Financial Performance Management Exam: Costing and Budgeting

VerifiedAdded on 2022/12/28

|10

|1638

|59

Homework Assignment

AI Summary

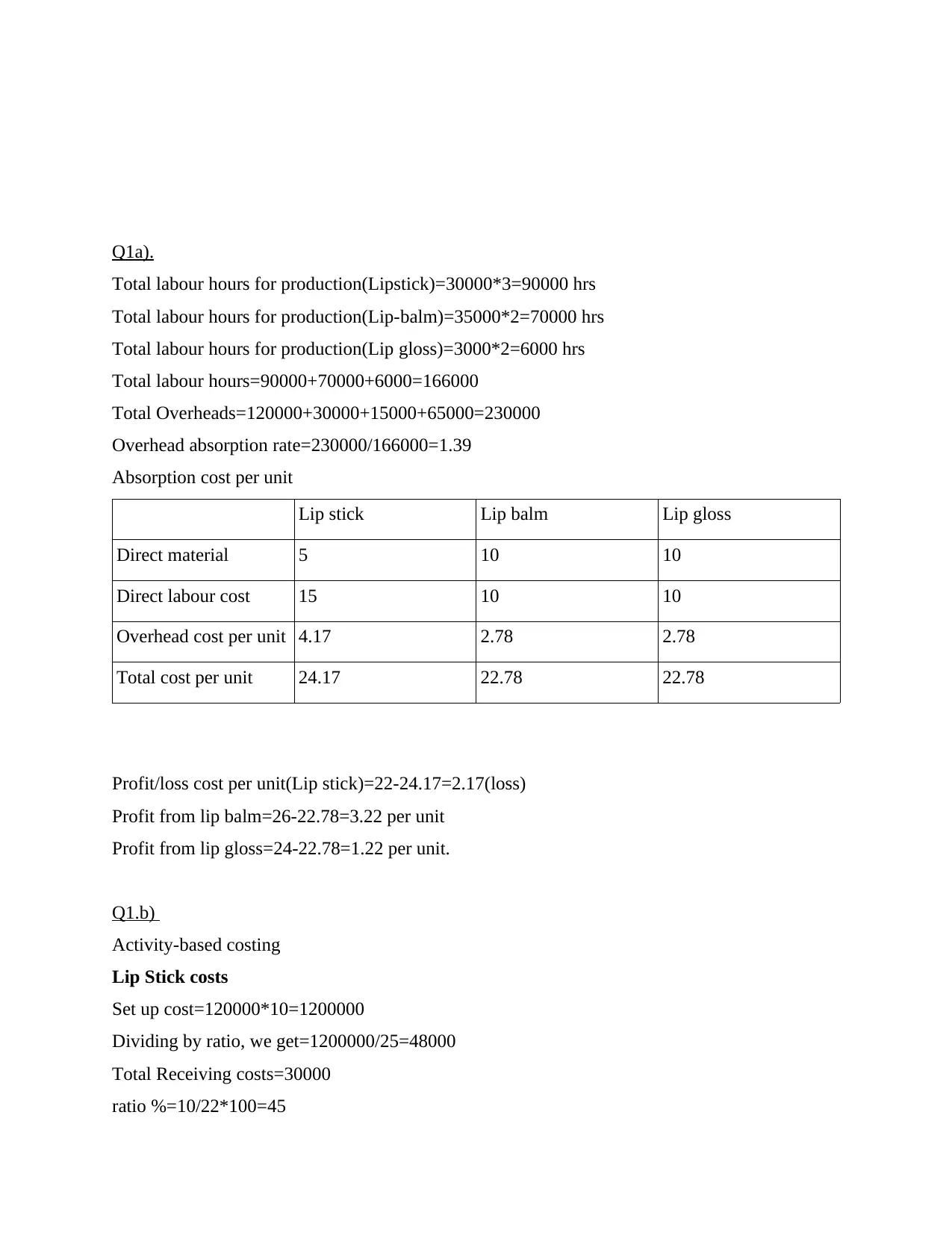

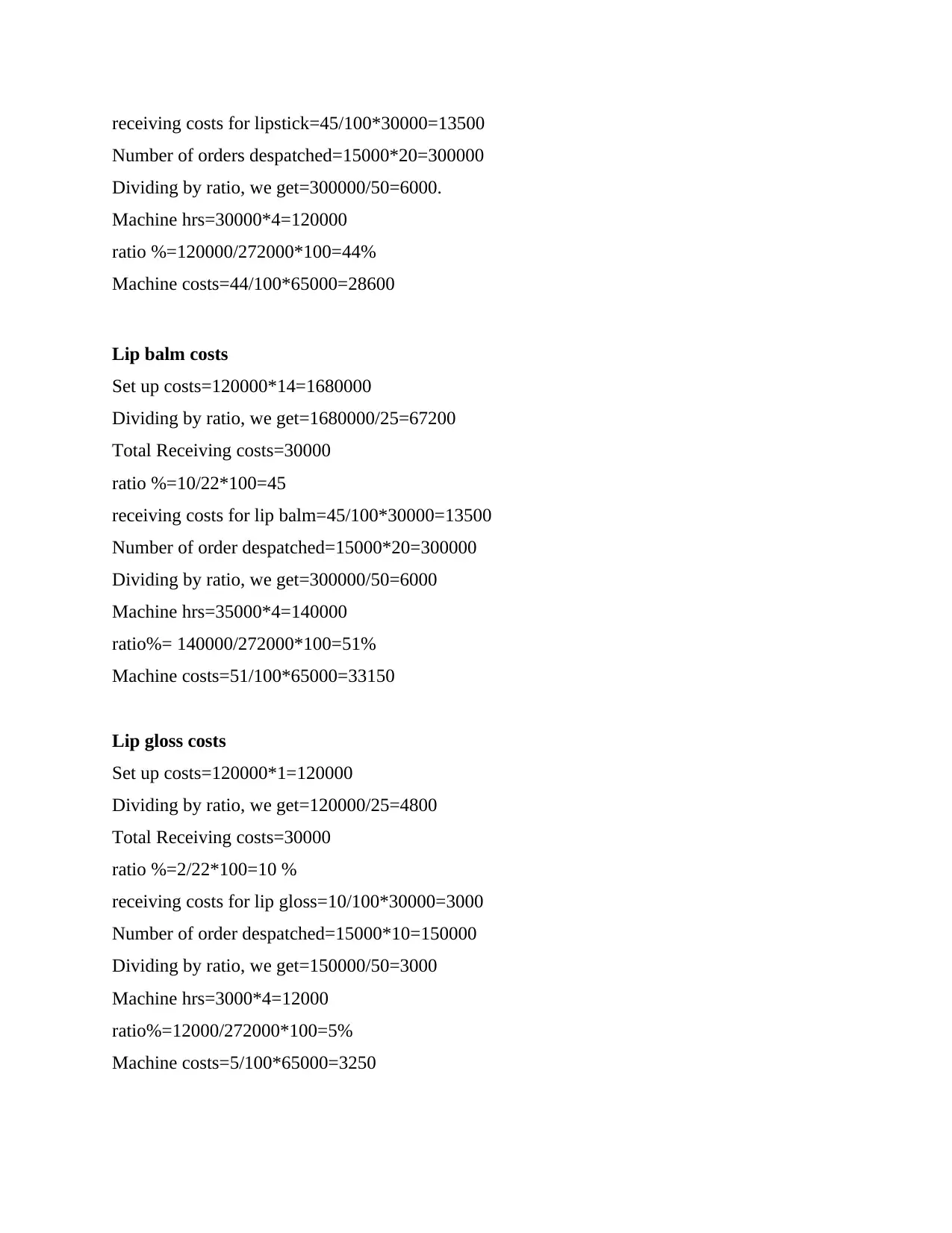

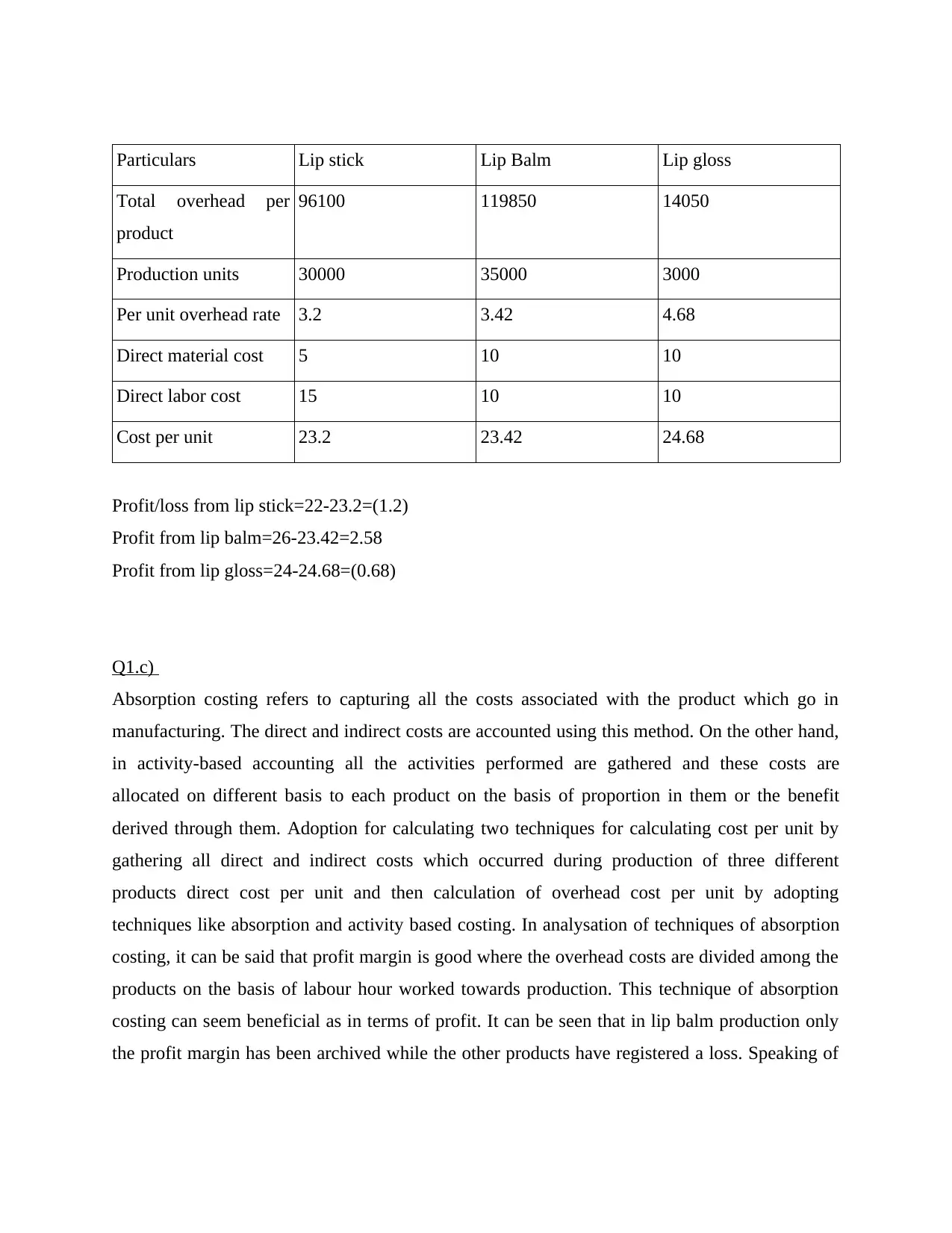

This document presents a comprehensive solution to a Financial Performance Management online exam, addressing key concepts in financial analysis and control. The solution begins with a detailed breakdown of costing methods, including absorption costing and activity-based costing, applied to a multi-product scenario (lipstick, lip balm, and lip gloss), calculating per-unit costs and profitability. It then delves into variance analysis, specifically material usage, price, and mix variances, providing calculations and interpretations of the results. Furthermore, the solution explores sensitivity analysis and its application in managerial decision-making, followed by a comparison of zero-based budgeting and incremental budgeting, outlining their respective advantages and disadvantages and advocating for a combined approach. The document provides a thorough understanding of the key financial concepts and their practical application in business decision-making.

1 out of 10

Related Documents

Your All-in-One AI-Powered Toolkit for Academic Success.

+13062052269

info@desklib.com

Available 24*7 on WhatsApp / Email

![[object Object]](/_next/static/media/star-bottom.7253800d.svg)

Copyright © 2020–2026 A2Z Services. All Rights Reserved. Developed and managed by ZUCOL.