CVP Analysis and Cash Budget: Managing Financial Resources

VerifiedAdded on 2023/02/03

|16

|901

|81

Presentation

AI Summary

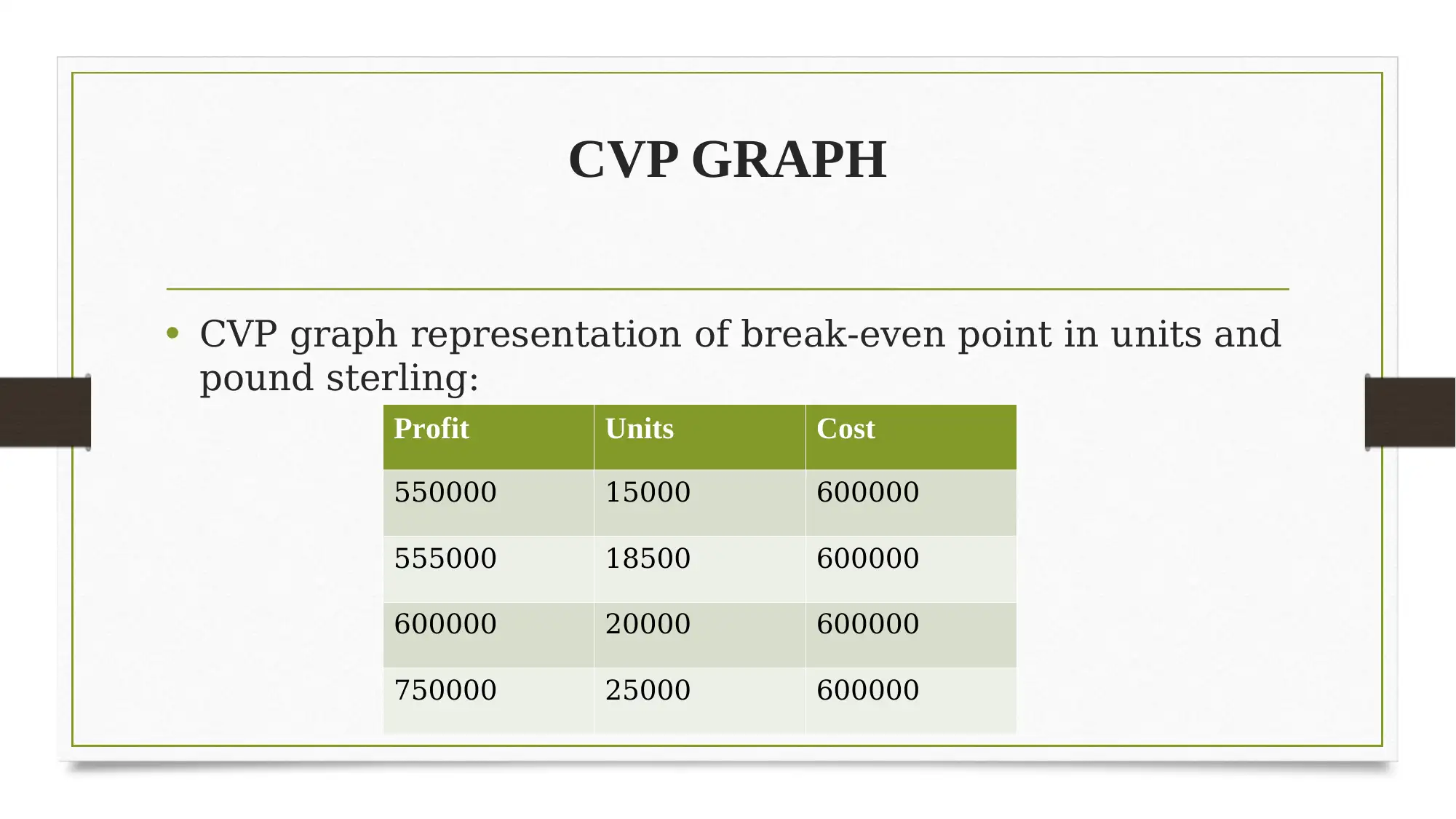

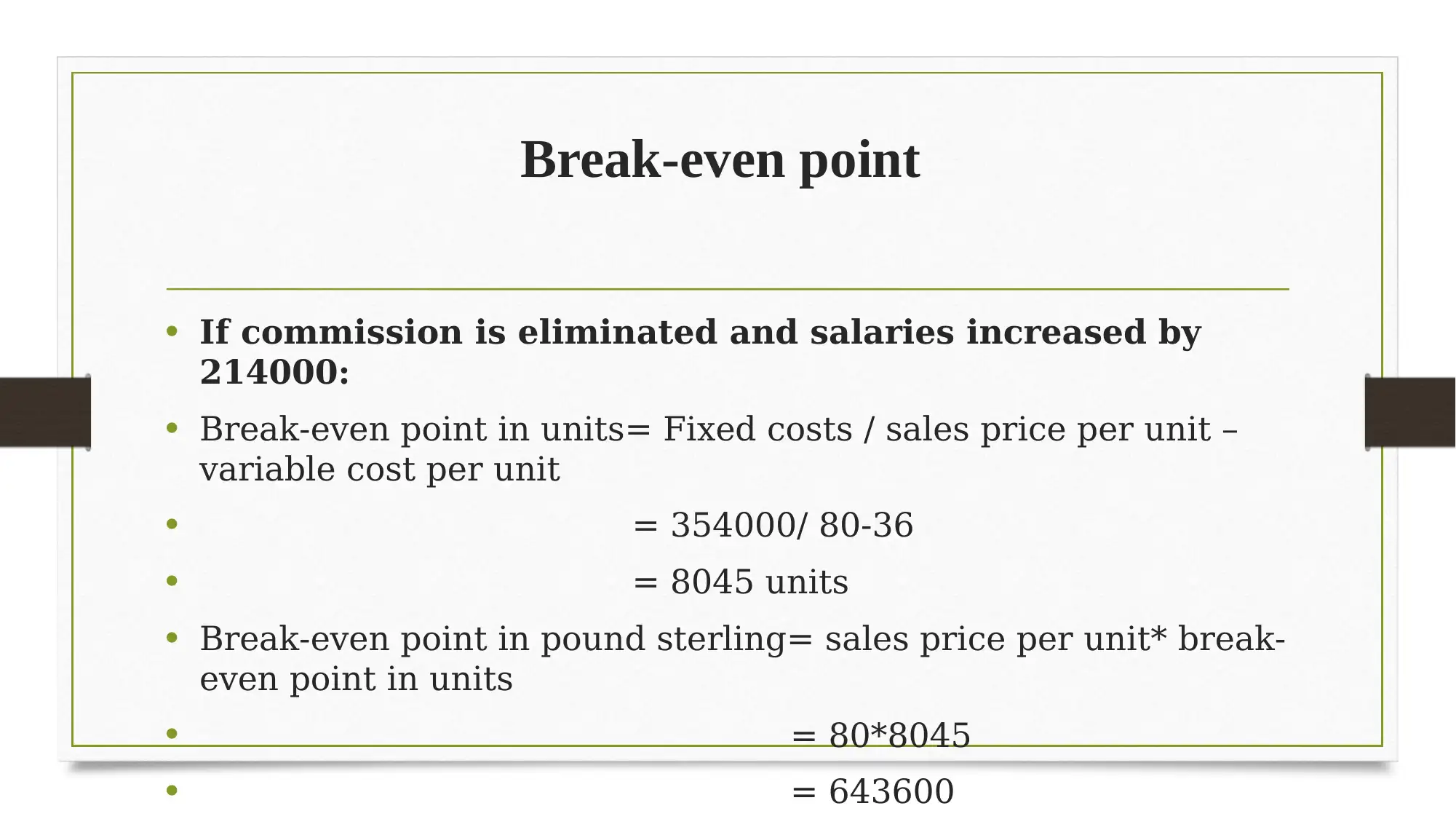

This presentation provides a comprehensive overview of managing financial resources, focusing on Cost-Volume-Profit (CVP) analysis and cash budgeting. It begins by classifying costs based on management function, traceability, time, and behavior. The presentation then delves into CVP analysis, explaining its role in determining the relationship between cost, profit, and volume, including break-even analysis in units and pound sterling, and a CVP graph. The analysis extends to calculating operating income or loss under different scenarios, such as changes in commission expenses. The presentation also includes a detailed cash budget for January, February, and March, outlining cash sales, collections from credit sales, payments for credit purchases, operating costs, and vehicle payments, with supporting working notes for credit sales and purchases. The conclusion summarizes the concepts of CVP analysis and the practical implications of cash budgeting, supported by relevant references. This presentation aims to equip the audience with the knowledge to make effective financial decisions.

1 out of 16

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.