Strategic Financial Management: Investment, Risk & Dividend Decisions

VerifiedAdded on 2023/04/22

|19

|4031

|356

Report

AI Summary

This report provides a comprehensive analysis of strategic financial management concepts, focusing on investment appraisal, risk management, and dividend policy. It begins with a Net Present Value (NPV) analysis of an investment proposal, considering initial investment, annual cash flows, and the impact of inflation. The report then discusses the impact of inflation on capital analysis, exploring real and nominal terms. Furthermore, it examines risk in capital analysis, detailing different approaches such as sensitivity and scenario analysis. The concept of real options is also explored, highlighting its flexibility and benefits in making strategic decisions. Finally, the report delves into optimal dividend policy, discussing various theoretical arguments including Walter’s Model, Modigliani-Miller Model, and the Bird in Hand Argument. This student-contributed assignment is available on Desklib, where students can find a wealth of resources including past papers and solved assignments.

Name of schedule:

Student reference number:

Title of assignment: Strategic Financial Management

Actual number of words: 2718

Student reference number:

Title of assignment: Strategic Financial Management

Actual number of words: 2718

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

A) NPV Analysis of the investment proposal.....................................................................3

B) Impact of the inflation....................................................................................................5

C) Risk in capital analysis and different approaches........................................................7

D) Concept of real Option..................................................................................................9

E) Optimal Dividend Policy..............................................................................................12

Various theoretical arguments on optimal dividend policy...........................................13

Walter’s Model (Relevant Theory):...........................................................................13

Modigliani-Miller Model (Irrelevance theory):...........................................................13

Bird in Hand Argument (Dividend and Uncertainty):................................................14

References.......................................................................................................................15

A) NPV Analysis of the investment proposal.....................................................................3

B) Impact of the inflation....................................................................................................5

C) Risk in capital analysis and different approaches........................................................7

D) Concept of real Option..................................................................................................9

E) Optimal Dividend Policy..............................................................................................12

Various theoretical arguments on optimal dividend policy...........................................13

Walter’s Model (Relevant Theory):...........................................................................13

Modigliani-Miller Model (Irrelevance theory):...........................................................13

Bird in Hand Argument (Dividend and Uncertainty):................................................14

References.......................................................................................................................15

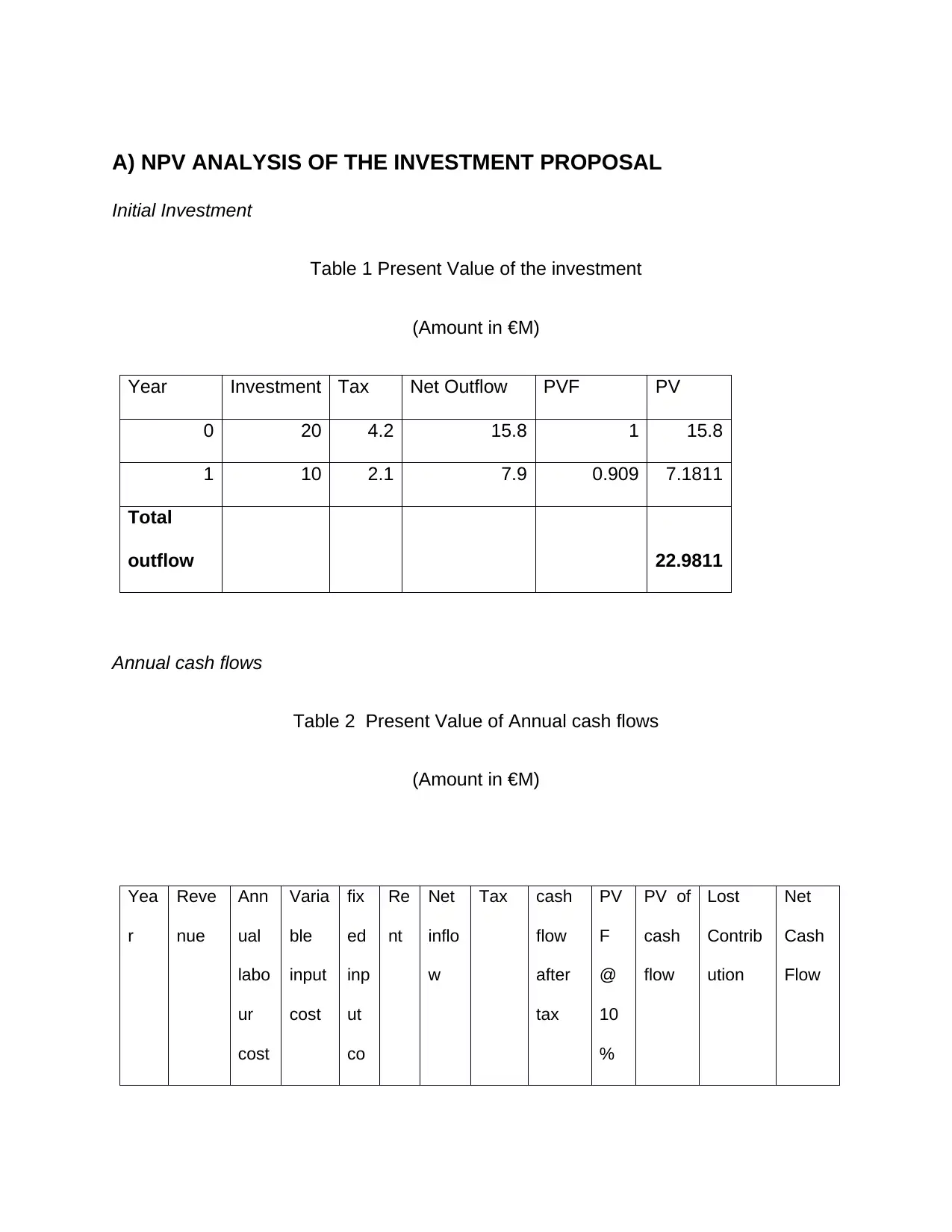

A) NPV ANALYSIS OF THE INVESTMENT PROPOSAL

Initial Investment

Table 1 Present Value of the investment

(Amount in €M)

Year Investment Tax Net Outflow PVF PV

0 20 4.2 15.8 1 15.8

1 10 2.1 7.9 0.909 7.1811

Total

outflow 22.9811

Annual cash flows

Table 2 Present Value of Annual cash flows

(Amount in €M)

Yea

r

Reve

nue

Ann

ual

labo

ur

cost

Varia

ble

input

cost

fix

ed

inp

ut

co

Re

nt

Net

inflo

w

Tax cash

flow

after

tax

PV

F

@

10

%

PV of

cash

flow

Lost

Contrib

ution

Net

Cash

Flow

Initial Investment

Table 1 Present Value of the investment

(Amount in €M)

Year Investment Tax Net Outflow PVF PV

0 20 4.2 15.8 1 15.8

1 10 2.1 7.9 0.909 7.1811

Total

outflow 22.9811

Annual cash flows

Table 2 Present Value of Annual cash flows

(Amount in €M)

Yea

r

Reve

nue

Ann

ual

labo

ur

cost

Varia

ble

input

cost

fix

ed

inp

ut

co

Re

nt

Net

inflo

w

Tax cash

flow

after

tax

PV

F

@

10

%

PV of

cash

flow

Lost

Contrib

ution

Net

Cash

Flow

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

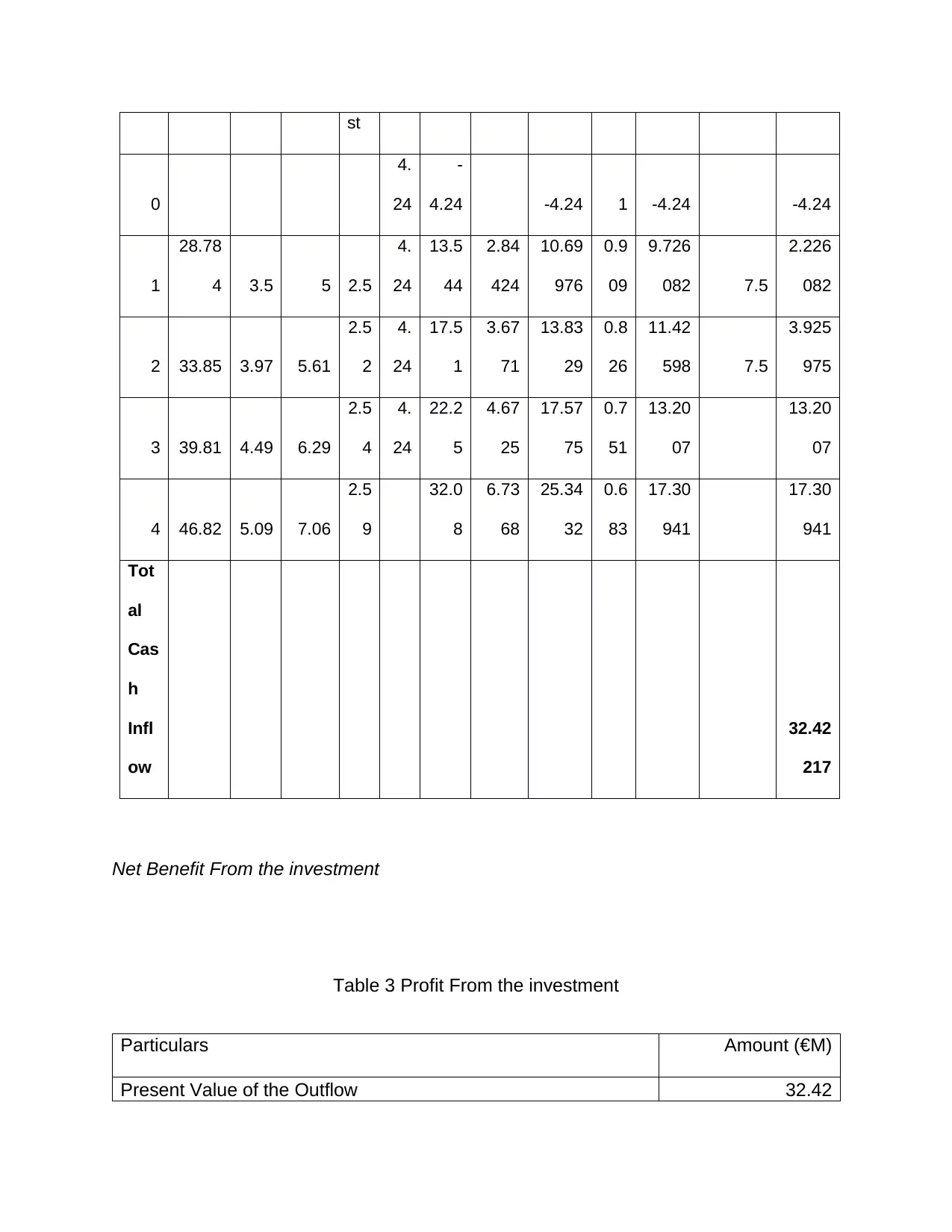

st

0

4.

24

-

4.24 -4.24 1 -4.24 -4.24

1

28.78

4 3.5 5 2.5

4.

24

13.5

44

2.84

424

10.69

976

0.9

09

9.726

082 7.5

2.226

082

2 33.85 3.97 5.61

2.5

2

4.

24

17.5

1

3.67

71

13.83

29

0.8

26

11.42

598 7.5

3.925

975

3 39.81 4.49 6.29

2.5

4

4.

24

22.2

5

4.67

25

17.57

75

0.7

51

13.20

07

13.20

07

4 46.82 5.09 7.06

2.5

9

32.0

8

6.73

68

25.34

32

0.6

83

17.30

941

17.30

941

Tot

al

Cas

h

Infl

ow

32.42

217

Net Benefit From the investment

Table 3 Profit From the investment

Particulars Amount (€M)

Present Value of the Outflow 32.42

0

4.

24

-

4.24 -4.24 1 -4.24 -4.24

1

28.78

4 3.5 5 2.5

4.

24

13.5

44

2.84

424

10.69

976

0.9

09

9.726

082 7.5

2.226

082

2 33.85 3.97 5.61

2.5

2

4.

24

17.5

1

3.67

71

13.83

29

0.8

26

11.42

598 7.5

3.925

975

3 39.81 4.49 6.29

2.5

4

4.

24

22.2

5

4.67

25

17.57

75

0.7

51

13.20

07

13.20

07

4 46.82 5.09 7.06

2.5

9

32.0

8

6.73

68

25.34

32

0.6

83

17.30

941

17.30

941

Tot

al

Cas

h

Infl

ow

32.42

217

Net Benefit From the investment

Table 3 Profit From the investment

Particulars Amount (€M)

Present Value of the Outflow 32.42

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

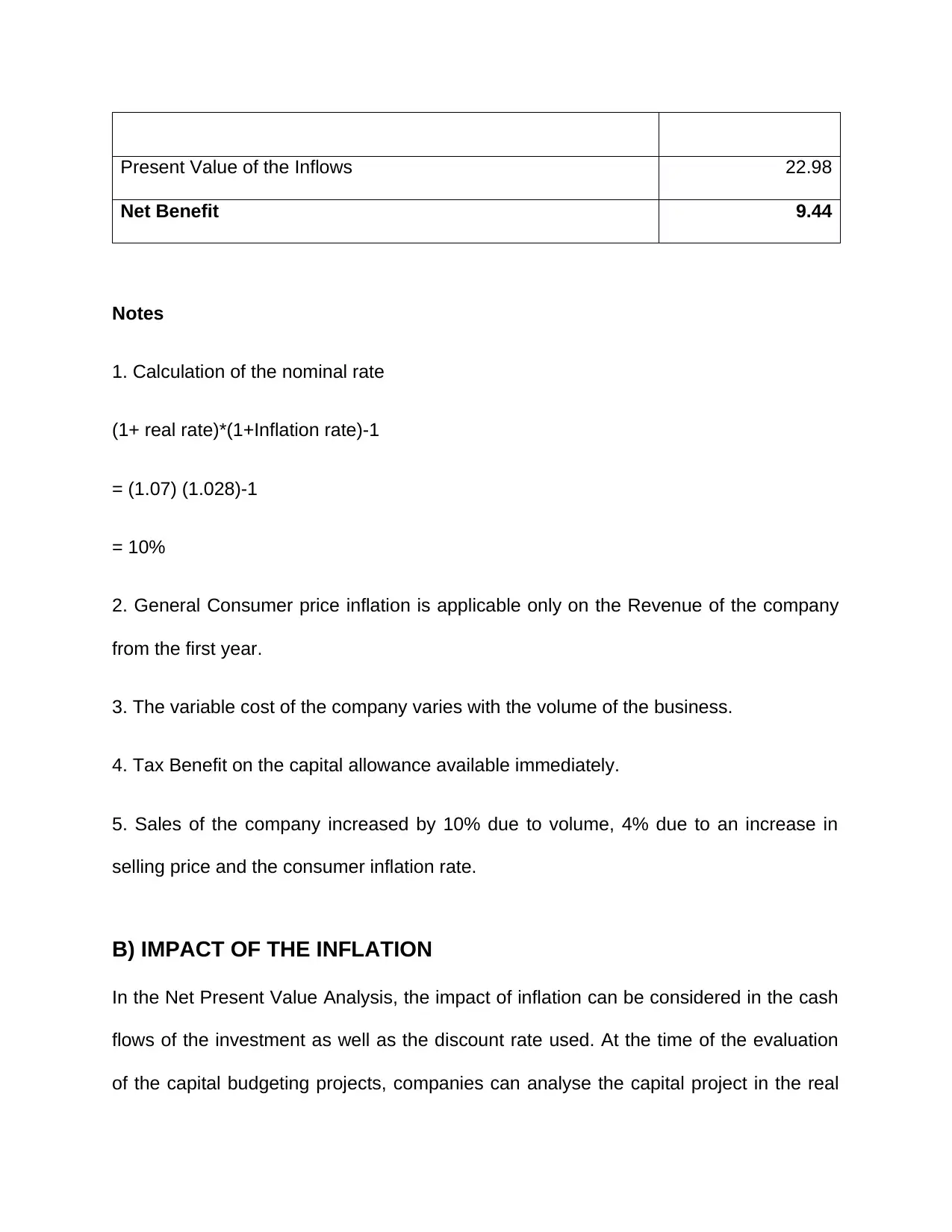

Present Value of the Inflows 22.98

Net Benefit 9.44

Notes

1. Calculation of the nominal rate

(1+ real rate)*(1+Inflation rate)-1

= (1.07) (1.028)-1

= 10%

2. General Consumer price inflation is applicable only on the Revenue of the company

from the first year.

3. The variable cost of the company varies with the volume of the business.

4. Tax Benefit on the capital allowance available immediately.

5. Sales of the company increased by 10% due to volume, 4% due to an increase in

selling price and the consumer inflation rate.

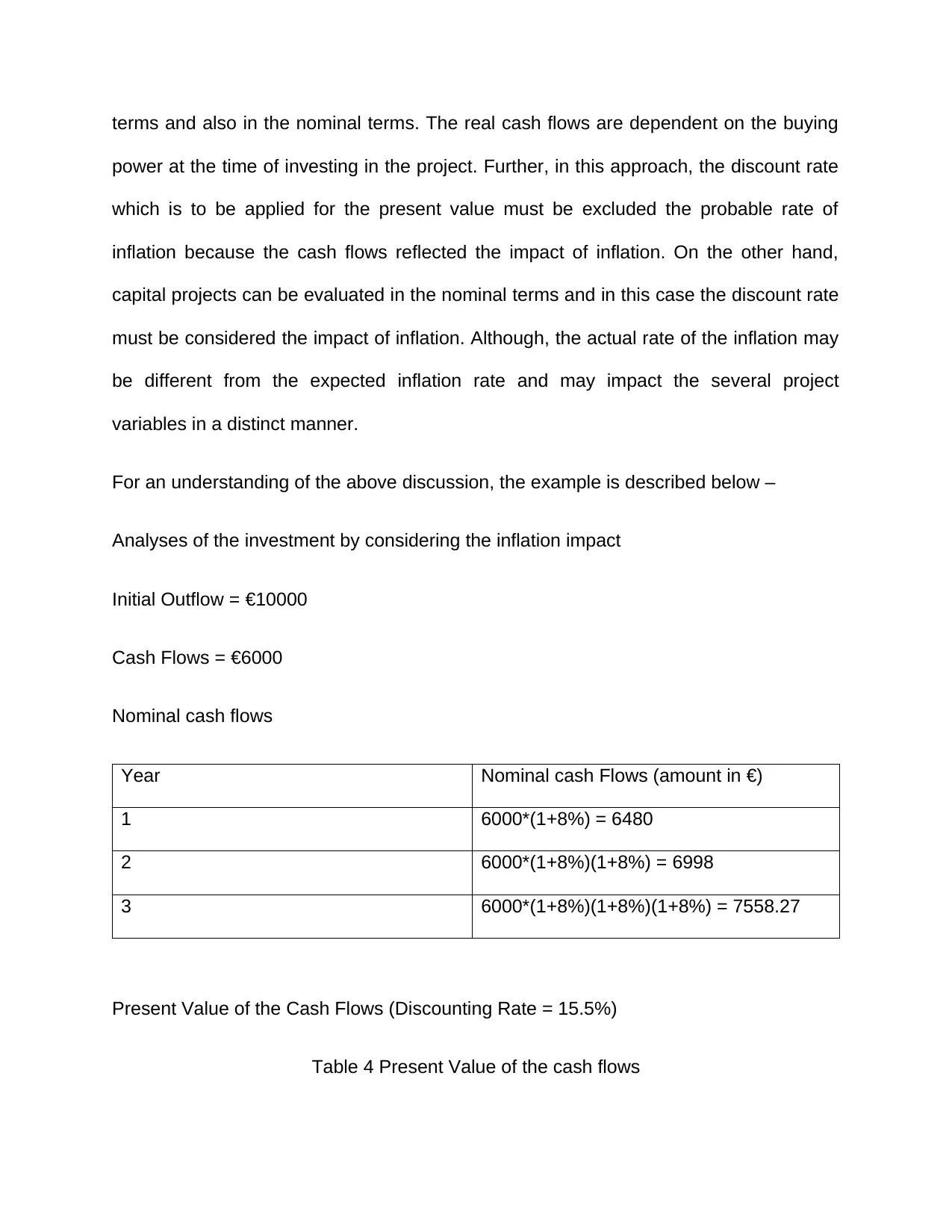

B) IMPACT OF THE INFLATION

In the Net Present Value Analysis, the impact of inflation can be considered in the cash

flows of the investment as well as the discount rate used. At the time of the evaluation

of the capital budgeting projects, companies can analyse the capital project in the real

Net Benefit 9.44

Notes

1. Calculation of the nominal rate

(1+ real rate)*(1+Inflation rate)-1

= (1.07) (1.028)-1

= 10%

2. General Consumer price inflation is applicable only on the Revenue of the company

from the first year.

3. The variable cost of the company varies with the volume of the business.

4. Tax Benefit on the capital allowance available immediately.

5. Sales of the company increased by 10% due to volume, 4% due to an increase in

selling price and the consumer inflation rate.

B) IMPACT OF THE INFLATION

In the Net Present Value Analysis, the impact of inflation can be considered in the cash

flows of the investment as well as the discount rate used. At the time of the evaluation

of the capital budgeting projects, companies can analyse the capital project in the real

terms and also in the nominal terms. The real cash flows are dependent on the buying

power at the time of investing in the project. Further, in this approach, the discount rate

which is to be applied for the present value must be excluded the probable rate of

inflation because the cash flows reflected the impact of inflation. On the other hand,

capital projects can be evaluated in the nominal terms and in this case the discount rate

must be considered the impact of inflation. Although, the actual rate of the inflation may

be different from the expected inflation rate and may impact the several project

variables in a distinct manner.

For an understanding of the above discussion, the example is described below –

Analyses of the investment by considering the inflation impact

Initial Outflow = €10000

Cash Flows = €6000

Nominal cash flows

Year Nominal cash Flows (amount in €)

1 6000*(1+8%) = 6480

2 6000*(1+8%)(1+8%) = 6998

3 6000*(1+8%)(1+8%)(1+8%) = 7558.27

Present Value of the Cash Flows (Discounting Rate = 15.5%)

Table 4 Present Value of the cash flows

power at the time of investing in the project. Further, in this approach, the discount rate

which is to be applied for the present value must be excluded the probable rate of

inflation because the cash flows reflected the impact of inflation. On the other hand,

capital projects can be evaluated in the nominal terms and in this case the discount rate

must be considered the impact of inflation. Although, the actual rate of the inflation may

be different from the expected inflation rate and may impact the several project

variables in a distinct manner.

For an understanding of the above discussion, the example is described below –

Analyses of the investment by considering the inflation impact

Initial Outflow = €10000

Cash Flows = €6000

Nominal cash flows

Year Nominal cash Flows (amount in €)

1 6000*(1+8%) = 6480

2 6000*(1+8%)(1+8%) = 6998

3 6000*(1+8%)(1+8%)(1+8%) = 7558.27

Present Value of the Cash Flows (Discounting Rate = 15.5%)

Table 4 Present Value of the cash flows

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

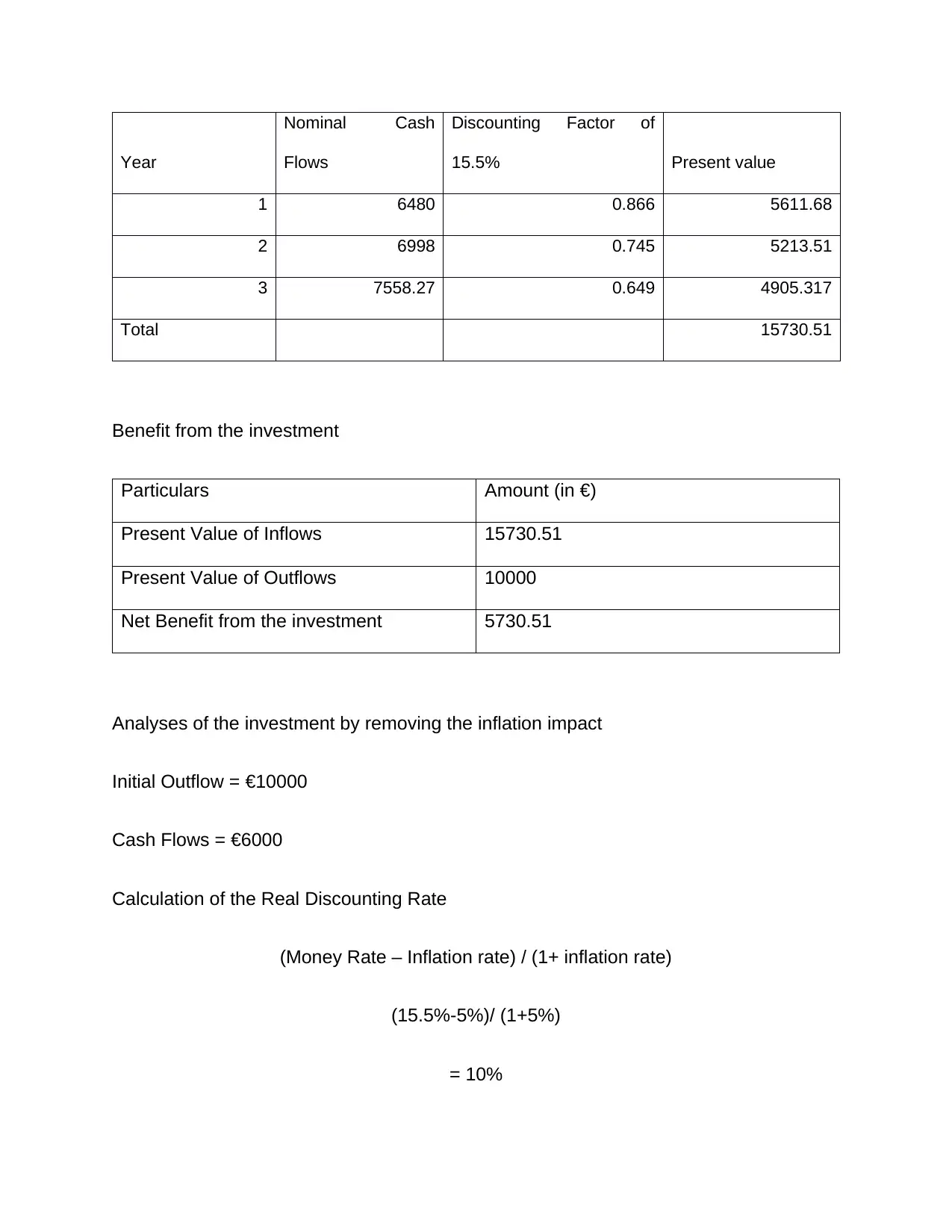

Year

Nominal Cash

Flows

Discounting Factor of

15.5% Present value

1 6480 0.866 5611.68

2 6998 0.745 5213.51

3 7558.27 0.649 4905.317

Total 15730.51

Benefit from the investment

Particulars Amount (in €)

Present Value of Inflows 15730.51

Present Value of Outflows 10000

Net Benefit from the investment 5730.51

Analyses of the investment by removing the inflation impact

Initial Outflow = €10000

Cash Flows = €6000

Calculation of the Real Discounting Rate

(Money Rate – Inflation rate) / (1+ inflation rate)

(15.5%-5%)/ (1+5%)

= 10%

Nominal Cash

Flows

Discounting Factor of

15.5% Present value

1 6480 0.866 5611.68

2 6998 0.745 5213.51

3 7558.27 0.649 4905.317

Total 15730.51

Benefit from the investment

Particulars Amount (in €)

Present Value of Inflows 15730.51

Present Value of Outflows 10000

Net Benefit from the investment 5730.51

Analyses of the investment by removing the inflation impact

Initial Outflow = €10000

Cash Flows = €6000

Calculation of the Real Discounting Rate

(Money Rate – Inflation rate) / (1+ inflation rate)

(15.5%-5%)/ (1+5%)

= 10%

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

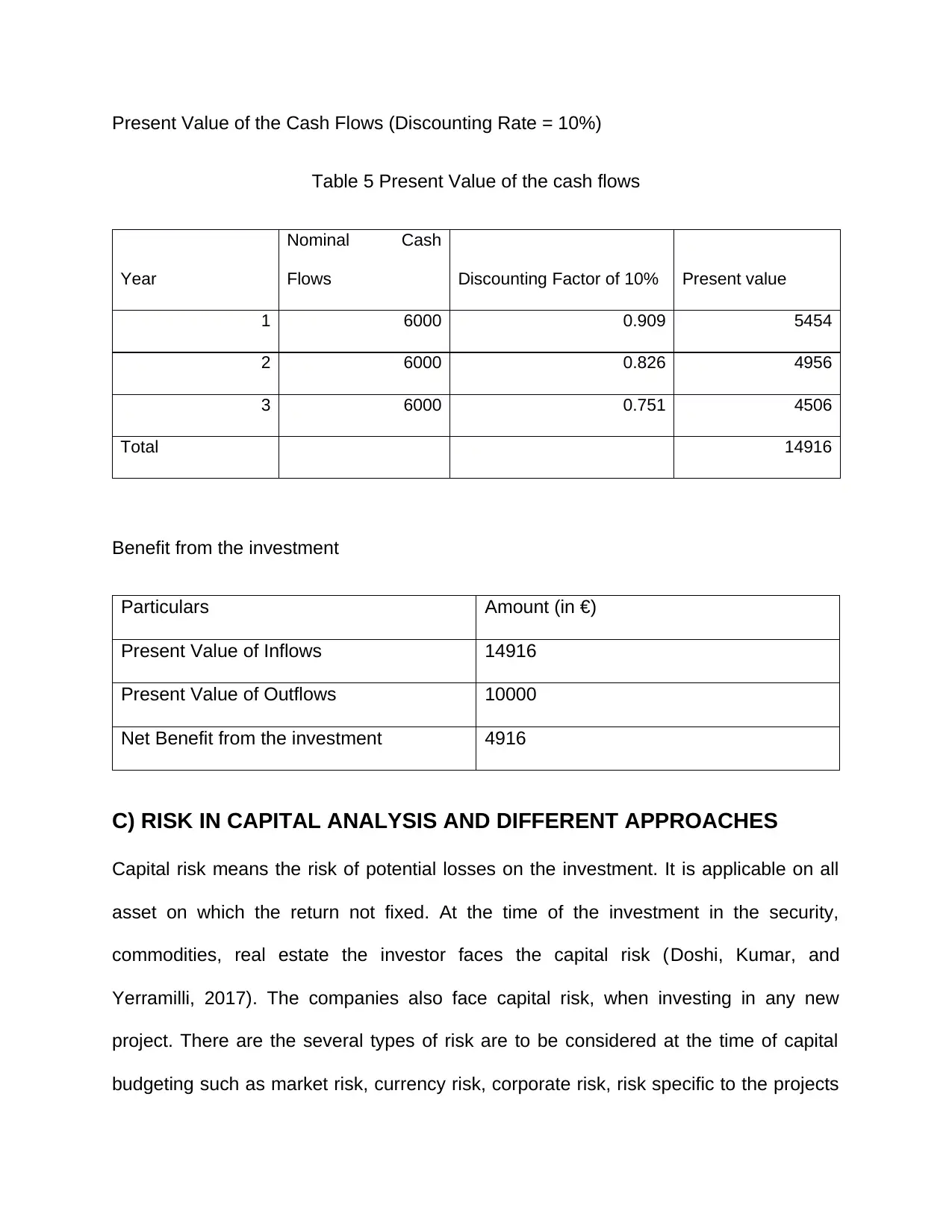

Present Value of the Cash Flows (Discounting Rate = 10%)

Table 5 Present Value of the cash flows

Year

Nominal Cash

Flows Discounting Factor of 10% Present value

1 6000 0.909 5454

2 6000 0.826 4956

3 6000 0.751 4506

Total 14916

Benefit from the investment

Particulars Amount (in €)

Present Value of Inflows 14916

Present Value of Outflows 10000

Net Benefit from the investment 4916

C) RISK IN CAPITAL ANALYSIS AND DIFFERENT APPROACHES

Capital risk means the risk of potential losses on the investment. It is applicable on all

asset on which the return not fixed. At the time of the investment in the security,

commodities, real estate the investor faces the capital risk (Doshi, Kumar, and

Yerramilli, 2017). The companies also face capital risk, when investing in any new

project. There are the several types of risk are to be considered at the time of capital

budgeting such as market risk, currency risk, corporate risk, risk specific to the projects

Table 5 Present Value of the cash flows

Year

Nominal Cash

Flows Discounting Factor of 10% Present value

1 6000 0.909 5454

2 6000 0.826 4956

3 6000 0.751 4506

Total 14916

Benefit from the investment

Particulars Amount (in €)

Present Value of Inflows 14916

Present Value of Outflows 10000

Net Benefit from the investment 4916

C) RISK IN CAPITAL ANALYSIS AND DIFFERENT APPROACHES

Capital risk means the risk of potential losses on the investment. It is applicable on all

asset on which the return not fixed. At the time of the investment in the security,

commodities, real estate the investor faces the capital risk (Doshi, Kumar, and

Yerramilli, 2017). The companies also face capital risk, when investing in any new

project. There are the several types of risk are to be considered at the time of capital

budgeting such as market risk, currency risk, corporate risk, risk specific to the projects

and many others (Paquin, Gauthier, and Morin, 2016). Every risk states about some

weakness or the vulnerability which impact on the plan and strategies of the company.

For instance, the market risk leads to the losses in the projects because of the change

in the market. There are several methods available for addressing the risk as well. With

this regards, the sensitivity analysis is one of the best methods by which the company

can minimize the risk from the investment (Korteweg, and Nagel, 2016). This analysis

assists in identifying the impact on the net present value by considering the distinct

variable. It helps in recognizing the most sensitive factor that could reason the mistake

in the estimation. Further, by implementing the sensitive analyses technique, the

company can observe the sensitivity of the output by making the change in one variable

and keeping the other input same (Chittenden, and Derregia, 2015). The investor can

evaluate the estimated performance of the project along with the alteration in the major

assumption on which the project is dependent such as the revenue from sales, cost of

the project, competition and other factors.

The sensitive analysis is a technique of evaluating the change in the net present value

of the project by making the change in one variable. It shows the sensitivity of the NPV

of the project related to the specific variable (Kengatharan, 2016). There are three steps

included for the sensitivity analysis which are described below –

Consider all variable which is connected with the NPV of the project.

Define the connection with the variables.

Evaluate the impact of the change in every variable on the NPV of the Project.

weakness or the vulnerability which impact on the plan and strategies of the company.

For instance, the market risk leads to the losses in the projects because of the change

in the market. There are several methods available for addressing the risk as well. With

this regards, the sensitivity analysis is one of the best methods by which the company

can minimize the risk from the investment (Korteweg, and Nagel, 2016). This analysis

assists in identifying the impact on the net present value by considering the distinct

variable. It helps in recognizing the most sensitive factor that could reason the mistake

in the estimation. Further, by implementing the sensitive analyses technique, the

company can observe the sensitivity of the output by making the change in one variable

and keeping the other input same (Chittenden, and Derregia, 2015). The investor can

evaluate the estimated performance of the project along with the alteration in the major

assumption on which the project is dependent such as the revenue from sales, cost of

the project, competition and other factors.

The sensitive analysis is a technique of evaluating the change in the net present value

of the project by making the change in one variable. It shows the sensitivity of the NPV

of the project related to the specific variable (Kengatharan, 2016). There are three steps

included for the sensitivity analysis which are described below –

Consider all variable which is connected with the NPV of the project.

Define the connection with the variables.

Evaluate the impact of the change in every variable on the NPV of the Project.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

By considering the data related to the investment in the above question, it has been

seen that the NPV of the project is 5730. The sensitivity of the NPV of the project with

respect to the annual cash inflows is (5730/15730*100) = 36.43%. It means if the cash

flows of the projects are decreased by 36.43% then in such case the NPV of the project

will be zero.

Another method for ascertaining the risk analysis is the scenario analysis. In this

technique, by analyzing the probable alternative results, future outcomes are

determined (Graham, Harvey, and Puri, 2015).

Therefore the Fiahlo can use the sensitivity and scenario analysis for ascertaining the

risk in the capital investment.

D) CONCEPT OF REAL OPTION

A real option is available for managers to make their choices for business investment

opportunities. It is considered optimistic as it involves projects that are associated with

tangible assets in spite of financial instruments. At the time when capacity restraints are

available by net present value analysis for making decisions regarding capital budgeting

then real options are appropriate for the evaluation of the risk (Pogrebova & et al. 2017).

It is the better technique for the estimation of the projects related to the capacity

constraints. For continuing the process market analysts is needed for recognizing the

implicit option which is made by the capacity constraints. As well as it decides the prices

for the fundamental variable that influences the price of the real option ( Byrne, and

Pecchenino, 2018).

seen that the NPV of the project is 5730. The sensitivity of the NPV of the project with

respect to the annual cash inflows is (5730/15730*100) = 36.43%. It means if the cash

flows of the projects are decreased by 36.43% then in such case the NPV of the project

will be zero.

Another method for ascertaining the risk analysis is the scenario analysis. In this

technique, by analyzing the probable alternative results, future outcomes are

determined (Graham, Harvey, and Puri, 2015).

Therefore the Fiahlo can use the sensitivity and scenario analysis for ascertaining the

risk in the capital investment.

D) CONCEPT OF REAL OPTION

A real option is available for managers to make their choices for business investment

opportunities. It is considered optimistic as it involves projects that are associated with

tangible assets in spite of financial instruments. At the time when capacity restraints are

available by net present value analysis for making decisions regarding capital budgeting

then real options are appropriate for the evaluation of the risk (Pogrebova & et al. 2017).

It is the better technique for the estimation of the projects related to the capacity

constraints. For continuing the process market analysts is needed for recognizing the

implicit option which is made by the capacity constraints. As well as it decides the prices

for the fundamental variable that influences the price of the real option ( Byrne, and

Pecchenino, 2018).

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Real options are considered as the choices that are made by the manager of the

company for expanding and altering the plans that are based on continually changing

market situations, technologies and economic conditions (Ming & et al. 2016). Real

options factoring majorly influence the assessment of possible investments even if it is

a generally applied valuation, for example, the net present value ( NPV) is unsuccessful

in case of probable benefits given by real option. Furthermore, management can

evaluate the opportunity cost of enduring or abandoning a plan and conclusions by real

option value analysis (ROV).

It is the flexible technique and provides the opportunities and the benefits to the

business (Wu & et al. 2015). For instance, making an investment in innovative

production system can offer real options to the managers; however for establishing

novel product, new adjustments and united proceedings for improving the situations of

the market. Company must consider the real option value for making the investments

decisions regarding new services and facility. The potential for mergers and acquisitions

(M&A) or else joint ventures are the other examples of a real option.

Moreover, even in a situation of the quantitative model it is working to value a real

option, the option of the model commonly seems as heuristic, and the reason behind it

is its selection that is different all across the company as well as across its project

managers (Ghamlouch, Fouladirad, and Grall, 2017).

Therefore, it can be said that real options reasoning is completely dependent on logical

financial choices by considering that such financial choices can make a convinced

amount of valuable flexibility (Regan & et al. 2015). When there is a financial choice

company for expanding and altering the plans that are based on continually changing

market situations, technologies and economic conditions (Ming & et al. 2016). Real

options factoring majorly influence the assessment of possible investments even if it is

a generally applied valuation, for example, the net present value ( NPV) is unsuccessful

in case of probable benefits given by real option. Furthermore, management can

evaluate the opportunity cost of enduring or abandoning a plan and conclusions by real

option value analysis (ROV).

It is the flexible technique and provides the opportunities and the benefits to the

business (Wu & et al. 2015). For instance, making an investment in innovative

production system can offer real options to the managers; however for establishing

novel product, new adjustments and united proceedings for improving the situations of

the market. Company must consider the real option value for making the investments

decisions regarding new services and facility. The potential for mergers and acquisitions

(M&A) or else joint ventures are the other examples of a real option.

Moreover, even in a situation of the quantitative model it is working to value a real

option, the option of the model commonly seems as heuristic, and the reason behind it

is its selection that is different all across the company as well as across its project

managers (Ghamlouch, Fouladirad, and Grall, 2017).

Therefore, it can be said that real options reasoning is completely dependent on logical

financial choices by considering that such financial choices can make a convinced

amount of valuable flexibility (Regan & et al. 2015). When there is a financial choice

than it can easily afford the freedom for creating the best choices while making

decisions, for example at what time and place all such capital investment should be

made. Different options related to the management are provided to the companies for

taking importance decisions in the future as per the present existing situations of market

Furthermore, it can be said that real options are the choices that are available to the

management for making decisions that are flexible enough and also provide the benefits

in the future.

Real option facilitates the evaluation of plans by means of capacity constrained cash

flow following techniques helps to incorporate the outcomes of the non-linearity of cash

flows because of its capacity restraints (Schachter, and Mancarella, 2016).

Various leading corporations use the technique of real options analysis in diverse ways.

It is also used to frame the method of proceeding regarding the problems related to

decision analysis that is linked with the capital investment. When this method is used for

their company’s investment problem, it majorly increases the alertness of the value and

different options which are probably there in the plans. Furthermore, it helps the

executives in identifying the valuable options that can be made or destroyed as

decisions are concluded by the managers (Konstantelos, and Strbac, 2015).

Real options are used by the managers for thinking regarding the uncertainty and risk

because assets might be subjugated in a plan; however in spite of its various negative

aspects it can be avoided. Furthermore, it helps the managers to concentrate on the value

of obtaining extra information before making irreversible investment choices. A real option

technique is also used as an analytical tool by various companies. Formal option pricing

decisions, for example at what time and place all such capital investment should be

made. Different options related to the management are provided to the companies for

taking importance decisions in the future as per the present existing situations of market

Furthermore, it can be said that real options are the choices that are available to the

management for making decisions that are flexible enough and also provide the benefits

in the future.

Real option facilitates the evaluation of plans by means of capacity constrained cash

flow following techniques helps to incorporate the outcomes of the non-linearity of cash

flows because of its capacity restraints (Schachter, and Mancarella, 2016).

Various leading corporations use the technique of real options analysis in diverse ways.

It is also used to frame the method of proceeding regarding the problems related to

decision analysis that is linked with the capital investment. When this method is used for

their company’s investment problem, it majorly increases the alertness of the value and

different options which are probably there in the plans. Furthermore, it helps the

executives in identifying the valuable options that can be made or destroyed as

decisions are concluded by the managers (Konstantelos, and Strbac, 2015).

Real options are used by the managers for thinking regarding the uncertainty and risk

because assets might be subjugated in a plan; however in spite of its various negative

aspects it can be avoided. Furthermore, it helps the managers to concentrate on the value

of obtaining extra information before making irreversible investment choices. A real option

technique is also used as an analytical tool by various companies. Formal option pricing

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 19

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.