M6 - Corporate Projects: Business Plan & Financial Management Report

VerifiedAdded on 2023/06/10

|17

|5545

|490

Report

AI Summary

This report presents a business plan focusing on the financial management of a corporate project, specifically a dairy product manufacturing and delivery business in South Africa. It includes a capital budgeting analysis, evaluating the potential profitability of the venture for Minenhle and Bokamosos, two entrepreneurs. The report discusses various capital budgeting techniques such as net present value, payback period, and internal rate of return, applying them to assess the business's viability. It also covers the uses, effects, pros, and cons of capital budgeting. The analysis aims to determine whether investing in this business would offer sufficient returns, considering the initial investment of R 10,000,000 for setting up the plant and the projected revenues, providing a recommendation based on the financial evaluation.

Running Head: Financial management of corporate projects

1

Project Report: Financial management of corporate projects

1

Project Report: Financial management of corporate projects

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management of corporate projects 2

Contents

Introduction.......................................................................................................................3

Capital budgeting..............................................................................................................3

Types of capital budgeting............................................................................................4

Uses of capital budgeting..............................................................................................5

Effects of capital budgeting..........................................................................................5

Pros and cons of capital budgeting...............................................................................5

Business overview............................................................................................................7

Investment overview and Capital budgeting analysis......................................................8

Recommendation and Conclusion..................................................................................13

References.......................................................................................................................15

Contents

Introduction.......................................................................................................................3

Capital budgeting..............................................................................................................3

Types of capital budgeting............................................................................................4

Uses of capital budgeting..............................................................................................5

Effects of capital budgeting..........................................................................................5

Pros and cons of capital budgeting...............................................................................5

Business overview............................................................................................................7

Investment overview and Capital budgeting analysis......................................................8

Recommendation and Conclusion..................................................................................13

References.......................................................................................................................15

Financial management of corporate projects 3

Introduction:

Capital budgeting is a technique of investment proposal and appraisal which is

basically a planning process that is used by the organizations and the financial manager of a

business to analyze that whether the project or the business plan would offer the long term

returns to the business or the investment into that business would lead to the company

towards the loss (Kaplan and Atkinson, 2015). The capital budgeting techniques process

evaluates the new machinery, new business plan, expansion of the business, replacement of

the property, plant and machinery, research and development projects, new products, new

planets etc which are worth of the funding of huge cash equivalents and the cash through the

overall capital structure of the firm. It includes the equity, debt and retained earnings.

Applying the capital budgeting technique at the initial phase of a business leads to the

business owners and the executives of the business at a better way of decision making. This

process makes it easier for the business owner to make a decision about the acceptance of the

new project or not. This process explains about the allocating of the resources for the

investment or major capital or expenditure (Jiashu, 2009). One of the important goals of the

capital budgeting investment is to enhance the value of the business among the shareholders

and at the security market.

In the report, a new business has been evaluated and it has been measured that whether

the business would offer higher returns to the company or not. The new business plan

explains about a new business which would be start up by the entrepreneurs in the South

Africa. The business would be related to the manufacturing and delivering of dairy products

in the South Africa market. The case explains that the Minenhle and Bokamosos, two friends

would start this business. The report focuses on the overall cost and the revenues from the

business and measures that whether the investment into the company would be profitable for

the business or not. In the report, various techniques of the capital budgeting has been

applied on the business to measure the overall position of the business.

Capital budgeting:

Business owners and the executives of the business are always responsible for

evaluating and managing the different functions of the business. Corporate finance is also

among those tools which are applied by the financial manager of the business to conduct the

capital budgeting process on the business. Financial planning process contains the various

Introduction:

Capital budgeting is a technique of investment proposal and appraisal which is

basically a planning process that is used by the organizations and the financial manager of a

business to analyze that whether the project or the business plan would offer the long term

returns to the business or the investment into that business would lead to the company

towards the loss (Kaplan and Atkinson, 2015). The capital budgeting techniques process

evaluates the new machinery, new business plan, expansion of the business, replacement of

the property, plant and machinery, research and development projects, new products, new

planets etc which are worth of the funding of huge cash equivalents and the cash through the

overall capital structure of the firm. It includes the equity, debt and retained earnings.

Applying the capital budgeting technique at the initial phase of a business leads to the

business owners and the executives of the business at a better way of decision making. This

process makes it easier for the business owner to make a decision about the acceptance of the

new project or not. This process explains about the allocating of the resources for the

investment or major capital or expenditure (Jiashu, 2009). One of the important goals of the

capital budgeting investment is to enhance the value of the business among the shareholders

and at the security market.

In the report, a new business has been evaluated and it has been measured that whether

the business would offer higher returns to the company or not. The new business plan

explains about a new business which would be start up by the entrepreneurs in the South

Africa. The business would be related to the manufacturing and delivering of dairy products

in the South Africa market. The case explains that the Minenhle and Bokamosos, two friends

would start this business. The report focuses on the overall cost and the revenues from the

business and measures that whether the investment into the company would be profitable for

the business or not. In the report, various techniques of the capital budgeting has been

applied on the business to measure the overall position of the business.

Capital budgeting:

Business owners and the executives of the business are always responsible for

evaluating and managing the different functions of the business. Corporate finance is also

among those tools which are applied by the financial manager of the business to conduct the

capital budgeting process on the business. Financial planning process contains the various

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial management of corporate projects 4

processes which must be followed by business owners and the entrepreneurs to accomplish

the carious goals of the business (Horngren, 2009). Capital budgeting is a tool which is used

by the business to find out the profitability level of the long term investment.

Capital budgeting involves various corporate finance formulas to assess the financial

return of the business opportunities of the business. The mathematical calculations offer the

business owners about the quantitative analysis which is used on the basis of the internal and

external economical and financial data. Business owner use the corporate finance formulas to

take the guess work about the various important decisions related to the capital of the

company and the investment into that particular project. Capital budgeting could also use the

qualitative analysis which is absolutely necessary for the business owners to make a decision

about the process of the company (Hillier, Grinblatt and Titman, 2011). Qualitative analysis

is the personal judgement of the business owners and he managers about the financial

analysis.

Types of capital budgeting:

The capita budgeting tools are of various types which include the different formulas

and result about the new business and the investment proposal of the company. Mainly, the

types of the capital budgeting include net present value tool, payback period, discounted

payback period, average rate of return, internal rate of return, profitability index etc. The net

present value formula estimates the cash outflow of the business and future cash inflow of the

business in current value (Gapenski, 2008). The future cash inflows of the company are

multiplied by the present value factor of the market to identify the current profitability

position of the business.

On the other hand, the discounted payback formula estimates the cash outflow of the

business and future cash inflow of the business in current value. The future cash inflows of

the company is multiplied by the present value factor of the market to identify the total time

period in which the total invested amount in the business would be get back by the company

on the basis of the present value factor (Higgins, 2012). In addition, the payback formula

estimates the cash outflow and future cash inflow of the business. The payback period

calculations is done in which the total invested amount in the business would be get back by

the company.

Further, the internal rate of return concept briefs that the internal return of a project

must be higher than the discount rate of the company as the internal rate of return presented

processes which must be followed by business owners and the entrepreneurs to accomplish

the carious goals of the business (Horngren, 2009). Capital budgeting is a tool which is used

by the business to find out the profitability level of the long term investment.

Capital budgeting involves various corporate finance formulas to assess the financial

return of the business opportunities of the business. The mathematical calculations offer the

business owners about the quantitative analysis which is used on the basis of the internal and

external economical and financial data. Business owner use the corporate finance formulas to

take the guess work about the various important decisions related to the capital of the

company and the investment into that particular project. Capital budgeting could also use the

qualitative analysis which is absolutely necessary for the business owners to make a decision

about the process of the company (Hillier, Grinblatt and Titman, 2011). Qualitative analysis

is the personal judgement of the business owners and he managers about the financial

analysis.

Types of capital budgeting:

The capita budgeting tools are of various types which include the different formulas

and result about the new business and the investment proposal of the company. Mainly, the

types of the capital budgeting include net present value tool, payback period, discounted

payback period, average rate of return, internal rate of return, profitability index etc. The net

present value formula estimates the cash outflow of the business and future cash inflow of the

business in current value (Gapenski, 2008). The future cash inflows of the company are

multiplied by the present value factor of the market to identify the current profitability

position of the business.

On the other hand, the discounted payback formula estimates the cash outflow of the

business and future cash inflow of the business in current value. The future cash inflows of

the company is multiplied by the present value factor of the market to identify the total time

period in which the total invested amount in the business would be get back by the company

on the basis of the present value factor (Higgins, 2012). In addition, the payback formula

estimates the cash outflow and future cash inflow of the business. The payback period

calculations is done in which the total invested amount in the business would be get back by

the company.

Further, the internal rate of return concept briefs that the internal return of a project

must be higher than the discount rate of the company as the internal rate of return presented

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management of corporate projects 5

about the total return from the project and the discount rate explains about the total cost of the

company firm. In addition, the profitability index and the accounting rate of return tools also

explain about the associated profit of a project.

These tools help the company to make different outcomes about the project and the

performance.

Uses of capital budgeting:

Capital budgeting process and the financial process of an organization works in a cycle.

As some rules and the goals and objectives are set by the business owners and the financial

managers to meet, they use the qualitative and quantitative analysis to measure the

performance and the make the business decisions. The tools of the capital budgeting offers

the requisite analysis information about the objectives and the goals of the business in the

process of financial planning and set up a new business (Ross et al, 2007). business owners

combines all the business management method in the business in order to ensure that the

business owners evaluate the financial return of the business decisions rather than accepting

the opportunities in order to sake the growth and the potential increment in the business.

Effects of capital budgeting:

The capital budgeting process is used by the owners of the business and the financial

manager to obtain the funds from the banks and the investors of the company. These tools are

use by the companies in making various decisions about the capital structure, source of

finance, investment into the project etc. these tools help the small business, medium capital

business and the large business to make decision about various financial related issues of the

business. It evaluates all the related expenses and the revenue of the business to measure the

overall performance and the position of the business (Ross et al, 2008).

Pros and cons of capital budgeting:

Capital budgeting is an important process as it creates the measurability and the

accountability of the business. Any business which seeks to invest into project in order to

enhance the investment amount and the return without evaluating the risk and return factor of

the business could lead to the investment at a wrong way. The importance of the capital

budgeting is as follows:

Capita budgeting helps a business to develop and formulas the long term objectives and

the strategic goals of the business. The capital budgeting process measure the overall

about the total return from the project and the discount rate explains about the total cost of the

company firm. In addition, the profitability index and the accounting rate of return tools also

explain about the associated profit of a project.

These tools help the company to make different outcomes about the project and the

performance.

Uses of capital budgeting:

Capital budgeting process and the financial process of an organization works in a cycle.

As some rules and the goals and objectives are set by the business owners and the financial

managers to meet, they use the qualitative and quantitative analysis to measure the

performance and the make the business decisions. The tools of the capital budgeting offers

the requisite analysis information about the objectives and the goals of the business in the

process of financial planning and set up a new business (Ross et al, 2007). business owners

combines all the business management method in the business in order to ensure that the

business owners evaluate the financial return of the business decisions rather than accepting

the opportunities in order to sake the growth and the potential increment in the business.

Effects of capital budgeting:

The capital budgeting process is used by the owners of the business and the financial

manager to obtain the funds from the banks and the investors of the company. These tools are

use by the companies in making various decisions about the capital structure, source of

finance, investment into the project etc. these tools help the small business, medium capital

business and the large business to make decision about various financial related issues of the

business. It evaluates all the related expenses and the revenue of the business to measure the

overall performance and the position of the business (Ross et al, 2008).

Pros and cons of capital budgeting:

Capital budgeting is an important process as it creates the measurability and the

accountability of the business. Any business which seeks to invest into project in order to

enhance the investment amount and the return without evaluating the risk and return factor of

the business could lead to the investment at a wrong way. The importance of the capital

budgeting is as follows:

Capita budgeting helps a business to develop and formulas the long term objectives and

the strategic goals of the business. The capital budgeting process measure the overall

Financial management of corporate projects 6

performance of the business plan and offer a base to the business owners to make an

idea about the goals and the objectives of the business (Barlow, 2006).

Capital budgeting process evaluates that what would be the profitability level of the

business and how much would it take to the business to get back the amount which

has been invested in the project.

It estimates all the cash outflows and future cash inflows of the company to measure the

overall financial performance of the company.

It facilitates the communication of the required information about the business plan to

the related parties (Reilly and Brown, 2011).

It controls and monitors the overall expenditure and the income of the company to

measure the overall performance of the business.

It is one of the better tools of the corporate finance which offers a base to the business

owners to make a decision about the financial performance of the company.

Further, the disadvantages of the business have also been measured to identify the

related cons of the capital budgeting process of the business. The drawbacks of the capital

budgeting process are as follows:

All the capital budgeting techniques presume that numerous investment proposal under

the consideration are usually exclusive that might not be true on the practical scenario

in some particular situation of the business.

Urgency is also a limitation of the capital budgeting process and the decision making

process of the business (Radebaugh, Gray and Black, 2006).

Capital budgeting techniques require future cash outflow and inflow estimation.

However, the future is always certain and the data collected for the future cannot be

certain. So, it is obvious that the data collected in reference with the future cash

inflow are not correct.

Further, uncertainty and the risk position of the business is also one of the biggest

limitations of the capital budgeting techniques.

There are few other factors of the business as well such as the employees morale, firm’s

good will etc that could not be correctly quantified but it otherwise substantially

performance of the business plan and offer a base to the business owners to make an

idea about the goals and the objectives of the business (Barlow, 2006).

Capital budgeting process evaluates that what would be the profitability level of the

business and how much would it take to the business to get back the amount which

has been invested in the project.

It estimates all the cash outflows and future cash inflows of the company to measure the

overall financial performance of the company.

It facilitates the communication of the required information about the business plan to

the related parties (Reilly and Brown, 2011).

It controls and monitors the overall expenditure and the income of the company to

measure the overall performance of the business.

It is one of the better tools of the corporate finance which offers a base to the business

owners to make a decision about the financial performance of the company.

Further, the disadvantages of the business have also been measured to identify the

related cons of the capital budgeting process of the business. The drawbacks of the capital

budgeting process are as follows:

All the capital budgeting techniques presume that numerous investment proposal under

the consideration are usually exclusive that might not be true on the practical scenario

in some particular situation of the business.

Urgency is also a limitation of the capital budgeting process and the decision making

process of the business (Radebaugh, Gray and Black, 2006).

Capital budgeting techniques require future cash outflow and inflow estimation.

However, the future is always certain and the data collected for the future cannot be

certain. So, it is obvious that the data collected in reference with the future cash

inflow are not correct.

Further, uncertainty and the risk position of the business is also one of the biggest

limitations of the capital budgeting techniques.

There are few other factors of the business as well such as the employees morale, firm’s

good will etc that could not be correctly quantified but it otherwise substantially

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial management of corporate projects 7

influence the decision making process and the capital decision of the business

(Phillips and Stawarski, 2016).

On the basis of the overall evaluation on the capital budgeting, it has been measured

that the capital budgeting is one of the finest tool to measure the overall performance of the

business. Capital budgeting involves various corporate finance formulas to assess the

financial return of the business opportunities of the business. The mathematical calculations

offer the business owners about the quantitative analysis which is used on the basis of the

internal and external economical and financial data.

Business owners and the executives of the business are always responsible for

evaluating and managing the different functions of the business. Capital budgeting is also

among those tools which are applied by the financial manager of the business to conduct the

capital budgeting process on the business (Peterson and Fabozzi, 2002). Financial planning

process contains the various processes which must be followed by business owners and the

entrepreneurs to accomplish the carious goals of the business. The study explains that the

entire related factor must be evaluated by the business after analyzing and measuring all the

related factors of the business so that a better analysis could be done and a better decision

could be made for the business.

Business overview:

Minenhle and Bokamosos are the two friends. Both of them are working in the South

Africa market from last 10 years and now they have decided to quit the job and open their

own business. They would start a new business in the market. The new business plan explains

about a business which would be start up by the entrepreneurs in the South Africa. The

business would be related to the manufacturing and delivering of dairy products in the South

Africa market.

The case mainly explains that for starting the business, they have to set up a plant for

the production of the dairy products. The cost of the new plant of the business would be R

10,000,000. It further explains that the plant would be run for the 5 years. For running the

operations at the plant, working capital worth 15,00,000 would be required by the business.

Further, it has been found that the total sales units of the product would be 100000 in first

year which would rise by 10% in next 2 years and after the 3rd year, the sales unit of the

influence the decision making process and the capital decision of the business

(Phillips and Stawarski, 2016).

On the basis of the overall evaluation on the capital budgeting, it has been measured

that the capital budgeting is one of the finest tool to measure the overall performance of the

business. Capital budgeting involves various corporate finance formulas to assess the

financial return of the business opportunities of the business. The mathematical calculations

offer the business owners about the quantitative analysis which is used on the basis of the

internal and external economical and financial data.

Business owners and the executives of the business are always responsible for

evaluating and managing the different functions of the business. Capital budgeting is also

among those tools which are applied by the financial manager of the business to conduct the

capital budgeting process on the business (Peterson and Fabozzi, 2002). Financial planning

process contains the various processes which must be followed by business owners and the

entrepreneurs to accomplish the carious goals of the business. The study explains that the

entire related factor must be evaluated by the business after analyzing and measuring all the

related factors of the business so that a better analysis could be done and a better decision

could be made for the business.

Business overview:

Minenhle and Bokamosos are the two friends. Both of them are working in the South

Africa market from last 10 years and now they have decided to quit the job and open their

own business. They would start a new business in the market. The new business plan explains

about a business which would be start up by the entrepreneurs in the South Africa. The

business would be related to the manufacturing and delivering of dairy products in the South

Africa market.

The case mainly explains that for starting the business, they have to set up a plant for

the production of the dairy products. The cost of the new plant of the business would be R

10,000,000. It further explains that the plant would be run for the 5 years. For running the

operations at the plant, working capital worth 15,00,000 would be required by the business.

Further, it has been found that the total sales units of the product would be 100000 in first

year which would rise by 10% in next 2 years and after the 3rd year, the sales unit of the

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management of corporate projects 8

company would be lowered by 15%. The sales price of the project would be 100 which

would rise by 4% in each of the year.

It has also been measured that the installation cost of the plant would be 10000 and the

expenses of the production of the company would be 50% of the total revenue of the

business. The operating cost of the business would be R 1500000 in initial year which would

be increased by 3% each year. Further, it has been measured that the depreciation has been

charged on the plant on the basis of straight line method. The taxes of the company would be

30%. The life time of the project is 5 years. The discount rate of the business would be 15%.

The plant would have no scarp value after 5 years and the overall position of the company

would be lower by that time.

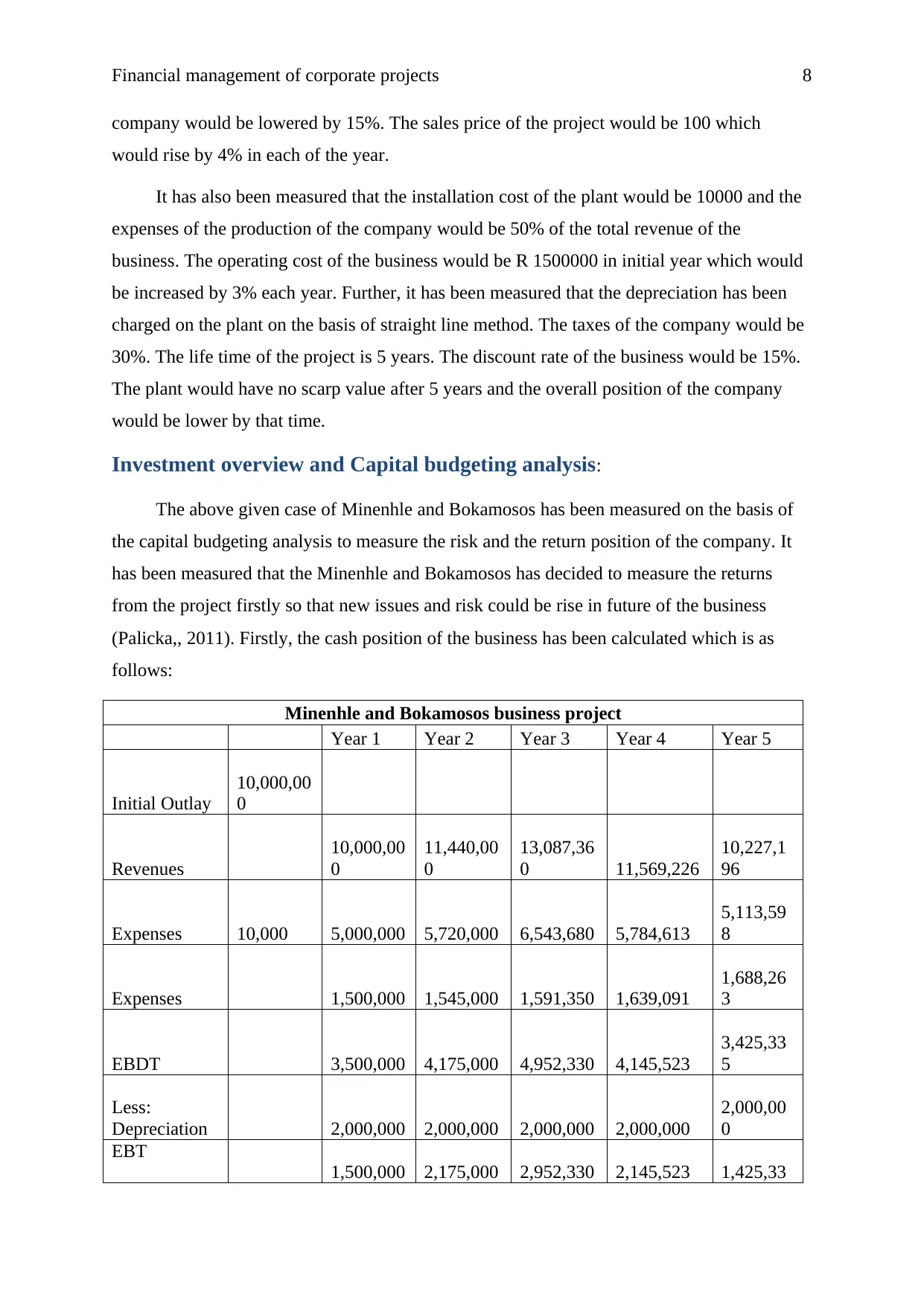

Investment overview and Capital budgeting analysis:

The above given case of Minenhle and Bokamosos has been measured on the basis of

the capital budgeting analysis to measure the risk and the return position of the company. It

has been measured that the Minenhle and Bokamosos has decided to measure the returns

from the project firstly so that new issues and risk could be rise in future of the business

(Palicka,, 2011). Firstly, the cash position of the business has been calculated which is as

follows:

Minenhle and Bokamosos business project

Year 1 Year 2 Year 3 Year 4 Year 5

Initial Outlay

10,000,00

0

Revenues

10,000,00

0

11,440,00

0

13,087,36

0 11,569,226

10,227,1

96

Expenses 10,000 5,000,000 5,720,000 6,543,680 5,784,613

5,113,59

8

Expenses 1,500,000 1,545,000 1,591,350 1,639,091

1,688,26

3

EBDT 3,500,000 4,175,000 4,952,330 4,145,523

3,425,33

5

Less:

Depreciation 2,000,000 2,000,000 2,000,000 2,000,000

2,000,00

0

EBT

1,500,000 2,175,000 2,952,330 2,145,523 1,425,33

company would be lowered by 15%. The sales price of the project would be 100 which

would rise by 4% in each of the year.

It has also been measured that the installation cost of the plant would be 10000 and the

expenses of the production of the company would be 50% of the total revenue of the

business. The operating cost of the business would be R 1500000 in initial year which would

be increased by 3% each year. Further, it has been measured that the depreciation has been

charged on the plant on the basis of straight line method. The taxes of the company would be

30%. The life time of the project is 5 years. The discount rate of the business would be 15%.

The plant would have no scarp value after 5 years and the overall position of the company

would be lower by that time.

Investment overview and Capital budgeting analysis:

The above given case of Minenhle and Bokamosos has been measured on the basis of

the capital budgeting analysis to measure the risk and the return position of the company. It

has been measured that the Minenhle and Bokamosos has decided to measure the returns

from the project firstly so that new issues and risk could be rise in future of the business

(Palicka,, 2011). Firstly, the cash position of the business has been calculated which is as

follows:

Minenhle and Bokamosos business project

Year 1 Year 2 Year 3 Year 4 Year 5

Initial Outlay

10,000,00

0

Revenues

10,000,00

0

11,440,00

0

13,087,36

0 11,569,226

10,227,1

96

Expenses 10,000 5,000,000 5,720,000 6,543,680 5,784,613

5,113,59

8

Expenses 1,500,000 1,545,000 1,591,350 1,639,091

1,688,26

3

EBDT 3,500,000 4,175,000 4,952,330 4,145,523

3,425,33

5

Less:

Depreciation 2,000,000 2,000,000 2,000,000 2,000,000

2,000,00

0

EBT

1,500,000 2,175,000 2,952,330 2,145,523 1,425,33

Financial management of corporate projects 9

5

Less: Taxes 450,000 652,500 885,699 643,657 427,600

EAT 1,050,000 1,522,500 2,066,631 1,501,866 997,734

ADD:

Depreciation 2,000,000 2,000,000 2,000,000 2,000,000

2,000,00

0

cash flow

17,138,73

1 3,050,000 3,522,500 4,066,631 3,501,866

2,997,73

4

Changes in

Working

capital 1,500,000

1,500,00

0

Total cash

flow 5,628,731

4,497,73

4

Working Note:

Sales unit 100000 110000 121000 102850 87422.5

Sales price

R

100.00

R

104.00

R

108.16

R

112.49

R

116.99

Revenue

R

10,000,00

0.00

R

11,440,00

0.00

R

13,087,36

0.00

R

11,569,226.

24

R

10,227,1

96.00

(Zimmerman and Yahya-Zadeh, 2011)

Cash flow analysis is an examination on the cash outflows and inflows of a project or a

business in a particular time period. The analysis starts from the opening balance of the cash

position of the company which leads to the ending cash position of the business. The cash

flow analysis is mostly used by the businesses to make financial decisions (Ward, 2012). On

the basis of the cash flow analysis of the business, it has been measured that overall revenue

of the business would be enhanced in next 5 years as well as the total cash flow position of

the business would be better and would be managed by the business in such a manner that

better study could be performed in the business.

After that, net present value of the business plan has been calculated. The net present

value tool estimates the cash outflow of the business and future cash inflow of the business in

current value (Zabarankin, Pavlikov and Uryasev, 2014). The future cash inflows of the

company are multiplied by the present value factor of the market to identify the current

profitability position of the business. It measures the overall profitability position of the

5

Less: Taxes 450,000 652,500 885,699 643,657 427,600

EAT 1,050,000 1,522,500 2,066,631 1,501,866 997,734

ADD:

Depreciation 2,000,000 2,000,000 2,000,000 2,000,000

2,000,00

0

cash flow

17,138,73

1 3,050,000 3,522,500 4,066,631 3,501,866

2,997,73

4

Changes in

Working

capital 1,500,000

1,500,00

0

Total cash

flow 5,628,731

4,497,73

4

Working Note:

Sales unit 100000 110000 121000 102850 87422.5

Sales price

R

100.00

R

104.00

R

108.16

R

112.49

R

116.99

Revenue

R

10,000,00

0.00

R

11,440,00

0.00

R

13,087,36

0.00

R

11,569,226.

24

R

10,227,1

96.00

(Zimmerman and Yahya-Zadeh, 2011)

Cash flow analysis is an examination on the cash outflows and inflows of a project or a

business in a particular time period. The analysis starts from the opening balance of the cash

position of the company which leads to the ending cash position of the business. The cash

flow analysis is mostly used by the businesses to make financial decisions (Ward, 2012). On

the basis of the cash flow analysis of the business, it has been measured that overall revenue

of the business would be enhanced in next 5 years as well as the total cash flow position of

the business would be better and would be managed by the business in such a manner that

better study could be performed in the business.

After that, net present value of the business plan has been calculated. The net present

value tool estimates the cash outflow of the business and future cash inflow of the business in

current value (Zabarankin, Pavlikov and Uryasev, 2014). The future cash inflows of the

company are multiplied by the present value factor of the market to identify the current

profitability position of the business. It measures the overall profitability position of the

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Financial management of corporate projects 10

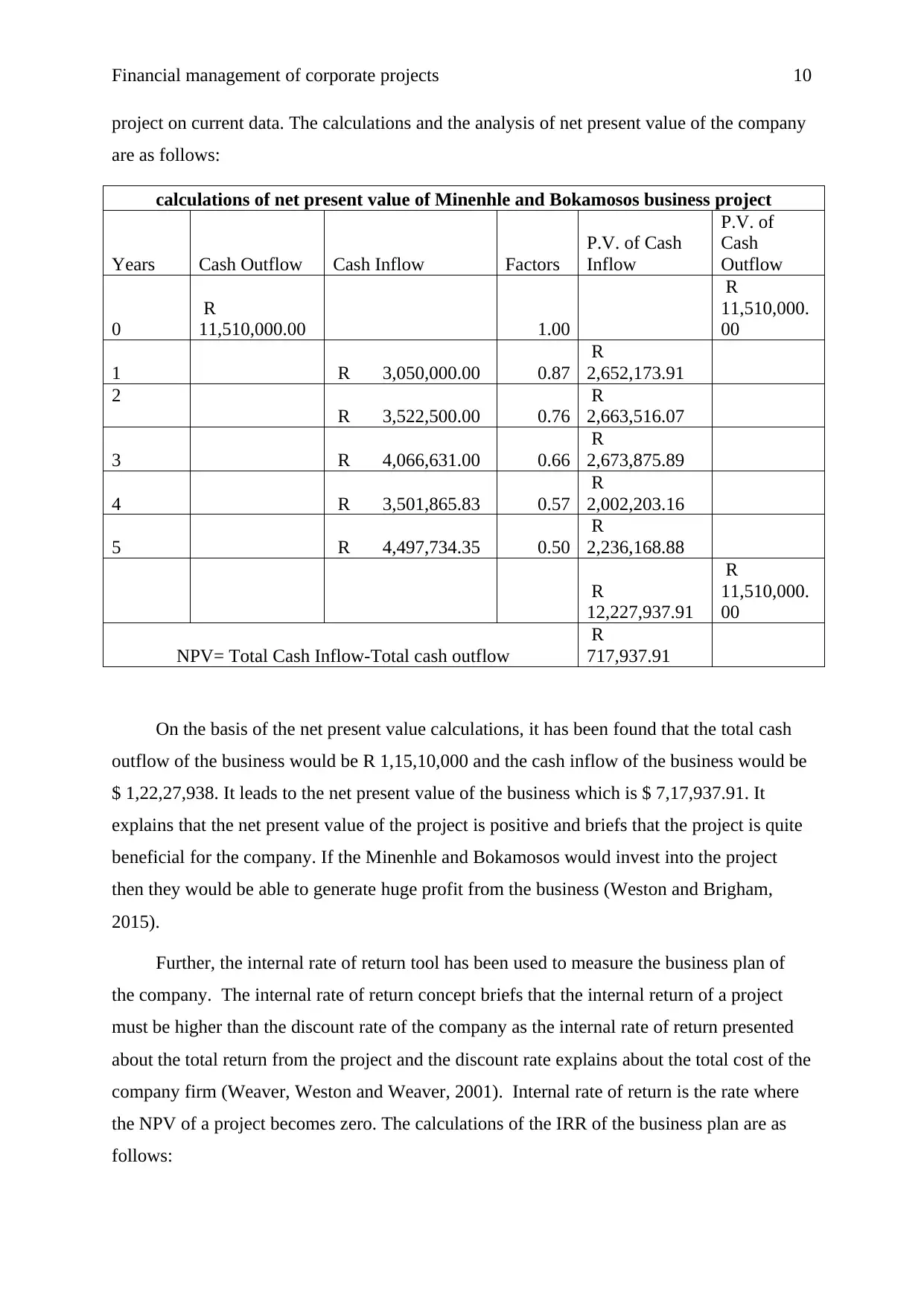

project on current data. The calculations and the analysis of net present value of the company

are as follows:

calculations of net present value of Minenhle and Bokamosos business project

Years Cash Outflow Cash Inflow Factors

P.V. of Cash

Inflow

P.V. of

Cash

Outflow

0

R

11,510,000.00 1.00

R

11,510,000.

00

1 R 3,050,000.00 0.87

R

2,652,173.91

2

R 3,522,500.00 0.76

R

2,663,516.07

3 R 4,066,631.00 0.66

R

2,673,875.89

4 R 3,501,865.83 0.57

R

2,002,203.16

5 R 4,497,734.35 0.50

R

2,236,168.88

R

12,227,937.91

R

11,510,000.

00

NPV= Total Cash Inflow-Total cash outflow

R

717,937.91

On the basis of the net present value calculations, it has been found that the total cash

outflow of the business would be R 1,15,10,000 and the cash inflow of the business would be

$ 1,22,27,938. It leads to the net present value of the business which is $ 7,17,937.91. It

explains that the net present value of the project is positive and briefs that the project is quite

beneficial for the company. If the Minenhle and Bokamosos would invest into the project

then they would be able to generate huge profit from the business (Weston and Brigham,

2015).

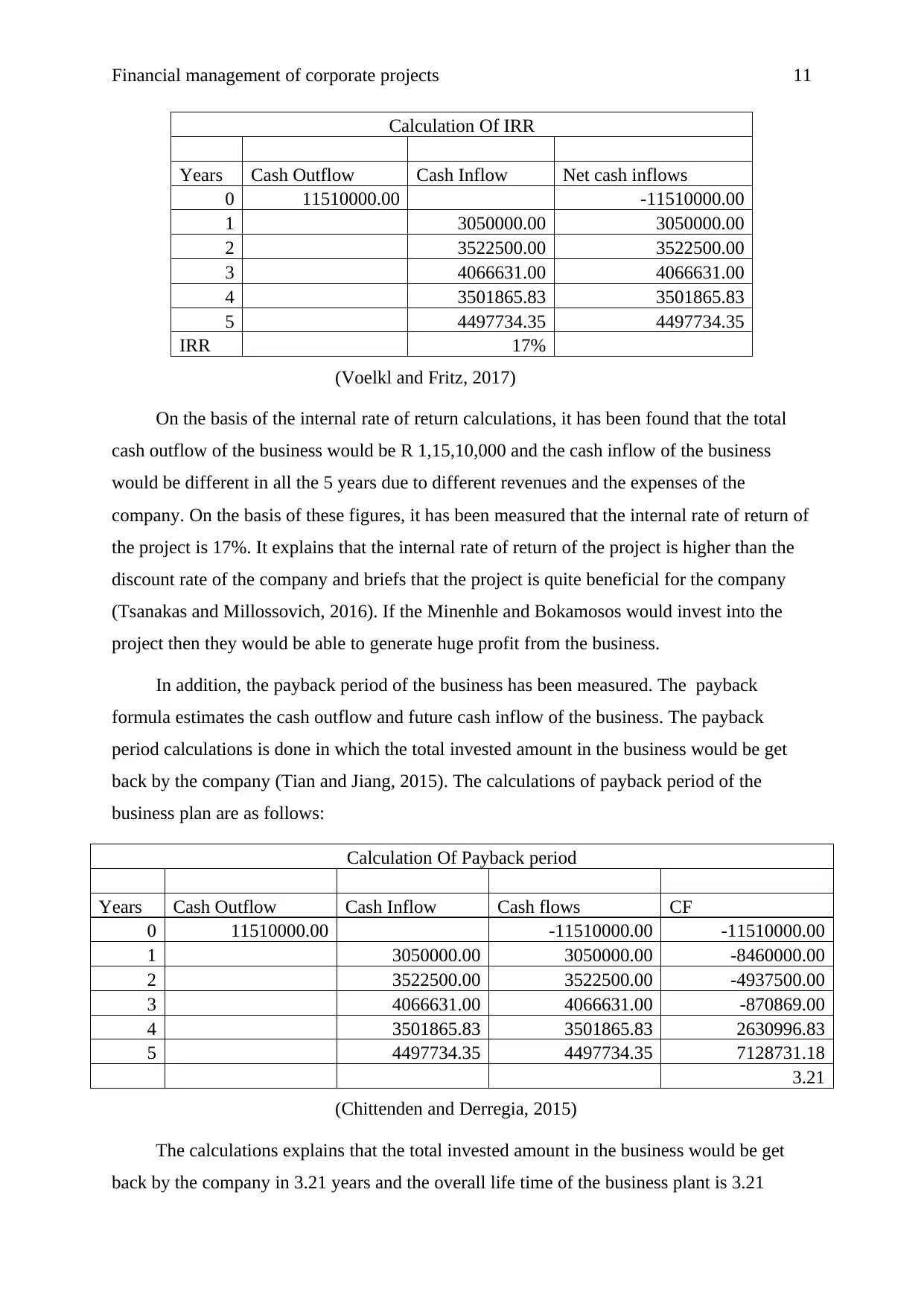

Further, the internal rate of return tool has been used to measure the business plan of

the company. The internal rate of return concept briefs that the internal return of a project

must be higher than the discount rate of the company as the internal rate of return presented

about the total return from the project and the discount rate explains about the total cost of the

company firm (Weaver, Weston and Weaver, 2001). Internal rate of return is the rate where

the NPV of a project becomes zero. The calculations of the IRR of the business plan are as

follows:

project on current data. The calculations and the analysis of net present value of the company

are as follows:

calculations of net present value of Minenhle and Bokamosos business project

Years Cash Outflow Cash Inflow Factors

P.V. of Cash

Inflow

P.V. of

Cash

Outflow

0

R

11,510,000.00 1.00

R

11,510,000.

00

1 R 3,050,000.00 0.87

R

2,652,173.91

2

R 3,522,500.00 0.76

R

2,663,516.07

3 R 4,066,631.00 0.66

R

2,673,875.89

4 R 3,501,865.83 0.57

R

2,002,203.16

5 R 4,497,734.35 0.50

R

2,236,168.88

R

12,227,937.91

R

11,510,000.

00

NPV= Total Cash Inflow-Total cash outflow

R

717,937.91

On the basis of the net present value calculations, it has been found that the total cash

outflow of the business would be R 1,15,10,000 and the cash inflow of the business would be

$ 1,22,27,938. It leads to the net present value of the business which is $ 7,17,937.91. It

explains that the net present value of the project is positive and briefs that the project is quite

beneficial for the company. If the Minenhle and Bokamosos would invest into the project

then they would be able to generate huge profit from the business (Weston and Brigham,

2015).

Further, the internal rate of return tool has been used to measure the business plan of

the company. The internal rate of return concept briefs that the internal return of a project

must be higher than the discount rate of the company as the internal rate of return presented

about the total return from the project and the discount rate explains about the total cost of the

company firm (Weaver, Weston and Weaver, 2001). Internal rate of return is the rate where

the NPV of a project becomes zero. The calculations of the IRR of the business plan are as

follows:

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Financial management of corporate projects 11

Calculation Of IRR

Years Cash Outflow Cash Inflow Net cash inflows

0 11510000.00 -11510000.00

1 3050000.00 3050000.00

2 3522500.00 3522500.00

3 4066631.00 4066631.00

4 3501865.83 3501865.83

5 4497734.35 4497734.35

IRR 17%

(Voelkl and Fritz, 2017)

On the basis of the internal rate of return calculations, it has been found that the total

cash outflow of the business would be R 1,15,10,000 and the cash inflow of the business

would be different in all the 5 years due to different revenues and the expenses of the

company. On the basis of these figures, it has been measured that the internal rate of return of

the project is 17%. It explains that the internal rate of return of the project is higher than the

discount rate of the company and briefs that the project is quite beneficial for the company

(Tsanakas and Millossovich, 2016). If the Minenhle and Bokamosos would invest into the

project then they would be able to generate huge profit from the business.

In addition, the payback period of the business has been measured. The payback

formula estimates the cash outflow and future cash inflow of the business. The payback

period calculations is done in which the total invested amount in the business would be get

back by the company (Tian and Jiang, 2015). The calculations of payback period of the

business plan are as follows:

Calculation Of Payback period

Years Cash Outflow Cash Inflow Cash flows CF

0 11510000.00 -11510000.00 -11510000.00

1 3050000.00 3050000.00 -8460000.00

2 3522500.00 3522500.00 -4937500.00

3 4066631.00 4066631.00 -870869.00

4 3501865.83 3501865.83 2630996.83

5 4497734.35 4497734.35 7128731.18

3.21

(Chittenden and Derregia, 2015)

The calculations explains that the total invested amount in the business would be get

back by the company in 3.21 years and the overall life time of the business plant is 3.21

Calculation Of IRR

Years Cash Outflow Cash Inflow Net cash inflows

0 11510000.00 -11510000.00

1 3050000.00 3050000.00

2 3522500.00 3522500.00

3 4066631.00 4066631.00

4 3501865.83 3501865.83

5 4497734.35 4497734.35

IRR 17%

(Voelkl and Fritz, 2017)

On the basis of the internal rate of return calculations, it has been found that the total

cash outflow of the business would be R 1,15,10,000 and the cash inflow of the business

would be different in all the 5 years due to different revenues and the expenses of the

company. On the basis of these figures, it has been measured that the internal rate of return of

the project is 17%. It explains that the internal rate of return of the project is higher than the

discount rate of the company and briefs that the project is quite beneficial for the company

(Tsanakas and Millossovich, 2016). If the Minenhle and Bokamosos would invest into the

project then they would be able to generate huge profit from the business.

In addition, the payback period of the business has been measured. The payback

formula estimates the cash outflow and future cash inflow of the business. The payback

period calculations is done in which the total invested amount in the business would be get

back by the company (Tian and Jiang, 2015). The calculations of payback period of the

business plan are as follows:

Calculation Of Payback period

Years Cash Outflow Cash Inflow Cash flows CF

0 11510000.00 -11510000.00 -11510000.00

1 3050000.00 3050000.00 -8460000.00

2 3522500.00 3522500.00 -4937500.00

3 4066631.00 4066631.00 -870869.00

4 3501865.83 3501865.83 2630996.83

5 4497734.35 4497734.35 7128731.18

3.21

(Chittenden and Derregia, 2015)

The calculations explains that the total invested amount in the business would be get

back by the company in 3.21 years and the overall life time of the business plant is 3.21

Financial management of corporate projects 12

years. It explains that the amount would be got back by the company within the life time of

the machinery and thus it is a better choice for the purpose of investment (Burns and Walker,

2015).

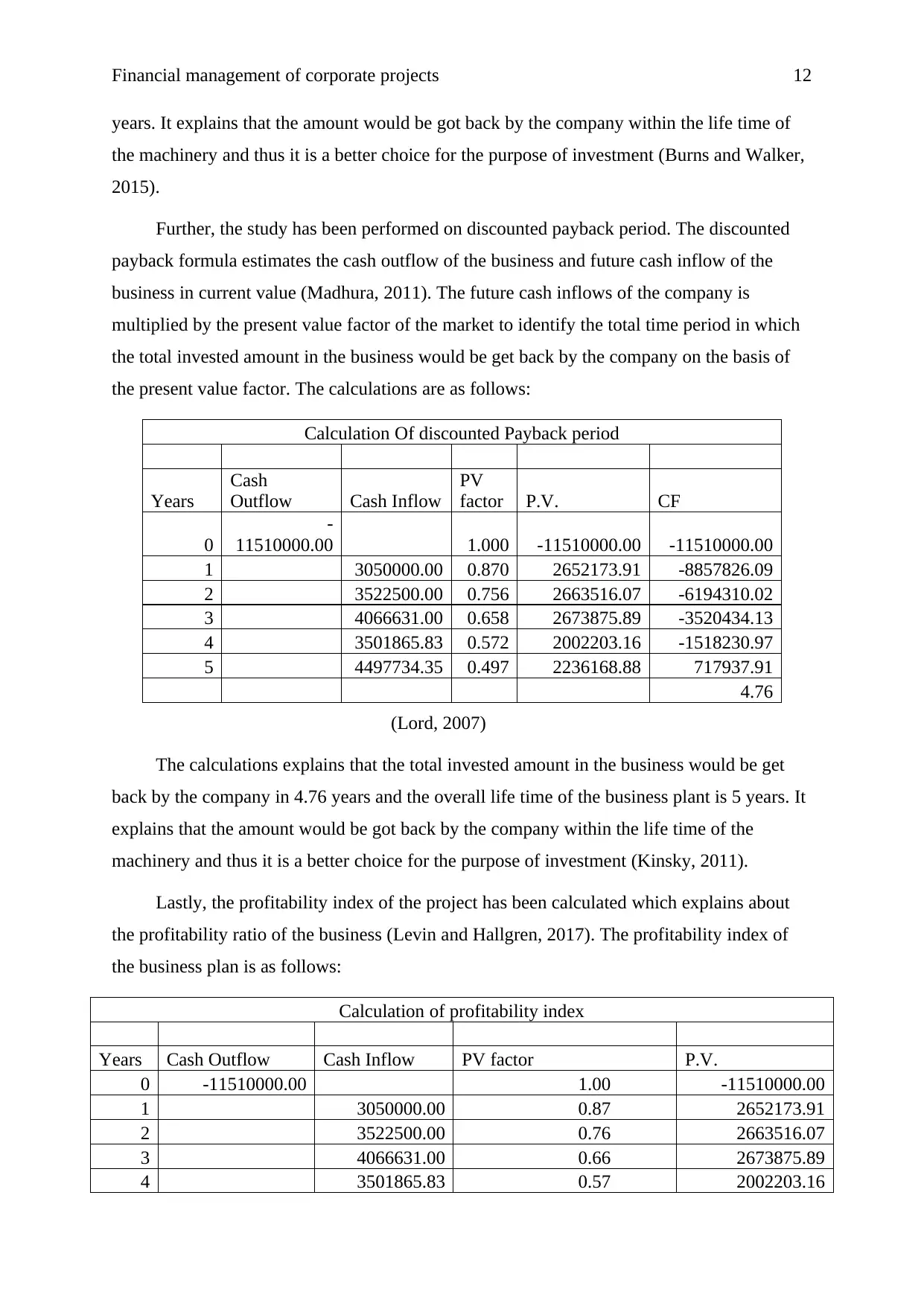

Further, the study has been performed on discounted payback period. The discounted

payback formula estimates the cash outflow of the business and future cash inflow of the

business in current value (Madhura, 2011). The future cash inflows of the company is

multiplied by the present value factor of the market to identify the total time period in which

the total invested amount in the business would be get back by the company on the basis of

the present value factor. The calculations are as follows:

Calculation Of discounted Payback period

Years

Cash

Outflow Cash Inflow

PV

factor P.V. CF

0

-

11510000.00 1.000 -11510000.00 -11510000.00

1 3050000.00 0.870 2652173.91 -8857826.09

2 3522500.00 0.756 2663516.07 -6194310.02

3 4066631.00 0.658 2673875.89 -3520434.13

4 3501865.83 0.572 2002203.16 -1518230.97

5 4497734.35 0.497 2236168.88 717937.91

4.76

(Lord, 2007)

The calculations explains that the total invested amount in the business would be get

back by the company in 4.76 years and the overall life time of the business plant is 5 years. It

explains that the amount would be got back by the company within the life time of the

machinery and thus it is a better choice for the purpose of investment (Kinsky, 2011).

Lastly, the profitability index of the project has been calculated which explains about

the profitability ratio of the business (Levin and Hallgren, 2017). The profitability index of

the business plan is as follows:

Calculation of profitability index

Years Cash Outflow Cash Inflow PV factor P.V.

0 -11510000.00 1.00 -11510000.00

1 3050000.00 0.87 2652173.91

2 3522500.00 0.76 2663516.07

3 4066631.00 0.66 2673875.89

4 3501865.83 0.57 2002203.16

years. It explains that the amount would be got back by the company within the life time of

the machinery and thus it is a better choice for the purpose of investment (Burns and Walker,

2015).

Further, the study has been performed on discounted payback period. The discounted

payback formula estimates the cash outflow of the business and future cash inflow of the

business in current value (Madhura, 2011). The future cash inflows of the company is

multiplied by the present value factor of the market to identify the total time period in which

the total invested amount in the business would be get back by the company on the basis of

the present value factor. The calculations are as follows:

Calculation Of discounted Payback period

Years

Cash

Outflow Cash Inflow

PV

factor P.V. CF

0

-

11510000.00 1.000 -11510000.00 -11510000.00

1 3050000.00 0.870 2652173.91 -8857826.09

2 3522500.00 0.756 2663516.07 -6194310.02

3 4066631.00 0.658 2673875.89 -3520434.13

4 3501865.83 0.572 2002203.16 -1518230.97

5 4497734.35 0.497 2236168.88 717937.91

4.76

(Lord, 2007)

The calculations explains that the total invested amount in the business would be get

back by the company in 4.76 years and the overall life time of the business plant is 5 years. It

explains that the amount would be got back by the company within the life time of the

machinery and thus it is a better choice for the purpose of investment (Kinsky, 2011).

Lastly, the profitability index of the project has been calculated which explains about

the profitability ratio of the business (Levin and Hallgren, 2017). The profitability index of

the business plan is as follows:

Calculation of profitability index

Years Cash Outflow Cash Inflow PV factor P.V.

0 -11510000.00 1.00 -11510000.00

1 3050000.00 0.87 2652173.91

2 3522500.00 0.76 2663516.07

3 4066631.00 0.66 2673875.89

4 3501865.83 0.57 2002203.16

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 17

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.