDEX OF TABLES

Table 1: Statement showing profitability ratios...............................................................................4

Table 2: Statement showing liquidity ratios....................................................................................5

Table 3: Statement showing gearing ratios......................................................................................6

Table 4: Statement showing asset utilization ratios.........................................................................7

Table 5: Statement showing investment ratios................................................................................7

Table 6: Working capital cycle of Brentwood Plc of 2014.............................................................8

Table 7: Working capital cycle of Brentwood Plc of 2013.............................................................9

Table 8: Profitability statement of product A, B and C.................................................................10

Table 9: Statement showing unit demanded in the market............................................................10

Table 10: Statement showing ranking of production as profit in accordance with consumption of

quantity of raw material ................................................................................................................10

Table 11: Statement showing unit to be produced.........................................................................10

3

Table 1: Statement showing profitability ratios...............................................................................4

Table 2: Statement showing liquidity ratios....................................................................................5

Table 3: Statement showing gearing ratios......................................................................................6

Table 4: Statement showing asset utilization ratios.........................................................................7

Table 5: Statement showing investment ratios................................................................................7

Table 6: Working capital cycle of Brentwood Plc of 2014.............................................................8

Table 7: Working capital cycle of Brentwood Plc of 2013.............................................................9

Table 8: Profitability statement of product A, B and C.................................................................10

Table 9: Statement showing unit demanded in the market............................................................10

Table 10: Statement showing ranking of production as profit in accordance with consumption of

quantity of raw material ................................................................................................................10

Table 11: Statement showing unit to be produced.........................................................................10

3

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

INTRODUCTION

Finance is a crucial resource of business thus; management of organization is required to

make appropriate utilization of available resources in order to enhance their profitability. In order

to strengthen the financial position, companies are required to make financial analysis by using

suitable tools (Ahrendsen and Katchova, 2012). Present project report is focused on the

evaluation of various financial tools in order to develop an effective control on business. These

techniques will be applied to given case scenario of Brentwood Plc and Griffin Plc. Further,

description will be provided regarding the use of investment appraisal techniques and key

assumptions that are linked to the model of break-even point.

PART A – BRENTWOOD PLC

Report on financial performance for the Board of Brentwood Plc

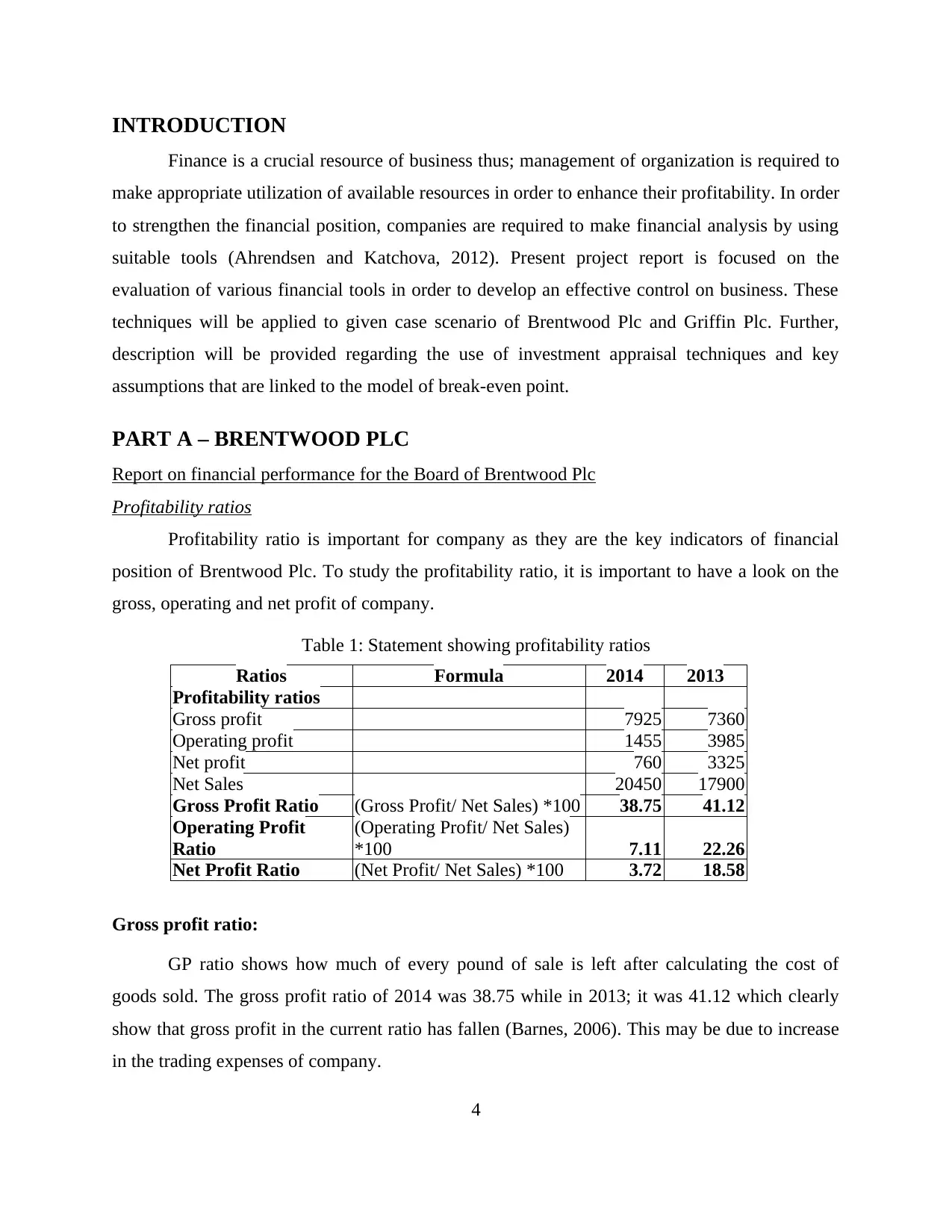

Profitability ratios

Profitability ratio is important for company as they are the key indicators of financial

position of Brentwood Plc. To study the profitability ratio, it is important to have a look on the

gross, operating and net profit of company.

Table 1: Statement showing profitability ratios

Ratios Formula 2014 2013

Profitability ratios

Gross profit 7925 7360

Operating profit 1455 3985

Net profit 760 3325

Net Sales 20450 17900

Gross Profit Ratio (Gross Profit/ Net Sales) *100 38.75 41.12

Operating Profit

Ratio

(Operating Profit/ Net Sales)

*100 7.11 22.26

Net Profit Ratio (Net Profit/ Net Sales) *100 3.72 18.58

Gross profit ratio:

GP ratio shows how much of every pound of sale is left after calculating the cost of

goods sold. The gross profit ratio of 2014 was 38.75 while in 2013; it was 41.12 which clearly

show that gross profit in the current ratio has fallen (Barnes, 2006). This may be due to increase

in the trading expenses of company.

4

Finance is a crucial resource of business thus; management of organization is required to

make appropriate utilization of available resources in order to enhance their profitability. In order

to strengthen the financial position, companies are required to make financial analysis by using

suitable tools (Ahrendsen and Katchova, 2012). Present project report is focused on the

evaluation of various financial tools in order to develop an effective control on business. These

techniques will be applied to given case scenario of Brentwood Plc and Griffin Plc. Further,

description will be provided regarding the use of investment appraisal techniques and key

assumptions that are linked to the model of break-even point.

PART A – BRENTWOOD PLC

Report on financial performance for the Board of Brentwood Plc

Profitability ratios

Profitability ratio is important for company as they are the key indicators of financial

position of Brentwood Plc. To study the profitability ratio, it is important to have a look on the

gross, operating and net profit of company.

Table 1: Statement showing profitability ratios

Ratios Formula 2014 2013

Profitability ratios

Gross profit 7925 7360

Operating profit 1455 3985

Net profit 760 3325

Net Sales 20450 17900

Gross Profit Ratio (Gross Profit/ Net Sales) *100 38.75 41.12

Operating Profit

Ratio

(Operating Profit/ Net Sales)

*100 7.11 22.26

Net Profit Ratio (Net Profit/ Net Sales) *100 3.72 18.58

Gross profit ratio:

GP ratio shows how much of every pound of sale is left after calculating the cost of

goods sold. The gross profit ratio of 2014 was 38.75 while in 2013; it was 41.12 which clearly

show that gross profit in the current ratio has fallen (Barnes, 2006). This may be due to increase

in the trading expenses of company.

4

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

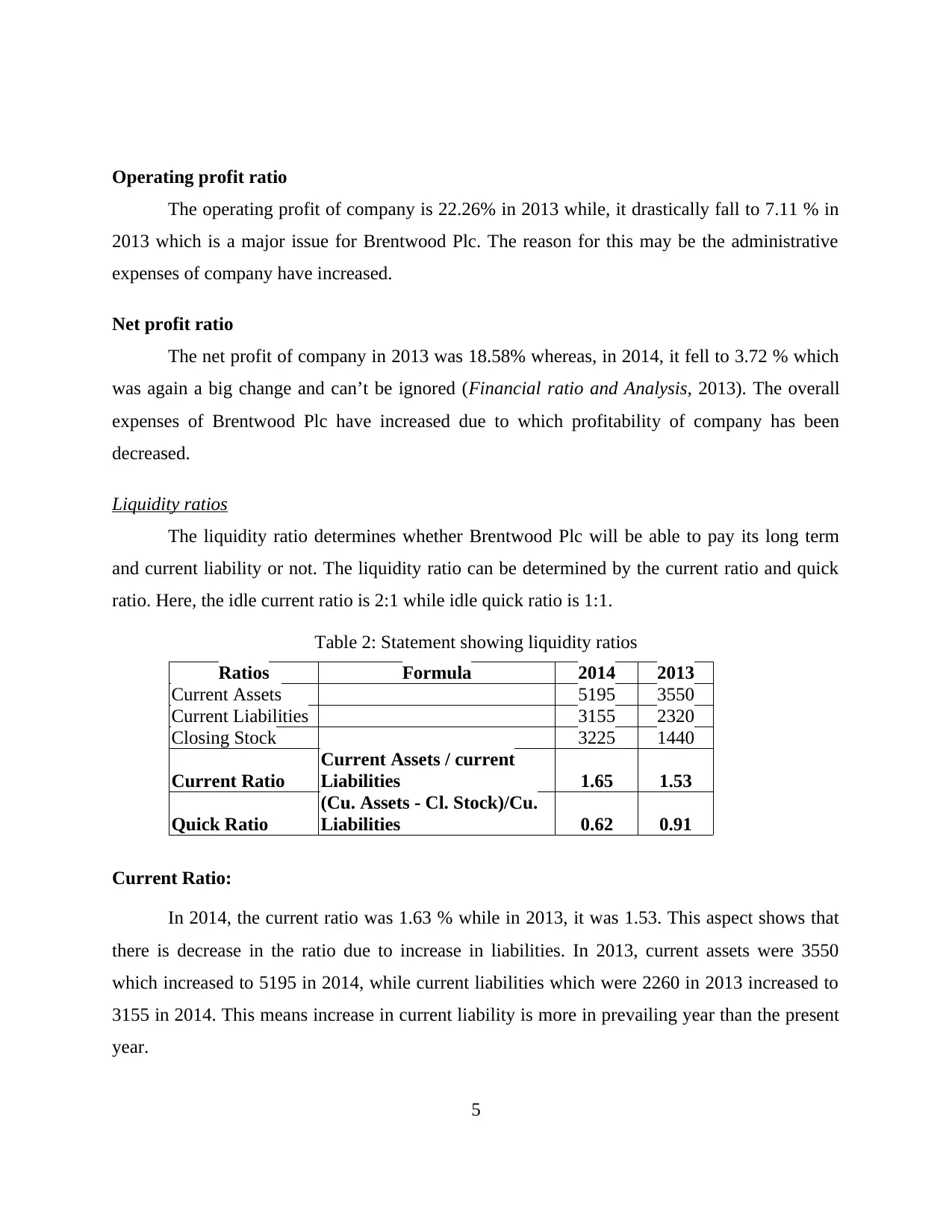

Operating profit ratio

The operating profit of company is 22.26% in 2013 while, it drastically fall to 7.11 % in

2013 which is a major issue for Brentwood Plc. The reason for this may be the administrative

expenses of company have increased.

Net profit ratio

The net profit of company in 2013 was 18.58% whereas, in 2014, it fell to 3.72 % which

was again a big change and can’t be ignored (Financial ratio and Analysis, 2013). The overall

expenses of Brentwood Plc have increased due to which profitability of company has been

decreased.

Liquidity ratios

The liquidity ratio determines whether Brentwood Plc will be able to pay its long term

and current liability or not. The liquidity ratio can be determined by the current ratio and quick

ratio. Here, the idle current ratio is 2:1 while idle quick ratio is 1:1.

Table 2: Statement showing liquidity ratios

Ratios Formula 2014 2013

Current Assets 5195 3550

Current Liabilities 3155 2320

Closing Stock 3225 1440

Current Ratio

Current Assets / current

Liabilities 1.65 1.53

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.62 0.91

Current Ratio:

In 2014, the current ratio was 1.63 % while in 2013, it was 1.53. This aspect shows that

there is decrease in the ratio due to increase in liabilities. In 2013, current assets were 3550

which increased to 5195 in 2014, while current liabilities which were 2260 in 2013 increased to

3155 in 2014. This means increase in current liability is more in prevailing year than the present

year.

5

The operating profit of company is 22.26% in 2013 while, it drastically fall to 7.11 % in

2013 which is a major issue for Brentwood Plc. The reason for this may be the administrative

expenses of company have increased.

Net profit ratio

The net profit of company in 2013 was 18.58% whereas, in 2014, it fell to 3.72 % which

was again a big change and can’t be ignored (Financial ratio and Analysis, 2013). The overall

expenses of Brentwood Plc have increased due to which profitability of company has been

decreased.

Liquidity ratios

The liquidity ratio determines whether Brentwood Plc will be able to pay its long term

and current liability or not. The liquidity ratio can be determined by the current ratio and quick

ratio. Here, the idle current ratio is 2:1 while idle quick ratio is 1:1.

Table 2: Statement showing liquidity ratios

Ratios Formula 2014 2013

Current Assets 5195 3550

Current Liabilities 3155 2320

Closing Stock 3225 1440

Current Ratio

Current Assets / current

Liabilities 1.65 1.53

Quick Ratio

(Cu. Assets - Cl. Stock)/Cu.

Liabilities 0.62 0.91

Current Ratio:

In 2014, the current ratio was 1.63 % while in 2013, it was 1.53. This aspect shows that

there is decrease in the ratio due to increase in liabilities. In 2013, current assets were 3550

which increased to 5195 in 2014, while current liabilities which were 2260 in 2013 increased to

3155 in 2014. This means increase in current liability is more in prevailing year than the present

year.

5

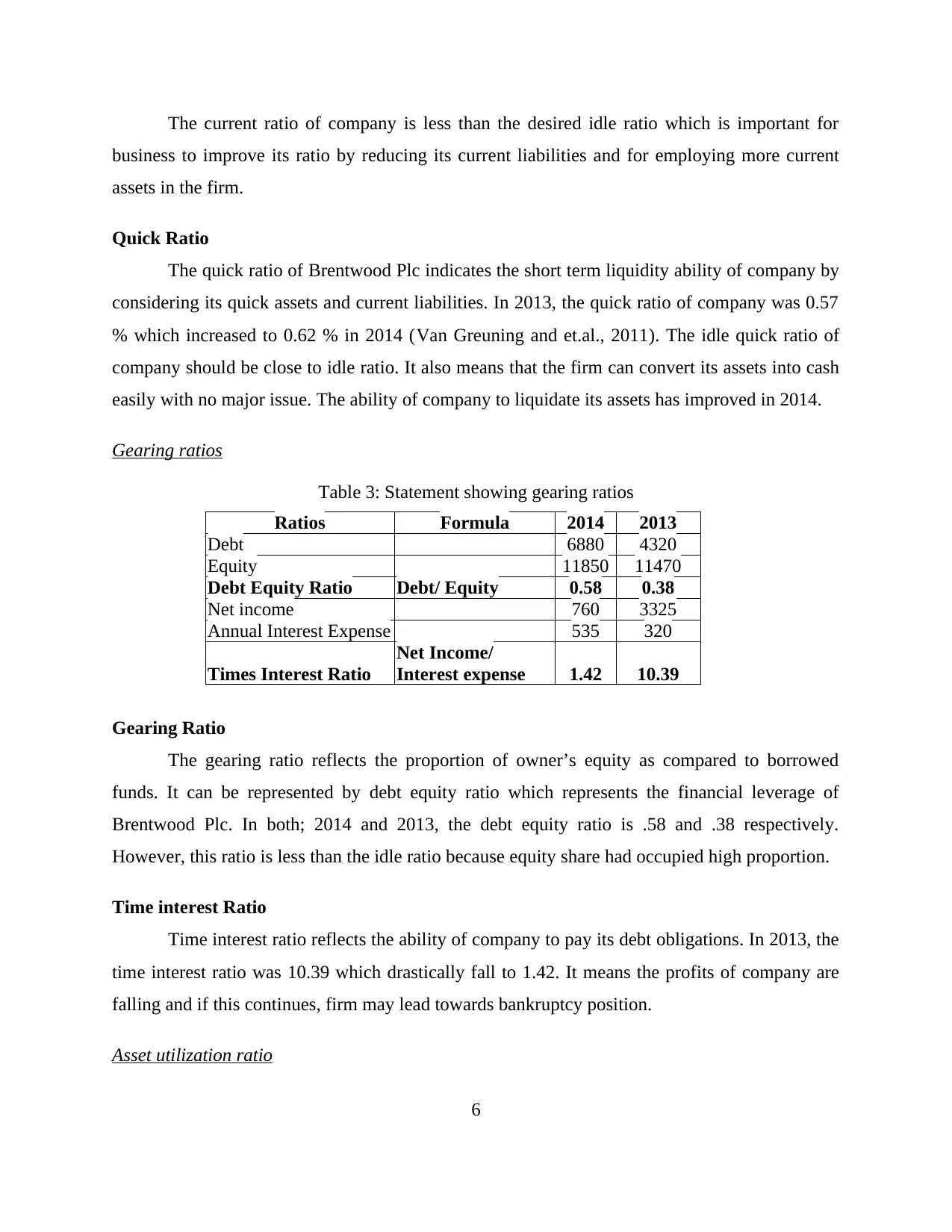

The current ratio of company is less than the desired idle ratio which is important for

business to improve its ratio by reducing its current liabilities and for employing more current

assets in the firm.

Quick Ratio

The quick ratio of Brentwood Plc indicates the short term liquidity ability of company by

considering its quick assets and current liabilities. In 2013, the quick ratio of company was 0.57

% which increased to 0.62 % in 2014 (Van Greuning and et.al., 2011). The idle quick ratio of

company should be close to idle ratio. It also means that the firm can convert its assets into cash

easily with no major issue. The ability of company to liquidate its assets has improved in 2014.

Gearing ratios

Table 3: Statement showing gearing ratios

Ratios Formula 2014 2013

Debt 6880 4320

Equity 11850 11470

Debt Equity Ratio Debt/ Equity 0.58 0.38

Net income 760 3325

Annual Interest Expense 535 320

Times Interest Ratio

Net Income/

Interest expense 1.42 10.39

Gearing Ratio

The gearing ratio reflects the proportion of owner’s equity as compared to borrowed

funds. It can be represented by debt equity ratio which represents the financial leverage of

Brentwood Plc. In both; 2014 and 2013, the debt equity ratio is .58 and .38 respectively.

However, this ratio is less than the idle ratio because equity share had occupied high proportion.

Time interest Ratio

Time interest ratio reflects the ability of company to pay its debt obligations. In 2013, the

time interest ratio was 10.39 which drastically fall to 1.42. It means the profits of company are

falling and if this continues, firm may lead towards bankruptcy position.

Asset utilization ratio

6

business to improve its ratio by reducing its current liabilities and for employing more current

assets in the firm.

Quick Ratio

The quick ratio of Brentwood Plc indicates the short term liquidity ability of company by

considering its quick assets and current liabilities. In 2013, the quick ratio of company was 0.57

% which increased to 0.62 % in 2014 (Van Greuning and et.al., 2011). The idle quick ratio of

company should be close to idle ratio. It also means that the firm can convert its assets into cash

easily with no major issue. The ability of company to liquidate its assets has improved in 2014.

Gearing ratios

Table 3: Statement showing gearing ratios

Ratios Formula 2014 2013

Debt 6880 4320

Equity 11850 11470

Debt Equity Ratio Debt/ Equity 0.58 0.38

Net income 760 3325

Annual Interest Expense 535 320

Times Interest Ratio

Net Income/

Interest expense 1.42 10.39

Gearing Ratio

The gearing ratio reflects the proportion of owner’s equity as compared to borrowed

funds. It can be represented by debt equity ratio which represents the financial leverage of

Brentwood Plc. In both; 2014 and 2013, the debt equity ratio is .58 and .38 respectively.

However, this ratio is less than the idle ratio because equity share had occupied high proportion.

Time interest Ratio

Time interest ratio reflects the ability of company to pay its debt obligations. In 2013, the

time interest ratio was 10.39 which drastically fall to 1.42. It means the profits of company are

falling and if this continues, firm may lead towards bankruptcy position.

Asset utilization ratio

6

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

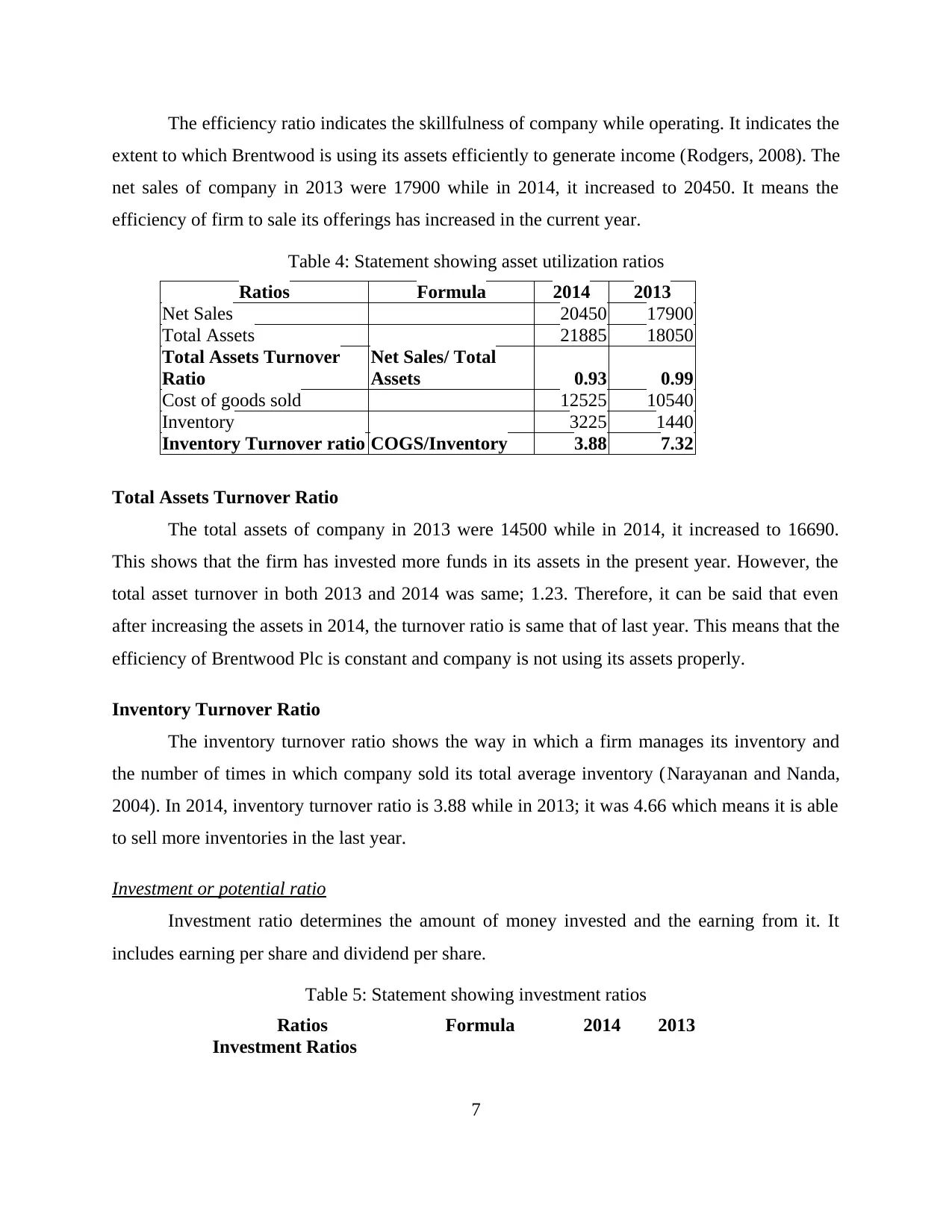

The efficiency ratio indicates the skillfulness of company while operating. It indicates the

extent to which Brentwood is using its assets efficiently to generate income (Rodgers, 2008). The

net sales of company in 2013 were 17900 while in 2014, it increased to 20450. It means the

efficiency of firm to sale its offerings has increased in the current year.

Table 4: Statement showing asset utilization ratios

Ratios Formula 2014 2013

Net Sales 20450 17900

Total Assets 21885 18050

Total Assets Turnover

Ratio

Net Sales/ Total

Assets 0.93 0.99

Cost of goods sold 12525 10540

Inventory 3225 1440

Inventory Turnover ratio COGS/Inventory 3.88 7.32

Total Assets Turnover Ratio

The total assets of company in 2013 were 14500 while in 2014, it increased to 16690.

This shows that the firm has invested more funds in its assets in the present year. However, the

total asset turnover in both 2013 and 2014 was same; 1.23. Therefore, it can be said that even

after increasing the assets in 2014, the turnover ratio is same that of last year. This means that the

efficiency of Brentwood Plc is constant and company is not using its assets properly.

Inventory Turnover Ratio

The inventory turnover ratio shows the way in which a firm manages its inventory and

the number of times in which company sold its total average inventory (Narayanan and Nanda,

2004). In 2014, inventory turnover ratio is 3.88 while in 2013; it was 4.66 which means it is able

to sell more inventories in the last year.

Investment or potential ratio

Investment ratio determines the amount of money invested and the earning from it. It

includes earning per share and dividend per share.

Table 5: Statement showing investment ratios

Ratios Formula 2014 2013

Investment Ratios

7

extent to which Brentwood is using its assets efficiently to generate income (Rodgers, 2008). The

net sales of company in 2013 were 17900 while in 2014, it increased to 20450. It means the

efficiency of firm to sale its offerings has increased in the current year.

Table 4: Statement showing asset utilization ratios

Ratios Formula 2014 2013

Net Sales 20450 17900

Total Assets 21885 18050

Total Assets Turnover

Ratio

Net Sales/ Total

Assets 0.93 0.99

Cost of goods sold 12525 10540

Inventory 3225 1440

Inventory Turnover ratio COGS/Inventory 3.88 7.32

Total Assets Turnover Ratio

The total assets of company in 2013 were 14500 while in 2014, it increased to 16690.

This shows that the firm has invested more funds in its assets in the present year. However, the

total asset turnover in both 2013 and 2014 was same; 1.23. Therefore, it can be said that even

after increasing the assets in 2014, the turnover ratio is same that of last year. This means that the

efficiency of Brentwood Plc is constant and company is not using its assets properly.

Inventory Turnover Ratio

The inventory turnover ratio shows the way in which a firm manages its inventory and

the number of times in which company sold its total average inventory (Narayanan and Nanda,

2004). In 2014, inventory turnover ratio is 3.88 while in 2013; it was 4.66 which means it is able

to sell more inventories in the last year.

Investment or potential ratio

Investment ratio determines the amount of money invested and the earning from it. It

includes earning per share and dividend per share.

Table 5: Statement showing investment ratios

Ratios Formula 2014 2013

Investment Ratios

7

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

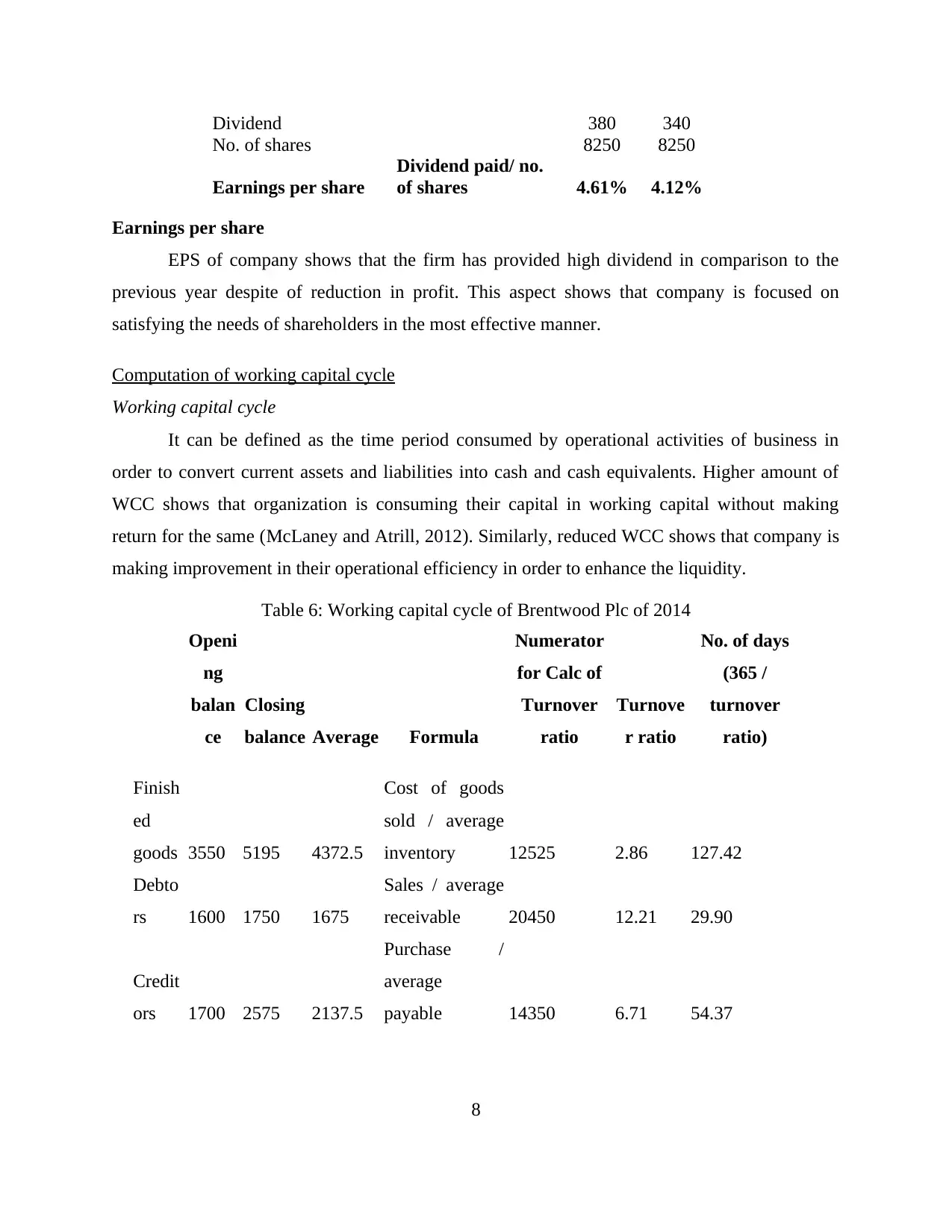

Dividend 380 340

No. of shares 8250 8250

Earnings per share

Dividend paid/ no.

of shares 4.61% 4.12%

Earnings per share

EPS of company shows that the firm has provided high dividend in comparison to the

previous year despite of reduction in profit. This aspect shows that company is focused on

satisfying the needs of shareholders in the most effective manner.

Computation of working capital cycle

Working capital cycle

It can be defined as the time period consumed by operational activities of business in

order to convert current assets and liabilities into cash and cash equivalents. Higher amount of

WCC shows that organization is consuming their capital in working capital without making

return for the same (McLaney and Atrill, 2012). Similarly, reduced WCC shows that company is

making improvement in their operational efficiency in order to enhance the liquidity.

Table 6: Working capital cycle of Brentwood Plc of 2014

Openi

ng

balan

ce

Closing

balance Average Formula

Numerator

for Calc of

Turnover

ratio

Turnove

r ratio

No. of days

(365 /

turnover

ratio)

Finish

ed

goods 3550 5195 4372.5

Cost of goods

sold / average

inventory 12525 2.86 127.42

Debto

rs 1600 1750 1675

Sales / average

receivable 20450 12.21 29.90

Credit

ors 1700 2575 2137.5

Purchase /

average

payable 14350 6.71 54.37

8

No. of shares 8250 8250

Earnings per share

Dividend paid/ no.

of shares 4.61% 4.12%

Earnings per share

EPS of company shows that the firm has provided high dividend in comparison to the

previous year despite of reduction in profit. This aspect shows that company is focused on

satisfying the needs of shareholders in the most effective manner.

Computation of working capital cycle

Working capital cycle

It can be defined as the time period consumed by operational activities of business in

order to convert current assets and liabilities into cash and cash equivalents. Higher amount of

WCC shows that organization is consuming their capital in working capital without making

return for the same (McLaney and Atrill, 2012). Similarly, reduced WCC shows that company is

making improvement in their operational efficiency in order to enhance the liquidity.

Table 6: Working capital cycle of Brentwood Plc of 2014

Openi

ng

balan

ce

Closing

balance Average Formula

Numerator

for Calc of

Turnover

ratio

Turnove

r ratio

No. of days

(365 /

turnover

ratio)

Finish

ed

goods 3550 5195 4372.5

Cost of goods

sold / average

inventory 12525 2.86 127.42

Debto

rs 1600 1750 1675

Sales / average

receivable 20450 12.21 29.90

Credit

ors 1700 2575 2137.5

Purchase /

average

payable 14350 6.71 54.37

8

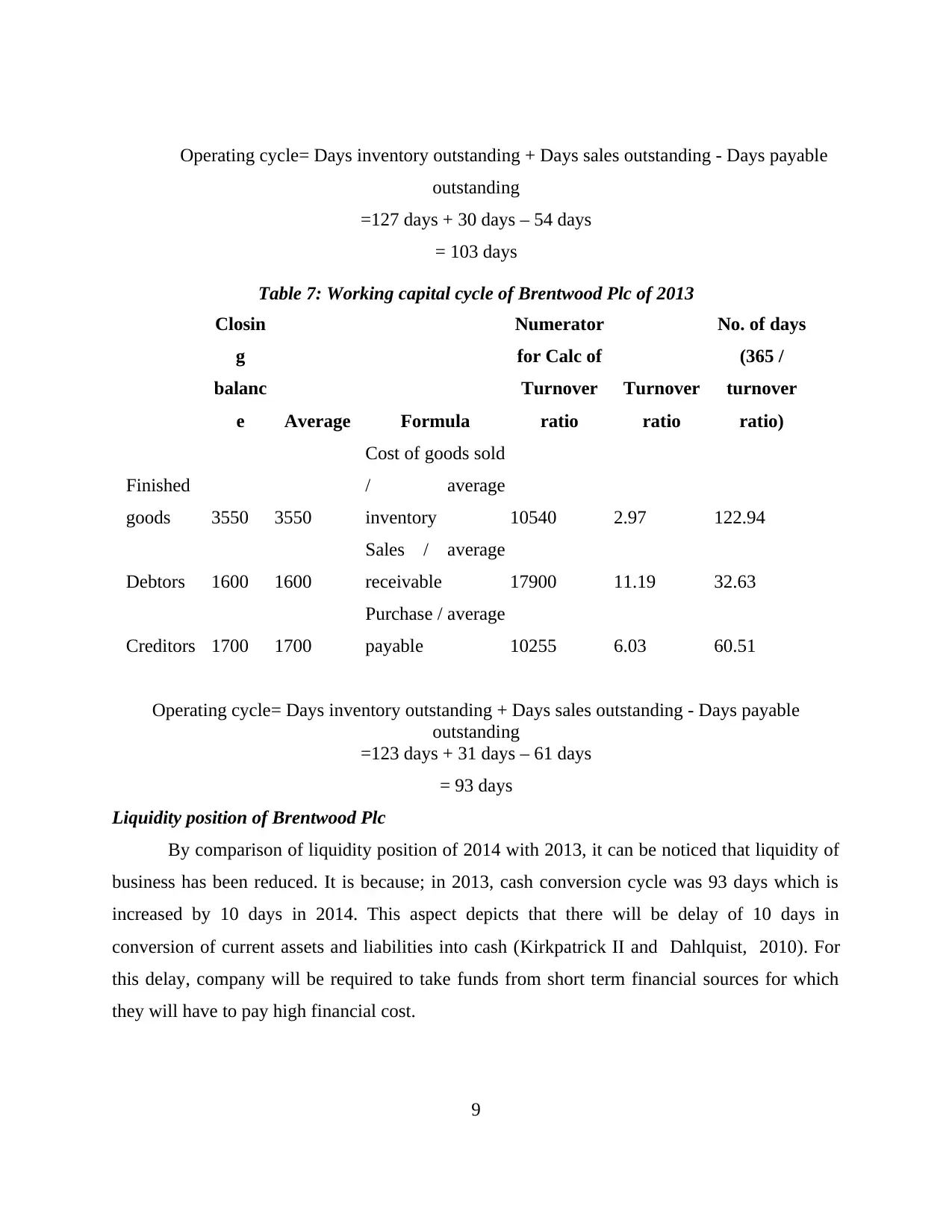

Operating cycle= Days inventory outstanding + Days sales outstanding - Days payable

outstanding

=127 days + 30 days – 54 days

= 103 days

Table 7: Working capital cycle of Brentwood Plc of 2013

Closin

g

balanc

e Average Formula

Numerator

for Calc of

Turnover

ratio

Turnover

ratio

No. of days

(365 /

turnover

ratio)

Finished

goods 3550 3550

Cost of goods sold

/ average

inventory 10540 2.97 122.94

Debtors 1600 1600

Sales / average

receivable 17900 11.19 32.63

Creditors 1700 1700

Purchase / average

payable 10255 6.03 60.51

Operating cycle= Days inventory outstanding + Days sales outstanding - Days payable

outstanding

=123 days + 31 days – 61 days

= 93 days

Liquidity position of Brentwood Plc

By comparison of liquidity position of 2014 with 2013, it can be noticed that liquidity of

business has been reduced. It is because; in 2013, cash conversion cycle was 93 days which is

increased by 10 days in 2014. This aspect depicts that there will be delay of 10 days in

conversion of current assets and liabilities into cash (Kirkpatrick II and Dahlquist, 2010). For

this delay, company will be required to take funds from short term financial sources for which

they will have to pay high financial cost.

9

outstanding

=127 days + 30 days – 54 days

= 103 days

Table 7: Working capital cycle of Brentwood Plc of 2013

Closin

g

balanc

e Average Formula

Numerator

for Calc of

Turnover

ratio

Turnover

ratio

No. of days

(365 /

turnover

ratio)

Finished

goods 3550 3550

Cost of goods sold

/ average

inventory 10540 2.97 122.94

Debtors 1600 1600

Sales / average

receivable 17900 11.19 32.63

Creditors 1700 1700

Purchase / average

payable 10255 6.03 60.51

Operating cycle= Days inventory outstanding + Days sales outstanding - Days payable

outstanding

=123 days + 31 days – 61 days

= 93 days

Liquidity position of Brentwood Plc

By comparison of liquidity position of 2014 with 2013, it can be noticed that liquidity of

business has been reduced. It is because; in 2013, cash conversion cycle was 93 days which is

increased by 10 days in 2014. This aspect depicts that there will be delay of 10 days in

conversion of current assets and liabilities into cash (Kirkpatrick II and Dahlquist, 2010). For

this delay, company will be required to take funds from short term financial sources for which

they will have to pay high financial cost.

9

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

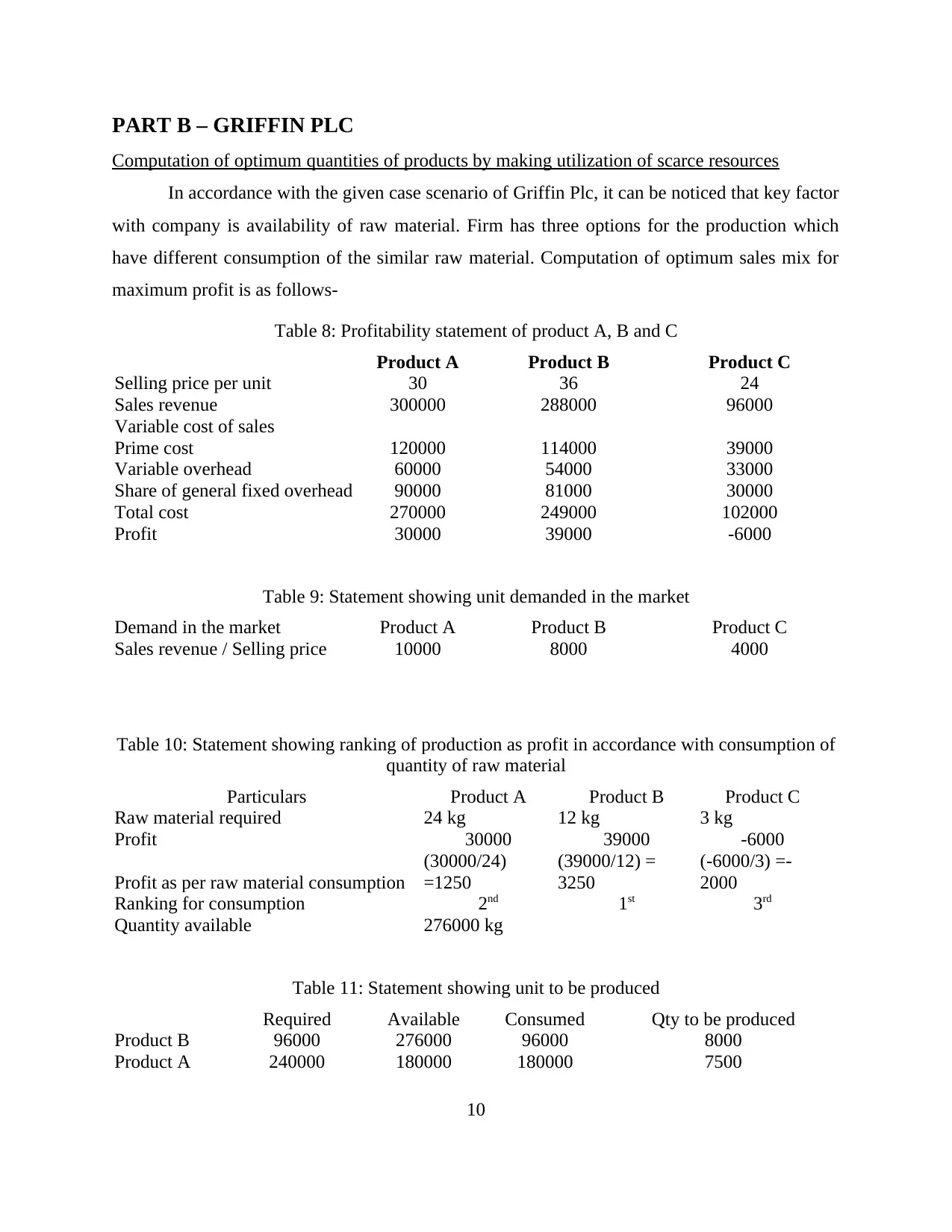

PART B – GRIFFIN PLC

Computation of optimum quantities of products by making utilization of scarce resources

In accordance with the given case scenario of Griffin Plc, it can be noticed that key factor

with company is availability of raw material. Firm has three options for the production which

have different consumption of the similar raw material. Computation of optimum sales mix for

maximum profit is as follows-

Table 8: Profitability statement of product A, B and C

Product A Product B Product C

Selling price per unit 30 36 24

Sales revenue 300000 288000 96000

Variable cost of sales

Prime cost 120000 114000 39000

Variable overhead 60000 54000 33000

Share of general fixed overhead 90000 81000 30000

Total cost 270000 249000 102000

Profit 30000 39000 -6000

Table 9: Statement showing unit demanded in the market

Demand in the market Product A Product B Product C

Sales revenue / Selling price 10000 8000 4000

Table 10: Statement showing ranking of production as profit in accordance with consumption of

quantity of raw material

Particulars Product A Product B Product C

Raw material required 24 kg 12 kg 3 kg

Profit 30000 39000 -6000

Profit as per raw material consumption

(30000/24)

=1250

(39000/12) =

3250

(-6000/3) =-

2000

Ranking for consumption 2nd 1st 3rd

Quantity available 276000 kg

Table 11: Statement showing unit to be produced

Required Available Consumed Qty to be produced

Product B 96000 276000 96000 8000

Product A 240000 180000 180000 7500

10

Computation of optimum quantities of products by making utilization of scarce resources

In accordance with the given case scenario of Griffin Plc, it can be noticed that key factor

with company is availability of raw material. Firm has three options for the production which

have different consumption of the similar raw material. Computation of optimum sales mix for

maximum profit is as follows-

Table 8: Profitability statement of product A, B and C

Product A Product B Product C

Selling price per unit 30 36 24

Sales revenue 300000 288000 96000

Variable cost of sales

Prime cost 120000 114000 39000

Variable overhead 60000 54000 33000

Share of general fixed overhead 90000 81000 30000

Total cost 270000 249000 102000

Profit 30000 39000 -6000

Table 9: Statement showing unit demanded in the market

Demand in the market Product A Product B Product C

Sales revenue / Selling price 10000 8000 4000

Table 10: Statement showing ranking of production as profit in accordance with consumption of

quantity of raw material

Particulars Product A Product B Product C

Raw material required 24 kg 12 kg 3 kg

Profit 30000 39000 -6000

Profit as per raw material consumption

(30000/24)

=1250

(39000/12) =

3250

(-6000/3) =-

2000

Ranking for consumption 2nd 1st 3rd

Quantity available 276000 kg

Table 11: Statement showing unit to be produced

Required Available Consumed Qty to be produced

Product B 96000 276000 96000 8000

Product A 240000 180000 180000 7500

10

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Product C 12000 0 0 0

In order to earn maximum profit, company is required to produce 8000 units of B and

7500 units of A. In addition to this, product C should be eliminated from the sales mix because it

is providing loss to the firm (Management accounting, 2014).

Relevance to the committed fixed costs in determination of optimum mix for production

Fixed cost plays a vital role in decision making for all the organizations because it assists

the management in achieving break-even point. In order to recover all the costs, firm is required

to assure that provided contribution by production units are able to recover the fixed cost of

business. In addition to this, production mix is narrowed or widened on the basis of their fixed

costs (Kieso, Weygandt and Warfield, 2001). It is because; production can be done by

commercial organization in accordance with their budgets. Products that are profitable but are

not in the budget of company will not be produced. For example in the above case scenario,

fixed cost of product A is not affordable then firm will not produce it despite of the fact that it is

the second most profitable product.

In addition to the fixed cost, following costs affect the decision of production mix of

company-

1. Profitability- All business entities aim to maximize their profit. Due to this aspect,

organization prefers to produce those options which will make positive change in the

profitability of business.

2. Production capacity- Production mix decision also varies with the production capacity of

plant or overall business capacity. By considering this factor, company designs their mix

in such a way by which available resources can be utilized in an optimum manner (Gray

and et. al., 2013).

3. Fluctuation in demand- Decisions regarding production mix are taken with the reference

to demand of product in the market. For example, if a product is profitable but it does not

have high demand in the market then company will switch to another option. For this

aspect, previous scenario can be considered (Gibson, 2010). In that example, product B

has maximum demand of 8000 units thus; remaining raw material has been consumed on

product A.

11

In order to earn maximum profit, company is required to produce 8000 units of B and

7500 units of A. In addition to this, product C should be eliminated from the sales mix because it

is providing loss to the firm (Management accounting, 2014).

Relevance to the committed fixed costs in determination of optimum mix for production

Fixed cost plays a vital role in decision making for all the organizations because it assists

the management in achieving break-even point. In order to recover all the costs, firm is required

to assure that provided contribution by production units are able to recover the fixed cost of

business. In addition to this, production mix is narrowed or widened on the basis of their fixed

costs (Kieso, Weygandt and Warfield, 2001). It is because; production can be done by

commercial organization in accordance with their budgets. Products that are profitable but are

not in the budget of company will not be produced. For example in the above case scenario,

fixed cost of product A is not affordable then firm will not produce it despite of the fact that it is

the second most profitable product.

In addition to the fixed cost, following costs affect the decision of production mix of

company-

1. Profitability- All business entities aim to maximize their profit. Due to this aspect,

organization prefers to produce those options which will make positive change in the

profitability of business.

2. Production capacity- Production mix decision also varies with the production capacity of

plant or overall business capacity. By considering this factor, company designs their mix

in such a way by which available resources can be utilized in an optimum manner (Gray

and et. al., 2013).

3. Fluctuation in demand- Decisions regarding production mix are taken with the reference

to demand of product in the market. For example, if a product is profitable but it does not

have high demand in the market then company will switch to another option. For this

aspect, previous scenario can be considered (Gibson, 2010). In that example, product B

has maximum demand of 8000 units thus; remaining raw material has been consumed on

product A.

11

4. Competition- An organization is required to design their production mix in a way that

competitive advantage can be achieved by the business. In addition to this, production

mix strategy used by competing firms will also affect the strategy of business.

5. Government rules and restriction- Companies are required to comply with regulatory

policies while formulation of production policies (Drake, 2012). Due to these factors,

sometimes, organization has to impose restrictions on certain products as they are not

permitted by the government authorities.

6. Overall condition of business and economy- In the present globalized era, no business

entity can ignore the impact of world economy. Thus, these factors are required to be

considered by the management while determination of production mixes for business.

PART C

Critical evaluation of investment appraisal techniques

Investment appraisal techniques are used to analyze proposed options for the investment

in order to assess their risk and potential profits. By making comparative evaluation of available

options, financial manager will be able to select the suitable option for their business (Deon,

2010). Description of various investment appraisal techniques along with their advantages and

disadvantages is as follows-

Net present value

In this method, computation of net inflow is done by considering the time value of

money. Organizations are recommended to make investment in option with the positive present

value (Positive Net Present Value Mean When Appraising Long-Term Projects?, 2013).

Advantages and disadvantages of this method is enumerated as below-

Advantages-

This method provides the importance to time value of money.

Analysis is done by giving priority to risk and profitability. In computation, all aspects are covered.

Disadvantages-

12

competitive advantage can be achieved by the business. In addition to this, production

mix strategy used by competing firms will also affect the strategy of business.

5. Government rules and restriction- Companies are required to comply with regulatory

policies while formulation of production policies (Drake, 2012). Due to these factors,

sometimes, organization has to impose restrictions on certain products as they are not

permitted by the government authorities.

6. Overall condition of business and economy- In the present globalized era, no business

entity can ignore the impact of world economy. Thus, these factors are required to be

considered by the management while determination of production mixes for business.

PART C

Critical evaluation of investment appraisal techniques

Investment appraisal techniques are used to analyze proposed options for the investment

in order to assess their risk and potential profits. By making comparative evaluation of available

options, financial manager will be able to select the suitable option for their business (Deon,

2010). Description of various investment appraisal techniques along with their advantages and

disadvantages is as follows-

Net present value

In this method, computation of net inflow is done by considering the time value of

money. Organizations are recommended to make investment in option with the positive present

value (Positive Net Present Value Mean When Appraising Long-Term Projects?, 2013).

Advantages and disadvantages of this method is enumerated as below-

Advantages-

This method provides the importance to time value of money.

Analysis is done by giving priority to risk and profitability. In computation, all aspects are covered.

Disadvantages-

12

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.