Financial Management Project: Highsky Company, Cost of Capital

VerifiedAdded on 2023/06/05

|16

|2391

|346

Project

AI Summary

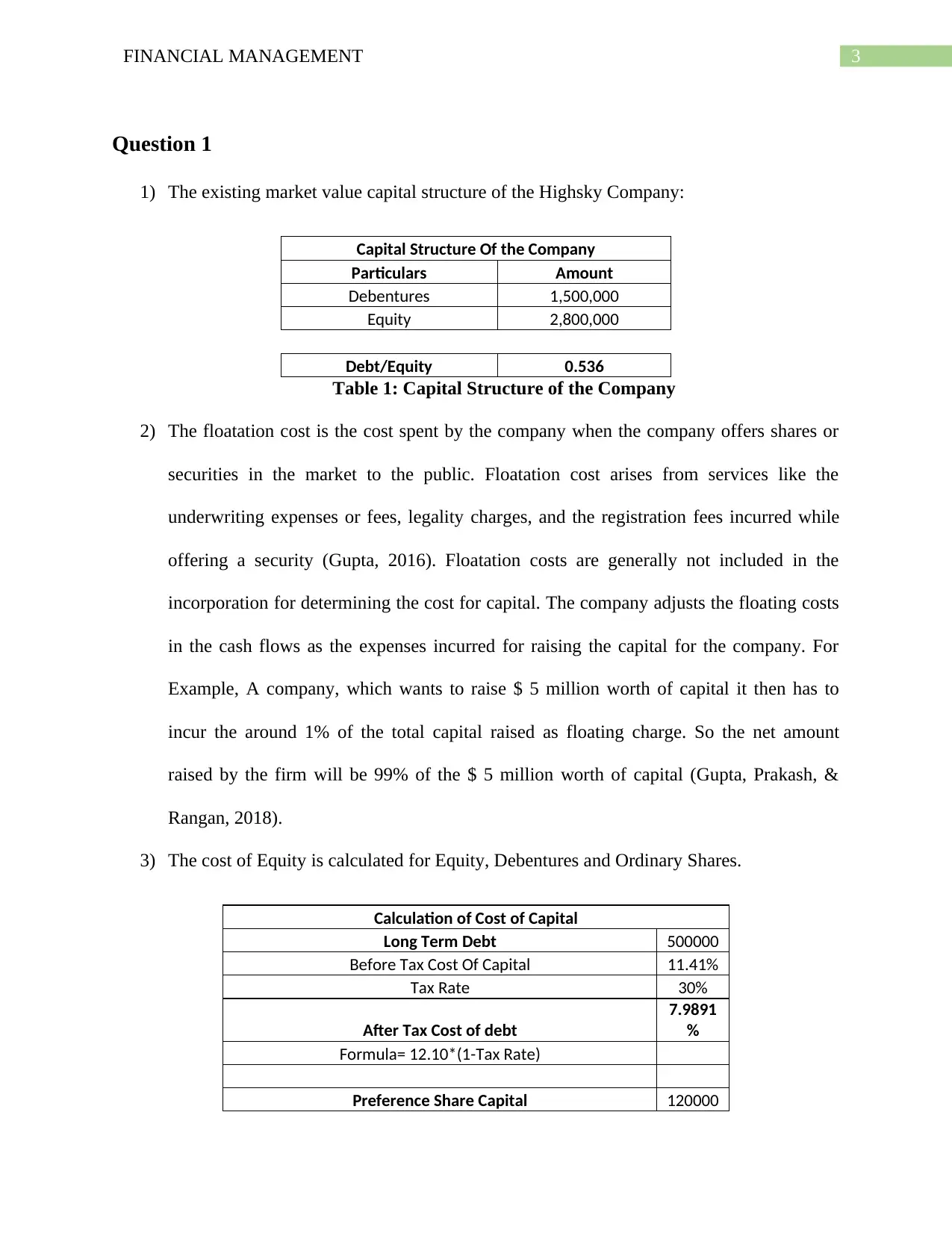

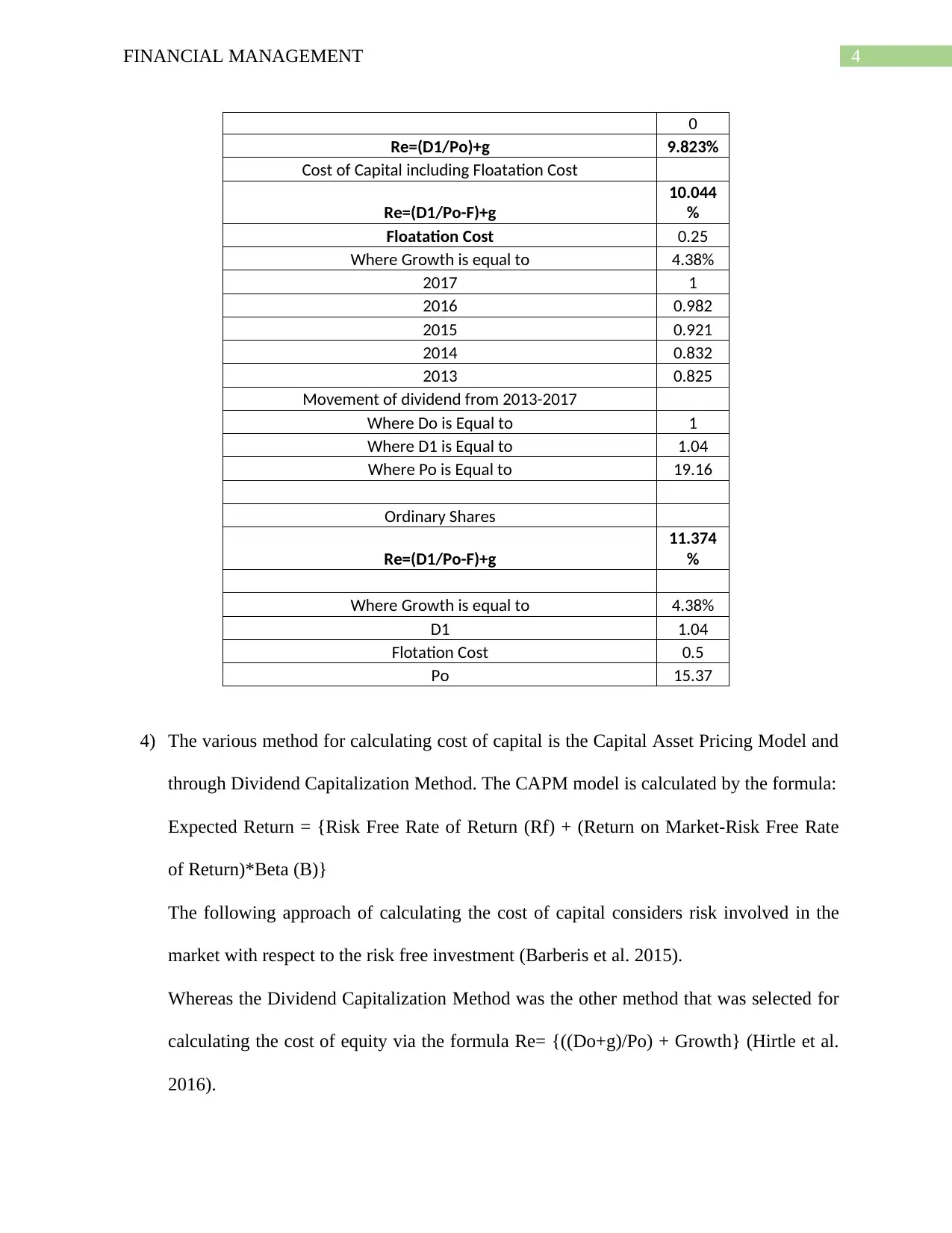

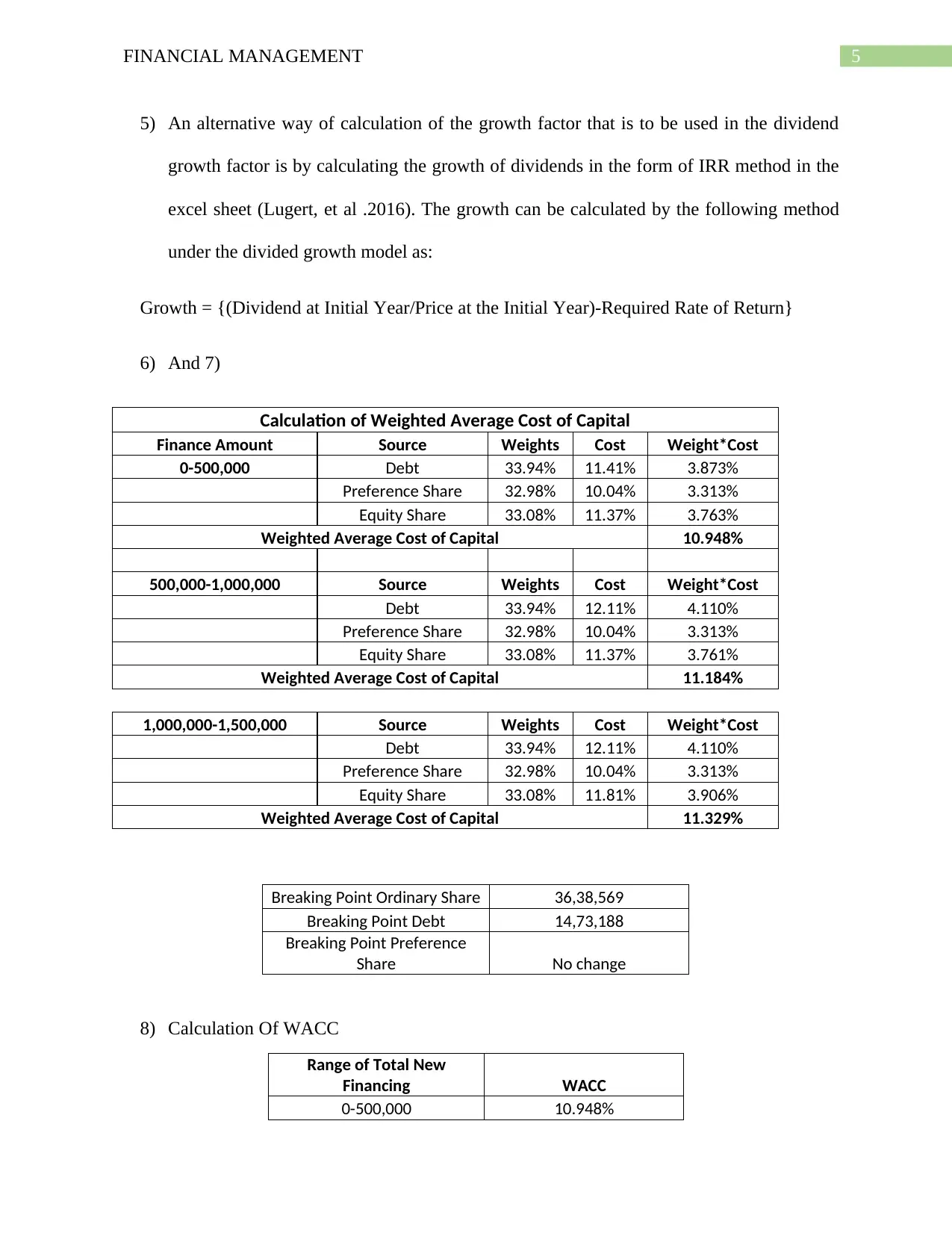

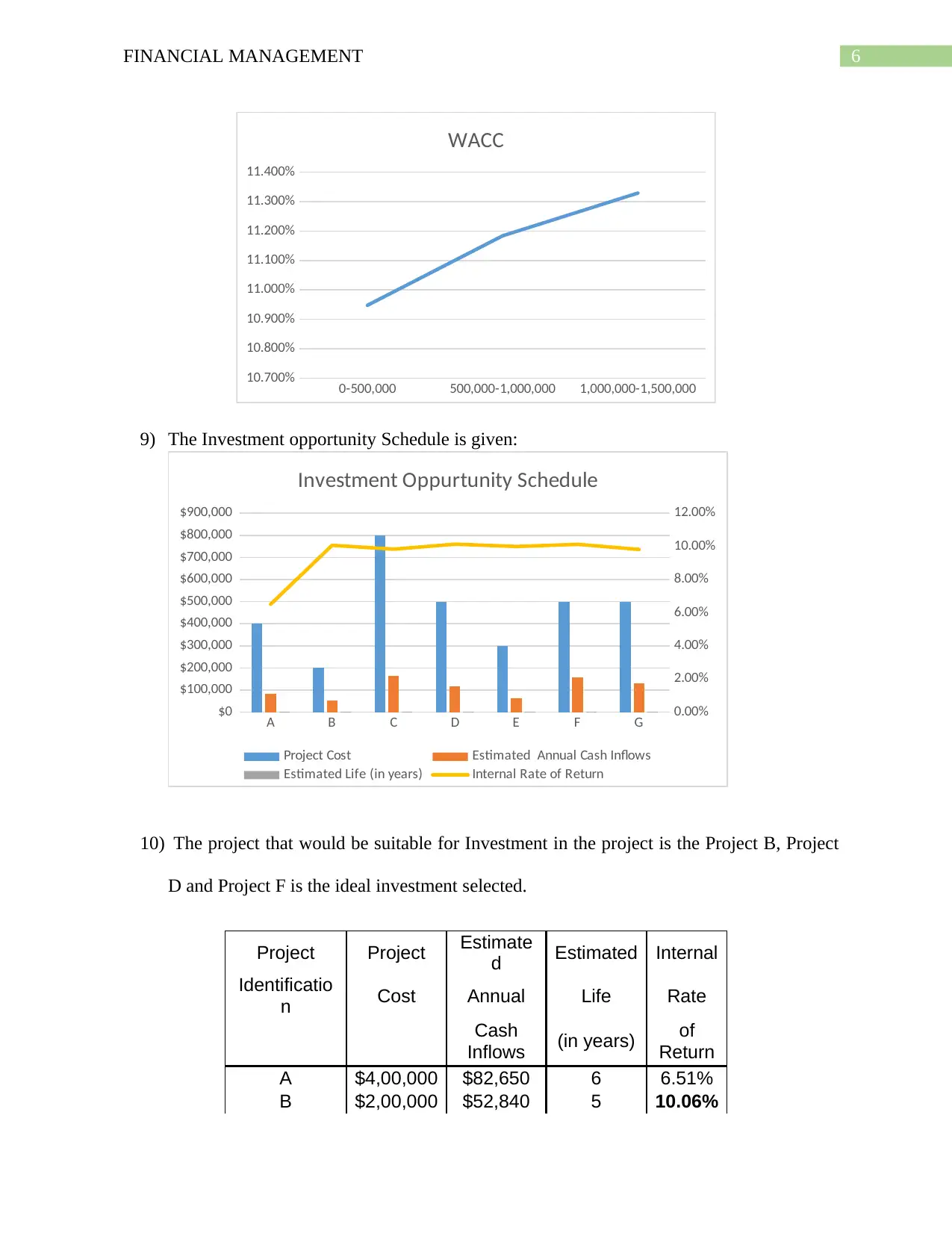

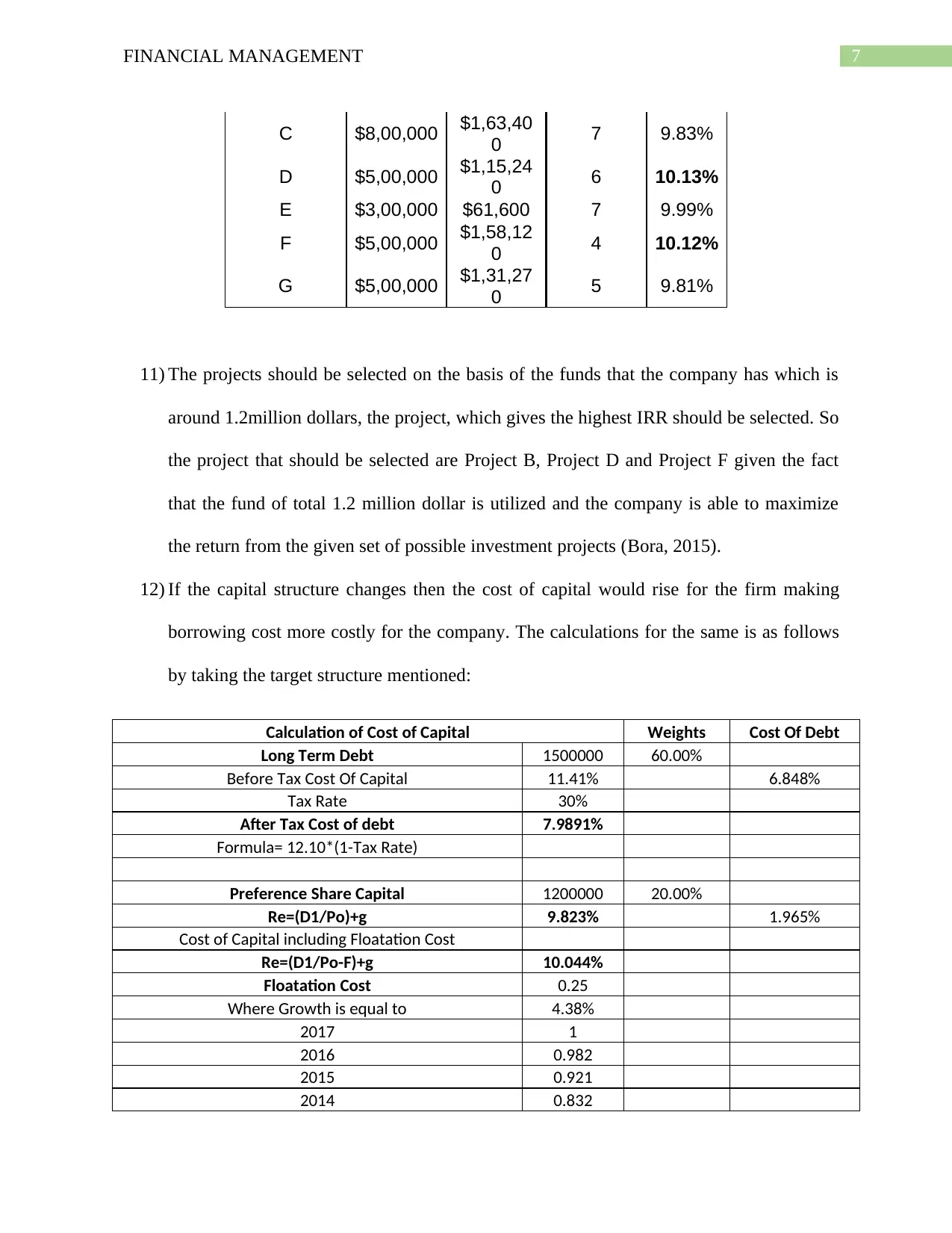

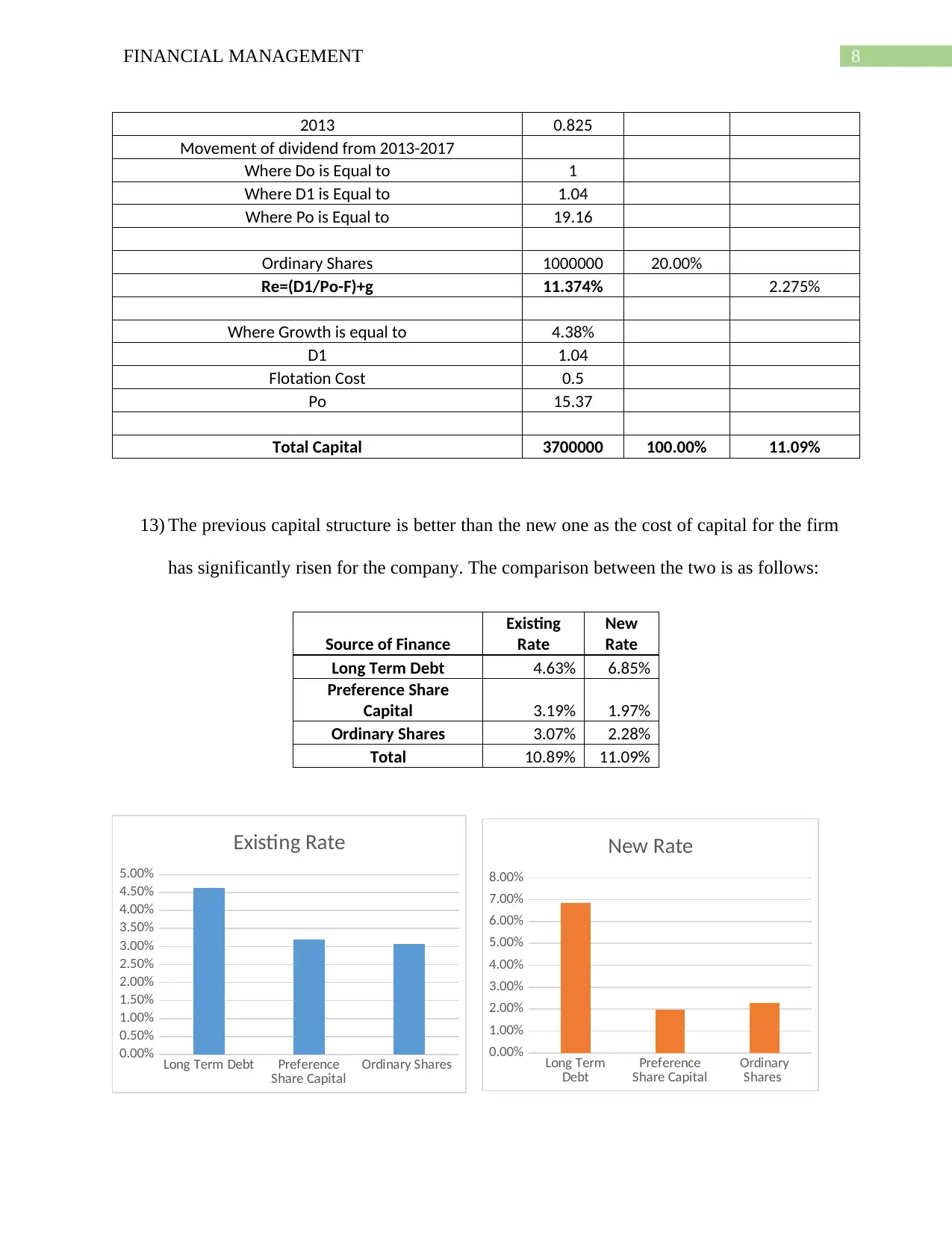

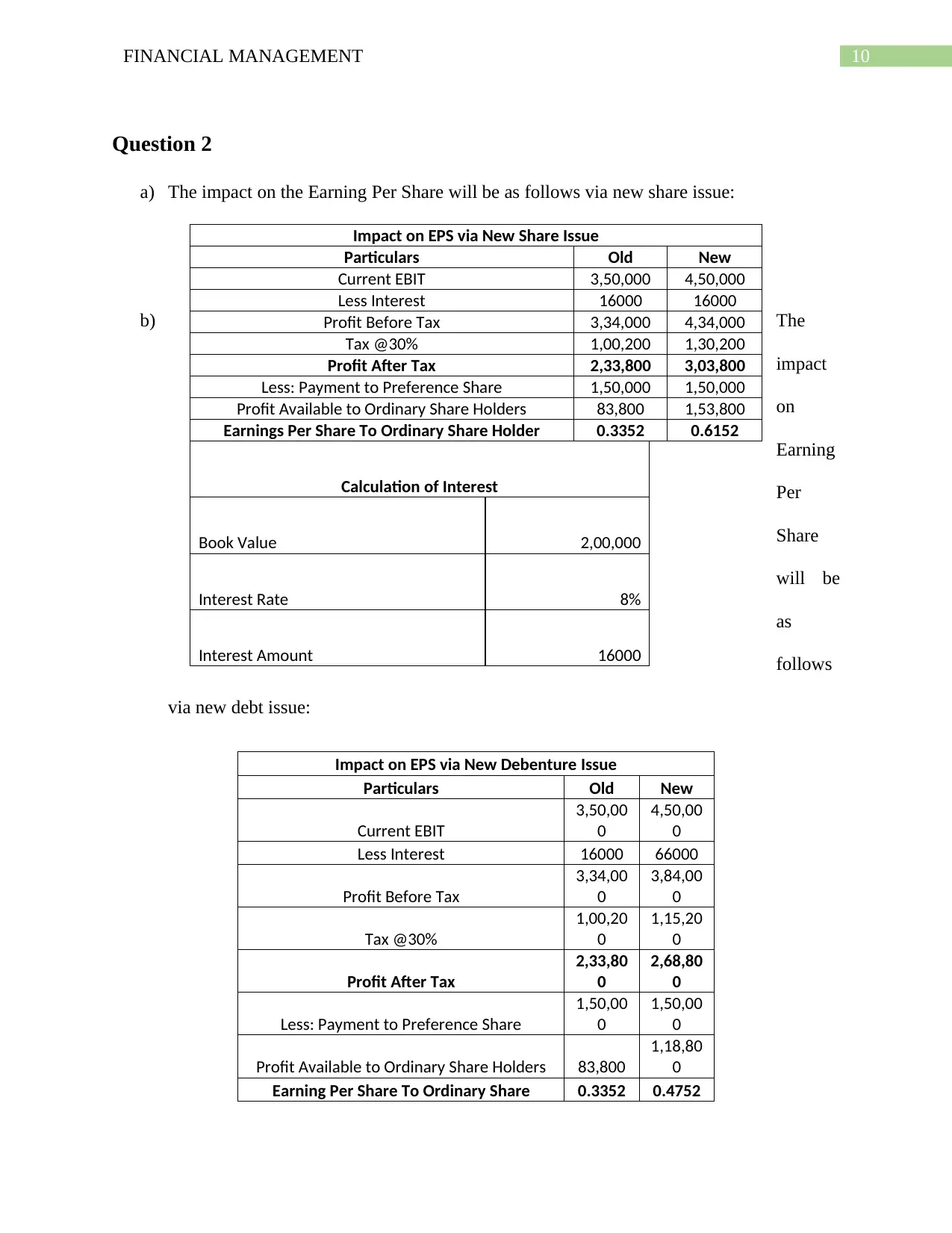

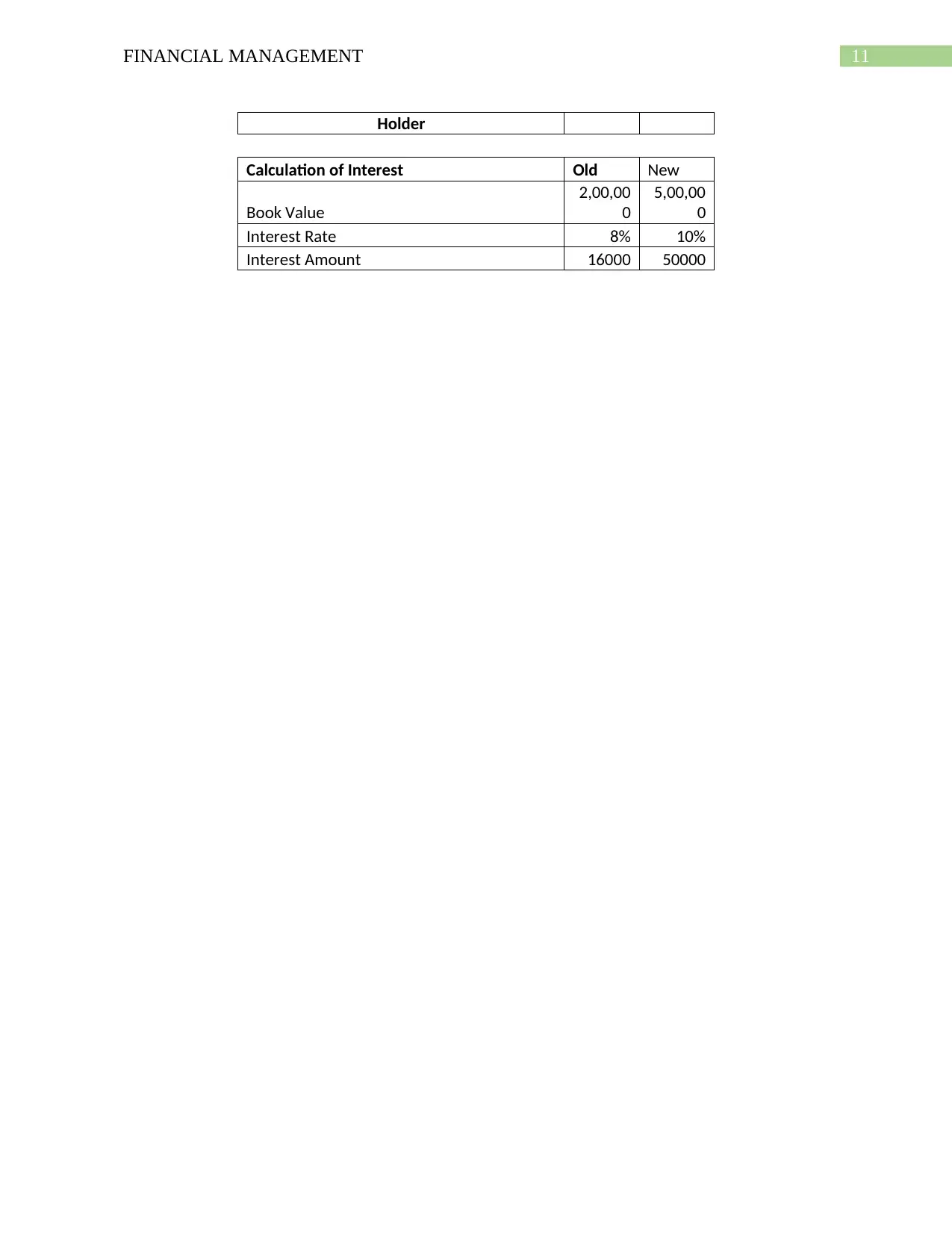

This financial management project delves into various corporate finance aspects influencing the cost of capital, including calculations for different sources and methods. It examines equity financing, the treatment of floatation costs, and expense classification. The project analyzes the Highsky Company's capital structure, calculates the cost of equity, debentures, and ordinary shares using methods like CAPM and dividend capitalization. It also explores an alternative growth factor calculation using the IRR method. The project determines the weighted average cost of capital (WACC) across different financing ranges and evaluates an investment opportunity schedule, recommending suitable projects based on IRR and available funds. Finally, it assesses the impact of changes in capital structure on the cost of capital and compares existing and new capital structures. Furthermore, the impact on Earning Per Share (EPS) via new share issue and debt issue under good and poor weather conditions is analyzed. The document concludes with probability analysis in different scenarios.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.