APC308 Financial Management: Equity Finance, Investment Appraisal

VerifiedAdded on 2023/01/17

|15

|4007

|51

Homework Assignment

AI Summary

This document presents a comprehensive solution to a financial management assignment, addressing key concepts in corporate finance. The assignment delves into equity finance, specifically focusing on right issues, providing detailed calculations for different scenarios, including the determination of theoretical ex-rights price and the analysis of various right issue options. It also explores the benefits and drawbacks of scrip dividends for both companies and shareholders. Furthermore, the assignment applies various investment appraisal techniques such as Payback Period, Accounting Rate of Return (ARR), Net Present Value (NPV), and Internal Rate of Return (IRR) to evaluate the feasibility of a new machinery purchase. The solution includes all the necessary calculations and recommendations based on the results of these techniques, providing a thorough understanding of financial decision-making processes.

FINANCIAL

MANAGEMENT

MANAGEMENT

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

Table of Contents

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 2. Long term finance: Equity finance......................................................................3

Question 3. Calculation as accordance of investment appraisal techniques..........................8

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

INTRODUCTION...........................................................................................................................3

MAIN BODY...................................................................................................................................3

Question 2. Long term finance: Equity finance......................................................................3

Question 3. Calculation as accordance of investment appraisal techniques..........................8

CONCLUSION..............................................................................................................................14

REFERENCES..............................................................................................................................15

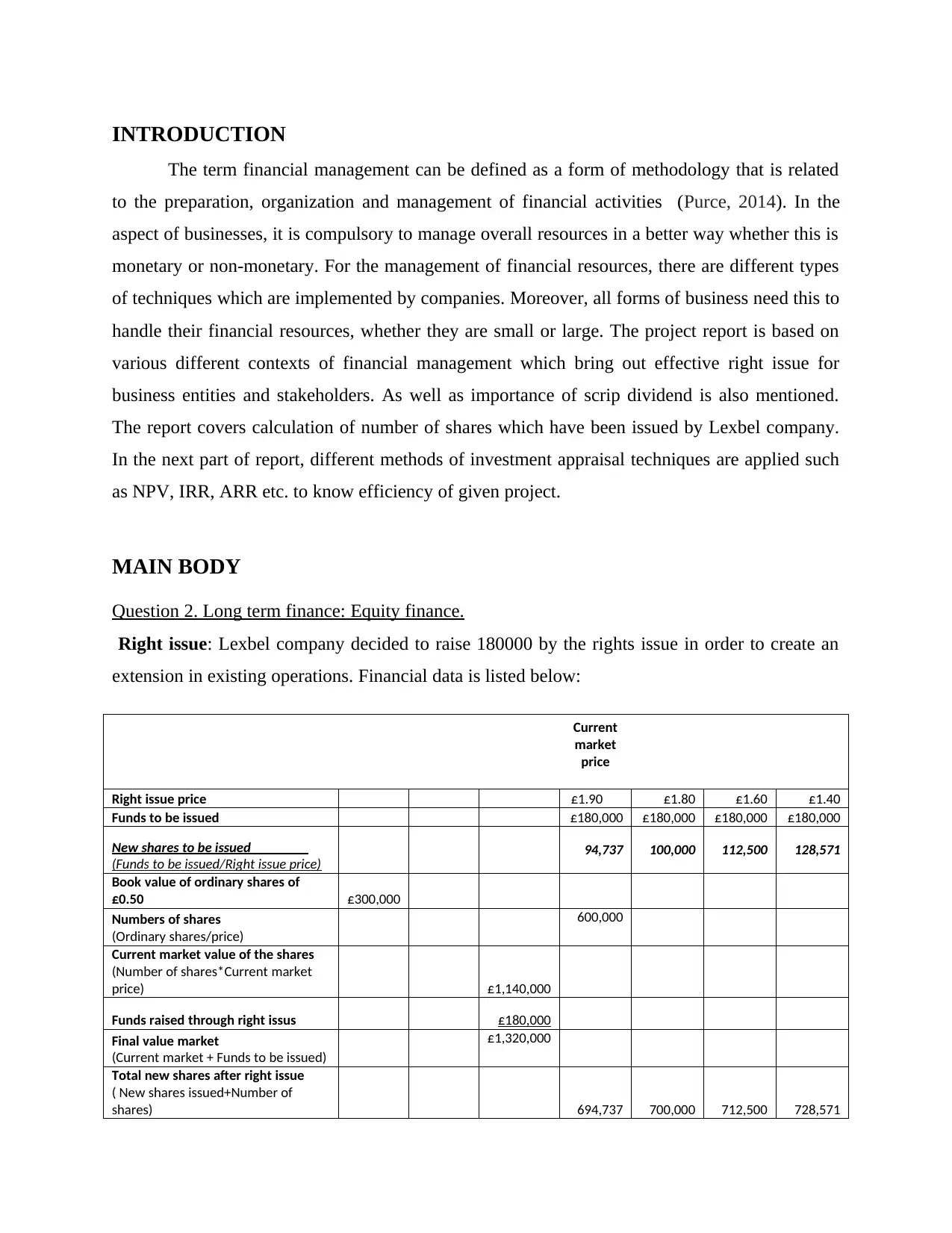

INTRODUCTION

The term financial management can be defined as a form of methodology that is related

to the preparation, organization and management of financial activities (Purce, 2014). In the

aspect of businesses, it is compulsory to manage overall resources in a better way whether this is

monetary or non-monetary. For the management of financial resources, there are different types

of techniques which are implemented by companies. Moreover, all forms of business need this to

handle their financial resources, whether they are small or large. The project report is based on

various different contexts of financial management which bring out effective right issue for

business entities and stakeholders. As well as importance of scrip dividend is also mentioned.

The report covers calculation of number of shares which have been issued by Lexbel company.

In the next part of report, different methods of investment appraisal techniques are applied such

as NPV, IRR, ARR etc. to know efficiency of given project.

MAIN BODY

Question 2. Long term finance: Equity finance.

Right issue: Lexbel company decided to raise 180000 by the rights issue in order to create an

extension in existing operations. Financial data is listed below:

Current

market

price

Right issue price £1.90 £1.80 £1.60 £1.40

Funds to be issued £180,000 £180,000 £180,000 £180,000

New shares to be issued

(Funds to be issued/Right issue price)

94,737 100,000 112,500 128,571

Book value of ordinary shares of

£0.50 £300,000

Numbers of shares

(Ordinary shares/price)

600,000

Current market value of the shares

(Number of shares*Current market

price) £1,140,000

Funds raised through right issus £180,000

Final value market

(Current market + Funds to be issued)

£1,320,000

Total new shares after right issue

( New shares issued+Number of

shares) 694,737 700,000 712,500 728,571

The term financial management can be defined as a form of methodology that is related

to the preparation, organization and management of financial activities (Purce, 2014). In the

aspect of businesses, it is compulsory to manage overall resources in a better way whether this is

monetary or non-monetary. For the management of financial resources, there are different types

of techniques which are implemented by companies. Moreover, all forms of business need this to

handle their financial resources, whether they are small or large. The project report is based on

various different contexts of financial management which bring out effective right issue for

business entities and stakeholders. As well as importance of scrip dividend is also mentioned.

The report covers calculation of number of shares which have been issued by Lexbel company.

In the next part of report, different methods of investment appraisal techniques are applied such

as NPV, IRR, ARR etc. to know efficiency of given project.

MAIN BODY

Question 2. Long term finance: Equity finance.

Right issue: Lexbel company decided to raise 180000 by the rights issue in order to create an

extension in existing operations. Financial data is listed below:

Current

market

price

Right issue price £1.90 £1.80 £1.60 £1.40

Funds to be issued £180,000 £180,000 £180,000 £180,000

New shares to be issued

(Funds to be issued/Right issue price)

94,737 100,000 112,500 128,571

Book value of ordinary shares of

£0.50 £300,000

Numbers of shares

(Ordinary shares/price)

600,000

Current market value of the shares

(Number of shares*Current market

price) £1,140,000

Funds raised through right issus £180,000

Final value market

(Current market + Funds to be issued)

£1,320,000

Total new shares after right issue

( New shares issued+Number of

shares) 694,737 700,000 712,500 728,571

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

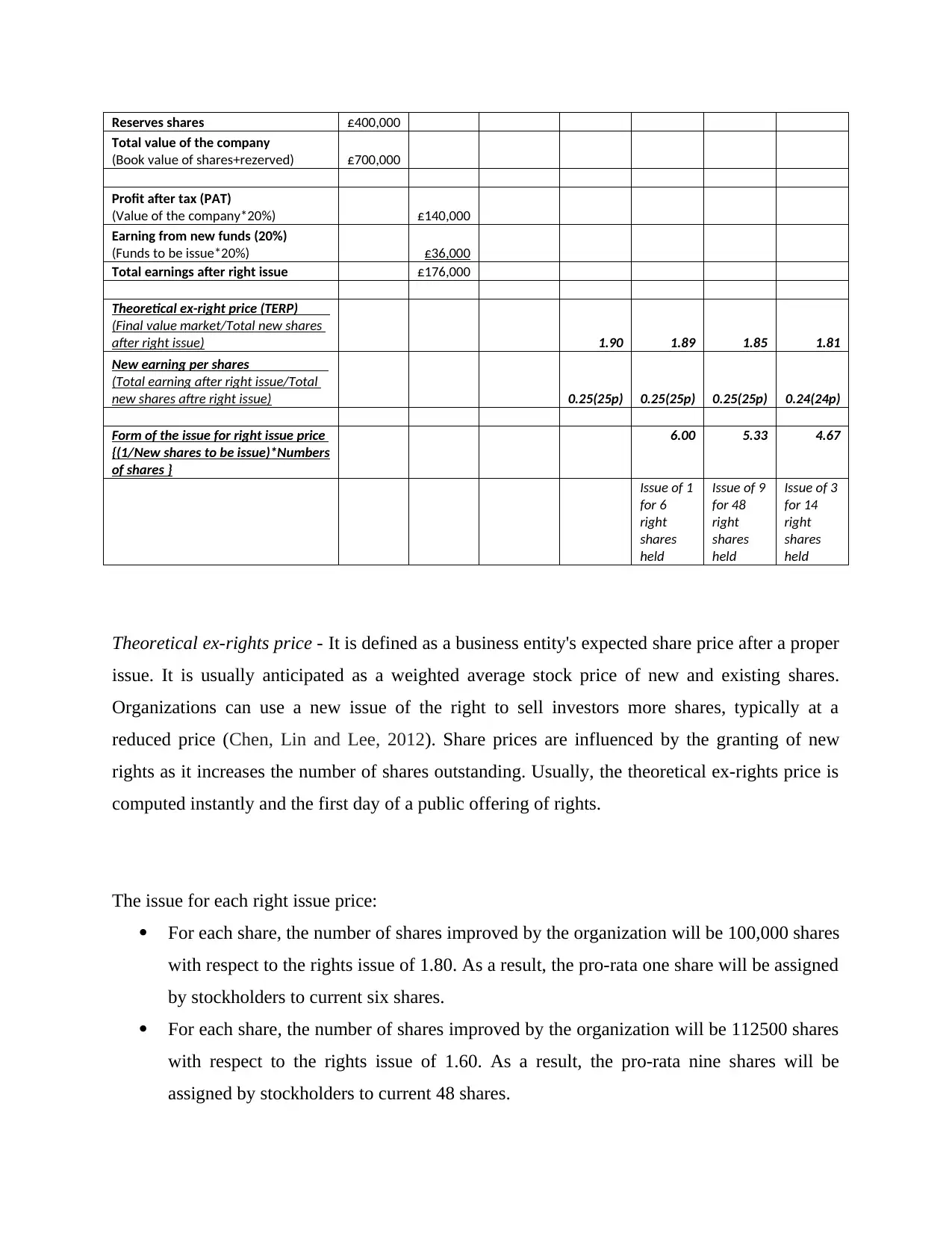

Reserves shares £400,000

Total value of the company

(Book value of shares+rezerved) £700,000

Profit after tax (PAT)

(Value of the company*20%) £140,000

Earning from new funds (20%)

(Funds to be issue*20%) £36,000

Total earnings after right issue £176,000

Theoretical ex-right price (TERP)

(Final value market/Total new shares

after right issue) 1.90 1.89 1.85 1.81

New earning per shares

(Total earning after right issue/Total

new shares aftre right issue) 0.25(25p) 0.25(25p) 0.25(25p) 0.24(24p)

Form of the issue for right issue price

{(1/New shares to be issue)*Numbers

of shares }

6.00 5.33 4.67

Issue of 1

for 6

right

shares

held

Issue of 9

for 48

right

shares

held

Issue of 3

for 14

right

shares

held

Theoretical ex-rights price - It is defined as a business entity's expected share price after a proper

issue. It is usually anticipated as a weighted average stock price of new and existing shares.

Organizations can use a new issue of the right to sell investors more shares, typically at a

reduced price (Chen, Lin and Lee, 2012). Share prices are influenced by the granting of new

rights as it increases the number of shares outstanding. Usually, the theoretical ex-rights price is

computed instantly and the first day of a public offering of rights.

The issue for each right issue price:

For each share, the number of shares improved by the organization will be 100,000 shares

with respect to the rights issue of 1.80. As a result, the pro-rata one share will be assigned

by stockholders to current six shares.

For each share, the number of shares improved by the organization will be 112500 shares

with respect to the rights issue of 1.60. As a result, the pro-rata nine shares will be

assigned by stockholders to current 48 shares.

Total value of the company

(Book value of shares+rezerved) £700,000

Profit after tax (PAT)

(Value of the company*20%) £140,000

Earning from new funds (20%)

(Funds to be issue*20%) £36,000

Total earnings after right issue £176,000

Theoretical ex-right price (TERP)

(Final value market/Total new shares

after right issue) 1.90 1.89 1.85 1.81

New earning per shares

(Total earning after right issue/Total

new shares aftre right issue) 0.25(25p) 0.25(25p) 0.25(25p) 0.24(24p)

Form of the issue for right issue price

{(1/New shares to be issue)*Numbers

of shares }

6.00 5.33 4.67

Issue of 1

for 6

right

shares

held

Issue of 9

for 48

right

shares

held

Issue of 3

for 14

right

shares

held

Theoretical ex-rights price - It is defined as a business entity's expected share price after a proper

issue. It is usually anticipated as a weighted average stock price of new and existing shares.

Organizations can use a new issue of the right to sell investors more shares, typically at a

reduced price (Chen, Lin and Lee, 2012). Share prices are influenced by the granting of new

rights as it increases the number of shares outstanding. Usually, the theoretical ex-rights price is

computed instantly and the first day of a public offering of rights.

The issue for each right issue price:

For each share, the number of shares improved by the organization will be 100,000 shares

with respect to the rights issue of 1.80. As a result, the pro-rata one share will be assigned

by stockholders to current six shares.

For each share, the number of shares improved by the organization will be 112500 shares

with respect to the rights issue of 1.60. As a result, the pro-rata nine shares will be

assigned by stockholders to current 48 shares.

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

For each share, the number of shares improved by the organization will be 128571 shares

with respect to the rights issue of 1.40. As a result, the pro-rata three shares will be

assigned by stockholders to current fourteen shares.

(v) Analysis of best option among three right issues.

This can be found on the grounds of the above estimate that issue @ £ 1.8 will be

advantageous to the corporation. This is because the cost of the estimated earnings per share at

this level is greater than the other two prices.

(c) Benefits and drawbacks of scrip dividend for companies and shareholders.

Scrip dividend- This can be described as an issuer's current stock shares that are distributed

instead of dividends to stakeholders (Richard, Kirby and Chadwick, 2013). It is used in case of

issuers wanting to pay their investors in any way, but not having enough money to issue a

dividend. In fact, investors are presented with this form of dividends as an option to the cash

dividend. It is more advantageous to investors because no transactions fees are needed for this

dividend to be charged as commissions. Often regarded as an option to legal tendering is the

scrip dividend. In addition, dividends from scripts usually apply to newly created stocks as

opposed to pre-existing shares. The term scrip, in a wider sense, applies to a sort of alternative

currency that substitutes legal tender. A script is a form of debt in many cases but is typically

always another form of debt documents. Following, the critical scrip dividend research is

conducted in this way:

Benefits:

For shareholders-

This dividend provides investors in the corporate entity with retaining power as well as

tends to increase the total value of assets. Therefore, in terms of compounding interest,

the market price of their share rises.

The scrip dividends enable investors with far more yields and financial gain as opposed

to cash dividends as time goes by.

Opposed to cash dividends, it is quite convenient for investors to handle scrip dividends.

with respect to the rights issue of 1.40. As a result, the pro-rata three shares will be

assigned by stockholders to current fourteen shares.

(v) Analysis of best option among three right issues.

This can be found on the grounds of the above estimate that issue @ £ 1.8 will be

advantageous to the corporation. This is because the cost of the estimated earnings per share at

this level is greater than the other two prices.

(c) Benefits and drawbacks of scrip dividend for companies and shareholders.

Scrip dividend- This can be described as an issuer's current stock shares that are distributed

instead of dividends to stakeholders (Richard, Kirby and Chadwick, 2013). It is used in case of

issuers wanting to pay their investors in any way, but not having enough money to issue a

dividend. In fact, investors are presented with this form of dividends as an option to the cash

dividend. It is more advantageous to investors because no transactions fees are needed for this

dividend to be charged as commissions. Often regarded as an option to legal tendering is the

scrip dividend. In addition, dividends from scripts usually apply to newly created stocks as

opposed to pre-existing shares. The term scrip, in a wider sense, applies to a sort of alternative

currency that substitutes legal tender. A script is a form of debt in many cases but is typically

always another form of debt documents. Following, the critical scrip dividend research is

conducted in this way:

Benefits:

For shareholders-

This dividend provides investors in the corporate entity with retaining power as well as

tends to increase the total value of assets. Therefore, in terms of compounding interest,

the market price of their share rises.

The scrip dividends enable investors with far more yields and financial gain as opposed

to cash dividends as time goes by.

Opposed to cash dividends, it is quite convenient for investors to handle scrip dividends.

The advantage for a scrip dividend stockholders is that they can humanely boost their

equity stake in the firm without paying the commissions of the intermediary or the stamp

duty on an exchange purchase (Yu, Chan and Chou, 2015).

For company

One of the main advantages of the scrip dividend is that it is beneficial for businesses to

save capital. It is because corporate entities are able to request this dividend to investors,

and this can contribute to wild money.

In fact, it allows companies to minimize the risk of increasing liquidity position. This also

raises corporate market capitalization on the stock exchange by increasing the number of

investors.

The advantage for the firm is that it doesn't need to find the funds to pay dividends and

could save tax in some conditions.

Drawbacks:

For shareholders-

The price of this share relies on the state of the economy; if the circumstance is not

favourable, this may result in investor loss.

Therefore, instead of getting any other option, people like to get money in exchange. This

makes it difficult for investors to pay any third party back scrip dividends.

Apart from the above disadvantages, another major issue is that dividend payments are

taxable, meaning that stockholders are required to pay dividend tax (Ogiela, 2013).

One major drawback in these dividend policies for scripts is that investors do not obtain

money to pay dividends taxation.

For company-

In the situation where the stock of the business does not function well, this can be a risk

of investor loss for them. As well as the risk of market credibility decreasing.

A scrip dividend is simply an option, not a cash dividend substitute. It requires a higher

time and cost that is not accessible to everyone.

As firms, attention must be given to selling shares in different ways of paying the

shareholders.

equity stake in the firm without paying the commissions of the intermediary or the stamp

duty on an exchange purchase (Yu, Chan and Chou, 2015).

For company

One of the main advantages of the scrip dividend is that it is beneficial for businesses to

save capital. It is because corporate entities are able to request this dividend to investors,

and this can contribute to wild money.

In fact, it allows companies to minimize the risk of increasing liquidity position. This also

raises corporate market capitalization on the stock exchange by increasing the number of

investors.

The advantage for the firm is that it doesn't need to find the funds to pay dividends and

could save tax in some conditions.

Drawbacks:

For shareholders-

The price of this share relies on the state of the economy; if the circumstance is not

favourable, this may result in investor loss.

Therefore, instead of getting any other option, people like to get money in exchange. This

makes it difficult for investors to pay any third party back scrip dividends.

Apart from the above disadvantages, another major issue is that dividend payments are

taxable, meaning that stockholders are required to pay dividend tax (Ogiela, 2013).

One major drawback in these dividend policies for scripts is that investors do not obtain

money to pay dividends taxation.

For company-

In the situation where the stock of the business does not function well, this can be a risk

of investor loss for them. As well as the risk of market credibility decreasing.

A scrip dividend is simply an option, not a cash dividend substitute. It requires a higher

time and cost that is not accessible to everyone.

As firms, attention must be given to selling shares in different ways of paying the

shareholders.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

Thus, these are some of the key benefits and disadvantages for stockholders and businesses of

scrip dividends. Moreover, this dividend is appropriate for businesses as compared to

stockholders because it offers them an alternative rather than paying a cash dividend.

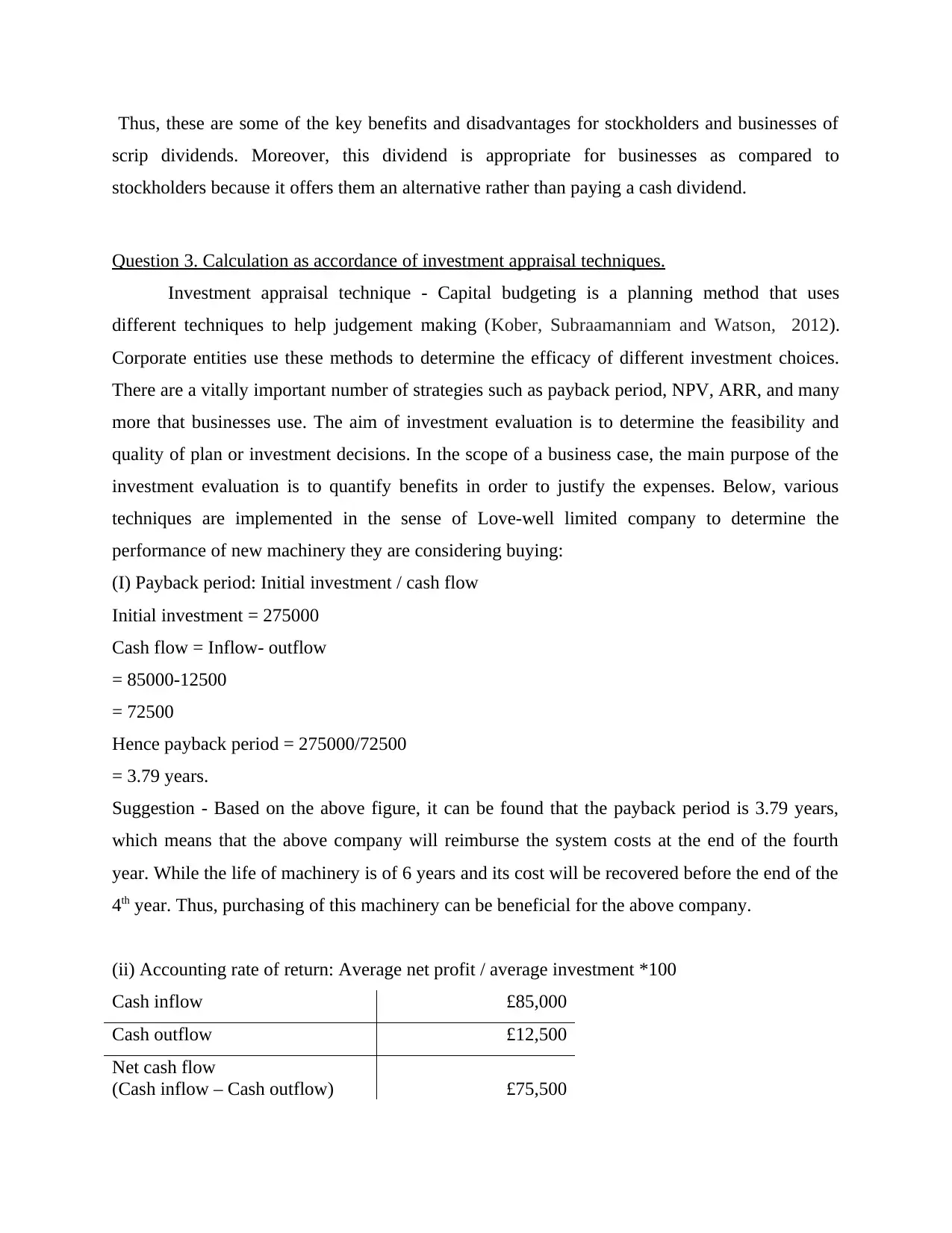

Question 3. Calculation as accordance of investment appraisal techniques.

Investment appraisal technique - Capital budgeting is a planning method that uses

different techniques to help judgement making (Kober, Subraamanniam and Watson, 2012).

Corporate entities use these methods to determine the efficacy of different investment choices.

There are a vitally important number of strategies such as payback period, NPV, ARR, and many

more that businesses use. The aim of investment evaluation is to determine the feasibility and

quality of plan or investment decisions. In the scope of a business case, the main purpose of the

investment evaluation is to quantify benefits in order to justify the expenses. Below, various

techniques are implemented in the sense of Love-well limited company to determine the

performance of new machinery they are considering buying:

(I) Payback period: Initial investment / cash flow

Initial investment = 275000

Cash flow = Inflow- outflow

= 85000-12500

= 72500

Hence payback period = 275000/72500

= 3.79 years.

Suggestion - Based on the above figure, it can be found that the payback period is 3.79 years,

which means that the above company will reimburse the system costs at the end of the fourth

year. While the life of machinery is of 6 years and its cost will be recovered before the end of the

4th year. Thus, purchasing of this machinery can be beneficial for the above company.

(ii) Accounting rate of return: Average net profit / average investment *100

Cash inflow £85,000

Cash outflow £12,500

Net cash flow

(Cash inflow – Cash outflow) £75,500

scrip dividends. Moreover, this dividend is appropriate for businesses as compared to

stockholders because it offers them an alternative rather than paying a cash dividend.

Question 3. Calculation as accordance of investment appraisal techniques.

Investment appraisal technique - Capital budgeting is a planning method that uses

different techniques to help judgement making (Kober, Subraamanniam and Watson, 2012).

Corporate entities use these methods to determine the efficacy of different investment choices.

There are a vitally important number of strategies such as payback period, NPV, ARR, and many

more that businesses use. The aim of investment evaluation is to determine the feasibility and

quality of plan or investment decisions. In the scope of a business case, the main purpose of the

investment evaluation is to quantify benefits in order to justify the expenses. Below, various

techniques are implemented in the sense of Love-well limited company to determine the

performance of new machinery they are considering buying:

(I) Payback period: Initial investment / cash flow

Initial investment = 275000

Cash flow = Inflow- outflow

= 85000-12500

= 72500

Hence payback period = 275000/72500

= 3.79 years.

Suggestion - Based on the above figure, it can be found that the payback period is 3.79 years,

which means that the above company will reimburse the system costs at the end of the fourth

year. While the life of machinery is of 6 years and its cost will be recovered before the end of the

4th year. Thus, purchasing of this machinery can be beneficial for the above company.

(ii) Accounting rate of return: Average net profit / average investment *100

Cash inflow £85,000

Cash outflow £12,500

Net cash flow

(Cash inflow – Cash outflow) £75,500

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

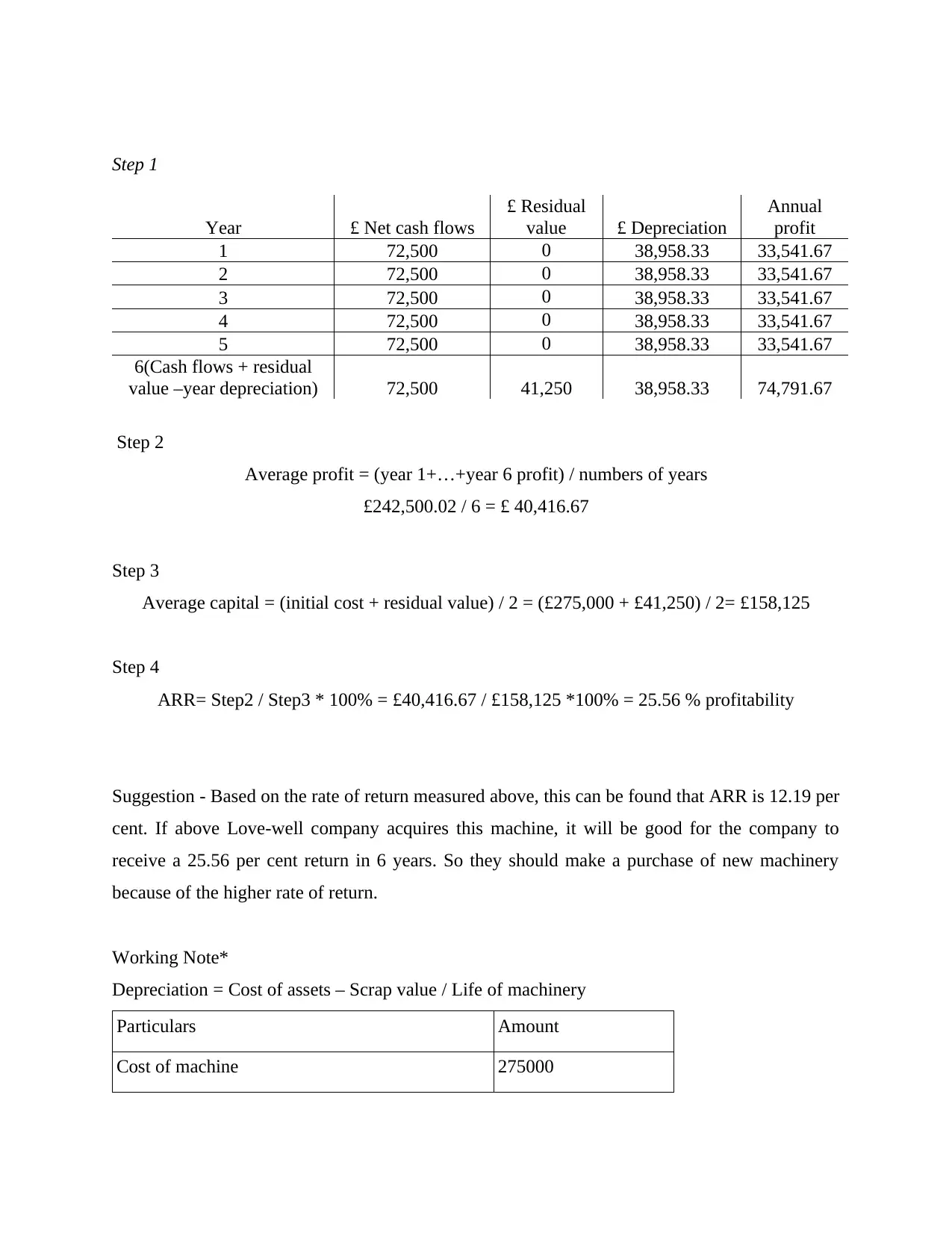

Step 1

Year £ Net cash flows

£ Residual

value £ Depreciation

Annual

profit

1 72,500 0 38,958.33 33,541.67

2 72,500 0 38,958.33 33,541.67

3 72,500 0 38,958.33 33,541.67

4 72,500 0 38,958.33 33,541.67

5 72,500 0 38,958.33 33,541.67

6(Cash flows + residual

value –year depreciation) 72,500 41,250 38,958.33 74,791.67

Step 2

Average profit = (year 1+…+year 6 profit) / numbers of years

£242,500.02 / 6 = £ 40,416.67

Step 3

Average capital = (initial cost + residual value) / 2 = (£275,000 + £41,250) / 2= £158,125

Step 4

ARR= Step2 / Step3 * 100% = £40,416.67 / £158,125 *100% = 25.56 % profitability

Suggestion - Based on the rate of return measured above, this can be found that ARR is 12.19 per

cent. If above Love-well company acquires this machine, it will be good for the company to

receive a 25.56 per cent return in 6 years. So they should make a purchase of new machinery

because of the higher rate of return.

Working Note*

Depreciation = Cost of assets – Scrap value / Life of machinery

Particulars Amount

Cost of machine 275000

Year £ Net cash flows

£ Residual

value £ Depreciation

Annual

profit

1 72,500 0 38,958.33 33,541.67

2 72,500 0 38,958.33 33,541.67

3 72,500 0 38,958.33 33,541.67

4 72,500 0 38,958.33 33,541.67

5 72,500 0 38,958.33 33,541.67

6(Cash flows + residual

value –year depreciation) 72,500 41,250 38,958.33 74,791.67

Step 2

Average profit = (year 1+…+year 6 profit) / numbers of years

£242,500.02 / 6 = £ 40,416.67

Step 3

Average capital = (initial cost + residual value) / 2 = (£275,000 + £41,250) / 2= £158,125

Step 4

ARR= Step2 / Step3 * 100% = £40,416.67 / £158,125 *100% = 25.56 % profitability

Suggestion - Based on the rate of return measured above, this can be found that ARR is 12.19 per

cent. If above Love-well company acquires this machine, it will be good for the company to

receive a 25.56 per cent return in 6 years. So they should make a purchase of new machinery

because of the higher rate of return.

Working Note*

Depreciation = Cost of assets – Scrap value / Life of machinery

Particulars Amount

Cost of machine 275000

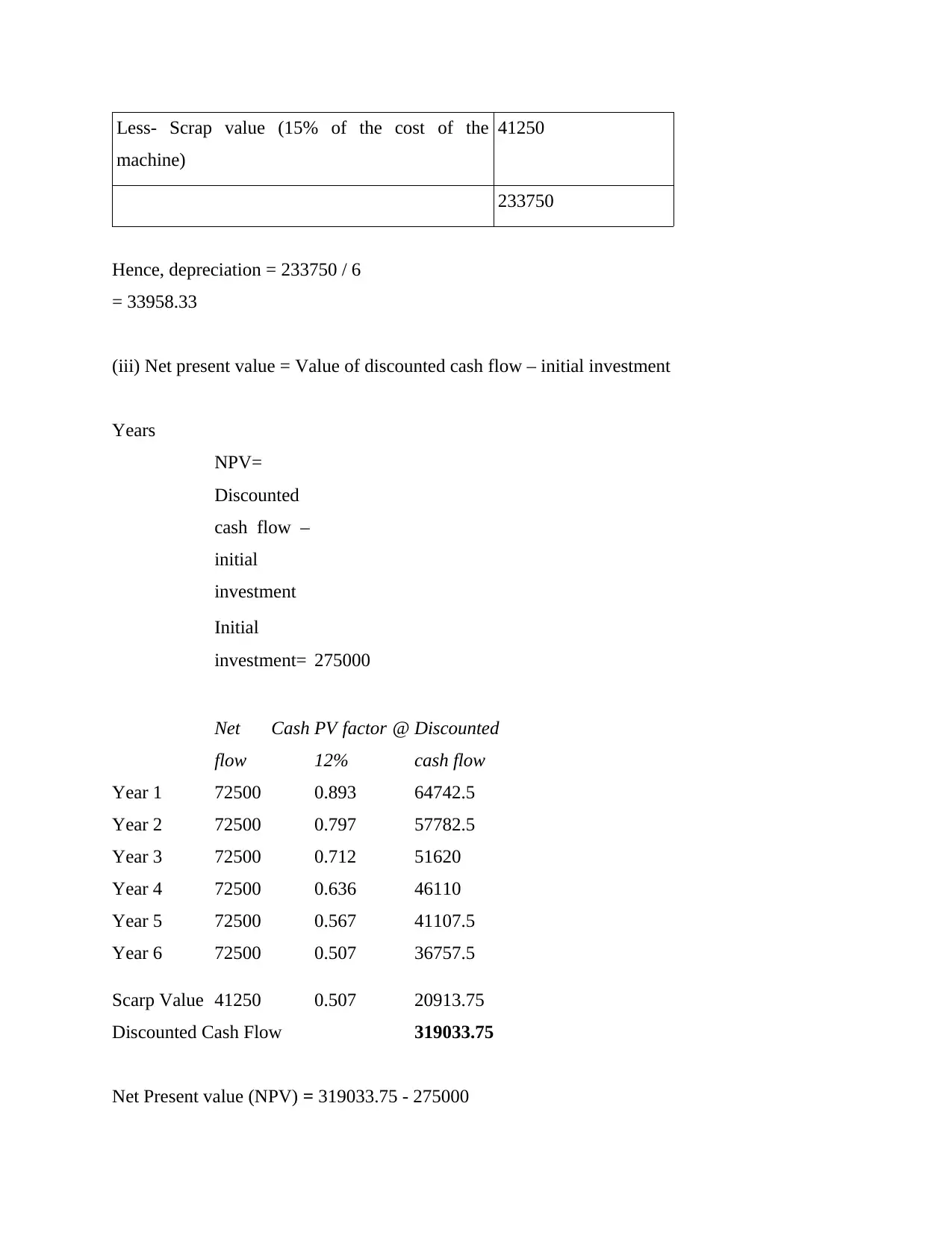

Less- Scrap value (15% of the cost of the

machine)

41250

233750

Hence, depreciation = 233750 / 6

= 33958.33

(iii) Net present value = Value of discounted cash flow – initial investment

Years

NPV=

Discounted

cash flow –

initial

investment

Initial

investment= 275000

Net Cash

flow

PV factor @

12%

Discounted

cash flow

Year 1 72500 0.893 64742.5

Year 2 72500 0.797 57782.5

Year 3 72500 0.712 51620

Year 4 72500 0.636 46110

Year 5 72500 0.567 41107.5

Year 6 72500 0.507 36757.5

Scarp Value 41250 0.507 20913.75

Discounted Cash Flow 319033.75

Net Present value (NPV) = 319033.75 - 275000

machine)

41250

233750

Hence, depreciation = 233750 / 6

= 33958.33

(iii) Net present value = Value of discounted cash flow – initial investment

Years

NPV=

Discounted

cash flow –

initial

investment

Initial

investment= 275000

Net Cash

flow

PV factor @

12%

Discounted

cash flow

Year 1 72500 0.893 64742.5

Year 2 72500 0.797 57782.5

Year 3 72500 0.712 51620

Year 4 72500 0.636 46110

Year 5 72500 0.567 41107.5

Year 6 72500 0.507 36757.5

Scarp Value 41250 0.507 20913.75

Discounted Cash Flow 319033.75

Net Present value (NPV) = 319033.75 - 275000

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

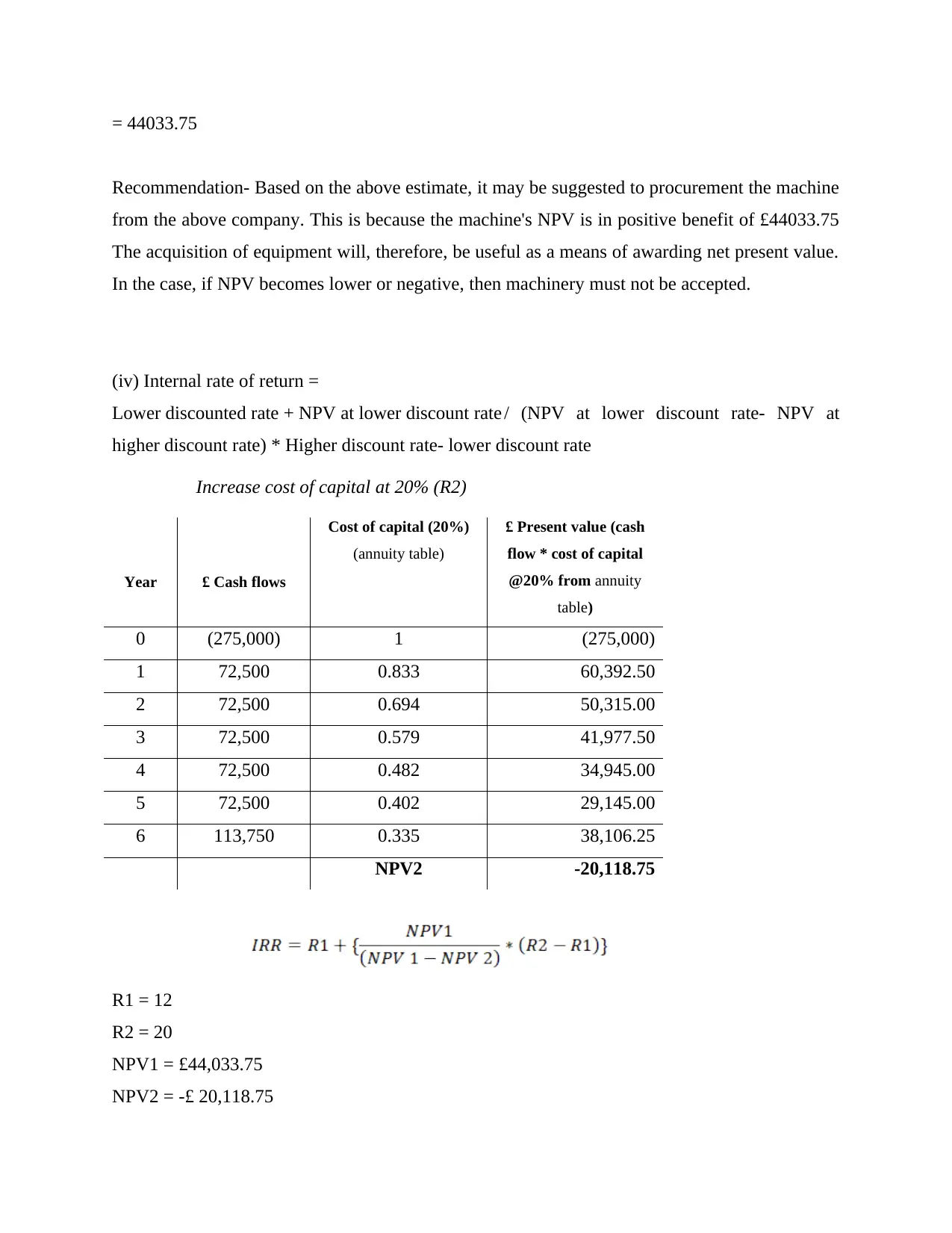

= 44033.75

Recommendation- Based on the above estimate, it may be suggested to procurement the machine

from the above company. This is because the machine's NPV is in positive benefit of £44033.75

The acquisition of equipment will, therefore, be useful as a means of awarding net present value.

In the case, if NPV becomes lower or negative, then machinery must not be accepted.

(iv) Internal rate of return =

Lower discounted rate + NPV at lower discount rate / (NPV at lower discount rate- NPV at

higher discount rate) * Higher discount rate- lower discount rate

Increase cost of capital at 20% (R2)

Year £ Cash flows

Cost of capital (20%)

(annuity table)

£ Present value (cash

flow * cost of capital

@20% from annuity

table)

0 (275,000) 1 (275,000)

1 72,500 0.833 60,392.50

2 72,500 0.694 50,315.00

3 72,500 0.579 41,977.50

4 72,500 0.482 34,945.00

5 72,500 0.402 29,145.00

6 113,750 0.335 38,106.25

NPV2 -20,118.75

R1 = 12

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

Recommendation- Based on the above estimate, it may be suggested to procurement the machine

from the above company. This is because the machine's NPV is in positive benefit of £44033.75

The acquisition of equipment will, therefore, be useful as a means of awarding net present value.

In the case, if NPV becomes lower or negative, then machinery must not be accepted.

(iv) Internal rate of return =

Lower discounted rate + NPV at lower discount rate / (NPV at lower discount rate- NPV at

higher discount rate) * Higher discount rate- lower discount rate

Increase cost of capital at 20% (R2)

Year £ Cash flows

Cost of capital (20%)

(annuity table)

£ Present value (cash

flow * cost of capital

@20% from annuity

table)

0 (275,000) 1 (275,000)

1 72,500 0.833 60,392.50

2 72,500 0.694 50,315.00

3 72,500 0.579 41,977.50

4 72,500 0.482 34,945.00

5 72,500 0.402 29,145.00

6 113,750 0.335 38,106.25

NPV2 -20,118.75

R1 = 12

R2 = 20

NPV1 = £44,033.75

NPV2 = -£ 20,118.75

Paraphrase This Document

Need a fresh take? Get an instant paraphrase of this document with our AI Paraphraser

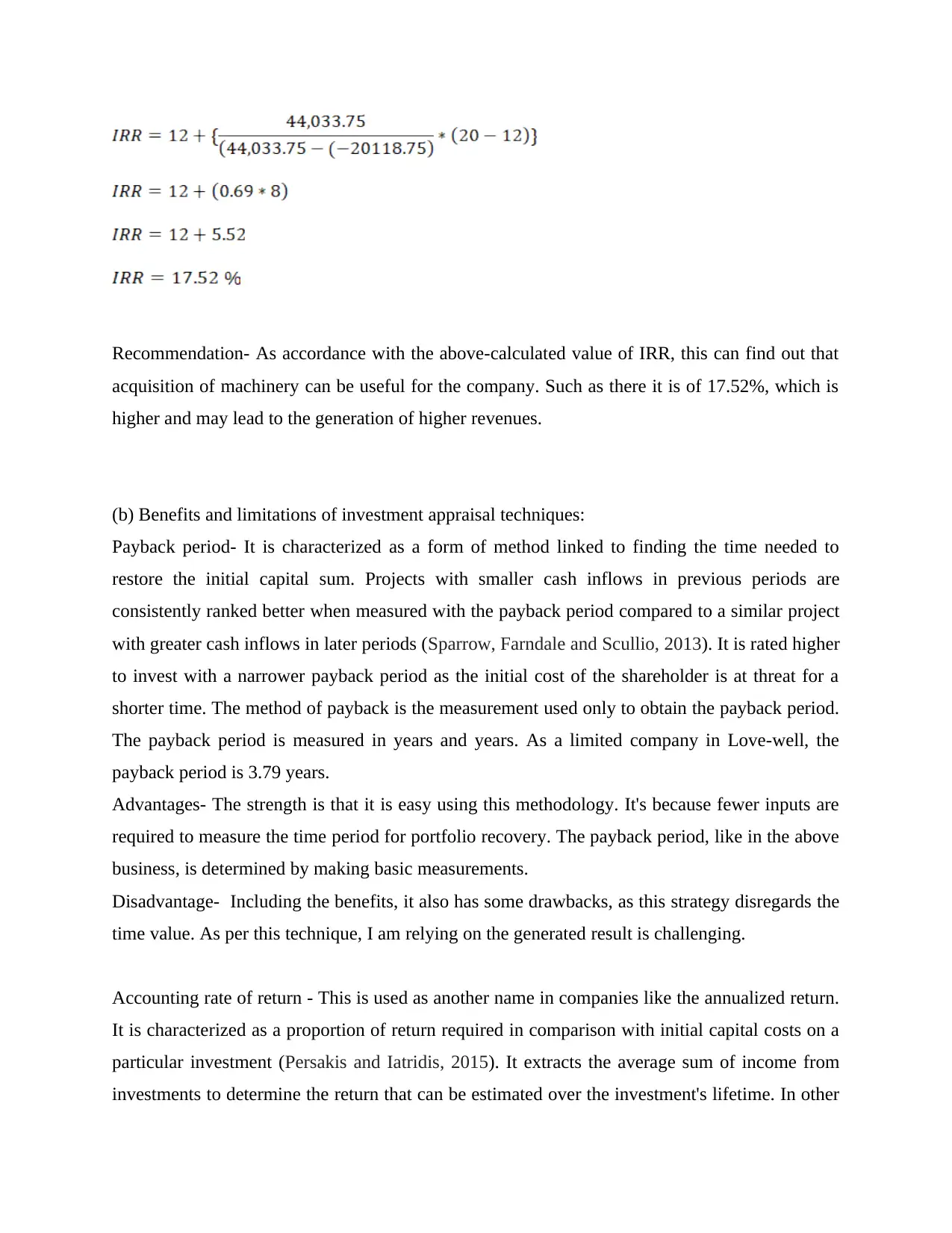

Recommendation- As accordance with the above-calculated value of IRR, this can find out that

acquisition of machinery can be useful for the company. Such as there it is of 17.52%, which is

higher and may lead to the generation of higher revenues.

(b) Benefits and limitations of investment appraisal techniques:

Payback period- It is characterized as a form of method linked to finding the time needed to

restore the initial capital sum. Projects with smaller cash inflows in previous periods are

consistently ranked better when measured with the payback period compared to a similar project

with greater cash inflows in later periods (Sparrow, Farndale and Scullio, 2013). It is rated higher

to invest with a narrower payback period as the initial cost of the shareholder is at threat for a

shorter time. The method of payback is the measurement used only to obtain the payback period.

The payback period is measured in years and years. As a limited company in Love-well, the

payback period is 3.79 years.

Advantages- The strength is that it is easy using this methodology. It's because fewer inputs are

required to measure the time period for portfolio recovery. The payback period, like in the above

business, is determined by making basic measurements.

Disadvantage- Including the benefits, it also has some drawbacks, as this strategy disregards the

time value. As per this technique, I am relying on the generated result is challenging.

Accounting rate of return - This is used as another name in companies like the annualized return.

It is characterized as a proportion of return required in comparison with initial capital costs on a

particular investment (Persakis and Iatridis, 2015). It extracts the average sum of income from

investments to determine the return that can be estimated over the investment's lifetime. In other

acquisition of machinery can be useful for the company. Such as there it is of 17.52%, which is

higher and may lead to the generation of higher revenues.

(b) Benefits and limitations of investment appraisal techniques:

Payback period- It is characterized as a form of method linked to finding the time needed to

restore the initial capital sum. Projects with smaller cash inflows in previous periods are

consistently ranked better when measured with the payback period compared to a similar project

with greater cash inflows in later periods (Sparrow, Farndale and Scullio, 2013). It is rated higher

to invest with a narrower payback period as the initial cost of the shareholder is at threat for a

shorter time. The method of payback is the measurement used only to obtain the payback period.

The payback period is measured in years and years. As a limited company in Love-well, the

payback period is 3.79 years.

Advantages- The strength is that it is easy using this methodology. It's because fewer inputs are

required to measure the time period for portfolio recovery. The payback period, like in the above

business, is determined by making basic measurements.

Disadvantage- Including the benefits, it also has some drawbacks, as this strategy disregards the

time value. As per this technique, I am relying on the generated result is challenging.

Accounting rate of return - This is used as another name in companies like the annualized return.

It is characterized as a proportion of return required in comparison with initial capital costs on a

particular investment (Persakis and Iatridis, 2015). It extracts the average sum of income from

investments to determine the return that can be estimated over the investment's lifetime. In other

words, ARR is a method for making decisions on capital budgeting. Those generally involve

circumstances where the company decides to choose whether or not make a different investment

(a plan, an expansion, etc.) based on the projected future net income compared to the price of

capital. Like the investment planned by the above company, the ARR is 12.19 per cent. This has

some advantages and drawbacks as follows:

Advantages- It is also very quick to use and straightforward, similarly to the above method.

That's because this approach only takes into account the total amount of income during the whole

proposal's economic life.

Disadvantages - It also has some disadvantages as it lacks external factors that can change the

overall productivity of businesses. In addition, under these techniques, the time period on which

profits are generated neglected completely.

Net present value - The word NPV is usually defined as the gap between PV of money inflow

and outflow for a particular time span. This is commonly used to examine project proposals in an

effective manner (Yunus, 2013). In general, NPV evaluation is a method of inherent evaluation

and used widely in finance and accounting to assess a company's value, capital protection, capital

plan, new venture, cost-cutting program, and everything involving cash flow. The NPV of the

planned equipment in the Love-well corporation is £ 22828. It has certain drawbacks and

advantages as follows:

Advantages- The most important role of the NPV method is that it helps businesses to make

decisions. This is because, by using its methodology, financial advisors can assess the

effectiveness of all kinds of projects, particularly projects with different sizes or of the same

scale. Similar as in the above Love-well company, this technique is being used in order to make

an evaluation of their proposed machinery.

Disadvantages- Just cash in and out of any plan is considered by NPV methodology. This does

not find additional costs such as capital costs and any other initial costs incurred in connection

with any specific project. As a result, this becomes difficult for businesses to make a proper

evaluation of the project or any investment appraisal. Similar to the Love-well company, this

method is applied to compute the present value of machinery by considering only in and

outflows. The rest of the costs are ignored completely.

circumstances where the company decides to choose whether or not make a different investment

(a plan, an expansion, etc.) based on the projected future net income compared to the price of

capital. Like the investment planned by the above company, the ARR is 12.19 per cent. This has

some advantages and drawbacks as follows:

Advantages- It is also very quick to use and straightforward, similarly to the above method.

That's because this approach only takes into account the total amount of income during the whole

proposal's economic life.

Disadvantages - It also has some disadvantages as it lacks external factors that can change the

overall productivity of businesses. In addition, under these techniques, the time period on which

profits are generated neglected completely.

Net present value - The word NPV is usually defined as the gap between PV of money inflow

and outflow for a particular time span. This is commonly used to examine project proposals in an

effective manner (Yunus, 2013). In general, NPV evaluation is a method of inherent evaluation

and used widely in finance and accounting to assess a company's value, capital protection, capital

plan, new venture, cost-cutting program, and everything involving cash flow. The NPV of the

planned equipment in the Love-well corporation is £ 22828. It has certain drawbacks and

advantages as follows:

Advantages- The most important role of the NPV method is that it helps businesses to make

decisions. This is because, by using its methodology, financial advisors can assess the

effectiveness of all kinds of projects, particularly projects with different sizes or of the same

scale. Similar as in the above Love-well company, this technique is being used in order to make

an evaluation of their proposed machinery.

Disadvantages- Just cash in and out of any plan is considered by NPV methodology. This does

not find additional costs such as capital costs and any other initial costs incurred in connection

with any specific project. As a result, this becomes difficult for businesses to make a proper

evaluation of the project or any investment appraisal. Similar to the Love-well company, this

method is applied to compute the present value of machinery by considering only in and

outflows. The rest of the costs are ignored completely.

⊘ This is a preview!⊘

Do you want full access?

Subscribe today to unlock all pages.

Trusted by 1+ million students worldwide

1 out of 15

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Unlock your academic potential

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.